“All of that negative news has kind of put a downer on consumer sentiment,” is how Jharonne Martis, director of consumer research at Thomson Reuters, explained the crummy consumer confidence reading on Friday.

The Thomson Reuters/Ipsos Canada Primary Consumer Sentiment Index had dropped to 51.6, the lowest so far this year and well below the 56.4 of last August before the oil-price crash soured the mood. By comparison, since 2010, the index has mostly been in the mid-50 range.

The “negative news” has extended beyond the price of oil. She pointed at some well-known retailer chains that have shut their stores in Canada recently, including Target, Future Shop, and photography retailer Black’s.

Already on March 30, Bank of Canada governor Stephen Poloz had warned that economic growth would be “atrocious” in the first quarter “because the oil shock is a big deal for us.” And he was right, with GDP dropping 0.6% annualized, the first quarterly decline since 2011.

It didn’t help that the Bank of Canada, in its Financial System Review released on Friday, pointed out that household indebtedness and the housing bubble were the top two vulnerabilities that threatened Canada’s financial stability. The top vulnerability:

“Elevated” – actually dizzying – “level of household indebtedness”:

The vulnerability associated with household indebtedness remains important and is edging higher, owing to an increase in the level of household debt and the ongoing negative impact on incomes from the sharp decline in oil prices. In addition, the quality of household debt may be decreasing at the margin….

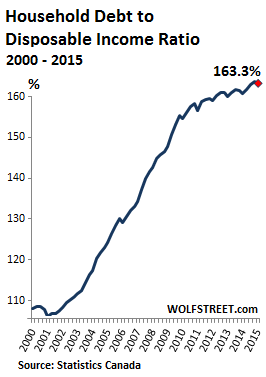

Household leverage has been pushing relentlessly higher. In the first quarter, according to Statistics Canada, the household-debt-to-disposable-income ratio edged down a smidgen for the first time in four quarters, from its all-time high, to 163.3%. Debt increased once again, but this time slightly less than income.

The second most important vulnerability to threaten financial stability, according to the Bank of Canada?

“Imbalances in the housing market”:

Regional divergences in resale activity and house price growth have become more evident, with an apparent trifurcation of the national market. Although house price growth on a national basis has slowed modestly, it continues to outpace income growth, and overvaluation in the Canadian housing market remains a concern.

The Bank of Canada considered the housing market up to 30% overvalued. That may be conservative. Deutsche Bank estimated that it was 63% overvalued. The IMF warned about high household debt levels and the “overheated housing market.” And the Economist determined the housing market to be overvalued by 35% compared to incomes, and 89% compared to rents.

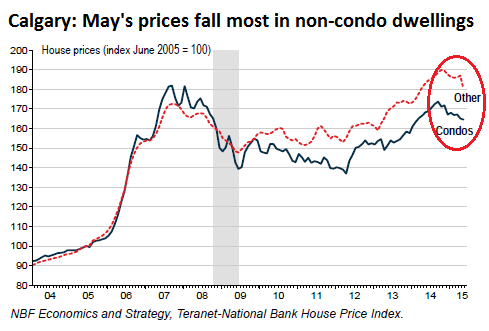

On Friday, the Teranet–National Bank National Composite House Price Index outlined this “trifurcation” in the housing market. The overall index rose 0.9% in May from April, the fifth consecutive monthly increase. But it was below the average increase for May of 1.1% due to a record 3.3% plunge in Calgary’s prices.

In Calgary, the epicenter of the Canadian oil patch, things are getting ugly. The index is down 5% from its peak 7 months ago. For thank-goodness, Calgary’s weight only accounts for 8.3% of the index. Marc Pinsonneault, senior economist at National Bank Financial, explained:

The record monthly drop in Calgary house prices was concentrated in dwellings other than condos. This is consistent with anecdotic evidence that so far, Calgary’s market for high-end expensive homes has borne the brunt of the collapse in oil prices.

Note how condos dropped at a nearly steady rate over the last seven months, while “other” – weighed down by “high-end expensive homes” – plunged in May:

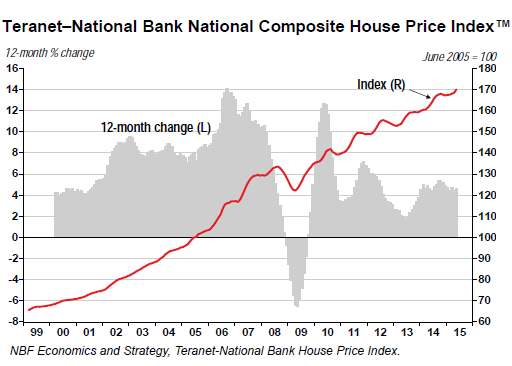

The indices for the other 10 metropolitan markets rose on the month, “a breadth last seen in August 2014.” Year over year, the national index was up 4.6%. The index is now 28% above its peak during the housing bubble before the Financial Crisis:

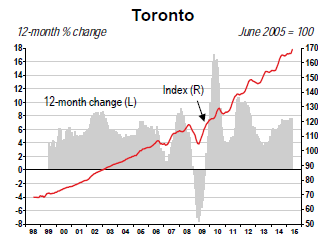

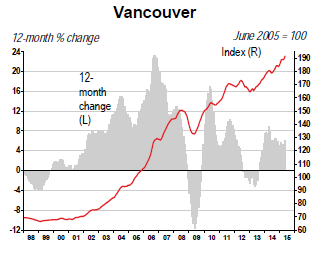

The biggest drivers were Toronto and Vancouver. In Toronto, whose weight accounts for 34.6% of the index, prices jumped by 7.6% year over year are now 44% higher than at the peak of the prior housing bubble:

In Vancouver, whose weight accounts for 19.5% of the index, prices jumped by 6.2% and are now 27% higher than at the peak of the prior housing bubble:

The overall index along with the indices for Toronto, Vancouver, Quebec City, and Hamilton are at all-time highs. There, the housing bubble reigns in its magnificent splendor, still, at least on the surface. But in the remaining seven metros, prices have dropped below their peaks, with Calgary down 5% in 7 months and Ottawa-Gatineau down 4.8% in 9 months.

High household debt and a magnificent house-price bubble coagulate into a toxic mix for Canada’s financial system. An increase in unemployment would put these highly indebted households under severe pressure, and if this happens as home prices succumb to gravity once again, it will give the good folks at the Bank of Canada a lot of gray hairs in trying to prop up the banks.

But even in Toronto, where the bubble is at its most splendid magnificence, the hiss of hot air can already be heard: unsold new condos spiked to an all-time record. Read…. Toronto’s Epic Condo Bubble Suddenly Turns into Condo Glut

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I think the foreclosure laws are different in Canada. The banks may not be as impacted there because the foreclosure laws are stricter. The underwater homeowners may be the ones that suffer more.

Regardless of laws, if interest rises (or job loss) and one cannot make payments….

The problem is, with 645K properties sold last year alone, 40% of them to first time buyers, the depth of this incredible debt pit all but guarantee that in case of spike in defaults, there will be no “plankton” to absorb the spike in listings. Canadian RE has long passed the threshold of “soft lending”. This ship will go down. Granted, there is huge demand for RE in Canada, but not at these prices. Our economy and our incomes cannot support $750K townhouses.

A lot of states had fairly strict foreclosure laws in 2007…..didn’t really help the banks here that much.

re: “Our economy and our incomes cannot support $750K townhouses.”

I would like to add: “Our Country cannot support or provide support for people stupid enough to buy a $750,000 townhouse”

Let them go down. It is time Canadians rediscovered sanity, realistic expectations, and learn to live within their means. My parents would simply not believe how this country has lost its way in the surge of debt and consumerism.

Sorry, you’re way too close to the US for sanity and realistic expectations.

Canadian snowbirds are a big factor in the Florida economy. They were the only buyers at the bottom of the financial crisis and own a large percentage of the waterfront condos. Maybe their Florida investments will cushion the blow. If they have a bad year, and don’t show up in large numbers next season, Florida will likely also have a bad year. Just in time for the election I may add.

Nothing could be better for Canadians than to bite the bullet, let house prices crash, and let interest rates rise.

Most homeowners don’t really get it though, as they believe the “top line” is all that matters. Take my in-laws for example. They have just managed to pay of their house and now are looking at when they can retire (they’re in their sixties). Their home, about an hour out of Toronto, is valued at around $450,000, and they think it’s GREAT that interest rates are so low that people can afford to own a home.

They don’t really clue in though, that if they sold their house for $450,000 and used that money for retirement, at 2% interest, they are going to have to retire on the whopping sum of $9,000/yr – which will mean abject poverty for them.

The same house, back in the early 1990’s, when interest rates were 8-9%, was probably worth around $125-$150,000, and if they sold the house and put the capital into a term deposit, they could have received an income of $10-$12,000/yr…. PLUS, people such as their children, would only have to save $12-$15,000 as a 10% downpayment rather than an unreasonable $45,000 down.

Jeez, that people don’t “get it.”

At 2% interest, it takes 36 years to double one’s capital. That means if you invest $10,000 at 20yrs old, by the time you are 92, compound interest will return you a whopping $40,000. The same 20 year old investing $10,000 at 8% interest, will have $320,000 by 65 (and over $2.5 million by 92).

Quite frankly, if housing does not collapse and interest rates don’t rise, how the heck do they expect any of us to retire? Ask yourselfe this, if saving up $300,000 in your RRSP will only yield you $6,000/yr at 2% interest, does that mean that if I start up a website generating $500/month income, that it is also worth $300,000? Because if that is the case, I’d say it’s far easier to start the website than to shake $300,000 out of my skinny ass, especially with interest compounding at only 2% (or less). I’d don’t see how any of us will be able to retire unless we generate extra passive income from things like websites or small home businesses in our old age. The traditional routes simply aren’t going to work in this kind of environment.

Most Canadians are property rich and money poor. There grabbing money anywhere they can and it’s not just them Americans are as well. Taking out 2nd mortgages, taking out cash advances on credit cards, going to legal loan sharks like money mart for pay day loans. All borrowing off of there portfolio value.

In Canada you can’t foreclose on a home. Instead you have to declare personal bankruptcies. And you are going to have a mess of them.

A lot of people here too have been brain washed into buying 2 or 3 homes and renting them out as rental properties or even worse they rent out there basement to someone to help pay the mortgage. More then likely that will end as well. Renting to people is a pain in the arse as most find out the hard way.

Another point too is that the Federal Gov’t is Canada’s largest employer. The next Gov’t after Harper will have to hack and slash these jobs in order to save money. Chretien did it after Mulroney and the same thing will happen again.

You also have to end all of these home improvement TV Shows and Channels. All they do is further brain wash people.

The Harper Gov’t was also giving out tax incentives to people who were renovating there homes for awhile. Here is one example for Seniors in Ontario. Another thing that isn’t helping things.

http://www.ontario.ca/seniors/healthy-homes-renovation-tax-credit

Im sure when it does crash it will take Home Depot, Lowes and Rona with it lol

re statement: “You also have to end all of these home improvement TV Shows and Channels. All they do is further brain wash people.”

Amen to that. My wife likes those shows and I watch them once in awhile. They all take place in Toronto and involve fixing up a $700,000 shack. It is a joke. Apparently, all life ends if one does not have granite countertops.

I am 60 and have been mortgage free for almost 20 years by buying what I could afford and fixing. I have always had a modest workingman’s income. The odd time I took out a LOC to buy property, the last time in 2007. I bought an old rural shack on a beautiful piece of riverfront, promptly sold the house in town and started to renovate. (Carpenter). I now have a beautiful but affordable home that we heat with wood. There are no granite countertops, but tile on cabinets which I built myself. The living area is either carbonized bamboo, or 1′ tiles which look like slate. What we saved allowed us to buy another 15 acres next door.

Even though I am a builder I believe people can do many things, themselves. Turn off the TV and try. It may not be perfect, but trade text books lay everything out and there are tons of DIY books on cabinet building, etc. It isn’t rocket science. Questions? Youtube videos are absolutely amazing resources. I use them for mechanics. My son-in-law started with building some bathroom vanities and a small shop. With a little help he would be able to do most of the grunt work on an addition which I am slated to help with.

My wife likes our house, (actually we love it), but if I were on my own or just starting out I would be content with a small cabin or trailer provided the property was nice. I simply do not understand people’s need to buy what society calls ‘top end’ on credit. Everybody knows they are all debt serfs, despite what their home looks like.

regards

Paulo, it sounds like you and I were both born without the “keep up with the Joneses” gene. I buy what I need to the extent that I can afford, and to hell with the Joneses. So much of this nonsense from toddler beauty pageants to helicopter moms to car leasing to curb appeal to phony knockoff Gucci gear drives me crazy! Are you a better person if you are wearing some designer’s name on your butt? Is it really that important to impress some stranger into thinking you’re better off than you are? Maybe you know their motivation, Paulo but to me it’s a complete mystery.

The Canadian housing market may yet get a break.

Within the next twelve months or so, 40 million people in California are all going to wake up in the morning to the same thought — they need to sell and get out before everybody else does, because there is no more water so they cannot continue to stay where they are.

Some of those refugees will be coming to Vancouver, and even Calvary and Edmonton….

I am not so optimistic as you are about Californians selling their property when there is only 1 year’s supply of water left. After all, who is going to buy a house there?

it is sad and scary seen these 25 years old kids with 600k to 700k debt that make them house poor…the prairies will die once all these condos bubble burst…300 k condos in winnipeg?? not a chance…will love to see them back at 80 90k

Thanks for bringing back the Housing Bubble 2.0 category, Wolf!