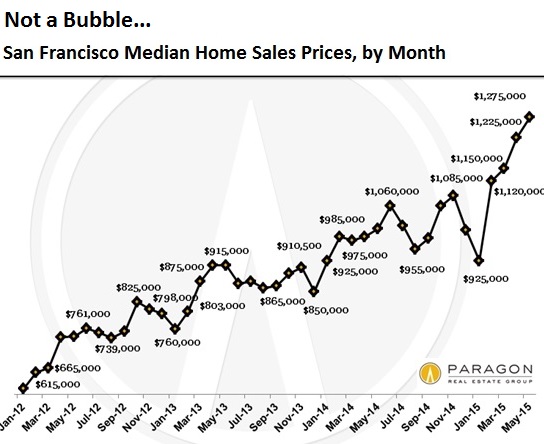

Another miracle happened in San Francisco. In May, the median sale price of all types of homes, after having already spiked in the prior months, jumped another 4%, to a vertigo-inducing $1,275,000.

That’s not a palace, but more likely a no-view two-bedroom apartment in a decent area, and if you’re lucky, with a shared garage and “tandem parking,” where you have to move several cars to pull out yours in the back.

During the prior housing bubble, the one that helped trip up the global financial system when it imploded, home prices in San Francisco peaked in November 2007 at a then mind-boggling $895,000. Valuations that afterward were called “crazy.” By January 2012, the median home price had plunged 31% to $615,000. But it was still a lot of money for that kind of home.

By then the tsunami of money that the Fed and other central banks had unleashed was already washing over San Francisco. The stock-market boom has powered a startup boom that the city is so dependent on. An office and condo construction boom took off. And ultra-low interest rates provided the propellants to make it fly. Everything came together.

Since January 2012, the median home price has skyrocketed 107%, according to Paragon Real Estate Group’s June 2015 report. It’s now 42% higher than it was during the peak of the prior all-time crazy bubble.

January is usually the low point in the seasonal fluctuations, followed by the white-hot spring selling season. With sales prices reflecting deals negotiated in the prior month or two, there is a lag. So from January to May 2014, home prices rose 9%. Over the same period in 2013, they surged 20%. But look at that gorgeous 38% spike year-to-date:

Paragon’s Chief Market Analyst, Patrick Carlisle, pointed at where the action has been – at the high end:

High-end home sales and prices in the city have been increasing rapidly, with interesting shifts occurring between older high-prestige neighborhoods like Pacific Heights and Russian Hill, and areas such as Noe Valley and South Beach, where surging sales of very expensive homes are a more recent phenomenon. Part of this shift is being fueled by the explosion of younger, high-tech wealth; another part is the recent construction boom of high-rise, ultra-luxury condo buildings south of Market Street.

There’s an “enormous variety in high-end real estate in San Francisco, from mansions to penthouses, Victorians to new, ultra-high-tech construction,” with one of the more common amenities being “spectacular views.” Pano views might include the Bay, the Peninsula, the Pacific, the Golden Gate Bridge, or the Bay Bridge, and if you’re very lucky, a different view from each side of the home.

Renting is a cheaper option, but it’s still dreadfully expensive. The median rent, according to Zillow, is $3,162 per month, the second highest in the nation, a smidgen behind another Bay Area miracle, San Jose.

In San Francisco, you’d need $126,500 in annual household income to be able to afford the median apartment without exceeding the recommended 30% rent-to-income threshold. At a wage of $15 per hour (the minimum wage effective July 2018), it would take four earners in one “household” to make this work. So mostly, forget it. These folks are priced out of the city, even if they were born here.

As impossible as it may seem, that’s still a heck of a lot cheaper than buying a similar unit and paying the mortgage, association fees, maintenance, water, garbage, and taxes.

But buyers are exuberant, certain that this is going to work out for them. In May, the average home sale was 10% above the original asking price, the highest rate since the prior housing bubble. “Fiercely competitive buyer bidding wars,” is how Patrick Carlisle described it. And nearly 93% of homes sold “without going through any price reductions, an astonishingly high percentage.”

Two of the biggest factors affecting the San Francisco real estate market are extremely low interest rates, which have a large impact on the ongoing cost of homeownership, and surging well-paid employment. According to Ted Egan, San Francisco’s Chief Economist, high-tech jobs alone jumped by 18% in the 12 months through March 2015, and as of April, the city’s unemployment rate, at 3.4%, was the lowest since the height of the dotcom boom.

In April, the city counted 524,100 employed residents, up 22% from the peak of the prior bubble in 2008. The employment boom is based on the tech boom where startups and corporate giants alike are hiring like maniacs because money is no objective. The booming stock market, corporations on an acquisition binge, yield-starved investors around the world, and near-global interest rate repression are making it all possible. But when it ends, as it always does, it ends swiftly.

Tech booms turn invariably into busts. It would happen at the same time when the global tsunami of money is suddenly receding and when stocks are heading south. Interest rates are scheduled to head higher. Mortgage rates are already on the way, with 30-year rates above 4% for the first time this year. When mortgage rates reach 6%, which would still be low by historical standards…. We don’t even want to contemplate the sort of mess this confluence of factors would cause.

But we know how to deal with this. We’ve been through this before….

“Let’s ride this wave while we can, as far as we can, for as long as we can,” the speaker on our Public Radio station, KQED, said this morning, referring to the recent warnings by Gov. Jerry Brown that the next “crash” and “recession” were just “around the corner.” Read… What Does California Gov. Jerry Brown Know about the Next Crash and Recession that We Don’t?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Where are all the H1B visa holders going to live? Are the companies building dorms or pitching tents for them?

I saw this in Japan when they imported 120,000 South Asians IT workers over 2 years (Japanese Ministry of Foreign Affairs statistics). Watched groups of them trundling down the streets with their luggage in tow, off to apartments where they’d be housed in bunk beds 4 to a room. They’re grateful just for the opportunity. So grateful that many of them (I was told personally by one Indian guy in Citigroup) paid an “agency fee” of $3-4000 to their recruiter just to get the job. They are horribly abused. Off topic: the only time I ever loaned money to someone and got it back on time was my Indian colleague who’s salary was 1/4 of mine for doing the same job. In the end when I left Citigroup’s Tokyo IT section I was the only non-Indian remaining. It’s their own people who do the abuse, of course. A large proportion of agencies in Tokyo now are Indian outsourcers scamming their own citizens from home.

I worked for a Brahman and he was surprised that an American even knew what that was. They practice their caste system here while Americans are blissfully unaware.

At this point the only thing I can add is that like other immigrants their salaries will be sent back home. Next time you see a story about consumption being down, add a reference to the consumption in the countries where the local immigrants originate. It will be an eye opener.

Mainly because people from those countries can live on much less compared to us. They don’t take things for granted while we, the Americans bitch that we don’t have enough. A real lesson to learn about how to live frugally, if you ask me.

…“Let’s ride this wave while we can, as far as we can, for as long as we can,” …

Beach Boys theme? Well maybe this recession coming via the real estate mania

will end at, Dead man’s Curve

https://www.youtube.com/watch?v=ukunx21UHCA

Have a good weekend.

Similar relative madness in Toronto for single family mom and pop houses: 10 to 30% over asking and they sell in 1 to a few days, a few days only because you are given a date on which offers are to be submitted. Line up please. Love those 2.75% mortgages while the government scolds people for borrowing so much – it’s all our fault.

In contradiction to this, the really high-end stuff ( 8 digits) sells (if it ever does, or maybe they just give up) at 30 to 40% less than asking; some places have been listed for years.

And for many months now, virtually every condo sale is less than list.

So: we have the patsies bidding 30% over list based on the fact that they think they’re making money by selling their old house to some other patsy who got a 3% mortgage with 3% down but they’re really just buying an overpriced tarted-up property and a bigger mortgage possibly soon to be underwater when people give their head a shake; we have nobody with big money buying anything big; and we have a glut in condos whereby specs are trying to rent a 400sf shoebox for 2 grand a month which doesn’t even cover costs so they’re trying to sell.

Shades of 1993, when prices dropped up to 60%, unless of course, This Time It’s Different, or maybe we’re going to have the legendary Soft Landing. Or maybe we’re at a permanently high plateau …

Yep SF bat area’s housing price is getting quite frothy and soon the muppets will learn that it ain’t different this time, RE is indeed cyclical and they’ve been had as they learn the greater fool theory.

I moved to SF bay area in 2011 and bought a house in east suburb in Sept 2011. I didn’t want to buy as I thought prices were still in decling but the wife and kids pretty much said they wanted to settle in and I couldn’t extend the free temp housing with ther caveat that I must buy a house by mid 2012 to take advantage of the relo package. The previous home owner sold the house for 26% less than what they paid for in 2007 plus money lost on landscaping with other upgrades in a new development. Roll forward 4 yrs and houses in the development are being sold for more than what they sold for in 2007.

But SF pricing is just out of this world exceeding the 2007 prices by whopping 42% (895 vs 1,275) or 100% over 2011 low (615) for a small flat? Geesh I think Tokyo flat housing ran up quite a bit till the music stopped in 1989?

Yep we learn history so as to ignore at our peril, rinse and repeat it…

Greetings from SF. I’d say about 1/4 of the sales are all cash, straight from China.

Yep. My sister and her hubby bought a parking lot in S.F. back in 1989 for $135k but built a home on it with 4 floors and a loft so they didn’t have rent studios anymore for their respective businesses. Zillow has the place pegged at $2.98 million (cost $600k to build) but call it a condo… they don’t even know what it is but it is about 4200 sq ft. Its kind of funny that zillow really has no idea what the value is in this FUBAR economy and housing market. The house I had in 2001 and bought for $169k in Portland, OR is supposedly worth almost 3 times as much as what I paid for it at 414k … totally insane. The economy has never been so crappy in all my life and, travelling a lot for my job (200k to 300k miles a year usually domestic), I see the signs everywhere around the country.

i was recently quoting a project and i put that number at $1,000 and i sat there wondering if i was overbidding, then it hit me.

25 years ago i had to do 200 of those projects to buy a house and now i have to do 600….(in san fran i have to do 1,250) the thing is i can’t raise prices, i’m lucky to even get the opportunity to do a free quote.

“Let’s ride this wave while we can, as far as we can, for as long as we can,”

someone once said “as long as the music is playing you have to get up and dance and we’re still dancing”

That was Chuck Prince, ex-CEO of CitiGroup. He lost the company $10Billion over his tenure and left with a $62Million golden parachute amongst other perks such as lifetime use of the company’s executive limousine and airfleet services. I calculated while he was employed he made more on his 1st day by lunchtime than I made in a whole year. The whole reason he got the job was because he was Sandy Weill’s (the previous CEO) personal lawyer and was needed to come in and clean up any traces of fraud and malpractice left behind (or so the rumour went).