Australia’s households are the third most indebted in the world, relative to GDP, after having passed the Netherlands in 2014. Aussies are now closing in on the leader of the pack, Denmark, and second place, Switzerland.

“Given the current boom in Sydney and Melbourne, it is possible Australia will soon exceed Switzerland to become 2nd, and with enough time, perhaps 1st,” write Lindsay David and Philip Soos in a new report by LF Economics (entire report for free here).

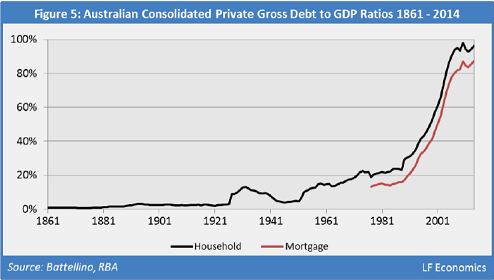

By the end of 2014, Australia’s unconsolidated household-debt-to-GDP ratio reached 118%. But it’s not because Aussies ran up their credit cards. Personal debt (credit cards, auto loans, and personal loans), after soaring in spurts and starts from 5% of GDP in 1976 to 13% of GDP in 2007, has since plunged back to just over 8% GDP, the lowest since the mid-1990s.

What they did run up was mortgage debt. It funded, as the report puts it, “the largest housing bubble on record.”

In this chart of the household-debt-to-GDP ratio, the black line (total household-debt ratio, including mortgages) has stalled thanks to plunging credit card debt, and remains below its prior peak. But the mortgage-debt ratio (red line), which accounts for most of the total household debt ratio, set a new record in 2014:

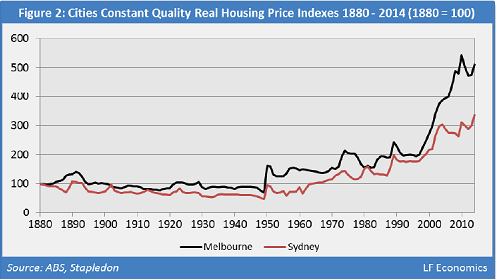

This boom in prices goes far beyond consumer price inflation and the quality improvements in housing over time. Adjusted for inflation and for these quality improvements, the Constant Quality Real Housing Price Index has soared nearly 75% for Sydney since the mid-1990s and 150% for Melbourne.

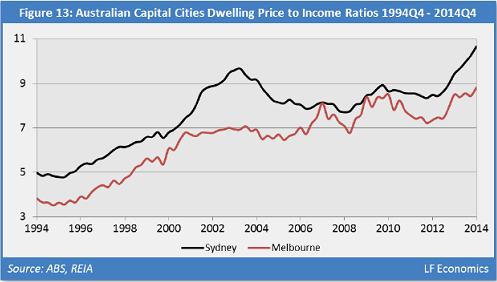

In both Melbourne and Sydney, the ratio of home prices to household incomes, a measure of housing affordability, has more than doubled since the mid-1990s, showing just how rapidly home prices have run away from incomes:

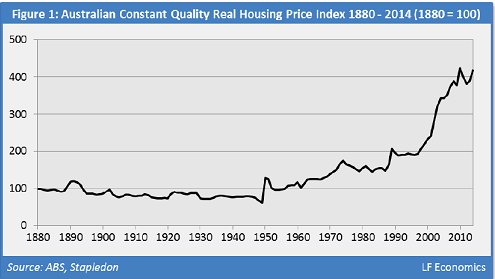

But every city has its own housing market. On an inflation adjusted basis, the capital cities Perth, Brisbane, Adelaide, Hobart, and Canberra have not yet regained their respective bubble peaks before the Financial Crisis, while Darwin has shot a lot higher.

Thus the overall picture of the Australian housing bubble. Since the Financial Crisis, it has largely been driven by Sydney and Melbourne. When adjusted for inflation and quality improvements, the national average started booming in 1996, dipped during the Financial Crisis, and according to the report’s estimate, is likely to hit a new high in 2015:

This confronts potential home buyers with prices that, since 1996, “have outpaced inflation, incomes, rents, and GDP, making it difficult for potential first home buyers (FHBs) to enter the market, while lower income households and marginal groups struggle to afford decent shelter.”

The sharp decline in interest rates since 2008 has lowered the burden of the mortgage payments, but it also provided an incentive to increase leverage for investors and homeowners and gave them the cheap fuel to run up home prices. The net result is what the report calls, “The Great Australian Debt Trap.”

All housing bubbles burst eventually. And when they do, they drag the economy into a deep recession. LF Economics in the report:

Contrary to the analyses of the vested interests, the data clearly establishes Australia is in the midst of the largest housing bubble on record. Policymakers are caught between a rock and a hard place, as implementing needed reforms will likely burst the bubble, causing severe financial and economic fallout as residential land prices revert to mean. The FIRE sector [Finance, Insurance, Real Estate] will surely blame policymakers for the bust and deflect attention away from debt-financed speculation.

The Australian mining sector is screaming towards what may be one of the most colossal economic breakdowns in modern Western history. Read… Australia Runs out of Luck, Now Needs a Miracle

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Most places with hot real estate markets have limited land availability. That is not the case with Australia. It is huge with a relatively small population. Why don’t the hot areas expand and build?

Probably because most parts of the country are not very desirable to live in, have limited infrastructure, lousy climate, etc., plus impact from the commodity bubble & Asian investors…….

Petunia,

I guess you have never been to Australia!!

Once you get out of the big cities there is basically…………………..nothing. A few mid sized cities here and there, but that is about it. Lots of worthless, non-productive land not good for much.

Think of western North Dakota or Wyoming.

Arid and semi arid areas take up some 70% of Australia. About 12% of Australia is also some kind of protected park area.

In some ways the problems about housing are similar to Japan: jobs and education.

Are you going to live in the middle of Woop Woop with no jobs or education or a vibrant, growing city with both?

In Japan small towns and cities are dying because of the lack of both and an aging population. Same here with people wanting to move to the ‘big smoke’.

Melbourne’s population is about 4.4 million people and has an area of around 3800 square miles. Our population is growing around 100, 000 people this year and estimates are that it will increase by 110,000 or so in 2016……….

High costs in the CBD and near CBD areas have forced people to move to outer areas which increase the sprawl. Years ago when we moved to our area there were few houses between the small ‘villages’ (cities??) in the outer east . Now it is nothing but kilometer after kilometer of houses on small (1/6 acre) blocks of land.

I recently talked to a client about why many Asian (ie, Chinese) are buying houses in the Mt Waverley and Glen Waverley areas of Melbourne and pushing up prices to ridiculous levels.

Private school here costs say about $25,000 a year. Public schools are a mixed bag with some very good and some very bad. Some of the areas that have good schools are the above two.

If you have three kids and pay for the cost of private schools for 12 years it is going to cost you a bundle – around $A900,000 or more just for tuition.

Why not buy a house in one of the above areas and send the kids to a quality school for little or no cost at one the better public schools? Suddenly that A$1.5 million house doesn’t ‘cost’ so much anymore and at the end of the schooling you’ll still have a decent asset.

Transport also plays a role in the places people want to buy. Right now if you want to drive into the city from where I live it will take you at least one hour on a good day. At 6:15 inthe morning the freeway is already packed. Even more when there is an accident. The Monash Freeway is more like a parking lot in the morning than anything else.

Live in an area close to the CBD and you transport nightmare disappears.

Public transport to/from the suburbs to the city is not much better with frequent cancelled and late trains. I can not remember one week where the train home has been on time every day. Buses are late or don’t show up at all.

Live in the near CBD areas or the CBD and again the problem disappears with many trains running on schedule 100% of the time. You also have a good tram network that runs in these areas and not in ‘burbs.

So there are lots of reasons for the demand of housing in the CBD and near CBD areas: education, jobs, transport, and an increasing population.

And by the way, the solution to more land here is simple: buy a house, knock it down, and build townhouses or units on the land.

Thanks for the reply. I grew up in NYC which can only grow by going up, so I am aware of what the problems of big city living are. I still think the Australians could grow by sprawl more effectively than they are doing now.

“while lower income households and marginal groups struggle to afford decent shelter.” Nope, its the middle class that are getting screwed. I was looking for an affordable place for my daughter recently in Brisbane and noted that there is a curious bottom to the market. There is no cheap and dirty available. That’s when I realized they put a plug in the bottom of the market too with schemes such as these:

http://www.qld.gov.au/housing/renting/nras/

Message to the middle class – “become a ward of the state or starve.”

Australia has plenty of land however there is a shortage of land that you can legally build on. This shortage of supply is a result of land banking by property developers who buy up surrounding farm land and withhold it from the market. They then re-zone and drip feed little by little such land into the market for the sole purpose of restricting supply to keep prices high.

Government policy promotes and protects this practise.

Sounds like Las Vegas. Thanks for all the info.

First of all many thanks Wolf for all your excellent reports.

Regarding your remark stating that Switzerland has the second largest household debt in the world, I would like to point out to you and the readers that there is a tax reason behind the high household debt figure.

Most of the Swiss citizen like to buy a house whenever possible. However, due to the lack of space and very strict building laws, appartment and house prices are sky high.

Moreover, the State calculates an imaginary rent income, which is added to your real income and on which you will have to pay taxes. However, you may deduct your mortgage interest charges from this imaginary income.

Therefore, most Swiss like to keep their mortgage even if they could pay back the money.

Due to the fact that over 60% of the Swiss are renting their house or appartment, it was so far not possible for the owners to get a change of law in this matter, although it is clear that this tax is a scandal.

Hope this helps!