The Fed speaks, the dollar crashes. The dollar was ripe. The entire world had been bullish on it. Down nearly 3% against the euro, before recovering some. The biggest drop since March 2009. Everything else jumped. Stocks, Treasuries, gold, even oil.

West Texas Intermediate had been experiencing its biggest weekly plunge since January, trading at just above $42 a barrel, a new low in the current oil bust. When the Fed released its magic words, WTI soared to $45.34 a barrel before re-sagging some. Even natural gas rose 1.8%. Energy related bonds had been drowning in red ink; they too rose when oil roared higher. It was one heck of a party.

But it was too late for some players mired in the oil and gas bust where the series of Chapter 11 bankruptcy filings continues. Next in line was Quicksilver Resources.

It had focused on producing natural gas. Natural gas was where the fracking boom got started. Fracking has a special characteristic. After a well is fracked, it produces a terrific surge of hydrocarbons during first few months, and particularly on the first day. Many drillers used the first-day production numbers, which some of them enhanced in various ways, in their investor materials. Investors drooled and threw more money at these companies that then drilled this money into the ground.

But the impressive initial production soon declines sharply. Two years later, only a fraction is coming out of the ground. So these companies had to drill more just to cover up the decline rates, and in order to drill more, they needed to borrow more money, and it triggered a junk-rated energy boom on Wall Street.

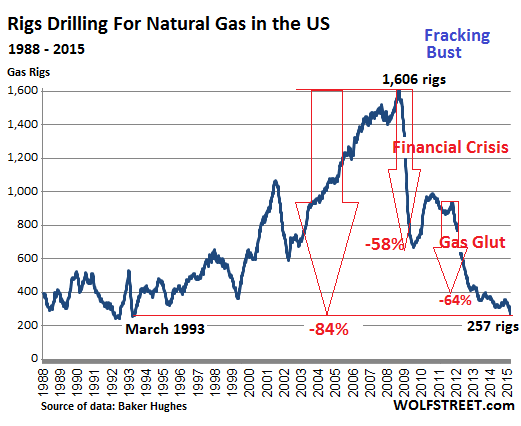

At the time, the price of natural gas was soaring. It hit $13 per million Btu at the Henry Hub in June 2008. About 1,600 rigs were drilling for gas. It was the game in town. And Wall Street firms were greasing it with other people’s money. Production soared. And the US became the largest gas producer in the world.

But then the price began to plunge. It recovered a little after the Financial Crisis but re-plunged during the gas “glut.” By April 2012, natural gas had crashed 85% from June 2008, to $1.92/mmBtu. With the exception of a few short periods, it has remained below $4/mmBtu – trading at $2.91/mmBtu today.

Throughout, gas drillers had to go back to Wall Street to borrow more money to feed the fracking orgy. They were cash-flow negative. They lost money on wells that produced mostly dry gas. Yet they kept up the charade. They aced investor presentations with fancy charts. They raved about new technologies that were performing miracles and bringing down costs. The theme was that they would make their investors rich at these gas prices.

The saving grace was that oil and natural-gas liquids, which were selling for much higher prices, also occur in many shale plays along with dry gas. So drillers began to emphasize that they were drilling for liquids, not dry gas, and they tried to switch production to liquids-rich plays. In that vein, Quicksilver ventured into the oil-rich Permian Basin in Texas. But it was too little, too late for the amount of borrowed money it had already burned through over the years by fracking for gas below cost.

During the terrible years of 2011 and 2012, drillers began reclassifying gas rigs as rigs drilling for oil. It was a judgement call, since most wells produce both. The gas rig count plummeted further, and the oil rig count skyrocketed by about the same amount. But gas production has continued to rise since, even as the gas rig count has continued to drop. On Friday, the rig count was down to 257 gas rigs, the lowest since March 1993, down 84% from its peak in 2008.

Quicksilver’s bankruptcy is a consequence of this fracking environment. It listed $2.35 billion in debts. That’s what is left from its borrowing binge that covered its negative cash flows. It listed only $1.21 billion in assets. The rest has gone up in smoke.

Its shares are worthless. Stockholders got wiped out. Creditors get to fight over the scraps.

Its leveraged loan was holding up better: the $625 million covenant-lite second-lien term loan traded at 56 cents on the dollar this morning, according to S&P Capital IQ LCD. But its junk bonds have gotten eviscerated over time. Its 9.125% senior notes due 2019 traded at 17.6 cents on the dollar; its 7.125% subordinated notes due 2016 traded at around 2 cents on the dollar.

Among its creditors, according to the Star Telegram: the Wilmington Trust National Association ($361.6 million), Delaware Trust Co. ($332.6 million), US Bank National Association ($312.7 million), and several pipeline companies, including Oasis Pipeline and Energy Transfer Fuel.

Last year, it hired restructuring advisors. On February 17, it announced that it would not make a $13.6 million interest payment on its senior notes and invoked the possibility of filing for Chapter 11. It said it would use its 30-day grace period to haggle with its creditors over the “company’s options.”

Now, those 30 days are up. But there were no other “viable options,” the company said in the statement. Its Canadian subsidiary was not included in the bankruptcy filing; it reached a forbearance agreement with its first lien secured lenders and has some breathing room until June 16.

Quicksilver isn’t alone in its travails. Samson Resources and other natural gas drillers are stuck neck-deep in the same frack mud.

A group of private equity firms, led by KKR, had acquired Samson in 2011 for $7.2 billion. Since then, Samson has lost $3 billion. It too hired restructuring advisors to deal with its $3.75 billion in debt. On March 2, Moody’s downgraded Samson to Caa3, pointing at “chronically low natural gas prices,” “suddenly weaker crude oil prices,” the “stressed liquidity position,” and delays in asset sales. It invoked the possibility of “a debt restructuring” and “a high risk of default.”

But maybe not just yet. The New York Post reported today that, according to sources, a JPMorgan-led group, which holds a $1 billion revolving line of credit, is granting Samson a waiver for an expected covenant breach. This would avert default for the moment. Under the deal, the group will reduce the size of the revolver. Last year, the same JPMorgan-led group had already reduced the credit line from $1.8 billion to $1 billion and had also waived a covenant breach.

By curtailing access to funding, they’re driving Samson deeper into what S&P Capital IQ called the “liquidity death spiral.” According to the New York Post’s sources, in August the company has to make an interest payment to its more junior creditors, “and may run out of money later this year.”

Industry soothsayers claimed vociferously over the years that natural gas drillers can make money at these prices due to new technologies and efficiencies. They said this to attract more money. But Quicksilver along with Samson Resources and others are proof that these drillers had been drilling below the cost of production for years. And they’d been bleeding every step along the way. A business model that lasts only as long as new investors are willing to bail out old investors.

But it was the crash in the price of “liquids” that made investors finally squeamish, and they began to look beyond the hype. In doing so, they’re triggering the very bloodletting amongst each other that ever more new money had delayed for years. Only now, it’s a lot more expensive for them than it would have been three years ago. While the companies – or their assets – will get through it in restructured form, investors get crushed.

And as these investors are pulling back to protect themselves, a special phenomenon occurs. Read… Junk-Rated Oil & Gas Companies in a “Liquidity Death Spiral”

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I still say the Fed/Treasury will backstop this implosion in some form or fashion. You see JPM stepping in to “assist”. This is only the start.

Since the US is complicit with Saudi Arabia in forcing oil prices down to hurt Russia and Iran, the US will “help” some of the main players in the fracking industry. Probably all. That would look too obvious. They will pick winners and losers just like 08/09. But they will not let the whole thing implode either.

This is a Saudi play alone. They want to drive the US frackers out of business and may succeed.

I don’t know what the US Public patience limit for bailing out Wall Street scum is, but we may find that out as well.

They (government) have already talked of buying 5 million barrels of oil to goose prices, but this would seem counterproductive if the drop in prices was a concerted effort to hurt Iran and Russia.

http://fuelfix.com/blog/2015/03/13/feds-to-buy-5-million-barrels-of-oil-for-emergency-stockpile/

I don’t think they planned it. This is just an inevitable occurrence from years of central bank credit infusion. Wall Street owns the government, and Wall Street is bleeding right now because of this, and more bleeding is to come. I think central banks around the world have backed themselves into a corner trying to placate the global sociopolitical elite and have no exit strategy for the coming crisis.

On the other hand, the coming crisis could just be a setup to justify another windfall of bailouts and “stimulus” to the big players, effectively thinning the herd by eradicating the up and comers who aren’t politically insulated from ruin, and of course fleecing the common man of more of his hard earned buying power. I suppose the outcome depends on whether enough of us common men realize what is going on and who to blame when it all goes down again.

the employees are more likely to be “crushed” than the investors…….

The only thing that has kept the whole fracking/shale business on its (increasingly wobbly) feet in face of plunging prices is the desperate hunt for yields. That’s it.

Take a look at corporate and sovereign bonds in investment grade (from AAA to BBB). Take a look if you dare. If you are lucky and it’s a good day you may find something yielding 2.1% after commissions and capital gain taxes. Bonds denominated in BRICS and mini-BRICS currencies (Brazilian real, South African rand, Turkish lira etc) may yield more… but is it a game you really want to play? The dollar stumbled yesterday, but it’s already climbing back. The Fed can (and most likely will) opt to stay out of the currency war. Ankara and Brasilia are already on the war path.

2.1% may sound reasonable, but we all know real world inflation will just chew all of that away and dent the capital as well. You need more yield just to stay in the same place.

At that point you have only one option: close your eyes and start scooping up junk. Now, the interest this junk pays doesn’t reflect how broken the fundamentals are. Greek bonds today pay 12-16% according to maturity. Does that really reflect the risks?

The same applies to fracking and shale outfits. Double digits yields may look good, especially after six years of ferocious financial repression, but do they really reflect the risks? These outfits weren’t making money with oil at over $80/barrel. They are loaded with debt that, by modern standards, is quite expensive to service. They need to keep pumping at full speed just to generate cash flow: they cannot adapt production to reduced demand to allow prices to normalize. And, probably worse than all, there isn’t a bailout in sight.

Banks in Texas, North Dakota etc which depend on the oil industry will most likely get a bailout, but only if things for them get really ugly: they have not enough political clout to pull an Immelt. But the outfits themselves… they’ll drop dead by the wayside one after another as they are crushed by their own debt.

If sanctions on Iran are lifted, expect the pace to quicken: the ayatollah are so desperate for hard cash they’ll pump every single barrel they can, and some, regardless of price.

At this point I maintain my original take: there won’t be an oil bust like we saw in the ’80s. This will be like Napoleon’s Grand Armée withdrawing from Russia. People falling over from sheer exhaustion and groups of stragglers left behind to be cut up by Cossacks and eaten by wolves.

The Cossacks and the wolves are vulture funds and giant oil companies such as Exxon-Mobil and Chevron. No need to tell why vulture funds have been smelling blood. And Big Oil will just be able to scoop up assets at rock bottom price using its unlimited credit. Why bother with Petrobras’ fire sale when you have a foreclosure auction in your own backyard?

The government cannot bail out the oil business, it has been subsidizing it from the beginning … and yet it has failed!

The man on the bottom goes bankrupt first, then the man in the middle, finally the tycoon cannot find either bottom men or middlemen to repay his debts; both he and his lender must fail.

The government has no independent source of funds it must borrow against the accounts of the bottom men …and they are already ruined. The ruin of the bottom man is the reason why oil prices have collapsed. The petroleum markets are international: the bankrupt marginal customer is likely Japanese or Russian … tomorrow, Chinese.

When the man on the bottom is ruined, there is nobody able to borrow … to retire the debts of the drillers. Of course, the bosses might set up a command economy as during WWII … but that would not work w/ the US as consumption would collapse even further. Anything else is more of what has obviously failed.

The entire (credit) system has run aground, not just bits and pieces of it. Minor adjustments won’t solve anything = what is underway is ‘Conservation by Other Means ™”

So the line to Chapter 11 (or 7) has formed and will grow in length every week as production continues unabated. At this point, a price jump to 50-60/bbl still can’t save a lot of these firms. And the vultures have already descended……