The oil-price plunge hit the industry when it was drunk on its own exuberance and awash in money. At the time, over-indebted junk-rated drillers had no trouble borrowing even more to drill more, efficiently or not. Dreadful IPOs flew off the shelf. Misbegotten spin-offs made Wall Street a ton of money. But in July, everything started to go awry. By October, it was clear that the oil-price plunge wasn’t a blip. By November, oil was in free fall.

Soaring production in the US, reaching 9.2 million barrels per day in January, and lackluster demand have caused US inventories to balloon. The “oil glut” was born.

So the industry adjusted by announcing waves of layoffs, whittling down operating costs, renegotiating prices with suppliers, and slashing capital expenditures. The number of rigs actively drilling for oil – a weekly gauge that indicates what’s going on in the oil field – has plummeted by 553 rigs, or 34%, since the peak in October. Never before has it plummeted this fast this far [The Fracking Bust Hits Home].

The crashing rig count was supposed to curtail production, and lower production would bring supply and demand into balance and allow the price of oil to recover. But the opposite is happening. And Devon Energy Corp. just told us why.

With total operating revenues of nearly $6 billion in the fourth quarter 2014, Devon isn’t the largest oil company out there, but it’s one of the larger players in the US shale revolution.

It reported Q4 results on Tuesday evening. According to its own measure of “core earnings,” it made $343 million. According to GAAP, it lost $408 million, after writing off “asset impairments” of $1.95 billion “related to the recent drop in oil prices.”

Stuff happens when the price of oil plunges.

But production soared – and will continue to soar. CEO John Richels explained the phenomenon in the press release:

We expect to sustain operational momentum in 2015 with the significant improvements we have seen in our completion designs and a capital program focused on development drilling. With strong results from our enhanced completions and a focus on core development areas, we expect growth in oil production to be between 20 and 25 percent in 2015, even with a projected reduction of approximately 20 percent in E&P capital spending compared to 2014.

So, despite slashing the capital expenditure budget by 20%, the company’s oil production in 2015 would grow 20% to 25%.

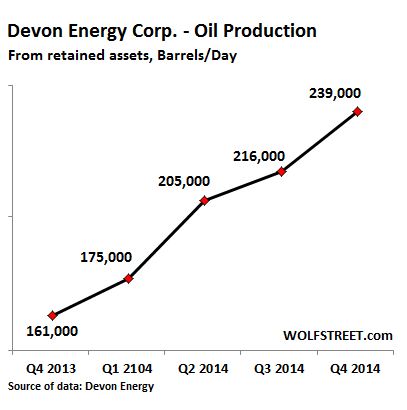

And in Q4 2014, production of oil, gas, and natural gas liquids from Devon’s “retained assets” had soared to an average of 664,000 oil-equivalent barrels (Boe) per day. This included record oil production of 239,000 barrels per day, up 48% year over year. While bitumen production in Canada grew more slowly, oil production from fracking in the US soared 82%!

This chart shows Devon’s oil production for the last five quarters:

Oil production is projected to grow another 20% to 25% in 2015. This is how Devon explained the phenomenon:

The strong growth in U.S. oil production during the quarter was largely attributable to prolific well results from the company’s world-class Eagle Ford assets. Net production in the Eagle Ford averaged 98,000 Boe per day in the fourth quarter, a 100 percent increase compared to Devon’s first month of ownership in March 2014.

And in 2015, it expects a 50% increase in production from the Eagle Ford shale.

Devon liberally praised its “significant scale in core plays,” “a consistent focus on efficient operations,” and “significant improvements in completion design.” In other words, it would spend less, it would use fewer rigs, but it would spend more efficiently – and produce more oil.

Oil – not natural gas. The price of natural gas has been a fiasco for years, and Devon has been moving away from it by selling assets and focusing its resources on oil-rich plays. Hence, natural gas production has actually edged down over the last three quarters even on a retained assets basis.

Devon will drill $1.1 billion in capital expenditures into the ground to achieve its oil production goals. It will use fewer rigs but accomplish more with them: its drill times, thanks to innovation, have improved by 47% over the last three years. And these rigs will be focused “almost exclusively” in DeWitt County, its most productive play in the Eagle Ford shale.

Other drillers are doing the same. Innovation, design improvements, efficiencies, and a relentless focus on the most productive plays will see to it that production continues to rise, despite the plunging rig count, despite the evaporating capital expenditures, despite the layoffs.

They will lose money. They have a lot of debt because the fracking boom was funded by debt. To stay alive, they must meet their interest costs. But if they slow down drilling, and production tapers off in line with the steep decline rates of fracked wells, their interest costs might eat up 50% or more of their shrinking operating profits, and the risk of default would soar – turning off the money-spigot entirely. Default might be next.

This is the brutal irony: drillers are hoping that rising production achieved with greater efficiencies allows them to meet their interest costs; but rising production pressures the price of oil to a level that may not be survivable long-term for many of them. They can lose money, burn through cash, and keep themselves above water through asset sales for only so long. And this is the terrible fracking treadmill they’ve all gotten on and now can’t get off.

In Canada, the floodgates opened in December. Perhaps it had something to do with oil, Canada’s number one export product, whose price plunge has triggered extensive bloodletting in the Canadian oil patch. Or perhaps foreign investors got spooked by something else. Read… Money Is Bailing Out of Canada

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Yes, it will get worse, but ironically, it’s because this time everyone assumed it would end quickly like 2008, so there was no capitulation, no severe cutbacks, and speculative bulls piled on, hoping to pick the bottom.

All of this has prevented $30 oil, and the necessary crash needed to begin a true recovery. And it will go on, still, most producers think it’ll be over soon, as do investors.

This is exactly why we will see a worst case scenario.

API just came out at 14.3M of buildup….I’ve never seen such a big number like that before when the number of rigs are falling.

This is not going to end nicely & it will take weeks until the dust settles.

All eyes are now on the EIA for its delayed crude oil stocks report on Thursday.

The bigger the oil glut the faster they will take us to war. A natural market for the oil glut. Johnson escalated the Vietnam war to help increase the price of WTI for his Texas buddies and the rest is history.

Obama will take us to war to distract attention away from the trillion$ in debt that cannot ever be repaid, and the trillion$ in promised social benefits that cannot be delivered, no matter how high taxes are hiked.

That is the real purpose of Obama’s “War on ISIL.”

Anybody with a functioning brain could figure out that, short of wiping them off the face of the earth, it is impossible to defeat enemies that are willing to commit suicide for their cause.

No it is not impossible. It just takes a really big stick. Think WWII

You forget that the Russians lost 2 million men helping us fight against the Nazi’s and without them we could have lost. Now we have managed to piss them off when they were trying hard to play nice with us.

The situation in oil at the moment is eerily similar to what happened at the end of WW1 in the grain markets. Farmers in the US had taken on a lot of debt to expand during the war. Europe, unable to feed itself due to the war, was an insatiable market for grain at inflated prices. When the war ended, and European farmers were home from the battlefields, the American grain markets more or less collapsed. Farmers saddled with debts that had to be serviced saw only one solution, increase production. But the more they grew, the more the price dropped. That encouraged them to grow yet more to generate cash to service their loans. The cycle was vicious and the result predictable bankruptcies, foreclosures, and forced land sales. But the losses were not limited to the farmers. Thousands of small farmer and mechanics banks could not recover their liquidity and went bust.

The irony is that the Fed of the day tried to help the farmers by pouring money into the economy, but there was little demand in the rural areas and that money ended up in the stock market instead. That was the reality that underlay the Jazz Age and the Roaring Twenties.

I think this WWI-grain theory is the best explanation to this oil problem. But the money isn’t making a Jazz Age nor a Roaring Tens, but a starving middle class and boom for the ultra-rich.

Considering typical well extraction profiles, an year-on-year increase of 50% will inevitably require a relevant increase in the number of on-line wells (> 30%). It is very doubtful so many wells are already drilled.

IMHO this looks more like a desperate company trying to assure shareholders that cash flow will remain flat. It won’t.

It is no secret that production rates lag behind rig shut-downs. When that finally runs its course, we will hit bottom – I’d say somewhere between $30 and $40 per bbl.

I think the worries of war as the ‘solution’ are mis-placed. Too many are making a buck gaming the price right now because of the previously mentioned lag.

If you think the price dropped fast from last July to January, you aint seen nothin’ yet! Nothing like a glut of oil at a time when the global economy is dead in the water.

Interesting to read this article in comparison to takes on the oil glut at other websites. Slate had an article on what I guess is the same Devon Energy report and drew markedly different conclusions. They seem to see Devon Energy as an example of American business ingenuity–more oil from fewer wells–and were quite upbeat about the oil fracking business. Then there is Market Watch which just sees the whole thing as a head scratcher. Why keep pumping instead of playing smart with supply and demand?

Well Mary, if you are still confused, there is an ad on the sidebar that shows a guy in a suit and wearing a Texas twit hat, who is recommending that you invest in the oil boom. I’m sure he would be glad to take your money.

My point was how well-informed Wolf seems to be in comparison to other commentators. In other words, an appreciation of his fact-rich journalism.

Why I’m surprised at you, clouding the issue with the facts! B-) One feature of these boom periods is the virtual disappearance of the bearish mentality. These things trigger the same circuits in the brain as gambling or drug addiction. (Some would say love) and they need more and more of the drug to keep the rush going. Mary, all that debt they took on seemed perfectly ‘logical’ at the time is now an albatross around their necks, the hurrieder I go the behinder I get. That the cheerleaders in the Fourth Estate find this brilliant shows just how much that Ivory Tower indoctrination has crippled their critical thinking skills (if they ever had any). I’m glad you’re out of their clutches and safely ensconced here at Wolf Street.

Working for Schlumberger in the 70’s and 80’s I saw two oil booms and two oil busts in the span of less than half a decade. Sound familiar? They were caused by the same problem, money printing and removal of the punch bowl. In those days, however, the industry was growing because the USA was still, technically, at least, solvent.

The business model I understood then I don’t think has changed today. It is margin. The oil business needs at least 4% to survive. This is true from the drillers all the way down to the gas stations. With today’s 0% ZIRP,, they’re not in trouble yet. The gas station owners were screwed long ago, so they’re having a last laugh so to speak, as the falling price has resulted in positive margins for the first time in nearly a generation. The bigger players raise production when margins are higher, and believe me they ARE higher, as they make almost $.25 per gallon now from production all the way to the dealer via the refinery (if they have the vertical integration.). The current oil price of $1.12/ gal means the effective margins for oil producers are an astronomical 22%! Last year, at $2.60 they were UNDER 10% and most of the majors were struggling with cap problems.

Even with debt, I think the industry is hiding its’ own boom. What do they fear, why another money printing boom which will cause them to ‘invest’ again. If you don’t believe me, take the REAL numbers from DEVON and let me know what you come up with, I came up with $.25 per gallon (assuming they own their own refining capacity) based on their projections and the CURRENT OIL (ETF) which is conveniently priced in decagallons.

I managed to retain my job through the Iranian hostage crisis, but lost it thereafter as the RIG count from our biggest customer (TOSCO) crashed after their bankruptcy, failing to find producible oil in the Utah shale country. If this doesn’t sound familiar to you, say 1973 (gold standard to fiat), 1979, 1986 … 2008, 2014, then history doesn’t repeat itself. I lost only one job because of it, but it was a valuable lesson on bubbles. The little people are the ones hurt by booms, not the ‘producers’, they will be just fine. The fall in prices IMPROVES their position, with very few exceptions.

Worked in R&D at Dowell-Schlumberger in Tulsa, OK from 1985-87 … few friends laid off every week, for 2 years … and then half of what was left all at once … fun.

We were in Tulsa at the time. I remember the impact of the oil bust on the business I was running. I remember how restaurants shut down, one after the other. The bank I bought my condo from (after the developer had defaulted on the loan) collapsed a few months later. I’d gotten the unit at 50% of the financed cost. My neighbor bought his unit half a year later from the FDIC and paid 20% less than I’d paid. Tough times, with some opportunities.

I don’t think Tulsa ever really recovered, unlike Houston. Part of the problem was that most of the major oil companies moved to Houston. The Oxy tower capped at the eight floor? Man, what glorious black stump it made/makes.

Mary, by continuing to pump they lose money at a slightly slower rate than they would if they stopped.

They dont have anything else to do anyway! :-)

A land lease agreement may dictate drilling and production activities (and royalty payments!) on a certain schedule or you lose the lease. So, produce until you go under…….

@Wolf sez:

“So, despite slashing the capital expenditure budget by 20%, the company’s (Devon’s) oil production in 2015 would grow 20% to 25% … “

If Devon could be persuaded to cut its investments another 80% its ‘production’ would certainly increase by that amount or more! Afterward, oil would be competitive with ‘fusion-in-a-bottle’, Thorium reactors and ‘Zero-Point energy’.

Devon is scraping the bottom of the energy barrel, the ballooning costs of doing so are shifted to (bankrupt) customers who cannot afford them any more, that is, the customers can no longer borrow.

The same customers will not be able to magically borrow when the prices fall further as they must. Bankruptcy is catching, all you need is to be indebted.

It’s not just energy prices but across categories; retail, construction, real estate (both in the US and elsewhere). Soaring bond prices speak for themselves: ROI = a few piddling basis points wherever one chooses to look (or negative ROI)

The 2008 recession never really ended, what we got was a fake.

I’m missing the chilling part of Devon’s comments re: their results. I agree with the view that highly levered, smaller companies in the space will struggle with interest expense if oil revenues remain at this level, but, taking a quick look at Devon’s public statements, their debt to EBITDA is somewhere around 1.5% – that does not seem highly leveraged to me. Expectations are that funds from operations to debt should remain above 45%.

Floyd, I hope you understand that I wasn’t using Devon as an example of a company that would not make it, but as an example of a company that is continuing to grow production, which was the topic of the article (the “Oil Glut” part). As you suggested, Devon is doing a lot of things right. It’s not junk rated, and at this point isn’t cut off from the financial markets.

A few weeks ago Western Canadian Select was selling at $20/barrel. I retired a while ago, but the last time I was working at Syncrude it was running around $30/barrel production cost.

I realize oil sands production can’t be compared to sand fracked wells that deplete so rapidly but I can’t see Syncrude or Suncor going on for more than 18 months before the lights get turned out. That would bankrupt Alberta.