The floodgates opened in December. Perhaps it had something to do with oil, Canada’s number one export product, whose price went into free-fall in November and triggered extensive bloodletting in the Canadian oil patch. Or perhaps foreign investors got spooked by something else.

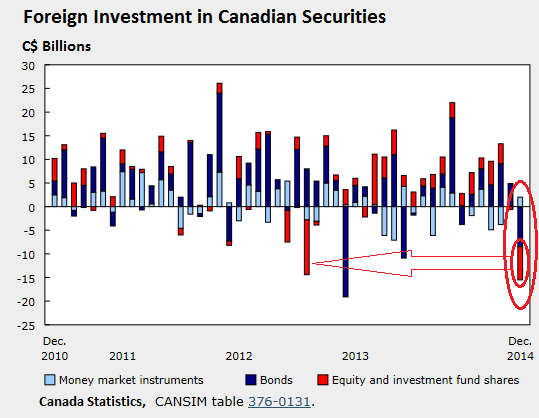

Until then, they’d been sanguine: from January through November, they’d added C$72.5 billion in Canadian securities to their holdings. But in December, they suddenly dumped C$13.5 billion – the most in 18 months.

That included C$8.5 billion in Canadian government and corporate bonds, according to Statistics Canada, which defines bonds as debt with an original term to maturity of more than one year. This wholesale dumping of bonds was partially offset by an increase of C$2 billion in money market instruments. They went looking for the safety of short maturities.

And as Canadian stocks fell a barely perceptible 0.8% in December, these frazzled foreign investors who’d splurged on Canadian equities from January through November by adding another $32.3 billion to their holdings, suddenly dumped C$7.0 billion of their shares, the most since February 2013.

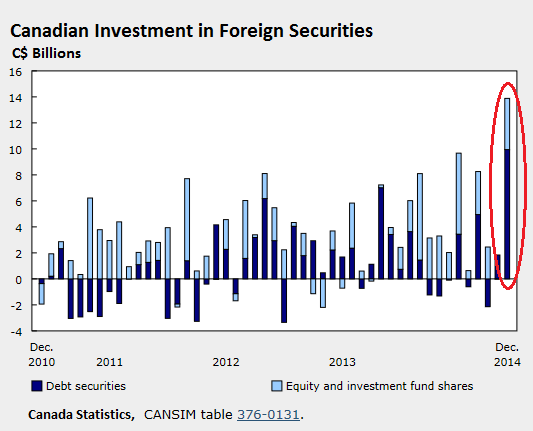

But it wasn’t just foreign investors who got frazzled in December. Canadians too ran scared and sent C$13.9 billion of their hard-earned money across the border – the most since December 2000!

The bulk of it went into US Treasuries. In October, with QE in the US petering out, Canadians were still trying to get rid of their Treasuries. But in November, they reversed course. And in December, they piled back in and bought C$8.5 billion in US Treasuries, an all-time record!

They also bought C$1.4 billion in other foreign bonds and increased their holdings of foreign equities by C$3.9 billion, mostly US stocks. Unlike Canadian stocks, US stocks rose 0.7% in December, Canada Statistics helpfully pointed out. For the year, Canadians bought C$35.7 billion in foreign stocks – nearly two-thirds of them non-US stocks – the largest annual buying spree of foreign stocks since 2000.

These fund flows exclude transactions in equity and debt instruments between affiliated enterprises, classified as foreign direct investment in the international accounts.

Note in the chart below the high proportion of foreign equity purchases for much of the year until November and December, when US Treasuries, considered a safe haven, became the investment of choice:

With foreigners bailing out of Canadian securities and with Canadians taking their money and investing it in foreign securities, the total outflow of funds from the Canadian economy for December reached C$27.4 billion.

The turn came suddenly: in the prior months, foreigners were still busily buying Canadian securities. But the December outflows dragged down the entire fourth quarter. With total outflows of C$15.7 billion, it was the worst quarter since Q4 2007 as the Financial Crisis was worming itself into the system.

The December outflows also dragged down the fund inflows for the entire year to $3.4 billion. It was the seventh year in a row of net inflows, but the lowest since 2008 during the Financial Crisis.

Perhaps these investment decisions were based on the assumption that the US economy would be strengthening, which has been predicted for years. But maybe the assumption is that this time, the predictions would actually come true.

Or maybe a bitter whiff of a toxic mix is worrying these investors.

Back in July, ratings agency Fitch had already warned about Canada’s housing bubble and “high household debt relative to disposable income” that “has made the market more susceptible to market stresses.” In September, the Bank of Canada too warned about the housing bubble and what an implosion would do to the banks. Then in January, oil-and-gas data provider CanOils found that “less than 20%” of the top 50 Canadian oil companies would be able to sustain operations with oil at US$50 per barrel. And these fears are now coming to pass. Read… Canada Mauled by Oil Bust, Job Losses Pile Up – Housing Bubble, Banks at Risk

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Heh, the Canadian banks are pretty smug too, thinking they’re better than everyone else because of our wonderful regulations.

I went in and moved money around to make sure I was covered for the majority of my holdings under the CDIC’s $100,000 per institution insurance. (In Canada, you get $100,000 PER Institution – so moving $600,000 around to ensure it is all covered under insurance means you need to deal with six different institutions). I also converted some of my “buy and hold” stocks which I plan on having for several years into actual stock certificates held in my safety deposit box.

Well, they looked at me like I was insane.

Canadian banks will NEVER go broke! Didn’t you see how well we sailed through the last market crash? (Um… that’s the problem – your bad debt didn’t wash out).

Holy crap, the one bank even set up an appointment for me to speak to a senior level financial advisor, who pulled all sorts of tricks trying to convince me Canadian Banks are 100% secure – most especially theirs, of course.

“Look,” I said, “the insurance is FREE so long as I use six different institutions. Where is your feduciary responsibility here? It is in MY best interest to have all this money under 100% insurance rather than only 17% of it!”

When I discussed things further with this great financial wizard, I asked her why the Bank of Montreal lost 60% of its market cap during the last correction.

“Because they were too exposed to US Debt,” she replied.

“Yes… so it’s NOT like you guys are immune from speculation.”

Pfft… when I asked where they got the higher interest rate to pay for one term deposit’s sky-high 2.75% interest when government bonds pay lower, she said it was “bundled” with the bank’s own mortgages as well a private infrastructure lending.

I see… so you pay out my “secure” term deposits with mortgages that are WAY over-valued and never corrected during the last crisis (meaning they are even higher risk now) and also with lending for “Public Private Partnerships” financed by municipalities… kinda like Detroit and other North American cities that either are, or soon will be, bankrupt.

Lol! Clowns. Who cares what they think. Maybe the CDIC insurance won’t help me when the SHTF (there are better hedges than the gov’t), but it’s better than not being able to claim at all because you’ve stupidly held all your wealth in one institution. Geez. It only took me a few days to insure over $500,000 of previously uninsured assets at no other cost than my time, and they FREAKED at me.

Good call, but you know CDIC isn’t able to cover a serious crash right? You may feel safer, but if this goes the way i think it’ll go, none of your money is safe IMO.

You got it. My guess is 100 ounces of silver will be worth more than your entire cash stash.

–> Mike

Ya, but when?

my man .. good post … glad ur thinking .. you are correct … a correction is coming. You are wise to position yourself accordingly. There are 2 points you may have missed. The Bank of Canada is only capitalized at less than one half of one %. Yes, that number is correct. Who is to say they can even meet their $100 000.00 threshold? And also, do you recall the 2012 budget whereby they announced plans to confiscate Canadian’s bank accounts in the event of a financial catastrophe? Hmmm, interest rate swaps, collateralized debt obligations, 1.2 quadrillion dollars in derivatives … loads of household debt, municipal debt, provincial debt, federal debt. Oh, the IMF is suggesting we print more. And finally not to mention Ukraine and Greece. It’s getting olive oil type of slippery out there. Confiscation is a threat you will hopefully, not fully dismiss. Let us not forget Cyprus …

Hi Vimy,

Yes, those are two good points you’ve made.

Here is my thinking on them: At the very least, even if there isn’t enough money there (and there obviously isn’t), I suspect what will happen is that they will still only insure people up to the $100,000 and then cut the rest off with absolutely no right to claim whatsoever beyond that amount… and then, since Canada has its own Central Bank, they will just print off the money to cover their obligations.

But of course, ultimately I have no idea what they will do in the future… but I do suspect that I will fair better with 6 separate claims against the insurance with which to pursue legal action than just one for $100,000, in the likely event that they won’t be able to cover. Even if I could only recoup $0.10 on the dollar (or less), I will be able to recoup 6 times more than if I had done nothing. Also, I suspect that not ALL the banks would go bust – we only have six major banks in Canada and that would mean there wouldn’t be a bank left standing in the entire country except for credit unions.

On the confiscation, you are right – in fact, it was Jim Flaherty’s announcement of bail-ins that originally spurred me to action. Here was another act of irresponsibility (I think) on the banks. Take that financial advisor… well, she came prepared with news articles and such other things trying to illustrate Flaherty’s insistence that he was NOT talking about bail-ins ala Cyprus.

Lol! However, little did she know, in my “research file” I had with me was a copy of the actual budget along with the legal definition of EXACTLY what was getting put on the books. Indeed, it stated quite clearly that the bank would have to draw off its “liabilities” (read deposits) rather than expect tax funding.

The gist of what Flaherty and the banks were “trying” to say was that they wanted the banks to set up their own equity funds – aside from their client’s deposits – to ensure they didn’t get over-leveraged.

Yeah, yeah… I get it. You guys are saying that the banks SHOULD set aside their equity-slush funds of BILLIONS of dollars, and have it sitting on hand at the ready to ensure they won’t need a bail-out.

Except, as I pointed out to the financial advisor, do they really expect me to believe that the bank is going to set aside say, $100 Billion in some slush fund and not try to collect interest on it? I mean, they won’t let that cash slush fund just sit there idle without earning a profit on it in the meantime, so even if the banks DID set aside their own extra equity to make sure they don’t get over-leveraged, where is the fine-print saying you aren’t allowed to speculate with THAT money in the meantime? It doesn’t exist, so of course the banks are going to re-invest that money and take risks on it.

And… it doesn’t really matter two hoots what the Finance Minister “says.” His “words” are not the law simply because he’s a politician. In our country, as in any other Western country, THE LAW is the law. As in, if Prime Minister Stephen Harper were catching a ride with me in my car and told me to ignore the speed limits and go as fast as I want, when I get pulled over by the police I have no legal recourse to say “Harper said this and that” because Harper is NOT above the law and neither is/was Flaherty. What it says in the law books is what matters, and despite what Flaherty “meant” to say and now claims was just misunderstanding, THE LAW clearly states that banks must use their liabilities rather tax-payer bailouts. It does not differentiate which liabilites, it only says “liabilities” – full stop – which legally includes my deposits.

Meh… in the end, I got it all done, despite their trying to make me feel like a foolish asshat for protecting myself as much as I could.

Screw ’em.

Vimy15 the doc you are referring to is the Economic Action Plan 2013 and it’s a freakin duzzy. My wife has upwards of 28K in one of the Big Five and I’m hoping that that is not lost when the govt. comes calling to prop up the “systemically important financial institutions”. Weird thing Vimy15, these days it’s scary to own 600K within the banking establishment. You are better off taking out some of that money, pay the penalties and purchase a sh#@load of gold and silver and stash it somewhere safe. You get my drift my man?

Of course they are smug. They fooled 99% of the population. I have tried to tell people (like my brother) that, yes our banks got bailed out too, but they won’t believe it. Propaganda works.

The Big Banks’ Big Secret

Estimating government support for Canadian banks during the financial crisis

https://www.policyalternatives.ca/publications/reports/big-banks-big-secret

I’ve been looking for opportunities in Canada. Virtually nothing in the way of credible financial blogs and the online news media is a tepid broth of economic boosterism.

From my travels there, the people seemed strained from ‘austerity’. Yes they call it that, just like in Greece. Jobs are scarce.

It seems

1) Job growth is minimal (except in Alberta as the news-media proclaim there is a worker-shortage attributable to a skills gap. Hmmm, sounds familiar!

2) household debt is high and housing prices have never corrected.

See crackshackormansion.com for how silly pricing has become.

3) Non-energy exports are weak to down.

It’s funny how in many areas there are housing building booms yet the communities that will serve these new properties are distressed. Foreign money I suppose. Store closings (US based ‘Target’ the most prominent) seem the rule.

Anyone know of any good Canadian financial web-sites?

Born and bred Canadian here, know the landscape well. Must’ve been a while since you’ve visited cause Alberta sure as heck isn’t the job capital anymore.

As for financial websites, you’re correct, just a mash of feel good sleeping pills for the masses. The best info is (sadly)found on blogs run by average people doing it as a hobby, nothing you could go to for a paycheck that’s for sure.

Like Mick, I wouldn’t be able to recommend one because I’ve never really found anything aside from the odd amateurish one, which usually peters out after a few months.

It’s really difficult to figure out the real deal in Canada too – the media here is way more PC than in the USA (believe it or not). The only Business News Channel in Canada is so far leftwing they might as well just blatantly represent Marxism rather than Capitalism.

I’ve had the best luck figuring things out by literally comparing things in the USA to what I see with my eyes here in person – like the CDIC insurance I spoke of further up. There is scant information on this stuff in Canada, so… I started researching the USA’s FDIC insurance of $250,000, and then compared the similarities and differences to Canada’s CDIC insurance. The things which were the same as in the USA I assumed were based upon the same principles, and the differences I investigated against what the USA had until I came up with a more complete picture of my person situation in Canada.

Some of the US info on Canada from the USA is vastly misunderstood by the US Media, and I suspect you would have to be fairly familiar with the intricacies of the country to grasp it in a proper concept.

Take the Vancouver housing market, for example. Yes, it is high – outrageously high and in need of major correction – but the extremes of Vancouver are unique to Vancouver, not the rest of the country, as many media pundits insinuate. Vancouver’s real-estate has always been high, and always will be significantly higher than anywhere else. It is, after all, Canada’s third largest city with a population of 2,000,000 – but it has a major land shortage, being that it is boxed in by the ocean, the mountains, and the Fraser River… further, when Vancouver’s city planners designed its expansion, they purposefully created a bottle-neck by allowing only a few scant bridges over the river, and also by eliminating any freeways going through the heart of the city. This was done to prevent urban sprawl – they’ve made it so difficult to get into Vancouver, that no-one can possibly do a 30 or 40 mile commute into the heart of the city on a regular basis. I live only 60miles outside of Vancouver and regularly schedule 2 to 2.5 hours to get there.

Also, Vancouver’s housing is high because southwestern BC is about the only place in Canada that has a mild climate in the winter (most often only 2 weeks of snow a year, or less) and thus, with its ocean, beaches, mountains etc. added, it is one of the most premier cities in the country for people to wish to live in (if you can stand all the freaks that also congregate there).

AND, when Hong Kong reverted back to China in 1999, Canada fully opened its borders to the people of Hong Kong – our partner in the Common-Wealth, allowing any of its citizens to immigrate to Canada with very little fuss should they want to leave before Communist rule. About 500,000 of them took us up on it and settled in Vancouver’s suburb of Richmond… and even to this day, the Chinese have an enormous presence in Vancouver, as it is now one of the premier places for the Chinese to invest in off-shore real-estate. (That is probably the most likely factor for Vancouver’s real-estate to go bust: A bust in Chinese real-estate investment)

Phew… but that is stuff that most Canadians just “know” and so when they point out how high Canadian real-estate is by showing Vancouver’s prices, we’re all like “so what?” When hasn’t it cost two to three times more than anywhere else in BC to live in Vancouver? It’s been that way since at least the 1970’s and likely will be even after the crash.

It’s not to say the place is currently “sane” though.

I rented a 550sf 1BR apartment in downtown Vancouver back in 2003. At the time it was for sale for $189,900 – which I just about crapped my pants over, since I could have bought a 4 Bedroom 1500-2000sf house on a quarter acre lot elsewhere in the province for significantly LESS than that… so I rented rather than buying.

By 2006, my apartment had risen in price to $360,000. And the units in that building are still selling for that or more today, despite the 2008/09 “correction.”

Certainly Vancouver is an over-valued Real Estate market… but no matter, after things correct, it will still be two to three times as much money to live there than anywhere else in the country.

Could be that this transfer of funds is what is causing the US stock market to reach new highs. Canadian money plus the new printed monies coming out of Europe may be what is driving the S&P to new heights.

The final push???

Jeb, you would have had a much shorter convo with the bank rep if you had asked if HE keeps more than $CAD100K in his own damn bank.

Yeah… it didn’t take me too long to just ignore them and do my own thing. It was their initial smug arrogance about their infalibity which really suprised me though. All I could keep thinking was “Pride Goeth Before the Fall.”

Jen et al: I am a former independent financial advisor and I can assure you that the vast majority of my former peers have absolutely no clue about what is going on in the world. Most are merely singing the company and industry song. Especially bad are those who are employed by banks.

” But in December, they suddenly dumped C$13.5 billion – the most in 18 months.” It didn’t help that bondholders and savers were savaged by massive devaluation of the loonie the past 18 months ( and for what- the privilege of giving foreigners their natural resources more cheaply)

Hey Wolf: here are some choice bullets from the article that I think are very interesting

(1) Canadians too ran scared and sent C$13.9 billion of their hard-earned money across the border – the most since December 2000! 1997-2001 was the last period of massive oil price deleveraging, the Canadians headed for the exits back then too!

(2) They also bought C$1.4 billion in other foreign bonds and increased their holdings of foreign equities by C$3.9 billion, mostly US stocks… largest annual buying spree of foreign stocks since 2000. The Nasdaq peaked in March 2000 and its’ about to peak again. Are Canadian investors the canary in our stock investment coal mine?

Curious, isn’t it?

Out of interest, does anyone know how much money the Bank of Canada (central bank) has printed using QE? Answer – 0.

What is Canada’s federal deficit? Close to zero.

Yes the provinces have issues, serious issues, but Canada has a lot more of a buffer than most against hard times.

Yes do not mistake Vancouver for Canada. Real estate is far from nuts everywhere.

Even the oil and commodity prices have to an extent been blunted – by the falling $C. A $50 US price is now C$62.50, and since most costs for running existing wells/oil sands are $C costs (labour) it is not as bad as it seems at first blush.

Canadian exporters are having a field day. We sell 90% in US$, mostly to the US. We have not adjusted our prices and now get 20% more for our products in C$. That goes straight to the bottom line – frigging amazing impact!

Also housing over valuation gets leveled by a lower dollar. My C$300,000 house was US$300,000, now it is US$225,000 – really quite reasonable if you ask me.

I’d say if Canada gets hit hard this time the rest of the world will be on life support first.

You’re forgetting your national credit card is maxed out to the tune of over almost 2 trillion dollars. Not bad, compared to USA %GDP wise. If your buffer is to go further into debt, then welcome to the club.

https://en.wikipedia.org/wiki/Canadian_Public_Debt

Non-energy exports are mediocre.

http://www.canadianbusiness.com/economy/canada-needs-to-confront-its-shrinking-exports-problem-mike-moffatt/

Sans oil I’m not seeing a vibrant growing Canada. I’m sold on the people and place, but the comments above by Jeb about foreign money goosing the market sounds very familiar to my ears. The real estate market in Canada is not based on ‘organic growth’ tied to internal consumption or trade; rather, flows of hot money.

I watched crap 1 bdr 700 sqft condos in Southern California go from 100k in 1992 to 400k in 2006. Watched them fall back to 200k (still outrageous).

What do we export, besides timber, minerals, and oil? The TSX consists primarily of gold miners.

Jim you are spot on that’s for sure. Canada is a very different animal because….it’s Canada. It doesn’t matter where our loonie goes we have wanted exports up the ying yang( I love our quaint phrases), it doesn’t matter how our housing market fleshes out because we have thousands of kilometres between economic regions AND it doesn’t matter what troubles our endless gold mines and oil patches seem to have because they’re still in the ground and still Canadian. If our Central Bank does what most Canadians believe Poloz and Company will do is ensure our interests are taken care of and in the end the greatest country in the world will always land on their feet and survive whatever comes OUR way because….that’s what always happens in our world. End of story.

Re: Canadian Federal Court of Appeal | January 26, 2015 | Canadians Win In Court Against Bank of Canada “et al”

All posters…please be aware of this Canadian landmark case. Please pass the word along as the mainstream media will not cover the story (I sent it to them but they have refused to advised Canadians of the importance of this decision).

http://investmentwatchblog.com/canadians-win-in-court-against-bank-of-canada-enormous-implications/

Here’s the link to the Federal Court of Appeal Case: http://decisions.fct-cf.gc.ca/fca-caf/decisions/en/item/100762/index.do?r=AAAAAQAFY29tZXIAAAAAAQ

Also note: HER MAJESTY THE QUEEN, THE MINISTER OR FINANCE, THE MINISTER OF NATIONAL REVENUE, THE BANK OF CANADA, THE ATTORNEY GENERAL OF CANADA have 60 days (from January 16, 2015) to seek “leave to appeal” to the Supreme Court of Canada. It is believed by Mr. Galati, Constitutional lawyer who brought the claim forth that the Federal Government will not appeal to the SCC.

Additional Information:

Rocco Galati is a prominent Canadian Constitutional lawyer. He and two other citizens William KREHM and Ann EMMETT filed the claim. Against the odds these people pursued the case relentlessly with the objective of forcing the Federal Government to adhere to the Canadian Constitution. Referring to the chart below the case progressed through the system; first, the Federal Administrative Tribunals, next, the Federal Court and then onto the Federal Court of Appeal (3 Judge panel), the highest Federal Court in Canada.

For more information you may google the topic, the lawyer Rocco Galati, and/or see below:

http://www.comer.org/

http://www.comer.org/archives/2013/COMER_March2013.pdf

Hear Hear!!

I want to thank our Canadian friends for the fascinating tutorial on “grandmother’s land”, I’ve been to the Toronto/London area a few times in the truck, looks like Ohio to me. I learn the most interesting things reading Wolf Street.

@ Wolf

Excellent article – a rare reveal of the ‘belly of the beast.’

While Canada may be in somewhat better shape than other developed countries where its national debt is concerned (thanks to Harper), Canadians are NOT is good shape, and owe much more than their US neighbours on a personal basis.

Canadian banks have done a great job of turning Canadians into an ‘indentured’ species, but have done nothing for small to medium sized businesses.

Through the years of the Oil Boom, and the 20 year dependence on the Immigration Industry, Canada has failed to produce Entrepreneurs. The socialist mentality which represents about 60% of the voting public seems to happily rail against corporations and can’t differentiate large ones from small. Capitalism is evil apparently.

The fact that a society can only be successful and sustaining if it inspires entrepreneurs and produces enough of then to create jobs, seems to have vacated the national dialogue.

Jeb’s note above that even the business channel,

“is so far leftwing they might as well just blatantly represent Marxism rather than Capitalism,” is unfortunately too close to the truth.

The media is feeding Canadians what they have become comfortable with. After generations of swallowing the same pablum, any alternative is distasteful.

I think you may have missed another large reason for bailing on Canadian investments – particularly for American citizens living in Canada – and that being the ratcheting up of US Treasury enforcement of PFIC rules which essentially and absurdly brands any Canadian mutual fund or ETF as a passive foreign investment corporation for tax purposes. The upshot of this is that US gains taxation is so punitive and the tax preparation time so onerous for very ordinary mutual fund or ETF investments, that there is no recourse but to redeem any positions in Canadian investments and repatriate the money back to US investments – either that or try to live on virtually non-existent interest for time deposits! It seems that enforcement is about to begin in earnest as Canadian banks are now required to report US citizens in their customer base to the US IRS. In fact, banks around the world are dumping and prohibiting US citizens as customers to avoid the onerous US reporting requirements.