Crude oil had rallied 20% in three days, with West Texas Intermediate jumping $9 a barrel since Friday morning, from $44.51 a barrel to $53.56 at its peak on Tuesday. “Bull market” was what we read Tuesday night. The trigger had been the Baker Hughes report of active rigs drilling for oil in the US, which had plummeted by the most ever during the latest week. It caused a bout of short covering that accelerated the gains. It was a truly phenomenal rally!

But the weekly rig count hasn’t dropped nearly enough to make a dent into production. It’s down 24% from its peak in October. During the last oil bust, it had dropped 60%. It’s way too soon to tell what impact it will have because for now, production of oil is still rising [my post from Friday… Oil Price Soars, Rig Count Plunges Worst Ever, But Bloodletting Just Beginning].

And that phenomenal three-day 20% rally imploded today when it came in contact with another reality: rising production, slack demand, and soaring crude oil inventories in the US.

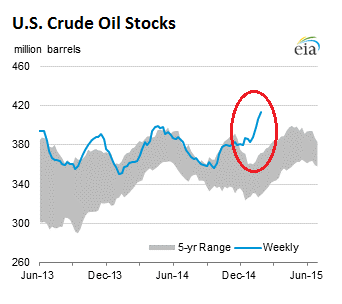

The Energy Information Administration reported that these inventories (excluding the Strategic Petroleum Reserve) rose by another 6.3 million barrels last week to 413.1 million barrels – the highest level in the weekly data going back to 1982. Note the increasingly scary upward trajectory that is making a mockery of the 5-year range and seasonal fluctuations:

And there is still no respite in sight.

Oil production in the US is still increasing and now runs at a multi-decade high of 9.2 million barrels a day. But demand for petroleum products, such as gasoline, dropped last week, according to the EIA, and so gasoline inventories jumped by 2.3 million barrels. Disappointed analysts, who’d hoped for a drop of 300,000 barrels, blamed the winter weather in the East that had kept people from driving (though in California, the weather has been gorgeous). And inventories of distillate, such as heating oil and diesel, rose by 1.8 million barrels. Analysts had hoped for a drop of 2.2 million barrels.

In response to this ugly data, WTI plunged $4.50 per barrel, or 8.5%, to $48.54 as I’m writing this. It gave up half of the phenomenal three-day rally in a single day.

Macquarie Research explained it this way:

In our experience, oil markets rarely exhibit V-shaped recoveries and we would be surprised if an oversupply situation as severe as the current one was resolved this soon. In fact, our balances indicate the absolute oversupply is set to become more severe heading into 2Q15.

Those hoping for a quick end to the oil glut in the US, and elsewhere in the world, may be disappointed because there is another principle at work – and that principle has already kicked in.

As the price has crashed, oil companies aren’t going to just exit the industry. Producing oil is what they do, and they’re not going to switch to selling diapers online. They’re going to continue to produce oil, and in order to survive in this brutal pricing environment, they have to adjust in a myriad ways.

“Efficiency and innovation, when price falls, it accelerates, because necessity is the mother of invention,” Michael Masters, CEO of Masters Capital Management, explained to FT Alphaville on Monday, in the middle of the three-day rally. “Even if the investment only spits out quarters, or even nickels, you don’t turn it off.”

Crude has been overvalued for over five years, he said. “Whenever the return on capital is in the high double digits, that’s not sustainable in nature.” And the industry has gotten fat during those years.

Now, the fat is getting trimmed off. To survive, companies are cutting operating costs and capital expenditures, and they’re shifting the remaining funds to the most productive plays, and they’re pushing 20% or even 30% price concessions on their suppliers, and the damage spreads in all directions, but they’ll keep producing oil, maybe more of it than before, but more efficiently.

This is where American firms excel: using ingenuity to survive. The exploration and production sector has been through this before. And those whose debts overwhelm them – and there will be a slew of them – will default and restructure, wiping out stockholders and perhaps junior debt holders, and those who hold the senior debt will own the company, minus much of the debt. The groundwork is already being done, as private equity firms and hedge funds offer credit to teetering oil companies at exorbitant rates, with an eye on the assets in case of default. [read… “Vulture” Investors Descend on the Oil Patch].

And these restructured companies will continue to produce oil, even if the price drops further.

So Masters said that, “in our view, production will not decrease but increase,” and that increased production “will be around a lot longer than people are forecasting right now.”

After the industry goes through its adjustment process, focused on running highly efficient operations, it can still scrape by with oil at $45 a barrel, he estimated, which would keep production flowing and the glut intact. And the market has to appreciate that possibility.

What ratings agency Fitch and the Bank of Canada had warned about has come to pass. Read… Canada Mauled by Oil Bust, Job Losses Pile Up – Housing Bubble, Banks at Risk

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

These oil companies were losing money @ $100/barrel. Somehow they will make a profit @ $50?

“To survive, companies are cutting operating costs and capital expenditures, and they’re shifting the remaining funds to the most productive plays, and they’re pushing 20% or even 30% price concessions on their suppliers, and the damage spreads in all directions, but they’ll keep producing oil, maybe more of it than before, but more efficiently.”

And make up their losses with volume! The hope-and-prayer is that fresh loans will pick up the slack … until the good times return.

But they aren’t coming back. What doesn’t change is the return on consumption … which is a negative number. No matter how much efficiency can be wrung out of the extraction side, nothing changes on the side that really loses money, the automobile- wasting of energy side.

Our cars have bankrupted us to the point we cannot afford to bid for oil any more. Our banks will not lend to us, they need to lend to the drillers even though the same drillers need to sell their oil products to us in order to retire these loans. We haven’t figured out what to do with the oil other than burn it up for nothing. We need loans like the drillers; because we are insolvent we cannot borrow.

It isn’t just the drillers’ overhead costs that spread in all directions. The (non)exchange of money for gasoline at filling stations millions of times per day determines the worth of money. Ordinary monetary policy as determined by finance and central banks becomes irrelevant, interest rates no longer matter. Currencies — particularly the US dollar — become hard and are hoarded, the dollar becomes the last-best chance at petroleum. The outcome is a steady deterioration in efficiency of consumption by way of dollar preference: no matter how low the price of oil falls it never is low enough to finance consumption …

We have not reached this condition … yet. But when we do (finger cutting gesture across throat).

At my investment firm, most brokers, and even the head analyst still don’t get it. They’re all chomping at the bit to try to buy the bottom. And that’s after being suckered into bull traps already. Reality takes a very long time to set in.

Good point.

I think the “lower” cost producers with huge welfare/entitlement programs like Saudis, Venezuelans and many of the OPEC nations will pump more to make up for the lower oil price. It’s catch 22 as many of these regimes cannot stay in power unless they pump like crazy to get their heads barely above the water.

As for Saudi conspiracy theory about brining oil price down to torpedo the fracking (especially in US) and the Russians – I say be careful what you wish for as low oil price may bring more instability to the middle east and their next move might be to start a “war” there to boost oil price. What a bunch of schmucks!

Meanwhile, the whipsawing continues…

WTI Jumps 5%, Tops $51 (Again)

http://www.zerohedge.com/news/2015-02-05/oil-collapse-over-again-wti-jumps-5-tops-51-again

Isn’t it fun?

Demand cannot be faked or printed. It’s either there or it is not. Right now? It is not.

The price of oil has a way to go before it hits bottom…

Now that gas has dropped below $3.00 in California, we still have a station that is selling gas above $4.00. Don’t know what to say about that business model.

Is that the station down the street from us?

Things are going to get worse before they get better.