Mortgages are hard to get, and inventories of homes for sale are low: Those have been the dominant reasons cited by the industry to rationalize the crummy home sales that have disappointed pundits for over a year. But now those memes have been debunked by homebuyers themselves.

Each real-estate data-gathering entity has its own methods, so results vary. But the direction has been consistent. Today, real-estate broker Redfin released the November data for the 41 or so major metro markets it serves across the US. The terrible numbers came with a conundrum:

With gas prices low and consumer confidence at the highest reported level in seven years, there was a lot to be cheery about heading into the holiday home-buying season. However, positive consumer sentiment did not translate into more real estate transactions last month as the number of homes sold plunged 21% in November versus October and was down 5% from this time last year.

Yet the median sale price rose by 6.2% year over year. It’s not jumping in the double-digits anymore, as in the two prior years, but it’s still rising, though sales are falling.

The National Association of Realtors, when it reported similar but not quite as dismal results before the holidays, offered its own conundrum: “Fewer people bought homes last month despite interest rates being at their lowest levels of the year.” It also blamed “stock market swings in October.” Which makes you wonder what’s going to happen to housing when an actual correction sets in, or a bear market or worse? And finally with a nod to reality, it admitted that “rising home values are causing more investors to retreat from the market.”

The NAR, a lobbying group, has been on the forefront of pushing Washington to bamboozle taxpayers ever deeper into subsidizing mortgage lending, and thus mortgage lenders, based on the premise that if nearly free money, guaranteed by the taxpayer, is made available, few questions asked, for mortgages that require nearly no down-payment, it would inflate home prices further and thus make agents more money, which would be good for homebuyers, and for the nation overall, or something.

So Fannie Mae and Freddie Mac caved. Earlier in December they unveiled mortgage programs with down-payments as low as 3%. It would put homeowners with nearly no skin in the game underwater at the slightest market downturn. It piles much more risk on lenders, and ultimately taxpayers, via the same sorts of shenanigans that contributed to the Financial Crisis.

The lobbying group was ecstatic. In its statement, it said, “NAR applauds Fannie and Freddie’s commitment to homeownership….”

It’s all part of “healing” the housing market by inflating home prices beyond the crazy levels of the prior bubble-peak, while putting the taxpayer on the hook again. It has worked so well that the market is now running into the same problem it had smacked into so catastrophically at the end of the prior housing bubble: despite super-low mortgage rates and increasingly loosey-goosey underwriting, home sales are tanking.

All year, we’ve been guessing that this was happening because people couldn’t afford the prices anymore or refused to pay them, and we’ve lined up data points and anecdotal evidence, and we’ve theorized about it. But now we heard it from the horse’s mouth: from homebuyers.

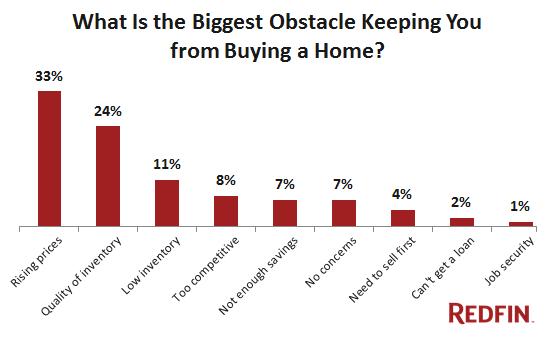

In Redfin’s Real-Time Buyer Survey of homebuyers, the biggest obstacle to buying a home wasn’t that a mortgage was hard to get or that there wasn’t enough inventory to choose from or that the stock market had a hiccup or whatever – but rising prices.

One-third (33%) of the respondents said that “affordability in the area I want to buy” was the biggest obstacle for them to buy a home.

And 24% griped about the quality – not the quantity – of inventory, which is another outgrowth of inflated prices. In the price range that a specific homebuyer can afford, there are suddenly only those homes that last year used to be in a much lower price range. Just to make a lateral move in financial terms, a homebuyer would have to step down a lot in terms of quality. But folks aren’t eager to step down and drastically lower their quality of life just because their incomes have stagnated while home prices have soared.

Those two categories combined accounted for 57% of what homebuyers considered the biggest obstacles to buying a home:

Low inventory – “not enough homes for sale,” – which the industry has held up as excuse all year, was seen as an obstacle by just 11% of the respondents. And here is the answer to Fannie Mae and Freddie Mac, and the army of lobbyists around them: only 2% – almost no one – complained that they couldn’t get a mortgage.

Redfin cites one of its brokers, who pointed at the same conundrum:

“If you can’t afford any of the homes for sale, it doesn’t matter how many homes are on the market,” said Leslie White, a Redfin agent in Washington, DC. “Despite the low interest rates, prices in DC are so high right now, many homebuyers feel priced out of the market. They’re being forced to decide between putting their home search on hold and renting another year, buying a significantly smaller home, or looking in neighborhoods farther away from the city.”

And if those hapless souls wait “another year,” and the housing market in DC continues to “heal,” they will be even further behind.

This rampant home-price inflation is the result of the Fed’s “bold actions.” The Fed has long prided itself in “healing” the housing market, along with inflating all manner of other assets, with its zero-interest-rate policy and by dousing Wall Street with newly created money. There is no limit anchored in reality how far stocks can be inflated. Irrational heights only encourage further buying, at least for a while. But housing is still subject to reality: inflating prices beyond the reach of homebuyers kills sales.

Sales in DC dropped 3.9% year over year, while the median sale price still edged up 2.6% to $360,000. Now imagine what a homebuyer faces in San Francisco where the median price, according to CoreLogic DataQuick, soared 27% year over year to hit an all-time record of $1,072,500. That might buy a 2-bedroom no-view apartment in a so-so area. Yet sales over the same period plunged 20%.

That was the moment when the prior bubble broke: exhausted buyers walked away while sellers continued to jack up their prices. And the whole kit and caboodle fell apart. Read… Housing Bubble 2: California November Home Sales Plunge to Multiyear Lows, Prices Soar

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Perceived value is a powerful motivator when making large purchases. The bottom lined is it has vanished in many markets, which explains the plunge in sales. Good analysis Wolf.

“…rising home values are causing more investors to retreat from the market.”

What? What??

“Home values”? How presumptuous. They must mean “home PRICES”…that’s what any twit who buys one now has to pay…

Hey, that’s the NAR. Give these folks a break. Their job is to make buyers feel better about having to pay a lot more for the same house. So a “high price” becomes a “high value” – and therefore worth it. They’ve developed their own jargon in their ceaseless efforts to produce housing propaganda.

Unless you have strong, consistent income from a W-2 or your own business, most people can not afford to own a home, even at zero mortgage interest.

For 30 years, I have been a landlord in a wealthy NJ commuter town to Wall Street. My properties are on the other side of the tracks and rented by blue collar workers. In 2014, I put on a full court press to upgrade all of my properties (and commensurately upgrade the rents). A totally upgraded 800 sq ft apartment with 3 beds and 2 full baths and 2 x off-street parking spots rents for $1,800 with the tenant paying all utilities. A couple with one child and two pets took occupancy in October. The husband and wife both work and have a combined pre-tax income of $100,000 per year. They have no down payment for a house – and – the husband’s income is mostly off-books.

In the general area, you can still buy a 70 year old, small house, in a decent neighborhood for $400,000. However, what all first-time homeowners have no clue about is the cost of maintenance and repairs. Today, I went to the hardware to pick up a replacement crank mechanism for a 30 year old, large wooden Anderson casement window in one of my rental bedrooms. $90.95 un-installed! Just for the metal crank, worm screw and arm.

Wolf writes about stepping down in quality. That is what I am driving at. The folks, who can barely pony up a 3% downpayment, can not handle an “unforeseeable” new roof rip-off job; new HVAC system; sewer line or water line replacement; wet basement remediation; etc. Handle that and lose one income – impossible. That is the reason why brand spanking new housing still sells – albeit, if they have good workmanship and materials.

I live in FL in an area with a large amount of corporate owned homes. These houses were in really bad shape when they were purchased out of foreclosure and just patched up for the rental market. These homes continue to be minimally maintained. Just enough to keep the rents coming in. The tenants are already paying high rents and have no incentive to invest in the properties. Overall these homes will hit a brick wall where they need major repairs to stay in the rental market or be sold. No one will be lining up to buy these well lived in houses.

In a seller’s market, the buyer gets fleeced…

So NAR is really fighting NAFTA and globalization in general. U.S. Bankers pushed NAFTA through to meet the threat of a unified Europe. It was all about seeing who could create the biggest economy. As a byproduct, global wage arbitrage is now preventing wages from rising and pushing many new jobs to emerging markets.

My employer sent 400 formerly good paying manufacturing jobs to Mexico. Additionally, we cannot hire domestically to replace retirees for white collar jobs. We are told to send the work to Mexico where my employer continues to invest and expand.

NAR is certainly out of touch with the issues facing middle class Americans. I refuse to wear their “I voted today” stickers which get distributed for free at the polling places each election. I encourage my fellow Americans to do the same.

Good call Owl!

Just want to let you Colonials know you are not alone in facing a crazed housing market.

My uncle recently started looking for a small country house for his retirement. Nothing fancy. Since I globetrot around Europe most of the year, I offered to look into home prices on some markets.

Spain is probably the worst basket case I’ve seen. We all know the excesses of their pre-2009 housing bubble: whole ghost towns built in the middle of nowhere, rampant speculation etc. Hence I expected prices to be at least in the realm of sanity as liquidation should be ongoing. I was dead wrong.

Despite an economic situation bordering on the dramatic, home prices are soaring to the highest level in six years. I did a bit of research since I could not conceive how this was possible and I found large PE firms have started probing the Spanish market for alternatives to the vastly overpriced US market, with the rationale of selling/renting vacation houses to wealthy foreigners, chiefly Germans and Britons.

In case someone doesn’t remember, this was exactly one of the main drivers behind the 2002-2008 Spanish housing bubble: vacation houses for foreigners. Starting in 2006-7 already, however, those foreigners drastically reduced their purchases for the same reason 33% of prospective US homeowners keep on renting instead: prices were simply too high.

Lesson not learned.

Fast forward to Italy. Prices are not in the same Bedlam level as Spain but are still outrageously high, especially in the North. This area went through a housing bubble as well which, unbelievably, is still ongoing: cranes and bulldozers are still hard at work, often right next to rows upon rows of unsold houses and deserted shopping malls.

The rationale here is a tad different than in Spain: to counter the massive decline in manufacturing, a decline they largely brought upon themselves, Italians went on a building craze, and are still living in a fantasy world were a house is still a blank check. Every dirty trick in the book has gone into desperately fighting the inevitable price decrease that goes hand in hand with a massive glut in supply coupled with declining real wages and soaring unemployment.

And finally we get to France. I limited myself to searches in areas I know well (PACA, Lozere etc) but I was pleasantly surprised to find prices seem in the realm of sanity, at least for the time being. Local legislation isn’t very amenable to large PE firms and the depopulation of rural areas is still ongoing: steer clear of Paris, Lyon, Toulouse etc and you can still grab a good deal.

Most of all, it seems French, differently from their Southern neighbors, still see housing for what it is and not a magical recipe to prospertity.

Happy New Year to all and thanks to Wolf Richter for his hard work!

3% down pmnt. won’t work to stimulate sales this time around since this cohort will have low credit scores and require higher interest rates. Waste of effort here.

Basic economics still applies – even after all the interventions and malinvestment in the housing sector – in that house price of approx. 2.5x avg. income for traditional buyers and or about 7% cap. rates for investors are the rule over the long term. It’s the same sad story of speculators driving up prices until the above two criteria are breached. Fundamentals still matter. Here’s the process: 1) gov’t/Fed interventions/machinations to attempt to help banks recover bad investment/loan losses due to their own speculation – in this case US RRE mkt./asset class. See FASB rule 157 where mark-to-market rules are suspended and mark-to-myth accounting now applies. 2) Speculators jump in to take advantage of skewed conditions via malinvestment. 3) Asset prices rise. 4) Speculators exit, or attempt to exit. 5) Main St. is either priced out of mkt., or left holding the bag – or both. 6) Rinse and repeat. This time around the banks have so completely eviscerated the economy that the first time buyer cohort is now living in parent’s basement and unable to consider buying. Most others priced out as well except high end, which will not save the mkt.

Humpty Dumpty sat on a wall,

Humpty Dumpty had a great fall.

All the King’s horses, And all the King’s men

Couldn’t put Humpty together again!

At this point in the US RRE cycle (i.e. post-bubble) the next step is mean reversion and prices should – after a few years of ineffective interventions – return to the long-term average. This is a slow, uneven process since housing is an illiquid asset and markets are local. The Spring ’15 season should be telling.

I am rather suprised that the employment security response in the survey was only 1%. I concur with Owl, my company is off shoring as fast as possible. I look forward to the two layoffs per year that have been the norm now for about 5 years.

Ah, but there’s a big elephant in the room called… The FED. What, you were expecting someone else? The FED can set up a Private Equity and start buying houses. It will take a couple of years before the game is detected.

true story – friend of mine contracted to buy a house.

I said, that will never work you have no money in the bank

and a 20,000 credit card bill.

Her mother gave her the 5 % downpayment

she got 95 % financing

and

if you can believe it, she did not have to pay off the credit card, they said

she could afford to make the minimum payments (forever I guess that would be)

and afford the home.

Boy did I look stupid.

Point. Anything goes is still the story.

another true story. I am a bit in the real estate business.

Friend wanted to sell the house, no buyers.

House in bad shape, friend had no job. No regular employment.

Friend said I will get a reverse mortgage.

They gave him (quite to my surprise) the reverse mortgage at an

amazing amount (more than property would ever sell for in my

opinion).

As far as I can tell, He has no plans to do any maintenance; he has no money to do any maintenance, even basic maintenance like having the lawn cut.

When they take that house back, If I had to guess, it will be worth

1/2 of what they gave him for the reverse mortgage. Because I do

not think he will ever do a new kitchen, bathroom, roof, or any

basic maintenance.

Reverse mortgage will be the next taxpayer bailout.

I would be 80 % of those getting a reverse mortgage live month

to month on the draw and have not a penny to put into needed

maintenance must less typical upgrades as say your kitchen is now 20 years old.

Please do not forget the education racket. Student loans!