The death of the dollar – as much as some folks were ready for it – didn’t occur in 2014. OK, there are a few days left, but you get the idea. Instead, the dollar has been hot.

It rose against a large number of currencies. Some of them, such as the Russian ruble, have plunged for reasons of their own and have engendered desperate efforts to stem the decline. Other countries, like Japan, have gone all out to demolish their currencies. Escalating the currency war is frowned upon. So Japan found more acceptable names for it and redoubled its efforts. And the ECB has been passionately talking down the euro, but has done relatively little by central-bank standards to actually water it down.

Central banks tried to dominate the currency markets, but currency markets are an unruly crowd that can’t be easily cowed. In sovereign bond markets, central banks rule with an iron fist by imposing zero or even negative rates and buying up sovereign bonds, or promising to do so, with money of which they can create an unlimited amount. These “bold actions” inflated valuations and pushed down yields to grotesque levels, such as the crappy 10-year Japanese Government Bond yielding 0.32%.

That kind of control eludes central banks in the currency markets. They’re doing a superb job devaluing a currency, but bringing it back up after it begins to spiral out of control is hard. It requires resources that a central bank can’t print. It requires interest rates so high that they might strangle the economy. It requires other expensive, painful, or even impossible measures. And so more often than not, that noble fiat currency just goes to heck. We’ve seen plenty of it in 2014.

In this environment, how fast and how far will the dollar continue to rise in 2015?

“Whenever a consensus is so unanimous, our gut tells us it is wrong,” BlackRock, the largest asset manager in the world, explained in its 2015 Investment Outlook. “Stretched positioning means even a mild disappointment to dollar bulls could prompt a sell-off in the currency.”

That “consensus” that the dollar will strengthen is based on the end of the Fed’s QE, shrinking trade deficits due to rising oil production in the US and dropping oil imports. The consensus also relies on more demand for dollars as the Fed is threatening to raise interest rates in 2015, at a time when the Bank of Japan is madly printing money and pushing yields to new lows; and when the ECB is promising outright purchases of sovereign bonds on a massive scale.

And true, BlackRock says, that increasing rate differential is going to create demand for dollar assets. But that “bullish dollar view is reflected in futures markets positioning. Trades against the euro look especially crowded, with short positioning almost three standard deviations from the mean.”

Then there’s the “malign path” to a higher dollar: a global economic slowdown that would trigger “safe-haven buying.”

Either way, the consequences of a higher dollar can be brutal in the Emerging Markets, where the hot money gathers. As dollar assets in the US become more attractive and as rates rise, that hot money simply evaporates from the Emerging Markets, and “funding sources dry up.”

This triggers a chain reaction. To prevent its currency from going to heck, the central bank ends up selling its foreign exchange reserves and buying the local currency. This “tightens domestic financial conditions,” just when the ballooning issuance of US-dollar corporate debt in EM countries to lock in lower interest rates – see Russia – has created “pockets of vulnerability.” To attract liquidity, EM countries raise rates. But these rates trigger “slowdowns and currency gyrations.” Major crises have been the result.

And speculators can muck up the scenario: short-term fluctuations in currencies are often the result of “flows and investor sentiment – which both can turn on a rupee.”

But is the dollar rise a sure thing? BlackRock hedges its bets: “Forecasting currency movements has created many orphans.”

The problem: these stubborn currencies don’t always play along. Turns out over periods of five years or more, currencies tend to behave in line with fundamentals, such as interest rate differentials and various central bank machinations. But not in the short or medium term.

“Getting the direction right is one thing; getting the timing right is another,” BlackRock says. Appreciation cycles in the trade-weighted US dollar tend to last about six to seven years. But here is the problem: “Expect air pockets along the way.”

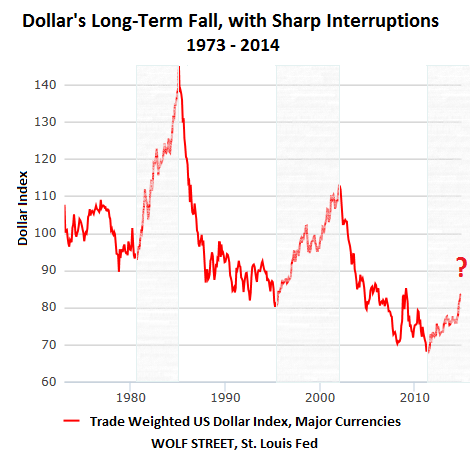

The Fed has engineered the long-term destruction of the dollar that exceeds even that of the currencies in the US Dollar Index, as the chart going back to 1973 shows. But there have been two periods when the dollar soared for years (shaded areas). BlackRock supposes that we’re now in the third such period (shaded area on the right). But mind the “air pockets.” For example, from August 1998 to October 1999, in the middle of the last appreciation cycle, the dollar fell 7% against the currencies in the index:

So the stronger dollar might remain elusive in 2015. There are reasons beyond the fact that the trade is too crowded. BlackRock cites the “Pavlovian tendencies” of the markets that have been “conditioned to wait for monetary policy to dictate market moves.” They might hold their fire until the Fed gives the go-ahead. In this case, “the US dollar will only take off when Fed Chair Janet Yellen fires off her first rate hike.”

That might not happen. Instead, the Fed might refuse to raise rates because of “growth disappointment (it has happened before).” And then, there is “an even worse scenario for dollar bulls: US economic momentum stalls, leading to expectations for a fourth round of QE.”

That might cause the dollar to return to its norm and sag once again. As the above chart shows, it’s unrewarding to be a dollar bull long-term. The dollar has been slated for destruction, but the Fed wants to accomplish this over many years, rather than all at once. And only occasionally do things get out of hand, and the dollar rallies for a few years – enough to infuse a lot of false confidence.

On the surface, BlackRock is in a bullish mood and is gung-ho about the US economy. Beneath the surface of its 2015 Investment Outlook, there are dire warnings, including of “financial instability,” a euphemism for “crash.” Read… How Asset Manager BlackRock Gave Me the Willies About 2015

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

China and Russia are both in trouble. What happen when one or the other (or both) start dumping Treasuries to buy gold?

“China and Russia are both in trouble.” ??

Only because they hold US debt.

Here’s what I see for 2015:

TPTB will continue to do ‘whatever it takes’ to discredit gold as a measure of monetary reality.

The world economy remains weak, weighed down by mountains of unpayable debt.

Interest rates stay low, perhaps falling further, to avoid the need to restructure unpayable sovereign debt.

JPY, EUR and CAD remain weak, giving USD the illusion of continued strength.

Does a black swan take flight, finally bringing down the financial house of cards and plunging the world into the depression that has merely been postponed since 2009? I don’t know.

The global economy is extremely over leveraged both long and short term, making it vulnerable to black swans that could take everything down.

But unless such a massive black swan event happens, it looks like clear sailing for the US dollar and the US economy.

Thanks to Cold War 2, declared by Washington against Moscow and Beijing, both are going to continue to be restructuring their economies leaving weak commodity markets globally.

The EU is going nowhere. They can kick the can down the road but it is a dead end street. The Euro is now in a secular bear market, even if it has a pop because Berlin green lights Draghi to print a few trillion more and hand it to the banks.

The collateral Draghi will take will be worthless in any black swan event, questioning who indeed is going to back stop trillions in ECB debt? And the more Draghi prints of debt money, the richer the bankers and elites will get, at the expense of ordinary Europeans and their fading social institutions.

The Americans will continue to make trouble in the MENA.

The US will continue to be the place of refuge for international capital.

Meanwhile inside the US Big Business will be in a near perfect environment. The Democratic Party is now the Republican Party lite. Workers have the lowest wage base in the first world, no political representation in sight with a massive pool of sidelined excess labor.

Commodity prices will remain low. Interest rates will remain low, as will inflation.

The US now has endless energy and now that Big Money has finished destroying the union movement, it is bringing production home to automated factories with embedded 3d printing.

Real profits will remain exceptional. Costs will remain low.

Outside of black swans, the only negative might be how much a demolished middle class can continue to fuel internal growth? And with the rest of the planet heading towards recession, how much can exports help take up the slack, especially in a rising currency?

The results, slow US growth amid global deflationary forces lapping at its shores. Forget any Fed tightening. And the continuation of pressure on US and world labor markets. Good times for a few capitalists. Bad times for the rest.

Henry Ford wants to ask you something: now that these US corporatists have driven wages so low, who will be the consumers of these 3 D factories goods you are crowing about?

You asked Farang; “now that these US corporatists have driven wages so low, who will be the consumers of these 3 D factories goods you are crowing about?”

If you read my post carefully, I wrote; “Outside of black swans, the only negative might be how much a demolished middle class can continue to fuel internal growth?”

This is perhaps the main bear argument and has a lot of the world’s super rich, the .0001% nervous. It is why Christine Lagarde of the IMF, who represents these people has been lecturing the Americans to raise wages.

And as I went on to say in my original post “And with the rest of the planet heading towards recession, how much can exports help take up the slack, especially in a rising currency?”

So indeed Farang we will have to wait and see.

EMs need dollars to repay debt -> demand for dollars.

US economy is the leper with the most fingers -> dollar safe haven.

US bond market is the largest and most liquid in the world -> where else can proceeds from large amounts of liquidated assets be parked? JGBs? Dim Sum bonds? German 10-year Bunds at 0.5%?

Dollar bull.

Good points all. And when the sovereign defaults start it will drive even more to the dollar.

I am no Chartist, but it looks to me like a long-term US dollar decline, not an indication of any long-term strength. Just draw a line from peak to peak, it is a marked decline.

I’m not a chartist either but many currency traders are and there’s a lot of talk about the dollar breaking out of a long term wedge pattern. To me it looks like a tiny blip crossing over to the upside – not much more than noise. But the guys who bid on these things rely on charts quite a bit.

If you know anyone in the shipping business ask them how sailors want to be paid. Dollars. They wait until they make port in the US to get paid and then they want fresh crisp currency. It’s delivered to the dock by armored truck with guards carrying rifles.

When the sailors start asking for yen, euros, yuan or rubles I’d start to worry about dollar supremacy.