High-Yield Bond Funds, Loan Funds Hit by “Market Conditions”

The phenomenal Fed-triggered feeding frenzy in stocks on Wednesday and Thursday was paralleled in the junk-bond market. Energy related junk bonds had gotten shredded over the past couple of months, as the price of oil has collapsed. The sell-off started spilling over to non-energy junk bonds. Tuesday, the day before the Fed’s announcement, junk bonds suffered their largest drop since October 2011. And just as all heck was breaking loose, and as yields were getting painfully high for our spoiled zero-interest-rate conditions, the Fed rode to the rescue once again to bail out the markets with its vague verbiage about being “patient.”

The markets interpreted this to mean whatever they wanted to: The stock market thought rates would stay at zero forever, sending stocks into a frenzy. The Treasury market thought rates would rise sooner than expected, sending 10-year Treasuries into a rout. And the junk-bond market had its own interpretation, in line with stocks, not Treasuries, unleashing the sharpest rally since August 16, 2011. It more than filled the hole left behind by Tuesday’s massacre and allowed junk bonds to end the week with a gain. Halleluiah, thank you Fed.

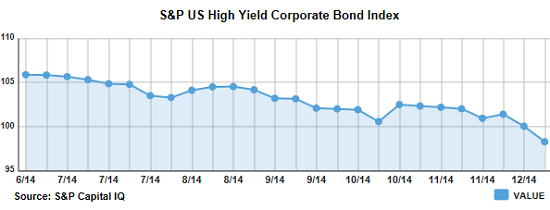

OK, it wasn’t enough. Over the two-week period, the average remains 157 basis points in the hole. And it’s down 536 basis points for the year. This chart of S&P’s High-Yield Corporate Bond Index, via LCD, goes back to the peak of the junk-bond bubble in June. Since then, junk bond values have dropped nearly 8%.

Investors have started to vote with their feet. All kinds of institutional investors hold junk bonds, but retail investors – the “dumb money” – hold them in their bond mutual funds or ETFs, often unaware that their bond fund is goosing its yield with junk. And until June, junk bonds were a great deal.

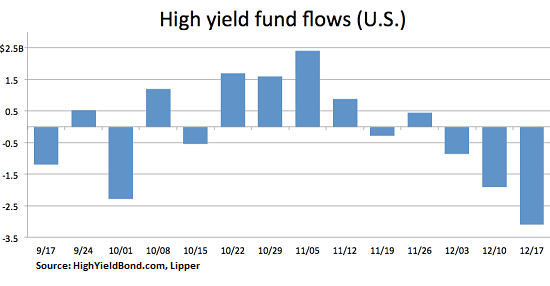

But for the week just ended, retail-cash outflows from junk-bond funds jumped to $3.1 billion, LCD reported. It was the third outflow in a row, and the second-worst outflow in 2014. With outflows of $5.8 billion over the last three weeks, junk-bond funds experienced net outflows of $5 billion for the year:

Junk-bond fund assets were also hit by “market conditions” that ate up 1.4% of total assets during the week ended December 17. But the breath-taking I-love-you-Fed rally on December 18 wiped away the tears from that week, for now.

Then there are leveraged loans, the ugly sisters of junk bonds. They’re bank loans to junk-rated over-indebted corporations. Banks can retain these loans, sell them to institutional investors, such as loan mutual funds, or repackage them into Collateralized Loan Obligations and then sell those. CLOs should have “Financial Crisis Material” stamped all over them [read… Treasury Warns Congress (and Investors): This Financial Creature Could Sink the System].

Last year, a record $606.7 billion in leveraged loans were issued. This year started out white-hot too. But then retail investors began pulling their money out of leveraged-loan funds. Tremors went through the market, and issuance plunged to $529.5 billion for the full year.

For the week ended December 17, retail investors pulled $1.8 billion out of leveraged-loan funds, S&P Capital IQ reported. It was the worst outflow since the week ended August 17, 2011, when fretting over a double-dip recession in the US and the debt crisis in the Eurozone hung over investors. And “market conditions” ate up another $1.2 billion during the week.

It was the 23rd cash outflow in a row, and the 34th in 36 weeks. For the year, outflows amounted to $14.9 billion, but that includes the period January through March when leveraged-loan funds were still ballooning. Over the same period last year, inflows reached an exuberant $51.6 billion.

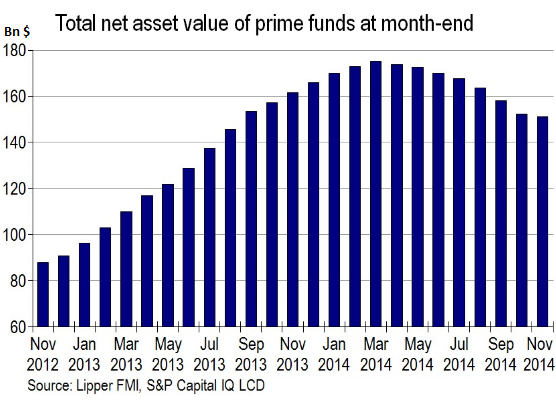

This two-year chart by S&P Capital IQ/LCD shows the monthly totals through November (it doesn’t include the outflows in December) in leveraged loan funds: a magnificent bubble that nearly doubled in 17 months, to peak in March 2014 at $175.1 billion, after which the dumb money began bailing out. By the end of November, it was down $24.1 billion from its peak, not including the outflows so far in December.

As retail investors got out, mutual funds’ share of total leveraged loans dropped to 21.8% this year, from 31.5% in 2013, according to S&P Capital IQ/LCD. Banks, under pressure from regulators, decreased their share to 6.2% from 6.5%. But hedge funds increased their share to 9.8% from 8.8% last year. And the share of leveraged loans packaged into CLOs jumped to 62.2% from 53.2%.

Junk bonds and leveraged loans performed miracles over the past few years. Companies with low credit ratings and too much debt were able to issue even more debt that, thanks to the Fed’s machinations, cost them very little and didn’t reward investors for the risk they were taking on. Some of this money funded the fracking boom in the US. But now that the price of oil has plunged 45% in six months, this debt is becoming precarious. And retail investors’ loss of appetite for it and their determination to let someone else eat the potential losses appear to be, for once, impeccably timed.

June was the peak for a lot of things beyond oil and junk debt, including service and manufacturing activities, as measured by the Purchasing Managers’ Index. And it has been one heck of a downhill ride since, culminating in a December dive. But this time, there is no polar vortex to blame. Read… Already Crummy US Economy Takes a Sudden Hit

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Hi Wolf,

Some months ago I promised I would keep you apprised of my junk bond saga. As you may recall, back in August I tried to liquidate a junk bond holding. The bond had been trading in the low 80s in early May, and had fallen to the low 40s in early August. At the time I first tried to liquidate it in August, the bid request came back ‘no response’ (i.e., no bid).

This morning, Friday December 19, I successfully liquidated that block of 10 junk bonds for 12.25, or $1,225 for bonds with a par value of $10,000. Since these bonds have a 90%+ chance of default at this point, the dealer quote excluded the accrued interest of approximately $133 which I normally would have received in addition to the $1,225 for the bonds.

Those who believe that today’s lofty stock market valuations are realistic or sustainable are likely to have their heads handed to them, perhaps sooner rather than later. Despite the hype associated with continued zero interest rates (ZIRP), the Federal Reserve cannot print revenues or earnings for publicly traded corporations. The facts are that (1) Fed money-printing (aka ‘QE’) has been a complete failure in terms of reviving the economy, and (2) the continuation of zero interest rates is indicative of a sick economy, not a healthy economy. In short, the assertion that the US economy is ‘healthy’ in any way, shape or form is a brazen lie.

I noted today that, after spiking about 10 basis points in total on Wednesday and Thursday in response to the latest Fed blather, 10-year and 30-year Treasury rates have resumed their decline, falling 2 and 4 basis points respectively today (Friday 12/19).

David Stockman, Reagan’s former Budget Director, has written that stocks have now entered a ‘delirium’ phase. I think Stockman is right. Even though they think I’m crazy, I expect equity investors will experience a haircut on the order of 60 to 70%, exceeding the 2008-2009 peak-to-trough decline of around 55%. This is because I think the amplitude of the Fed’s serial bubble-blowing activities will continue to increase with each successive bubble, until Fed policies finally succeed in destroying what is left of the US economy.

Best regards,

VegasBob

Thanks, VegasBob for the update on your junk bond saga. Can you name the company? If you don’t want to do it publicly, can you let me know via email?

Bob, you’re clearly very informed on what’s really going on, so what would possess you to invest 10k in junk bonds?

Sorry to hear of your loss, but sounds like a self – inflicted wound to me.