Homebuilder KB Homes, when it reported earnings for the quarter ended August 31, revealed that the average price of the homes it sold rose 9% to $327,000. In the West, prices jumped by 20% to $579,700. With these juicy price increases, sales in dollars were up 7% from a year ago. But the number of homes it sold actually declined by 2%. That’s how the housing market in America operates these days – even at the high end that KB Homes serves.

At the same moment, the Commerce Department reported that new home sales suddenly jumped by 18% in August from July, and a breath-taking 33% from August last year, after having been in the doldrums or declining for months. But the margin of errors are elephantine (±16.3% and ±21.7% respectively), so a grain of salt comes in handy.

With such an enormous jump in sales, if it doesn’t get revised back down next month, you’d think that inventories of homes for sale would have been drawn down during the month. On the surface, that happened: supply dropped from 6 months to 4.8 months. But…

The actual inventory of new homes still for sale at the end of August, despite the burst in sales, rose 2% to 206,000, from July’s 202,000 – and was up 16% from August a year ago. August and July were the only two months in the 12-month period when inventory was over 200,000 new homes. Among these homes, the inventory of “completed” homes – rather than “not started” and “under construction” – jumped 23%. These homes, despite the presumed spurt in sales, are stacking up!

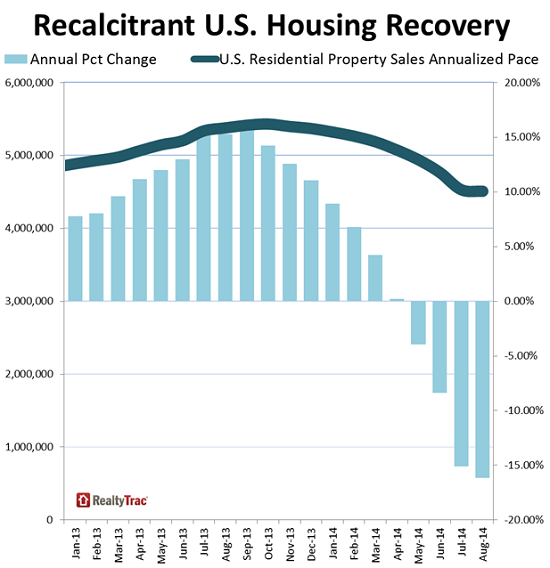

Now RealtyTrac found that sales of all residential properties – single family homes, condominiums, and townhomes – in August dropped 0.5% from the already dismally low level of July to an estimated annual pace of just over 4.5 million. Year over year, a 16% plunge!

Until mid-2013, the annual rate had been rising toward 5.5 million homes. Investors had been scouring the hottest markets, buying up homes by the thousands, and driving up prices in the process. But they succeeded so well in driving up prices that their equation wasn’t working anymore. And they walked. What was left was a toxic mix.

Mid-2013, everyone thought the housing market was once again entering the paradise of eternally rising prices and sales. But in the fall, the hot air started hissing out of it. Sales spiraled down, amidst a slew of now industry excuses.

This chart shows the change of the annual rate of sales every month, starting January last year (fat line, left scale). Note how beautifully it rose toward 5.5 million homes in mid-2013. Then investors began to bail out. The light blue bars (right scale) indicate the year-over-year percentage changes in the annual rate of sales, which has plummeted relentlessly over the last 12 months:

But here is the miracle: Despite plunging sales, the median price rose 3% from July to $195,000 – the highest since August 2008 – and was up 15% from a year ago. These soaring prices are hurtling along on the same time-honored collision course with plunging sales. In the past, that type of race ended in a crash.

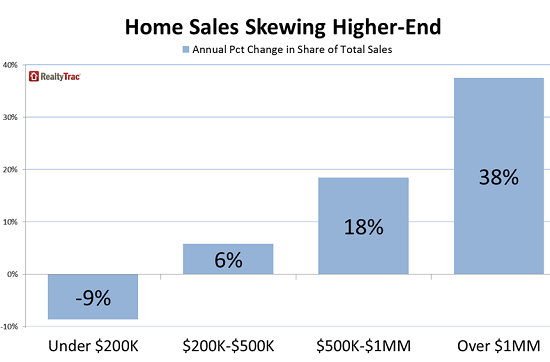

And there is a Fed-induced twist to just about everything in this economic “recovery”: the higher end, where the beneficiaries of the Fed’s “wealth effect” operate, is doing well, while the bottom is falling out at the lower half: The share of sales in the price range below $200,000 dropped 9% year over year. With the median sale price at $195,000, over half of the homes sold were in this miserable category.

But the categories above $200,000 gained in share. Homes over $1 million saw their share explode by 38% year over year – even as the total home sales pie shrank by 16%!

This chart shows how the overall sales pie is split up, with the lower half of the housing market in terrible shape, while at the expensive end, the Fed’s “wealth effect” has kicked in nicely. The problem? The number of people who can afford a $1 million home is minuscule.

The housing market has become Exhibit A of what happens when the Fed is trying to engineer a “recovery” by dousing Wall Street with free money that then needs a place to go. It went everywhere, and in late 2011, it found fertile grounds in the American Dream. The middle class had no chance against the hundreds of billions of dollars that suddenly poured in. Now it’s largely priced out of the market.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

One part that supports economic recovery is the ability of the workforce to migrate to locations with better growth and jobs. The previous housing bubble crash took that ability away from a large portion of the workforce (I saw this first hand trying to recruit people from across the US to come to high paying tech jobs on the west coast – they couldn’t afford to move due to the drop in their home values).

The complication now is that a housing crash will restrict the mobility of the workforce, just as the overall economy slows, which leads to even more difficulty in recovering. The more one looks into the details the more trouble is found.

Don’t forget most of those home sales were 30-50% over valued!

I sold my house last may 22nd for a whopping 1.250 cash!

Yup the house I bought in 09 for 750 was sold for 1.250 mill!

I wished lots a luck to the new owners.

Most of south Florida is now in the under 200K category. Even when homes are listed at higher selling prices you know the value is just not there. Most families don’t have the income to buy or lack the credit score to qualify. These are problems that will require decades to overcome. Rental houses are expensive but they will not be sell-able, for good prices, in the future because they are not being kept up by the landlords which are only stripping value. Overall I think home ownership is dead for the average person for a long time to come.

Mobility in the job market is also a big issue for almost everyone.

The Census Bureau numbers were completely bogus. I’d love to have a peak at their “seasonal adjustment’s” model.

The homebuilders are going to start reporting numbers that are far worse than expected and shorting them right now is easier than shooting fish in a barrel:

http://investmentresearchdynamics.com/homebuilders-look-out-below/

Well, I continue to find myself nodding in agreement with everything you write about the housing market. What I’ve been see on the “front lines” of the market definitely supports what you are saying. I can’t speak about other markets but the DC market – a longtime darling of the real estate industry for it’s “recession proof” reputation – has cracks in the facade as well.

On Investors: The true investors who know what they’re doing, who live and breathe this every day, were quietly buying up properties here in DC in 2009-2012 and prepping for a turnaround. They made the most money by flipping. They buy off-market, going door to door and offering people who own their homes outright but have no cash on hand a “nice sum” of $250,000 cash to get out. They renovate the house, putting in $100,000 and flip for $600,000. This was going on throughout 2012 and 2013.

When the straggler investors arrive, and you get calls from everyone and their mother who watch HGTV, see “Property Brothers” and think they can do this too – that’s when you know that it’s done, flipping has effective “jumped the shark.” Or when you get calls from investors in other cities, who don’t realize how it works in this market – that you can’t just toss renters out on their ear – that’s a sign that the tide has turned. Because inevitably by the time the rest of the world knows that investors were making 60% profits flipping houses, everything else has self-corrected to remove such a profit margin from reality. Sellers aren’t foolish enough to part with their only asset for $250,000 cash when should have received much more. So the real investors leave and the wanna-be investors arrive and they just can’t make those numbers work.

Sellers: Many sellers in DC are pretty stubborn, still maintaining the fantasy that their house is worth 10% than it was last year. Pretty much what you said in your 9/12/14 article on Millennials is spot on: “Sellers are the last to accept the trends as they cling by their fingernails to some notional value of their home and to the tens or hundreds of thousands of dollars in wealth that they thought they already had in their pocket, only to see them evaporate.”

Buyers: Buyers who are still in the market right now are holdovers from spring or even last year and they have a higher bar than many who went before them to the settlement table. (Some agents might call them “picky.”) The buyers now don’t want to fix up, they don’t want to renovate, and they won’t overpay or get involved in a foolish bidding war. Anyone who was willing to toss money (their own unearned equity!) at an overvalued home just for the purpose of buying while “rates were at all time lows” might be left holding the bag. Unless they walk away – as many did who purchased in the previous run-up in prices.

Have you seen the Joshua Pollard letter? http://www.joshuapollard.info/

Love your take on the market. No rose colored glasses on this site!

Melissa, I just posted your comment on the front page, right column so that more readers get to look at it. Thanks!

Here it is: https://wolfstreet.com/2014/09/26/the-recession-proof-housing-market-in-dc/

Wolf,

You write some awesome articles! The flippers are going to get slaughtered and even more DA’s (dumb @sses) are going to find themselves severely underwater when this FED inducing bubble blows shortly…

Thanks for the kind words, Mike.

Inflating stocks via QE and ZIRP causes its own problems, but inflating home values that way has the insidious side effect of making it too difficult for many folks to get a decent roof over their head. Yellen should take a good look at that.

The “flipper” shows are back on late night infomercials, again. That schmuck from A&E’s “Flip this house” has his own infomercial. BUT WAIT! THERE’S MORE. Some woman is also touting the great money to be made in “flipping”. Why it’s so simple a chimpanzee can do it. We are doomed.

And did any one of the “geniuses” that told us that home prices were “rising”. Did you even look at the basic costs of material and labor, especially any material made from crude oil and steel, which is up fourfold and subtracting that from your home “prices” Hmm? Anyone? Bueller?