With home prices rising for three years in much of the country, and soaring at dizzying rates in a number of metro areas, the inevitable is happening: sales stalled. But prices have continued to rise, even as sales have deteriorated further. Something has to give. And it’s not going to be maxed-out American consumers. They’re not going to all suddenly inherit enough money to buy these mid-range homes that have moved beyond reach.

But something else is happening.

In the Las Vegas-Paradise metro area, one of the epicenters of the former housing bubble, and one of the epicenters of Housing Bubble 2, the ratio of homes sold to absentee buyers (mostly investors) as a percent of total sales in July plunged by a quarter year-over-year, according to DQNews, a division of CoreLogic. The ratio of homes sold to cash buyers plunged by a third. The ratio of homes flipped swooned. Total home sales have dropped year-over-year for the past 10 months; in July, they were down 11.8% to 4,260 units, the lowest for any July since crisis-year 2008.

And the median price? $190,000, up 9.6% year-over-year. The highest since November 2008. It has now booked 28 months in a row of year-over-year gains that reached up to 36.5%. Crazy! But July was the first month in two years with “only” a single-digit gain.

These price increases have moved homes up the price ladder across the board, and potential buyers looking at the lower end found their American dreams evaporate: the number of homes that sold for less than $100k plunged 32%; the number of homes that sold for less than 200k plunged 21%; but the number of homes selling for over $500k rose 11%.

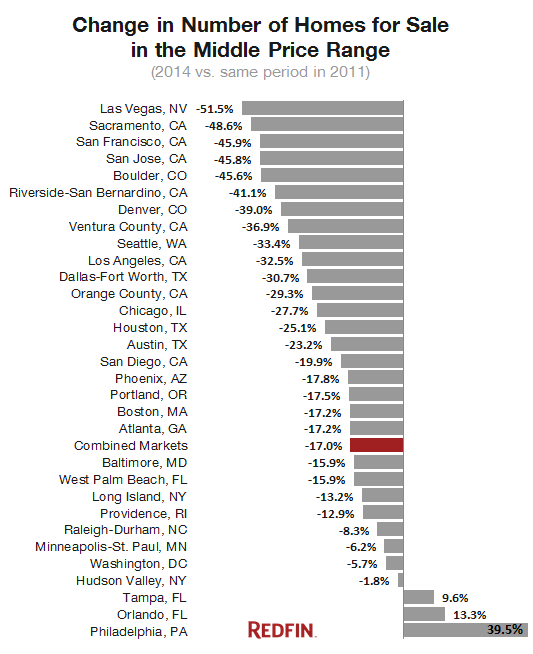

And not just in Las Vegas. So Redfin, an online broker represented in the major markets across the country, analyzed what happened to the crucial “middle price range” of homes for sale where most buyers are looking. In July 2011, that range was $130k to $375k. But by July 2014, the number of homes for sale in that range had dropped 17%. The number of homes priced below $130k had plummeted 50% from 2011. But the number of homes priced above $375k jumped 16%.

“The issue seems to be that a lot of what’s on the market is overpriced, and buyers are feeling uncertain about whether it’s a good time to buy,” explained a Redfin broker in Phoenix.

In Las Vegas, the number of homes for sale in the middle range ($77k to $177k in 2011) plunged by 51.5%; same thing in Sacramento, down 48.6%. As prices have soared over those three years, that “middle range” has moved up-market – and increasingly out of reach of the middle-range buyer whose real income has stagnated.

This chart shows to what extent the problem has spread across the country:

On the other hand, the number of homes for sale toward the more expensive end has skyrocketed from 2011: by 69% in Phoenix for homes over $270k, by 67% in Philadelphia for homes over $365k, by 51% in Riverside for homes over $475k. (here is the list)

And the middle price range of homes for sale has gone ballistic: Across Redfin’s markets nationally, it soared 37% to range between $155k and $429k. Only Philadelphia saw a slight decline of 3.2%. In Phoenix, it was up 77% ($160k to $399k); in Sacramento up 76% ($235k to $532k); in Las Vegas up 66% ($130k to $297k); and in the San Francisco metro area up 63% ($650k to 1,695k … yup, $1.7 million, which causes some rational people to scratch their heads).

What gives, as incomes of prospective home buyers haven’t budged?

Home sales across the country have declined steeply. In the nine-county San Francisco Bay Area, in July, home sales dropped 9% year over year. In San Francisco itself, they plunged 24%. Anecdotal evidence: in June, two homes went up for sale on my block where nothing had gone up for sale since 2011. In August, one of them finally sold. The other one still hasn’t sold. It’s tough out there, at these insane prices.

Sales have also been eviscerated in San Diego, Phoenix, Washington, D.C., and other cities where, as Redfin noted, “price growth has been the strongest.” This is the wall, and home prices have run into it. Even buy-to-rent investors and home flippers are bailing out because their business models no longer work at these inflated prices. Who’s going to pick up the slack? The student-loan debt-slave first-time buyer? Hardly.

What will happen to prices? In July, sellers got nervous, and started to lower their listing prices: in Denver 38% of the homes for sale had their prices lowered; in Ventura County, CA, 35%; in Sacramento 34%. Across the nation, 24%. Bidding wars are history. The price pressure is on. And home flippers are see that the magic mix has become toxic. Read… Home-Flipping Collapses in San Francisco, Losses Spread

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Ah yes . My beloved home of Philadelphia where they are building 2 million dollar Condos at Broad and Walnut in Center City in hopes that people will buy them.

I love Philly but the prices are shocking considering that the pay scale is not high there. Maybe its all the people escaping from NJ where wages are higher and so are the taxes.

We just moved from San Jose to Vegas, primarily to escape insane Bay Area housing prices.

We are in escrow for a 2000 sq ft house here at a price less than half of what a 14000 sq ft condo costs in San Jose. Vegas prices may have risen some, and there were multiple bids, however comparatively, Vegas is still a huge bargain.

Yeah, Las Vegas will be a great bargain when the entire metro area runs out of water and you are only allowed to take 3 showers a week. What will happen to your “bargain” home value then?

The Southern Nevada Water Authority says they have enough water stockpiled across the state to last 50 years. Las Vegas itself recycles and reuses all indoor water, including toilet water. It is purified, pumped back into Lake Mead, and reused over and over again.

I follow water issues closely and have lived in multiple cities in California. Nevada is so far ahead of California in reusing water that’s it’s comical. Seriously. California just decided maybe they should regulate groundwater pumping, something all other Western states have done for years.

SNWA chief:

” “We have a secure and sound water portfolio” for the next 50 years at least — one that will allow the community to grow responsibly while living within its comparatively small share of the Colorado River.

As far as Entsminger is concerned, water is not a limiting factor for growth in the Las Vegas Valley.

The reason lies in the community’s unique ability to recycle virtually all of the water it uses indoors. Whatever runs down the drain or gets flushed down the toilet is treated and returned to Lake Mead, where it earns so-called “return-flow credits” that allow the water to be pumped from the lake and used again.

As a result, it’s possible for the valley to add efficient new homes with minimal landscaping and “almost zero water footprints,” Entsminger said. “We can grow in this community — diversify our economy in this community — while using less water”

http://www.reviewjournal.com/news/water-environment/water-official-vegas-not-running-dry

I heard similar stories when I lived in AZ about developers claiming a “100 year” water supply. I would like to see the assumptions that went into your 50-year Las Vegas water supply estimates in terms of annual rainfall and population growth. I suspect the “50 year” water supply is just developer BS. They won’t be around in 50 years and don’t really care what happens after they sell the house.

Also, I’ve been reading stores recently about how the level of Lake Mead is so low it is almost below the level of the pipeline that takes water to Las Vegas. So, how does that story jibe with your 50-year, recycling water through Lake Mead story?

Thanks for the article, but it states “Even if the situation worsens at Lake Mead, the authority has socked away enough water to sustain the community for five full years.” They are planning ahead 50 years, but they really only have water to last us for five years.

I live in Las Vegas myself, and there is a huge risk here. If rainfall was like playing roulette or blackjack, then a 15 year drought would be like a losing streak in which you keep losing 15 times in a row with only one or two wins in between. Statistically, such losing streaks are to be expected, and they are nothing to worry about because over the long term, you’ll make up for it with winning streaks. It’ll average out.

Unfortunately, climate is trickier. We can easily have the drought continue for another 25 years and it wouldn’t be anything out of the ordinary when viewed in a historical context.

The water situation today is similar to the oil situation we had in the 90’s. Back then, I paid $0.85 a gallon for gasoline and thought to myself “This is crazy. This stuff is cheaper than bottled water.” Today, I get my water bill and I think to myself “This is ridiculously cheap. They could increase the price of water 1000% and my bill would only go from $14 to $28 a month because 90% of the bill is just the service charge.” If the water gets scarce, they’ll start building desalinization plants in California on a large scale and we’ll see that 1000% price increase happen. We just have to hope that there is enough time to build the infrastructure, so that means we need a few “good” years with above average rainfall now and then.

Most of the water gets used by utility companies. It’s not the toilets and showers that consume massive amounts of water, but the A/C units. I can live comfortably without air conditioning, but 95+% of the residents won’t go for that, so there is little flexibility in reducing our water use.

I hope you brought a supply of water..

The housing market is in big trouble. It’s worse than Wolf is showing. The homebuilder stocks are the best short opportunity in the stock market – shooting fish in a barrel:

http://investmentresearchdynamics.com/the-housing-market-is-in-big-trouble/

Dave, I agree with you on new homes and builders. It just didn’t fit into this article. Here’s where I warn about dropping sales and ballooning inventories of new homes – and false optimism by builders (based on the sky-high prices they’re asking for, despite dropping foot traffic).

https://wolfstreet.com/2014/08/25/housing-bubble-2-drowning-in-unsold-new-homes/

Whoops, 1400 sq ft, not 14000!

It is over course different this time, in the sense that a substantial number of these sales have been completed in all cash. Nonetheless, I can’t help but wonder whether there is still a lot of bad debt or investments floating around (like there was in 2008) which will result in another government intervention when the inevitable crash finally comes.

From what I have been reading prices have flattened/ falling in the area now with foreclosures starting to spike again. Yes, the consumer always wins in the end. Where I now live In the Edgewood area of Md some homes have been for sale for over 3 years and in a “new ” housing development that is not even 15 years old. Several of these homes have already been foreclosed on. Heavily dependent on the military due to being next to Aberdeen Proving grounds . My best friends home across the street was short saled and actually was in a bidding war. Nicer and older than the “newer ” Ones! And that one is 20 years older!

When elephants dance mice get crushed.

The elephants borrowed at zero, bought en mass, have seen nice gains, now they are exiting their investments and taking their profits. This was the plan all along.

For the last few years the mice have partied right along side the elephants, but now the elephants are stampeding for the exits …

This does not bode well for the mice.

Unless you hide in your mouse hole and only come out when it is time to feast. The elephants are gone and your mice friends are dead.

I relocated to the SF bay area 3 years ago from Seattle area.

Housing price in the bay area is beyond where it was in 2007 bubble. I live in often name dropped city 40 miles northeast of Sillycon valley and 30 miles from downtown SF where people proudly display the city name on license plate. Our city is “served” by corporate shuttle buses from major tech and large biotech companies. Our house price went up by 40% in 3 yrs and selling for more than it sold for as brand new house in 2007. It’s all paper gain unless I sell the house and move out of CA. House price in Seattle area jumped as much. Seen this before twice in early 90’s and 5 yrs ago.

That said I think everyone who wanted buy bought and seeing the houses for sale in my development stagnate this late summer vs. last 1 year or so when it often sold for more than asking in bid frenzies. I mean it’s more or less greater fool theory of suckers paying lot more than what it may be worth until suckers bought already and no other suckers are willing to bid up.

I think rest of 2014 will see flattening price and 2015 will usher in steady decline till the housing price reaches more affordable level.

As much as I’d like to believe that a market-correction will bring prices more in line with what people, who actually want to live in a community, can afford, I’m not holding my breath. The housing market is messed up—investors increasingly crowding out would-be homeowners, wanting somewhere to live—but I don’t see a good or easy way to fix it, especially considering that many of the new properties being built have been high-end not the affordable variety.

The Florida papers say that a new round of foreclosures will hit the market due to the courts clearing out all the old foreclosure cases. The mortgage modification houses are now also starting to reset to higher interest rates and owners are defaulting again. I think this time they will just walk away. Mortgage re modifications basically turned owners into renters by extending mortgages to 40 years. The house rental market is currently expensive and tight with families doubling and tripling up. No one really wants to buy because you can’t predict where your next job will come from. I learned my lesson and will probably never own again.

Power of leverage can be awesome magnifying the gains but what about those who pay all cash when RE market tanks?

Low down or even no down (get 2nd mortgage as downpayment) was common during the halcyon days of last RE bubble in 2007. Not to mention neg amortization, interest only and liar loans. Many walked away with little capital lost or even got ahead as lived mortgage/rent free till foreclosed (heard some people paid no mortgage for 2 years till booted).

Latest fad is all cash deal with some people pulling money out of 401k or borrow from friends and families, buy the house and some apply for mortgage or HELOCS and pay back the loans.

But what about those who pay cash and not tap the equity? They may indeed become the bagholders as if price went down 10% then they’re down 10%, etc. I mean it sucks to loose capital.

Wonder how these all cash deal will impact the RE market when it indeed adjusts to “norm”…

Vespa P200E AKA Duke

With major hedge funds in on the game (especially rentals), I wouldn’t be surprised to see the losers lobbying Congress for a handout when the crash comes.

From Zero Hedge. Congress to the rescue: H.R. 5148: Access to Affordable Mortgages Act.

Affordable mortgages doesn’t do you a lot of good when your up against all-cash offers. A seller will almost always take the latter because they can close faster and they’re guaranteed to get their money–there’s no risk of a loan falling through.

1) The Affordable Mortgages Act applies only to junk/distressed properties in rundown neighborhoods. Definitely nothing that is going to rescue home sales for the average person.

2) It is only a bill that has just now been introduced for comment. Early predictions are that it has a 22% chance of passing based on those who analyze such things.

3) Any govt. program with the word “affordable” in it, isn’t.

Having started investing in Las Vegas in 2011 in the midst of the biggest foreclosure crisis ever, I had seen some prices so low that I just couldn’t believe it. I bought a 2 bedroom condo ($26,000) for less than the price of a car and rented it out for $625 a month. So as the banks stopped unloading their foreclosures on the open market in 2012(but rather through bulk sales nowadays), inventory in Las Vegas dried up and buyers began bidding up prices. I know friends who have elected to pay higher prices and moved to the edge of the town just to buy a house.

Although I think the rise in prices help bring some homeowners out from underwater, the greater problem was that it prevented potential homeowners from getting into the market. In the Vegas market, we as investors tend to get much better deals than what a homeowner could get. After all, a lot of investors can pay cash and many potential buyers just can’t compete with that. Usually new buyers have to bid higher or purchase newly constructed homes, which most investors aren’t interested in. So since 2012, we saw a quite fast appreciation in the market.

Despite the challenges, home affordability is still quite low in Las Vegas. You can still buy most 3 bedroom single family homes in decent locations for around $175,000, a price that is considered quite affordable compared to many cities, including San Francisco. The mortgage payments are not that much higher than what you would have to pay for rent. Thus, I don’t believe there is a housing bubble in Las Vegas right now. We are still getting a decent 5-6% return on our investments. In fact, many of us investors are hoping home prices will drop. If prices drop we will definitely flock in and snap up all the inventories. As much as I hoped for a collapse in real estate in Vegas, I don’t think it is quite in the works yet. If home prices appreciate another 20-25% within the next couple of years, then we may start becoming less affordable.

Based on Armstrong Economic’s model, we are currently in a 26 year contraction (we are just about at the peak of a wave of inflation.) Afterwards, there will be a steady decline of prices. Whether or not, we plummet to 1950’s levels remains to be seen. With sovereign debt at unsustainable levels, 54 million baby boomers retiring over the next 15-20 years, and a monumental pension crisis looming – I don’t see a surge of real estate investing.

My advice is don’t buy new home. Go for the ones that are built at least before 2000. Of course, they all look nice with no maintenance. But the major property developers use very cheap materials and the workmanship is really substandard. You will start seeing problems in 5-8 years on.

Also don’t go for the size if you plan to stay in the property longer. The bigger the house, more chance to go wrong, more property tax to pay, higher maintenance cost and eats your wallet to heat up the house, especially in the long run. You just end up buying more junks to fill up the space.

With property in two states (CA, TX), I see regional differences really are deciding factors on whether to buy or not. Zillow research is showing some markets never recovered or even grow today (Chicago, Long Island, and others). I bought a CA condo in cash earlier this year to avoid renting and airbnb it while out of town. There’s so many different scenarios with real estate, which makes it an excellent way to invest and have control over your capital.

Grant, Nevada is allocated only 1-2% of water from Lake Mead, so it doesn’t really matter how much lower it gets. One intake could go dry if the lake drops much more. There is a second intake lower than that. They are also drilling a giant intake that will come from the bottom of Lake Mead like a bathtub drain.

20% of all Lake Mead water goes to the Imperial Valley in California for agriculture because its water rights are so ancient. If Lake Mead drops further, emergency cuts could impact Nevada and Arizona. If that happens, most observers think the Imperial Valley will simply have to take a cut and the law be damned.

Grass lawns and golf courses in deserts will probably need to vanish.

I’ve followed water issues closely for several years on my blog. The drought is absolutely a problem. However, in my opinion, Nevada and Arizona are way more proactive that California. Tuscon, for example, now uses less groundwater than in 2000 despite a big jump in population. California is only just now thinking about regulating groundwater pumping.

The Sacramento Delta is crucial for California water and there simply isn’t enough to go around. Ditto for the Colorado River, which seven states rely on.

its nice to have hard assets when hyper inflation kicks in, its just a matter of time. then those house prices will be a bargain. have not you been listening, the fed wants inflation.

If the number of homes for sale in the $100 to $375 price range has fallen as much as you say, wouldn’t that indicate someone is buying them?

I know in my area of the West Coast, inventory of homes for sale is very low.

Wolf, I’m sure you will be discouraged to discover that immediately to the left of this column, at the top, is an ad for learning how to flip homes.

[Still, I assume the ads come up randomly and you have no control over them.]

It’s “Google Humor” or as some call it “Google Sarcasm.” Google serves these ads, and readers get their own individual mix of them. A reader once sent me a screenshot of one of my articles on the Fukushima nuclear fiasco; it had a sushi ad to the left…..

Good luck to you house buyers of the past five years. I wish you well. I have stayed away from what is in my opinion a continuation of 2008 all this overpriced residential real estate and have been renting and will do so until the major reality check comes in to this madness. Do you actually think this DOW is sustainable? Has anyone any sense of history and what it tells us? What does one do with a small 500K or 700K place when the rates go back to normal? What do you do with it? I do not see where a buyer comes in at that time because that few point raise in rates means a lot more in payments. I remember the early 1980s when mortgage rates were what over 15%! Yes, kiddies. Good luck to anyone falling for this smoke and mirrors game of stock and real estate. It is amazing to me what people do.