The largest retailers in the US are struggling to get their sales up. Walmart’s US comparable-store sales were flat for the quarter ended August 1. Macy’s reported disappointing sales and cut its forecast for the year. Other retailers have chimed in, some with better results (Home Depot, for example), some with fiascos (Elizabeth Arden, with a 28% plunge in sales).

It has been tough out there. Retail sales, which make up about a third of consumer spending, were supposed to increase 0.2% in July, according to the inveterate optimists that economists have become. But that didn’t happen.

Instead, they stagnated, not adjusted for inflation, after a measly growth of 0.2% in June. But on Tuesday, the Bureau of Labor Statistics tossed the Consumer Price Index for July into the mix. With official inflation up 0.1% for the month and 2.0% for the year, it was considered “tame” by those who clamor for more inflation because it suits their own purposes, like repressing real wages. Tame or not, inflation knocked real retail sales into contraction.

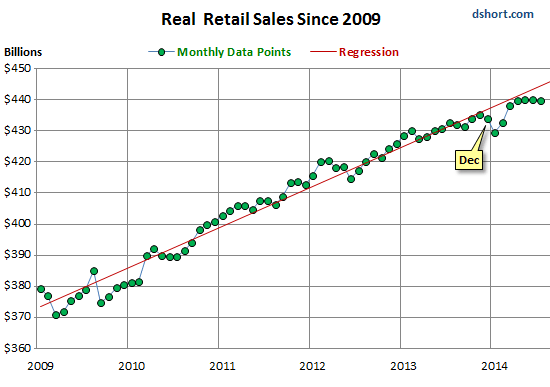

And not only for July, but also for June. Doug Short of Advisor Perspectives has been tracking retail sales on an inflation-adjusted basis for years. They’ve been recovering unevenly from the Great Recession. But then something happened in November and they stalled. They dropped in December, plummeted in January – the weather was blamed liberally – then recovered some in February and March. But since April they’ve stagnated, and actually lost ground in June (-0.02%) and July (0.05%).

This chart, with sales data chained in constant July 2014 dollars, shows the recent retail reality of stagnation:

With inflation picking up earlier this year, consumers, already at their limit, got pinched, or at least the vast majority of them – those who haven’t benefited from the asset bubbles the Fed has engineered so relentlessly, those who don’t have enough money to invest in stocks or bonds, including those 60% who don’t have enough money in a bank account to pay for an “emergency expense” of $400, as the Fed itself admitted.

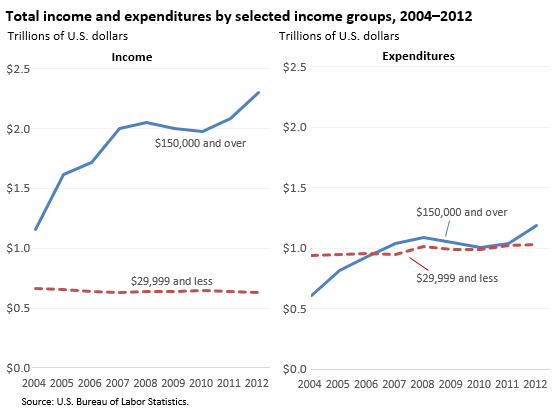

As if to drive home the point, the Bureau of Labor Statistics coincidentally released a study to confirm what has become the biggest economic problem in the US: those at the lower-income levels, those who’ve gotten ripped off by inflation and wages, have become terrible consumers in an economy dependent on consumer spending.

The report found that the average income of households in the top 20% grew by $8,358 per year from 2008 through 2012. But the lowest 20% saw their already minimal incomes get whittled down by $275 per year. The earnings of the second and third quintiles increased only $143 and $69 per year. So for the bottom 60% combined, there really wasn’t any improvement.

And their spending patterns? The lowest quintile cut their spending by $150 per year in total. They cut where they could: in seven categories, totaling $490 per year, mostly on apparel, entertainment, housing, and personal care. And they increased spending where they had to: in seven other categories totaling $340, topped by “cash contributions” such as alimony, “miscellaneous,” and healthcare.

This principle of cutting back where they can and spending more where they have to, in order to make their shrinking ends meet, has been dissected by Gallup, which found that consumers are “straining against rising prices on daily essentials” and are cutting back on things they want to buy [read… Gallup Slams Lid On Hopes For US Economy].

But not everyone has this problem. The top two quintiles raised their expenditures by $1,348 and $2,365 respectively. And that’s where the entire increase in consumer spending since 2008 has come from. But over the long run – and that’s now – the math just doesn’t work out.

This is the picture of that distortion, the one that is dragging down the American economy:

That was during the years when consumer spending actually increased. But for 2014, the jury is still out.

There’s no room for doubt, however. Not in the Wall Street hype machine. “We expect this slowdown to be short-lived and we look for consumer spending to rebound strongly in the coming months,” said Millan Mulraine, deputy chief economist at TD Securities.

And on the other hand, predictably: “It will provide Fed Chair Janet Yellen with some of the rationale she needs to justify why the Fed should move gradually and keep interest rates low for longer than hawks within the Fed would like,” said Diane Swonk, chief economist at Mesirow Financial.

This is the Wall Street hype machine, as reported in one breath by Reuters. Out of one side of its mouth, it propagates the myth that the crummy retails sales will “rebound strongly” to lead to that ever elusive escape velocity so that stocks could continue to soar; out of the other side of its mouth, it propagates the hope that the Fed now has an excuse to keep the Wall Street punchbowl spiked with ZIRP so that stocks could continue to soar.

You’d think the housing market is in fine shape, based on the sizzling optimism of our home builders. But now comes the bailed-out mortgage giant with a belated dose of reality. Read….. Fannie Mae Sledgehammers Housing Forecasts

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Interest rates can never get back to “normal”. The amount it would take to service outstanding debt would take the economy to a literal standstill, even worse than it is.

War may be close.

Get right with God. John 3:16

Proverbs 27:12

A prudent man foreseeth the evil, and hideth himself; but the simple pass on, and are punished.

Consumers (cannibals) are broke. To waste capital they borrowed, now the capital is gone with nothing to show for it except (massive) debts. Whoever thought of this brilliant business plan should be taken out and shot.

The economy of the insane: our measure of ‘success’ is a matter of how fast people can burn down their houses.

The problem is at the end of your driveway, as long as it is there the more downward bends will appear on charts.

You just described Keynesian economics perfectly.

If I don’t need it I don’t buy it and then I have to save up.

I posted some of this elsewhere but I suppose it fits here better. We are a one income family (I am a woman with two degrees who chose, when my kids were born to stay home with them full time and who never wanted to get back into the corporate world) with a professional income and a VERY safe job. No one is laying off my spouse or will be. We have A SON in college (a large expensive state school with an excellent rep in the East)- graduating next year. The other is graduating in December after many years in school with an MA and a PhD and a lot of papers published and with excellent peer reviews and substantial lab and supervisory experience as well as the boffo computer skills required by her field( note – it is not a STEM field however). We, the parents, have dramatically cut back our spending in order to be available to help our kids. First we pay all four year college costs so our son and daughter will have no loans for that. Lucky we have an income that easily allows us to do that. BUT our daughter insisted on taking charge of her own grad school( MA and PhD) and has appx 100K in loans now. And, with this great and growing economy, has had little luck in finding a full time with benefits job in her field at least so far( she is ABD and so eligible for professorships now) . She is adjuncting full time at two premier private universities with tuition above 45k a year, for less in total than she would make as a full time waitress in a nice restaurant…… Let that sink in. THAT is the real America now folks…….And by the way she actually waitresses on the weekends as well. Her health is starting to suffer. Lucky that we pay through the roof for a good health policy and have since she fell off our excellent insurance- (pre ACA )at 22, because she has a spinal condition that requires expensive care and the uni policies available were too basic.

The point is you do not have to be any where NEAR ‘low income’ or have an insecure job to not be spending. We have a reasonable good upper middle class income and have never had a problem buying what we want, taking our kids abroad every year when they were young or buying cars or houses or pools etc. until the last few years when we looked at what was going to greet our kids when they were out in the world starting their lives and decided it was necessary to stop all unneeded major expenditures( and an awful lot of minor ones as well- like eating out) in order to be ready to assist our kids if needed. We had every intention of buying a smallish beach house strictly for our family to use( no renting) as we are not all that far from a coast. We can afford the prices- not an issue. But we are not going to do it- likely ever now- unless things turn around dramatically, Just in case our kids have a financial crisis we want to be liquid. We are not doing our usual regular car replacement either and instead are keeping the ones we have. We are not vacationing on our usually two each year cycle – just in case. Our daughter is marrying next year – we are not having the blowout wedding we all always hoped for at our daughter’s request because she says she may need our help in other areas. Our soon to be son -in -law is a dedicated and nationally recognized teacher… In a very low income school and even with the extensive recognition his job is on the bubble EVERY year. And of course is pay is abysmal….They despair of ever buying a home and are also worried they will not be able to afford even one child and the associated costs.

I bring all this again around to my main point. NOT everyone who is not spending is ‘poor’ or ‘low income’ or uneducated. This economy is ruined for EVERYONE and sensible people are altering their behavior at all income levels in order to be ready for what may happen. For example – Golf club memberships at our private, and may I say prestigious club, are being turned back at a staggering rate and not because of age or job loss but from uncertainty. Ours is going to be next at the end of playing season this fall. We just cannot justify it despite the fact we play every weekend and I play during the week nearly every day.

This country is in serious serious trouble and the financial powers that hold sway as well as our government policy makers better get their sh** together and actually see what is going on on the ground in real families and take action or we are going to be a banana republic before the end of this decade….

Desertmer, I posted your comment on the front page, right-hand column. Thanks for sharing your insights and thoughts.

You’re welcome and thank you as well for allowing me to express myself.

And you still believe that interest rates will be out of control by when? The interest rate has already raised by 100 basis points during the middle of 2013 which of course was poo pood by the experts as too little too late and yet affected the economy long before the snows came and is still seeming to affect it? Walmart as an example is pouring more money into new buildings and E-commerce aka investing in MORE stores! People are making remarkable progress in living within their means and of course are vilified as being poor because they aren’t keeping the spending spree going like their parents did? Record stock buybacks and a historic generational low in stock ownership trumps any normalization of interest rates ( few remember double digit interest rates and less would allow it to happen again) basically you can only dump gold as a limitation once and we have already jumped that hurdle in the ’70s!

I’ll be spending plenty to replace stuff stolen from my wife’s car in the yard, including her revolver and everything in the trunk. I’ll also be buying silent alarms and a game camera. Hope to bag the next SOB.

The rich keep getting richer, so…….. “if it ain’t broke, don’t fix it”. The top 1% have the ears of the politicians (lobbyists), so the right thing to do, will not be done.

By the way, if the middle class disappears, who pays the taxes? Here in Canada, we don’t have taxes – we have “revenue tools”.