New vehicle sales in July disappointed our dreamy analysts. The seasonally adjusted annual rate (SAAR) of 16.48 million vehicles sold was down 2.4% from June’s revised rate of 16.90 million, which had been the highest since July 2006. The decline touched all categories – cars and light trucks, domestic and foreign.

In dollar terms, sales were even less rosy. The motor vehicle component of the retail sales report by the Commerce Department already showed a drop of 0.3% for June, when unit sales were still rising. Now that unit sales have begun to taper as well, dollar sales are likely to drop even further, to drag down overall consumer spending in July.

Inventories are piling up, and new models are coming down the pipeline, and dealers have to move the iron. So the industry has been whipping sales with all its might, largely through aggressive lending – particularly subprime auto loans – and the bane of automakers: incentives.

In a mad scramble, dealers are stuffing people with bad credit into cars they can’t afford, and finance companies are eager to lend to them. Loan-to-value ratios now average over 100% across the industry. Dealers roll everything into these loans: title and taxes, credit life insurance, and other fluff-and-buff, plus the amount buyers are upside-down in their trade-in. To bring the payments down on these monster loans, lenders lengthen the terms. Subprime auto lending is booming, and charge-offs are rising. “Signs of increasing risk are evident,” the Office of the Comptroller of the Currency had warned in June [Federal Regulator Details Crazy Risk-Taking By Banks, Blames Fed].

The bane of the automakers: incentives

Loans that blow up in the future are a cost that will be eaten by a variety of players, including banks, and if all else fails, by the taxpayer. Incentives are costs – or rather a reduction in revenues – that are eaten on the spot by manufacturers. The incentives in June caused the dollar sales decline in the motor vehicle component of the June retail report. And July is looking even worse.

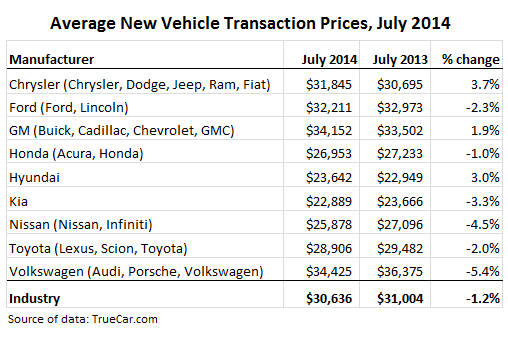

Overall, TrueCar estimates that the average transaction price (ATP) for light vehicles in July dropped 1.2% from a year earlier, to $30,636. Reason: incentive spending. Because sticker prices of new vehicles went up, not down! As the table of the top manufacturers shows, only Chrysler, GM, and Hyundai bucked the trend.

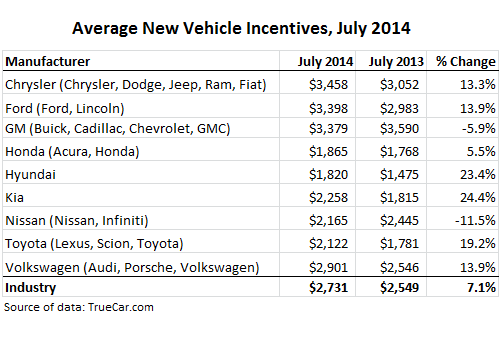

Average incentive spending jumped 7.1% from July a year ago, to $2,731 per vehicle, the highest level since the car-crisis year of 2010.

Note that GM’s incentives, though down from a year ago, were by far the highest in the group. GM was spending like mad to whittle away at its bloated inventories, the highest in the industry. It’s just that last year, they’d spent even more!

Booming auto sales over the last few years, from the abysmal levels during the Great Recession, had been one of the pillars of whatever strength there’d been in consumer spending. Consumers can’t afford these cars. So auto lending has soared as well. And consumers with bad credit, no problem; subprime auto lending stepped in. Prices and payments too high? No problem, stretch out the term of the loan. Upside down in the trade-in? Fine, plow the shortage into the new loan and find a lender that will close its eyes….

It all worked. And without the boom in auto sales, consumer spending would have been even drearier than it has been. But someday, these strategies reach their limit. Lenders get scared. Regulators start fretting about losses. Consumers are maxed out. And suddenly, even booming subprime auto lending and the highest incentives since 2010 – the toxic mix in auto sales – can’t move enough of the iron. The check-engine light just came on.

Tech companies are on a white-hot acquisition binge, swallowing anything that isn’t nailed down. But layoffs have started soaring. And it’s getting worse. Read…. What The Heck Is Wrong with Big Tech?

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I don’t think it’s limited to cars. Past 12 months of GDP growth has been $354 billion in inventories and $321 billion for everything else.

We just bought a new mattress. They offered us 0% financing for 5 years. I hate having debt and pay my credit cards off every month, but even I took that deal. Of course, for those folks who miss a payment it’s 25%.

When we bought a new car in April we were offered an extra $1500 off only if we financed at 0.9%. WTF? Well, in the size 4 font of the loan agreement it said some or all of the interest payment might go to the dealer. We took the loan to get the discount but since it was simple interest we just paid it off later that week.

Back in the day when I was in the car business, these kinds of incentives – 0% financing, $2,500 “cash back,” etc. – were moves of desperation. I’m not on the inside anymore, so I’m not sure, but it sure smells like it.

I think its desperation. They have over 70 days of inventory and it seems to be creeping up. What do you think about the claims of channel stuffing? After the GM IPO there was a lawsuit alleging that but I can’t find anything recent on it. ZH has been pushing the story but I have heard others say this is just business as usual, or unfortunate inventory management, and that there’s no conspiracy to channel stuff. Inventories in general seem to have been slowly rising for several years. The backdoor feeding of the 0.9% to the dealer smells funny as well. Did you ever see that when you were in the business? Is this new? I’ve read about 84 month loans.

Then there are leases. As you know, it’s a great way to make the cap cost equal to MSRP, and they get the payment down by making the residual value sky high. Another deferred liability waiting to blow up down the road but for now, it’s marked as a sale at full asking price.

Meanwhile industry spokesmen say it’s all good and there’s plenty of room for more aggressive incentives. Nothing to see here.