By Editor, Fabius Maximus, a multi-author website with a focus on geo-politics. This is a shortened version of two articles that originally appeared here and here.

Growth slows in the developed nations due to several factors, as debt levels rise. Have we entered the “coffin corner” where we cannot grow sufficiently fast to service our debt?The US economy has repeatedly failed to resume normal growth after the crash. But potentially worse is the decline in long-term growth estimates.

Our plight: our maximum growth rate slowing to our stall speed.

In January 2011 the Federal Research estimated the long-term growth rate of the US economy at 2.5 – 2.8%. By June this year, their estimate had fallen to 2.1 – 2.3%. Years of low investment by the private and public sectors, a decaying education system, rising debt levels, and demographic headwinds (an aging society) — all are slowing America’s growth.

The potential boost from technology so far remains speculation about the future.

For tangible evidence, see the economy’s inability to “take off” since the crash (GDP has limped along at an average of 2.2%). On January 3, JP Morgan forecast 2014 GDP to be 2.8%, the fastest since 2005. Now they expect half that, 1.4% — the slowest since the 2008 crash.

That’s far too close to the economy’s stall speed of 2%, below which it’s at risk of falling into recession — much like an airplane going too slow, generating insufficient lift to stay aloft (this is a controversial theory; now we’re testing it). Perhaps the US economy cannot accelerate by much from current growth rates (without undesirable rates of inflation), and it cannot slow without falling into recession (ruinous under current conditions, with monetary policy tapped out, and with fiscal deficits and unemployment still too high, but falling).

This will make economic management quite difficult for the foreseeable future. Persistent slow speed will create pressure for stimulus (perhaps with long-term ill consequences). Failure to quickly stimulate to even small mistakes might easily trip the economy into recession.

The Economic Cycle Research Institute (ECRI) also sees the problem in its “Cognitive Dissonance at the Fed?:

Federal Open Market Committee (FOMC) members have long submitted their projections of U.S. real GDP growth for the “longer run,” to which they expect it “to converge over time – maybe in five or six years – in the absence of further shocks and under appropriate monetary policy.”

… So what is being gradually acknowledged – without any publicity or fanfare – is that long-term U.S. GDP trend growth is converging towards its 2% stall speed. If so, almost every time GDP growth experiences a slowdown that carries it below trend, it will also fall below the recessionary stall speed. This is an implicit endorsement of ECRI’s longstanding “yo-yo years” thesis, which predicts more frequent recessions for the advanced economies than we have seen in past decades.

Ian Hathaway and Robert E. Litan, The Brookings Institution, point at a similar phenomenon in “Declining Business Dynamism in the United States: A Look at States and Metros“:

Business dynamism is the process by which firms continually are born, fail, expand, and contract, as some jobs are created, others are destroyed, and others still are turned over. Research has firmly established that this dynamic process is vital to productivity and sustained economic growth. Entrepreneurs play a critical role in this process, and in net job creation.

But recent research shows that dynamism is slowing down. Business churning and new firm formations have been on a persistent decline during the last few decades, and the pace of net job creation has been subdued. This decline has been documented across a broad range of sectors in the U.S. economy, even in high-tech.

John G. Fernald, Federal Reserve Bank of San Francisco, in “Productivity and Potential Output Before, During, and After the Great Recession,” explains:

US labor and total-factor productivity growth slow ed prior to the Great Recession. The timing rules out explanations that focus on disruptions during or since the recession, and industry and state data rule out “bubble economy” stories related to housing or finance. The slowdown is located in industries that produce information technology (IT) or that use IT intensively, consistent with a return to normal productivity growth after nearly a decade of exceptional IT-fueled gains.

In the absence of effective and comprehensible economic theory, economists often rely on analogies. Such as comparisons with aerodynamics. Flying complex vehicles at high speed under variable conditions, often with inadequate or old information — the role of pilot has similarities with that of central banker.

A common mistake of central bankers is raising rates to curb inflation while the economy is in fact on the brink of recession. That’s similar to another dreadful aviation term, the graveyard spiral: “This flying by ‘the seat of the pants’ and failing to recognize instrument readings is the most common source of ‘controlled flight into terrain.'”

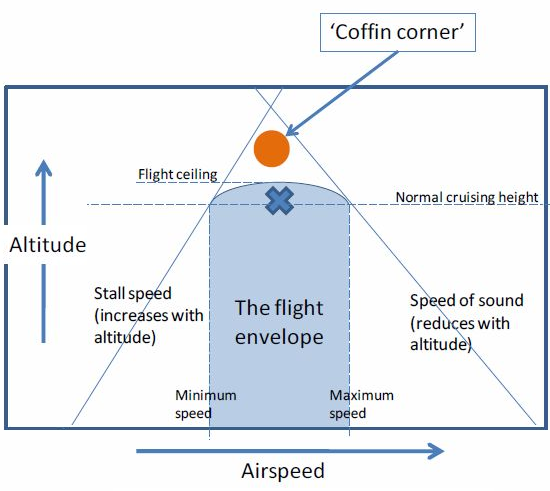

Today the US economy might have flown into conditions similar to another perilous aerodynamic situation — the coffin corner. From the Sky-brary (slightly edited):

The coffin corner (aka Q Corner) is the altitude near which a fast aircraft’s stall speed equals its critical Mach number. As an aircraft climbs towards the altitude that defines its coffin corner, the margin between stall speed and critical Mach number becomes smaller and smaller until the Flight Envelope boundaries intersect. At this point any change in speed creates serious problems. Turning the aircraft could result in exceeding both limits simultaneously, as the inside wing slows down and the outside wing increases speed. Encountering turbulence can push the aircraft outside its flight envelope.

Is the US economy at the “coffin corner”?

Andrea Cicione of Lombard Street Research, a top-quality macroeconomic forecasting consultancy, uses the aviation metaphors of stall speed, overspeed, and coffin corner to explain US economic risks (PDF):

Well, replace “airspeed” with “GDP growth”, and “altitude” with “debt-to-GDP”, and you can probably start to see where we’re heading with this. According to the OECD, the government debt-to-GDP ratio for 10 large economies (Australia, Canada, France, Germany, Italy, Japan, Korea, Spain, the UK and the US) has surpassed the previous peak recorded at the end of WWII. … the overall debt burden for the 34 OECD member countries will continue to climb in coming years. While there has been selective deleveraging in certain sectors of the global economy (e.g. US households and DM banks), debt, rather than having been reduced, has mostly been transferred from the private to the public sector.

The question is whether advanced economies, in an effort of trying to limit the damage caused by the Global Financial Crisis, have put themselves into a debt coffin corner. With debt-to-GDP (altitude) as high as it is, they can’t allow growth (airspeed) to slow too much, or debt risks becoming unsustainable. At the same time, high debt levels are likely to be a material drag, making growth hit an insurmountable economic “sound barrier” much earlier. This is because without the boost provided by credit growth, it is difficult to achieve the kind of GDP growth that was possible when debt-to-GDP was lower.

But there’s more. High levels of debt-to-GDP ratios make it difficult for governments and central banks to steer the economy – just as excessively high altitude makes it difficult for a pilot to keep control of the aircraft. Central banks have successfully employed Zero interest rates policy (ZIRP) to keep debt sustainable but, as the economy continues to recover, they may now find themselves cornered: keeping rates as low as they are may lead to overheating (or even bubbles) in certain sectors of the economy; but raising them may stall others by making the existing debt impossible to service.

Now for a bad scenario

What if the economy’s long-term growth rate continues to decline? What if our aggregate debt continues to increase so that the economy’s “stall speed” increases (i.e., a higher minimum speed is needed to keep the economy aloft)? What if the two lines cross? There is relatively little research on these matters, and little agreement among economists, but if the metaphor holds, the outcome wouldn’t be desirable. By Editor, Fabius Maximus. The full-length articles are here and here.

There are some good reasons for this stall speed. Consumers are “straining against rising prices on daily essentials” and are cutting back on things they want to buy, Gallup found in a new survey. Read…. Gallup Slams Lid On Hopes For US Economy

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

“if the metaphor holds, the outcome wouldn’t be desirable.” Talk about underplay.

That being said, I was struck by the number of times the word “growth” was used in this article. Isn’t it high time we start questioning this perpetuous growth model thing in earnest? Provided we even have the resources at our disposal, what is it exactly we want to grow into? A giant legion of human cockroaches, eventually destroying everything in its path? 14 billion instead of 7? Or a 140 billion? Or do we hope that things will somehow magically rebalance somewhere along this road? Maybe they will, but wouldn’t it be prudent to start thinking about the feasibility of an economic model that takes growth out of the equation, or at the very least slows it down significantly?

And before anyone starts throwing labels: no, I am not a member of Greenpeace. I do have 46 chickens, though, so maybe I need some professional help after all.

Here is the problem – for which there is no solution. High priced oil destroys growth – yet even with the price over $100 Exxon and Chevron have announced capex reductions citing inability to turn a profit with oil at the current price.

But of course oil prices cannot go higher without destroying the consumer.

They cannot go much lower otherwise exploration will end – shale ends – tar sands ends (and as you can see those are the only types of oil that are seeing production growth https://gailtheactuary.files.wordpress.com/2014/07/us-crude-oil-production-including-tight-oil.png)

HIGH PRICED OIL DESTROYS GROWTH

According to the OECD Economics Department and the International Monetary Fund Research Department, a sustained $10 per barrel increase in oil prices from $25 to $35 would result in the OECD as a whole losing 0.4% of GDP in the first and second years of higher prices. http://www.iea.org/textbase/npsum/high_oil04sum.pdf

THE PERFECT STORM (see p. 59 onwards)

The economy is a surplus energy equation, not a monetary one, and growth in output (and in the global population) since the Industrial Revolution has resulted from the harnessing of ever-greater quantities of energy. But the critical relationship between energy production and the energy cost of extraction is now deteriorating so rapidly that the economy as we have known it for more than two centuries is beginning to unravel.

http://ftalphaville.ft.com/files/2013/01/Perfect-Storm-LR.pdf

If alternative oil production destroys our water supply, we won’t be needing as much oil! Problem solved?

Just to riff a little more on the analogy….. we ought to add that the ‘central banker pilot’ is trying to keep the ‘plane’ aloft whilst strapping on his own parachute, making sure that his/her buddies have chutes also, whilst telling those in coach that everything is going swimmingly and we will all be ok!

. …..oh and those in coach are worrying about what movie they should watch! (ignorance is truly bliss).

S

PS And of course when it all ends in a big flaming hole surrounded by small charred pieces in a field somewhere, those who parachuted to safely will be charged with flying the new plane.

That’s fabulous! The central bankers are literally giving their buddies trillions to buy up everything of value before the crash.

Perfect analogy.

Some numbers:

1% of the population owns 99% of the actual wealth,

while 99% of the population would rather hear comforting lies

than uncomfortable truth. The Fed and Goverment are only too happy

to supply the latter.

Suppose everything is great with the plane, crew and passengers but a sudden storm ahead destroys everything. The NYC banksters and Obama have so angered the BRICS, Germany, France, etc, that they have decided to destroy the US/UK by dealing in their own gold backed currencies, with their own world banks, and their own internet system. We need a revolt at the polls 4Nov2014.

Robert H. Sidell Jr…

Unfortunately, when it comes to voting for a good leader…

Democrats and Republicans.

Different circus.

Same clowns.