The Price-Sales ratio (among others) has blown through the roof

The California Policy Center published an interesting study – “interesting” in all kinds of ways, including its outline of the doom-and-gloom future of California’s state and local pension plans if stocks turn down sharply, preceded by its prediction that stocks will turn down sharply because valuations are totally unsustainable.

The huge, simultaneous, Fed-engineered rallies in stocks, bonds, and real estate – typically the three biggest holdings of state and local pension funds in the US – have inflated the balance sheets of these funds, thus elegantly, if only partially, papering over their fundamental problems. Most of these funds have a similar doom-and-gloom future when the asset bubbles get pulled out from under them. Plenty of pension funds don’t even need a market correction: they’re already in serious trouble despite the asset bubbles.

So what happens when these asset bubbles burst, or when, to be merciful, just one of them bursts?

Ed Ring, president of the California Policy Center and author of the evocatively titled study, “How a Major Market Correction Will Affect Pension Systems, and How to Cope,” uses a long-range cash-flow model with a number of variables to simulate different scenarios for California’s state and local pension funds. To figure out what a stock market crash might look like, he looked at three key stock market ratios for the S&P 500:

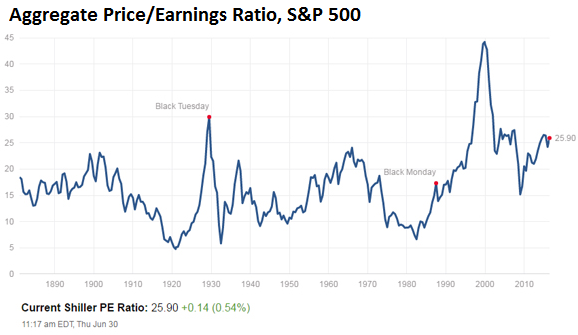

The S&P 500 Aggregate Price/Earnings Ratio

The P/E ratio of the S&P 500 companies is at 26. It spiked higher than that only three times over the last 136 years: in 1929, it peaked at 30; in March 2000, it spiked at 44; and just before the Financial Crisis, it peaked at 27. The thing to understand is that the aggregate P/E ratio didn’t plateau or level off after these three spikes. It plunged (chart via CPC):

So according to Ring (emphasis added):

If the P/E of the S&P 500 were to revert to a sustainable historical average of 16, the S&P index would fall by 36% to 1,362. And while that’s a usable projection, in reality when corrections occur, the P/E ratio falls below the average for a time, i.e., a correction to 1,362 might be a best-case scenario for the S&P 500.

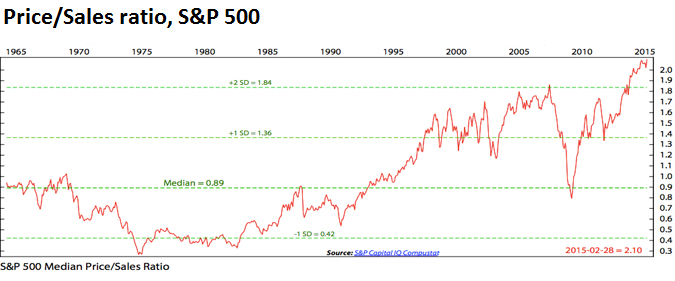

The Price/Sales Ratio

It measures the annual revenue of the S&P 500 companies, divided by their aggregate market value. A sour note that the report didn’t mention: these revenues have been declining year-over-year for six quarters in a row!

Ring points out that the “sustainable historical average price/sales ratio for the S&P 500 is 0.9x.” In 2000, the ratio peaked at 1.6x. In 2008, it peaked at just over 1.8x. In 2015, it reached 2.1x! It has since moved even higher, as sales have fallen while the S&P 500 has risen to new highs (chart via CPC):

Ring puts the scenario this way (emphasis added):

If the P/S of the S&P 500 were to revert to a sustainable historical average of 0.9x, the S&P index would fall by 57% to 912.

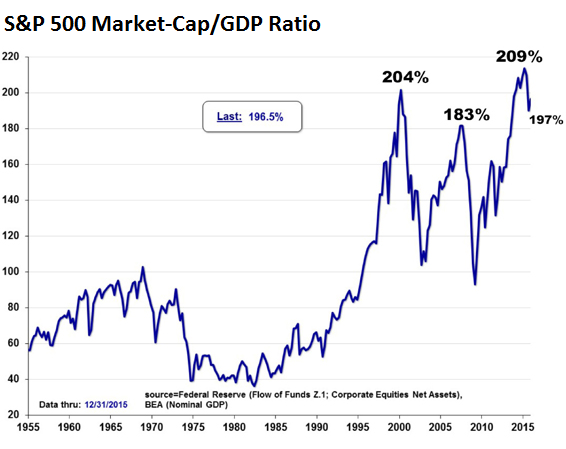

The Market-Cap/GDP ratio

It measures the market capitalization of the S&P 500 as a percent of nominal GDP. It soared to 204% in 2000, and to 183 before the Financial Crisis. During the respective crashes, the ratio plunged to about 100. In 2015, it soared to 209, before the subsequent market swoon took it down to 197 by the end of the year. Since then, stock prices have risen by lot more than GDP, and the ratio – once we have Q2 GDP data – should be setting new highs (chart via CPC):

Ring points out (emphasis added):

If public stocks in the U.S. were to revert to a market cap/GDP ratio of 100%, the S&P 500 would fall 50% to 1,064.

The conclusion of this section, using the average of the three ratios just considered, is that if stock prices were to return to sustainable levels, the indexes would fall by 47%. This is consistent with the findings of the previous article, which demonstrated that debt formation can no longer be used to stimulate the economy and the markets because interest rates have been stuck at or near zero for the last seven years.

CPC constructed a model (spreadsheet) where you can play with different inputs to do a what-if analysis. With the current assumptions of the pension funds, including a return on investments of 7.5% per year forevermore, the model portrays the funds in a nice light:

The results calculated by the model, based on this “business as usual” are surprisingly positive. They show the unfunded liability being consistently whittled away, such that by 2020 the consolidated systems are 72% funded, by 2025 they are 81% funded, by 2030 they are 91% funded, and by 2040 they are 118% funded.

So we’re dreaming.

But what if the stock market crashes 47% in 2017 and then earns 5% afterwards for years to come, with no changes to pension benefits? The consolidated average contribution would jump from 32% of payroll to 80%, which would cost Californians an additional $51 billion per year.

That’s the baseline scenario, not the worst-case scenario.

That type of crash has already happened three times during my exposure to the markets. Only this time, everything is more inflated and more messed up than before, and risks are piled higher than ever before, and none of them are priced in. So there are plenty of reasons for this scenario to play out. Yet global QE, ZIRP, and NIRP have systematically removed all reason from the investment equation. And that’s the biggest risk of all.

We just had a propitious day in our negative-yield pandemic. Read… The “Mass Psychosis” in Bonds Takes a New Twist

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Maybe equities no longer depend on such things as income, revenue and health of the economy. Maybe equities have become too politically important to be allowed to go down. Fed’s integrity, Obama’s legacy, reelection prospects of incumbents along with faith in the current banking system and retirement prospects of an entire generation is tied to equities.

Without an outside shock can and will equities be allowed to go down?

Yes, I wonder the same. It sure looks these days like the central banks are in total control of the stock market, and possibly the bond and RE markets as well.

‘Everything can only go up’, except rates of course … Come to think of it, maybe this is a good subject for the European Parliament to vote into legislation. I have no doubt they will be massively in favor ;-(

You nailed it. Stocks are completely disconnected from the old underlying reality. Just look at Tesla. I don’t care one pip if their cars are good or bad, if they pollute or save the environment. What I see is they lose money, often lots of it, on every single car they sell, yet stock values remain frothy.

Or look at Caterpillar, whose sales have been mauled both by their Asian competitors becoming really aggressive and China’s fantastic housing bubble showing some (actually a lot of) signs of strain. Stocks do not reflect how bad CAT sales have been not for months but for years.

There’s no doubt there’s something else but company performances that prop up stock values and that something is politics.

And here’s the really funny part: just how many voters/taxpayers own stocks and hence are interested in them? Here in Europe not many, albeit Draghi’s financial repression is pushing more and more desperate souls into stock markets which are nowhere near as safe as New York. It goes without saying that if Deutsche Bank, Credit Suisse, Unicredit, Santander, Credit Agricole etc get whacked a bit more on the head whole stock indexes are bound to take a pounding.

I made a prediction that by the end of 2017 the ECB will be either buying selected junk bonds or enganging in direct equities purchases. Yes, not even I believe they’ll be doing both.

The BOJ has been openly buying Japanese stock ETF’s since 2010 and plans to buy the entire market by early 2018 at latest. As not even this has been enough to push the Nikkei 400 back to its 80’s glory days the BOJ may start buying individual equities, possibly because they are running out of domestic financial paper to buy but more likely in a desperate attempt to mimick China’s legendary “plunge protection team”.

Inevitable bank tightening can bring it all down. Default rates have picked up in the US, and banking is capital constrained, so tightening and a credit freeze of some kind in the private sector is inevitable.

the percentage of EU taxpayers who actively own stocks is indeed quite small compared to the US (if I remember correctly less than 10% compared to 30-40% in the US).

However, many EU taxpayers own huge amounts of stocks through their pension funds. The average ex-government pensioner in my country has a pension with a cash value at present rates of at least several million euros. You can bet that politicians and ECB take this into account when they consider how far they will go to support the stock market. That they support the bond market and RE market through ultralow rates is obvious.

Does it matter if the ECB buys stocks directly? They are buying stocks INdirectly in massive numbers because they are providing free money to the big speculators, and much of that goes into stocks. The only difference is that with the current setup the financial industry gets to make loads of easy money for doing what the ECB itself officially is not allowed to do.

Yes. My prediction for some time now is that the central banks will end up trying to buy up all the world’s financial assets. Equities will vanish into debt-funded stock buybacks, then the corporate debt will become part of the QE squared bond buys by the CBs.

I watched the last episode of Wall Street Week because they were having a conversation about how they could “sucker”(my word) the millennials into the stock market. Apparently the millennials are avoiding the market in mass. It seems the millennials are in line to inherit the largest pool of money in history and the market wants it to stay in stocks and bonds, where they have access to it.

I do believe the current market capitalization is totally political, but it attracts onlookers at these levels, which is probably the point. I feel for the millennials who get ensnared in that rat’s nest.

my country has a clever use for all this still to be inherited money: push up the RE market even more, and do it NOW! More attractive than pushing up stocks, because over 50% of voters own a home while only about 10% speculate in stocks …

For about ten years (probably from 2008) we have had a tax rule that allows totally tax-free transfer of 25K euro per year from parents to offspring (aged 40 or younger), provided the money is used to buy a home. For one single year this could even be 50K euro per child. If the parents are wealthy we are talking about very significant amounts of money that is shifted completely tax-free between generations in order to support the housing bubble.

This year the rule was updated and the tax-free transfer has now increased to 100K, again provided the money is used to buy a home.

There is one bright side: due to the currently low rates many of these young buyers will buy the home cash or with a relatively low mortgage. Which means that there is less risk for the taxpayers, because with the average ‘homeowner’ in Netherlands all the downside risk for home prices lies with the taxpayers and not with the ‘owners’.

On the other side, I’m suspecting that a significant amount of this transferred money was not really owned by the parents, but taken out of their own home piggy bank. Which means that the taxpayers lose twice, and the risk might be even bigger because older people often have the most expensive homes that have appreciated by ridiculous amounts, to values that are WAY above the purchasing power of the younger generations.

For many millennials the Great Recession was the defining moment of their early careers and early lives. They have not lived a lifetime in which stock market has benefited them. Instead they have had to contend with diminished opportunities and lower pay as a result of the financial meltdown.

They view the stock market with suspicion, a behavior that is unlikely to be overcome. Not that many have much to invest anyway after paying for ever increasing student loans, healthcare bills and rents.

Central banks will be in the market for a long time to come. Who else will buy the stocks coming out of boomer’s 401k plans?

The millennials saw their parents lose houses, jobs, and savings. They are a cynical bunch and now Bernie has made them even more cynical.

My Aunt, who saw the same things as you describe Petunia from ’29-’34, could never understand why anyone was in the stockmarket in 1990. She never got over it. Maybe TPTB could convince the boomers to sell everything and buy the market, or maybe they won’t be given a choice(financial repression).

My impression is that many people of my generation (Gen-X) have left the stockmarket for good after being hit by the madness around 2000 and the years that followed. But the Millennials seem to be speculating a lot in the stockmarket, although the amounts of money are probably small. All they know is that the market (central banks) always has your back.

Maybe the plan is to make the Millennials rich enough through a booming stockmarket to have them splurge it on boomer homes ;-)

Yes, the outside shock will be third World War and nothing else.

Only such mess could clean central banks balance sheet.

Until then stocks will go up to infinity, mark my words.

Central banks divorced with logic long time ago and it works fine for them.

I don’t get how a world war would clean cb’s balance sheets. Make everybody bankrupt and reset? That didn’t happen the last two times…

‘I don’t know what the weapons of the Third World War will be but I know the weapons of the Fourth World War: Sticks and stones and bows and arrows.’

Einstein

This is pretty optimistic by the way, it assumes there will be bow and arrow makers

If your biggest fear about 20, 000 nukes is bankruptcy you are REALLY an optimist.

They did not stop the 87 crash. They did not stop the 2000 crash. They did not stop the 2008 crash. What makes you think they will or can stop the next one? They can’t stop it and it will come.

sounds very similar to the pension system in Netherlands which is relatively well funded.

Our funds are still assuming 8-9% yearly returns, and while the central bank and some independent economists state that those returns are extremely unlikely for the future, the boomer generation together with trade unions and consumer organizations does everything they can to paint a rosy picture for the pension funds, so they can receive their golden pensions (which they feel ‘entitled’ to but never paid for) for a bit longer. Damn the young workers who will receive nothing by the time they retire, and damn future taxpayers who will probably have to rescue the pension funds of government workers. Cutting entitlements is not an option, although a few private sector funds have cut pensions in recent years.

Just like in the US, politics and central banks have been forcing pension funds to invest massively in ‘safe’ government debt that yields nothing. They have also been working for some time on regulations that encourage the pension funds to invest in mortgages for private homes, which is also a high risk, low return investment in the current situation. but in this case the included government put option proved too outrageous even for the EU financial authorities (the Dutch government wants to guarantee that the funds can never lose on this investment, just like they do this for private homeowners – without this guarantee the funds won’t bite, maybe they know there is a problem under the rug?). Even if stocks keep climbing 10% per year the pension funds will be in big trouble within a few years because there other investment cannot yield anything for years to come.

One year ago I was at a hotel pool in Tucson and spoke with a couple from Netherlands. They told me the government guarantees a household income of $42k/year if you lose your job and you have an indefinite time period to get another one. No wonder the population believes in government promises. Life is secure. Nobody will rock the boat.

The problem with pension plans is not that the stock market will fall, but that it will rise.

Pensions don’t just earn money, they pay benefits. It’s not the fund values that are a problem, it’s the CONTRIBUTIONS. Most US corporations with pensions have contributions of 1/2 to 1/3 of what they need. Every year they pay benefits as if they are 100% funded.

Look at UPS. They owe their pension $8 billion and their internal ROR is 8.75%. If they reduced their ROR assumption to what Ray Dalio said the real long term ROR is, they’d be insolvent. They ALREADY, because of idiotic stock buybacks, have negative tangible book. It gets worse every quarter.

If the stock market fell, the long term ROR assumption would rise. This would allow companies to retool and future contributions would have more value.

Meanwhile, the S&P 500 is up 10% in 14 days!!!

Like whatever happened to the good old days that when companies do well on their bottom line, stocks go up, when they do poorly, stocks go down. Not the ludicrous shit show we have today.

Last time I checked, CALPERS and CALSTERS were some $300 billion underfunded. A good friend of mine retired from a high ranking police position at the age of 57 and receives 99% of his highest year’s earnings (well into 6 figures) which “spiked” his last year by cashing in unused sick and vacation pay. He is actually making more retired than when he worked! Like many of his colleagues, he promptly moved to TX and pays no state income tax, denying CA the opportunity to at least get some tax revenue for the beleaguered taxpayers. I keep hearing this system is unsustainable, but the union owned politicians will not tackle this issue.

California will mirror what is happening in Illinois. The State and local governments and public unions will put the squeeze on the taxpayer to make good on their platinum benefits.

Its really too bad the sheep here roll over every year for increased taxes and bonds.

well…now we have Pokemon Go……….so everyone can go virtual…and not care one whit about the downsides of real life…..right??

“panem et circenses”

“panem et circenses”

Yes…. in spades !!!

Leading the sheep to slaughter, 21st century version:

Pokemon Go and sponsored locations

“Small retailers are already experiencing a surge in sales from Pokémon Go players who might need a slice of pizza or a drink as they hunt nearby creatures.”

http://qz.com/732339

Will stocks crash ? I am not sure. Even the Venezuela Stock Exchange, although now 20% off, reached its all-time high in February 2016.

Zimbabwe’s stock market soared during its hyperinflation period of 2008.

A determined central bank can destroy the economy before stocks crash apparently.

To me hyperinflation looks the most likely outcome now. What else can central bankers do ? It’s too late now to let the system self-correct through deflation.

In what currencies were/are these stocks denominated? If that currency loses its value rapidly, stocks would have to skyrocket just to stay flat in real terms.

In their respective local currencies, confirming your observation about staying flat in real terms.

The point is, I think, that central banks can keep stocks at high valuations until these become meaningless through hyperinflation.

There was a two page bit about Venezuela in the Vancouver Sun today.

Worse than you can imagine. The lead photo was a huge crowd run across the bridge to Columbia for a rare permission to cross and stock up on basics.

Note: Columbia, not a part of the developed world is now a shopping mecca for once high fliers.

Everyone spends hours per day in lineups- and these lineups are jungle land. One time thugs robbed a kid of his cell phone, shot him, and no one left their place in the lineup.

One lady is doing ‘well’- she’s started a lineup biz, renting chairs, cell phone chargers etc.

The scramble is for toilet paper, tooth paste etc. but above all for food.

Bring a handkerchief if you are heading to a funeral- embalming supplies have run out and refrigeration may not be working ( power)

Meanwhile former bus driver Maduro blames the CIA etc. while former Uruguayan president ( and socialist) describes Maduro as ‘mad as a goat’

Is there a coalition of Latin American states that could get involved?

I don’t know.

So I will throw a monkey into the works. The very much overlooked affect and effect is the Russia/China oil and gas relationship. Russia never forgot the $8.00 oil that the USA orchestrated to crush the USSR ( which (had nothing to do with Reagan). China has no love for the USA either. ( Getting harder to have friends).

Look at what China did today, flood the world with cheap gasoline out of nowhere. Did anyone see that coming? I am not sure anyone even knew China was refining except may be the Kock brothers.

Between Russia and Iran, they can flood the world with cheap fuel, cheap oil as China ‘the cheap source’ with their preferred trading status. How would the USA handle a flood of cheap fuel…well, it sits in New York harbor right now, so lets see.

The resources these three have and potential to turn the West upside down by massive undercutting of fuel, must be considered. You can be sure Washington is concerned….why else line Russia’s borders with troops? It is still all about resources folks and getting them.

The stock market can not survive such a shock s as if some independent entity. Think about $30 oil, 1.25 gas, 0.50mcf LNG……It is all dominoes, and this will be the mother of them all.

$1.25 gallon? To feed my Avalanche tank? I’m lovin’ it.

….cheap oil would be fantastic for consumers and domestic manufacturing in the US. But China and Russia undercut Saudi? Not likely…

Russia is rolling out the red carpet for Kerry to sort out Syria. It seems the Russians have had quite enough playing with Assad, they want to go home.

Russia produces approx 10 million bbl/day petroleum, the world uses close to 95 million. Russia is at peak production and has been for awhile. China uses approx. 10 million bbl/day and produces approx 4.5 million bbl/day. China refines slightly higher levels than she consumes (just over 10 million per day). Between them, there is not one chance of flooding the world with excess capacity.

The easiest explanation of the so-called oil glut is as follows. LTO (Shale) and Cdn Tar Sands need about $80/bbl to turn a profit, for most operations. However, they receive about $40 for their product. Bitumen, much less. Their debt has increased and fixed costs have been reduced as much as possible, already. They are still losing money with every barrel produced. The lower the price, the more oil they try and produce to keep the bills paid with cash flow. Production continues to increase while losses continue. It is self-reinforcing and will only end with depletion of completed wells.

Right now, the world is consuming oil at 10X the rate of new discovery. The day is looming when yearly declines of 4-5% will be upon us. That will not be a good time for the stock market or for society. Some say this will occur before 2019. It all depends on the state of the economy. It will be very sobering.

I continue to be amazed at how many political narratives there are explaining oil price crashes, when in fact there have been dozens, going back over a century.

One of the biggest was shortly after the first real gusher, Spindletop.

There was at this point no huge automotive demand ( 1905?) and the stuff quickly became a nuisance- dropping to a negative value.

The last crash has all kinds of explanations (Washington wants to topple Putin etc. etc. ) except the one that explains all previous crashes, demand and supply.

Stocks are worth the net present value of their future cash flows .The lower the interest rate the higher the resulting P/E’s

Todays ridiculous rates result in pension funds earning a small amount on the bond portion of their investments .In order to reach their assumed rate of return ,pension funds will have to make more than expected on the stock and alternative investments portion of their fund.Is this possible ,Yes.Probable ,NO

Shortfalls will result in higher contributions

… but those higher contributions will not work well for the real economy.

So again, the only trick to keep this charade going means hyperinflation is the endgame. I guess they hope to take their time with this, or maybe they are confident like the Bernank that they can dictate inflation rates as they like and the real economy will follow ;-(

“Stocks are worth the net present value of their future cash flows ”

No Sale.

‘Predictions are difficult, especially about the future!’ or something like that.

How about Herb Stein’s quote

If something can not go on forever ,it will eventually stop

Will Stein eventually be wrong? If one thinks so, then one has a future in central banking.(:*)

It’s simple:

2000 and 2008, there were still Mom and Pops to rob from i.e. giant wealth transfer through the stock market.

At this point, you can only rob from the state itself.

P/E’s are meaningless, share buybacks have seen to that. GDP is manipulated to hell, so Price to Sales is your only meaningful measure

Sounds stupid but maybe stocks will not crash.

If the USD continues to strengthen why won’t money flee to US dollar assets?

If NIRP continues in Europe and Japan why wouldn’t money flee into the USD & US bonds? Perhaps then the bond trade would become so crowded that some $ would divert into US stocks looking for protection from a deflationary – rest – of – the – world?

The question in all this is what specifically will break the cycle.

It used to be that the bond market would go on a buying strike and force rates up (for sovereigns or companies) to a level where the market get paid a fair, risk adjusted return.

That cannot happen anymore now that CBs have shut down real price discovery by buying almost anything in sight – the (short)sellers are all gone.

When you have a player with unlimited funds sitting at the table, you´ll get your head handed to you if you´re trying to force down prices drive up rates.

But, when CB´s can buy anything they want from a computer keyboard, in any amounts they want, that disciplining mechanism beaks down.

CBs as quasi bond market vigilantes ? I don´t think so – those assets will be on the CBs´ books and will stay there as far as the eye can see – lest they want to depress asset prices.

Imagine the market reaction if the CB´s announced that they will ¨normalize¨ rates, by liquidating 10% of their balance sheets (without sterilization) ? There would be bedlum in equity and debt markets, and they would have to withdraw their offer faster than you can spell JYFF (Janet Yellen flip flop).

The assets the CB´s put on their balance sheets are ¨gone¨. Gone., Forever. No longer available. Locked away. Replaced by cash. Liquidity. Reserves. Whatever you want to call printed money.

Best of all, nobody (seemingly) gets hurt. The CB´s just continue to do it, all in the name of the public interest (minus savers, pensioners/pension funds – but who cares).

So what gives ? When will the whole house of cash come down?

SCENARIO I – ENOUGH ALREADY

Let´s see: there is a glut of cash and increasingly scarce income producing assets. At some point – and that may be YEARS AWAY – the market will (up)rise and say: we don´t want more cash. We have cash oozing from our balance sheets. We don´t know what it is worth, what it will buy – in fact the cash we are holding is starting to cost us money (NIRP).

So, Drahgi, we understand what you would like us to do, but we have enough of what you´re pitching – we don´t want or need more cash. We don´t need it, we can´t value it (in terms of a claim on current and future resources – how much for a Big Mac in 5, 10, 50 years?). Go take your keyboard and play in the backroom.

SCENARIO II – THE RETURN OF THE BOND MARKET VIGILANTES

As Japan shows, a BOYCOTT OF CASH COULD BE YEARS AWAY because the tidal wave of good intentions keeps finding new assets and asset classes to backstop: €150 bn here (for the Italian banks), €410 billion (after Brexit) FROM THE BoE, Helicoptor cash in Japan – all pacifiers that will keeps things going longer than anyone would have thought possible.

What will bring about a crash is that current buyers of NIRP paper are relying on a rise in prices of that paper – that is the only way that they will earn a positive return.

To put it in slightly more colorful terms:

¨Yeah, I will buy your stinking negative yield paper, but only if I make 5,10,15% annually on price appreciation of that paper. ¨

CB´s have to effectively guarantee continued capital appreciation for investors to buy paper that otherwise invariably loses them money.

Problem is that to keep that ¨promise¨, the banking system will effectively bleed to death because negative rates don´t work for most banks´business model.

Nobody buys 50 year swiss bonds for their negative yield to maturity. Nobody, except Mario Drahgi.

Investors won´t buy them, if they don´t have an implicit (through front running) or explicit (policy statements) assurance of capital appreciation that offsets the negative yield to maturity ?

So, the hamster has to run faster and faster to make good on that promise to NEW buyers of negative yield paper.

THE TRIGGER GETS PULLED

In the end, the promise of capital appreciation on NIRP/Zirp paper can no longer be kept – because rates have dropped to the point where the whole banking/pension system is at risk – and the music will (suddenly) stop because bond buyers face the prospect of REAL negative rates (i.e., the loss to maturity is no longer outweighed by profits from capital appreciation)

So, if and when the capital appreciation slows down or flattens is when the music suddenly will stop. And Central Banks will be relegated to trading with each other because nobody in the market can figure out the future value (both on a trading and purchasing power basis) of the ´assets´ they create with a few keystrokes.

The banking system and the bond market are on a collision course. The confidence trick by the CB´s is to let there be no doubt whatsoever that they will drive rates lower.

Can’t fight the Fed, the ECB, the Bank of Japan and everybody else. The bears are correct and poorer for it. A moral outrage leading to nothing good.

I started the process in 2010 to close my client’s defined benefit pension plan, which had been in place since 1978. When I read that CAT and IBM were closing their’s, I knew that a 100 person company could no longer carry its plan.

The basic problem is not the cost of annual funding. It is the burden that the plan has to earn money to cover pay-outs. This is an investment risk. And, a company, which manufactures machinery, is not in the business to make stellar portfolio investments (even if the like of Merrill Lynch are coaching the company).

In 2014, we terminated the plan and paid a hefty sum to cover the shortfall in cash. Most employees elected to take “in kind”, meaning that they took their allocate share of the fund portfolio. Others, elected to take an annuity, the after-age 65 payout of which was pathetic. The rest took cash and paid the pre-payment penalty.

So, what has happened since then. Well, the company now matches, in cash, the employee’s cash contribution to his/her 401-k. Of course up to a certain Dollar amount of W-2 income. Guess what: 30% of employees make a matching contribution of $0.00. That means no company match for them.

In 2015, the company’s cost of pension-matching is less than 70% of the cost in 2014. But that is really not gist of the message. The gist is that the company matches with cash and has no future liability. It is up to the employee to do or die with his 401-k investment decisions.

One point about Market Cap/GDP ratio that I never see pointed out (and maybe it’s me who misses the point here): There are many companies that no longer have public markets for their capital stock. How are these accounted for in the ratio (if at all)? For example: For a long period since 1987, the market value of RJR/Nabisco was zero, yet the company still accounted for over $20 billion of GDP. This number reduced the value of any market cap index for many years before the company sold stock back into the public markets.

Also: Cyclicality of some industries does not always show a line-up between market cap and sales for that industry, which can also cause the ration to be slightly off.

My conclusion: The indicator works only in long-term analysis, and does not necessarily mark any turning points in market values.

Kevin, in this article as well as in most cases that I know of, the Market-Cap/GDP Ratio is based on the market cap of the S&P 500 stocks, as the chart says. So these are 500 big companies whose shares are publicly traded. They’re liquid and trade frequently during every hour of the trading day. So market-cap data on these 500 companies is available at all times.

If a company is no longer publicly traded (has been taken private or goes out of business), it is replaced in the S&P 500 by some other company that is publicly traded.

If an S&P 500 company is acquired by another publicly traded company, the acquired company’s stock is removed from the S&P 500 and is replaced by some other company. And so on.

This measure doesn’t reflect total value of US corporate shares, public and private. I don’t think there is an accurate measure out there. It would have to include companies like Uber that do not have a “market cap” but some “valuation” set by a handful of investors and company insiders. And it would have to include the value of the shares of my own tiny company, and millions of others like it, and that would be impossible to do. Hence the practice of limiting the ratio to the S&P 500 companies.

And that makes sense, since this is a measure of stock-market over/under-valuation. So you need to look at a representative sample of the stock market, which the S&P 500 fulfills.