Consumers Finally “Getting on with Their Lives” as Credit-Card Debt Slaves: Equifax

Equifax, which profits from the process when more people apply for credit and load up on debt, sees the miracles of the current economy this way: “American consumers continue to show signs they are recovering from the Great Recession by steadily increasing their credit card debt….”

In its report on credit card debt, Equifax raved about these newly empowered American consumers that are once again buying things they can’t afford and charging these purchases to their credit cards because they didn’t have enough money to pay for them otherwise, given their stagnating salaries. It shows up in the numbers:

Total credit card debt rose to $634 billion at the end of the second quarter, a 5% jump compared to $604 billion a year ago.

That’s nationwide. And 5% is a big gain, given that there was supposedly zero inflation over these 12 months, and that the economy over the last four quarters has grown at the blinding speed, based on the newly re-rejiggered methods of figuring GDP, by a whopping 1.8%.

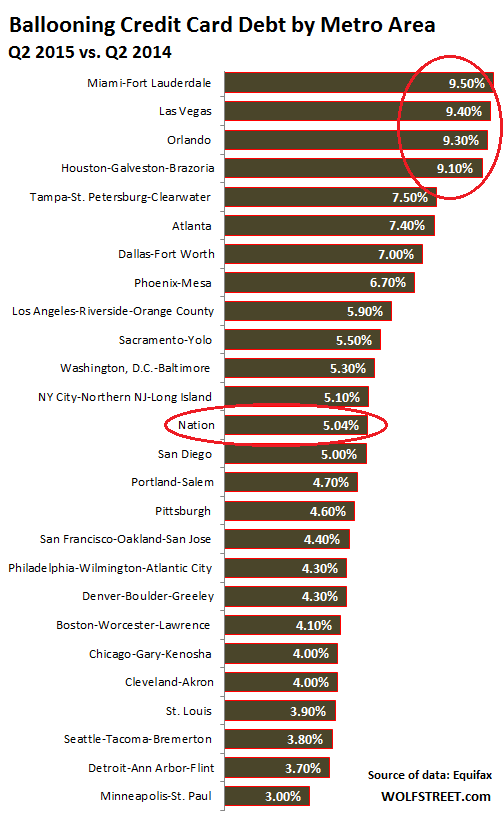

But in a number of cities, credit card debt soared far beyond the national average. And in a few, the rate of growth is not only accelerating, it’s going through the roof. Equifax was practically giddy:

The rate of growth in credit card debt more than doubled year over year in many of the metro areas hit hardest by the housing market crash, and more than tripled in other cities less affected by the crash.

Even the credit-card-debt laggards among the metro areas are finally getting into the mood: in Detroit, the rate of growth of credit card debt – not total credit card debt – soared by 222% from a year ago, in Phoenix by 308%, and in St. Louis by 317%. These folks are really making an effort.

This is what we’ve all be waiting for, finally, the true recovery of the American economy when people once again borrow to the hilt to buy imported gadgets or clothes, when they charge even food to their credit cards, and rent payments, and certainly healthcare expenses, and when they charge down payments on their cars to their credit cards… in short, when they try to make up with debt what their stagnating salaries cannot deliver.

It’s once again the era when American consumers live beyond their means, slither ever deeper into the glorious condition of debt slaves, all in order to crank up the economy and make it grow at, well, that measly 1.8%.

“This suggests that consumer confidence in the American economy is growing across the board,” Equifax sums it up – even as consumer confidence is plunging – aptly equating “consumer confidence” with sinking ever deeper into credit card debt. So it may not be confidence that’s driving this, but desperation or necessity.

At any rate, the credit-card debt binge is picking up speed:

“Every major market has seen increases in credit card debt, even those cities where the housing market issues are not completely resolved,” the report said, given that Housing Bubble 2 is now even more magnificent on a national basis than the prior one that turned into such splendid debt-fueled fireworks, though there’s a bitterly ironic twist this time [read… What’s Left of the American Dream Withers at Record Pace].

The importance to the economy of this consumer binge on expensive credit card debt cannot be underestimated. Equifax:

This shows that American consumers are more confident about their financial futures, and that means the U.S. economy has entered an expansion mode.

Consumers are doing the greatest job in Miami, where total credit-card debt soared 9.5% from a year ago, in Las Vegas (9.4%), in Orlando (9.3%), in Houston (9.1%). These are the cities where consumers have been most actively engaged in cranking up the economy by buying things they can’t afford. Here is the growth of total credit card debt in the largest 25 metro areas:

This is the final effort in the debt-fueled “recovery” of the US economy. Companies have gorged on debt. The federal government has piled on the most debt at the fastest rate ever. State and local governments, despite any balanced budget requirements, and even public pension funds have loaded up on debt. And consumers have been binging on debt to buy cars and get an education and buy homes at a feverish pace. Outstanding auto loans now amount to over $1 trillion. Payments are routinely extended over 72 months. Loan-to-value ratios have jumped. And automakers have become outright ecstatic.

What had been missing? Consumers charging up their credit cards. Now finally, the US economy has jumped over that hurdle too. Equifax explained in its eloquent manner, “These trends suggest that American consumers are getting on with their lives.”

The lives as debt slaves. Because they can’t maintain their standards of living with their stagnating household incomes. This too was part of the movie we’ve seen before.

But not everything may be this rosy. At first, it’s a sampling error, a statistical fluke, or the weather, but suddenly it’s serious. Read… Americans’ Economic Confidence Gets Mauled

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Forgive me for being ignorant, having never had a credit card in my life, but aren´t interest rates on credit card debt extremely high? In the barrage of adverts that the issuers of such cards publish in all fora they seem to typically operate with 15%-20% annual interest rates. Does this mean that Americans are paying between 95 and 125 billion dollars in interest each year?? How on earth could that be positive for anyone?

I don’t have stellar credit (just went through a foreclosure) but I have had a card with USAA for years (over ten?) with balance anywhere from zero to max and my rate is 9%.

While I doubt this is the normal behavior of others, I prefer to cash checks and hold hard cash versus deposit checks or pay some debts off. I take an interest rate hit, but all my debt is unsecured (except a four digit debt on an old truck – couldn’t pass up the deal).

Regards,

Cooter

But even assuming a rate of 9%, the fact that Americans have a total of 634 billion $ in credit card debt (quoted from the article) would mean an astonishing 57 billion in interest annually! And the brother part of that borrowed sum is spent towards consumption. Talk about an extra tax! 190$ for every man, woman and child in the US per year, that could otherwise have been spent on anything, if folks just had the patience. No wonder this Equinox entity is happy. I hope for you guys´ sake that you turn your back at this usury at some point.

You are not ignorant but right on. What is good for Equifax is not good for the average American. Neither a borrower or lender be……

Wolf, this is simply explained……Whole Foods no longer takes checks.

But wait… the amounts and percentages in this article are about outstanding credit card debt. When you pay with a credit card for convenience and pay off the statement every month, it doesn’t add to the outstanding credit card debt. It’s not an interest-bearing amount. (If you pay off your statement every month, there is no interest due.)

Outstanding credit card debt is the total amount of credit card balances that people owe, carry forward, and have to pay interest on month after month.

Ok, then it becomes less drastic. But hang on… since all those who pay down their balance before interest is applied effectively get free credit, does that mean that the whole business model is based on fleecing those hapless souls who mismanage their balances?? A $634 billion Candy Crush scheme?

I think you got it :-]

Everything you charge on a credit card is extended credit, even if you pay off your balance monthly. It is free to you but the merchant is really paying the interest for you through the credit card fee, which can be as high as 3%. If all the people who use credit or debit cards went to cash, the cost of doing business would decrease for the merchants and maybe they could afford to lower prices.

So let´s face it. Whichever way you twist and turn it, credit card use is a quite significant tax on households and businesses, the only benefit of which is to enrich issuers and boost sales figures in the short term. Brilliant. It´s huge here in the UK too, only I have never had one. I cannot for the life of me see the point.

I’m not surprised that credit card use is up in the cities where the foreclosure crisis was the worst. Most of those people had to declare bankruptcy which stays on your credit report 7 years and then drops off. Then you can reapply for credit and start again. I get credit card offers daily and my credit is not good due to foreclosure.

The Federal Reserve shows total US revolving debt at 901 billion as of May,2015 so I guess Equifax only counts major credit cards ( Visa/Master Card) and misses single store cards like Target, Macy’s, Mohammed’s Convenience Stores etc.

I’m also not getting those bank offers to transfer my balance that used to clutter my mailbox before the GFC of 2008 though maybe my demographics have deteriorated or improved, whichever makes me a better target for the banks.

Then again, there is the possibility that 7 years after 2008 those that had defaulted on their mortgage, credit cards, Helocs and what have you have now

been ‘rehabilitated’ by the credit agencies to the point they are now re-eligible for another credit card.

The Fed also includes other consumer revolving debt, such as credit lines, that are not attached to credit cards. But I don’t know how much of a role they play (not a big one).

Equifax’s numbers never match the Fed’s numbers on any category, whether it’s outstanding auto debt, credit cards, etc. It seems they’d come up with the same numbers, but they don’t :-]

You can go to companies like Lending Club and refinance your CC debt at a lower fixed rate if you want although the term is also fixed.

But that’s the point I made in the other thread i.e. Amerikans spend no matter what their confidence level is so confidence is a poor indicator at best. Perhaps we just need to accept that the business model of Amerika is companies financing consumers and that this model still has ways to live yet.

Moi? I had credit cards through thick and thin (i.e. unemployment while seeking another job) and gradually ran up the balances to over 30,000 and they gave me yet another increase in my credit line. My main card was charging me 29% interest on my debt which meant /I could never hope to pay it off. I tried to talk to them to be more reasonable but they wouldn’t hear of it. I felt I had no choice but to declare bankruptcy. Based on my financial situation, I paid off 30$ of the debt over several year and that resolved my debt for good. I never again touched a credit card though I don’t miss them as debit cards can do nearly all the same things. Years later, I got a mortgage on a decent house and made payments for 8 years. When my financial situation worsened I just sold the house rather than risk foreclosure and pocketed the loot and moved in with my father who was in hi 80’s and appreciated having Number One Son around to keep him company and help him out.

I love my debit card but credit cards are the temptation of the Devil(Hissssss, come on, you know you want it! Just sign here……”

it used to be that credit cards were issued very sparingly and warily only to the most solid credit risks and then only if they really needed one. what they are doing now is like fully legalizing heroin and assigning major corporations to peddle it. The first hit i free with a complimentary syringe. It will feel really good, but then……………

Equifax gets the Lawrence Yun Putting Lipstick on a Pig Award.

Fed up with those crappy old 1080p flat screen TV’s, Americans are using credit to upgrade to 4K even though they can’t afford it. And while they’re at it how about a new car financed at 120% LTV for 84 months?

The good news is that credit expansion is inflationary, which should warm the cockles of Ms Yellen’s heart. The bad news is that bad debt written off is deflationary.

I wonder who is buying those subprime auto loan CDOs? Well-bribed pension fund managers, maybe?

I like most of the analysis on this site, but what do you mean specifically by this: “The federal government has piled on the most debt at the fastest rate ever. “? My understanding is that the federal deficit has gone down quite significantly in the past few years, are you adding other line items to that?

As Michael mentioned, there is a difference between debt and deficit: the annual deficit has gone from catastrophically high to somewhat less catastrophically high. So it has gone “down,” though it’s still a big deficit. But the debt (the accumulation of all prior deficits) that is now owed by the government is totally gigantic. It has gone from $8 trillion to $18 trillion in ten years. It’s not going down anytime soon.

Here is a chart of the US gross national debt through the last fiscal year. Make sure you’re sitting down:

http://wolfstreet.com/2014/12/02/us-national-debt-jumps-181-billion-in-two-months-hits-18-trillion/

Thank you, that was interesting and instructive. As a dual Canadian-American, living in Canada with about half of my resources in each currency and no mortgage, I find your various analyses of both the short-term and long-term outlooks very informative.

Wolf, to my mathematically trained eye the graph’s curve looks like an exponential growth rate.. the cardinal character of an exponential growth rate is it increases by a constant percent of the total amount per unit of time. Think of compound interest, which is a good model of exponential growth. Does the U.S. debt over the long term increase by a roughly constant percentage? Then it has exponential character. Exponential growth starts out, often for a long time, as very slow and the graph looks nearly flat But then all of a sudden it starts moving steeply upward and it just explodes. In fact, exponential functions are the standard model for explosive phenomena, from a stick of dynamite to an atom bomb. Now if the percent annual rate of increase is not holding steady but actually increasing, then you have a hyperexponential rate and that is really bad news!

Terminology. The deficit is the difference between revenue and the spending in a given year. The debt is the total deficits from prior years.

Wolf – The area that I live in was not covered in the the top 25 metro areas in your chart. Is there a more extensive list somewhere that would show credit card in smaller metro areas? Thanks in advance!

I’m sure Equifax has the data, down to the street, but it didn’t publish the data. I don’t know where to get detailed data like that, without paying for it.

I am Canadian, and at the top of this site is an ad for General Motors 2015 Clearnce sale…0% for 84 months, and as I write this, there is an ad just beneath this for Capital One Credit Cards with the tag line “Great Selection of No Hassle Cards”.

There are no borders when it comes to credit and debt and how the average person is living these days.

Use of credit at no cost to me, and with that wonderful cash rebate of 2% to 5% is a plus. As I pay the balance in full each month, why should I not use them?

It is the ones who do not pay the balance each month who finance the dividend of the stockholders of Mastercard, Visa, and others. (Bless ya)!

The merchants have built in the cost of credit to their pricing, few places where I am offered a discount for CASH. Dam few places, but I keep asking. Sometimes there is a discount for cash (perhaps an unrecorded sale?) who knows. I get a token return either way I guess.

Firearms for some reason are discounted for cash, whether local, online, or gun show. Sellers typically pass along the credit card fee.

Dear Retired Boomer – I too am a retired Boomer…

I get 4% cash back on all “Grocery Store” and “Gasoline”, 2% back on “recurring bills” things like my Internet, hydro, etc., and 1% back on everything else. I have NEVER not paid the card in full and therefore pay no interest costs.

My card costs $55.00 per year – as of the end of July my “earnings” are at $422.00 I’m up $367.00 with half a year to go. I seriously don’t understand how come everyone doesn’t do this?

It’s literally free money – at least to me – some merchants and those paying interest to Visa at 29% are paying me a yearly average (the last 10 years) of just over $600.00 – that’s $6,000.00 in my pocket in 10 years. You’d be a fool not to do it.

obviously if most people did that then you would NOT be given such favorable terms. Yobviously if most people did that then you would NOT be given such favorable terms. you would get no cash rebates and you would have to pay some kind of fee for paying off your balance in full. Obviously that is not what most credit card holders can do. They have to build up balances during hard times (which are more and more frequent) to keep from ending up destitute and hope they can pay off the balances in good times (rarer and rarer).

I am glad you are doing well and what you are doing is very wise. /Congratulations! You should be proud. But most people are not that well off anymore, especially families with children with their constant crises and costly responsibilities. Please try to understand. ^,..,^

Interesting how the first 8 line up almost perfectly to underwater town USA.

I’m a retired boomer too. And I also am fortunate enough to be able to pay of any CC use monthly. And I only use CCs for mail order purchases. So, I don’t even know what the interest rates are on the cards I use.

But the article sure explains what I see going on where I live. When you consider the median income here compared to the preferred lifestyle, liberal use of credit is the X factor. So here we are again with a healthy modern consumer driven economy. People buying crap they can’t afford with money they don’t have. Another game of financial musical chairs. I guess it’s all good, with the usual caveat that nothing bad ever happens.

NT – Was not the band playing as the Titanic started to sink?

I also pay my one cc in full each month and have 99.9% of the time since 1985 when i got the card. The few times i didn’t, the interest was so punitive I swore “never again”!

I have a lot of younger friends (20 and 30 (somethings) and I see what they are up to. The ones that use credit cards to buy fancy stuff are usually in a financial position to do so and use them to smooth over cash flow issues so they can handle the payment over an extended period of time without missing the rent and the utilities. This really is what credit cards were meant for. My friends are mainly working class and lower middle class and some came from significant poverty. They grew up witnessing their parents’ struggle with financial problems and are not stupid when it comes to money. The ones who get in trouble are those who use credit cards for survival. You have an accident or get sick and you lose your job and get wiped out financially. Then your choice is between adding to your credit card debt or watching your kids go hungry or getting thrown out in the street if you don’t pay the rent. It is this kind of credit card debt that is in the long run going to be the dire problem. I know from personal experience that that kind of debt tends to never get repaid and you end up with debt peonage.

Corto, your analysis is spot on. Of course by coming to Wolf Street you’re sort of ‘preaching to the choir’. The only credit I have open is an overdraft account which I never use and a credit card for emergencies on the road as I am an OTR trucker and occasionally have to rent a car to get home for a funeral or some such. On vacation I put a charge on it and paid it off when the bill came. Cash oddly enough is becoming a “barbarous relic” in its own right, but I keep some “under the mattress” in case of a Greek style bank holiday. Good hearing from the UK!

I have been thinking of getting some silver bars and keeping them in a safe deposit box. The price has really come down. Given a crisis sufficiently dire, money may not retain its value but silver always will.

Yes in small and larger sizes only issue is it must be brought at the right/LOW price.

You need some copper as well people always need change this is another reason why gold is a pain, the 1 OZ value is simply WAY TOO HIGH to be usable.

In a cash crisis the value of metal rises, who has change for an Effective $1200.00 + coin

Who has change for a $1200 coin? The guy selling a dozen eggs for $1250. ?

In the non-hyperinflation scenario silver is probably more fungible. However gold is the more concentrated form of wealth. Crossing the border with $20,000 in gold requires a decent sized shirt pocket. Crossing with that much silver requires a back pack and part of that will go to pay for your hernia repair. You can hide thousands of dollars of gold in a funeral urn labeled “Mom” and sit it on the mantle in your den. With silver you need a laundry basket.

Silver is also an industrial metal and that can affect the price in a direction opposite to that intended as a store of value.

I keep chickens and ducks with my neighbor I will sell you eggs for 1250 dozen.

Silver and copper along with lead and tin are industrial and minor currency metal’s, which increases in value in times of stress.

Gold is a rich mans toy. nothing more.

Silver and copper are the oldest coin metals and serviceable.

You used gold to buy horses and guns, and copper to buy food, and will again.

Well that’s certainly a unique point of view. Let’s see . . . how much gold are China and Russia accumulating and how much silver? Is Germany repatriating gold or silver? Did the State of Texas, at the urging of Kyle Bass, purchase a huge amount of gold or silver? Was Bretton Woods about gold or silver? Did Nixon close the gold window or the silver window? Did the Federal Reserve Act require 40% backing of Federal Reserve Notes with gold or silver?

Feel free to substitute copper, lead, tin, nickel or whatever else you like for silver in those questions. And let me know how you plan to store $10,000 worth of copper at $2.35/pound, tin at $7 or lead at 77 cents. The only copper and lead you need is in your ammunition.

Yes, gold is definitely just a rich man’s toy.

Gold = Hype.

When it comes back to under 300 Oz where it belongs, maybe, untill then its all hype and hot air. In any form of cash crisis it is useless.

india is the biggest annual consumer of it, ask the indian gold dealers.

I was taking to one this afternoon, they will tell you it is for hoarders, who loose on it, every time they sell it.

It is big business in india today, as the state is continually debasing the currency. The smugglers and dealers of it are making a fortune. Yet not putting their personal reserves, in gold.

this quarter Capital One increased their provisions for bad debts by 21%. I realize that with Capital One, they have subprime car loans also, but it would appear to me the use of credit cards is caused by desperation, and not consumer confidence.

Most of my friends in the Portland, Oregon seem to be getting hit with rent increases of 20-30%.

They’re not getting raises. Most of them live paycheck to paycheck, so they are using credit cards to cover the increases in their monthly expenses.

This won’t end well…