Stock market participants and the players around them cling to every word proffered by the Fed that might reveal its secret plans because everyone knows that the words from the Fed and the money it prints and the interest rates it sets have been the fuel for the stupendous rally that started over five years ago. Wall Street wrings the last drop of hype and hope out of these words and spins them and doctors them to rationalize ever higher stock prices.

But recently, there has been one word that has moved up on the central-bank public worry list. As so often, it did so in a coordinated manner, and within days, it cropped up at the Fed, the Bundesbank, the Bank of England, the ECB….

“Complacency.”

It’s a condition of super-low volatility where the markets have become a one-way ticket to heaven, when market participants think that asset prices can only go up, that stocks will always rise, that a 4% decline is a correction, that even the worst junk bonds won’t ever default, that inflation doesn’t exist – and no one demands being paid for the risks they’re taking on because there are no more risks. Just look at the VIX volatility index, or fear index as it’s called: it has descended into a state of somnolence.

Central bankers are now worried that this creature of their making – this happy state of complacency amidst gorgeous and plump asset bubbles – might cause the next crisis. They’re worried that no one will be prepared for when it all turns around.

Alas, beneath the surface, stocks have already turned around.

Volatility is already tearing into stocks, and those holding them outright, rather than safely out of view in some confidence-inspiring fund, have watched “wealth” and dreams go up in smoke. But they know their formerly red-hot darlings will soon reach new highs, and that’s when they’ll sell them to a greater fool, and so they’re hanging on by the skins of their teeth, and others are buying because complacency still rules the day.

LinkedIn skidded 40.6% from its 52-week high, Twitter 57.5% in five months. It’s not just a few fallen angels. The Russell 2000, which tracks the 2000 smallest stocks in the Russell 3000, is down 9.1% from its 52-week high. The FDN Internet Index 16.1% in three months, the NBI Nasdaq Biotech index 16.5%, the Social Media Index SOCL 24.4%. Stock after stock has taken a brutal licking, papered over by the Dow and the S&P 500 whose components, the largest companies in the US, have largely held up so far. But beneath them, the Fed’s illusory “wealth effect” has begun to reverse.

And just as these stocks were coming off their peaks in March, the one thing that wasn’t supposed to happen, happened: margin debt, after having spiked for months, declined.

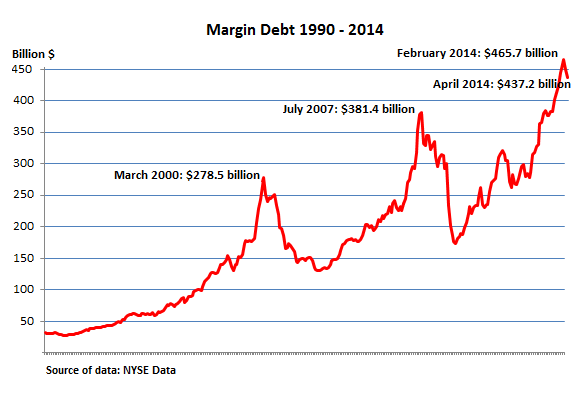

Margin debt – newly created money that is plowed into stocks – is the great accelerator on the way up. It inflates values and increases leverage, and when it spikes, it performs miracles. But it has a terrifying habit: after going into a majestic spike, it reverses abruptly right around the time stocks crash.

Over the last 15 years, margin debt had three spikes and reversals:

The first spike peaked in March 2000 at a record of $278.5 billion, or 2.66% of GDP. By the time it reversed in April, the stale air was hissing out of stocks with epic speed.

The second spike peaked in July 2007 at $381.4 billion, or 2.60% of GDP. In November, stocks began to swoon. No one will ever forget what happened next.

The third spike – the most phenomenal yet – peaked in February 2014 at $465.7 billion, beating the prior record by 22%. It reached 2.73% of GDP, the highest ratio ever! In March, the spike reversed. And in April, it declined again.

And it’s forming an increasingly terrifying chart:

Margin debt is down 6.1% from its February peak. $28.6 billion was drained from the stock market in two months, rather than added, as it might have been the case during the spike – a difference of $57 billion. And the dough that was yanked out isn’t piled up on the sidelines either, waiting to be plowed back into stocks. It was used to pay off debt. It simply evaporated.

During those months, the former red-hot darlings have been eviscerated, and thousands of stocks have skidded in sympathy. It’s brutal out there. But hey, the VIX is asleep, volatility isn’t visible from the top, complacency rules, and to heck with the last two times this scenario played out and blew down the whole flimsy construct.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

![]()