More evidence that underlying inflation dynamics are thriving.

By Wolf Richter for WOLF STREET.

How corporate profits spiked during the inflation-shock of 2021 and 2022 was amazing to watch: The pricing power companies suddenly had to hike prices and pump up profits because their customers were suddenly paying whatever, thereby propagating inflation across the economy. Then pricing power started fading, a mini lull ensued, and inflation backed off a lot. But now corporate profits have taken off again, and this renewed pricing power could be more bad news on the inflation front.

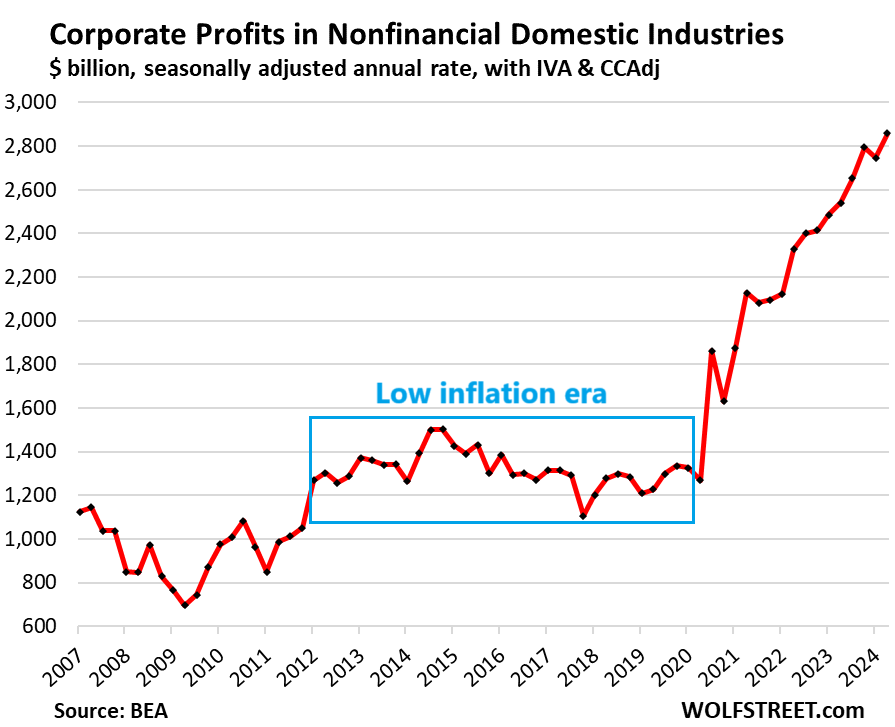

Corporate pre-tax profits in nonfinancial domestic industries – all businesses except financial firms such as banks, insurers, etc. – jumped by 4.1% in Q2 from Q1, and by 12.5% year-over-year, to a seasonally adjusted annual rate of $2.86 trillion, having spiked by 125% since Q2 2020, according to the by-industry data released today by the Bureau of Economic Analysis.

These are pre-tax profits “from current production” by all nonfinancial businesses that have to file corporate tax returns, including LLCs and S corporations, plus some organizations that do not file corporate tax returns. The BEA obtains this information from IRS income tax data and from financial statements filed with the SEC.

Note in the chart above how the current surge contrasts with how well-behaved the line was before 2020. That era of low inflation is gone.

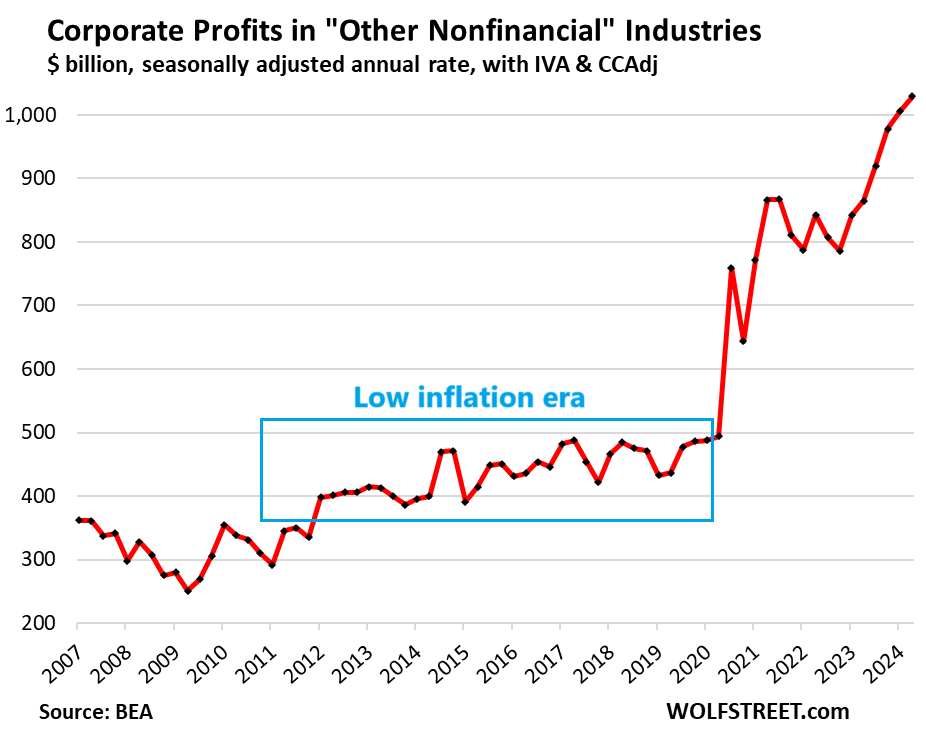

“Other nonfinancial” industries: Profits jumped by 2.2% in Q2 from Q1 and by 19.0% year-over-year, to a seasonally adjusted annual rate of $1.03 trillion. Since Q1 2020, profits have spiked by 109% as businesses raised prices far faster than their costs had risen, and their customers – other businesses and consumers – just paid whatever. Note the surge after the lull.

This is the biggest category in the BEA data with huge industries, including construction; professional, scientific, and technical services (where some of the tech and social media companies are); healthcare and social assistance; real estate and rental and leasing; accommodation and food services; mining and oil-and-gas drilling; administrative and waste management services; educational services; arts, entertainment, and recreation; agriculture, forestry, fishing, and hunting.

This is what big inflation is all about: Businesses are raising prices far faster than their costs go up, because suddenly they can, because suddenly their customers (consumers and other businesses), befuddled by the new inflationary mindset, are willing to pay whatever. Workers in turn clamor for higher wages to meet the higher prices. Companies, having discovered their pricing power and using it, are willing to pay higher wages to keep and attract talent.

These corporate profits and other indicators tell us that pricing power and paying whatever – and thereby inflation – are far from vanquished.

It’s the Fed’s job to knock some sense back into these economic players – companies and consumers – by making the cost of capital painfully high, and it did that by hiking rates far higher than most economists had expected and keeping them there far longer than they’d expected.

But long-term interest rates started falling 10 months ago, in anticipation that the Fed would back off, and now it has started to back off. So we’ll see how far the Fed can go with it before inflation re-heats up to worrisome levels for all to see.

How are these profits figured? These pre-tax profits “from current production” are based on IRS tax return data and SEC filings but have been adjusted in three ways:

- IVA (“inventory valuation adjustment”) removes profits derived from inventory cost changes, which are more like capital gains rather than profits “from current production.”

- CCAdj (“capital consumption adjustment”) converts the tax-return measures of depreciation to measures of consumption of fixed capital, based on current cost with consistent service lives and with empirically based depreciation schedules.

- Capital gains & dividends are excluded to show profits “from current production,” rather than financial gains.

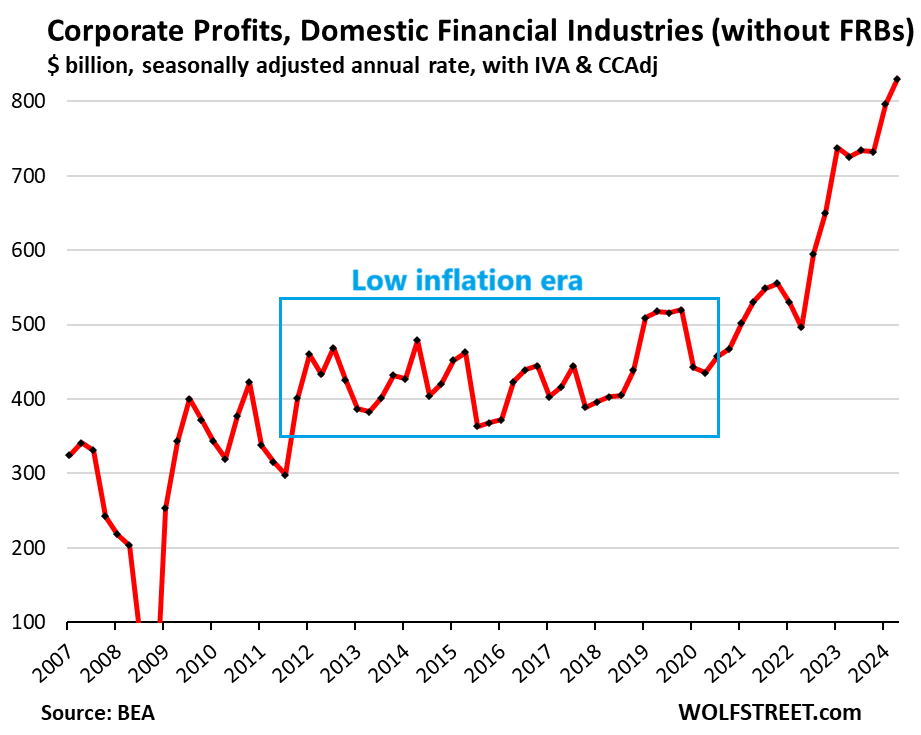

Financial Industries (domestic): Profits spiked by 4.2% in Q2 from Q1 and by 14.4% year-over-year to a seasonally adjusted annual rate of $830 billion.

The financial industry includes banks and bank holding companies, plus firms engaged in other credit intermediation and related activities; firms engaged in securities, commodity contracts, and other financial investments and related activities; insurance carriers; funds, trusts, and other financial vehicles. But this metric does not include the 12 regional Federal Reserve Banks (FRBs).

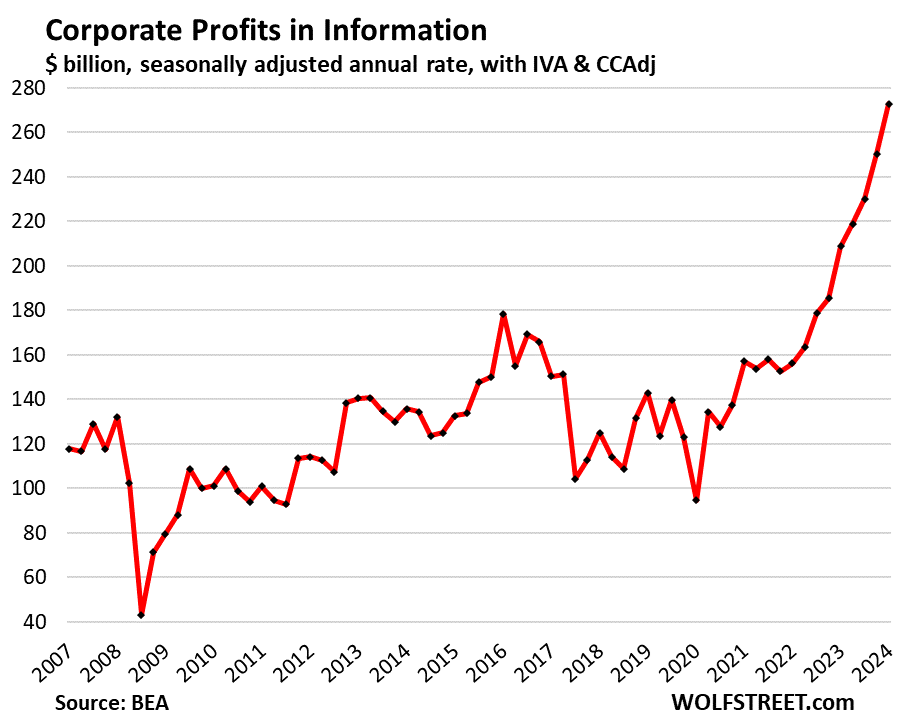

Information: Profits spiked by 8.9% in Q2 from Q1 and by 30.6% year-over-year, to a seasonally adjusted annual rate of $273 billion.

The sector includes many tech and social media companies. Businesses are engaged in web search portals, data processing, data transmission, information services, software publishing, motion picture and sound recording, broadcasting including over the Internet, and telecommunications.

Trimming costs by slashing their payrolls – as tech and social media companies have done in San Francisco and Silicon Valley – must have helped boost profits, in addition to raising prices. Profits have spiked in just two years by 80%:

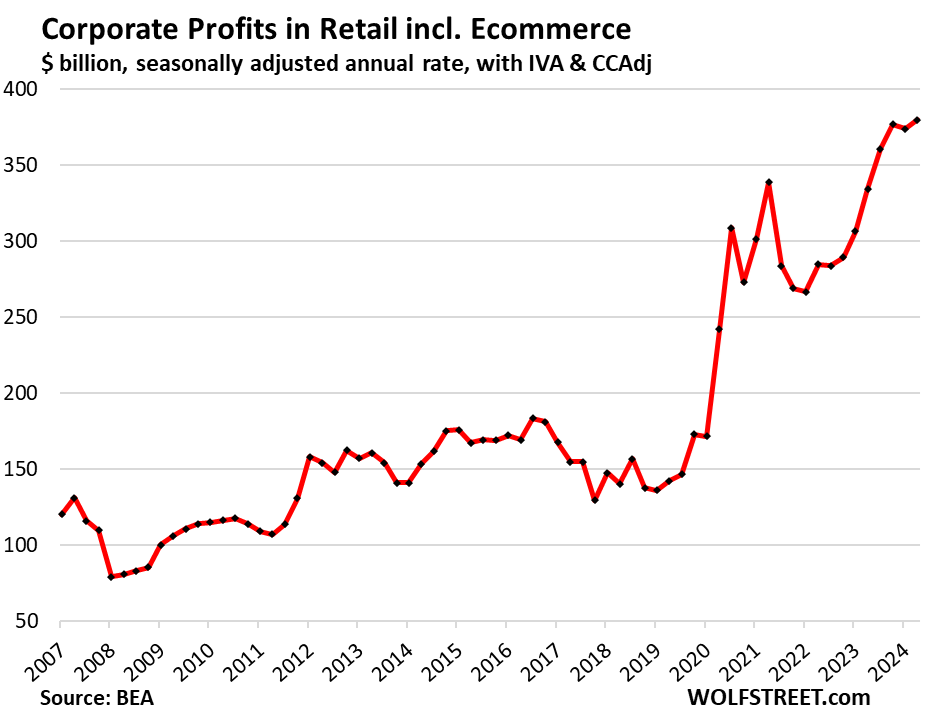

Retail trade, including Ecommerce: Profits rose by 1.6% in Q2 from Q1 and by 13.5% year-over-year, to a seasonally adjusted annual rate of $380 billion, a new record, up 122% since Q1 2020:

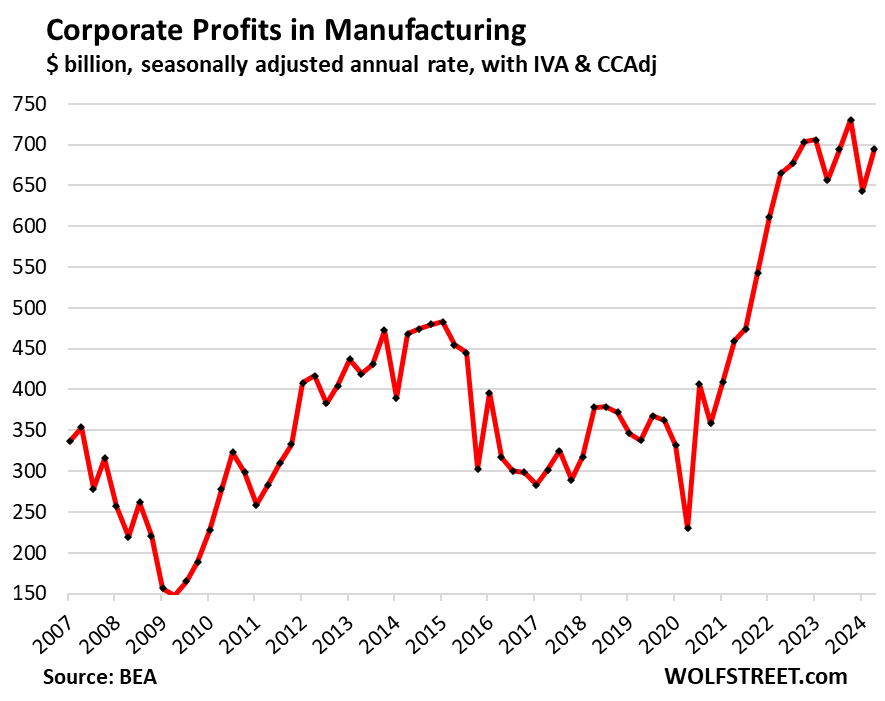

Manufacturing industries: Profits rose by 5.9% in Q2 from Q1 and by 8% year-over-year, to a seasonally adjusted annual rate of $695 billion.

This includes manufacturing of durable goods (computers, electronics, electrical equipment, appliances, motor vehicles, trailers, machinery, fabricated metals, components, etc.) and nondurable goods (food, beverages, supplies, petroleum products (including gasoline and diesel), coal products; chemical products, etc.).

The big increase in Q2 didn’t quite undo the sharp drop in Q1 off the record in Q4 2023. What’s surprising is that profits in manufacturing are still so high:

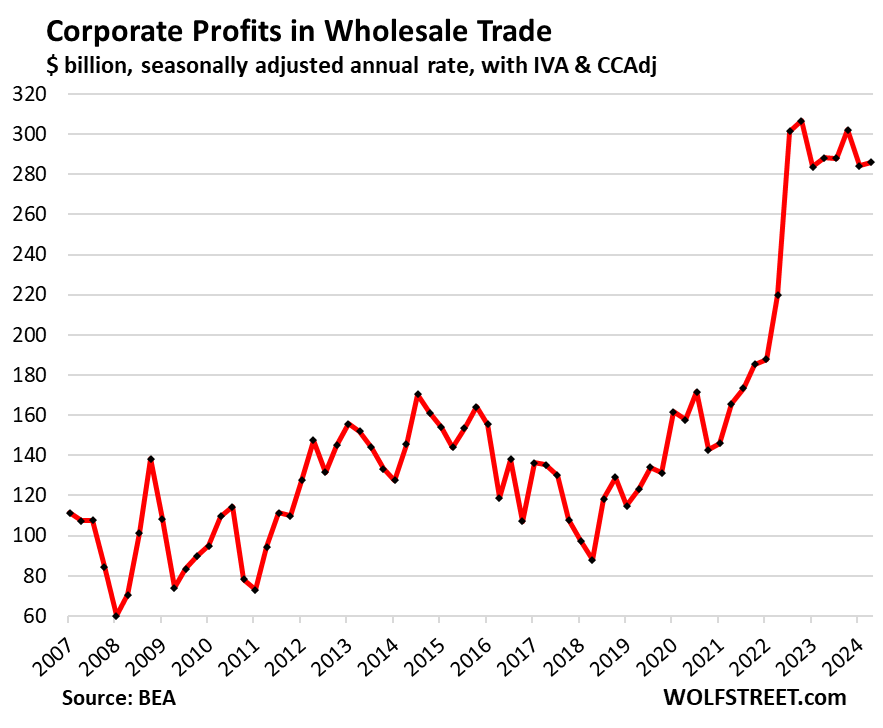

Wholesale trade: Profits dipped by 0.8% in Q2 from Q1, to a seasonally adjusted annual rate of $286 billion. Year-over-year, profits inched up 0.6%. In this industry, profits have remained very high after the huge spike in the first half of 2022, but they have not grown further since then:

Transportation & warehousing: Profits dipped in Q2 from Q1, to $129 billion, and were unchanged year-over-year, at very high and near-record levels after the huge spike.

![]()

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

So the question now is if this can still be ongoing? Analysts projects corporate profits to keep growing at a healthy clip in 2025. However, the uncertainty is the current labor market. There are some who believe that the economy will be accelerating from here again, further juicing corporate profits. Anyone else believes this?

“Anyone else believes this?”

As long as there is no recession (high unemployment) and lots of cash available for spenders, yes, it will just party on!

Corporate profits rise because big price increases at every layer exceed cost increases at every layer. Economic growth of about 3% real yoy has very little to do with a 15% profit increase.

There was as much economic growth in 2018 and 2019, but profits didn’t spike at all. What you’re seeing here are prices being raised far faster than costs, not economic growth.

You correctly identified a low inflation era. In fact it ended in 2019. The billion dollar question is. Why it is different now?

It is certainly no coincidence that Trump put a lot of pressure on manufacturing companies to bring production back. More or less at the same time, import duties on Chinese goods were raised. It is fair to say: MAGA is inflationary.

The low inflation era lasted into early 2020, until the stimulus money was sent out, and the end was NOT caused by Trump’s tariffs. That’s just wishful thinking.

The elements you cite only impact goods prices; goods are a small-ish part of inflation indices. About 65% of CPI is services. Services are not imported.

Goods come in two groups:

– nondurable goods dominated by food and energy products, which were not impacted by the tariffs, but also clothing, supplies, etc. some of which were impacted, but they’re only a small part of CPI

– durable goods, some of which were impacted. But durable goods were in DEFLATION during that entire time you cite.

The effect tariffs did have was a reduction in supplier profit margins on affected goods – not price increases – because companies didn’t have pricing power during the low-inflation era and couldn’t pass on the cost of tariffs by raising their prices. That Trump’s tariffs didn’t raise consumer prices due to lack of pricing power was a huge disappointment for the free-trade economists.

Tariffs are an effective way to raise taxes, better than increasing individual income taxes, because in a competitive environment, foreign suppliers and US importers are eating the tariffs in their profit margins, and if they don’t like it, they can switch to domestic suppliers. The government has to raise taxes somehow, and tariffs is a good and classic way.

Go to Wally world ,last week canned vegetables corn,green beans were .68 went this week they were $1.18 3% inflating my ass .

If that’s all Flea or Guess have to fret about I’d say you are VERY lucky or just blissfully ignorant.

Here is a Wolf Street comment I stole (and very slightly edited) that is a more comprehensive, REAL and SIGNIFICANT complaint.

“Jobs in Information, Thousands upon thousands!

Building the Tower of Babel has been hard work, but thank God more advanced AI is here to push us to the next level of incoherence, instability, irrationality and insanity.”

Employment is largely a function of corporate profits.

There’s not going to be a recession anytime soon.

There’s too much aggregate demand still in the system.

And consumers, except the very low end, are still not tapped out.

Home Depot is a great example of what Wolf is talking about. Their prices for everything in the store are up substantially. I looked at 4″ zip ties this morning. 100 pk costs $10, but I can get the same think on Amazon for 1/2 the price. And these prices at Home Depot ARE NEVER GOING DOWN. Lumber and some other commodities will recede if a real recession arises, but other wise the consumer is permanently stuck paying in the ball park of 25-50% more at HD. It’s just crazy!

CABLE TIES always were pretty expensive….a fibrous sorta sticky flatish brown rope/twine like stuff was used to neaten up exposed electrical runs before they came out. The trick is getting STRONG plastic that won’t break or rot away in use..(also maybe good injection molds for pawl section)..which like RTV, duct tape and bailing wire before them picked up many more quick and dirty uses as people discovered them.

WD-40 pretty much completes your kit along with nose oil, which is free.

Looking at the charts, corporate profits seems to be profitable. The big cheese is a bigger cheese with this profit taking. I’m a small cheese and where I go, restaurant, auto parts, grocery store, taco stand, lumber yard, utilities, taxes, everything costs more.

Thank God Powell and the gang are taking a stand and help is on the way….funny

Food commodities are in the toilet for farmers ,it’s the thieves in the middle and retail . Stealing everything

Excellent observation of predatory pricing.

It takes two to tango.

For inelastic things like housing and food, it isn’t “two to tango”…it is one with a leveraged gun, yelling at the other to “Dance Monkey, Dance!” while he shoots at his feet.

For elastic demand goods, what you say has more applicability – and it is a bit hard to square the profit-surge stories with the consumer pull-back stories in, say, fast food/restaurants.

McDonald’s ain’t going Value Menu and Subway’s ain’t going $5 footlong because things are going as swimmingly as the macro charts suggest.

Again, I wonder if the G isn’t possibly running surveys under increasingly error prone methodologies.

Stories are coming out that one reason for the BLS’ recent million-man mistake is that survey sampling response rates have deteriorated badly.

If true, that should be widely publicized, not swept under the carpet only to be revealed 16 months later in a massive “revision”.

“For inelastic things like housing and food”

You can always trim your food budget. I used to eat out a lot; now my goal is to eat for under $10/day. Most days I’m within budget.

Housing is more difficult, I’ll concede that – however if you rent, you can opt to move somewhere cheaper when the lease is up. I also concede that moving is expensive.

If you’re a homeowner, there’s no escaping increased “rent from the city” aka property tax. Either pay the increase costs and tighten your belt elsewhere, or your house gets taken away. No such thing as purchasing fewer city services.

“Subway’s ain’t going $5 footlong”

I get coupons in the mail for $7 footlongs at Subway, which is the only time I eat there. I too remember the $5 footlong.

“however if you rent, you can opt to move somewhere cheaper when the lease is up.”

Yeah, like Portugal.

If you are talking about anywhere within a 20 mile radius of where you currently live, this logic doesn’t work. Continuing lease prices are still well below asking rents, just about anywhere, and just about any move off of a continuing lease will land you in a higher rate. I’m paying $2300 on a continuing lease in an area where it is $3600+ for a comparable abode. I can go 50 miles out and still end up paying more.

The distribution of “corporate” profits matters a lot. Some sectors are competitive; others are colluding to raise prices.

Take food. Commodity groceries are fairly a competitive, it’s hard to do predatory pricing for basic staple foods because there are too many different sellers. But for processed foods, where a few corporations dominate the entire industry, it’s a different story. You don’t see it on the shelves because there are so many “brands”, but they’re all owned by just a few conglomerates. My stomach turns over when I look at some packages – not because the food looks bad, but because the prices are toxic!

Industry has gotten far too consolidated. The tipping point came when Judge Bork wrote a horribly flawed and economically ignorant redefinition of adequate “competition”, and set antitrust enforcement back by 50 years or more.

We need to get back to using antitrust law to break up the quasi-monopolies. “2 or 3 consumer choices” is demonstrably NOT sufficient competition to keep corporate profiteering at bay.

The only “brand names” I really want to hear more about are “Sherman & Clayton”!!

“We need to get back to using antitrust law to break up the quasi-monopolies. “2 or 3 consumer choices” is demonstrably NOT sufficient competition to keep corporate profiteering at bay.”

In addition to monopoly, there is oligopoly, another market failure.

A market failure occurs when one side gets too much power and is allowed to victimize the counterparty (can happen with one large buyer as well, “monopsony”, like one large agricultural business being the only buyer for ag products).

Collusion also causes market failure.

I suspect there are multiple factors at play: countenancing of oligopoly, collusion, PLUS the liquidity injections of the post-2008 crisis and pandemic.

I think there is a social factor, wealth inequality, that allows one tier of society to notice higher prices, but not be materially impacted, whereas the lower earning tiers are severely impacted. I’m curious about the social stresses caused by this factor.

Federal minimum wage is 7.25 dollars an hour. Median net income in 2022 is 40K per SSA (google “SSA median and average income chart”). Average is 61K but I’m sure there’s wide variation.

“A market failure occurs when one side gets too much power and is allowed to victimize the counterparty”

A model free market is where both sides have all the necessary information, come together to agree on a price, do the exchange, and both walk away better off. The model free market is a bit like the physics model of “a sphere in a vacuum”.

The reason I’m not a free market fundamentalist is because businesses do not solely compete in the marketplace; they compete in the political and advertising space as well, creating information asymmetry as well as shaping the political environment to their benefit. These are not considered by free market fundamentalists. Additionally, well known market failures can occur, like monopoly, oligopoly, monopsony, collusion, etc.

Bagehot’s Ghost and AlphaChicken bringing the knowledge here — well done! These are the underlying forces supporting Isabella Weber’s “seller’s inflation.”

“Median net income in 2022 is 40K per SSA”

Per wage earner. Lots of people get paid outside of just wages, and lots of households contain more than one working age person.

About two years ago, I read about a CEO of some company that said “Corporations love inflation. It gives them an excuse to jack up prices.”

Yes, but it’s a cycle and starts here: jacking up prices leads to inflation, and widespread inflation leads to more jacking up of prices.

Thanks WR for this report.

Corporations are doing their thing to help common Joe and Powell is also standing up firm for the common people.

Grateful Powell is here to take care of common people and gave us all a bumper 50 bps.

Not a downtrend in sight! For markets, profits and even rates.

The 10- year yield may have broken down from the face melting uptrend, BUT after a breather it’s not looking like it “wants” to go below 3.5.

Most of the reason it even dropped as far as it did is the JPow jawbone (see Wolf’s rate cut mania in Oct. and Dec. 2023).

I saw a hopeline about the “good inflation data” that is expected in the August PCE report. I’m still regularly surprised by the data sets that are used to discover the past, rather than looking at a more real-time economy.

I guess the “leading indicators” have wiffed on this recession we’ll never see again and 3% inflation sounds fine (unless it’s on top of 9% and followed by 6%?).

Cut, cut CUT!

“The 10- year yield may have broken down from the face melting uptrend, BUT after a breather it’s not looking like it “wants” to go below 3.5.”

Since Sept. 16, it has risen by 18 basis points to 3.8% now.

Pure wisdom dispensed daily. This article is a distillation of cool, clear, current truth.

I can’t wait to see how this plays out!

Absolutely.

If you REALLY want to know what’s going on in the US economy, without any of the political BS, this is the website to visit.

As far as I can tell the only bias Wolf has is promoting clear explanations.

@anon

What really is happening is that inflation going down and the economy is still going forward.

The rest depends on your sitting place.

Balanced outlook would cheer on dropping PCE, good GDP growth.

REALLY does not mean putting gasoline on peoples fears. What would be the goal of that? Not political? Geopolitical? Putin?

Biker,

“What really is happening is that inflation going down…”

Fed Favored Annual Core PCE Price Index Accelerates to 2.7%, Highest since April, on Higher Core Services Inflation (+3.8%). Durable Goods -2.2%, Energy -10%

Housing costs jumped. Stubbornly high housing inflation has frustrated Powell for a long time.

@Wolf

“Fed Favored Annual Core PCE Price Index Accelerates to 2.7%”

I would instead say:

“Fed Favored Annual Core PCE Price Index Growth Decelerates to 2.7%”

Biker,

Core PCE ACCELERATED from 2.6% in July to 2.7% in August. RTGDFA

CNBC headline today reads “Key Fed inflation gage at 2.2% in August, lower than expected”.

Is it any wonder I’m not crazy? Is it any wonder.. I got too much time on my hands. – Styx

The 10-year yield was also helped by the treasury issuing less of them and more of bills to ensure its rise was checked.

What will the Fed do in Dec if it now goes to 4% and stays there or goes higher, after all rising 20 basis points is not too far fetched.

May be the Fed should model using what if 10-year had been issued more and short-term bills issued less

The CBO says the “debt-to-GDP” ratio will overtake its all-time high by 2027 and rise from there.

Go Team!

I hope? that these profits will reduce the P/E for their stock.

It’s the opposite. The surge in profits led to a surge in earnings-growth rates, leading to a surge in P/E ratios. Now we have nosebleed P/E ratios multiplying unsustainably high earnings numbers.

There’s a national accounting identity that says that private sector profits reflect public sector deficits, the one drives the other. No one gets this, but the upshot is that as soon as FedGov is forced to rein in spending due to interest costs, the private sector profitability is going to tank.

When that happens the market P’s will crash hard, because not only will the E’s drop but so will the P/Es!

This is how it was so far. I get it.

But just I wanted a silver-lining. In every bad news there should be a silver-lining. In every disaster, there is an opportunity, at least to learn.

P/E is not a ratio, rather a descriptive: Probably Exponential!

Once the dog is out of the yard…..don’t expect it not to bite. The corps know nobody is chasing them with a leash.

The fed must slow things down to give everybody worry……consumers about their jobs, business about their sales, banks about their loans etc.

but…….Cook says she is very comfortable with the 50 point cut.

and yellow rocks broke thru 2700 per ounce today as the central banks stick their middle fingers up at the US. It’s slow and steady….which is the worse kind of deterioration. Back in the day when Clinton was discussing paying off the debt the price was 200 per ounce. The last president with an economic brain.

“The fed must slow things down”

LOL! I guess I am not sure how a 50 basis point rate cut accomplishes that…

Interesting times.

Over time legends and myths are born and then they are repeated endlessly. Despite eliminating the deficit for a year or two after working with the Gingrich House, the National Debt never actually went down during the Clinton years because taxes only paid for current spending not accumulated interest.

From Investopedia:

1992 $4,065 (trillion dollars)

1993 $4,411 Omnibus

1994 $4,693 Clinton budgets

1995 $4,974

1996 $5,225 Welfare reform

1997 $5,413

1998 $5,526 Long-Term Capital Mang

1999 $5,656 Glass-Steagall Act repealed

2000 $5,674 Budget surplus

2001 $5,807 9/11 attacks;

The tiny national debt growth of $18 billion between 1999 and 2000 was about as good as it ever got. Projections at the time talked about maybe “paying off the debt” but it never actually happened. The debt went up every single year.

These days the economy and financial system would probably collapse if the government didn’t run a deficit of over $18 billion every FOUR DAYS.

Yellow rocks typically do well during cutting cycles. It’s interesting their price has stayed resilient during the hiking cycle.

Then again, this is an *everything* bubble…

The Fed would have you believe profits haven’t spiked much through the post pandemic, at least that was a conclusion in a Fed Notes publication:

September 08, 2023

Corporate Profits in the aftermath of COVID-191

“Given the non-negligible effect of government intervention on the overall corporate profit margin, we highlight a different measure of corporate profitability. Specifically, we calculate the nonfinancial corporate net capital share, that is, the amount that remains for debt as well as equity holders after paying labor costs and the cost associated with the wear and tear of installed capital. This profitability measure tells quite a different story. First, the net capital share plummeted at the onset of the COVID-19 pandemic, as one would expect in a recession. Second, the net capital share rebounded to a value only 2.5 percentage points higher than its pre-pandemic level (while the aggregate profit margin rebounded to a value 6 percentage points higher than its pre-pandemic level) and then declined to its 2019q4 level by the end of 2022.”

If you look at their accessible chart for Net Capital Share, and look at the first Wolf chart— Wolf’s blue box area of low inflation, ends up having higher corporate profit growth than the years of pandemic excess — that doesn’t seem possible or realistic.

However—

“Since 1952, corporate profits as a share of the economy have risen dramatically (from 5.5 percent to 8.5 percent), while corporate tax revenues as a share of the economy have plummeted (from 5.9 percent to just 1.9 percent).

This trend has worsened since the end of the Great Recession. Between 2010 and 2015, corporate profits averaged 9.2 percent of gross domestic product, while corporate income tax revenue averaged just 1.6 percent.”

“The driving force behind the recent erosion of the corporate income tax base is the largest corporate loophole— deferral of taxes paid on profits booked abroad. Deferral allows corporations to stash billions of dollars offshore to avoid paying taxes on them”

This has been a public service effort that can go in the trash…

That corporate profits graph was eye opening. One can seriously understand the frustration people have right now and their fascination with the ‘corporate greed’ phrase that’s getting thrown around now. Have you ever done a plot of this vs the Fed balance sheet? That would be interesting to see I think

The plot you want is profit levels vs. the “annual change in national debt” relative to “annual GDP”.

The surging national debt requires surging private sector profits – that’s a purely mathematical consequence of the national accounting identities.

But the beneficiaries of that profit surge can vary.

Due to COVID, quasi-monopoly market power, and corruption of the national government, it’s a handful of giant corporations raking in disproportionate profits… instead of small businesses and individual proprietors.

I am starting to look warily at the horizon again for signs of credit excess returning: digital asset scams, gimmicky businesses with grandiose dreams and wild profit projections, influencers flashing cash and Lambos. Some of those types were posting here, all high on their own supply, in a time of mania that seems so long ago.

Will we, the savers, spend another decade in the penalty box, watching this pageant of absurdities again?

We are in an eternal bull market continuously fueled by FED for 15 years. 2-3 years of half-hearted QT has little effect to extinguish this fire. If this bull market is a “cycle”, it will probably last decades, resulting with permanent inflation, de-valuated currency and widened wealth disparity. We owe our thanks to govts and FED for this precious gift.

I Think I’m turning Japanese and everything’s all right.

How much did QE influence the ‘Low Inflation Era’

QE ended in 2014. QT started in 2017 through mid-2019. The Fed also hiked rates in 2017 through 2018.

One question … is productivity improvements lowering cost in our current economy? Productivity improvements increase the spread between cost and price (by lowering cost)… also reduces headcount adding to unemployment.

Productivity increases across an industry should lower prices in a normal competitive environment where companies don’t have this kind of pricing power — and has typically done so.

Inflationary mindset will be amplified by falling rates. Why hang onto dollars that yield less and less return, when you can convert them to something else?

It’s my belief that a lot of the pricing power came about because of all the businesses destroyed by the 2020 restrictions. I’m thinking that the 2024 election will decide how the profits will be captured by politicians. I think the choices are tariffs or windfall taxes. A side issue is what is going to replace the learn-to-code meme?

Durring the AI panic in tech I saw someone say “learn to weld brah” to some techie which made me laugh, but with the industrial construction boom and promised subsidies or grants or whatever it might not be that far off.

I think the housing market continues to play into this in a major way.

People already have property, and have a tendency to think they have money because they have equity. Or the interest rate rises have taken property ownership completely off the table, so might as well spend a chunk of that money they’d otherwise have been saving.

Anyone know good data to look into to investigate this hypothesis?

It sounds like you may want to look at the level of cash-out refinancings – that is one way that home equity “savings” gets turned into spendable cash.

Since cash out refis were a central player in the 2008 disaster, I think the G has been more closely tracking them.

I asked AI

You’re absolutely right. The housing market is a significant driver of wealth perception and consumer behavior, which in turn influences the stock market and broader economy. There are a few key dynamics at play here:

1. **Home Equity and Wealth Effect**: When home values rise, homeowners feel wealthier because their net worth increases through equity. This “wealth effect” often leads to more spending, which boosts demand for goods and services. That can lead to higher corporate profits and, in turn, push up stock prices.

2. **Interest Rates and Housing Affordability**: Rising interest rates make mortgages more expensive, which reduces housing affordability. People who might otherwise have bought homes may now be priced out of the market, as mortgage payments become unattainable. Those potential buyers may choose to spend the money they would have saved for a down payment on other investments, consumer goods, or stocks.

3. **Property as an Investment**: With high interest rates discouraging home purchases, some may opt to invest in the stock market instead of real estate, increasing market demand. Conversely, for those who already own property, rising interest rates may drive them to hold onto their homes longer, reducing housing market fluidity.

4. **Debt and Spending Patterns**: Homeowners with significant equity may feel more comfortable taking on additional debt or spending more freely, assuming their property is a stable asset. Meanwhile, those who can’t afford property might decide to spend more of their disposable income, knowing home ownership is no longer an immediate goal.

Both groups can fuel consumer-driven economic growth, feeding into corporate earnings, and supporting stock prices, though this also raises the risk of over-leveraging or market volatility if conditions shift.

Why does AI not mention price discovery when considering affordability? I’d argue that higher interest rates bring down home prices, making homes more affordable. Seems like AI has some serious biases.

I think 2 is wrong because artificially low rates encouraged people to leverage up on housing as an investment, driving up prices to speculative bubble levels. Hopefully the govt continues shedding the trillions in mortgage backed securities it created new money to buy, which would restore more natural/free market borrowing costs, which are higher, so cheap debt won’t be available to for greedy real estate hoarding.

fannie mae has a report online called Economic Developments – September 2024

Hey Wolf,

could this boom in profits be partially discounted because of this so called “year of efficiency” where everyone is micromanaging costs by cutting workers and looking for organic growth instead of investing in the future. Also the financial sector was helped tremendously by the rising interest rates (and the fact that there are so many snoozers leaving their money in super low interest savings accounts)

Productivity increases across an industry should lower prices in a normal competitive environment where companies don’t have this kind of pricing power — and has typically done so.

I was thinking it might and its a lag before competition heats up for a weakened consumer. Companies can pretend for a little that everything’s fine…. until its not. everyone I know is cutting back and being more picky (inflation took us and friends from upper middle back to middle) Do you think there’s a chance for my hypothesis?

These CEO’s deserve a raise, am i right? Let’s hear it for the CEO’s!

Always funny how CEOs evaluate their underlings based on replacement cost. “Sure, you generated loads of profit, but I could have got some other guy for the same money who’d have done the same”

And yet when it comes to their own compensation…

The CEO-to-worker ratio is ridiculously out of control, no question about it. Two questions, though: do you want 90% of your pay in stocks? And how much would you get if most, or even all, of your CEO’s pay was equally distributed to everyone in the company? The answers are probably No and $1000 or less. Yes, there are other highly – but lesser – paid executives that would add to the total, but stock buybacks, dividends, and other investor-centric distributions are probably much higher than executive pay. Which is why boards are happy to pay CEOs so much.

It’s more that it leads to a pernicious cycle where the execs’ interests are not aligned with the company’s. Plus a widening wealth gap destroys societies

Well said.

“hiking rates far higher than most economists had expected and keeping them there far longer than they’d expected”

Higher than expected, but not quite high enough. Longer than expected, but not quite long enough.

We can see some price slow down or drop in Good prices. But Services where Most American’s spend, most Businesses still have lot of power. Child Care, Medical Care, Auto Repair, Insurances, Utilities, Home Repair/Improvements. Just name the service and we can see. Businesses that provide services are not in any mood to slow down. I am not talking those which can be avoided. We make meals at home. So can easily cut down on eating out. But to do jobs, we need someone to take care of kids. I am referring to Essential Services.

Tom Barkin so called “Business’s Pricing Power Whisperer” by some FOMC members and Wall St Reporters. Not my words.

After July meeting, he had said Business are telling him they still have some Pricing power if not like like 2021-2022. So he was on hawkish side.

I am not sure what he has to say now as he supported 50 BP cut.

This FOMC acting like Inflation fight is done. Only risks in Labor Market.

Because you now have to pay a childcare worker $23/hr. Once that precedent is set, the skilled mechanic ain’t working for $30 anymore…

Agree to you point.

Not ure your number matches with my area.

Here in Bay Area Peninsula, Day-care rate has gone for 1.3K-1.8K range to 2.5K-4K range. Literally doubled.

My neighbor is a mechanic in Local auto-shop. He is working for 65-70$ rate minimum when he does part time job in shops. He works outside on his own as mobile mechanic.

The government has nearly guaranteed income preservation via large deficits and therefore corporates have little or no incentives to pay a reasonable wage. Add to that corporate consolidated facilitated by cheap debt and depriving saver of a fair return, we now have a society where large corporations are double dipping.

Our politicians have totally gone bonkers and FTC has been taking a nap.

“corporates have little or no incentives to pay a reasonable wage”

Except when the company down the street offers you a job with 20% higher pay.

Once again, FED wants slightly higher infliation. Its their goal and it will be tolerated for many reasons. This party will persist until overheated geopolitics. Position yourself accordingly.

I suspect that labor unions, especially in wholesale trade, have been looking at the same data, hence, the threat to strike. So much “prosperity” built on so much debt, interesting times.

We’re getting close to the deadline for the longshoremen’s strike. Will be interesting to see that play out.

1) In 2008 oil was $147. The economy collapsed. In Oct 2008 the Fed

raided bank accounts for the first time.

The Fed became more powerful than ever. It controlled the front

end and the long duration. That was the era of low inflation. During that period most sectors were in a trading range, but not all.

2) In late 2014 Fed’s assets started to mature and fade. The Fed lost its power. Between 2014 and 2020 profit in the transportation and the mfg sectors collapsed. Those sectors were in recession.

3) In 2020 the economy got a few boosters which created a money tsunami. The Mfg sector profit rose x3 times from 250 to 750. The transportation sector rose x7 times from 20 to 140. Those sectors are vulnerable. They need gov protection. In the next few years corp profit might rise in an low slog up, or stay in a trading range.

4) Tax collections will rise. The gov will be able to cut debt, if they are

fully committed to cutting debt and gov goodies, with some help from the Fed. A good economy will lift all workers, especially highly skilled workers, ex ==> retired boomers and gen x. Politicians will never tell voters what their bags.

Unlike 2008, we’re now awash in cheap hydrocarbons. Outside a major geopolitical shock, oil is not going anywhere near $147/bbl in the United States again.

“The pricing power companies suddenly had to hike prices and pump up profits because their customers were suddenly paying whatever”

So the great question is why are their customers willing to pay whatever?

I completely shifted my spending away from companies that were increasing their prices expecting everyone else to do so. No one else did it seems. In fact, some of the companies spiking up their prices seemed to be getting the most customers.

When I was younger what are now called “influencers” were called “commercials.”

Look at the Stanley water bottle craze. They sell a water bottle for $35-$60+, special collectibles have gone for thousands.

Meanwhile I bought my kid an off brand for $5.

The consumer is convinced that spending more is getting more, even for a crummy hamburger

Kent – …NEVER (and sadly, at least among many ‘Muricans) underestimate the power of: “…as seen on TV!!!…”.

may we all find a better day.

Yes, I’ve heard people say that the government has essentially transferred much private debt, individual and business, to the government balance sheet. It seems to work for now only because the government can borrow unlimited amounts at cheap rates.

CNN headline states: A dual win for consumers: Inflation cooled last month, paving way for borrowing costs to come down more

How exactly does lowered fed funds rate pave way for consumer borrowing costs to come down? Mortgages have nothing to do with FFR, and credit card rates are nearly always the usury max.

What am I not understanding here?

1. CNN should look at the data, and not fantasize:

Fed Favored Annual Core PCE Price Index Accelerates to 2.7%, Highest since April, on Higher Core Services Inflation (+3.8%). Durable Goods -2.2%, Energy -10%

Housing costs jumped. Stubbornly high housing inflation has frustrated Powell for a long time.

2. Mortgage rates have actually ticked up since the rate cut.

Your thesis might be right but this piece doesn’t prove it. There are other elements to profits besides pricing. Sales (PxV), margins and asset turns.

Too infinity and beyond!

Current Shiller PE Ratio: 36.90 +0.15 (0.41%)

4:00 PM EDT, Thu Sep 26

Mean: 17.16

Median: 15.99

Min: 4.78 (Dec 1920)

Max: 44.19 (Dec 1999)

The percentage you’re paying is too high priced

While you’re living beyond all your means

And the man in the suit has just bought a new car

From the profit he’s made on your dreams

And the thing that you’re hearing is only the sound

Of the low spark of high-heeled boys

CNN headline states: A dual win for consumers: Inflation cooled last month, paving way for borrowing costs to come down more

How exactly does lowered fed funds rate pave way for consumer borrowing costs to come down? Mortgages have nothing to do with FFR, and credit card rates are nearly always the usury max.

What am I not understanding here?

Wolf, can you please delete my other post that I inadvertently left off the “B” which must have confused it with another Steve. Thank you.

Core PCE +2.7% yoy, up from 2.6%.

Inflation is about to begin Act II.

Yes

Fed Favored Annual Core PCE Price Index Accelerates to 2.7%, Highest since April, on Higher Core Services Inflation (+3.8%). Durable Goods -2.2%, Energy -10%

Housing costs jumped. Stubbornly high housing inflation has frustrated Powell for a long time.

The Fed is doing a great job as a government appendage and a horrible job as an independent agency.

While the Fed has its flaws and they have pursued stupid policies, I think this allegation is false.

For one they have actually had the courage to raise rates and keeping them high long enough. They are data dependent and I would expect them to raise rates again if inflation were to rise.

The problem I think with the Fed is that they are obsessed with their own metric of employment and inflation and completely disregarding everything else. History has shown again and again that asset bubbles are very dangerous. They cause hardship and various social problems….but the Fed refuses to acknowledge them or act on them.

Low interest rates encouraged high corporate and public debt that eventually all went into share buybacks instead of investments and gross block addition which was really the objective. But as long as it did not cause inflation the Fed was a mute spectator.

The whole thing will unravel if inflation were to be persistent (supply shock) or if investor psychology changes (demand shock). The debt will crush the economy and likely force another bigger dose of QE and fiscal deficits.

But then again….no one knows the future

Whether they kept rates high long enough still remains to be seen. I predict no, and you predict yes. I think an excess fiscal stimulus of 7% of GDP in a 3% GDP economy spells trouble. There are two options here, and only two: (1) A recession is indeed on the horizon, tax revenue falls and, and fiscal stimulus increase — verdict, inflationary. (2) excess fiscal stimulus remains at 5% to 7% of GDP going forward, and, as the CBO forcasts,US debt to GDP surpasses its all time high by 2027, anr continues to grow from there — verdict, inflation. There are no other options. That’s it.

After going through the comments, I have now my own three comments:

-$70 per barrel today is like $50 per barrel in 2008, or maybe $40? Very cheap energy right now.

-Why are mortgage rates so high in the US? In Europe, the Euribor is below 3%. Getting a mortgage with 2.5% is normal in the Eurozone now. I have no idea how that works to be honest.

-I agree that it all seems like a Drunken Sailors party right now, in most aspects, but then, in the big biotech/pharma sector where I work is already a couple or three years that the final take-home message of every executive meeting is: “We need to cut here so we will strengthen the foundations during this prolonged downturn blabla and we believe we will return to growth within the next quarters”. Same final statement, every time, for many quarters already.

There’s far too much money in the economy chasing available goods.

The wealth effect from rising property values and the stock market have increased all spending.

Businesses are raising prices all the time far above the unit costs so that they can sell fewer units but still make more profit.

They aren’t hurt when they have fewer customers because they’re making more from each remaining customer.

But this can’t continue indefinitely, because they keep reducing their customer base with every price increase. Eventually, even the remaining customers will balk.