Monthly payment of a 50-year mortgage of $500,000 would be only $91 lower than of a 30-year mortgage, but homeowners would get crushed by nearly $1 million in interest.

By Wolf Richter for WOLF STREET.

The Trump administration is proffering the idea of 50-year government-backed mortgages, like the current 30-year and 15-year mortgages. This may be a great idea for the mortgage industry, banks, shadow banks, and investors that invest in mortgage-backed securities, but it’s a very costly mortgage for homebuyers.

The small amount of payment reduction gets crushed by the huge amount of additional interest they have to pay. It would be the ripoff of the century.

Note that the principal portion of the mortgage payment remains your money; it’s like a forced savings account. But the interest portion of the payment is the bank’s money, the cost of the mortgage that makes someone else rich.

There are fundamental mortgage dynamics involved here, some of which can be seen by using online mortgage payment calculators. But to get the nitty-gritty, the way I’m doing below, you might have to build your own amortization schedule on a spreadsheet.

Longer term loans come with higher interest rates. Mortgage rates are determined by the mortgage market which is tied to the bond market. And mortgages with longer terms come with higher interest rates.

For example, per Freddie Mac last week, the average 30-year fixed mortgage rate was 72 basis points higher than the average 15-year fixed mortgage rate:

- 15-year mortgage: 5.50%

- 30-year mortgage: 6.22%

The difference between the two has averaged 74 basis points over the past five years.

So a 50-year mortgage would have a similarly higher mortgage rate than a 30-year mortgage compared to a 15-year mortgage.

For our example here, I estimate that the 50-year mortgage rate is 70 basis points higher than the 30-year mortgage rate. Using Freddie Mac’s average of 6.22% for 30-year mortgages, the average 50-year mortgage would have had a rate of 6.92% last week.

The monthly payment would only be $91 lower. Monthly payments of our $500,000 mortgage, at 5.50% for a 15-year, 6.22% for a 30-year, and 6.92% for a 50-year mortgage:

- 15-year: $4,085

- 30-year: $3,069

- 50-year: $2,978

- Difference: $91

So the 50-year $500,000 mortgage would have a monthly payment that is $91 lower than the $30-year mortgage.

But that $91 a month comes at a huge cost for homeowners.

Amortizing the mortgage over 50 years versus 30 years or 15 years means that the principal amount of the mortgage – $500,000 of our example mortgage – would get paid off in much smaller increments, and that therefore the interest portion of the monthly payment would decline much more slowly, with the effect that the borrower would pay much more in interest.

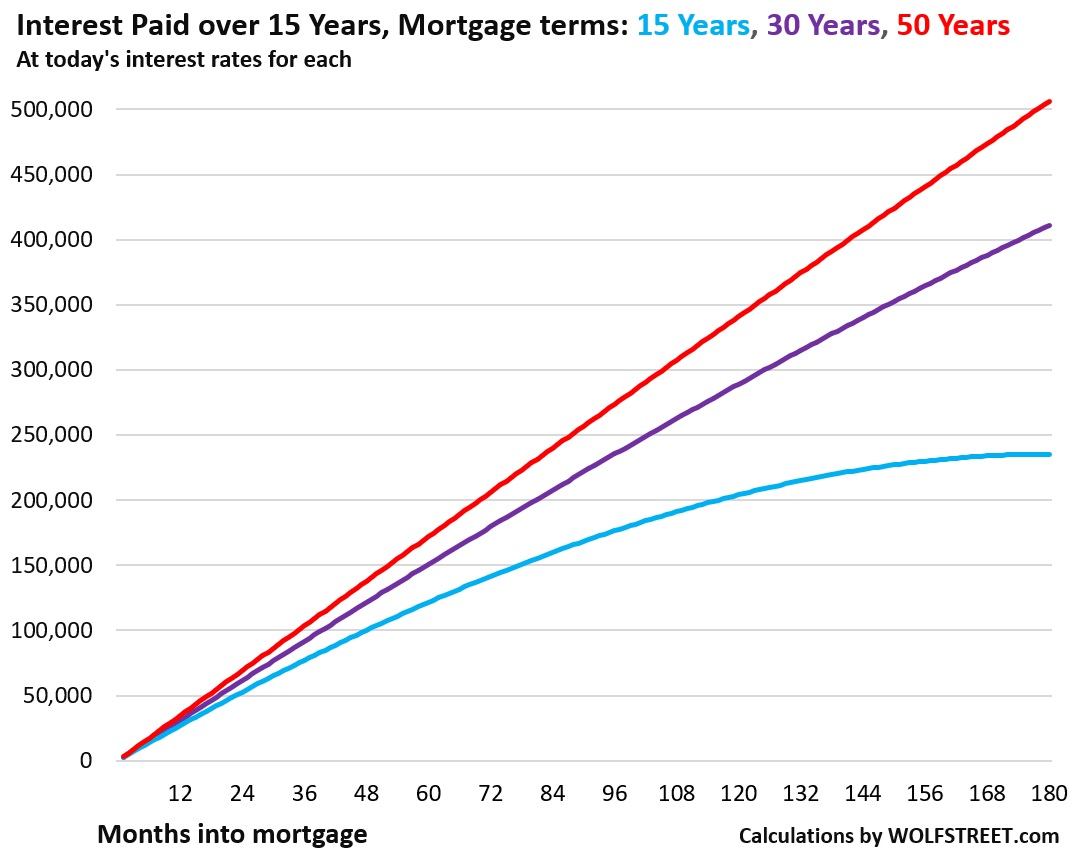

Interest paid over the entire term of the $500,000 mortgage:

- 15-year mortgage: $235,375

- 30-year mortgage: $604,779

- 50-year mortgage: $958,514

Even if the 50-year mortgage is paid off in 15 years, such as when the home is sold or refinanced after 15 years, total interest paid would be much higher.

Interest paid for our $500,000 mortgage over those first 15 years:

- 15-year mortgage: $235,375

- 30-year mortgage: $410,988

- 50-year mortgage: $506,261

In other words, over the first 15 years of the 50-year mortgage, the borrower paid more in interest ($506,261) than the original loan value ($500,000). That’s a lot of money to have handed over to the banks in 15 years.

With a 15-year mortgage, the borrower would have saved $270,886 in interest expense over a 50-year mortgage that gets paid off in 15 years.

With a 30-year mortgage paid off in 15 years, the borrower would have saved $95,273 over a 50-year mortgage that gets paid off in 15 years.

The chart below shows the cumulative interest paid over the first 180 months (15 years) of those three $500,000 mortgages: a 15-year mortgage at 5.50% (light blue); a 30-year mortgage at 6.22% (purple), and a 50-year mortgage at 6.92% (red).

After 15 years of payments, the remaining balance of the $500,000 mortgage would be:

- 15-year mortgage: $0

- 30-year mortgage: $359,800

- 50-year mortgage: $470,511

Even if the 50-year mortgage is paid off in 5 years, total interest paid would be much higher.

Interest paid for that $500,000 mortgage over those first 5 years:

- 15-year mortgage: $121,570

- 30-year mortgage: $150,649

- 50-year mortgage: $171,918

In other words, over just the first 5 years, the 50-year mortgage costs $21,269 more than a 30-year mortgage, and $50,348 more than a 15-year mortgage.

With the 15-year mortgage (light blue in the chart above), the curve flattens out 130, 140, or 150 months into the mortgage as the remaining outstanding principal of the mortgage shrinks every month, and so the interest portion of the payments declines, while the principal portion of the payments increases to where near the end of the mortgage, almost the entire payment is principal.

This flattening out of the curve also occurs with the 30-year mortgage but further in the future beyond the 180-month time frame of the chart. And it occurs with the 50-year mortgage, in theory, but the homeowner will likely die or sell the home before then and may never get there.

So this would be the deal at today’s mortgage rates. The 50-year mortgage would be an extraordinarily bad deal for homeowners, for a mortgage payment that is only $91 a month lower. And that $91 a month would do next to nothing for “affordability.”

What would help affordability is an unwind of the 50%-plus price explosion between mid-2020 and mid-2022, which has already begun in some of the bigger markets:

The 23 Bigger Cities where Condo Prices Dropped by 12% to 28% through September

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Yeah but what about a 500 year mortgage?

nah, too hard to market that, even 100yrs will be a tough sell, but take a page out of Patek Phillippe’s marketing, they can do a 100 yr mortgage and repackage it to you’re not the owner of your loan but just a keeper for the next generation and make it so it’s generational mortgage and your children and their children will “own” it…now that’s a sizzle you can probably sell

Oh I was just joking lol.

But this sounds like an even better idea!

“just a keeper for the next generation and make it so it’s generational mortgage and your children and their children will “own” it…now that’s a sizzle you can probably sell”

I thought along these lines too (ie, how this turd is going to be pitched to the public).

Simply continuing the financial manipulations, in order to lower monthly mtg payments regardless of impact on any other personal/societal financial measure, is just deeply, deeply sick and a symptom of a dying society and economy.

DC/Fed is scared to death of the inevitable reversal of the phony wealth effect their 2002-2020 ZIRPS ginned up (doubled/tripled home “values” despite close to stagnant HH incomes during a very large part of that period).

So they are desperate for some way to continue to prop up housing demand at irrational valuations – so behold the Ronco 50 year mortgage.

And Fannie Mae is eliminating the 620 credit score standard (I haven’t delved into the details, but it is all of a piece – desperately stripping away rational safeguards in order to keep hopeless bubbles inflated).

***Trump scribbling furiously***

Econ version of shoving UV lights or bleach down airways to “clean the Covid out”, based on some studies of table top cleaning…….by Dr Trump, the self-appointed polymath of our times.

If Trump endorses it the MAGA freaks will comply.

Actually the MAGA’s I know are all up in arms about the 50-year mortgage boondoggle. As in really, really mad. This along with all the sabre rattling on Venezuela and elsewhere when no one cares for yet another war, and Prez’s comments apparently supporting the despised H1B visa recently (on Fox of all places) have done something all the other scandals couldn’t, they’re finally enraging his base and turning them against him. It’s even showing up all over their social media.

These are the very things they voted for him on, especially bringing down prices for homes and health care. And they can see the corruption behind the 50-year mortgage as well anybody. Just a sop to prop up inflated housing costs a little while longer and fatten up how much the bank can extract for the mortgage like Wolf shows here,

“Interest Only” mortgages DO exist, though I believe they’re mostly for commercial properties.

Japan does the 100-year mortgage to ‘assist’ in affordability. Possibly or probably even the grandkids would be paying it off.

Personally I think if you need anything over 20 years you can’t afford the property. Look for something cheaper.

Where would that leave Tom Selleck?!!!!

Still beloved by old ladies (ripe for some more de-moneying) as;

“Such a nice man”.

Thank you for using realistic rates. Everyone else out there is comparing a 30 year to a 50 year using the same rate.

Why are those “realistic rates”? They struck me as the most non-sensical part of this analysis. Interest rates are typically much more sloped in the short end than the long end. That’s especially true of mortgages due to the embedded option.

Right now, treasury yields are as follows:

10y: 4.11%

20y: 4.68%

30Y: 4.70%

So it makes sense that the 15Y mortgage would be lower than 30Y. But the curve is basically flat 20Y and out. There’s no way a 50Y mortgage would be 70bps higher than a 30Y unless it’s due to some sort of market technical.

I’m not a fan of a 50Y mortgage. Not for any mathematical reason, but rather that mortgages represent a “forced savings plan” for a lot of people who are very bad at saving. In theory, people would apply the savings from a 50Y mortgage to their investment accounts, and they would do just fine, but we know that’s unlikely to happen (or it will happen on a low delta). They’ll just spend more. Mortgage principle repayments enforce a form of savings discipline on the average Joe (putting aside those who jail break with a HELOC).

You have no idea what you’re talking about. The comparison with the 20-year Treasury bond is clueless.

So let me tell you:

1. The 20-year Treasury bond was introduced in 2020, and that yield at the time was 25 basis points HIGHER than the 30-year yield because there was little liquidity for a 20-year Treasury bond because none existed. So for several years, due to these liquidity issues, the 20-year auctions were kept small, and the yield at auction was higher than the 30-year yield. In recent months, some of the liquidity fears have eased, as more 20-year bonds are out there, and the 20-year auction yield has now dropped below the 30-year yield. In October, the 20-year went through the auction with a yield of 4.506% while the 30-year went through at 4.734%, a spread of 23 basis points for an additional 10 years despite whatever remains of the liquidity issues.

You cannot use the 20-year Treasury bond as an example because it’s a new bond with liquidity issues.

2. Also:

20 years difference between a 10-year and 30-year Treasury.

20 years difference between a 30-year and a 50-year mortgage.

The 20-year Treasury doesn’t even fit in there at all.

So go look at the spread between a 10-year and 30-year Treasury (=20 years additional): 58 basis points. Duh!

Wolf, would it take an act of congress to force banks to adjust amortization schedules that woyld be more beneficial to the borrower? Say a 50/50 split over rhe early years so the borrower has the chance to build some equity

Philm,

An amortization schedule is just math. I don’t think an act of Congress can override math. If Congress attempted to do that, it would no longer be an amortization schedule.

There are only 2 ways to do a 50/50 equity/interest split early in the mortgage.

1. Have initial payments be much larger than final payments

Or

2. Have banks give people equity for free in the first few years’ payments for no good reason and then delay the interest payment until the end.

Since 2 is completely non sensical and 1 defeats the purpose, this ain’t happening.

There is a simple way to build equity at the beginning, though. It’s really complicated and very secret. It’s called “saving for a down payment before you buy your house”.

“I don’t think an act of Congress can override math.”

Congress certainly thinks they can override math with the way they spend money…

Congress and altering math. How about this one? In 1897 the General Assembly of Indiana passed a bill ruling that Pi was four.

@Sea Captain

“Congress and altering math. How about this one? In 1897 the General Assembly of Indiana passed a bill ruling that Pi was four.”

I think they rounded it to 3.2. Not 4. But I see your meaning.

Counter-party risk. The loan term increases, so does the rate. Banks will want more assurance that you will pay them because others can do it with less time. It’s a risk asset to them.

I did that as a thought exercise and it is still a terrible deal lol

Crazy how clueless people are which explains $38T debt and counting….

Apparently not even the entire adminstration is behind this idea according to an article citing sources from the inside. It amounts to the genius Pulte, likely looking out for his own self interest went directly to the King and sold him with heavy smattering of flattery as the bait.

“On Saturday evening, Pulte arrived at President Donald Trump’s Palm Beach Golf Club with a roughly 3-by-5 posterboard in hand. A graphic of former President Franklin Roosevelt appeared below “30-year mortgage” and one of Trump below “50-year mortgage.” The headline was “Great American Presidents.”

Roughly 10 minutes later, Trump posted the image to Truth Social, according to one of the people familiar, who was with the president at the time.

Almost immediately, aides were fielding angry phone calls from those who thought the idea – which would endorse a 50 year payback period for a mortgage – was both bad politics and bad policy, a move that could raise housing costs in the long run, the person said.”

You already highlighted how much more interest and how much longer before you have any equity in the home, still interesting to see it in a monthly form which is more relatable to our society that tends to run on monthly unit of measure, these numbers are truly comical on a $1M mortgage, which seems to be pretty common in SoCal nowadays…I am sure RE agents and NAR will still tell you it’s worth it…even if 50/50 ratio of interest vs principal won’t be until 2062 even if you took out the loan now…

I like the idea of them, the swing in trading these turds when interest rates shift will be huge, and the money to be made spectacular. For the buyer, well eff ’em. S.B.

In other words, Pulte is a facking moron. But hey, the taco in chief likes it!

Once again, anything the trading, ruling class likes to make more money, sure- sounds great. Should have elected Elizabeth Warren President in 2020.

Meanwhile, metals are back on the run. Sigh.

Like the fed lowering interest rates lowered mortgage rate was working, er totally not.

We live in an era of moron marching mindlessly off a beeeg cliff, but until the impact, it’s all great!

Shiny object du jour.

Just like the 84 month automobile loan. Negative equity….

Exactly.

All this utter crap, from ZIRP on, is simply about artificially, unsustainably manipulating one or the other of the small number of variables which determine present values (ie, home demand/valuations).

ZIRP was all about destroying interest rates to lower monthly mortgage payments (in practice only resulting in keeping monthly payments fairly constant while empowering an absurd McMansion doubling/tripling in home “values”/prices despite a stagnant US macro-economy.

The Ronco 50 Year Mtg – simply grossly increases the number of mtg payment periods in order to artificially/unsustainably prop up/worsen the home valuation/cost crisis.

Contemplate the utter sickness of US economic policy when an actual *productive efficiency based lowering of home prices* (or significantly increased supply via any means) would likely result in a massive collapse in the Fed’s virtual reality “wealth effect” world.

Actually, honestly, lowering the cost of housing would cause an economic collapse – that is where decades of an essentially demented housing/interest rate policy has gotten us.

Local credit union here, offers 96 months on 2022 or newer vehicles @ 6.99%.

It really is amazing – it is also fairly easy to believe that if Americans just had learned to haggle like a mofo and simply pushed back on *price*, the manufacturers/dealers would not have been compelled to compete on final, total *price*.

It is though a 70 year focus on productive efficiency/end price simply (and lastingly) evaporated once (and magically simultaneously with) the arrival of extreme financing techniques.

The implicit story is that 90% of the public (in a handful of years comparatively speaking) had their brains drop out their *sses and only, utterly, focus on monthly payments – and that essentially 100% of manufacturers simply accommodated “consumer preferences”.

I think the actual details of that version of history needs to be closely reviewed.

Most importantly, the essential unanimity of manufacturers ceasing to compete on final, total prices. Out of maybe 20 worldwide makers…not 1 thought it might be a good idea – for market share growth reasons – to compete on the very axis that had historically prevailed…in this and every other market?

And the very same dynamic (competing on final, total price) which *still* (to this minute) prevails in China – which, this second, demonstrates the most final price competition in the history of humanity.

It seems like the instant to add speculation to that mix it just short circuits the whole market, especially when the government comes in and backstops the speculative prices. So now to have people, at best, not caring what the total price is because they know it’s going to go up, or at worst, actually competing to make it go up. So now price becomes this sort of ethereal idea and the payments become the only place where reality can still assert itself, and the central banks are doing everything they can to bash those payments down, partly because the people are demanding it. If you don’t let a speculative bubble correct itself, and if that bubble happens to be in an asset that is a basic necessity, then you essentially end up with a giant unintended zero-sum wealth transfer from one part of the population to the other.

Wish I had 50 years on the refi I did in early 2021

Yes! Imagine locking in a 50 year mortgage in 2021 at around 3%

Then waiting for the same irresponsible people who just proposed the 50 year mortgage decide to inflate away the national debt by printing money next year and driving inflation up and the 30 year Treasury rates to 15% similar to the 1980’s.

Chaos!!! But I’d have been set for life. I should have invested all of my paper route money in 30 year bonds in 1981. I could have paid for a house.

My crystal ball broke in the Northridge quake and I’ve been lost ever since trying to figure out what our leaders will do next.

It just puzzles me how many people believe a 50 year mortgage is a good deal JUST because Trump called for it. And that is the underlying problem, too many Americans don’t understand economics and would get stuck in one of these monstrosities.

This was BILL PULTE’S incredibly stupid and moronic idea.

True but nobody would listen to Pulte.

Oh except the dog and pony pitch to the King worked and someone did listen to him and this is why we’re talking about it here…so maybe no one serious listened to him but the one with the most power did and that’s all that matters in our current time

He would make a fine used car salesman.

A 50 year mortgage would outlast a Pulte Home.

It seems to me that the Pulte family wanted to get rid of the red headed step child and paid the government to take him off of their hands.

“…how many people believe a 50 year mortgage is a good deal JUST because Trump called for it”

Isn’t THAT the problem?

The abdication of the responsibility to think for oneself?

…that’s okay, seems like AI is arriving just in time to fill that gap…(/s…or not).

may we all find a better day.

Recon in the smoke….situational awareness……sitrep……

May we all find better understanding and strength

Take care brother.

“how many people believe”

We haven’t really seen it yet.

Internet dissemination of knowledge probably kept ZIRP Bubbles 2/3 maybe just 50-60% of ZIRP Bubble 1, in terms of numbers of actual numbers of buy/sell transactions at idiotic valuations.

Once people stick their face on a stove (ZIRP Bubble 1) they do tend to learn, if slowly.

The arc of history bends slowly towards…exposing shoddy magic tricks.

The tragedy is that the internet only arrived within the last 30 years or so – so the increased spread of knowledge could not penetrate fast enough, far enough.

Well Trump himself believes it is a good idea.

My daughter (40 year old Masters in engineering ) might like the 50 year mtg unfortunately. She has moved on from engineering into STR hype that promotes cash on cash returns and ignores the debt in the calculation and the negative equity with that loan. Much like interest only Commercial and Business bonds . Does Canada have interest only mortgages?

STR?

Short term rental

Unfortunately there are many people out there that do not pay attention to long term ramifications when they finance something. They don’t necessarily pay much attention to interest rates, amortization schedules, or total cost over the life of the loan.

They only short term look at what monthly payment they can afford, or want to afford. This is even if it is only $91 difference.

I know some of these people. They could be forced to read this article, it could be explained to them, and they will say…. “But my monthly payment”

Those are the people that will unfortunately choose a 50 year mortgage.

The real estate cabal, realtors, mortgage companies, closing attorneys, et al will sell the 50 year mortgage as manna from heaven. People believe what suits their best interests.

Most people have not taken a college level finance class. I’m not being dismissive, but I have a son with a finance degree and a daughter with an environmental science degree. Both are smart, both went to good schools and did well in their classes, but my daughter wouldn’t be able to compare 50 to 30 year mortgages the way we are casually throwing around numbers – especially when you start tossing around complexities like points or adjustable rates. How many people in the US do you think have taken a college level finance class? 25%? Fewer?

Greg,

Much fewer than 25% – but there is Google, and people have friends who have more financial knowledge, and the internet in general (Google, Facebook, etc.) should be aiding the speedy dissemination of all sorts of information.

It is happening but slowlly – Housing Bubbles 2/3 likely had only maybe 50-60% of the number of actual closed transactions that Bubble 1 did – because the Bubble 1 disaster was widely discussed and *explained*.

So many fewer got suckered into Bubbles 2/3 – although still in disturbingly large numbers.

The truly horrible thing is that a ton of corporate America’s financial “health” has, over the last few decades, become more and more wholly dependent upon these risky (to everyone) and abusive (to product buyers and asset-backed-security investors) financial manipulation techniques.

Isn’t this Trump and team realizing that they will not be able to budge interest rates on the 30 year? This feels like a desperate ploy to unlock the housing market and save values.

The more those morons try to lower short term interest rates, the higher long term interest rates will rise.

Trump has been dead wrong on interest rate policy from day 1 and if he’s not careful this game he is playing will sink his presidency.

The administration and the Fed have both been extremely reckless concerning inflation and voters at least will not be fooled come late 2026 if it is still raging.

Arguably Harris lost because of inflation, not because Trump was popular – does he think the same can’t happen to his people?

Based on the polls about the percentage of people unhappy with the economy, both under Biden and now under Trump, that should lay to rest the idea that a booming stock market means Americans in general are happy with the economy.

Yes.

Unfortunately, you can’t both unlock the housing market and save values. It’s more of an “or” proposition.

Oh I know this, but the people who control this country don’t care. They will do everything they can to subsidize asset values so that they don’t have to lose.

Absolutely insane for the homebuyer………that my boy even floated the idea makes me wonder “what the hell” he was drinking ??!…….. terrible idea really …….ok on to more important iteams…..food prices………utilities…….fees ……and those damn bookie I mean, credit cards…….work those first Washington.

could be a good inflation hedge if a decent rate.

Everyone is looking at this the wrong way. Its not 50yr vs 30 yr, its 50yr vs renting.

But the interest! I’m getting 0 equity on my rent, which is increasing every year. A 50yr is just rent control! And i’d give up a toe or to be paying 2015 levels of rent for the next 40 years, ask any renter right now if they’d do the same?

I’m running the numbers for my own situation, calculating in the big tax write off that mortage interest is. Basically a free month of mortage payment until year 9 back in taxes.

At the 10 year point, Assuming 2% asset appreciation, estimating property taxes and 65k worth of maintenance(overshooting estimates), hoa fees(with some increases), a 3 bedroom house is looking not that much more expensive than my 1 bedroom apartment. That’s assuming a very modest increase to my rent over the same time.

If appreciation is 2% yr/yr, i’m paying 20/30k more over 10 years than my 1 bedroom apartment to have a whole ass house and garage.

If appreciation reaches 3% yr over yr I’m ahead of rent by low 5 digits. Math gets even better if I get a roommate, which I couldn’t possibly do in my 1 bedroom apartment.

I’m not sure I understand what you’re saying about the mortgage interest “write off” and the “free month,” but to clarify: if your 50-year mortgage interest is 6.9% on a $500k house = $34,500 in interest in the first year. If your marginal income tax rate = 20%, you get to deduct from your taxes $6,900 of the $34,500 in interest for the first year, assuming no caps on the deductibility of mortgage interest. The rest of the interest for the first year, $27,600 you pay yourself, it’s profit to the lenders that you will never recoup.

The 50-year mortgage will cost you nearly $1 million in interest over the 50 years, or $800,000 after taxes if you’re in the 20% marginal tax bracket with no caps.

Plus you pay rising property taxes for 50 years, you’ll pay for at least one new roof, probably two, at least one new HVAC system, at least one new water heater, lots of other maintenance and repair expenses, and annually surging homeowner’s insurance out the wazoo.

If you compare to renting, you need to figure in ALL expenses of homeownership. I don’t know which will come out to be a better deal for you, but you need to figure it correctly.

Pulte is getting pilloried for this mindlessly stupid notion.

This reasoning is too rational, therefore above the grade of those who will potentially vote for it.

Mr. Wolf did an excellent job of showing the tiny amount of interest rate reduction versus the long increase in payoff time and huge increase in interest ultimately payed. At the extreme is the “creative financing” of the Federal Reserve’s huge inflation under Federal Reserve chairman Burns; where the payment period is infinite through paying an “interest only mortgage.” The 1970s to 1980s, had an even worse mortgage of paying less than even the interest only and giving the borrower (“sucker”) a huge balloon payment at 5 years to try and refinance. It is strange that President Trump would try to “pawn off” essentially the initial entry into “creative financing” for actual housing relief; i.e., tariffs, zoning, etc. when he and a large percentage of people (now parents and grandparents) are old enough to remember “the good Ole days.” However, young people today do have it worse in that the monthly payments are high, but ultimately caused by the much higher principal; i.e., the financial pain is similar, but the causation is worse. Though ultimately the housing prices are amenable to political pressure, just look at the “freak out” caused by voting in the new mayor of New York.

Every single idea from politicians, no matter which “side,” just makes the problem worse, and screws the young even worse, because they’re working for their wealthy masters.

Pretty soon this country will be torn apart by angry young people, all because billionaires just couldn’t be satisfied with the outrageous lucre they already had amassed, constantly chasing more.

I totally agree

It’s like going to the doctor because you have an infection, but instead of giving you an antibiotic which will clear it up they secretly conspire to give you another disease in addition to what you already have, but they sell it to you as the antidote while gaslighting you that the new symptoms are actually mild side effects of the medication which will cure you.

Instead, you wither away in pain and hopelessness, slowly heading towards the grave while the doctors are busy lining up recipients for your organs that they will sell for even more money after they have extracted every bit of insurance payments they can from your policy. You see, you are nothing but a commodity to be used and abused until you are of no use anymore. This is how these narcissistic sc_mbags operate.

That may be a bit of a stretch, DC. This is more like going to your doctor because you’re overweight, never exercised or ate well, and instead of the doc outlining the concepts of a good diet, giving you links to read and a nutritionist to see, he simply tells you to eat less fat and lots more carbs, and dangles an Ozempic RX if you want.

@Depth Charge & Ethan in NoVA I get to know a lot of young people since I rent to them and every year they get dumber and dumber and deeper in debt thanks to the education industrial complex that keeps charging more and more and giving less in less (giving most kids straight A’s so they borrow $100K for another year and/or another degree).

Not all kid, but even true for some, it is unsustainable.

I work for a state college in the facilities area. I have a B.S… I used to think the faculty must be extremely learned, gifted, etc. To be sure, there are some bright folks teaching but the majority are dumber than a barrel of rocks… at least in a ‘common sense’ meaning. Paleontology is fascinating to some people, but in the real world, doesn’t pay squat professor.

However, this is changing – a number of states are now tying funding / grants / loans to specific degree earnings metrics and the Feds are heading in that direction as well. Changes are happening now but slowly. As it accelerates, it wouldn’t surprise me to see 25% of all colleges and universities fold shop in the next few years; especially smaller boutique types.

I agree with this. Without getting too political, while I don’t think Mamdani is particularly well informed nor do I like his ideas, it’s a big mistake for people to ignore the environment that created him.

In a lot of ways, he’s the opposite side of the same coin as Trump. They’re the result of people being deeply unhappy with the status quo, for a number of reasons. You can think they’re (they being Mamdani voters *or* Trump voters) misinformed, ignorant, overreacting, replacing something bad with something even worse, etc.) but the elite should take heed of the underlying message.

Mandami will not do much to change NYC. First of all, he doesn’t have as much executive power with all the interests in control of the city. Second of all, if he is like every other “left of center” Democrat that obtains an executive position, he will tack right so fast. Obama ended up to the right of Colin Powell after he was voted in.

Great comment. I know a lot of Trump supporters who just hate the status quo, but could care less about Trump’s positions. They just want to “stick it to the man”. The man being corporate Democrats that abandoned working class folks decades ago. Folks are accepting more extreme views as the status quo continues to fail them, and the status quo continues to obviously just line the pockets of the donor class. Mamdani just represents someone who seem to care about regular folks, whether his policies work or not. Same as Trump.

That’s exactly it. And the people who hate the status quo also hate being gaslighted. The donor class and elite keep telling them to shut up and be grateful about how great the economy is and how great they have it.

Nobody wants to be told that, whether true or not. It comes off as condescending and tone deaf.

FYI: new candidate for SPAC pantheon thing:

Sonder is also the latest bankruptcy victim that stems from the frenzy of special purpose acquisition company (SPAC) deals that began about five years ago

That thing imploded right out of the gate. It merged with a SPAC in Jan 2022 and imploded, just like that, just fell off a cliff from day one. By July 2022, the stock had already collapsed 90%.

Sonder filed Chapter 7. A straight liquidation, without even pretending to restructure.

I remember the hype after the SPAC merger. Crazy times.

If you give me a loan for eternity, at 1% interest, I and my descendents will happily pay you an infinite amount of money. We will be the winners in that deal.

But the interest isn’t 1%.

Nominally no, but the real interest rate could be. If you believe very high inflation is inevitable, there is a world where locking in a 50 yr makes sense.

there were loans like that out there:

e.g.:

Dutch Water Board Perpetual Bonds (13th–17th centuries)

Issuer: Various Dutch waterschappen (water boards)

Date: Some as early as 1624

Terms: Perpetual bonds — no maturity date, only periodic interest payments

Payment medium: Originally silver coins or gold florins

Example:

In 1648, the Lekdijk Bovendams water board issued a bond for 1,200 florins at 5% interest to raise funds for dike maintenance.

Interest was payable “in specie” (actual coinage, not paper).

Yale University owns such a bond and actually collected interest in 2015 — they were paid in euros equivalent to the silver content.

Would you still be happy to pay interest in gold or silver in perpetuity?

Excellent article challenging this nonsense of a 50 yr mortgage.

The best thing folks can do is pay off any mortgage early by doubling up on payments, no matter how hard that may be.

My grandparents bought their small farm in 1928; back then loans were for only 5 years or so. They operated a small dairy farm for the town during the Great Depression and somehow made those payments.

Debt, long term drawn out debt, is bad news, unless the interest rate is 0.

I thought we just went through 10-year auto loans. Was lose-lose-lose for everyone involved (subprime buyers, unsophisticated investors and greedy dealers).

Are we really going to go there?

Wolf is spot-on. The real danger isn’t just the **$91 saved** vs. the **$1 million in interest**—it’s the engineered **zero-equity trap**.

The 50-year term institutionalizes an ultra-slow amortization curve, leaving homeowners in [b]negative equity territory much longer. [/b] If rates rise or prices dip, a forced sale (common, given the 50-year timeline) guarantees a loss.

This isn’t an affordability fix; it’s a generational debt treadmill designed to transfer wealth from households to MBS investors while structurally inflating home prices. Your thoughts on the systemic risk this creates?

Everything you said is correct, but the G is really doing it to prop up the already existing housing bubbles.

Reflecting on it a bit, the G maybe doesn’t even really need a huge number/precentage of increased buyers (demand) as a result of this vast stupidity.

Even if a pretty darn small number of buyers use this obscenity to barely qualify for today’s hugely inflated home prices…that might “set the market price” – allowing for the fiction that 100% of inflated home values are still “accurate”.

For example,

1) During the pandemic bubble, maybe 6.3 million or so home sale transactions took place at/near peak prices/valuation.

2) As unZIRP allowed interest rates to rise in 2022, the number of annual closed home transactions collapsed to maybe 4 million each in 2024 and 2025 (because 7% mortgages vs. 3% mortgages more than doubled necessary monthly payments at Pandemic era nosebleed valuations),

3) But…what Trump’s Ronco 50 Yr Mortgage would enable…might be for a pretty smallish number of suckered annual home buyers (1 million?) to continue to prop up the illusion of those Pandemic era nosebleed valuations.

4) This is because *even if the number of closed transactions continues to collapse because of insane overvaluations*…from 4 milion to 3 to 2, etc….so long as some fig-leaf levels of closed transactions occur (2 million per year? With 1 million coming from Trump Ronco 50 yr mtgs?) that would enough of a fig leaf for the banks, regulators, and the Fed to all pretend that 100% of home valuations haven’t fallen at all.

5) Thus preserving the bubble and avoiding a “wealth effect” collapse.

cas127

Yeah but read the article. On a $500k mortgage, the monthly difference between a 50-year and a 30-year is only $91.

Payments:

30-year: $3,069

50-year: $2,978

$91 a month does not change anything in terms of what people can afford.

Fair enough…perhaps rather than fully sustaining the bubble era transaction price levels, the Ronco 50 Yr (vey) might simply *slow* the deflation…

(Interestingly, even Trump – uber hypester – was fairly subdued when ad hoc’ing an answer on the 50 yr – perhaps Pulte/Trump Social got *way* in front of things with a very flashy Trump=FDR roll-out)

I can’t quite intuit whether the huge increase in permitted payment periods would have an *increasing* impact as transaction-prices fall – but I sense that it might – I’m going to have to mull/Excel it a bit.

Anyway, I guess my main lightbulb thought was that “median values” in the housing market (for the uses of shallow reportage, bank pretending, regulatory gaze aversion, etc.) don’t really require high/normal levels of home buy-sale transactions to occur.

Such impostiture promoters would be sufficiently happy if closed deals were only 3-2-1 million…the only key part being the *price* that deals go off at (however many/few).

I know it is antidotal….

And it is perplexing to me…

But I do know people who would and have made both car and home loans due to a monthly payment difference of similar amounts to the $91 you referenced.

Not necessarily common, thankfully. But I assure you it exists. Because I have witnessed it with my own eyes.

It does not make any sense, blows my mind, but is real just the same.

Can you imagine paying on a mortgage 15 years, a housing correction occurs and suddenly you are under water? Crazy!

WhT A CROCK OF SHIT….

I always though the 30 year mortgage was a rip off, with too much interest over the life of the loan. 100 year is insane.

A 30-year loan is not a rip off, it’s just how the math works out. If you don’t like the results, then get a different loan.

The median time period for staying in a home is 12 years lately, and I’d guess 90% or more stay less than 20 years.

So why do we need 30 year mortgages, let alone 50 year mortgages?

Once you go above 15-20 years, the mortgage length does not align with needs of the homeowner and this adds speculative risk where it doesn’t belong. The extended mortgages create financial instabilities.

You can probably blame FDR who set the mortgage standard to 30 years to enable millions to afford a house at the time.

Before that you had to be able to buy a house with cash or a 5 year mortgage which was too high for most people.

This has probably inflated the price of houses for the last 90 years since it enabled the demand for home ownership.

My point is that you are correct but far fewer people can afford a 15-20 year mortgage payment so house prices would have to fall.

“far fewer people can afford a 15-20 year mortgage payment”

Is monthly p&i that much higher on a 15yrfm? I woudn’t think so based on the 30/50yr delta being so small. 15yr also comes with a lower rate.

ShortTLT,

I think it is a matter of perspective and income. From Wolf’s excellent example above:

15-year: $4,085

30-year: $3,069

50-year: $2,978

It is a little over 1K more per month for a 15 year mortgage.

For a 78K average household income in the US, that is 15% and likely makes a difference between qualifying for a loan or not.

Wolf’s excellent point is that $91 per month probably makes no difference to someone buying a house so why get a 50 year loan?

$1K/month does make a difference to the average earner. I didn’t qualify for a 15 year loan for my first house in the late 80’s because my new salary was too low. I did qualify for a 30 year loan and refi’d my 30 year 10.5% loan to an 8% 15 year loan within a few years when I could. Otherwise, I could not have purchased a house.

After further thought, maybe I shouldn’t have purchased my first house and just rented. I sold after 6 years because of my job and barely broke even for tax purposes. The house didn’t appreciate much and the first 3 years of my 30 year loan was almost all interest. It would have been cheaper to rent.

I think it is much cheaper to rent now than to buy. My kids are waiting.

This 50 year mortgage idea is a typical intuitive response by the ignorant. Payments too high? Spread em out over longer, problem solved!

As noted above, at best, it does nothing for affordability. And as Wolf says above, PRICE is the problem, rates are not. Rates could go to zero and while that would help those who own and can refi, it makes buying a home less affordable for sure.

Yes. It seems like trying to fix the problem of 1 pie of pizza not being enough for everyone by cutting it into 12 slices instead of 8…

Floating the idea of a 50 year loan,seems like a drunken/shroom inspired idea from someone on 4chan humor!

It’s all political theater because his ratings are falling and Democrats are winning elections. Now they’re talking about $2,000 checks for select Americans, 50-year mortgages, and 15-year car loans. We ended up with a bad apple, and after the midterms his presidency is going to look very different.

Are there any home loans out there on the market that operate like an interest only loan? Say a 30 year loan, but you only pay off 30% of the principle over the life of the loan and need to come up with the other 70% at the end of the 30 years if you haven’t sold already. If you can’t pay it up you get foreclosed.

I would think you could have a higher rate on a vehicle like that due to the slower return of principle. and a lower payment since you aren’t paying the principle back through the life of the loan. Does it exist? Is there a strong reason it doesn’t?

Interest-only loans are fixed for much shorter periods, such as five years. And then rates adjust.

Interest-only mortgages can be appropriate for properties that generate cash flow, such as rentals. It’s not and should not be a mass-market product.

Having zero debt means no one ownes You financially.

You sleep fantastic at night.

50 year loan, You better get pre-qualified at 15 years old in order to see it paid off at medicare age..

Have a fantastic Evening all.

.

Debt is indentured servitude to the bank. Never had a loan in my life. Never bought anything unless I could pay cash.

The affordability fix is multifaceted. But, the first policy off the rank should be to impose Minsky Lending Criteria which ties the amount lent to the real/implicit income derived by the asset being purchased. Max loan amounts would fall significantly directly correlated to falls in asset price.

Out of all of Trump’s advisors, Pulte really stands out and not in a good way. Not meant to be political; he’s just the wrong person to be in that position when his industry and company has just reaped the benefits of serial housing bubbles when what is needed is a price correction.

You are absolutely right! I spent 52 years in the mortgage business and used amortization tables with varying rates and terms to illustrate your point. After ten years, a 25 year amortization mortgage balance still exceeds 90%! Why extend the pain to 50 years at an even higher interest rate?

Actually, it would be the ripoff of a half century

Why stop at 50 years? Why not 75 or 100 years? Call them “generational mortgages” that you can pass on to your children with the house. If the B-piece buyers of MBS are on board with this, what’s the problem? It’s a win-win!

Passing on debt to the unborn, yes, feudalism 2.0. Hooray! We can all be “lords” again!

I just bailed out a relatives with a nice balloon payment, they might have been better off with a 50 year.

I’d sign up for a 50 year mortgage if I was 80+ years old with no heirs and the payments were less than my rent.

Maybe not… my cats just gave me a dirty look.

Those cats will come after you in your sleep if you mess with their inheritance.

Feudalism 2.0

Hedge accordingly.

Then there is this other argument that you never have to pay for 50 years because youll probably move out in 10 years. The only problem is that you dont really build any equity.

Is that really it ?

https://x.com/Chris_Smth/status/1988026545517293846?s=20

That argument is BS. RTGDFA

Because a 50-year mortgage will come with a higher interest rate than a 30-year mortgage which comes with a higher rate than a 15-year mortgage. I gave you a chart of the interest paid after 15 years of 50-year, a 30-year, and 15-year mortgage at today’s interest rates. I cannot believe people in finance are this stupid!!!

And if you had read this article, you wouldn’t post this BS here.

Long-term (beyond 30y) mortgages can work, see for example Switzerland where these are very common. But it would require extensive system changes. If implemented point blank in the U.S. it will only prop up the existing bubble.

– Swiss mortgages are rarely fully paid off, as the income-tax system incentivizes debt. In fact, most mortgages only amortize 1/4th of the property value.

– Swiss has historically low & very stable interest rates.

– Culturally working towards ‘owning’ your home is a norm that just doesn’t exist in Switzerland. U.S. home ownership is 65% while swiss is 42%. In fact, the Swiss system is structured as a permanent tax-vehicle over property than anything else. Trying to implement it in the U.S. for the sake of making home-ownership more widely available is a complete farce.

This article seems to have generated the most anger among posters that I’ve seen here. People outraged at the idea that SOMEONE ELSE might chose a different financial route than they did and therefore that route shouldn’t exist. Do these same posters follow other people to the mall and scream at them for buying $120 jeans when $30 Wranglers are available at Walmart?

Housing is a mess and it’s all due to 2020-2023 monetary inflation and the resulting high prices. You’ve shown here how housing prices have dropped from the 2022 tippy top but it’s more than three years later and they aren’t falling that fast. Nothing like 2008-2011. It will take time and inflation to make today’s flat/down prices seem cheaper. As I’ve said before people paid 2032 prices in 2022 with cheap loans.

I actually think there is room for an interest-only mortgage option. It would basically be the same as renting BUT you are protected from hyperinflation and you retain the option to pay down the principal at any time. Fixed 6% on a $500k loan is $2500 a month. Forever. Can anyone say they’ve had the same rent for a decade or more? I keep hearing people say they are going to pay $20-40k a year in rent to “wait out” the housing bubble. Then what?

As long as the government continues to strap taxpayers with bailouts, I believe mortgage loan terms are everybody’s business.

If they passed a constitutional amendment preventing housing bailouts and QE, nobody should care what others do.

If you think an interest-only mortgage protects a “homeowner” from hyperinflation, I have a few words for you to consider: insurance, property tax, roof, water heater, HVAC. Two of those disclose their new prices every year (the new price is almost never lower than the old price). The rest of those hide for 10-20 years before they present the bill and yell “Surprise!” You don’t think rent goes up just because landlords are greedy, do you?

Great article, I agree 100%.

I’m getting a lot of heat on X (all 33 viewers and 3 commentors) for disagreeing with 50-year mortgages. The argument I see the most is that housing will appreciate at 4.5% per year so any “knucklehead” should know the 50-year mortgage is amazing. Easy arbitrage with the equity they’re saying.

That’s one argument, but the idea of housing appreciating at that rate during the next 10 years seems a bit far-fetched based the price of housing now. If housing doesn’t appreciate in the first decade and the roof, a/c units, and/or hot water heater have to be replaced, aren’t a lot of those people who took the 50-year mortgage f’d?

What’s the average time that someone owns the same house? Fair amount of turnover historically over a 50-year period, right? Not paying down the mortgage and not getting appreciation would freeze a lot of the families who take the 50 year.

This would be one of the smaller consumer debt expansion mechanisms I’ve seen in my 45 years of adulthood.

When I was startiing out, 20% down was the standard. You could get a mortgage for 10% down, with the added cost of PMI. We chose more modest housing with the former. Linolium counters and floors and a makeshift bedroom set.

The horror!

It was also before the ubiquitousness of craft beers, body art, gaming and specialty coffee tugging at pocketbooks. Starbucks alone sucks $60B out of the consumer economy.

The latest statistic that floored me was that the average new car loan was over $41K. We’ve done pretty well in life, never felt impoverished. We recently bought our first new car in over a decade. A base Honda CRV for $32K cash, loaded with more features than I ever dreamed I’d have in car, actually more than I wanted.

Who’s buying these cars? One could say it’s the effect of the K economy, the top half keeps getting richer. But remember, these are loans. And not come-on loans, the average rate is 6.9%. So I’m gonna say many/most of these people can’t afford it.

All-in-all they’d be better off with a 50 year mortgage. At least the house would still be standing when their kids finish paying it off.

…ah, but would it, really? The lot remains, in any case (unless a new financing instrument to divide structure and dirt to lower monthly payments, etc., appears…).

may we all find a better day.

“…unless a new financing instrument to divide structure and dirt to lower monthly payments, etc., appears…”

That’s actually a REALLY interesting idea. Isn’t there something like that for commercial properties? Air rights or somesuch? What are the complications keeping that from being applied to residential properties?

The house I spent the 2nd half of my childhood is still standing and occupied. Some of the neighbors are still in the houses they grew up in.

None of the cars they grew up with are still there.

Oh, and neighborhood is likely lower relative income now, but most of the counters are granite/quartz

who cares if there are 50 or 100 year notes on real estate. isn’t it up to each person to decide. the last dozen properties i have bought have been with no debt. sold them 2 years ago. probably won’t borrow in future, but who knows. who cares. the world of r/e financing around the globe has many different options. why the nanny state nosey body attitudes? i don’t get that part. the math will depend on future rates and peoples situations. who cares. freedom is the answer. what is the question ?

” why the nanny state nosey body attitudes?”

LOL, did you miss it? The proposal is for GOVERNMENT BACKED 50-year mortgages.

Sure, if a bank wants to offer you a 50-year mortgage without government backing at 9%, fine with me.

fair enough. however, in the 21st century, the government backs all of banking anyhow. including my old employers of lehman bros and bear stearns. 2 time loser. ha ha ha. the idiots at lehman bros were too stupid to take the korean offer.

Howdy Youngins. Are we learning yet? Of course a politician will try and make you a debt slave. Don t be anyones tool or fool.

I would hope someone would use common sense and state that supply and demand still impact the costs of housing. The 50-year mortgage will not address this.

“The housing supply shortage is a long-standing structural issue, with estimates of the shortfall ranging from 1.5 million to 5.5 million units, depending on the methodology used.

A 2025 analysis by J.P. Morgan estimates the current shortage at approximately 2.8 million units, a figure that could take around a decade to resolve.

This shortage is driven by decades of underbuilding, particularly following the Global Financial Crisis, and is exacerbated by restrictive land-use regulations and zoning laws that limit new construction, especially in high-demand metropolitan areas”.

Wolf will be along shortly to shoot this down. There’s no shortage when there’s 8 months of supply.

I would love to hear his thoughts.

If there is a larger supply than there is demand, prices would fall in all areas.

The Law of Supply and Demand is still a very large factor in markets.

In some markets, there is lots of supply and falling prices (some places are down by over 20% already).

In other markets, there is tight supply and still rising prices.

This site is full of articles and hundreds of charts that spell out market by market what inventories and prices are doing.

You can get them all here:

https://wolfstreet.com/category/all/housing/

I re-posted three of those charts further below. Have a look ⬇️

…I believe the old real estate term is: “…location, location, location…”.

may we all find a better day.

The shortage was driven by the Keynesian economists who think there’s no difference between money and liquid assets. It was driven by disintermediation of the nonbanks, beginning with the thrifts, then the S&L crisis, then the payment of interest on interbank demand deposits.

Folks will convince themselves using the following arguments:

1. I can qualify for a home now. I could not before.

2. Except for the costs of insurance and taxes I can lock in the costs of home ownership over the forseeable future.

3. If I rent I will pay the same or more and rent prices will continue to go up ad infinitum. The landlord will pass on the costs the same as if I owned it.

4. Over the long run the house will appreciate at 5% as they have done for most of the time. I may have nothing on the principal but I have the value of the appreciation.

5. If interest rates go down I can refinance for a shorter mortgage at a lower rate. If they go up, I’m locked in at whatever rate I started with and I save.

6. The landlord pays the same as I do or more for the cost of ownership plus a profit. Over the long run I’m better off owning.

I think you summarize very well the plan that will be sold to the folks.

I would love to hear your thoughts on the potential for portable mortgages and what the impact would be to the economy and housing market if Pulte gets his way and they become standard. At first glance it seems like a good policy but I am sure there are trade offs I am not aware of.

VA mortgages are already portable. And hardly any of them get transferred because it’s complex and difficult to do.

For example, when you sell your house for $500,000 and you have $200,000 in equity plus a $300,000 remaining balance on your VA mortgage, the buyer would have to come up with $200,000 in cash and assume the mortgage. If the buyer doesn’t qualify for the mortgage or doesn’t have $200,000 in cash, you don’t sell the house.

The buyer could also try to get a second-lien mortgage for the $200,000, but current second-lien mortgage rates are substantially higher than current first-lien mortgage rates, currently over 9%. So maybe finance $200,000 at 9.4% and assume a $300,000 mortgage with a rate of 3%. And suddenly, you’re worse off than with a new mortgage for the whole thing?

And there are other problems.

And you cannot make an existing standard 3% mortgage from 2021 suddenly portable in 2026. Any change in policy on portability could only affect NEW mortgages. Contracts of existing mortgages that have been sold to investors cannot be changed. So you cannot make a 3% mortgage from 2021 portable in 2026. So any change would have no impact on existing 3% mortgages, home sales, or prices.

In addition, if new portable mortgages are issued and sold to the GSEs to be securitized and sold to investors, these investors would demand higher yields because they might get stuck with low mortgage rates beyond the statistical average payoff expectation. So a policy change might increase mortgage rates.

The analysis leaves out the most important issue. The rate of appreciation vs the interest rate. If the interest rate is lower than the rate of appreciation than the longer the loan the better as one leverages the benefit of capital appreciation while being able to deduct the interest expense. In most cases, current rates are just too high to make this a worthwhile bet.

“Rate of appreciation” in local markets:

The Cities Where Condo Prices Are Now Below their Housing Bubble Peaks 20 Years Ago

The 23 Bigger Cities where Condo Prices Dropped by 12% to 28% through September

The 15 Bigger Cities with the Biggest Price Declines of Single-Family Homes (-10% to -24%) through September

For example:

Relative to the average wage, “housing bubble 2” still need to deflate in order to make housing “affordable”.

Most homeowners start with a 80% LTV (i.e. 5x leverage) regardless of mortgage duration. A 30/50 year will stay highly levered for longer than a 15 year, but I think it’s a moot point considering how easy/cheap it is to refinance if one desired.

At this point, everything is just speculation without knowing what the actual spread will be. There are cases where a 50 year mortgage would be beneficial for the same reasons someone would choose a 30 year over a 15 year. That usually entails treating the 30yr/50yr mortgage as if it were a 15yr and either paying the mortgage off early or investing the extra cash flow into higher-yielding assets like stocks. This gives someone a lower minimum monthly payment they can fall back on if need be and a higher return on their cash as long as rates are below the 15-year average return of the stock market.

Here is a current example from AI: ‘How do I pay off a 30 yr mortgage in 10 yrs.’ Make one extra payment per year.

That’s either an AI hallucination or something is missing, such as the size of those 10 extra payments 🤣

So 10 extra payments in our 30-year $500,000 mortgage example here is about $30,000 in extra principal paid on a $500,000 mortgage, which won’t pay it off in 10 years obviously.

So I just plugged this into my handy-dandy homemade amortization model: it would take 10 extra payments at year-end of $31,340 EACH to pay off the 30-year $500,000 example mortgage in 10 years.

Ya I started wondering about that, after just pasting it direct.

Maybe the payments are based on 10 year am with one extra one per yr.

This example is from about 50 yrs ago but it did happen: I was just a student many years from buying a house but did know some math. Got talking to a blue collar guy who was buying one and I mentioned that if he doubled the monthly payment, the am period went from 25 yrs to 5 yrs. Years later I met him again and that’s what he’d done and now owned the house. OK, this was when houses were much cheaper compared to wages so it prob wouldn’t work today but it illustrates the effect of raising the payment, whereas lowering it also has an equally dramatic effect but in the other direction.

The simple fact is that banks and mortgage companies hold relatively few mortgages ; they mainly originate and service these mortgages for a fee . The vast majority of mortgages are backed by a Fannie Mae or FHA guarantee and are then sliced , diced snd sold to investors .

As an investor in bonds of various durations

and credit qualities , I question the markets desire for even longer term paper at rates that are anywhere close to current long term rates . Although no long term Treasury auctions have failed in 2025, a number have attracted weak to poor demand . Since few people ( outside of the administration ) are confident in the Federal governments ability to rein in spending , there is a good probability that some auctions will fail in the future . Add in the Feds statement that they will not replace their holdings of MBS that have been paid off and differential between Treasuries

will only increase.

11:11 AM 11/12/2025

Dow 48,298.58 +370.62 0.77%

S&P 500 6,852.75 +6.14 0.09%

Nasdaq 23,401.42 -66.88 -0.28%

VIX 17.49 +0.21 1.22%

Gold 4,214.10 +97.80 2.38%

Oil 58.39 -2.65 -4.34%

Apparently, its a good deal according to Brent Johnson of SantiagoAuFund, IF one expects soaring inflation in the future. Sure, but what are the conditions needed for that to work out in favor of the buyer ? What’s the mortgage rate?

https://x.com/SantiagoAuFund/status/1988398469925785882?s=20

There is a lot of stimulus in the system already, and it has out home prices in the stratosphere.

-Government loan guarantees

-Only 3% down payment for FHA loans

-$500k home sale gain tax exemption

-Mortgage interest deductibility

-like-kind exchange tax gain exemption

-6 years or ZIRP

-$6T of Fed balance sheet expansion, including MBS purchases.

-State RE tax deductions

What next? 50 year mortgages? 1st time home buyer tax credits?

They are running out of viable options to support home prices.

Yes,being in debt for 50 years is a very bad idea.Some guy Garth Turner always touts the compounding returns of his portfolios and hates 50 year mortgages but he loves high fees for portfolio services 1% to 1.5% per year for his financial advisor stuff.You know the difference of 1% to 1.5% on say a 6.5% versus 5% yearly return.It is huge cost over 50 years. For example, on a $100,000 invested, a cost of $659,000 to $1,184,000 less money in the investor’s pocket and more in their pocket.The only reason I see why he hates 50 year mortgages are he can’t get that money if the mortgage company,finance company got it first.

If inflation eats away enough at the value of the currency, over enough time, say 30-50 years, would it matter?

As long as the mortgage holder’s income broadly keeps up with inflation, up to and then over that period, that is.

The problem is that you’re paying a higher interest rate on a 50-year mortgage than on a 30-year mortgage (see article); and a 30-year mortgage comes with higher rates than a 15-year mortgage (see article). So the longer the term of the mortgage, the less likely the rate will be near or below the rate of inflation. The 30-year mortgage rate now is over double the rate of inflation. A 50-year rate would be higher than that.

A story today on another site says 900,000 new homeowners are underwater on their mortgages.

Time to lower the lifeboats!

1. Being underwater is normally common for recent homebuyers with lower down payments. It doesn’t matter. It means some measure of market value is below the outstanding mortgage amount. So what. If the homeowners don’t look on Zillow every day, they won’t know the difference. They will keep making their payments. If ALL of those 900,000 lose their jobs and are unemployed for a long time, eventually, SOME of them quit paying their mortgage.

2. 900,000 is about 1% of owner-occupied homes 🤣

3. I thought it would be a lot more by now, given the big price declines we’ve seen in a lot of cities. But 40% of homeowners don’t have a mortgage, and most of the remaining 60% have made mortgage payments for many years and are way above water.

But 900,000… WOW sure sounds like a lot when you’re sitting in a bar drinking a beer.

The media can make clickbait out of ANYTHING. Look, if I thought this was an important number, I would have reported on it. But it’s a minuscule number within the overall context. So if you see some headline about the housing market somewhere, and it’s not on my site, go look up the context and you will see why it’s not on my site. Because it’s irrelevant.

Trump screwing over workers and consumers while benefitting lenders and investors?

Obviously, nothing but communist, socialist, Democrat, immigrant, terrorist, drug cartel propaganda… right, MAGA?

I wish I could get a 50 year TFSA GIC fully deposit guaranteed and paying a decent interest rate fixed for 50 years.

I am almost 19 and saved my first $30,000 from my first 12 months of my job.I can see it my $30,000 at say 6% compounded for 50 years worth……..$553,000.All tax free.

How does an interest-only, zero-amortization mortgage compare?

My belief, possibly naive, is that the liquidity of global finance should assure competitive rates in all conditions, with differences for risk. And the condition that has the most extreme benefit to the lender is zero-amortization — each month is 100% interest with no declining balance. Repayment isn’t a part of the structure. All gains are equity.

There is no interest-only 50-year fixed-rate mortgage. Interest only mortgages are for shorter terms, and if their terms are longer, their interest rates adjust after a while. After the term ends, they have to be paid off in full. If the borrower doesn’t have the cash to pay off the loan in full, or cannot refinance the property with a big enough a loan to pay off the maturing loan, then they default and lose the property. This is the problem in CRE right now as the fixed-rate mortgages come due, and cannot be refinanced because the current rates are much higher, and rents aren’t enough to pay the interest of the new loan.

I assume this was Bill Pulte who floated this one?

How much longer before he gets kicked out?

I’m embarrassed for the Trump Admin that this idea was allowed to get to POTUS’ desk and repeated.

I’m glad the response has been so visceral.