Are disclosures of “unrealized losses” on bank balance sheets next?

By Wolf Richter for WOLF STREET.

Acting Chairman of the FDIC Board of Directors, Travis Hill, who was sworn in as FDIC Vice Chairman on January 5, released a statement today, along with the materials of the quarterly report by the FDIC on the FDIC-insured banks, that the FDIC would no longer disclose as of today the total assets on its “Problem Bank List.”

The list had previously shown total assets and the total number of banks on the Problem Bank List. As of today, it only shows total number of banks on the Problem Bank List, forget the assets.

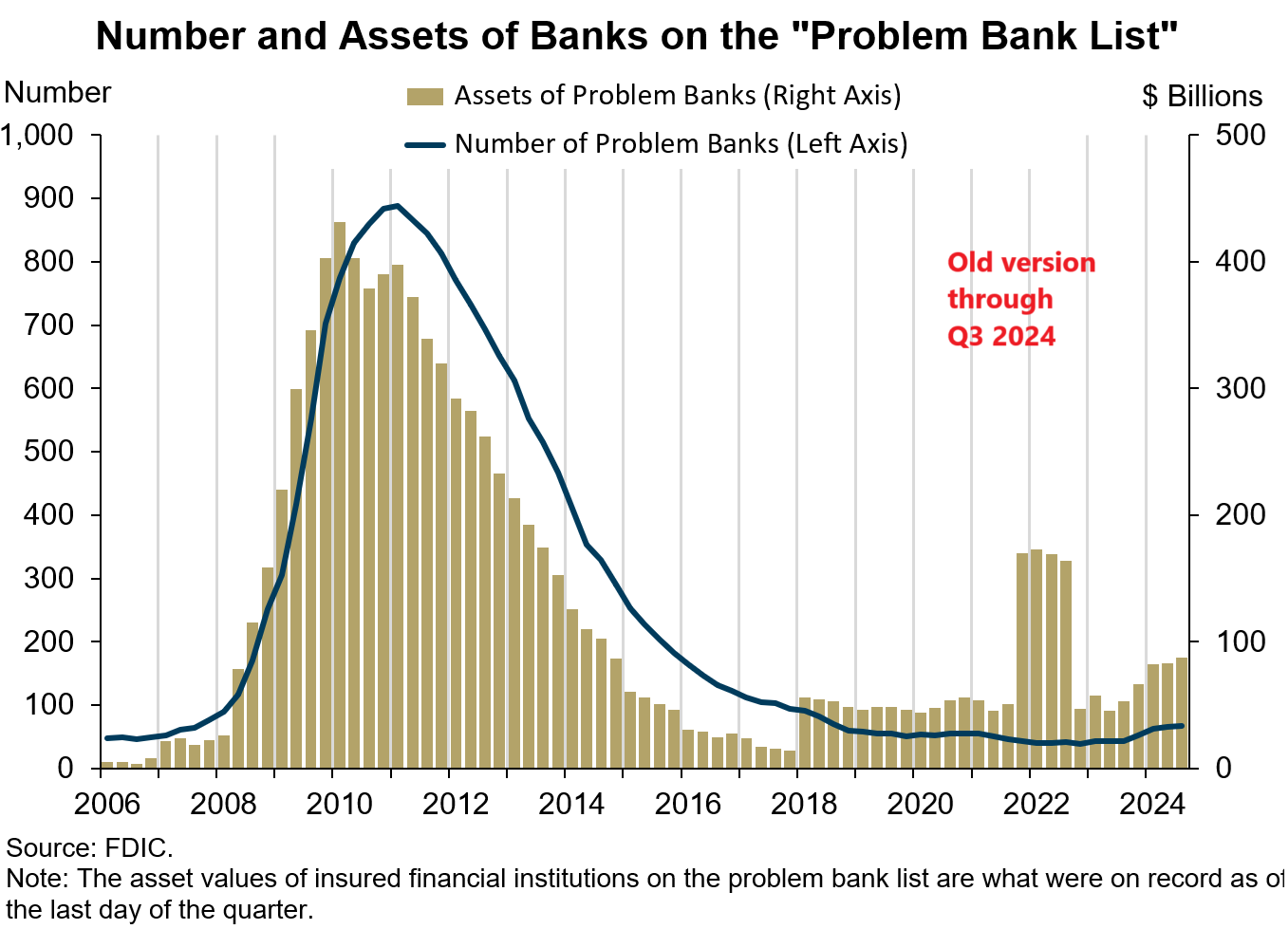

This sudden end of the disclosure is a problem because a jump in assets on the list used to indicate that a bigger bank had gotten on the list, something we’d need to start paying attention to, and now we don’t know if a bigger bank has gotten on the list. We just see the total number – 66 banks in Q4 2024, according to the FDIC today. This is what the FDIC’s chart used to look like through Q3 2024.

In the chart above, by jump in the gold columns in Q4 2021, we could tell that a bigger bank had gotten on the Problem Bank List as assets of Problem Banks spiked. Then, in 2022 SVB went to hell for all to see and finally imploded in Q1 2023, followed by ultimately two other banks. We didn’t know which banks had gotten on the list, but we knew something was going on with one or more bigger banks. And people guessed rightly or wrongly. Now we won’t see that anymore.

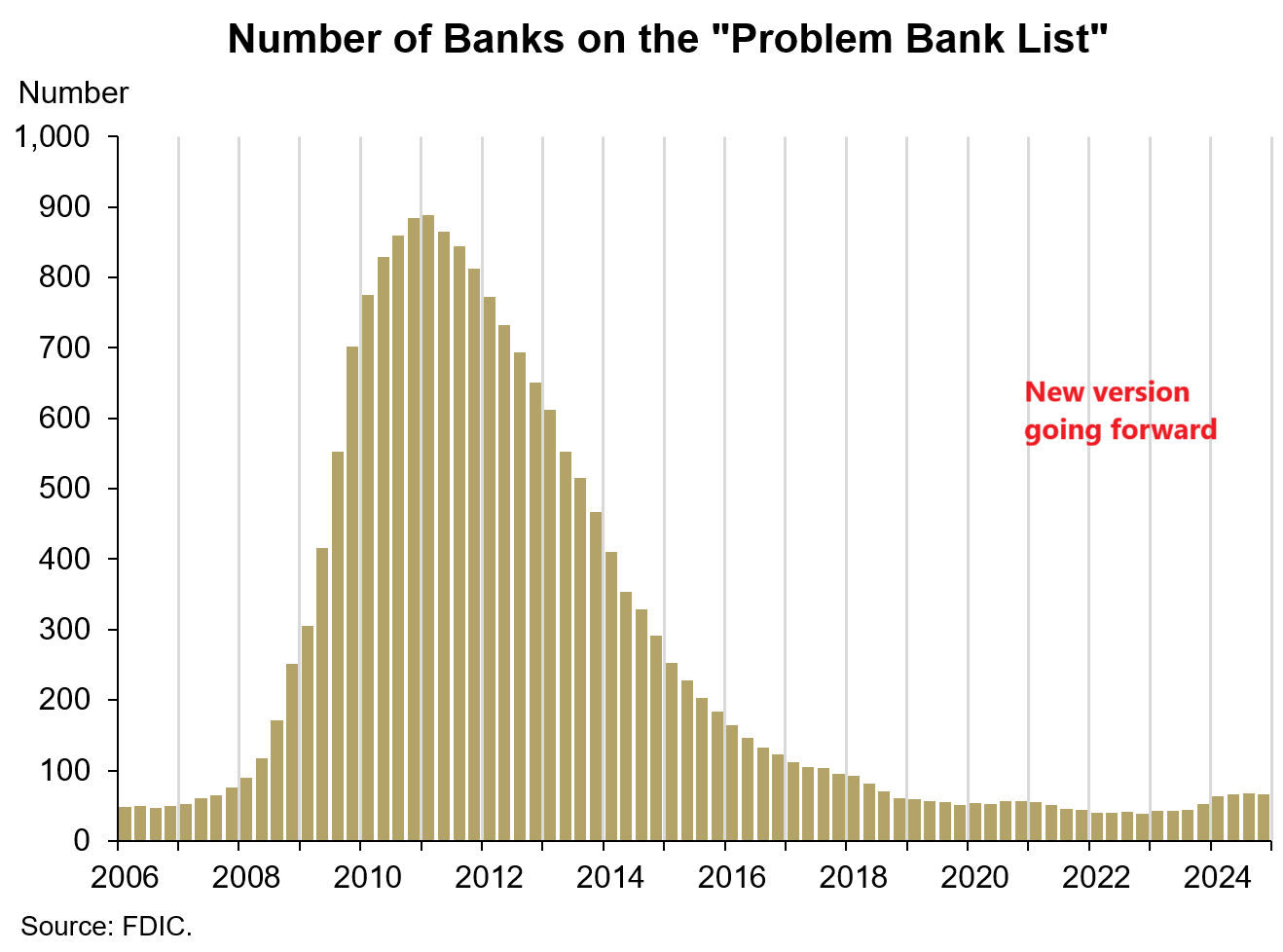

And this is what the FDIC’s Problem Bank List chart looks like today. Q4 2024 is the first time since 1990 that total assets of Problem Banks are not disclosed. The gold columns now represent the number of banks (which used be indicated by the black line), and the total assets data (used to be the gold columns) has vanished:

In the statement, Hill addresses the irony of this act: “Upon becoming Acting Chairman, I issued a statement that noted the FDIC would ‘expand transparency in areas that do not impact safety and soundness or financial stability.’”

That disclosure of total assets of Problem Banks didn’t “impact safety and soundness or financial stability” from 1990 through Q3 2024. And now it suddenly does, and the disclosure gets nixed?

Are “unrealized losses” on bank financial statements next?

Sure, he gave four reasons why this suddenly was necessary:

When a large bank ends up on the list, the public might identify which bank that is – or wrongly identify a bank that is not on the list – and start yanking its money out, “prompting a disorderly run,” he said.

So, that could have happened, but what prompted the run on SVB was the disclosure on its financial statements of its unrealized losses on its holdings of Treasury securities and MBS, and its total dependence on big uninsured deposits by well-connected depositors. So, will the disclosure of unrealized losses on bank balance sheets be next?

He added another reason: “Supervisors fail to downgrade a large bank in poor condition for fear the disclosure could spark a bank run and/or financial instability.” But financial statements of banks could and did spark bank runs, so just replace bank financial statements with bank PR statements full of pap and bullshit? Is that next? To avoid “disorderly runs?”

And he added another reason: “A large bank is downgraded for reasons other than deteriorating financial condition (which, as a general matter, occurs regularly), prompting customers to withdraw funds out of misplaced fear of insolvency.”

Forced disclosures of sins, and fears of the consequences of these disclosures, are part of what is supposed to keep banks from doing stupid things. The purpose of these disclosures is to impose some discipline on banks and bank CEOs; and if they do stupid things, allow markets and depositors to punish them. And the fear of that punishment is supposed to keep banks from doing stupid things. That’s what disclosures are all about. And doing away with these kinds of disclosures isn’t going to make the banking system stronger.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

law of unintended consequences coming right up

no more adults in the room anymore, anywhere

thought i could hide thru what’s coming, but not anymore

wolf, tell us what you really think

He’s already peppered a bunch of opinions in the article:

“And doing away with these kinds of disclosures isn’t going to make the banking system stronger.”

“That disclosure of total assets of Problem Banks didn’t “impact safety and soundness or financial stability” from 1990 through Q3 2024. And now it suddenly does, and the disclosure gets nixed?”

I think Wolf generally reserves broad opinion till he sees broader data points.

I believe Wolf will get those data points in the coming months.

I received this email today…

Now what could possible be wrong with an offer like this? What institutions are selling this paper to “investors”?

==

We have recently added this new product to our lineup. It works great for self-employed who qualify with alternate documentation such as bank statements or 1099s. No tax returns are used to qualify.

Highlights-

Loans up to $500k

LTVs up to 90%

Minimum FICO 680

Fixed rate fully amortized 2nd lien (NOT a HELOC)

Alt-Doc options to qualify (1099 only, Business or Personal bank statements)

Hmmm. Loans up to $500k, and you only need a FICO of 680 or better? Alt-Doc’s accepted.

My first thought is this might be a phishing email. Intending to get your personal info.

meant for income properties

I get them all time

based on LTV

phishing for paid off properties/ones with lots equity

Suddenly sounds like getting a mortgage leading up to the financial crisis. Good we’re doing away with regulations. /s

As we all know, when you sweep problems under the rug, they just magically go away, right? Right?!

I also noticed that the 10yr is now equal to the 3mo at 4.30% as of 2/25. So not exactly inverted, but just on the cusp. Could be a double inversion in the months ahead, who knows? Some say it no longer holds any significance, but as for me, In Yield Curve Inversion I trust.

Update for 2/26: 10yr 4.25%, 3mo 4.31%, 6bps inversion.

Morale Hazard has left the station a lonnnnng time ago.

*Both* moral and morale hazard…

…no moral existence, then moral hazard is, at best, a relative-at worst a null-proposition, ergo: no problem!

may we all find a better day.

Just another case of extend and pretend, or in lay terms, all shit sandwiches will now be considered steak sandwiches.

I don’t understand what the problem is with being transparent about which bank is in trouble. Yes, people will take their deposits and run. But likely to another bank. So i would think the system as a whole would not be at risk.

If it was a rotten tree, you would cut it down to prevent it falling unpredictably.

To think of a possible reason to close the shutters, I’ll have to put on my tin foil hat and come up with a conspiracy theory. Or do i?

It looks like Warren B got the memo early last week.

And now we get a hint that there is something worrisome going one.

i don’t totally agree. you want to avoid a self-fulfilling prophecy, where minor problems cause a bank run that creates major problems.

so “taking their deposits and running” would lead to consolidation where all banks would end up failing except the too big to fail banks. that’s not good either.

i don’t have a good solution.

The Resolution Trust Corp from the 70’s S&L disaster is a good starting point

This is all completely disgusting. But I’m not sure if they’re hiding something this very moment: in fact, all kinds of transparency is being systematically removed across the board. Just believe what you’re told to believe. It’ll come down through the church or from YT and FB; your choice.

No one should be surprised by the dismantling of the transparency and data that drove efficient decision making.

Now a select few will pick winners and losers and the public will have no clue because the signals that inform us would be kept out of side.

There’s a reason why many banks themselves evaluated a Democratic president to be better for the US economy.

This happens at scales small and big, incompetent people will make up data, hide the data or manipulate the data to get away with anything.

“data that drove efficient decision making.”

I agree that hiding the data is a terrible and quite possibly a counter-productive idea (can’t see if something is sh*t?…assume *everything* is sh*t…).

But…to think this latest perversion/stupidity is somehow unique…is to ignore the past 20 *years* of saver expropriating ZIRP that *actively/directly* lowered allegedly free-market rates (using what amounts to forgery in store-of-value terms) in order to finance DC’s agenda (over saver’s interests…literally).

So, the latest is a terrible idea…almost certainly necessary to hide/delay the high probability consequences of decades of terrible *policy* decisions.

When you spend decades incentivizing the creation of crap loans…you end up with a big-*ss mountain of crap loans.

Then what?

What did the Fed think was going to happen?

Rates would never, ever have to go above ZIRP again?

That bond math had been repealed, so unrealized loan losses would magically vanish?

“so just replace bank financial statements with bank PR statements”

I lol’d

A couple of thoughts.

Which large bank was about to end up on the list?

How do they expect this thing to last? It is so retarded and goes against every principle of capitalism.

Expected credit loss models were based on optimistic macroeconomic outlooks and I assume that outside pressure from auditors forced the banks to update them and that is why we have landed here.

Who could have seen this coming? /sarcasm

The FDIC imitating the ostrich.

But deposit insurance was always meant to “paper over” the sins of poor bank management by easing the pain felt by the less informed public AFTER the malfeasance has occurred, so maybe it fits…

Given that banks are regulated by several authorities, is it possible this important info could be provided by one of them? Maybe it’s about time for little competition in the regulatory realm. OCC, FRS, CFPB, state banking examiners? Anyone out there?

There is a ton of bank data available…soooo many data points, my sense is that some of them (or ratios using them) can be assembled to generate rough/very rough proxies of “unrealized losses”.

If nothing else, the mere aging of loans (securities?) in various non-accrual vintages says a lot…a bit more slowly.

That may be the entire point of now hiding the big spicy meatball of unrealized losses…to try and swallow it more slowly.

Quite disturbing to think the Fed is an accomplice in pulling the wool over the public’s eyes. This will obviously play into the plans of the oligarchy.

Why shock *now*?

Via QE (and earlier techniques) the Fed *directly* *confiscated* the economic value of private USD savings…and transferred it to the US Treasury.

Compared to *that*, predictably hiding things is a relative misdemeanor (albeit one with bad consequences).

This is the FDIC making the change, not the Fed.

I agree it’s a step in the wrong direction, and goes against the spirit of transparency being preached by the current admin. Disappointing.

Thanks, I’m hearing the Treasury Dept. will be assuming the role of the FDIC.

Heh…the Fed assumed the role of both the FDIC (by gutting rates to save poorly run banks) and the Treasury (by gutting rates to save a poorly run government) a long, long time ago.

Many employees were fired from the FDIC last week. Perhaps the persons responsible for tracking/consolidating/reporting were among those fired.

“The Fed assumed the role of… the Treasury by gutting rates to save a poorly run government”

No disagreement – BUT the Treasury also assumed the role of the Fed by shifting the tenor of new debt issuance towards the short end of the yield curve in order to push down long-term yields.

I guess both institutions need to stay in their respective lanes?

“…spirit of transparency”

Hahahahahahahahahahahahah

I hope he was kidding. If not, then definitely being sarcastic.

This article is about the FDIC, not the Fed. I don’t see how the Fed is an accomplice.

Regulatory capture.

I remember the first cracks in the system showing up in early to mid 2007, then spiraling into 2008 when the mainstream news started admitting problems. Back then one of the things that happened was revealing information was changed or reduced as the problems got worse. So here we are again?

Banks are for borrowing money FROM. Never for lending money TO. There are better and safer ways of storing your cash that avoid the opaque banking system.

What, if anything can be done by we the people? To whom do we direct our protest and raise the alarm? Wondering whether whinging to our Congresscritters would matter in the slightest, and especially, what is it we’d want to say, which would serve to help get their heads out of their backsides of fundraising? This, since financial media aren’t to be trusted to do it for us, other than the likes of Wolf.

We can write to authors at a range of national publications, like the WSJ, New Yorker, Fox Business, Bloomberg, and tell them they’re all fools if they don’t follow and cover this story. I think that’s a good place to start.

Posting about it in their comment sections is also a good idea.

nothing. there’s a reason the far right is gaining support throughout the western world.

there’s nothing that can be done short of a collapse and a reign of terror.

as mark twain wrote “history doesn’t repeat itself, but it often rhymes.”

When there is a run, a solvent banks gets funding from the Fed so it gets through the run. But the Fed doesn’t lend money to insolvent banks, and that’s what happened to SVB et al.

I’m always impressed that there’s still remaining tricks up the sleeve to keep the party going.

Reverse Repo Market almost depleted, uh oh, excess liquidity almost gone, what to do, what do to, ah ha, let’s remove disclosures slowly, that’s the trick.

In terms of reverse repos on the Fed’s balance sheet (ON RRPs), which is what you’re talking about, that was excess cash in the money markets (markets for short-term liquidity). But excess cash in the banking system is reflected in the “reserves” on the Fed’s balance sheet, and they really haven’t come down much, they’re still at $3.27 trillion, same as when QT started, and there is still a huge amount of excess cash in the banking system.

This pile of money can be used in many ways. One wonders what the hive minds on wall street have come up with, e.g.,

1) More yield curve games if the Fed were to reduce the reserves rate to meaningfully less than targeted .gov bonds. The pile is so large that treasuries etc. are the only place they could go.

2) Some new Fed/Treasury acronym program that would “force” this money out of the Fed system and “into” the economy in the event of a recession type event.

3) Shenanigans. Well, ignoring the risk free return that is currently being received.

The more they try to hide things, the worse shape you know those things are in. This is what moral hazard gets you, a bunch to clowns that know they’ll get bailed out no matter what. Govt should’ve taken them all to the woodshed last time. Idiots.

Here here! *Repeatedly hammers Wolfstreet mug into table in vehement agreement*

P.S. It’s due time I write Wolf a check and get me a mug.

Hear hear* my teachers scolded me for not proofreading before turning in my assignments. Still haven’t learned my lesson.

Wolf, could this be construed as an end around QE? if banks do not disclose bad loans then what’s to stop them from simply going on mac daddy supper lending spree just for the sake of more bigger commissions. Sort of like what happened in the 2007 era… When banks lent to everyone with or without a pulse with stated incomes… and pick a payment plans.

Yes sir, wallstreet gonna pop on this news for sure.

“…could this be construed as an end around QE? if banks do not disclose bad loans then what’s to…”

No, this is not at all what this is about. Banks still have to disclose bad loans. This is about the list of banks that the FDIC considers “Problem Banks.”

I was thinking the only way a bank can be a ‘problem bank’ is by handing loans that become bad underwater loans. My bad

That’s one way, but that’s not what happened in 2022/2023, and that’s not why these banks got on the Problem Bank List. The loans of SVB and First Republic were perfectly good.

But these banks had huge unrealized losses on their huge holdings of long-term Treasury securities and MBS. Those unrealized losses are a result of interest rates surging (market prices of bonds drop when yields rise). A 30-year Treasury bond bought at auction in mid-2020 lost over half its market value by 2023 due to the surge in interest rates. The holder will get face value at maturity in 2050, but until then they’re priced at market. Those unrealized losses exceeded the bank’s capital, and they were therefore insolvent and collapsed in March 2023 when the run started. They had made a big bet in 2020 on long-term Treasury bonds and MBS that blew up due to interest rates, while credit was pristine. This “duration risk” is a huge problem for banks if they don’t hedge properly, which is why they’re required to report these “unrealized losses” on their balance sheets.

Wolf,

In reality isn’t it pretty hard to see this as anything other than an implicit acknowledgement that one or more systemically important banks is on the brink of having to disclose very large, *new* (read aged) unrealized losses/some related deterioration – but only to regulators.

I get the bit about avoiding a run (threading the needle (again) by treating depositors like mushrooms – keep them in the dark and feed them…-) but closing down the flow of information isn’t going to fool too many people who have heard of the internet…instead it could trigger a *systemic* panic (don’t know which biggest banks are crappiest? Safest to assume they are all crappy).

Wonderful use of graphs! When two curves generally move together, nothing special is happening. Those sudden popups in 2022 are salient.

Bye Bye King Dollar!

It isn’t that hard to figure out which banks may be in trouble. Insiders have begun selling their shares. All you need to do is google it.

And what a surprise. One of them is a big holder of derivatives.

Right. Derivatives. Good thing everything is so stable and predictable right now, no surprise risks have actualized in the past month…

…

Crap. We’re all living in the walking ghost phase at the moment, aren’t we?

I wonder how many sour CRE loans involved.

Now we’ve talking! A very interesting article of interest, with pertinence to today’s world, which is outside the bounds of the weekly wash, rinse repeat cycle. Very good, Wolf!

Now, excuse me as I go outwit the rest of the plebs and go make a withdrawal “.

That South Park episode sums it up perfectly –

“And it’s gone!” If anyone hasn’t seen that clip, please go to the (video site) to see it.

I guess with bank runs, that old saying sums it up perfectly – the early bird gets the worm. Although, when I go to my bank, I’m not lookin’ for no worm!

In that episode, they way they depict decisions being made at the Treasury probably isn’t far from the truth…

The CEO of JPM just unloaded $237.7 Million of his company stock a few days ago. 🤔🤓

Maybe he is buying a new yacht?

One more reason to be in short term Treasury bills.

Lie through omission. Nothing screams modern era more than changing the rules of the game to avoid consequences. No point playing by the rules, just go so far and so big that you can change the rules in the end.

like playing chess with a child.

corruption

In the computer science business, the kind of reasoning embraced here by the FDIC is referred to as “security through obscurity.” And it is roundly derided, as it should be.

Thank you for shining light on this troubling policy change, Wolf.

…as opposed to an “orderly run”?

❤️🤣

My bitcoin aint doing so hot

Gold fine.

I’m not a fan of crypto, but if people really believed that bitcoin’s price at 100k was justified because of its supposed characteristics, they can now get it on sale. But there are reasons to avoid it. The govt could ban it like in China, many other tokens could have a limited supply, proof of work too, etc.

You can still track the Texas Ratio if you are concerned!

The Government does what it pleases. It doesn’t take a genius to know banks are in trouble because they hold treasury bonds with low yields. This year about $9 trillion are rolling over and will be refinanced by the treasury at higher yields. Interest costs on federal debt will just from $1.1 trillion last year to a much higher number, perhaps as high ast $1.5 trillion in total interest costs by the end of the fiscal year. America has been on the cusp of a debt implosion for years and the debt number is getting worse. Despite DOGE I expect debt to increase almost $2 trillion this year to $38.5 trillion. Increments of this size will in time cause a national bankruptcy with the FED forced to buy the bonds, just as Japan has done for over 20 years. Expect yield suppression by the FED just as they did during the COVID crisis which directly caused the house price bubble when 30-year mortgages got as low as 2.65%. Of course people will buy homes, condos and real estate when money is essentially free to borrow. We had a fake bank print fake money at fake interest rates to jack up our fake economy and fake GDP. They printed way too much money during the COVID crisis and it caused the worst inflation in 40 years. Asset classes were inflated as well. All this debt is an enormous risk. The Great Depression was largely liquidation of debt and it lasted 20 years. Debt to GDP is far worse now than it was in 1929.

The house reconciliation just passed extending tax cuts included a provision to add 20 trillion 8n debt in 10 years…1 republican voted no who brought this fact up…1…it’s ALL SCRIPTED, it’s why our presidents come from Holly weird…it’s occultic also…

Gazill,

It’s the failure of the Tea Party. They rolled into Congress collectively as the largest group we’ve ever seen and their self-appointed job was to cut back on spending. But what happened? They folded, got picked off one by one by Washington swamp creatures and the Tea Party caucus ceased to exist. Murdered essentially. Haven’t seen or heard from any fiscally responsible group of GOP’ers ever since.

…appeared more to me that the expression and election of their feelings of general anger were sufficient for them, without presenting a truly-reconstructive, flexible, and cohesive vision for the nation’s 21st-Century economy. The term, as I recall at the time, was: “…the barking dog that caught the car…”.

may we all find a better day.

It’s only after the implosion has happened that all the self-declared geniuses will say, how it was all bound to happen, that it was inevitable, that they could see it happening two, even three, years ago. How anyone “with any sense” could see it coming.

When their only qualification at that point, writing about the collapse in the more highbrow mainstream media is nothing more than a degree in hindsight, which we all have.

Despite what you, and today Elon Musk, say, countries do not go bankrupt. They simply print more money, leading to hyperinflation, like we saw with Zimbabwe and Weimar Germany. For example, at a bakery: “I’d like to buy a loaf of bread with my wheelbarrow full of twenty dollar bills”.

Denial is not a strategy, plan, or solution, but it is often fatal. The FDIC’s decision should really not be a surprise to anyone as for the most part, one of the current administration’s primary policies is to remove, suppress, eliminate, restrict, and/or outright prohibit vital information from being made available to the public. Look no further for an example than the restrictions applied to federal scientists from being able to work on climate change research and reports or information being removed from the White House’s website.

One of the more famous quotes from the book 1984 is simple – “The Party told you to reject the evidence of your eyes and ears”. Right in front of your eyes, ears, nose, mouth, and brain, the Party is telling you to reject your own intelligence and somehow believe that removing critical information related to the size of the bank in trouble is not important. Yeah, right, go ahead and feed me some more BS. This is like saying that a company that has 1,000 customers, and only 10 are having trouble paying their invoices. Ops, I forgot to mention that one of the 10 represents 30% of our annual sales and comprises 40% of the total receivables owed to the company.

Unfortunately, I would anticipate these types of denials, misinformation, lies, and outright disinformation campaigns to continue for the foreseeable future until some type of spectacular, if not catastrophic, financial accident occurs which of course will be blamed on anyone and everyone except the current administration. So I would offer you these two pieces of advice to navigate what is surely going to be a very turbulent period.

First, self and direct education will take on an entirely new meaning over the coming years. If you rely entirely on the “party” or “state” (or whatever you want to call it) for your information, you’re doomed and will become nothing more than a sheep being lead to slaughter.

Second, although it may become increasingly difficult to seek out sound, credible, and reasonable information/knowledge, it will be imperative continue to engage with sites such as Wolf Street. No matter how hard they try, math, data, logic, science, and knowledge cannot be eliminated via hitting the “delete” button.

Tage – spot on.

may we all find a better day.

…or, as attributed to a sotto-voced Galileo: “…it STILL moves…”.

may we all find a better day.

This is only the beginning, and only a minor step towards data opacity. It will be interesting to see if and how Wolf’s analysis evolves as this country continues down the path of falsified data. Hopefully we don’t get to the point of Internet censorship, we’re probably closer than many here would think.

“Hopefully we don’t get to the point of Internet censorship”

That ship sailed long ago.

Despite Trump administration #1 trying to roll back Net Neutrality, it persevered. If you think the Internet is censored in the US, you’d be in for a rude awakening if you lived in China or North Korea. We have it good, at least for now.

The ten year is at 4.25. Something is up. Bank stuff? Oh boy..

Decisions like this actually make me think banks are in more trouble than I thought.

FDIC insures for $250,000. If you like your bank and like a simple life, you can easily increase that number using a “Deposit Placement Agreement”. This moves any money over $250,000 to some other bank, yet you keep track of it at your bank, it does all the bookkeeping. My bank even pays the same interest rate on it, even though the money is at another bank. I don’t need to use this option anymore because I am now into T-bills.

In any case, we have learned that the FDIC will bail out depositors exceeding the $250,000 limit, as we saw with Silicon Valley Bank.

So I wonder what the FDIC is afraid of by reducing transparency. Like I said, it makes me think banks are in a lot more trouble than I had originally thought.

Are they reducing transparency so they can “fix”a big problem quietly and not cause financial or public harm to the bank?

Perfect article to be summed up by a favorite Wolf quote. Remember folks, “Nothing goes to heck in a straight line.” Critters in Washington have been reading Wolfstreet.

What do you think happens when we can no longer even *see* the line? Surely nothing will go to heck… /s

The Redaction Reduction Act must be in play. Obviously accomplishing another case of needed force reduction of Watchers Watching their Watches on their Watch. And with that,

Oh Elon, you’re emails all will fly aflusk.*

And Oh Elon, you’re words they are so brusque.

And Oh Elon, I know you are the Candy Musk.

And Oh Elon, let us fly…to Mars..at dusk.

I am the Candy Musk.

I’ll jab you with my tusk.

I am the Candy Musk.

I fly to Mars at dusk!

[*New word copyright claim..Aflusk, meaning widly scattered.]

It’s dawning on the markets that they are in trouble with these jokers.

At the time SVB failed, most USA banks were holding unrealized losses . Banks had purchased long date Treasuries and Mortgages. Their prices move inversely to interest rates. As long term rates went up, these assets devalued. The longest term treasuries lost 50% of their value.

At the time of the SVB failure I was thinking most USA banks were 10% to 20% underwater due to these unrealized losses. I was expecting most banks in the USA to fail in a massive bank run that would dwarf 2008 and the Global Financial Crisis.

Always watch your FDIC limits. If you have more than $250,000 in your bank, open an account at a different bank and move the excess so as to stay within FDIC limits.

Some banks are “too big to fail” (TBTF) also called “systemically important”. The government must shore them up at all cost because the failure of a financial giant could be devastating to the economy. The list is here:

https://en.wikipedia.org/wiki/List_of_systemically_important_banks

It is best to have your assets at a TBTF bank. These are less likely to fail. Not impossible, but less likely to fail.

Phil,

“too big to fail” (TBTF) list is all BS. Anybody who has paid attention to the history of banking in America, its kinda obvious that JP Morgan Chase is really the only TBTF. If there is a fire on Bank St… Wells Fargo, BOA, Truist, Citi, will just be burning to the ground while all the firefighters will be putting water on the JP Morgan building. They all will go before Chase goes. Believe that

Doesn’t seem like a strong and resilient banking system… Maybe more like a fragile and worsening crisis

Wolf,

Considering how often banks fail, and their totally different business models, is money parked in a big brokerage like Fidelity/Schwab “at least as safe, if not safer” than money parked in a big bank like BofA/WFB?

I’m sure the answer would be of high interest to the whole group!

Thanks.

Money in a brokerage is insured by SIPC not FDIC. The limit is $500K for the brokerage account with a limit of $250K on cash and cash equivalents.

For example, if you have $200K in Treasury bonds and $260K in Money market (total $460K) and the brokerage fails, SIPC will pay you the $200K for the bonds but only $250K for the Money Market because the Money Market is over the limit.

Brokerages are a lot different from banks. If you are using a broker, you should not be holding a lot of money in its “cash” or “settlement” account. Like almost nothing. For example, I buy a lot of T-bills using Schwab. If Schwab goes belly-up, I have a record of all my T-bills which I can present to Treasury if I choose to sell them. Schwab kindly keeps track of my T-bills, but if it goes bankrupt, I still own the T-bills. Schwab has nothing to do with the ownership of the T-bills I buy, other than it keeps track of them.

Schwab does not charge to buy or sell Treasuries. It makes money by hoping you put a lot of money, even just for a few days, in its cash or settlement account which pays a meager .45% last I looked. I deal with this as follows: I buy a new T-bill at auction, for say $50,000, which settles on the exact day that an old $50,000 T-bill matures, so I end up never having any money in the cash (or settlement) account for that transaction. That’s the game I play with Schwab. I don’t know how Fidelity or Vanguard work.

You are correct and I hadn’t thought of that before.

The description of what is and is not covered by SIPC protection is given at their website:

https://www.sipc.org/for-investors/what-sipc-protects

TO QUOTE: SIPC only protects the custody function of the broker dealer, which means that SIPC works to restore to customers their securities and cash that are in their accounts when the brokerage firm liquidation begins.

SIPC does not protect against the decline in value of your securities.

MY ASSESSMENT: In a brokerage, the cash or settlement fund is almost always a mutual fund with the price per share fixed at $1.00. The money in this account is denominated in SHARES not dollars.

For example, in my Vanguard account the settlement fund is Vanguard Federal Money Market Fund (VMFXX). All other brokerages have a similar fund.

SIPC protects against missing assets in your account, but des not protect against decline in investment value.

If the brokerage goes bankrupt and funds are missing from the mutual fund used for settlement, this will cause a decline in the Net Asset Value (NAV) of the fund. For example, the settlement fund could drop its NAV from $1.00 to $0.50 per share.

In the example I gave above, where $260K is held in the brokerage cash account, this would cause a 50% decline in vlaue to $130K. This loss would NOT be insured by SIPC.

Thus, you ae correct. Money in a brokerage setteltment accoutn is NOT safe.

Your brokerage may park your cash in an FDIC-insured sweep account. Schwab does this and pays almost zero interest.

“We need to make sure you don’t protect your assets (actually we consider them ours) from our friends’ poor financial choices”

– The FED