This is about stock market craziness, not about solar power.

By Wolf Richter for WOLF STREET.

This is about stock prices that get inflated beyond recognition on nothing but wild mania, and when the mania subsides, the stocks collapse and are inducted into our pantheon of Imploded Stocks. And we’re going to look at eight of these imploded solar stocks.

This is not about solar power. Rooftop and utility-scale solar installations are now a fairly large business. Utility-scale batteries have become a profitable way of arbitraging the highly volatile electricity spot prices that can spike during high-demand hours and plunge during low-demand hours, and in this arbitrage, batteries work well with big solar installations, buying electricity when the price is low, and selling when it’s high. And they work well with small-scale solar too. Some of the eight companies here are involved with both solar power and energy storage.

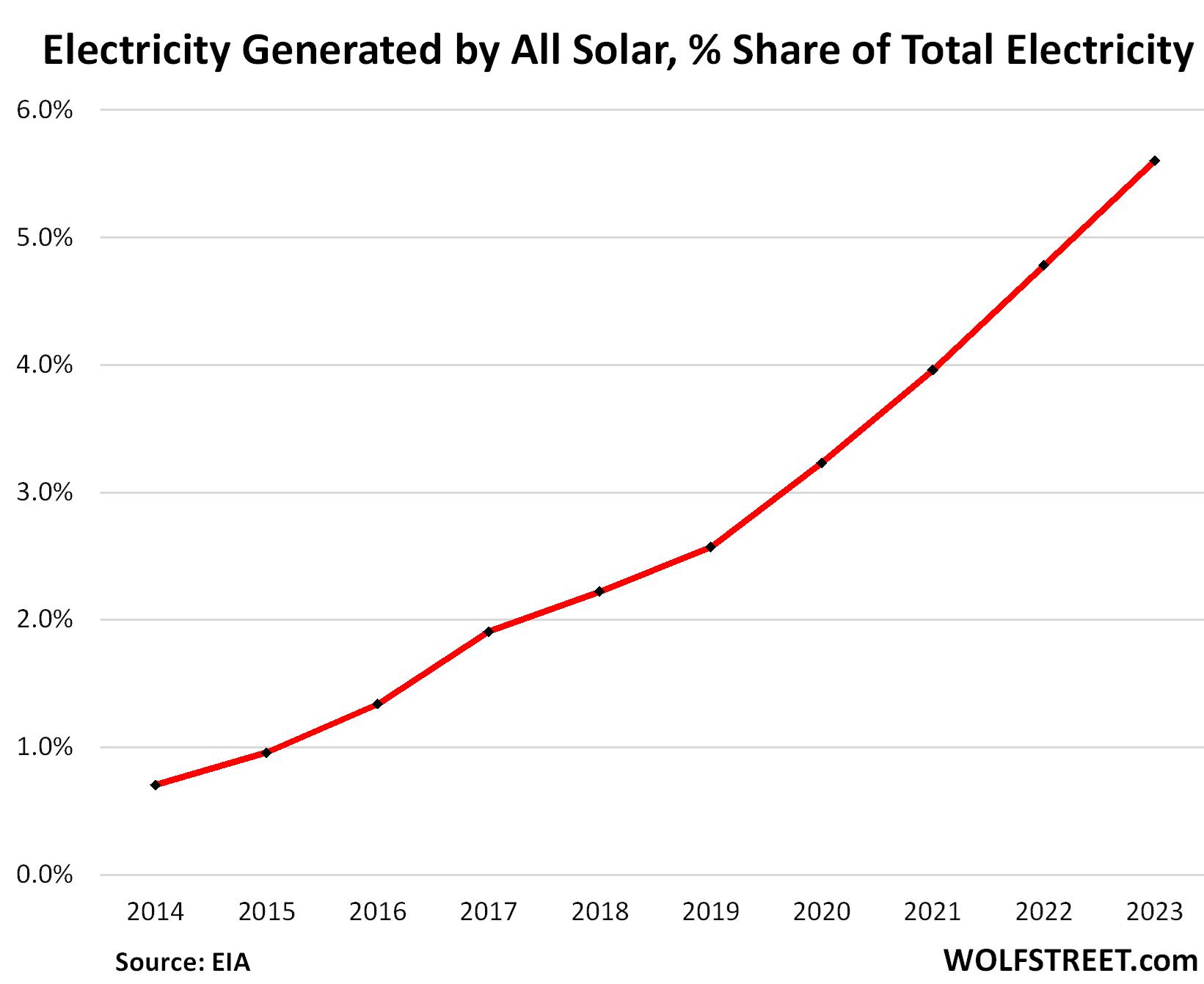

There are up-front costs with solar power, as there are with every power plant. But with solar, the “fuel” is free for the life of the installation, and the math has been getting better as the price of photovoltaic panels has come down over the years. In 2023, the share of electricity generated by small-scale and utility-scale solar installations rose to 5.6% of the total electricity generated in the US.

The eight companies here are sort of pure-plays in the solar-power field. Big utilities are all over solar power, as are big equipment providers, and of course, Tesla. But these eight companies here are specialized players, many of them with over 1,000 employees at the peak, and with hundreds of millions to several billion in annual revenues.

Globally, about 85% of the photovoltaic panels are manufactured in China, which is also its own biggest customer. Vietnam is #2 with a share of a little over 3%. There are some efforts underway to boost manufacturing of photovoltaic panels in the US, to not be so totally dependent on China. But that will take a while to pan out.

This is about stock market craziness, not about solar power.

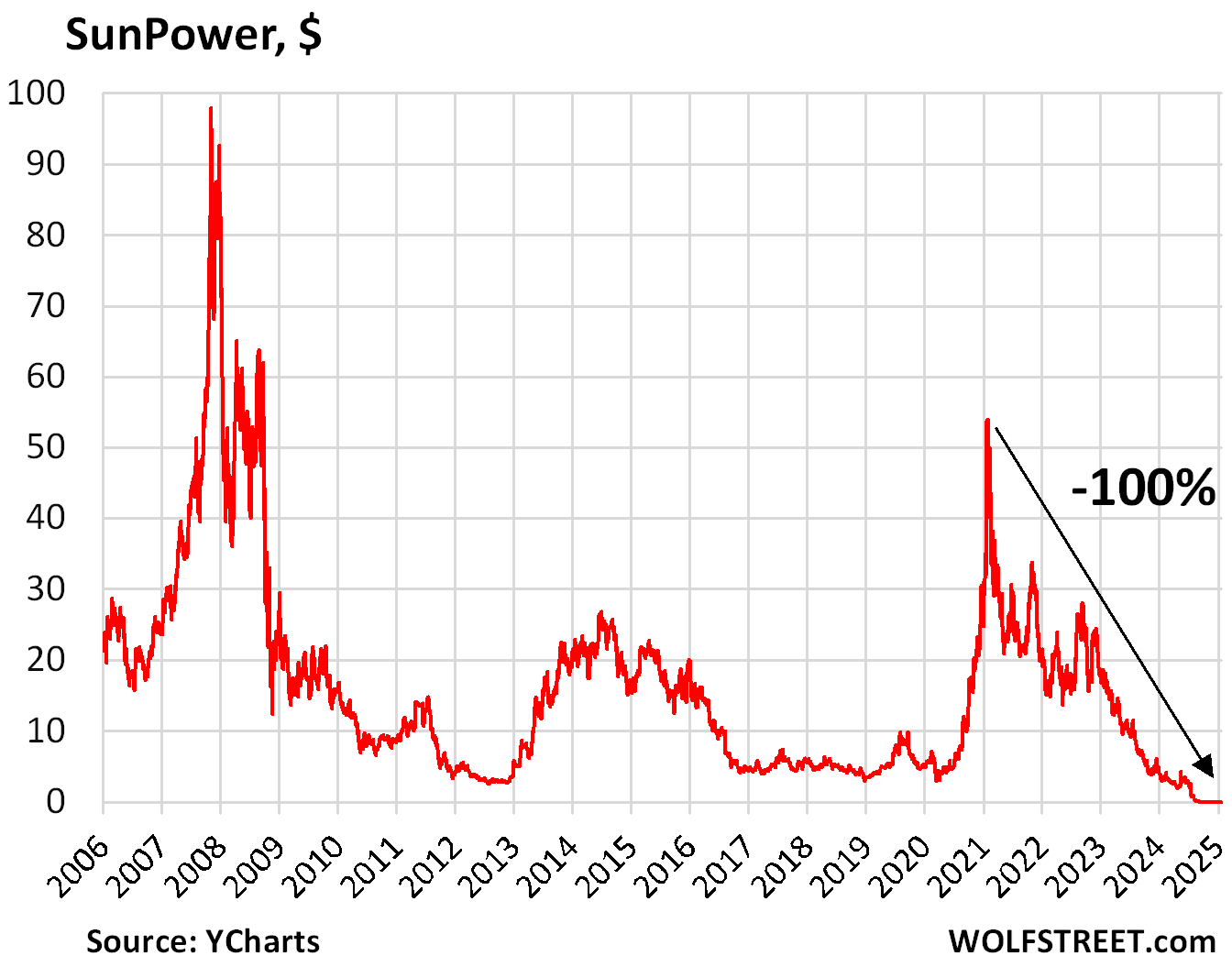

SunPower has been around for a long time. It went public in 2005 as a spin-off from Cypress Semiconductor. It was one of the big boys at the time.

Its stock experienced two huge bubbles. The first in 2006-2007 when it went from $20 a share to $100. The second started in May 2020, when free money turned brains to mush, and the stock multiplied by 12, from $4 a share to $54 a share in about 18 months to peak in January 2021. Then it collapsed.

There was a mix of operational issues, years of substantial losses, accounting issues, missed filing deadlines, defaults, etc., etc. When it could no longer raise new cash to burn, after it had already burned everything it had, it was over.

In August 2024, SunPower filed for bankruptcy. Most of its assets were acquired by solar SPAC Complete Solaria for $45 million (more in a moment), and SunPower’s shares and investors got wiped out.

This stuff happens. What was crazy were the two spikes in share prices on nothing but mass-mania, and after it subsided, the stock collapsed to zero (data via YCharts).

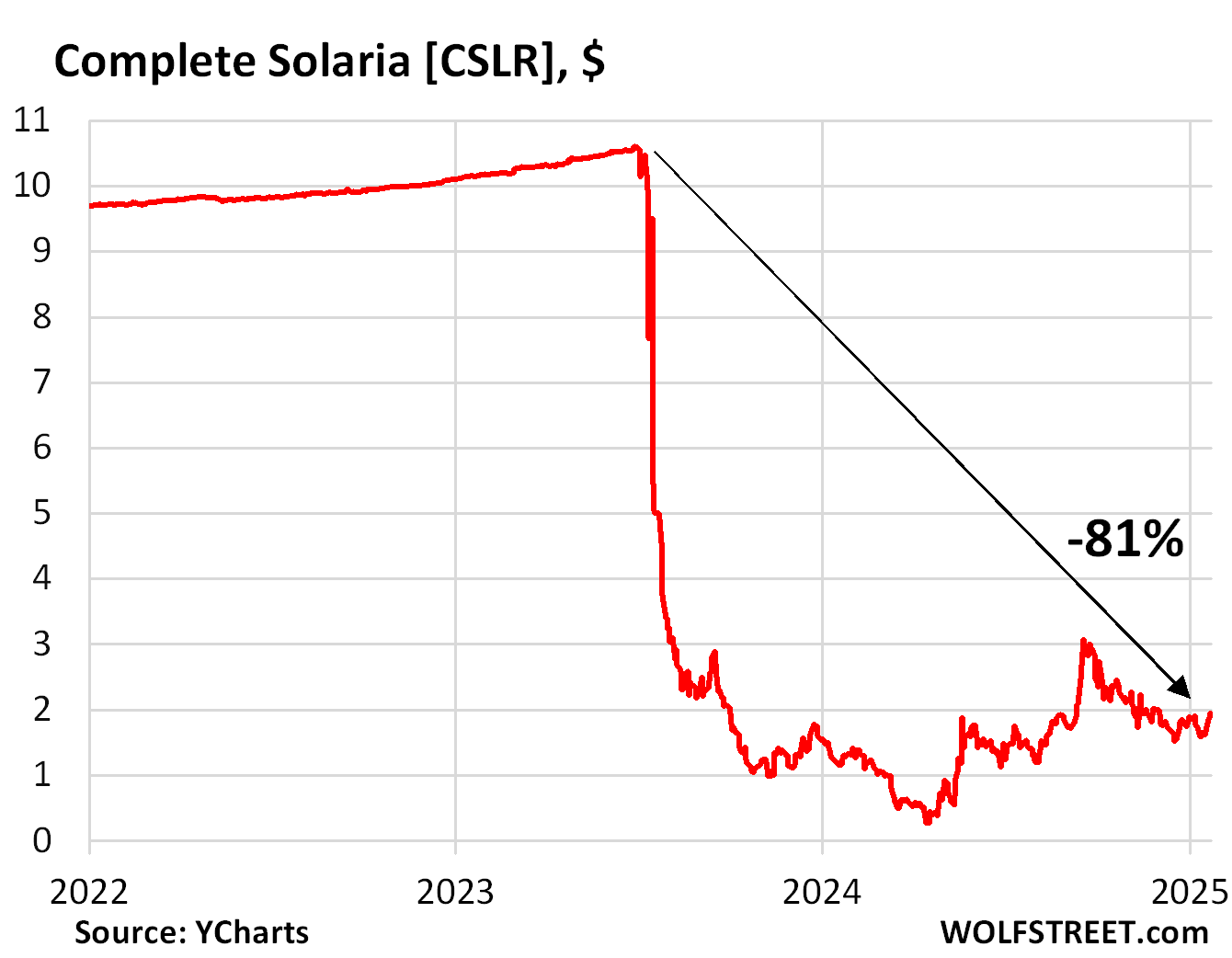

Complete Solaria [CSLR], the residential solar systems provider that acquired SunPower’s assets for $45 million, had gone public via merger with a SPAC in July 2023, an amazing feat, given that the ignominious SPAC bubble had already collapsed. From the merger-share price of $10 a share, the stock has plunged by 81% to about $1.90 currently, including a slick rug-pull right after the SPAC merger was completed (data via YCharts).

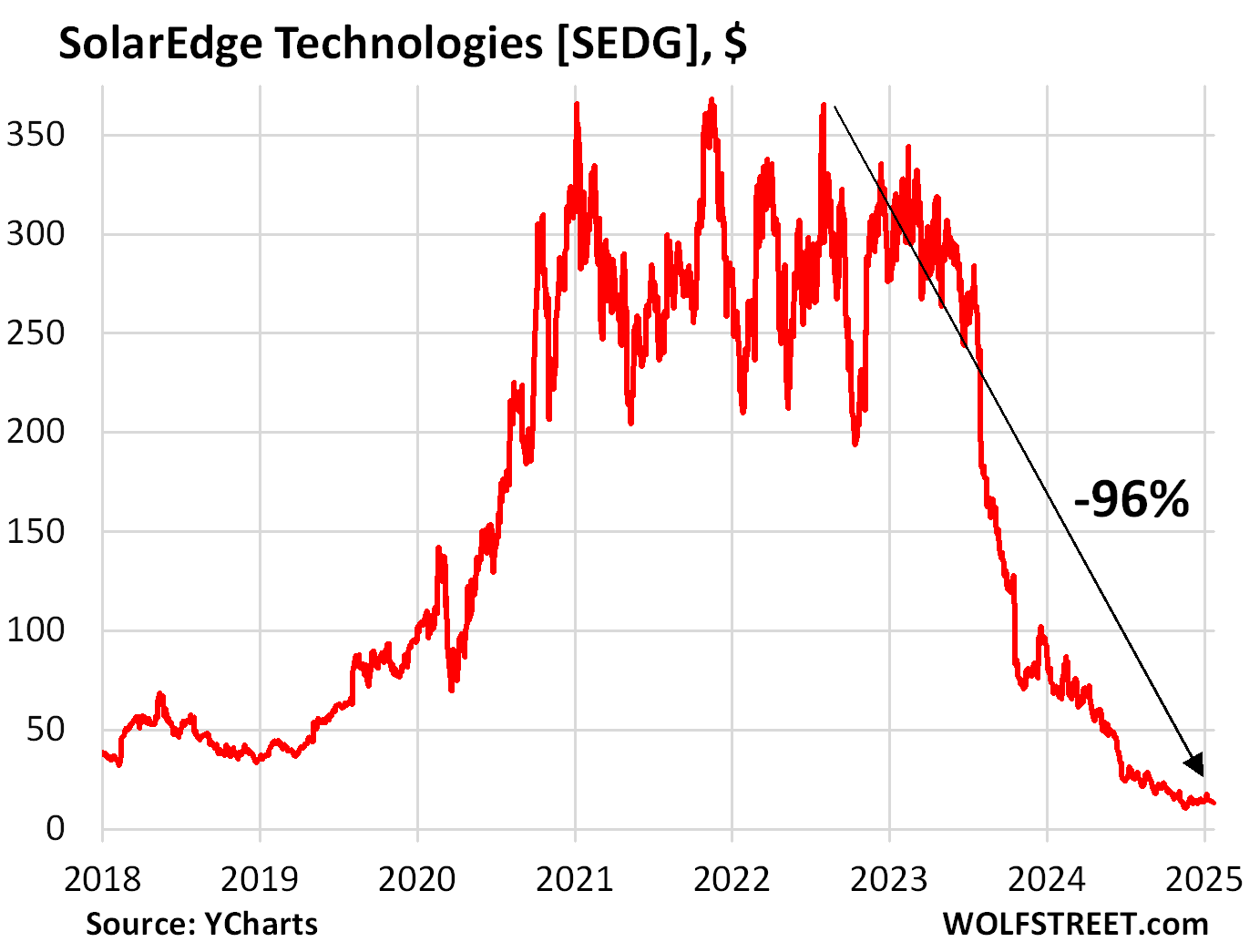

SolarEdge Technologies [SEDG] makes inverters, batteries, power optimizers, and other equipment for solar systems. Back in 2015, when it went public via IPO, SolarEdge made a deal with Tesla Energy to provide inverters for Tesla’s Powerwall. But eventually, Tesla produced its own inverter.

The company, which is headquartered in Israel and is largely active in Europe, made several acquisitions: In 2018, it acquired a major stake in South Korean maker of battery cells and batteries, Kokam. In 2019, it acquired a majority stake in Italian EV powertrain manufacturer SMRE, and it acquired UPS maker Gamatronic. In 2023, it acquired UK-based software-as-a-service provider Hark Systems.

In prior years, the company booked some net income, but over the past five quarters, it booked massive losses, totaling $1.72 billion, including $1.2 billion in Q3. And sales collapsed in 2024, including by 65% in Q3 2024.

The stock price had multiplied by 10 between early 2019 ($36 a share) and January 2021 ($360 a share), then plunged and spiked a few more times within the same range, before the big kathoomph in the second half of 2023. The stock has now plunged by 96% from the triple peaks in 2021 and 2022:

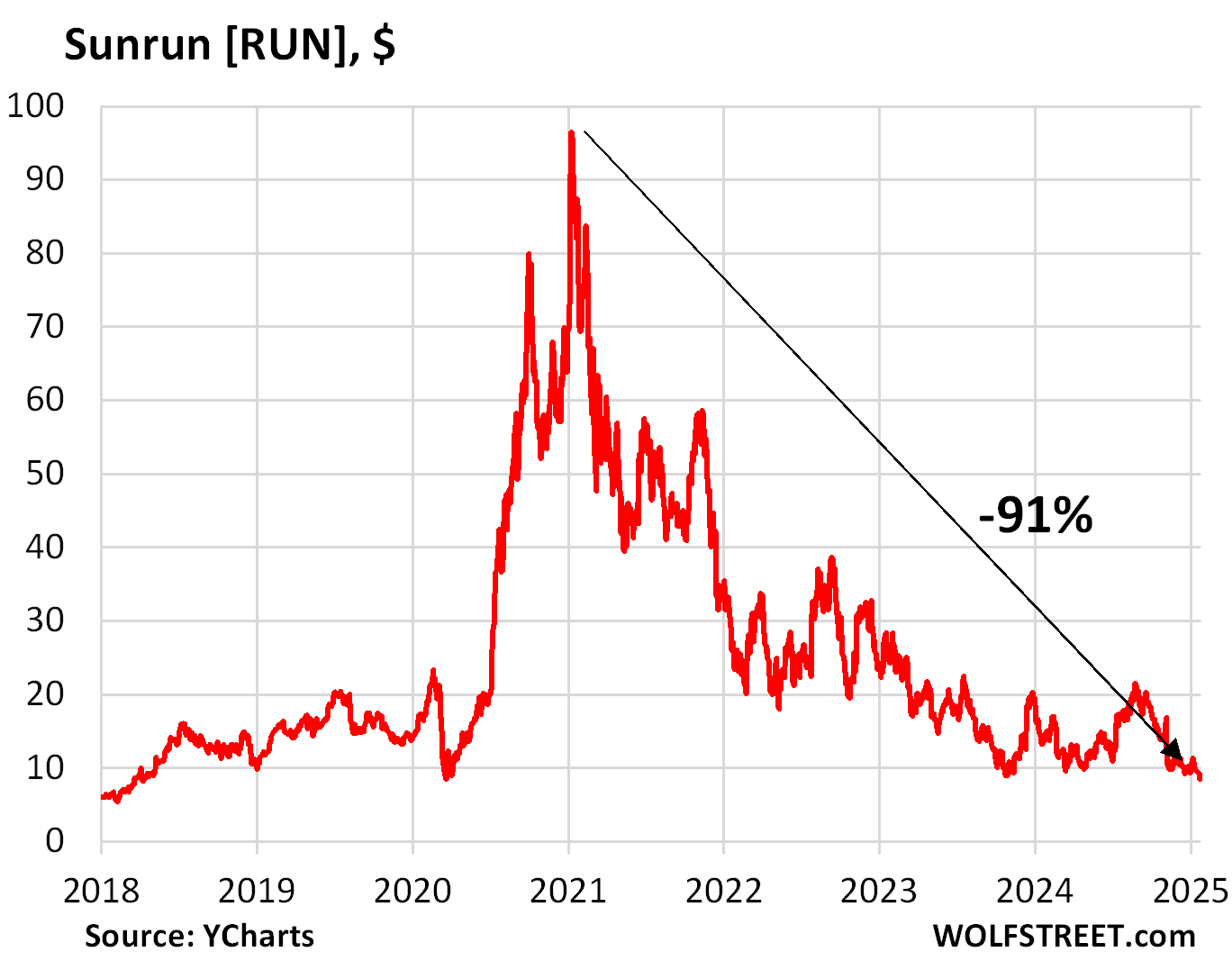

Sunrun [RUN] makes and installs residential solar systems that it sells as a subscription or financed purchase. The company, which is based in San Francisco, went public via IPO in 2015. There had been some profitable years, but over the past five quarters, it lost $1.45 billion.

The stock had multiplied by 11 between April 2020 ($8.36) and January 2021 ($96.50), but then collapsed and today, closing at $9.23, is down by 91% from that peak.

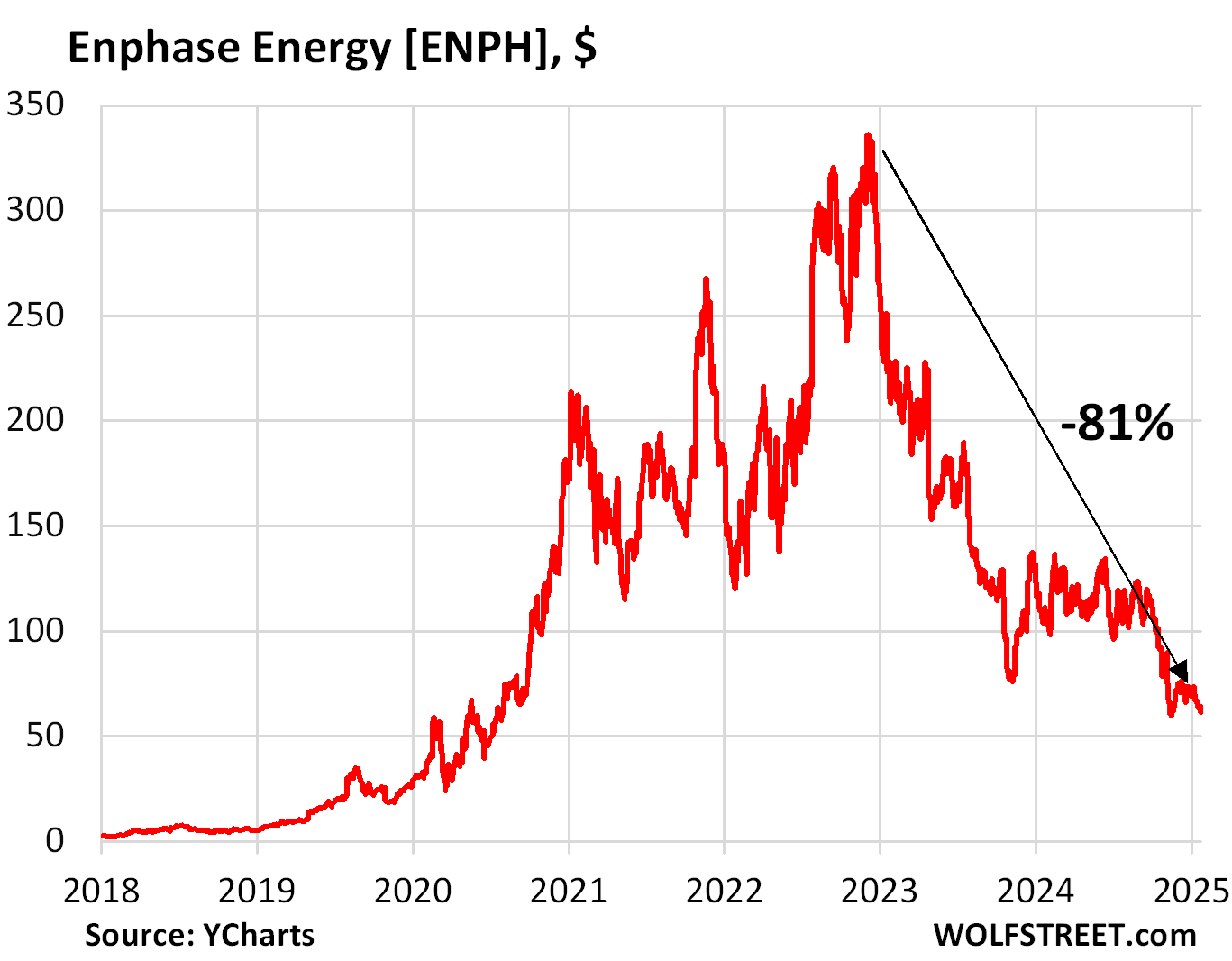

Enphase Energy [ENPH], makes equipment for residential and business solar and storage systems, and EV chargers. After the California-based company had gone public via IPO in 2012, its stock wobbled along the single-digit-dollar line for years. But then in 2019, it took off and multiplied by 48, to $336.00 in December 2022, before collapsing. Today, it’s down by 81% from that high.

The company has been mildly profitable. But revenues declined since 2023, including a 31% year-over-year plunge in Q3 2024.

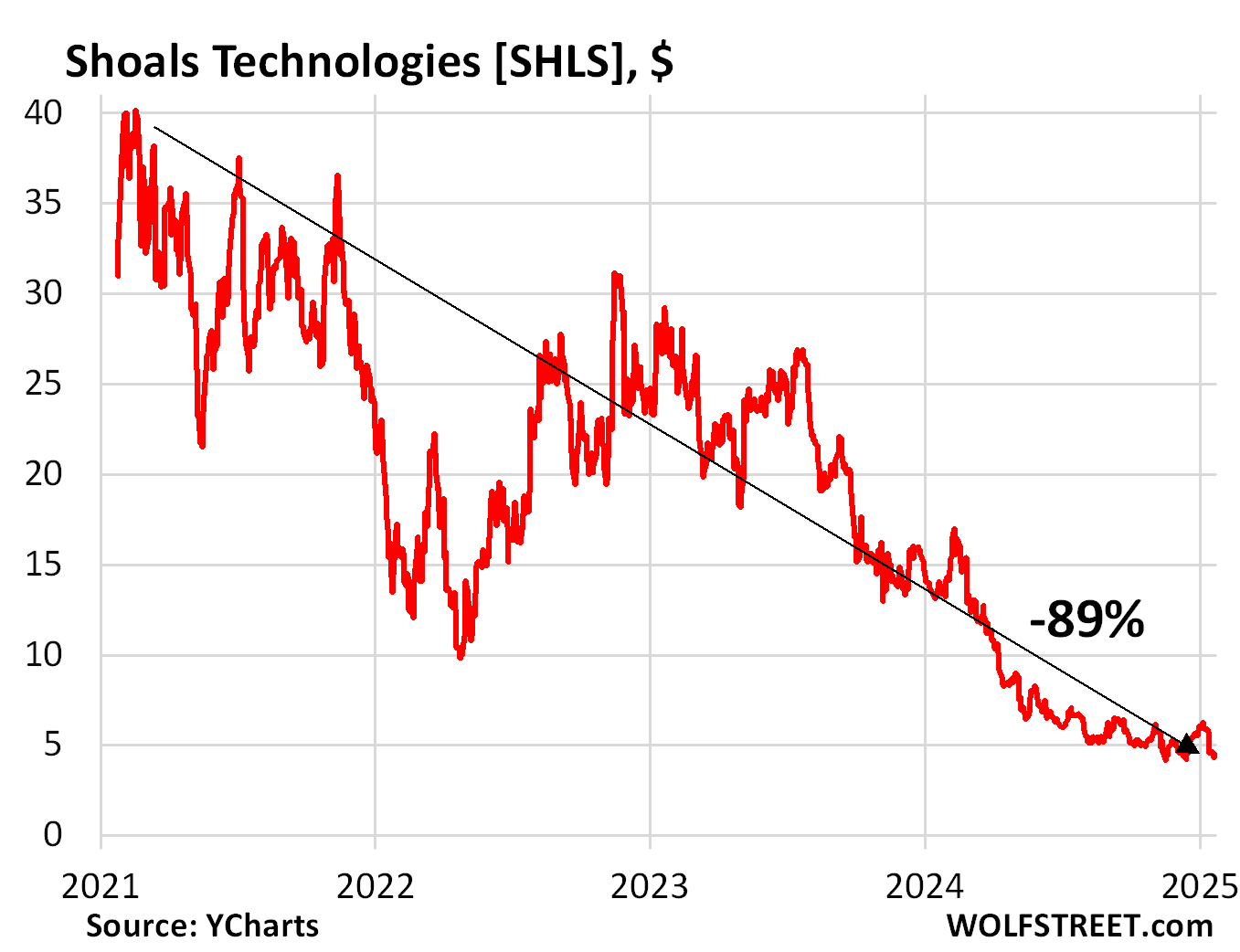

Shoals Technologies [SHLS], which makes assorted equipment for solar systems, including utility-scale systems, went public via IPO in January 2021 at $25 a share. A month later, it was at $40.17, which was also the peak. Since then, shares have plunged 89% to $4.67 today.

The company had been mildly profitable in recent years, but revenues plunged 30% in Q3, and it booked a loss.

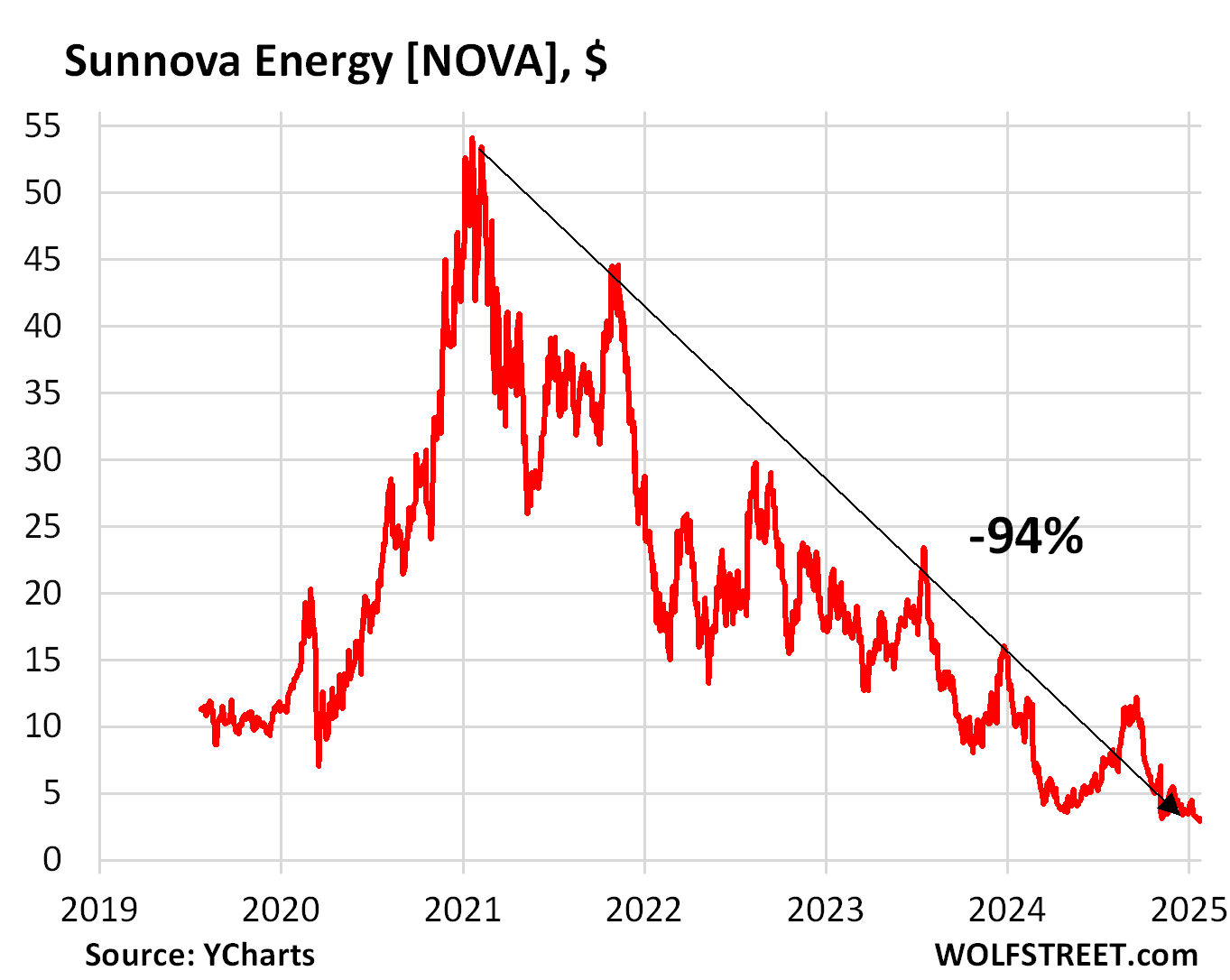

Sunnova [NOVA], which sells solar energy equipment and services, went public in July 2019 at $12 a share, and the stock traded largely around $10 until the covid money came along, when it multiplied by 5 from March 2020 till February 2021.

Just around the peak in February 2021, and still flying high, the Texas-based company acquired SunStreet, a residential solar platform, from homebuilder Lennar, and as part of the deal became the exclusive residential solar and storage provider for Lennar’s new developments.

Since that peak in February 2021, the stock has collapsed by 94% to $3.13. The company has consistently lost large amounts of money, including $418 million in 2023 and $225 million in the first three quarters of 2024. Lennar probably knew why it dumped SunStreet.

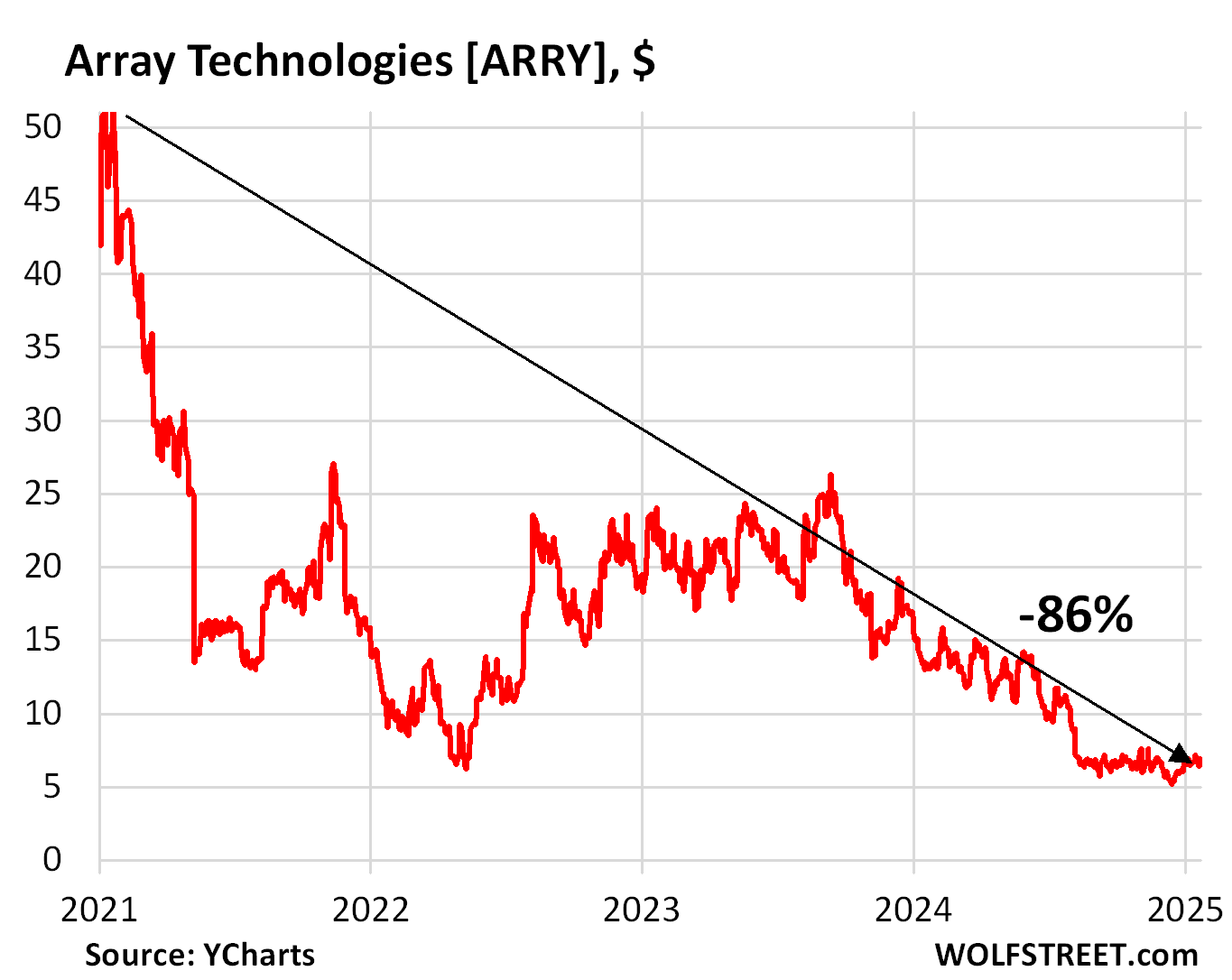

Array Technologies [ARRY], which manufactures ground-mounting systems for solar installations, went public via IPO in October 2020, at $22 a share. The stock popped out the gate and quickly rose to over $40 a share, peaking at $51.01 in January 2021, four months after the IPO.

The IPO was notable for two reasons: One, it raised over $1 billion amid huge demand for the shares; and two, it was the beginning of the exit for PE firm Oaktree Capital, which had backed Array.

The company had some mildly profitable years. Sales grew through 2022 but began to decline in 2023. In recent quarters, sales plunged, including by 34% in Q3 2024, generating a large loss.

The stock has now plunged by 86% from the January 2021 high, to $6.97.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Solar can make sense. But a lot of installations would not have happened without government subsidies (not arguing if these subsidies are good or bad, just stating a fact).

I can tell from my install here in MA: tax rebates + state subsidy paid for 30% of installation cost, which came out to $8k in subsidies. Another big subsidy is net-metering because it acts as if building/maintaining/load balancing the network is absolutely free. In comparison in Germany where cost of inbound electricity is ~40ct/kWh, you typically only get 8ct for outbound solar (even those 8ct are still subsidized, it just got a lot less over the years). About half of my yearly 6MWh production gets buffered through the network, so taking the above 20% as an approximation of ‘worth of outbound excess solar energy’, that’s an 80% subsidy of 3MWh worth of electricity or another ~$800 subsidy per year. Cost of government subsidies over the amortization time of the system (10y) is thus $16k on a system that cost $24k.

So apart from the hype cycle having naturally ebbed, if the government decides to cut down on subsidies and increases installation costs through tariffs, a lot less new installations will make sense. Most likely cost/benefit will only look good in high sunshine / high electricity cost areas.

Re net metering: just remember for inbound electricity you pay for generation and transmission, whereas for outbound electricity you’re only credited for generation.

That must be how we ‘pay’ for load balancing.

Here in MA, we get full per kWh cost (incl transmission charges) credited for energy going into the system though. So these costs are paid by net positive electricity users, not by solar system owners who keep a net-zero balance over the year. The only charge that is not included in the compensation for outgoing energy is a flat monthly customer charge of 7$.

In any case, those transmission charges are only part of the true cost. The further north you get, the less will demand peaks correlate with solar production. Right now my system produces nothing (because the panels are covered by snow) while the heat pump is working near full capacity. The cost of providing backup gas power plants for such situations is quite high, but not included in the transmission charges. It will just increase overall generation price level. Not that it really matters in which item exactly it appears on the bills, it’s a transfer payment, paid for by other electricity consumers as mandated by state law. The Germany example provides better insight into the true worth of excess solar in an area where you have anti-correlated solar production and demand peaks, and the government decided to mostly remove transfer subsidies.

The situation will be different in a place like Arizona where solar production and demand peaks (AC) correlate well and thus solar actually reduces the need for backup power plants.

Interesting. In NH we’re only credited for generation, so my system is designed to produce 20% more than my consumption annually.

I heat with natgas and wood pellets, so my peak use correlatates fairly well with peak generation. Well almost: peak generation is April and May, and peak AC season is August. But during the winter my avg daily consumption is <half what it is during the summer.

I am concerned that too much solar would depreciate the value of outbound solar as you say. Fortunately it looks like there's still plenty more daytime demand than supply here in New England*.

I can't really see a scenario where we don't need baseload generation. Solar is great, but in addition to nighttime, you have cloudy days, days where snow covers your panels (I'm the nut who goes up on my roof and shovels them out), etc. I can see less baseload generation needed in AZ, but not no baseload.

*ISO-NE has graphs comparing actual demand vs demand including estimated behind-the-meter usage, visually demonstrating the daytime demand 'sag' caused by solar generation and net metering.

Demand and supply peaks may coincide better in AZ, but there are a lot of small gas “on demand” power generation stations in that state.

Add a battery, and correlation of demand and generation becomes less sigificant

That’s because you’te not providing the transmission

True but solar subsidies are hardly the only place where massive government energy subsidies exist. And as you mentioned nothing wrong with subsidies and other policies in general except if they interfere in the development of other areas that could compete if given some runway.

People in the USA are being ripped off on the price of residential solar systems.

Here in Victoria Australia you can get a new 6 kWh residential solar panel system fully installed from around A$6500. With state subsidies you can knock off between A$1500 to A,$2000 if you qualify.

That is about US$4300 for the system.

However, as a result of so many systems being installed here from 1 July this year the proposed feed in tariff is going to be 0.04 cents per kWh.

Yes, you read that right. So for 25 kWh of excess generated electricity you will get a whole penny.

This is going to decimate the industry here.

And people without battery storage are thinking about just turning off the feed in ability of their systems rather than basically get nothing for their excess electricity generation.

This can be done with the newer type inverters, but probably not with older ones.

Actually, it kinda is.

Solar is still more lifecycle expensive, power density/efficiency is abysmal (think lots of land needed) and still requires massive government support to remain as option.

It has it niches and, in many of them, is the clear winner. Niches don’t make much of a market.

“This is not about solar power.”

Right, if it’s not about solar then which solar company stocks are doing well?

RTGDFA. Your anti-solar BS is clogging up your mind and blinding your eyes. These stocks were priced about right at $8 share or at $5 a share or at $10 a share or maybe over priced at $20, years ago, no problem, and most of them made a little money, and revenues grew, and fine. But then shares multiplied by 10 or 40 or whatever in just a couple of years, without much changing, other than the stock market mania, and that is the problem, and now those shares collapsed, and this mania and its collapse is the topic of this article.

Respect. And I concur.

Thanks for another good article Wolf.

Yeah, this anti-whatever hijacking is pretty weak sauce.

Banana,

Feel free to start a “drill baby drill” blog. I was essentially told exactly how to do that and had to confess to being too damned lazy.

Makes me a “bathroom wall level” thinker/writer just like like you.

Enphase is a real company that does real stuff. I’m using their app right now to look at my consumption.

Their stock being overvalued is what the article is about. But the app still works even if their stock is down 81%.

Consumption or production? I have the latter on my app, and would love the former.

Mine does both. I can see gross generation, gross comsumption, net in/out, and other secondary data (grid use %, etc.).

Lazard puts out a respected annual report on the levelized cost of energy by source. Their last report – summer of 2024 – puts the cost of utility scale solar at between $29 and $92 per MWh, depending on the details of the project. This is non-subsidized. With subsidies, the report puts the low end at $19 per MWh.

By comparison, nuclear is between $142 and $222, onshore wind between $27 and $73, coal $69 to $168, gas combined cycle $45 to $108.

If you want to talk about intermittency, land usage, or a number of other disadvantages as reasons not to build solar, those might be valid arguments. But the statement “solar is still more lifecycle expensive” is not true. Nor does it require government support.

Add battery storage to the equation, and those numbers for solar would surely look a lot different.

Bird,thanx for this post,I missed it and this gave me a answer and a way to look into more in the questioning part of me post further down.

Like all things tech it will get cheaper over time.

In my bar days I decided Pong was stupid and went back to shooting pool….but neither is the reason I went to bars, anyway.

Usually due to economies of scale.

Godd luck with dat!

The insanity of these previous valuation is mind boggling.

With “the tech companies” there is at least room to spin a pile of BS about exponential growth market capture etc… I don’t know how these companies managed to spin their share price to the moon in the boring market of electricity supply.

Here in Australia solar has been around for a very long time. I’ve never crunched the numbers myself but it has long made economic sense even without subsides. (evidence by corporate & industrial take-up) With subsidies can be a no-brainer.

However in some places here the market is reaching saturation. Nobody wants to buy power at noon in summer. However at night or in winter then there is demand that needs to be met.

No surprise that income from solar is dropping off a cliff during the middle of the day. And somebody still needs to fill the gap when the sun isn’t shining.

Bubbles, manias, and crashes are simply a part of investing life. If you want to get rich–quick, you’ll probably go broke–fast!

The dunces will always find something to latch on that doesn’t sound absolutely bonkers, to them.

Those are some pretty spectacular charts. It does seem like increasing interest rates from basically 0% in ~2022 is steadily letting the air out of at least some of all these overinflated tires we have around here. I guess we should just be patient for all the different pots of malignant money to finish draining out.

One of my old friends worked at a fairly dysfunctional solar company (I already forgot which it was). The charts here and his anecdotes more or less match up. Fortunately, somewhere in 2023 or 2024 my friend moved on to a better company, and seems to be doing better. Maybe he bought puts?

I think I’m trying to say that the stock prices tell incredible stories on their own, but there’s also the personal cost to the little droplets of human glue holding these incredible messes together. Not much thought given to the glue after the building catches fire, I suppose.

I’m still looking forward to one day having our own solar & battery setup. But for our use case, we’d like the technologies to mature some more, and for our bank account to mature more too. Until then, the generator will be there for us next time old man winter breaks a power line or a careless driver shears a utility pole in half in the middle of the night (I still can’t believe it either)

Looks a lot like a long pump and dump. There was/is no rational reason for those valuations. Most of those stocks had collapsed before California NEM3, so that can’t be it.

Line clearance, with 200 ft. trees, is a delusion during high wind events.

“Malignant money”……now THAT is a term deserving of several FULL economic papers, maybe a book….

..even a department in banks and a career specialization.

Borrowing terms/concepts from the “harder” sciences is very common in the social sciences, in their quest for a status above novels and such.

And a damned good overall comment, too.

Let’s put solar in perspective in terms of the energy mix:

https://wolfstreet.com/2024/02/27/u-s-electricity-generation-by-source-in-2023-natural-gas-coal-nuclear-wind-hydro-solar-geothermal-biomass-petroleum/

Did retail investors eat most of the losses or did some institutional investors get taken out behind the shed too? Curious if it was big names losing bigs bucks or just lots of little guys?

Are there any examples of solar companies that have gone through a 5-10x multiple expansion like this and held on to it? I’d say SEDG platuea’d for a couple years before the plunge, but I am curious if there is a more successful example?

First Solar and Nextracker are on my watchlist, but I likely won’t nibble until/if their stock prices fall another 80% and 50%, respectively.

Wolf, if you do another industry specific, stock market craziness article, please consider the beer/booze/wine industry. I would like to see your thoughts on the selloff there. Like solar, seems to still have a long way to go since the price/sales ratio got so high.

Thx,

Shocka

The plunge in wine consumption, after the boom during the pandemic, is quite something. A big issue here in California Wine Country. The industry is reeling. No one knows what to do with all this wine. Beer consumption has been dropping for years, so the industry is used to it. What may be new is the drop of craft beers. I have to collect some data on this stuff.

Seems like the craft beer industry got oversaturated with breweries while the number of enthusiasts inevitably plateaued. But there may be more to it than that.

The big lovers of hoppy craft brews are getting old, and they’re cutting back on alcohol consumption, which is good obviously. And many young people either don’t like beer at all, and if they drink, they might go for fashion drinks, seltzers, etc. Many young people go for pot instead of alcohol (I saw some reporting on that, but don’t remember the details).

The world doesn’t need 10,000 IPAs. The breweries all seem like carbon copies of the same beers. Only a few here seem to have differentiated themselves with beer lineup or locations.

Plenty of competition from new ‘trendy’ drinks e.g. spiked seltzer.

” No one knows what to do with all this wine.”

That’s a no brainer, just make it into brandy or other distilled spirit(s) and put it down to age for a couple decades…

Just take a look at the whisky and other distilled spirits to see this.

Some of the best are actually keeping up with inflation!!

Sales of whisky and bourbon have plunged too. So they can just keep all this stuff in barrels for another generation or two and see if there will be a market for it then. I think I just put my finger on a new business model.

On 13 January 2025, from ‘Red River Farm Network’, Grand Forks:

“Hoping for a Beer Market Rebound”

“One of the biggest negative impacts on the barley industry in recent years has been the decline in beer sales. Steven Edwardson, executive administrator, North Dakota Barley Council, said that has been concerning. “Less demand for malt and less demand for barley to make the malt,” said Edwardson. “Hopefully, that is a consumer demographic that will change at some point.” Growing competition from cannabis and ready-to-drink cocktails has contributed to the slump.”

Very interesting. I have read that the younger generations are avoiding alcohol and using MJ or nothing at all.

California reds are great. If prices drop yoy I can’t say I’ll complain but I understand that’s catastrophic for the producers if it goes on too long.

That is why makers and distributors of spirits have been the most vocal backers (and deep pocketed) against legalization efforts. They knew MJ would start to replace alcohol for people wanting to take the edge off of an increasingly chaotic world.

Edibles and drinks are the real stars of that shift; clear dosing, no smell, and no lung irritation.

It is sad that many young (under 30) people are getting together less and less to hang out and have a few beers or glasses of wine. I recently saw a chart that showed “time spend with friends” dropping almost every year since the 80’s while “people reporting feeling lonley” was increasing almost every year since the 80’s.

I think it started with series Friends and Big Bang. They were always hanging around but not drinking. In the 70s and 80s, we were ALWAYS hanging around and ALWAYS drinking. Best times!

Do we drink for taste or effect? Do we smoke for taste or effect?

The shelter renter is very concerned and sad about our lost ability to talk to each other and discuss subjects like, “Is your rent high, too?”.

I remain confused, as usual.

“No one knows what to do with all this wine.”

You set that up for some easy jokes, and no one took the bait! Send it to me!

Strange that prices don’t seem to have fallen. At least on the nicer stuff like Napa cabs, Sonoma pinot, chards, better French and Italians, etc.

I’d be curious about pistachios, myself. From what I can tell they are an absurdly profitable cash crop with infinite demand but suck the aquifers dry as dust.

A recent Freakonomics episode delved into how cannabis consumption might be displacing alcohol. It said cannabis had reached a crossover point where number of daily and near-daily users of cannabis has exceeded the number of daily and near-daily alcohol consumers. There was also some discussion of possible benefits if all alcohol use could magically be replaced with cannabis. There are still some cannabis unknowns. Some products on the market have insanely high levels of TCH, and we have no data on what the long term effects of those products might be. Also the cannabis business environment is still totally messed up by the dual-legality status.

Cannabis is not a panacea, it’s not as toxic to the body as alcohol but there are very real mental and physical consequences of long term use, especially in the young demographic.

Freakonomics Podcast had a series on Cannabis industry. The claim they support is that legal Cannabis industry is fraught with problems on all sides (well that’s pretty clear), but that the industry’s other products like Cannabis-infused beverages are becoming significant competitors to Alcohol. This l likely combined with societal behavior changes due related to either generational differences or post-pandemic norms. The Podcast also points to M&A interest from Alcohol to Cannabis.

It’s fascinating though you typically observe a more by-the-numbers financial look vs fundamentals. Still interested in your viewpoint.

Shocka Locka,

Had some neighbors who owned a winery in central valley and they put a lot of energy into China. Tariffs however on those made other foreign brands more competitive and less expensive. Obviously down turn hurt because people would go out and buy glasses of wine instead of a bottle and they would say the first two glasses pay for the wine, the rest is profit.

I second this idea, and would add a request to include pot stocks as well.

I still have an article filed away from the Globe and Mail, from Jan 2019, just as a time-capsule of Canadian stupidity.

The headline was: “This Alberta couple has all their kids’ education money in cannabis stocks. What could possibly go wrong?”

And the subhead read: “Planner says couple’s portfolio is bold, but risky, especially when you factor in three rental properties with negative cash flow”

It doesn’t (didn’t?) get more Canadian than that…

I know the Vancouver and Toronto real estate markets have blown up, is that not the case for areas like Edmonton or Calgary? Am I right about the Province? Ok…I’m right. Had to look it up.

They could be super nice landlords who haven’t increased their rents since 2005, which could definitely be the case. But if they’ve kept up with market rates they should be doing better, right? Because I don’t think the pot stock strategy is a winner.

Excellent article Wolf. What it truly illustrates to me is the downfall of the Biden administration. Most of the action begins in 2021 and ends in 2024. Now I’m not a fan of either solar or President Biden so make of it as you want.

Politics are forbidden I know. But I was offered the option of installing the panels on my roof, along with all the subsidies. Which I could not find to be advantageous.

“Most of the action begins in 2021 and ends in 2024.”

No, most of the “action” begins in early 2020 through early 2021 with the ridiculous spike, and that was during Trump 1, and some of the spikes were turning south already by the time of Biden’s inauguration.

Trump got the spike, Biden got the plunge. The problem was the ridiculous spike during Trump. The plunge during Biden was the unavoidable consequence of the spike.

I have no idea how you can bring Biden into these stock price charts, especially in the wrong place.

and then investors all seemed to “rotate” into the mag7. their valuations are truly stupid.

Now that we’ve got the asset-pumper to end all asset-pumpers back in office, you ain’t seen nothin’ yet. Brace for unrelenting inflation.

Already demanding ZIRP.

But is going to solve inflation.

just like liz warren was demanding reduced rates to supposedly help low income borrowers, which reductions did no such thing.

all of these people work for the rich, while playing lip service to the middle class.

If there is pressure to go with zirp or QE or whatever, would longer dated yields comply or would they go up like they have recently as the fed has lowered rates? Now that there’s inflation, would zirp have the same effect on long yields as in the past? truly curious what people think.

rm, i think long term yields could blow out if rates are lowered back to 0 or close to it.

Not to get too off topic, but agree with Franz G. The bond market has final veto power.

I’d like to think the incoming Treasury secretary understands this at least. Then again, it seems like he wants to normalize the tennor of new issuance (fewer bills and more coupons), which would put upward pressure on long rates…

No easy answers.

Do you drive at full throttle and low speeds on your “softtail”? Turn left a bit and just lean, when you turn right…..or just wobble?

I’m not a fan of Harley riders.

We are all not fans of something from time to time.

Means next to nothing.

I thought he was talking about a mountain bike, showing my obvious Colorado bias…

Could be. I don’t know much at all about pedal bikes (since 6-7th grade) except when a friend tried to get me into them the seat hurt my butt and I was totally terrified around cars. Sold it. I’ll walk.

Trump likes nuclear, so permitting might get easier. We could see a nice run there.

He does but is mulling which type. May have it down to short list of:

Advanced gas-cooled reactor (AGR) …

Light water graphite-moderated reactor (LWGR) …

Fast neutron reactor (FNR) …

Apparently Candu out.

Did anyone know they made a mile or so long special, clear tunnel from ground zero on a Pacific Thermo Bomb test just to see if there really were “fast neutrons” that would get out before everything vaporized and otherwise got weird and knocked every which way in the explosion?

I forgot if there were any results, but I kinda think the consensus is there is a range of neutron speeds….not really sure about that.

I still want to know what an electron REALLY is, even though I was once pretty good and making them do different useful stuff. From amps to LASERS to OCRs.

Given the time-frame it seems pretty clear that these solar pump and dumps were induced by JPow’s nonsense pandemic money printing bacchanalia, nothing more nothing less.

It’s amazing how many other mini bubbles have already come and gone within the overarching mega everything bubble: crypto, metaverse, SPACs (which I had forgotten about), marijuana, now crypto again. Reminds me of Jeremy Grantham’s thoughts on the dot com bubble: how the junk went first and people held on to the larger companies as the “safe bets,” but then even all of those tumbled like 80%-90% over the next few years. Seems like we’re at that stage with the mag7 now.

Canopy Growth Corp (CGC) went from at least $527 in 2019 to $2.20 yesterday.

$1000 invested down to $4.17

Wolf, I believe you just called the bottom for solar. Congratulations, sir – excellent timing. 👌

Gabe

I think that call belongs to you.

Value may be found in the corollary to this post, being the forward tariff level on the import of solar panels from China and the scale of the possible opportunity in the US for a few of the entities listed above and new entrants.

Maybe another spike catalyst rather than the bottom.

I would agree, the energy plan coming out ot the new administration dismisses solar and wind as NOT energy sources. Most of that is paybacks to big oil and gas, solar and wind still have their place. Oil and gas will have their crisis at some point proving that putting all your eggs in one basket is never a good idea.

If all you have is a hammer, everything looks like nail. There’s a best energy source for everything. Natural gas is hard to deploy in mountain terrain, underground electric is expensive, above ground electric has its own set of problems, hydro requires large amounts of water, etc. Nothing is perfect, it comes down to what best meets the need given the location, available resources, and infrastructure.

Sandy – very well-said. An apparent widespread binary view of a complex-and-finite systems reality serving the massive world-resources appetite furnace never fails to amaze me. Whether this view is disingenuous or not, it should be apparent that ANY available energy source will be tapped going forward, divil take the hindmost while crying for new tech free lunch…

may we all find a better day.

Hi dustoff,

Agree..with ya both…I don’t think many appreciate tech (and a ball in space) have limits. It’s like Reagan with Starwars or Trump with Stargate. Have the vision for it and then set the scientists/techs to scurrying about, and presto, your vision is a reality.

I read the Pomo Indians around here counted in base 8. They counted the spaces between their fingers because they knew numbers were not real? Kinda cool, huh?

…hey, NBay – …seems, that in Pomo eyes, Octal may have been the true ‘final frontier’…

Hope the body problems are easier. Best.

may we all find a better day.

PG&E introduced net metering 3.0 in the largest solar market in the country. Of course all the solar stocks were crushed. The only way residential solar is viable now is with batteries. Commercial solar only gets 6 cents per kWh wholesale. The only one that can survive is Tesla because no one can compete with their economies of scale for batteries and the only reason they are doing much business is because the cost of electricity in CA from the big utilities is essentially double or more from everywhere else in the USA. Why would anyone want to invest in that?

Tesla mainly doesn’t make it’s own batteries. They’re supplied by the likes of panasonic and catl.

NEM3 was approved in Dec 2022, well after the stocks shown had started to crash.

The reason for NEM3 is that the California produces so much solar that in the afternoons we are having to pay other states to take our excess generation. Storage at that level just isn’t soup yet to get us through the peak. Peak consumption has shifted from morning and afternoon to 4pm – 9pm, reflecting the period when solar panels largely stop producing but people still need lighting, cooking, and air conditioning.

If you look up California Duck Curve, you’ll see what I mean. Some salt in the wound for utilities is that the grid infrastructure was designed to be a one-way street, a lot of work has to be done to make it a two-way.

Solar for homes that have the right sun exposure and roof layout is still a good idea, it just takes longer to pay back with NEM3 and you need storage to smooth the transition to peak load. To bring it back to the GDFA, the idea that somehow solar stocks were going to be massively valuable out of nowhere is the power of magical thinking, possibly just a place to park Covid money until enough bag holders had bought in.

Read China has at least 2 2K mi DC super “freeways” in their grid. We probably cover more E-W than they do, especially counting PR, AK. and HI.

Good place to unpark ANY money, especially from AI and pills which seem to be in fashion with Mr Market now, along with quantum comp, various fission monsters, and fusion, etc,etc.

Another great article, Wolf.

How is Wind looking since the off shore politics have begun?

These stocks could disappear all together with Trumps renewable energy policies and high tariffs on China panels.

They were already dead with California going to NEM 3.0.

What is amazing to me is how Gavin Newsom and Elon Musk feud publicly yet California energy and climate policy seems to significantly increase Tesla’s business. It’s almost like we’re all being played.

Trump just now said — under pressure from his billionaire buddies around him — that he doesn’t want to put additional tariffs on China-made products.

This last big drop in solar stocks has everything to do with the rise in interest rates. Many, if not most of the rooftop systems were financed as second mortgages on properties. The economics were compelling.

Secondly, small solar (rooftop and on the ground) will continue; however, the early incentives by utilities for generous buybacks continues to fade away. The reality is that US utilities can only “use” so much of this power source due to it’s unpredictability and intermittency. And of course they too have invested in solar in the form of large farms.

People with money and land will install solar as a from of “off grid” power but that will require batteries which are expensive. So the early and attractive cheap systems with net-metering will clearly fade and only grow at the rate of overall grid growth.

We drove down the 5 recently on the way back from Sacramento and saw a number of massive solar farms along the way. Which makes sense from a land use perspective, there’s a limit to how much of the Central Valley we can irrigate with existing water supplies and saline deposits build up over time and can make it unfarmable. Large patches of fallow land can be repurposed for solar while the soil recovers, giving it a role in permaculture (plus it helps power the irrigation pumps).

All I know is that when I finally get around to buying an electric car for puttering around, I have enough wall space on my shop to solar panel it and charge the car off of that.

Gotta run some numbers but sounds like w super low maintenance costs on the cars it might come out pretty good on the $/mile front. When they get the solid state batteries going it’ll take care of the range anxiety issues.

Might even go for a used electric the first go-round as it sounds like the batteries are holding up pretty well in a lot of cases. Gonna have to stick w diesel for the work gear for awhile tho.

The math on EVs as a commuter car is great when factoring the maintenance and the updated information of battery life…used, especially with subsidies. You do probably pay a bit more on insurance.

But these guys depreciate hard. Very 1st-2nd gen tech. Plus, the Chinese and Koreans seem like the only ones who are making them cheap where depreciation is just less of a hit.

I love my lil’ used, subsidized and rebated Bolt I got for 50% off. I wouldn’t touch a EV truck, SUV, or sportsy sedan with a 10 foot pole.

My cunning plan is to drive it till it pukes and just carry required minimal insurance on it. ;-) Not a serious purchase until they can drive themselves reliably. I’m guessing that’ll take until about the time I’m actually in need of a chauffeur by the looks of it so far…

Another angle to this:

When I got my solar system, I didn’t do a lease a la Sunrun, I went thru a local company and bought the system outright. I was able to qualify for a subsidized ‘energy improvement’ loan with a rate of 4.25% at the end of 2022 (and it would have been 3.75% if I had rate-locked earlier).

Surely these energy improvement loans have much higer interest rates now, thus reducing affordability even for folks doing installs with small local companies. Another ZIRP distortion that needs to be worked off.

Wolf, you might save this article as a template for an article about AI stocks sometime in the future.

First will be the “Collapse of the Quantum Computing Stocks” … many of them SPACs.

AI is kind of funny. It’s everywhere, and the Mag 7 are all dressing themselves now as AI companies. So when the AI bubble begins to leak hot air in terms of stocks, the whole market deflates, from Nvidia down to utilities.

Everything in software is now addressing itself as AI. It is absurd. Even some of the most AI-ish are not even AI, just increased automation.

i mean at its core, isn’t all software, and all computing dating back to the 60s, a form of “artificial intelligence?”

think about a basic 4 function calculator. they don’t have every combination of equations stored. it’s just they’re programmed to do the calculations.

maybe i’m just an old man, but i don’t see generative ai as anything groundbreaking. it’s just the next step on the same computing trajectory that has happened for 50 years now.

I’m expecting big things from “off-shell W Boson” computing,

I think R Feynman’s diagram of how it works clearly shows some massive, fast, and inexpensive on/off data storage possibilities.

Of course fusion power is just around the corner, so maybe there is no point in worrying about cost. These concepts may be just what a “Malignant Money” specialist my be required to resolve.

Thanks again to whoever mentioned that term here…..

And the two are connected. An AI query costs 10X electricity that a google search requires. Will be interested where AI settles. Our project doesn’t want to use AI out of fear of AI but it is funny as the product has a chatbot which they label AI but such is the hype. Waiting for AI toothpaste any day now.

Every software company that I deal with as a business, and whose services I pay for, is trying to shove their useless AI down my throat: Microsoft (via its 365), Google (in my corporate email accounts), Mailchimp (which I use for my email service), WordPress/Jetpack that this site runs on… some are trying to charge for it separately. Microsoft is raising the subscription price because now it comes with AI… Microsoft is going to make me pay for AI though I don’t use it. Google will soon figure this out too. Jetpack and Mailchimp for now charge on a per-use basis. These are services that I cannot easily replace. As far as I can tell, AI raises my costs and makes my work more complicated and less productive because I now have to deal with the constant intrusions from their AI reminders.

Holy cow – was that annoying paperclip that popped up relentlessly in Office ’97 actually the first AI?

The ‘AI’ these companies are referring to is Artificial Inflation.

Just FYI off-topic, I believe there is a way to opt out of the Microsoft AI charge, saw people talking about it online, but didn’t read further as I just pay the one-time charge for Excel and Word and don’t pay for an MS subscription as I don’t like the way subscriptions cause you to end up spending more money on things than you otherwise might.

It’s not just AI. I wasted all morning today dealing with “improvements” from Intuit (Quickbooks) and my email provider, that only raised costs and made things worse for me.

We have been in a new tech drought for about the last 10 years. Nothing new for companies to sell you. That is why they are pushing AI so hard, they got nuthin’ else to push.

Ol’B – man I miss the old MS office ‘assistants’

Starting in (I think) Office 2000, you could change clippy to a few other characters. One of them was a dog who would do various tricks if you double clicked on him. Quite fun but distracting.

That was kind of AI, but I never really thought about it back then. It was just a context-dependent UI.

I have a 3D design software package that I bot in 2016 and Windows kept updating the display driver to one that wouldnt work with the software (which isn’t updated) so I set the driver to ‘read only’ and now Windows can’t finish any updates which has stopped all the software bloat. I keep the virus software updated and that’s about it. :-) I find convenience features not very convenient most of the time…

Mr. Richter, I feel your pain. I often wonder what kind of world the people who create this constant “forced change” (and quite often, not for the better) live in.

Like one has nothing better to do then spend countless hours trying to figure out how to make the latest technoligical “cram down” do the work of what previously woked just fine.

And, oh, by the way, it’ll be be more expensive.

Your welcome.

Wolf,

Agreed. I’m getting so sick and tired of all this crap that Microsoft keeps shoving down my throat, licensing scams, bundled add ons, overly complicated menues, unwanted features, unwanted upgrades, that I’m thinking of going back to Office 97, and taking some of my antique Windows XP PC’s out of mothballs. I have complete sets of software for these machines and they still run seamlessly. I’ll keep it separate from my on-line work and transfer files via SD cards when needed.

Do any of you have a full solar system? I have one at an off grid camp house.

They start off good and degrade fast. Always something to do like clean the panels.

There is a good future when you get better batteries and storage. It is just to early to be a good investment.

Are the data centers looking at solar or do they know better?

They are working on one just South of me. Plenty of water and natural gas.

The data centers are looking at solar as a backup and supplement. With as much energy as AI consumes, they also siting them carefully. I will not be surprised if nuclear is on the table and undergoes a rapid transformation using AI to plan and manage power, storage, backup, risk management, and waste disposal.

I bought LG panels and enphase controllers over the last 5 years it has paid well over 50% of the cost . I bought it when banks were paying near 0% interest and we actually produced more power last year than the first 3 years. We are grid tied and the system locks in our energy cost for well over 1/2 of our power. We would do it again. The system has been flawless.

I own a PV system. It’s only 18 months old but haven’t noticed any degradation. Yes cleaning can be a pain – I just shoveled nearly a foot of snow off my panels, although I didn’t really have to I suppose.

Data centers won’t care for solar except to augment their baseload power. The future is datacenters located in the Permian and other gas-producing regions so they can run their own combined cycle gas turbines and be off-grid.

Bear – 1990 first solar installation at our off-grid home was 12v/110w/110 battery system to replace the oil-lamp+candle lighting with 12v auto/rv incandescent bulbs and CFL’s, along with a small 12v b&w TV and NiCd battery charger for the flashlights and radios (even prior to its end in ’96, REA subsidies just wouldn’t pencil/answer reliability issues for us in our rural area. Expanded to 400w and tripled battery bank size in the early aughts, due primarily to laptop computing/satmodem power demands. The advent of LED lighting and NiMh batteries extended our small system’s capacities until it became necessary to adopt a new 48v/1200w/sealed AGM expanded battery system to provide for my wife’s late mother’s needs when she came to live with us in the mid-teens, as well as taking that opportunity to switch from propane to AC-electric refrigeration. That said, we’ve retained the old 12v system, replacing the old maintenance T110’s with a FeLion battery for supplemental/backup, now all-LED lighting, the 1990/2004 US-manufactured PV’s still performing at their rated outputs. Replacement equipment for the original system’s 28-year primary service life were three battery-banks, an uprated charge controller, and an electronics-friendly, true sine-wave inverter.

Our situation, though typical in our ‘neighborhood’, is atypical, of course, elsewhere else. I don’t know anyone in an ‘offgrid’ rural situation who isn’t running what would be termed a ‘hybrid’ utility infrastructure, and accepts the operational/maintenance requirements and challenges therein (for example, we are solar/battery electric (48v-110v main/12v-12v aux) with ICE-generator backup; wood space heating; propane cooking, H2O heating, supplemental space heating; H2O source uphill spring. Landline (still Cu, still most reliable for county emergency services) phone service with poor and intermittent local cellular, but active local Ham and GMRS radio participation; satmodem service. Planning solar H2O heating/hydronic space heating project after rainy season). No subsidies offered for our situation since Reads end). As you say, ‘always something to do’, but still find it all worth those tradeoffs to live here. (…apologies for the windy comment).

may we all find a better day.

921B20 – out of curiousity, what fuel do you use for your genny?

Reminds me of an ATV park up in rural Maine that I’ve visited. Completely off-grid with solar/batteries + a diesel genny and propane for cooking & heating.

ShortTLT – at prox 38+’N, we still have decent winter daylight hours, and our newer, larger 48v PV array has the advantage of MPPT over our old 12v one, so our gasoline gen (7kw) use is acceptably light, even in extended periods of storm weather. (Some of our neighbors run propane gens (no messy gas handling/storage) with auto start capability, but all have noted propane’s reduced thermal potential (runtime/gal.) vs. petrol with its stiff price increases over the last couple of years). No one close to us running diesel, but reckon some of the larger properties with bespoke shops must be). Best.

may we all find a better day.

RE valutions, should these stocks be treated like utility companies?

The economics for private solar installations have changed substantially over the last 10 years. I installed a ground-mounted 10 kW array in OR about 15 years ago. Despite marginal average solar influx (3 hours) in the western part of OR, the installation has been profitable (4% tax-free ROI over 15 years) and largely trouble-free.

I recently moved to AZ. You’d think solar is a home run in AZ. Not so. The average solar influx is, of course, much better at 5.5 hours/day. However the utility deals nowadays are much worse. Export rates of only 2c per kWh and minimum/peak fees make computing any ROI difficult. Adding battery storage might help but that would almost double installation costs. I’m still on the fence about adding solar in AZ.

Until storage costs come down significantly, small scale solar may not see attractive growth rates.

That implies that market has already reached its saturation point with solar. $0.02/kWh means the grid is awash in supply during peak generation periods.

Speculative margin accounts should be eliminated. They are just funds dissipated in financial investment, not real investment.

Does anyone else think that Stargate is Trump’s Solyndra?

Funny nobody here is talking about the potential impact on all energy sources of “drill, baby, drill”. I remember when gas was .19 a gallon. It will never get that cheap again of course, but a big increase in oil supply will impact all the new alternative (I call them boutique) energy sources.

I think it’s because we are already drilling quite a bit. If we just keep increasing the supply then the price for oil will drop. If the price of oil drops, then producers in the U.S. will suffer because the cost of getting oil out of the ground in the U.S. is higher than it is in the Middle East.

So that could slow down Trump’s “drill baby drill” enthusiasm. Of course I wouldn’t expect him to understand this but oil producers would.

“So that could slow down Trump’s “drill baby drill” enthusiasm. Of course I wouldn’t expect him to understand this but oil producers would.”

Oil producers absolutely do not understand this. They will consistently drill themselves into bankruptcy if left unchecked.

That said, oil is historically very expensive relative to natural gas right now, so the principles of arbitrage dictate oil will have to come down (and/or natty gas will rise) in price.

The U,S, is the largest crude oil producer in the world. We are the “swing producer” now instead of the Saudis.

Drilling and production costs in the U.S. have come down quite a bit in the last 15 years due to the advent of horizontal drilling and enhanced production techniques. There are roughly 3,500 drilled and not completed wells in the U.S. that can be brought to full production in 30 days. Oil companies are quite good at balancing production to hold prices where everyone wins.

Oil is a worldwide commodity and there are 50+ various grades of crude oil prices daily on the market.

I was in the oil & gas business over 30 years. Biden drilled more wells in his 4 years than Trump did in his previous 4 years. Look it up.

Trump and the oil companies are no longer shackled by the environmental nutcases and their absurd policies as of Jan 20, 2025. Drill, baby, drill. My money is on oil and natural gas, not wind, solar, lithium, coal, or nuclear.

Thurd2

Drill baby drill has been the rule in US for many years, has made the US the largest oil and gas producer in the world, has made the US the largest LNG exporter in the world, has made the US a net exporter of petroleum and petroleum products, and has caused prices of oil and gas to collapse multiple times and for long periods to where hundreds of these oil and gas drillers when bankrupt during each wave. I have called the episode that occurred in 2014-2016 the Great American Oil Bust. Lots of stories on this site about oil and gas drillers going bankrupt, with lists, etc. And then just after the industry and oil prices seemed to recover, there comes the second wave in 2020. Now the industry wants to exercise discipline, rather than over-produce, to keep the price where it is so they can make money and stay in business. The LAST thing they want is for the oil price to drop. Trump is going to have a hard time persuading them that a lower oil price is somehow good for them.

That’s because we don’t use Oil for electricity in the US. Less than 1% of our electricity generation comes from petroleum. The price of oil has nothing to do with how competitive solar and wind are in the electricity markets.

The big oil companies are already ignoring Trump anyways. Good luck with that big increase in oil supply: https://oilprice.com/Energy/Crude-Oil/Shale-40s-Capital-Discipline-Outweighs-Trump-20s-Pro-Growth-Rhetoric.html

This is a misleading comment because a significant chunk of our electrical generation comes from natural gas.

Natural gas is not literally oil nut is effectively oil. All hydrocarbons are fungible and any price difference that’s big enough will eventually be arbitraged away.

I think on Wolf’s recent snowcation (snow vacation) they used a solar powered snow machine (maker) to make snow. Oh, and those high winds – those were also produced with a solar powered tornado machine. Oh, the joys of solar power.

Hey Wolf. You might wanna check out the Deepthink furore. Big Tech just lost the moat that rationalizes their valuations.

I just wrote and deleted the same comment before I read yours. It it real or cold fusion? BTW is AI real or cold fusion? Makes a difference. I don’t expect many can independently evaluate. Like, how many can write a quantum computer program?

But I look forward to more realistic AI p**n.

I wonder how the costs add up in the of all the different sources of power generation including any damage to ecology ec.t(they all seem to cause some issues0.

When(if) I ever get me land and home will consider it but not to sell back but just for battery storage for emergencies,i.e. a water pump/few lights/fridge/small heater ect.Will first have wood stove and deep well hand pump.

As tech moves forward will be interesting to see changes/new products come online.

I used to work in solar. Solar has so many moving pieces, its hard to generalize at times.

If you pay up front money for a set return (in theory true with PURPA agreements), you are buying something much like a bond.

Bonds price inversely with interest rates, so solar output should as well.

So it isn’t stunning that an industry that had a lot of hot money starts having issues when the water goes out. The Chinese themselves pushed solar capacity way to fast for their needs. Since that goes back to at least 2012, they may have actually worked themselves into their capacity.