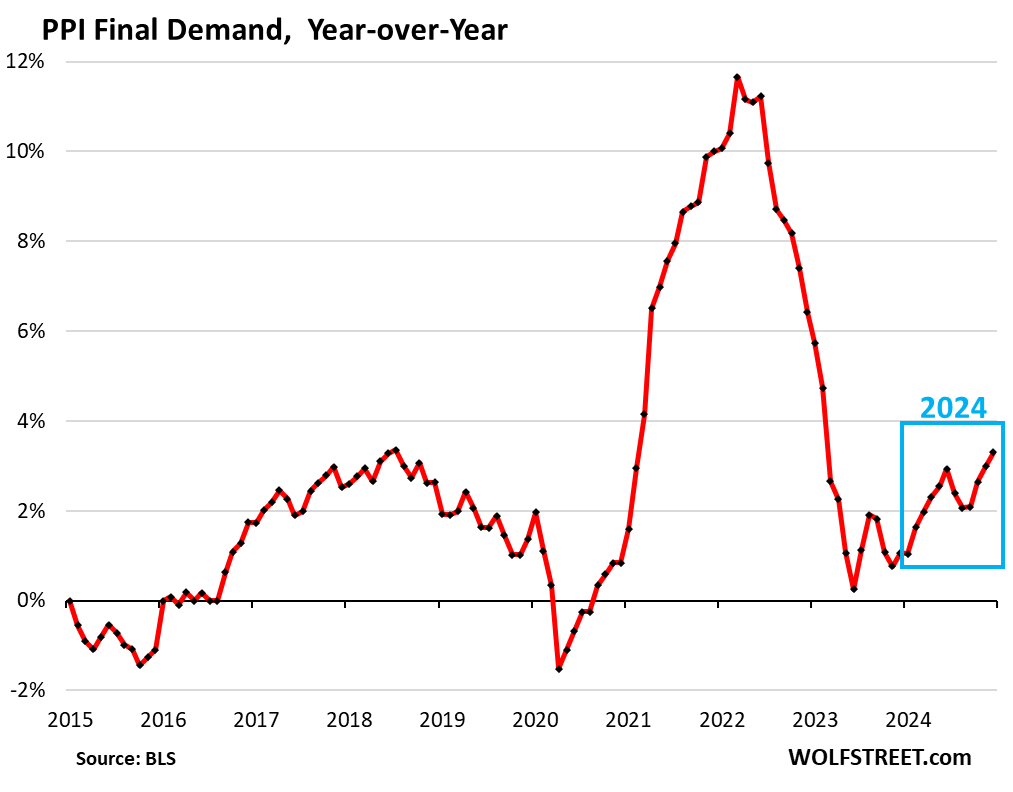

2024, the year of sharp acceleration. Services, accounting for two-thirds of PPI, are where inflation is festering and accelerating.

By Wolf Richter for WOLF STREET.

This time, the prior months’ data of the Producer Price Index were revised up by relatively small amounts, unlike the whopper up-revisions over the past four months. So November’s overall PPI reading was revised up to a year-over-year increase of 3.00%, from 2.98% reported a month ago. So that lack of big up-revisions was refreshing.

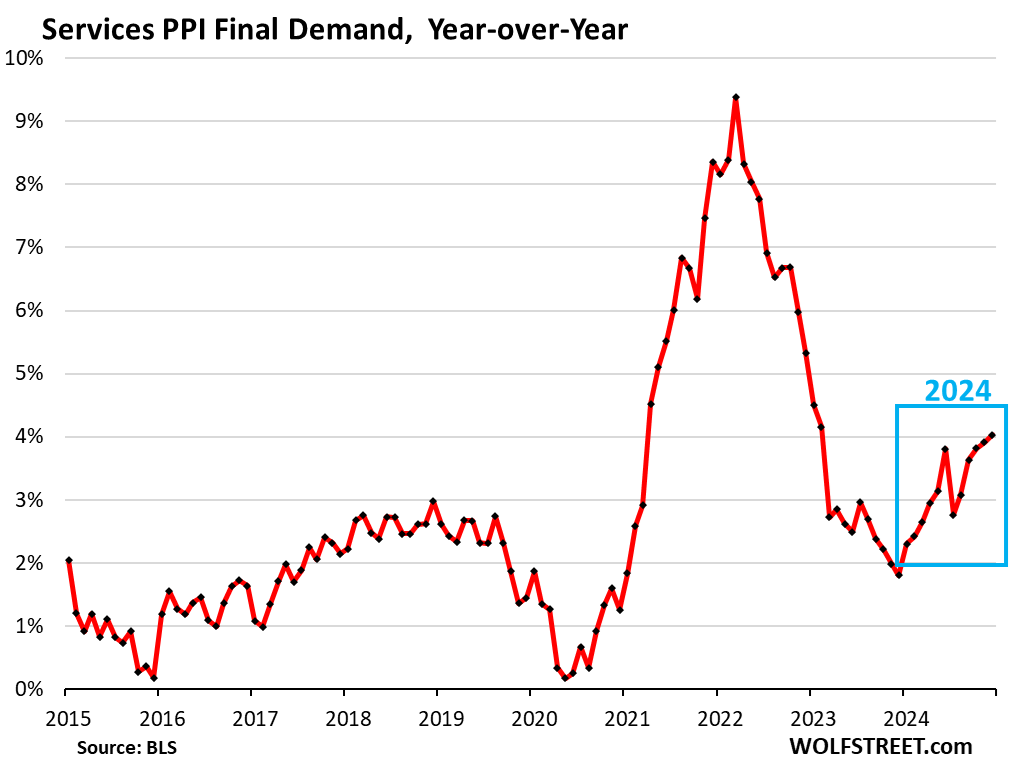

But then the December PPI, as reported today by the Bureau of Labor Statistics, accelerated to an increase of 3.31%, driven largely by services, which account for two-thirds of the overall PPI, and which accelerated to 4.03%. Both increases were the worst since February 2023.

The year of sharp acceleration: Overall PPI accelerated from 1.06% in December 2023 to 3.31% in December 2024, driven by services, which accelerated from 1.80% in December 2023 to 4.03% in December 2024.

The PPI tracks inflation in goods and services that companies buy and whose cost increases they ultimately try to pass on to their customers.

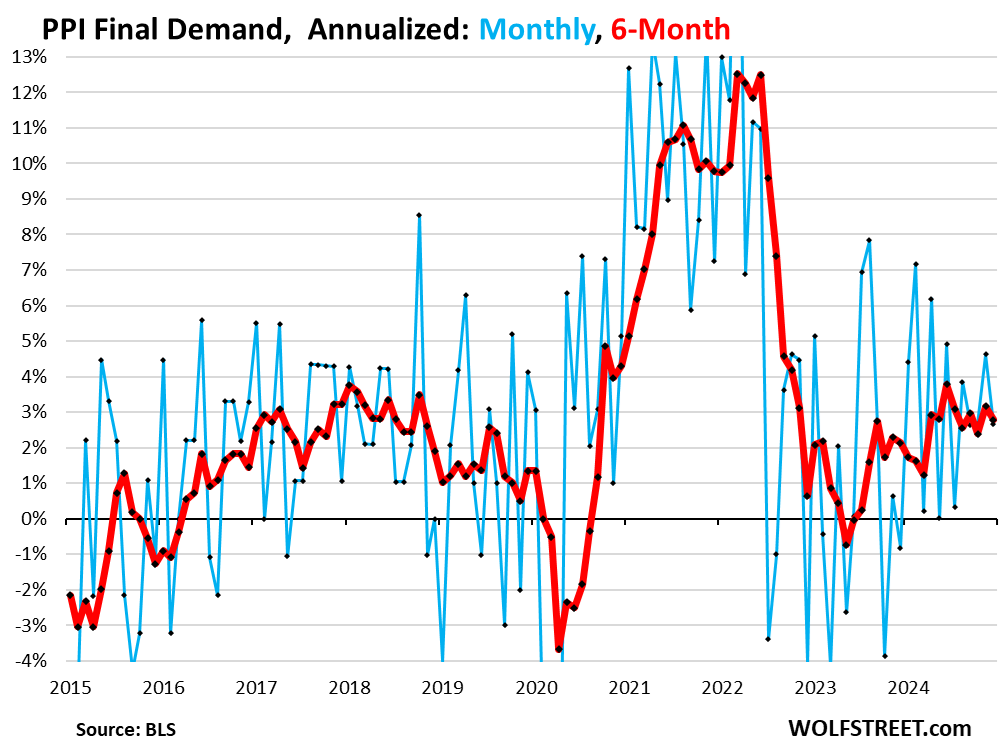

On a month-to-month basis, the PPI for final demand rose by 0.22% (2.7% annualized) in December from November. The six-month average has been around the 3% line for the past six months.

The plunge in energy prices from mid-2022 has stopped. It had reduced the overall PPI increases into the pre-pandemic range, and papered over the inflationary forces in services. But over the past three months, energy prices stopped dropping. In December, the energy index jumped by 3.5% from November, but thanks to the plunge earlier in the year was still down 2.0% from a year ago.

Food prices declined by 0.1% in December from November, after a 2.9% spike in the prior month, and on a year-over-year basis rose by 4.7%.

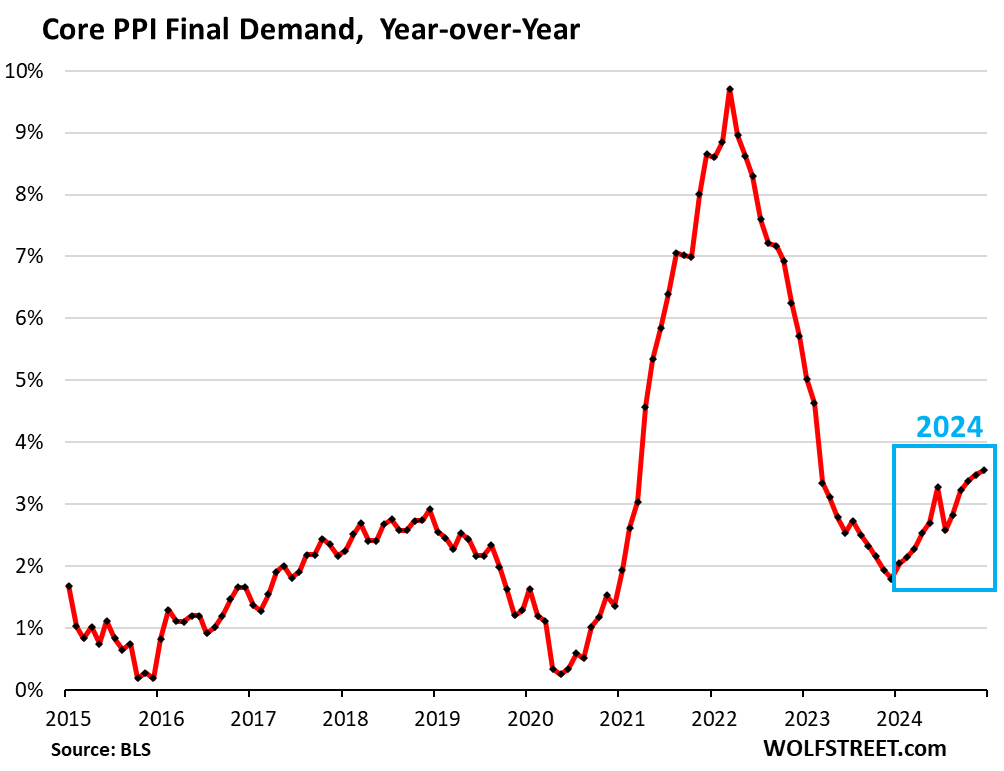

“Core” PPI, which excludes food and energy, accelerated to 3.55% year-over-year in December, the fastest pace since February 2023, up from 3.47% in the prior month.

On a month-to-month basis, Core PPI edged up 0.04% (0.5% annualized), after a series of hefty increases in the prior months.

The Services PPI, which accounts for two-thirds of the overall PPI, accelerated to 4.03% year-over-year in December, the fastest pace since February 2023, and up from 3.91% in the prior month.

Month-to-month, the Services PPI edged up by 0.5% annualized (+0.04% not annualized) after a series of hot increases over the past four months, ranging from +3.1% in November to +6.0% in August.

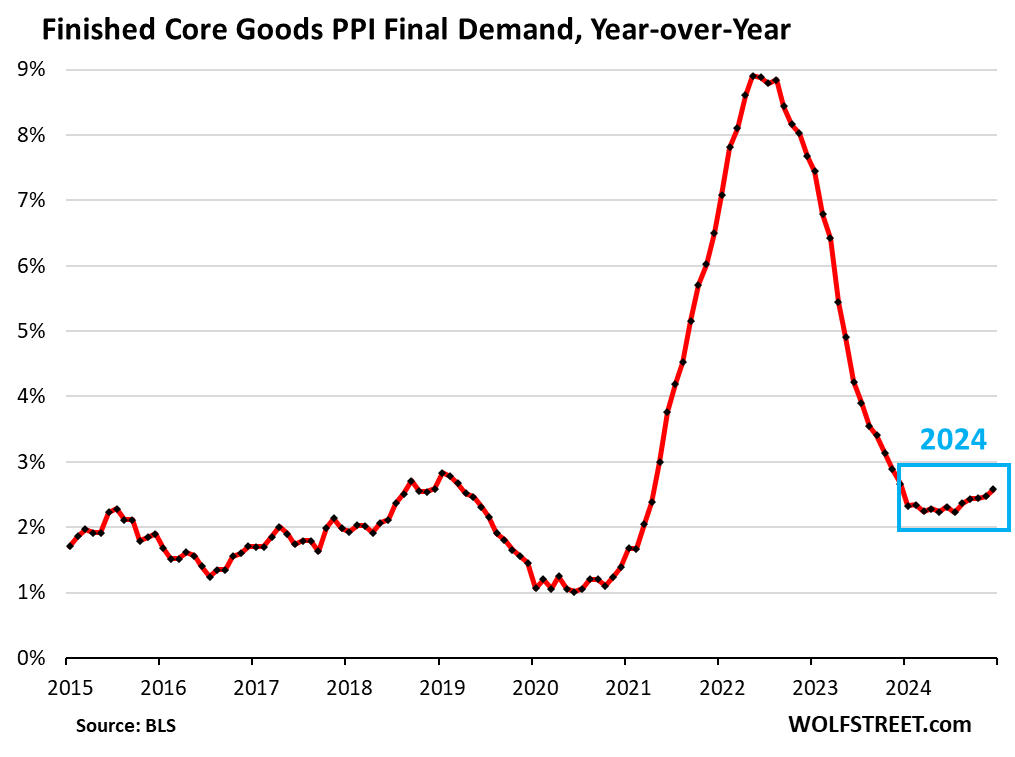

The “Finished core goods” PPI rose by 2.58% year-over-year in December, an acceleration from 2.48% in November, and the fastest increase since December 2023. On a month-to-month basis, the index rose by 1.9% annualized.

The index has more or less gently accelerated over the past six months. But the goods sector is not where inflation is a big issue at the moment.

The PPI for “finished core goods” includes finished goods that companies buy but excludes food and energy products.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The bond “market” is telling us as much…

Great summary, thanks Wolf. When I saw the numbers this morning, I was not impressed. The talking heads were happy numbers were better than expected. Markets popped, now gyrating as they argue about it.

I liked the analysis at https://www.stlouisfed.org/on-the-economy/2025/jan/look-inflation-recent-years-lens-macroeconomic-model which I read as saying Congress and the Fed were almost entirely at fault for inflation. The model says the supply issues will be back.

Keep watching those long term bond rates !

“Hi Yo silver…away!”.

For some strange reason I find this report to be good news.

Look at month-on-month annualized. That is a good predictor of where inflation may be going.

I like hearing “Services PPI edged up by 0.5% annualized” and “finished core goods index rose by 1.9% annualized.”

I think anyone here would love it if a year from now both are .5% and 1.9% year-over-year

Look again at the blue line in the month-to-month chart. The big jumps and drops and middle values are randomly distributed, and each by itself gives no indication of what the next one will look like, except that when you have a couple of low readings in a row, it’ll be followed by some high readings. You cannot conclude anything from these volatile month-to-month charts.

can’t wait to see 2025 roll thru

with brent crude at $80

I would say we have 15% in gas + another 10% services

fiat $dollar gonna make this ugly

None of those charts support 100-BP cuts by the Fed.

Powell is quickly falling below the curve just like 2021 into early 2022.

Fortunately, the bond market is going to get him above the curve.

Today January 18Barrons reports:

Back on Track. It was a good week for inflation. As a result, it was a good week for stocks. The S&P 500 rose another 1% today to finish the week up 2.9%. It’s the best week for the large-cap index since the U.S. election week in November. The Dow Jones Industrial Average gained 335 points on the day, bringing its one-week gain to 3.7%.

While there was no big news Friday, traders seemed to be digesting a week of positive developments across the economy and market. The consumer price index, excluding fuel and energy, cooled more than expected in December.

yes, that kind of stupid reporting is exactly the problem.

Bit of a bounce on that “soft landing”.

There was no landing. Still flying at 40,000 feet.

Yeah! CPI came in lower than expected so wall street is happy because now stocks can go up in price, BTC can go up in price , and Treasury interest rates dropped and thus housing can go up in price. LOL

It’s called a touch & go!

But inflation is still rising. I guess the market spin works on rising inflation too.

Financial media is almost uniformly pushing the “lower than expected” angle, using headline adjectives like “tame” and ” subdued.” You would think producer inflation had gone down if you weren’t paying attention.

Noted the same. I didn’t look at the details until now. What propaganda!

Look at the month-over-month annualized (see above). Is that so bad if it continues?

Look again at the blue line in the month-to-month chart. The big jumps and drops and middle values are randomly distributed, and each by itself gives no indication of what the next one will look like, except that when you have one or two low readings in a row, it’ll be followed by some high readings. You cannot conclude anything from these volatile month-to-month charts.

Gurus on fintwit saying the same thing, inflation is cooling. No one thinks a bear market could ever happen again, Fed is just too good at what they do, lol.

Come on Jerome. Time for a rate cut.

The main stream media are “304”s in street language.

Almost all US media is owned by six corporations and they spin everything based on their needs, which include advertisers, click through rates, political manipulation, and portfolio burnishing.

Correct, with advertising clients being one of the high priorities in their biased and agenda-driven reporting.

Whatever spin will result in their financial industry advertising clients receiving the highest volume of trading transactions, that is the angle they will take.

No wonder so many people are actively seeking out alternative sources for information other than the MSM.

Pea Sea-

You captured my surprise perfectly when I saw the Dow and RSP up, and going to MSMedia, saw “lower than expected” talk

Wonder how long it will take for the stock market to appreciate the risks that the bond market is sniffing out…

Higher inflation can mean higher revenue and profits, hence higher stock prices. Some will win, some will lose.

Tomorrow there will be more metrics to throw into the spin cycle.

Wolf, thanks for giving us the real data and charts so that we can see it. I need to delete CNBC from my phone. Their headlines are always misleading and biased.

I always enjoy your post.

Thank you for the informative data analysis Wolf I have pivoted my portfolio to fidget spinners I think they will do well in this new inflationary regime

Me too! Looking forward to Wolf’s CPI breakdown as well!

I just spit out my salad. Thanks for the hearty laugh.

is mr wolf not going to delete that?

When I was young and dumb, I bought a big box (96 count) of incandescent light bulbs. I thought enviro groups would get them outlawed, and I’d be able to resell them with a big markup.

In other words, it tripled.

“PPI accelerated from 1.06% in December 2023 to 3.31% in December 2024,”

That’s the real story, thank you!

I am very glad to find this site, the mainstream media has an agenda and it is near impossible to trade stocks listening to their skewed reporting. It is refreshing to find just the facts.

It’s getting harder and harder to believe the Fed has the conviction to achieve 2% inflation in the foreseeable future. They probably need at least 3-4% inflation to avoid recession. Everybody admits this, except the Fed.

I wish they’d make 2% inflation a real priority at this time when unemployment is very low. If the goal is to balance inflation and employment, the course should be obvious when inflation is too high and unemployment is too low. What am I missing?

Recessions are not disasters, unless they are continually avoided with monetary or fiscal subsidies.

What am I missing?

The perspective of the next administration…

As long as there are buyers for Treasuries, the Fed has room to let inflation run above target.

Fed could have a problem if actual bond vigilantes return…

The 10 year has gone up 100 bps in the past few months. That’s something for sure. Maybe not vigilante status but getting there.

Yep, bond funds are feeling the heat again.

But is it transitory ? Inquiring minds would love to Know.

Bond market knows

Noticed some big increases in insurance premiums as the New Year takes hold. My Blue Cross/Blue Shield premiums just went up 12%. It ate up nearly half of my COLA. Add in inflation and I’m losing take home pay. Most people are in the same boat. They think they are getting a pay raise and are actually getting squat.

My Anthem “EPO” plan up almost 20%. I’m switching to Canada

My United Healthcare Medicare advantage plan went from $0 to $12/month, eating up nearly half of my COLA also. But this is consumer price index, not producer.

Still hurts!

My Anthem plan went up too. At least it reduces my taxable income.

I had Blue Cross/Blue Shield through the ACA. Like you said, they went up right around 12%. Fortunately, I’m not subject to the whims and laziness of corporate HR. I dropped Blue Cross and get insurance through a company that represents most of the hospital systems and doctors in Central Florida (HealthFirst). My monthly premium dropped to $0 though my deductible went up by $6k. Fortunately, my wife and I are healthy, and I’m estimating spending less than $1500 out of pocket this year for everything. Worst case (a terrible car accident or something) I can write a check for the deductible. Not everyone can do that though.

So with PPI increasing, as an individual this is just another reason of many to tighten my belt for 2025. I admittedly was quite the drunken sailor in 2024. I held off from 2020 through 2023.

As onshoring of manufacturing has continued, might this be a disproportionately large component of PPI increases? I’m all for onshoring, and think taking an inflationary hit from say 2% to 3% is WELL worth it. But can an onshoring/PPI relationship even be evaluated?

CNBC and Yahoo News reported better-than-expected results, causing the market to initially rise. Are they purposely setting lower expectations to keep the market rising? Lol

A lot of people are heavily invested in both keeping real estate prices high and stock prices high. Some likely because they need plenty of greater fools to rescue their positions for a fast exit.

Lower for Longer!!

Lower TLT prices for longer.

Definitely looks like inflation is about to drop again. End of the cycle. Treasure yields already pulling back. Pretty amazing that Mr Powell got it right.

LOL, CPI inflation ROSE YoY by the most since July and MoM by the most since February.

https://wolfstreet.com/2025/01/15/beneath-the-skin-of-cpi-inflation-yoy-cpi-2-9-yoy-worst-since-july-mom-cpi-0-39-4-8-annualized-worst-since-february-core-cpi-stuck-for-7th-month-at-3-1-3-3/

I heard some bond fund manager back in November say the ten year would trade between 4.25-4.75% and he has been mostly correct.

Doesn’t the bond market historically figure things out faster than the stock market?

I think I need to charge more for the services I provide, so that I can afford to pay for everyone else’s services!

MW: U.S. budget deficit swells to record $711 billion in first quarter of fiscal year

Just a minor detour in Jerome’s race to the bottom.

Jerome’s replacement is likely to not as good and extremely easy to manipulate.

OMG I have to agree with you!

Jerome was picked by the guy who will now pick the next guy. Keep that in mind.

And the guy who is going to pick the next guy is all of a sudden a crypto bro, set to adopt BitCON so all the billionaire whales can get even fatter. This country is, IMO, f**ked no matter which party gets in. The corporations and billionaires won. They control everything.

Let us hope he learns from his mistakes.

The replacement will be picked based on nepotism, loyalty, or some other irrelevant reason. There is little reason to believe the replacement will possess much knowledge or experience with economics.

👍👍 @enlightenlibertarian,

That should be the real headline !!!

I don’t know. Not living there I look at aldi ads occasionally to compare prices. Not services I know but those prices seemed stabilized.

For services before covid could rent Economy car with enterprise one month for around $1,050.00. Then that more than doubled and would not budge. Switched to turo which was an OK experience and much cheaper.

Now checking enterprise again and three different months at three different locations and I get Economy car for 1,130.00.

Anecdotal for sure but I’m going to saying a sign inflation coming down.

I can finally plan months long road trips again.

There is a chart for goods, last one. Look at it. It’s “stabilized.” But this is not retail inflation. These are goods that companies buy.

Rental cars are a minuscule part of services in CPI.

You are absolutely right Wolf. It’s a very small part overall. But for me its kind of big and allows me to road trip the usa. Looks like they say inflation did ease a bit and market responding positively.

To see such a drop in enterprises rates something is up for car rental anyway. Although I’m not looking at pure summer months. More sep and later. Time will tell

I would not be buyer of car rental companies stocks

Car and truck rental CPI (0.1% of overall CPI), and included in my services CPI table, fell 6.2% yoy.

https://wolfstreet.com/2025/01/15/beneath-the-skin-of-cpi-inflation-yoy-cpi-2-9-yoy-worst-since-july-mom-cpi-0-39-4-8-annualized-worst-since-february-core-cpi-stuck-for-7th-month-at-3-1-3-3/

Don’t forget that your rental car has an extra transmission gear and cupholder now, so for CPI the price is unchanged. :-)

Thanks Wolf for clearing out the smoke!

“Thanks Wolf for clearing out the smoke!”

….and “mirrors!”

As Dr. Milton Friedman said: “inflation is like alcoholism”. “In both cases…the good effects come first, the bad effects only come later.”

At 3 percent inflation, prices double in 24 years.

What do these numbers tell us, if anything, about getting back into the high quality bond market? Feels to me like if we are going to see more inflation it won’t go where it was and looks like interest rates will stay put or go down slowly.

now the 10 year is down 12 bps based on a “low inflation” report.

the tail’s lies are wagging the dog. we live in a dystopian society.

“BitCON solves this.”

Well absolutely! Especially if the coin is really doggy! /s

We are in a full-on speculative mania that the FED created, which unleashed massive, rampant inflation. Not only were they too late to start fighting it, they exited the fight too early and it has now re-accelerated.

They will likely rest on their laurels and watch it continue to eat away at the value of the dollar until, once again, they do too little. This is all by design. The goal is to debase the dollar to pay for all of the sins of the past, at the expense of the working class and poor.

Prepare accordingly.

DC

It’s rotten to the core.

theCon dot TV

No, this manic speculation was not created by the Federal Reserve at all, not can it be tamed by the Federal Reserve. Blame stupid speculators throughout the US economy and major Wall Street players and ;the Congress of the US.

So interest rate suppression didn’t add any fuel to the fire???

Just to be clear, is it also your opinion the Fed had nothing to do with the ongoing surge in US federal debt?

TRANSITORY

Transitionary

DM: National craft store JOANN chain files for bankruptcy and sparks fears all 800 shops face the ax

A beloved craft and fabric retailer with a history spanning over 80 years has filed for bankruptcy – and a retail expert warns its demise is now almost certain.