The 6-month core services PCE inflation index, accelerating since August, hit 3.7% annualized. Chip prices and software wreak havoc amid consumer electronics.

By Wolf Richter for WOLF STREET.

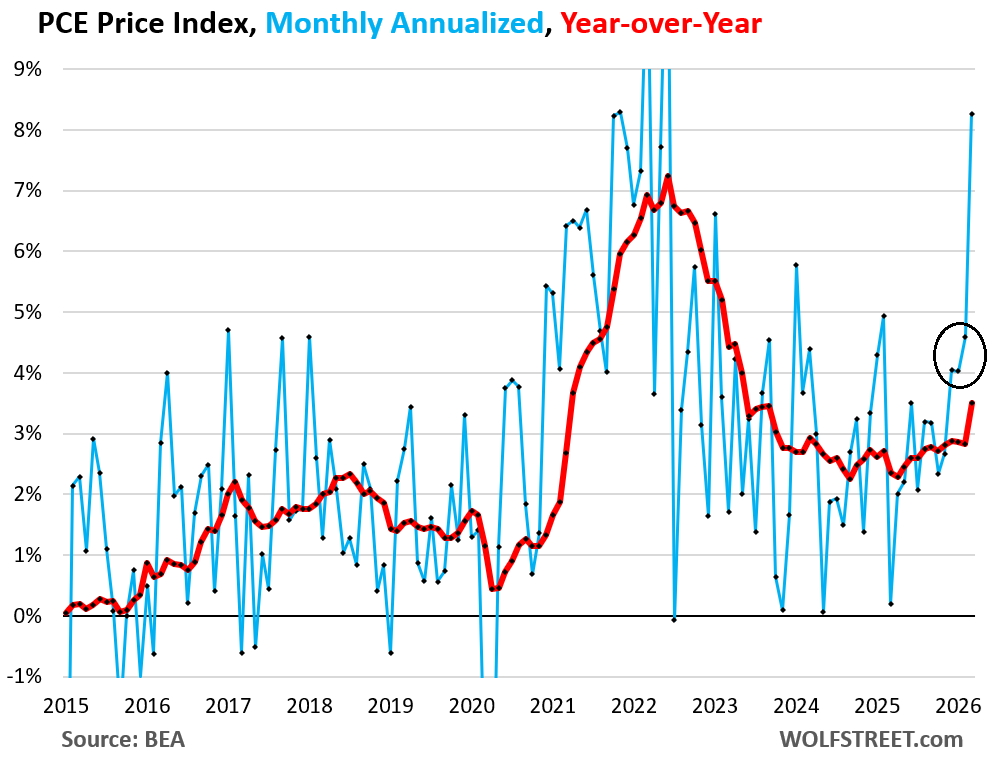

The PCE price index, which the Fed favors for its inflation yardstick, spiked by 0.66% in March from February (+8.3% annualized), the worst spike since mid-2022 at the peak of the inflation surge.

Inflation has been accelerating since mid-2025. In each of the three months of December, January, and February – so before the war and before the energy price spike – the PCE price index had already surged by 4% to 4.6% annualized (black circle in the chart). The March spike is on top of that acceleration (blue line). And it was energy, but not just energy.

Year-over-year, the PCE price index jumped by 3.5%, the worst since May 2023 (red line). The Fed’s target for the year-over-year measure is 2.0%, and PCE inflation has been moving away from it relentlessly for the past 10 months, and the energy price spike came on top of it.

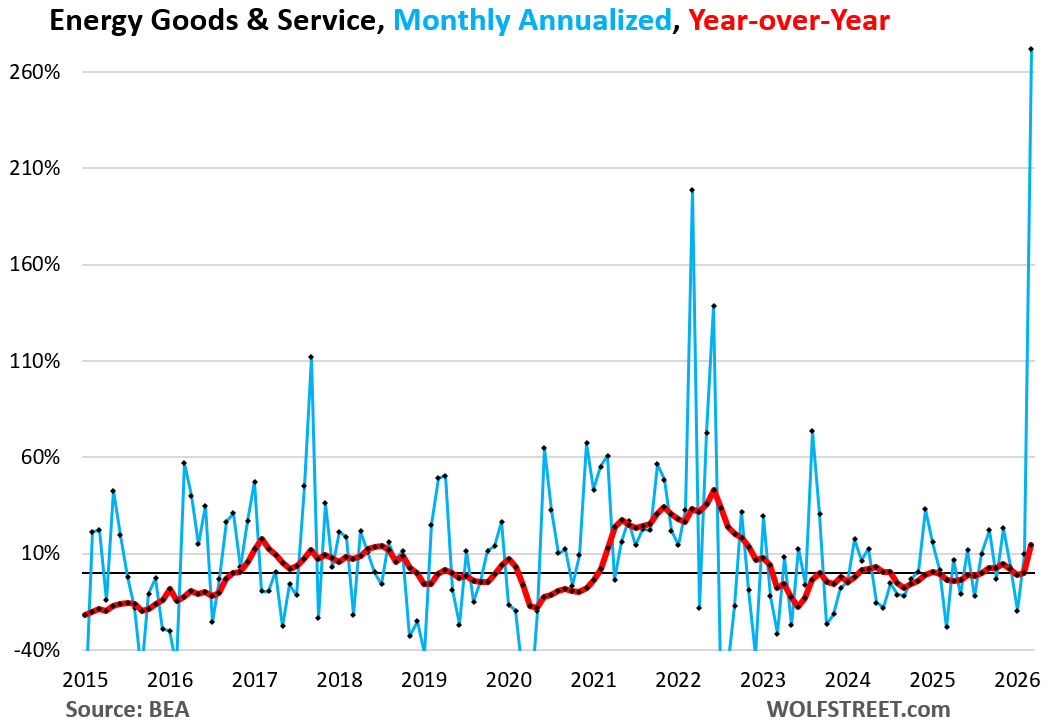

The energy PCE price index exploded by a historic 11.6% in March from February (+272% annualized).

March pushed the year-over-year increase to +14.4%, from a negative reading in February. This is what a price shock looks like.

Note that the US is the largest crude oil and petroleum products producer in the world, a large exporter of crude oil and petroleum products, including gasoline and diesel, and gets very little crude oil from the Strait of Hormuz. The gasoline whose prices spiked in March had already been in tanks at gas stations or at refineries or in transit, purchased at the low February-and-before prices, and that price spike went straight to profit margins of oil companies, refiners, and gasoline retailers.

It was not just energy.

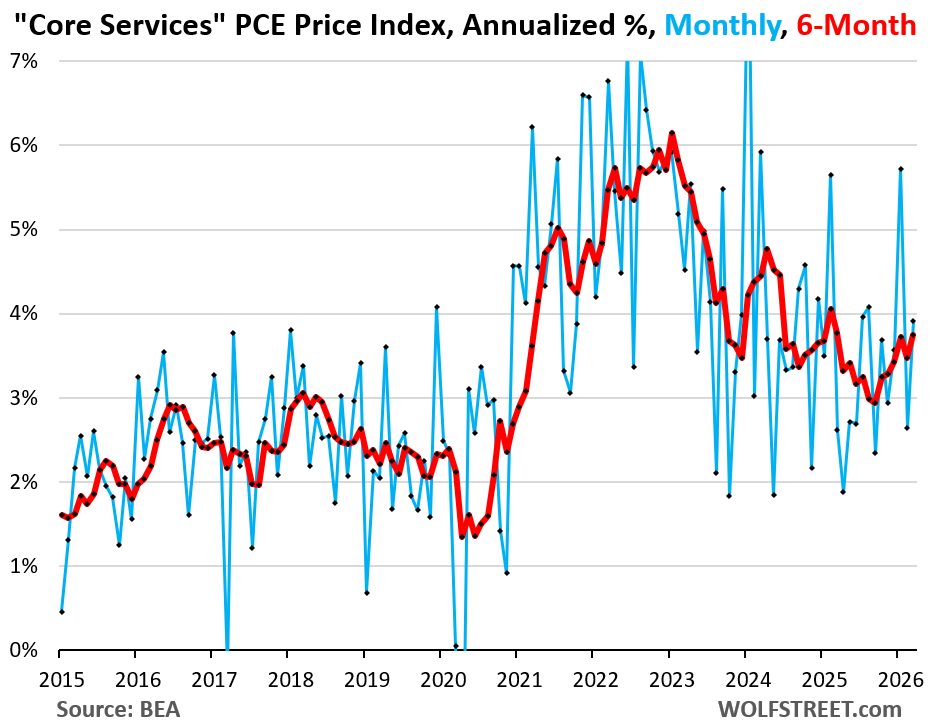

Core services, which account for about 60% of the PCE price index, jumped by 0.32% in March from February (+3.9% annualized).

The six-month core services index has been accelerating since August. In March, it jumped by 3.7% annualized, the highest in a year. The six-month average shows the recent trend beyond the month-to-month squiggles.

Year-over-year, the core services index accelerated to 3.3% (not shown).

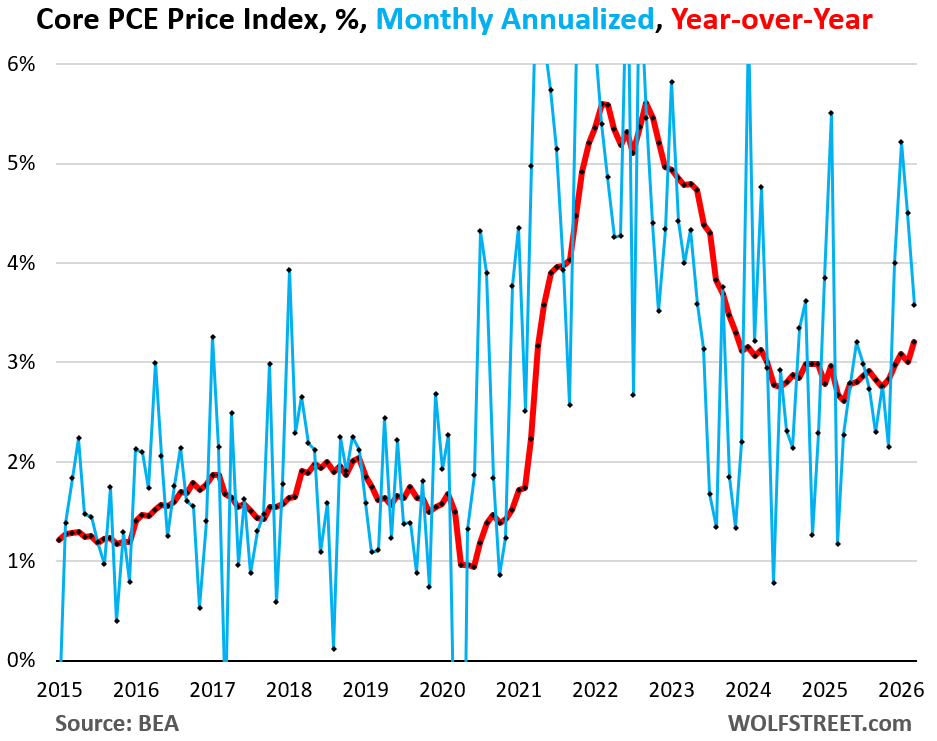

The core PCE price index, which excludes energy and food, jumped by 0.29% in March from February, or +3.6% annualized, after three months in a row of 4%+ annualized readings (blue in the chart).

This pushed up the 6-month core PCE price index to +3.7% annualized, the worst since June 2023. The six-month index reflects the more recent trend, and that trend has been going in the wrong direction.

The year-over-year core PCE price index (red in the chart) rose by 3.2%. The Fed’s target for this measure is 2.0%. And being a “core” measure, it does not include the gasoline price spike.

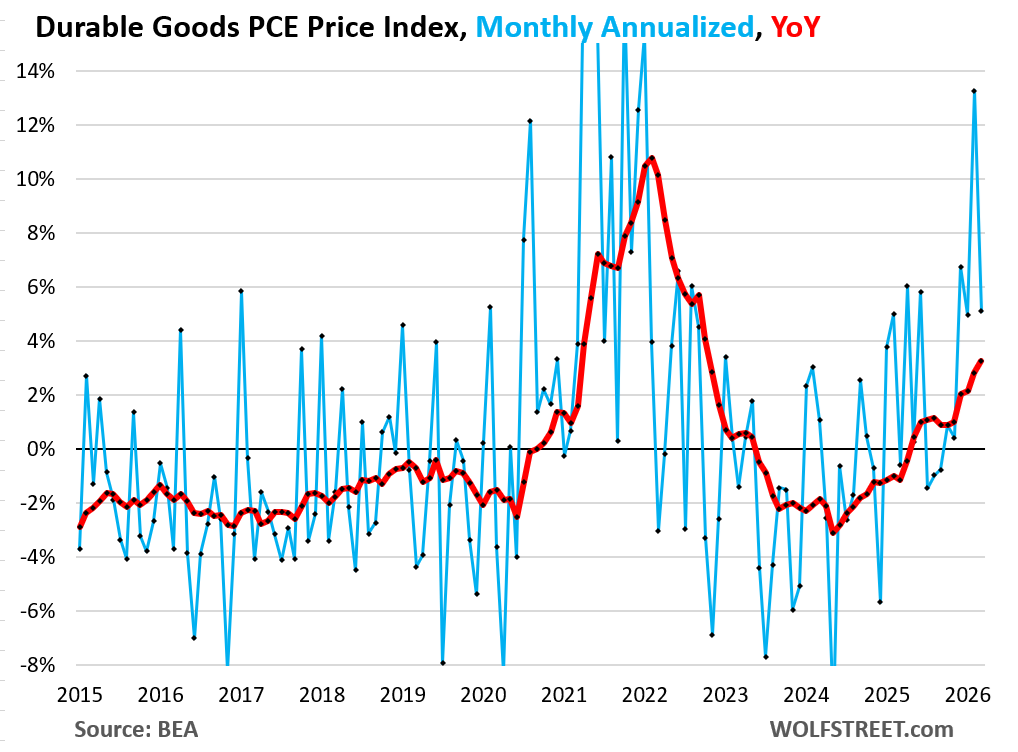

Durable goods prices jumped month to month by 0.42% (+5.1% annualized).

Of the major categories, many had declines or only small increases:

Declines or only tiny increases:

- Appliances: -2.3%

- Cars & trucks: +0.07%

- Motorcycles: unchanged

- Auto parts and accessories: +0.1%

- Furniture and Furnishings: -0.5%

- Video & audio equipment: -0.02%

- Sporting equipment, supplies, guns, ammo: -0.2%

- Books: -0.4%

- Phone & related communication equipment: -0.8%

But some had huge increases, such as computers due to spiking chip prices due to the AI investment bubble; software subscriptions that got jacked up; and jewelry as jewelers passed on much higher gold prices.

Large increases:

- Glassware, tableware: +0.5%

- Tools and equipment for house & garden: +1.2%

- PCs, laptops, tablets, driven by the surge in chip prices (see AI): +1.5%

- Computer software & accessories (jacked up subscriptions): +4.0%

- Pleasure boats & aircraft: +0.4%

- Jewelry, passing on the much higher gold prices: +1.2%

- Musical instruments: +1.4%

- Bicycles & accessories: +0.4%

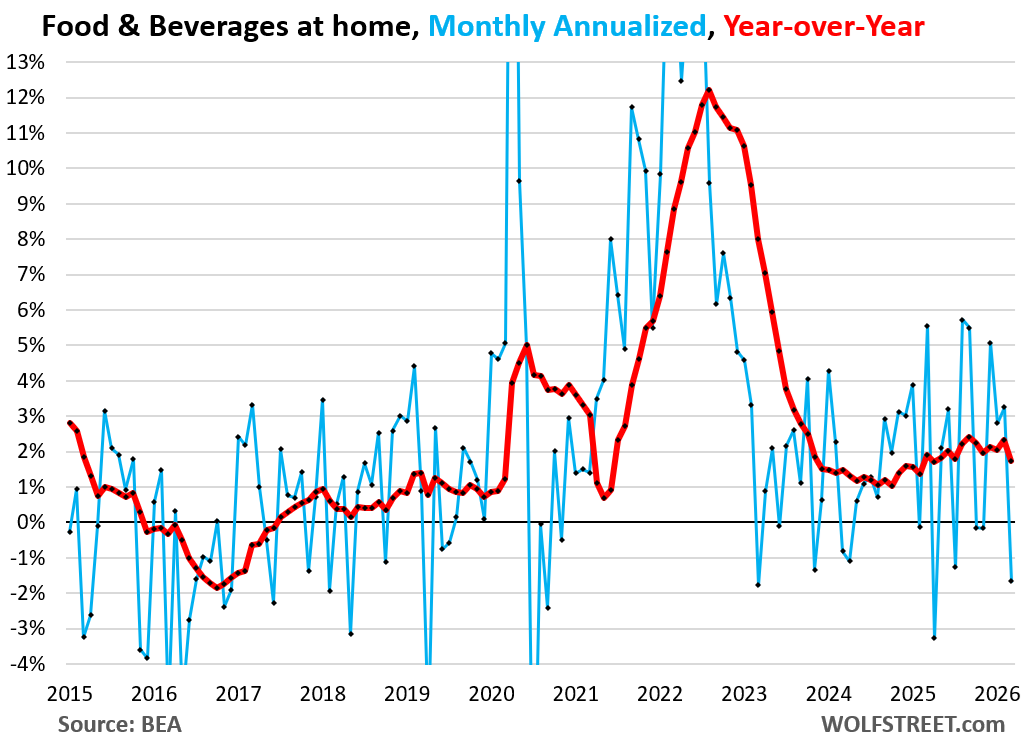

Food prices dipped by 0.1% in March from February (-1.7% annualized), after three months in a row of substantial increases (blue)

Year-over-year, the index decelerated to +1.7% (red).

Inflation in the entire US economy is rocking and rolling.

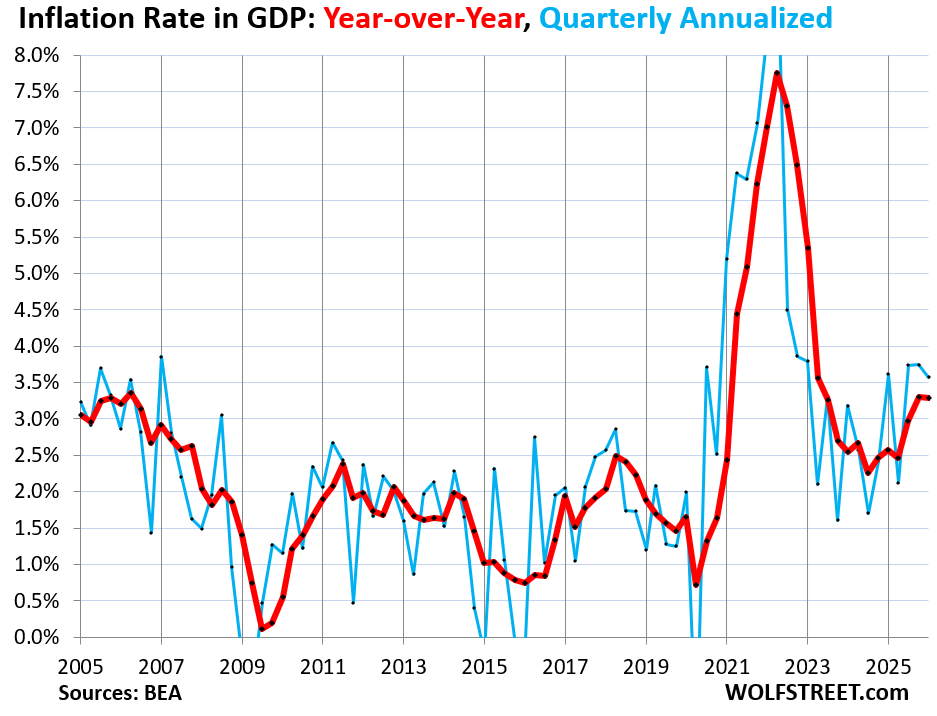

The above measures are tracking consumer price inflation; inflation in goods and services that consumers are paying for. But businesses and governments also face inflation for the goods and services they purchase.

The inflation measure that tracks inflation in the overall US economy for consumers, businesses, and governments is the GDP “Implicit Price Deflator,” also released today by the Bureau of Economic Analysis as part of the Q1 GDP data.

This overall inflation rate has been running hotter than consumer price inflation: In Q1, it increased by 3.6% annual rate, after increasing by 3.7% annual rate each in Q3 and Q4 (blue line).

This is a quarterly measure, and so the energy price spike in March was counterbalanced by the plunge in January and the smaller increase in February .

Year-over-year, inflation in the overall economy in Q1 of 3.3% matched inflation in Q4.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Media hails Jerome Powell as a hero for supposedly standing up to Donald Trump, a flattering myth that won’t age well.

In reality, he is on track to go down as the worst chairman in Fed history: the man who destroyed price stability, stripped American workers of roughly 40% of their purchasing power in just five years, and inflated asset prices to the point that housing is now out of reach for anyone but the wealthy. All of it fueled by a balance sheet ballooned to $8 trillion, complete with legally dubious forays into junk bond buying.

His epitaph practically writes itself: “inflation is transitory.”

Had the Fed stuck to its mandate and delivered price stability, it wouldn’t be politicized today. Instead, Powell seemed intent on dragging it into mission creep climate policy as well.

The result is outright failure, an incompetent stewardship that will be remembered for damage it left behind.

Agree. The asset bubble Powell helped inflate with mega QE is too insidious and damaging to be justified or forgiven.

No mention of the massive US deficit. Hard to take this post seriously.

So when can I expect rate cuts?

Howdy Gomer. SHAME SHAME SHAME. But could the FED really be that stupid??? You bet it can…

Who wants the DOJ up in their business? I don’t know about cuts but CPI will probably need to explode before they’ll dare to raise.

Glad I got into TIPS. Just gotta bail out in time, which will be tricky.