The spread between the 2-year and 10-year Treasury yields now the widest since January 2022.

By Wolf Richter for WOLF STREET.

The government sold $766 billion in Treasury securities this week, in 10 auctions, including six Treasury bill auctions and four Treasury note auctions.

The T-bill maturities ranged from 6 weeks to 26 weeks this week, totaling $538 billion. Every month, the Treasury Department is now selling over $2 trillion of T-bills, most of them to replace maturing T-bills, but auction sizes have been increasing, and those increases add additional debt to the $38.6 trillion pile. These T-bill auctions are a huge well-oiled machine:

| Type | Auction date | Billion $ | Auction yield |

| Bills 6-week | Jan 27 | 94.2 | 3.635% |

| Bills 13-week | Jan 26 | 93.1 | 3.570% |

| Bills 26-week | Jan 26 | 80.6 | 3.525% |

| Bills 4-week | Jan 29 | 105.4 | 3.630% |

| Bills 8-week | Jan 29 | 95.4 | 3.635% |

| Bills 17-week | Jan 28 | 69.3 | 3.590% |

| Bills | 537.8 |

The maturities of the four Treasury note auctions ranged from 2 years to 7 years, and totaled $228 billion.

The 2-year Floating Rate Note (FRN) was sold at a “spread” of 0.099%. Investors who bought them get an interest rate that resets every week. That weekly interest rate reset is based on the yield at which the most recent 13-week T-bills were sold at auction. Plus investors get a “spread” (discount margin) that is determined at auction.

| Notes & Bonds | Auction date | Billion $ | Auction yield | Spread |

| Notes 7-year | Jan 29 | 47.1 | 4.018% | |

| Notes 5-year | Jan 27 | 74.9 | 3.823% | |

| Notes 2-year | Jan 27 | 73.9 | 3.580% | |

| FRN 2-year | Jan 28 | 32.1 | 0.099% | |

| Notes & bonds | 228.0 |

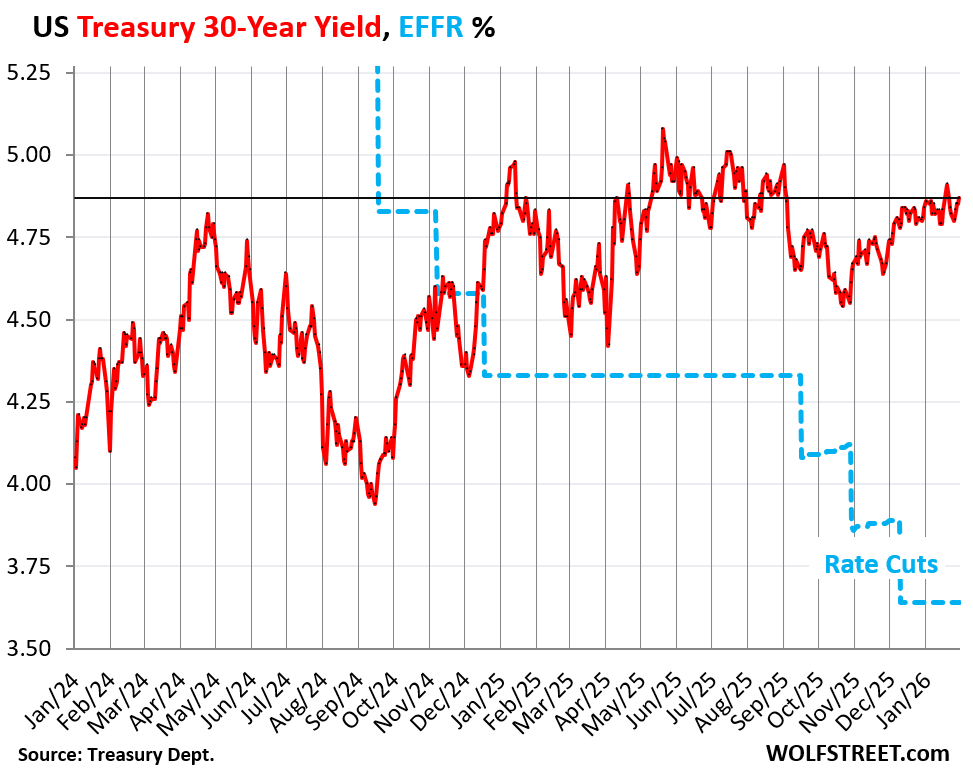

Long-term yields have trended higher since October.

The 30-year Treasury yield inched up 2 basis points to 4.87% on Friday, and was up by 5 basis points from Friday last week. It started increasing in late October, just before the Fed’s rate cut and has since risen by over 30 basis points.

The dotted blue line in the chart shows the Effective Federal Funds Rate (EFFR), which the Fed targets with its policy rates.

Since this rate-cut cycle began in September 2024, the Fed has cut its policy rates by 150 basis points. Over the same period, the 30-year yield has risen by nearly 100 basis points.

The widening gap between the EFFR and the 30-year yield, now at 123 basis points, shows that the Fed’s rate cuts have led to rising long-term bond yields because investors in long-term bonds are worried about future inflation. A lax Fed that cuts rates as inflation is accelerating is a worrisome signal for those investors.

But a 30-year Treasury yield of 4.87% is still low considering that inflation is now about 3% and looks to be accelerating amid a “let it run hot” economic philosophy at the government.

The Fed’s rate cuts have pushed down short-term yields, such as the yields at the T-bill auctions, but long-term yields are negotiated in the bond market and reflect the bond market’s concerns about future inflation.

The bond market is also worrying about future supply of long-term Treasuries to fund the ballooning deficits, and thereby new investors might have to be pulled in with higher yields. But higher yields mean lower prices for existing bondholders.

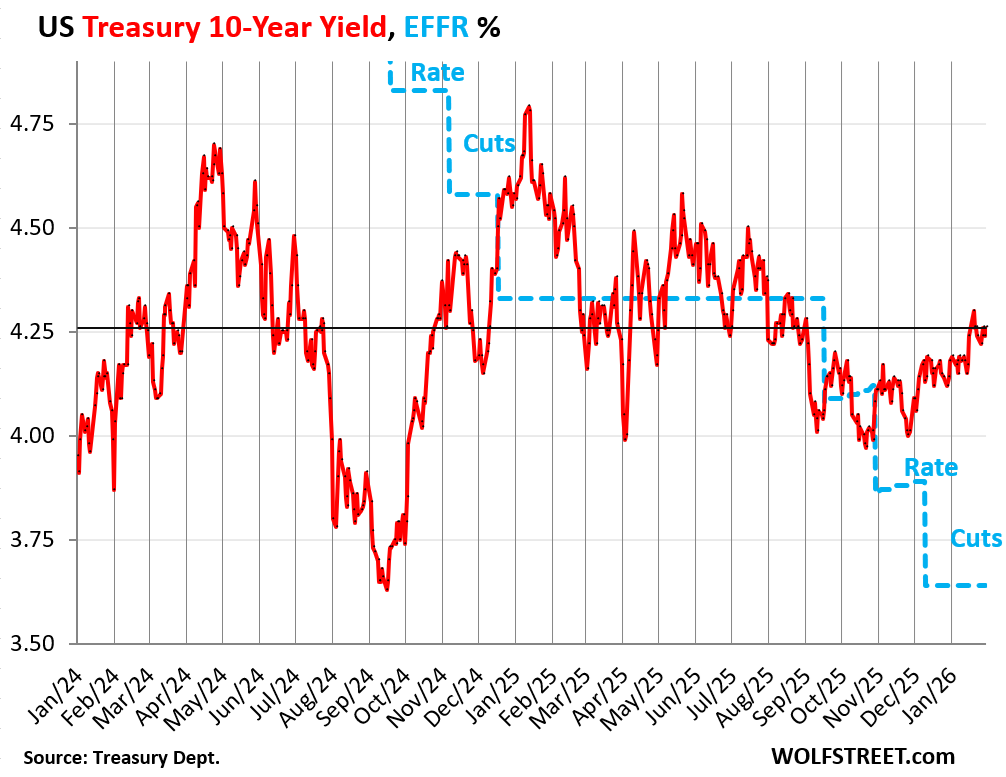

The 10-year Treasury yield was unchanged on Friday, at 4.26%, despite the utter chaos in the silver and gold market, upon the news that Trump had nominated Kevin Warsh for chair of the Federal Reserve.

The 10-year yield is up by 4 basis points from Friday a week ago. It too started rising on the eve of the October rate cut and has risen by 28 basis points since then.

Warsh has been hostile to QE and the Fed’s large balance sheet, and hasn’t changed his tune to get the job, and he had already put his career at the Fed where his mouth was when he quit in 2011 over QE-2. So Trump must have bought into his logic that a smaller balance sheet, by reducing the money supply, would lead to lower inflation, and eventually lower inflation would lead to lower long-term interest rates (my discussion of Warsh’s QE hostility is here).

Under this theory, the Fed might cut short-term rates a little more, and reduce the balance sheet (money supply) at the same time, in the hope that inflation and long-term rates would follow.

This kind of monetarist thinking is heresy at today’s Fed, and he’ll have to struggle with a resisting staff, and he’ll have to persuade enough members of the FOMC to get a voting majority to get anything like that implemented. So it won’t be a cakewalk.

Some other FOMC members have also expressed thoughts to the effect that the balance sheet could be smaller. I assume that Powell, the architect of the mega-QE during the pandemic and the still huge balance sheet despite $2.4 trillion of QT, has squashed further discussions of those thoughts, and will resist them as long as he is on the Board of Governors (his term as governor expires in January 2028).

That strategy of reducing the money supply by reducing the balance sheet pulled the rug out from under the “debasement trade,” which is why the dollar rallied on the news, cryptos tanked further, gold plunged, and silver collapsed by 30% from the high of the day before.

But the bond market seems to be cool with it. Just get that inflation down!

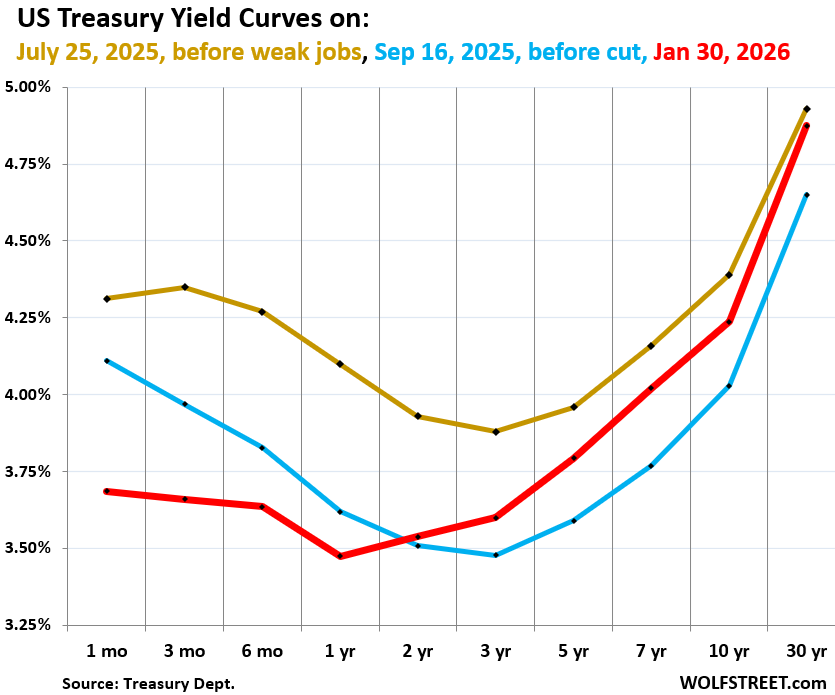

The yield curve has steepened since the Sep 2025 rate cut.

The chart below shows the yield curve of Treasury yields across the maturity spectrum, from 1 month to 30 years, on three key dates:

- Red: Friday, January 31, 2026.

- Blue: September 16, just before the Fed’s first rate cut in 2025.

- Gold: July 25, before the labor market data turned sour.

Long-term yields have risen since September 16, 2025, but the three rate cuts since then have pushed down short-term yields, causing the yield curve to steepen.

And the big sag in the middle is nearly gone, with the lowest yield now being at the 1-year marker (3.48%)

The 1-month yield (3.69%) is bracketed by the Fed’s policy rates (3.50%-3.75 %) and closely tracks the EFFR (3.64%).

Every yield from 2 years on up has risen since the September 2025 rate cut.

The spread between the 2-year yield and the 10-year yield widened to 74 basis points on Friday, the widest spread since January 2022, indicating to what extent the yield curve has steepened between the two.

Part of the reason why the spread has widened is because the 2-year yield is still so low, at 3.52%, and has barely ticked up since September 16. Investors in the 2-year yield are still counting on a rate cut or two later this year:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Is it just my poor recollection, or were yield curves typically bowed outward back in the olden days … versus being sloped inward as they have been recently. (Ignoring when they were inverted.). Any significance to that?

In a perfect world, yields are linear. A 1000 loan paid in 1 month should get a better interest rate than 1 year and 10 years respectively. It’s only recent that we see a more linear pattern. The problem I forsee is long term yields going up.

Why am I continually thinking of our national debt? Why am I concerned? I don’t think any of our elected officials think too much about it. Should I just forget it??

That’s what tariffs are for, right? To pay that down.

Whew! I can sleep like a baby tonight…

very interesting reactions. something is not like it was for past 30 years……As of early 2026, gold has overtaken U.S. Treasury bonds as the world’s largest foreign reserve asset, with central bank holdings approaching $4 trillion, driven by record high prices and reduced confidence in dollar-denominated debt. separately, the dow/gold ratio for the entire 21st century has had gold a 4x better investment since Y2K new years eve. i enjoy the work and charts and analysis and education. thank you Sir.

“gold has overtaken U.S. Treasury bonds as the world’s largest foreign reserve asset”

1. Gold is NOT a “foreign reserve asset.” It has nothing to do with foreign currency. It’s a “reserve asset.”

2. The only reason why gold has overtaken Treasury securities is because the price of gold has nearly DOUBLED over the past 12 months through Thursday, and has more than tripled in five years. And many central banks, including the ECB, which hasn’t bought any gold in a very long time, mark their gold to market, doubling and tripling their holdings just because the price has risen. A decline in prices would unwind that. Yes, gold prices have a tendency to plunge long and hard, last plunge was 50% starting in late 2011.

Hello mr Richter,

A question from the Netherlands.

I did some research online but can’t find the answer to my question.

Is there and overview how much debt the US has to refinance this year 2026 and next year 2026. I think it’s called a maturity wall

Can the amount of refinancing also be catagorized in short term debt and long term debt.

Thanks, I enjoy reading your articles.

If you visit the Netherlands someday, you’re welcome to visit.

T-Bills get refinanced all the time. So a 1-month T-bill gets refinanced every month. There are something like $400 billion in 1-month T-bills outstanding, so every month $400 billion in 1-month T-bills have to get refinanced, nearly $5 trillion a year, but it’s the same $400 billion in T-bills that get rolled over.

So now do that with all other T-bills, and you’ll get some huge numbers. That’s why the big numbers of the maturity wall stuff are just kind of irrelevant. Rolling over the debt isn’t a problem, and has never been a problem. Adding the new debt becomes a problem over time.

– Off Topic: I received an email from WOLFSTREET for this post (which is good). But I also received a different email supposedly also from Wolfstreet with the title “Advertisement-Putt.live” ???????

Was this an attempt to “phising” ? Was this from WOLFSTREET at all ? I can send it to you if you want (I assume you have my emailaddress ??)

Sorry, my mistake. Just delete it.

I clicked on the wrong thing as I was playing with a technical thing, and my automatic email system sent out an email with the title “Advertisement-Putt-Live” but there is nothing there, so when you click on the headline, you will get a 401 error message (page not found). I love my automatic email system, but I cannot ever make a mistake LOL

Given the US debt of $38 trillion and rising and roughly $10 trillion in maturing debt that has to be refinanced in the next twelve months I suppose monthly auctions of this magnitude will be common practice. I am surprised that foreigners are happy to purchase this debt at such low rates rather than purchase more gold after this steep correcttion.