Consumers may be in a foul mood, but they’re making money and are spending it, and are still saving some.

By Wolf Richter for WOLF STREET.

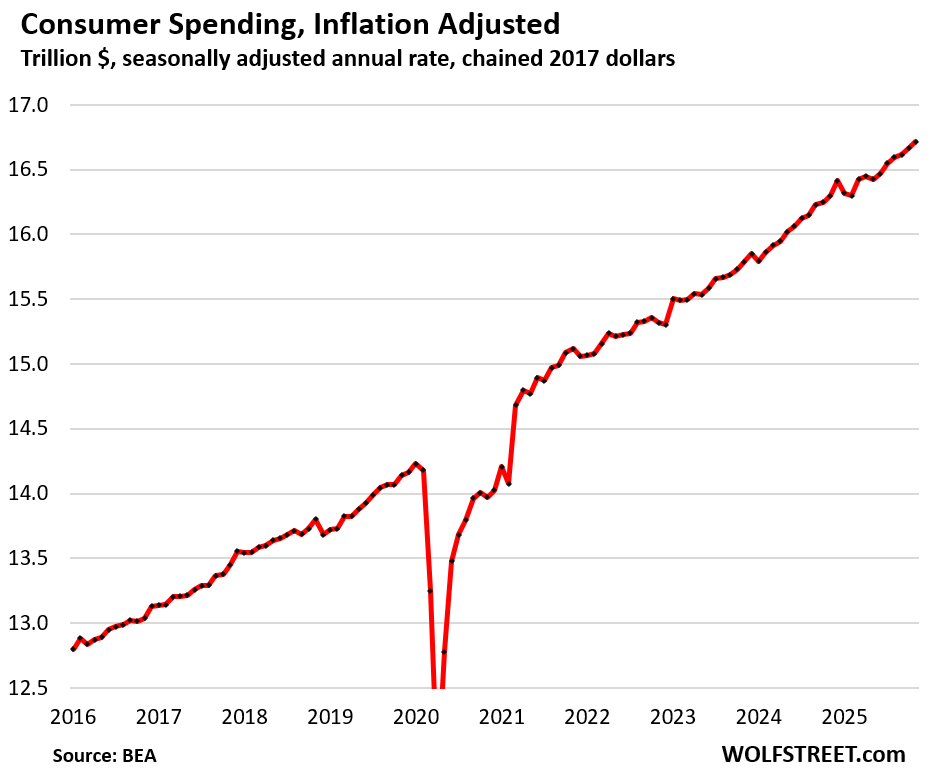

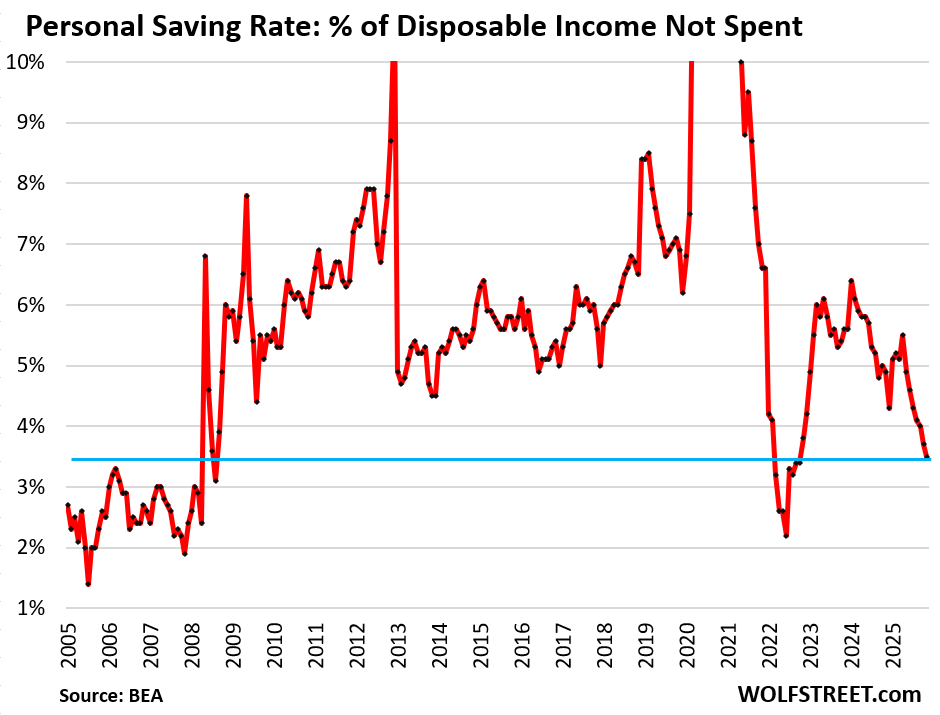

Consumers outspent inflation at a solid clip despite their sour mood, despite the wailing and gnashing of teeth in the media, despite the government shutdown, and despite the massive job losses at federal and state governments. Their incomes outgrew inflation as well. The savings rate declined to 3.5%, meaning consumers spent 96.5% of their disposable income and saved 3.5%, lower than before the pandemic but higher than before the Financial Crisis. A positive savings rate shows that spending growth isn’t funded by debt, but with income, and that there was still money left over to save.

Not adjusted for inflation, consumer spending jumped by 0.5% in November from October and by 5.4% from a year ago, according to Bureau of Economic Analysis today.

Adjusted for inflation, consumer spending (a.k.a. “real” consumer spending) rose by 0.3% for the month, and by 2.6% from a year ago, right in the range of the Good Times in the years before the pandemic, solid growth for the US economy.

The month-to-month inflation-adjusted increase in November of 0.3% was driven by substantial growth in spending on durable goods (+0.6%) and nondurable goods (+0.5%), with a smaller growth rate for services (+0.2%), adjusted for inflation.

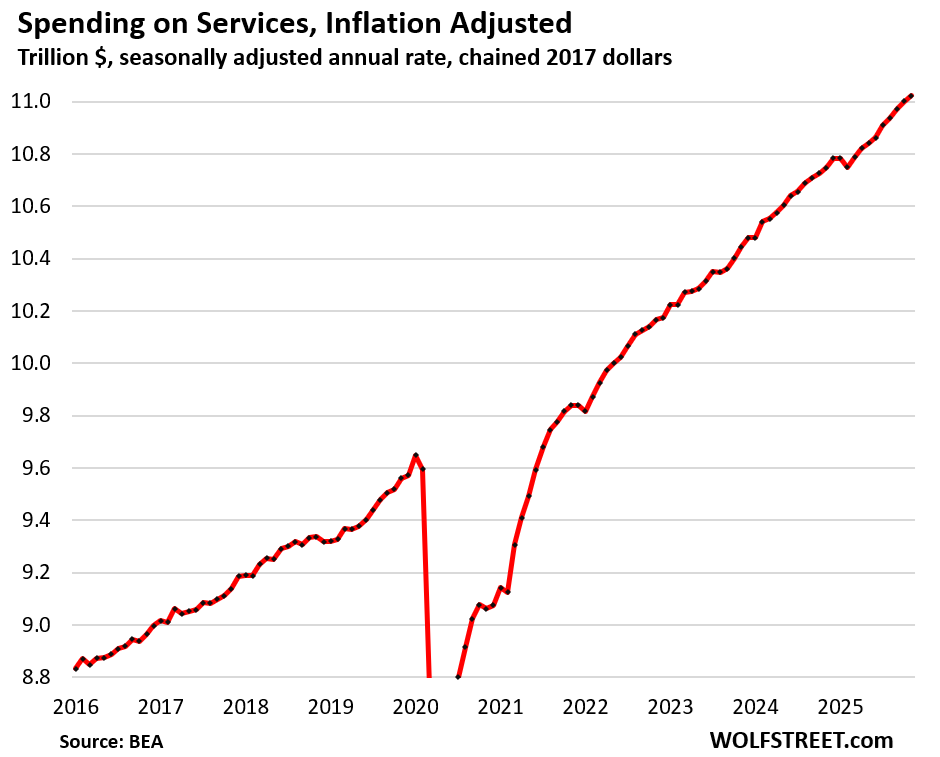

Spending on services, adjusted for inflation, ticked up by 0.2% for the month and by 2.6% year-over-year.

Not adjusted for inflation, consumer spending jumped by 0.4% for the month and by 6.0% year-over-year. Inflation in services is much higher than inflation in goods, and is difficult to dodge because many services are essential and have little or no competition or are difficult to shop around, such as healthcare and utilities.

Spending on services accounted for 66% of total consumer spending. It includes rents, utilities, insurance, streaming, broadband, cellphone services, entertainment, healthcare, airfares, lodging, rental cars, memberships, etc.

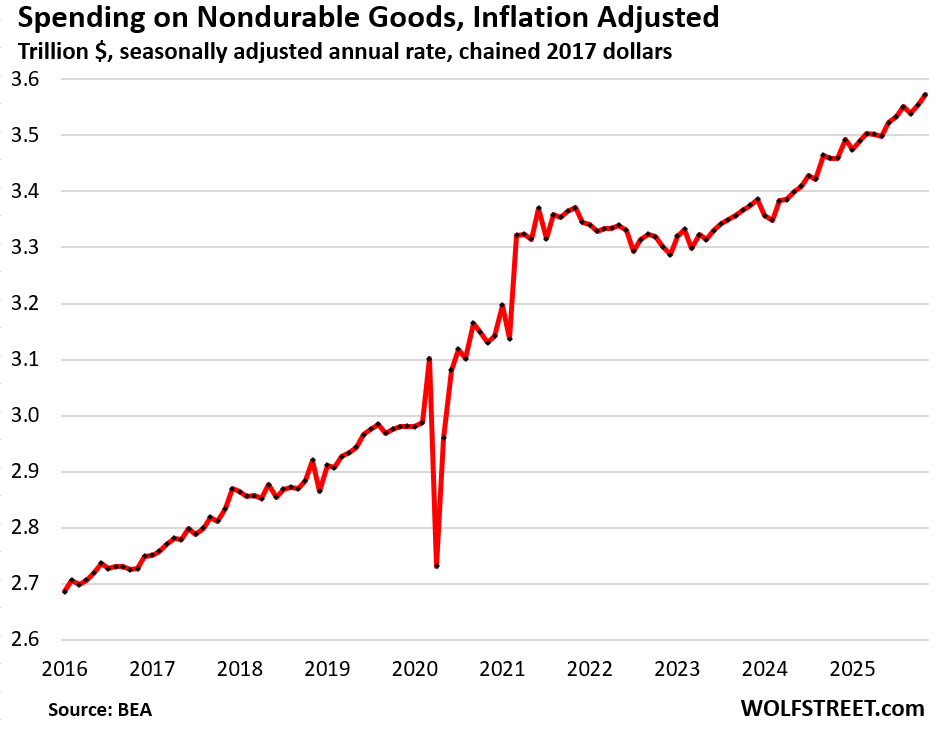

Spending on nondurable goods, adjusted for inflation, jumped by 0.5% in November from October and by 3.3% year-over-year.

Nondurable goods are dominated by food, gasoline, apparel, footwear, and household supplies:

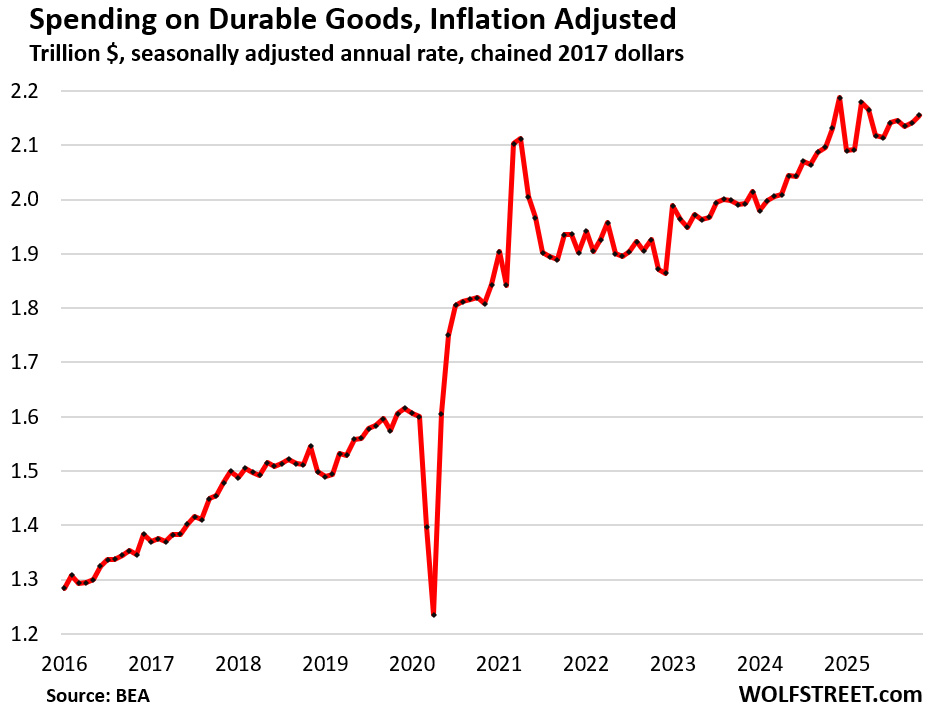

Spending on durable goods, adjusted for inflation, jumped by 0.6% for the month, and was up by 1.1% from a year ago.

In November and December 2024 and in March 2025, frontrunning the tariffs had caused big spikes in spending on durable goods. In November 2024, the month against which today’s year-over-year figures are compared, durable goods spending had spiked by 1.7% from October, which was huge. That November 2024 is the base for today’s year-over-year reading for November 2025, and that spike a year ago is the reason today’s year-over-year reading is only 1.1%; and for December 2025, the base will be the massive spike of December 2024.

Incomes

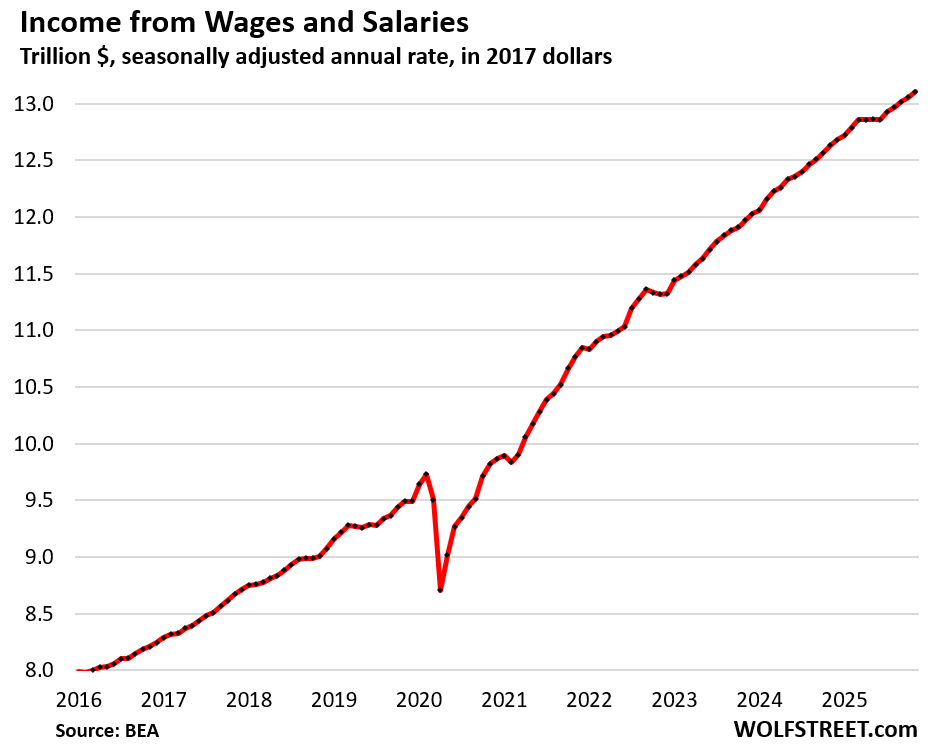

Incomes from wages and salaries, not adjusted for inflation, rose by 0.4% for the month and by 3.8% year-over-year.

This is only one part of consumer income and does not include any other forms of incomes. And it’s not adjusted for inflation.

Personal income without transfer receipts, adjusted for inflation, rose by 0.1% month-to-month and by 1.5% year-over-year.

So this is the above income from wages, salaries, plus interest, dividends, rental properties, farm income, small-business income, etc., and then all adjusted for inflation.

It means consumers continue to out-earn inflation after having taken a beating during the inflation shock in 2021 and 2022 (blue box).

But it excludes income from transfer receipts from the government (mostly Social Security benefits, but also all other government benefits, such as unemployment compensation, Welfare benefits, etc.).

![]()

Transfer receipts from the government, adjusted for inflation, dipped by 0.1% for the month but were up by 5.9% year-over-year.

The year-over-year increase of 5.9% was in part driven by the rapidly growing number of boomers receiving Social Security benefits and by an expansion earlier in 2025 of who receives Social Security benefits, which included a one-time payment of catch-up benefits in April, which caused Social Security benefit payments to surge in 2025.

During the pandemic, transfer payments spiked due to stimulus checks, unemployment benefits, including the extra unemployment benefits, and other pandemic payments made to consumers (blue in the chart below).

The chart below shows transfer receipts in blue and personal income without transfer receipts in red, all inflation adjusted. Transfer receipts account for about 19% of total personal income:

![]()

Income not spent.

The personal savings rate declined to 3.5%. That’s the portion of disposable income that consumers didn’t spend. It means they spent 96.5% of their income and “saved” 3.5%. It doesn’t mean that they put it into savings accounts. They might have bought stocks with it, or left it in their checking account, or used it to pay down debt, or whatever.

Americans have never been big savers. Money is there to be spent and keep the economy moving. But some income gets saved anyway. The current savings rate of 3.5% is lower than in the decade before the pandemic, but higher than in the years before the Financial Crisis.

Obviously, with stocks having ballooned to such an extent, 401(k) accounts and brokerage accounts have ballooned, and a majority of consumers now have stock holdings, and they look at these ballooning numbers, and they’re looking at the ballooning value of their precious metals, and surely that’s an incentive to save a little less.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

BuySome – Did you forget to put on your tinfoil hat today?

Why? Has tin become a good investment now too? 😜

The substantial drop in savings rate indicates the wealth effect is alive and well.

It’s worth considering what would happen if the current economy wasn’t benefiting from a wealth effect, as well as out-sized deficit spending, both of which are temporary economic drivers that should mean revert.

If the economy seems overly strong, it may be because we are stealing prosperity from the future, which is not responsible stewardship.

There’s no question in my mind that if the stock market dropped even 25%, (and stayed there for a while), we’d end up getting a recession.

Right now, investors believe the Fed put is alive, and investor confidence is supreme that “buy the dip” is an always successful strategy, that there is no reason to save (in their minds).

I’m of the same mind.

It puzzles me that stock market players don’t seem to notice the Fed Put has been withdrawn over in the housing market. That MBS pig-in-the-python on the Fed balance sheet is slowly being digested down to zero, as chronicled by our host. I don’t think it’s a stretch to make the connection to slowly deflating housing prices.

So a bet on a Fed Put under any kind of market in turmoil may not be a sure thing while inflation is still above target after, what, five straight years?

Yes. There was an article somewhere that retail investors keep “buying the dip,” and that Wall Street is now looking to follow them.

Retail investors are the first to panic, but they believe it’ll always work. Right now, the Fed Put doesn’t even have to exist, as long as people believe it does, they’ll act in accordance with it, and we have a self-fulfilling prophecy.

I’ve been saying that for years now. The asset bubble will continue for so long as investors have confidence that there is no real risk. If something happens to shake that confidence, it’s in a lot of trouble.

You keep hearing people telling everyone to just “dollar cost average into solid index funds, as even if there’s a correction, it’ll be higher in 2 years.” Nobody, literally nobody, thinks a prolonged drop is possible.

To have such a huge percentage of the population believing that that risk assets are without risk is really scary.

They look for any excuse. “Don’t fight the Fed” was the big thing when they were printing money but when the Fed started withdrawing it, the narrative changed. I’m mostly out of the market these days but that doesn’t mean I have any confidence as to _when_ there will be a correction.

The market can stay irrational longer than you can stay solvent.

IDK, I’ve heard similar concerns for decades. Maybe we don’t save enough. Maybe deficits are too high. Maybe everything is in a bubble poised for collapse. Maybe not. Maybe banks have been lending to create productive investments and the economy is where it should be. Maybe its somewhere in-between.

Bobber said: “If the economy seems overly strong, it may be because we are stealing prosperity from the future“

Look at the past 50 years.

The result? $38T in debt, and climbing!

They measure household income and realized gains were 39.2 percent as of 2021. That doesn’t count how much were borrowed against unrealized gains and spent.

What evidence do we have that the Fed put no longer exists?

The TACO reaction function certainly exists. So if the TACO can exist why would the Fed be any less active if something happened that suggested a chance of a recession? Heck, the FOMC has already cut rates with inflation above their target and rising. The doves are in command, and only getting more dovish.

Voters asked for growth at any cost. They are getting it. The cost is and will be inflation. That’s OK. It’s the only way to manage the national debt. We just have to be smart, keeping our debts in dollars and our assets in something other than dollars.

“Americans have never been big savers” got me questioning how we stack up against the EU, so naturally I asked my AI overlord:

Using the standard “household/personal saving rate” (saving as a % of disposable income), Europeans are saving a lot more than Americans right now:

United States: the personal saving rate was 3.5% in November 2025.

Euro area (using the Eurostat household saving rate): 15.1% in Q3 2025.

So on this commonly used metric, the euro area is saving ~11–12 percentage points more, which is roughly 4× the U.S. rate at those latest readings.

One important nuance: these series are not perfectly apples-to-apples—Europe’s national-accounts “household saving rate” includes certain pension adjustments in the definition used by OECD/Eurostat-style measures.

Europeans live “smaller” too. Much more sustainable. Just an observation. No judgement but the US is the consumer powerhouse if the World. Stop at any Buc-ee’s and you realize it….

I was at a Buc-ees the other day. Gas was $2.07 a gallon. Cheapest gas I found on the multi day trip. Used their super clean and private restroom facilities. The place has a successful formula that requires volume. But I can’t see how anyone would have a problem with them.

I’ve stopped at a Buc-ees a grand total of one time towing my RV. Never again. The place is a $#@*?+! zoo, for people who act like animals. It’s just a madhouse, with weird humans worshipping a beaver god.

I don’t understand the cult, but I do agree that it probably is a good representative sample of the American consumer and voter, unfortunately.

The official US savings rate excludes realized capital gains. That’s a lot of income for a lot of people.

I love it! RUN…..IT….. HOT!

As everyone and his dog are buying gold and silver bars, I thought maybe this might be in this data, but it does not appear it is under any of these categories. Perhaps it might be included under “personal savings”?

Perhaps just hidden?

Gold, silver, stocks, etc., are assets and buying assets is NOT consumer spending and has zero to do with this data here.

Also, the total value of all gold on existence is only $32 trillion, it about twice what Americans spend each year. So even if somehow Americans were buying 1% of all gold in the world (which would be physically impossible given where it’s being held), it would be a tiny blip on these charts.

Well,with gold over 5000 and silver over a 100 am very happy was a large/in hand stacker……,but,feel these price increases so quickly may mean things I will not like at all,time will tell.

In elastic markets with tiny volumes, small fluctuations can greatly affect the market price, without actually changing much about who owns what.

Is buying jewelry consumer spending or is it buying assets?

Jewelry like real estate are illiquid assets

A 3.5% savings rate ain’t much to begin with and that even includes debt payments. So a guy buys a truck with monster tires for 70k and the monthly payment is considered savings even though the truck will be almost worthless in thirty years? Modern day mathematics I guess…

Most industrialized countries have better savings rates I believe. I should have saved more when I was young.

Twisted hypothetical nonsense. The purchase of the tires is spending, no matter how he pays for it. And after all the spending is done, and he has some income left unspent, that’s savings. The leftover unspent income can be left in a checking account or can be invested or can used to pay down the mortgage or whatever.

Thanks – didn’t think that made sense!

I have a 1985 F-150 built to the hills,that said,only have 25 into it and at moment could easily sell for 30 I believe,but…….,it is NOT for sale!

My Irish pub that I go to regularly is still doing great. It’s hard to get a seat when there is live music. The Drunken sailors are alive and well in Swampland.

It won’t be when its buried in snow later this week!

5:10 PM 1/22/2026

Dow 49,384.01 +306.78 0.63%

S&P 500 6,913.35 +37.73 0.55%

Nasdaq 23,436.02 +211.20 0.91%

VIX 15.64 -1.26 -7.46%

Gold 4,962.70 +49.30 1.00%

Oil 59.66 +0.30 0.51%

MW: Intel’s stock could see its worst post-earnings decline in a year and a half

Exhibit A for why growth companies should never start paying a dividend. The whole culture imploded.

Natural gas futures have soared 70% upwards as the ‘worst storm ever’ is about to affect 230 million Americans which will put a huge damper on going out and spending anything, not to mention heating bills in January.

Here in the South we spent like drunken sailors on disaster supplies. Two days ago we went out looking for a nicer camp stove, and they were all bought up along with the propane.

Sounds like a great opportunity to short?

I have a friend who was a trader at the CBOE. He pursued a degree in meteorology, with the thought that he could make a killing on nat. Gas.

He did not.

It’s a notoriously tough market. Even crude boggles me for the most part: too many geopolitical/ news driven moves.

Our people are living large on 2 trillion federal deficit. Low tax rate for our legal of federal spending equals increase spending in the economy. Bloomberg just had an article “ India sales of treasury deepens, pivots away from dollar assets”. Our time of reckoning is coming, we have been living on borrowed money to keep the consumer machine rolling.

Cheers :)

I should proofread better before I hit send. “Large”federal spending. We are strung out on federal stimulus into the economy without paying the tab. Hangover will be real!

I completely agree. If Americans were paying the same tax rates as their parents and grandparents did, the consumer wouldn’t be so bulletproof. The greatest generation, that won WW2, put the highest marginal tax bracket at 90%(for the Musks and Bezos of the world). Middle class brackets were higher as well. We are all benefiting from and living in a debt bubble.

Thomas Massie Is the only person in DC who consistently cares about the debt. He will face a primary this year due to his constructive criticism and not being afraid of telling the truth. Freedom of speech is on the ropes, retribution is real. Massie is my favorite politician. I hope he stands firm and wins reelection to fight the spending.

Rand Paul has an issue with the debt as well. He also isn’t afraid to call out the MIC. A true statesman. He has been consistent in telling congress that they need to fund the things they want. No new revenues means no new spending.

I live in Massie’s district. Debt is the only thing I agree with him on (well, the only thing that matters, I also like him sticking it to the cult re: Epstein, but that doesn’t matter, it’s just fun to watch).

That said – his seat is safe – my guess is he takes the primary by 25 points.

Are forgiven PPP “loans” considered as transfer payments? Please don’t tell me they count as wages, salaries, tips.

They were transfer payments if given to individuals. They were technically loans, but their “forgiveness” function made them transfer payments.

But many of them were given to companies (LLCs, C-corps, etc.), fairly big ones too, and this here is about consumers, so the PPP loans given to companies would not show up here at all.

The entire economy is grotesquely overheated, and now the socialist President is talking about $2,000 stimmy checks again. Sickening what is going on.

Stimmy checks with our debt is just buying mid-term votes.

Add to this analysis, reported Inflation is close to 3% and has been above 2% for approximately 5 years, Remind me why the Federal Reserve is planning to cut rates ?

Post-COVID transfer payments fell to an elevated baseline versus pre-pandemic. Any idea what that is?

“Americans have never been big savers. Money is there to be spent and keep the economy moving.”

The savings rate was at or above 10% from at least the 60s up until the mid-80s when it begin a steady decline to its current rate.

As the methodology appears unchanged, your statement seems to be more generational bias than empirical truth.

But now people have 401ks, brokerage accounts, and capital gains. Capital gains are not included here. They’re a huge factor in people’s retirement savings. But capital gains are not part of the income here, and are therefore not part of the savings rate.

Inflation is personal. If you spend more on insurance and medical care, you might experience much higher inflation than a guy who spends more on gasoline and electronics.

Party, party, party. HH San Diego.

Largely more boomers on Social Security.

Looks to me like the is plenty of inflation in our future…

Thanks Wolf!

Just wanted to say best of luck to all with the storms,as a New Englander and paranoid prepper am more then ready.

I would also ask if you safely can help those who deserve and need help,for some folks this may be life threatening.

The stores here in the Swamp are price gauging on storm related supplies. I just paid nearly $40 for one 50lb bag of ice remover. They don’t even price their merchandise. I got 4 different quotes for the same item. People here are in full panic mode.

Yeah, we’re spending 25+% more on basically everything from a decade ago – but we are getting less for it than we ever have.

That’s what happens when you get old. You don’t get raises anymore, you don’t get promoted anymore, you don’t get a new job that pays a lot more, etc. Being young has some advantages…

Corollary:

By the time you’ve gotten old you’ve accumulated most of the stuff you “want” and don’t need to buy it a second time at inflated prices. Hence the explosive growth of storage REITs like ExtraSpace, Public Storage, etc.

Well, but then their rental rates go up with inflation…on second thought I guess you really just can’t win.

i put an asterisk on the PCE price index based on this bit from the technical notes in the press release:

Due to a lapse in federal appropriations, the Bureau of Labor Statistics (BLS) could not collect October 2025 consumer price index (CPI) data. To replace the missing CPIs, BEA derived seasonally adjusted price indexes for October using the geometric mean of the September and November CPIs. BEA derived non-seasonally adjusted price indexes by applying seasonal adjustment factors from October 2024 to the imputed seasonally adjusted values for October 2025.

Since the majority of the price changes incorporated into the computation of the PCE price index are sourced from the BLS’s CPI data, the PCE price index data is similarly suspect…

Did you just wake up?

But it has zero impact on pre-October data, and I have gave you long-term charts so you don’t have to put an asterisk on your brain

I contributed to the increase in durable goods spending by blowing $20,000 on a used car.