One thing is clear: a bond market as strung out as Japan’s doesn’t want to hear about spending increases accompanied by tax cuts when inflation is already 3%.

By Wolf Richter for WOLF STREET.

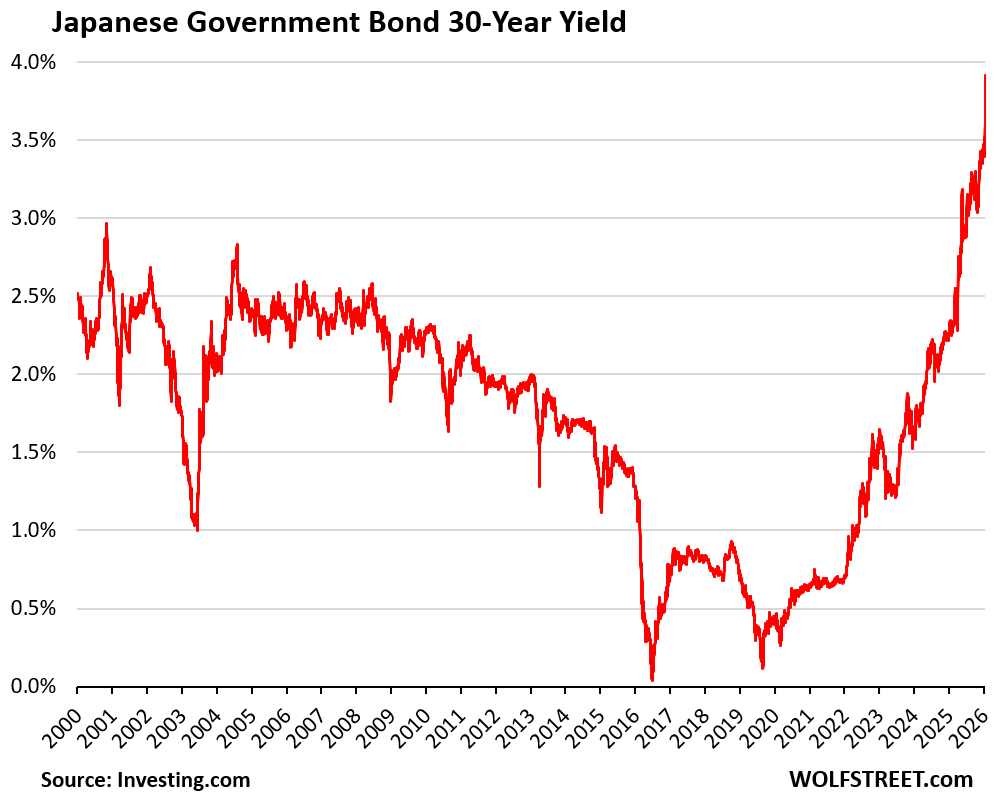

The 30-year yield of Japanese Government Bonds (JGBs) exploded by 30 basis points today and by 42 basis points over the past two days, to 3.91%, the highest since the 30-year bond was introduced in 1999, after Prime Minister Sanae Takaichi called for increased government spending with simultaneous tax cuts by pausing the 8% consumption tax on food purchases. And she announced snap elections — three months after taking office — to get the public support her party needs to push those plans through parliament.

Inflation in Japan has been around 3%. Japan’s debt-to-GDP ratio is the worst in the world, at 256% at the end of the last fiscal year, more than double what it is in the US. Japan’s credit rating by Fitch (‘A’) is five notches below ‘AAA’ while S&P’s rating (‘A+’) and Moody’s rating (‘A1’) are four notches below ‘AAA’ (my cheat sheet of bond credit ratings by rating agency).

And the bond market – what’s left of it since the Bank of Japan still holds more than half of all JGBs outstanding though it is now shedding JGBs – is getting a wee bit nervous.

Maybe the dreaded “bond vigilantes” – big institutional investors that refuse to buy government bonds because risks are too high and yields too low – are rising from their graves? Nah?

But apparently, hedge funds got caught on the wrong foot and were turned into forced sellers, and it was a mess.

Another trigger today was the 20-year JGB auction, which was marred by weak demand, not surprisingly. And in the secondary market, the 20-year yield spiked by 22 basis points today, and by 32 basis points in two days, to 3.48%, the highest since 1996.

The crucial 10-year JGB yield rose by 7 basis points today and by 8 basis points on Monday, to 2.33%, the highest since 1999.

And yet, the 10-year JGB yield is still way below the rate of inflation (around 3.0%), when it should be significantly higher than the rate of inflation. So at those still too-low yields, those JGBs are still extremely unappetizing, and the fact that there are buyers at those yields at all is another sign that the bond vigilantes may still be dead.

Japanese government officials fanned out to calm down the markets, and even Bessent got in touch with Japan’s finance minister to discuss the situation, as Treasury yields in the US were also being roiled. So whatever.

But one thing is clear, a bond market as strung out as Japan’s doesn’t want to hear about spending increases accompanied by tax cuts when inflation is already at 3%.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Interesting. Also interesting: the real (inflation adjusted) yields have been negative since 2013, though for much of that they were between 0 and -1. They’ve only been drastically negative since 2021.

Still, by some combination of inflation and yield increase they will most likely revert to the 1-3% level they traditionally hold.

I was in Japan a year ago. Prices (at the then exchange rate for the dollar) for very high-end food in the Ginza department store markets were very low. These stores charge the highest prices. I could buy a large sashimi platter for about $12! If the equivalent was even available in the US, it would be closer to $75-$100. A friend of mine in Japan has stopped all international vacation travel because of the unfavorable exchange rates.

Japanese people have gone from having high 1st world global purchasing power to low to mid 2nd world over the last 35 years it’s wild that people have stood for it.

I really doubt that the quality of sushi in the is anywhere near that of the sushi in Ginza.

@Bondy The Big-Name Department Store charges the Yuppie Price, same as here.

Imagine a large Sushi Platter at Needless Markup in San Francisco: That is the relevant comparison.

What this really sheds the light upon is how truly manipulated the yield on U.S. Treasury debt is by way of the Federal Reserve and its puppet master, Wall Street.

The Japanese market is reacting in a rationale free market manner. We should be so fortunate.

This is literally nonsensical. Wolf points out below that the Japanese Central Bank owns more JGB than the Fed owns Treasuries.

The spillover in the US Bond market is rather sharp. Isn’t it also rumors of a Denmark fund and the EU threatening to sell US Bonds?

“The Danish pension fund AkademikerPension, which said it will exit the market by the end of the month, holds only about $100 million of Treasuries. Still, its statement revived concerns about the financial consequences of US antagonism toward allies. Trump over the weekend escalated his pursuit of American control of Greenland, an autonomous part of the Kingdom of Denmark, threatening opponents with tariffs and even hinting at possible military action.”

Just my opinion, but when countries start seizing other countries financial assets, then the ripple effects can become quite deadly. The agreed upon world order is cracked. Repairs need to be made before the cracks worsen.

There may be some people reading this site that could sell more than $100 million in Treasuries. The Treasury market, the most gigantic bond market in the world, doesn’t even notice a portfolio of that size getting unwound.

I agree on the $100m. So is it perception? or?? The yield spike began on Friday but the Ten Year bond has been price consolidating for 5 weeks before exploding higher. The volatility spike is not normal. Why would dumping Japanese bonds spillover into dumping US bonds? Logically, it would cause a flight to safety in US Bonds.

It’s unusual, but it’s a known response to news of a potential catastrophe or crisis (specifically a supply shock in which supply of his and services becomes limited). People pull out of stocks because they expect the economy to struggle and they pull out of bonds because they expect inflation due to scarce goods (and thus increasing interest rates).

The “yield spike” aka the Bond Bear, began in 2020!!!

This is because: 0.333% (on the chart) on a 10-year bond is absolutely nonsensical!

Granted, the Japanese are well-conditioned to paying their government to spend their money.

Also the US 10-yr has kindly been dubbed as the “return free risk” by Grants interest rate observer.

The 10-yr yield is still widely considered as “the most important interest rate in the world.”

The MSM has convinced us, along with the Street to call Bear or Bull daily. History is showing us a massive tide change in the financial seas.

A secular bear market in bonds has begun. The bull run lasted 40 years. I’m not confident that the powers that be can do much to stop it?

I think Bessent doesn’t speak for all Americans when he follows with “…like Denmark itself, is irrelevant” These words will eventually come back to hurt us.

A single small pension fund may not matter, it’s a sign of the times though. I just read an article in a German newspaper (one that usually has a staunch transatlantic bias) about German central bank gold repatriation. In the past, people who were calling for it were framed as lunatics, now the article’s logic goes: ‘Maybe it makes sense but now is a bad time to do it, or it may create further tensions’. Fear of being exposed to US financial retribution is definitely shifting from BRICS countries to classical US allies. And this will have effects on treasury yields.

Hi Wolf, when do you plan on releasing your next installment on “The Foreign Investors Who Bought the Recklessly Ballooning US Treasury Debt and Why They’re so Important?”

Your last publication was mid-September 2025, and before that was mid-July. I and other readers would love an update, especially with all the geopolitical changes and increasing Japanese bond yields. Thanks again for all you do!

In November (data released last week), foreign holdings jumped to a new record of $9.36 trillion

But there is this issue with the Treasuries held by US hedge funds domiciled in the Cayman Islands that are apparently not getting picked up by the Treasury Department’s Treasury International Capital data, which considers those Treasuries held in the US. So holdings in the Cayman Islands by US hedge funds (for the basis trade) could be understated by $1 trillion, according to a study by researchers of the Federal Reserve last October. The Treasury Department has not yet changed the tracking of those Treasuries in its TIC data. I was hoping to see this addressed, before I post it again. That said, this has no impact on holdings of other foreign countries. But it does impact US holdings by institutional investors, which is where that $1 trillion is now accounted for.

If the Treasuries held by the Cayman-domiciled US hedge funds are accounted for properly, foreign holdings would jump to $10.4 trillion.

Sorry – I have a very thick skull. So is it:

1) the case that the Treasuries held by hedge funds in the Cayman Islands have historically been considered foreign ownership?

2) the case that the Treasuries held by hedge funds in the Cayman Islands have historically been considered US-entity (i.e., domestic) ownership?

Looks like this is a fun rabbit hole to go down.

Treasuries held in other financial centers, such as in Belgium (Euroclear), Luxembourg, the UK (City of London), Ireland, etc. have the same issue, as I point out in every one of these articles: these Treasuries might be held by US companies or hedge funds with mailbox entities in these financial centers. For example, a Senate investigation into Apple over a decade ago made this very clear that Apple was holding a big chunk of Treasuries and other assets in mailbox entities in Ireland to store its foreign profits there to avoid having to pay US income taxes on them, but instead pays Ireland’s low corporate tax rate.

Cracks have been here for decades and ignored. I don’t sense there will be a winner take all situation but the Cross-Border Interbank Payment System (CIPS) and other initiatives create more balance. No ability for the US to use the ownership of financial systems to enforce sanctions and project geopolitical power. That and systems like Swift are so dated as to be comical.

If the US is willing, which I don’t think it is, it could easily help facilitate a new world order but hard ask when you have dominated for 80 years.

An additional worry is that the US is putting the Formosa Straights on the back burner thus relegating the Pacific Theater to the back of the bus while we concentrate on America first giving more of a free hand to China. This puts Japan in a very difficult position.

Isn’t Japan’s 256% debt level a bit illusory? If half is owned by the central bank, hasn’t that half been monetized and extinguished from a practical standpoint? There is no way the central bank will sell that debt back into markets.

1. It’s being de-monetized through QT.

2. Sure, you could say that the debt doesn’t exist because the BOJ holds it, and in terms of interest expense that’s kind of true since the BOJ remits its income back to the government. And that’s exactly the same for the Fed.

https://wolfstreet.com/2026/01/06/bank-of-japans-qt-cuts-502-billion-from-balance-sheet-jgb-yields-surge-as-boj-steps-away-from-bond-market/

Doesn’t help that Japan clearly aligned with the US versus China. Not like they were ever on great terms, for very valid historical reasons, but Japan had the opportunity to build a relationship with Beijing and went the opposite direction. South Korea took a more pragmatic approach.

I don’t disagree, but very different strategic situations. South Korea has North Korea as its primary military threat, while China could attack via land, sea, and air, probably in concert with North Korea. Choices are to rely solely on US deterrence (US troops as firewall, US Navy and nuclear capabilities) or make friendly to some extent with China while hoping US will at least talk tough. Almost no chance the US engages in a land war on the peninsula. Even if China decapitated Japan, taking and keeping control of Japan would be far more difficult, and even the attempt would torpedo the global economy. Great for revenge, but sayonara to the export economy. Russia ain’t making up for lost US and EU markets.

Exciting to finally see some solid movement in the last year(ish) on these long rates after such an unreal low rate period.

Hopefully inflation in Japan has now become ingrained and self reinforcing such that only a recession or high interest rates can break it. That should provide the fuel needed to get the 10y above 3% and bring some overdue fireworks to the global markets.

Are the US treasuries held by “Japan” all held by the BOJ or does that include those held by Mrs Watanabi? If not, I wonder what the total holdings of Japanese interests are and at what point might the holdings be unwound in favour of JPY debt?

So will this continue to make the basis trade less desirable? Would that negatively affect equities in the rest of the world? Or do we have a ways to go before that?

Yes, yes, and no.

I asked Gemini this morning if it could tell me what has happened in recent weeks to the spot-futures basis on 30-year JGBs.

Gemini said the basis had widened 45 basis points between Year End 2025 to Jan 20, due to a “Liquidity Vacuum in Spot [JGB] Bonds.”

In general Gemini’s info struck me as pretty good, warrantably plausible. Perplexity had nothing to say on this topic & so far, neither has the mainstream media.

But I’m baffled as to why the JGB basis would have widened instead of tightened. That doesn’t make sense to me, unless one imagines seeing replays of Autumn 2008-type events, which I’m not imagining.

Some are “official” holders and some are private holders.

Nice to see Japanese Bonds returning towards normal and reasonable yields after a 30 year hiatus.

Donnie’s working hard to Make America GRATE again!!!

U.S. 10 Year Treasury US10Y

Yield | 4:16 PM EST

4.293% up +0.062

Giving someone your money for 10 years and receiving 4 percent and change seems silly, especially when inflation is eating up some amount of your return.

I think we need to look at our system, something is not right??

Yes, these yields are too low.

But the huge factor you excluded is zero risk to your principal when you hold to maturity. That’s not offered by other investment choices. Your stocks and cryptos might lose 100%, PMs have a history of crashing, as does RE.

The average 10 year yield for the last 100 years is 4.7%, so these rates are totally normal. Average inflation over that same time period is 3%. So the average real 10 year yield is 1.7%. The current real yield is about 1.5%.

Should we be above average right now? That’s a tougher question, but we’re right at historical averages.

Also, inflation adjusted total return for 10 year Treasuries averages 1.8% over the last century. This varies considerably. It averaged +5% between 1980 and 2020, but -2% from 1940 to 1980.

What is the interest expense on government bonds to receipts ratio for the Japanese government? Where would it be at 3% blended rate of interest on outstanding securities?

Current blended rate is less than 1% and even that is 24% of revenue. A doubling would take it to 50%. That’s when it gets serious.

I was just talking about the bond vigilantes as a possible scenario (albeit in America) on this site the other day. I don’t think we’re there yet. But this could definitely be an ominous sign of things to come.

US is still one of the cleanest shirts in the dirty laundry. That matters. But it can change quickly with our current leadership antics and actions.

3.91% on a 30 year bond? You wake up 30 years later and realize you were a chump – taken to the cleaners. Sadly, many of these ‘chumps’ aren’t individuals, but pension funds. And what is left after 30 years is taxed for a double whammy!

Maybe it’s worth looking at this as a FX investment with yield. It may look rather shrewd in the years ahead. That’s not my opinion necessarily, it’s simply a perspective to consider.

The same logic applies to USTs, depending on where you are in the world.

Pretend and extend for the sovereign debt ends soon. No more free lunches!!!. Here in the USA; Bond vigilantes will square off with “My morality is my only check on my power”. Who will lose? Hint… the whole world. How much sovereign debt did the USA purchase from China and Russia? That answer may determine how much future debt the ROW will purchase from USA. Who will win.,..Russia! Shorting JGB was called the widow trade for decades. The times are a changing!

Widow “maker” trade. As we get older we naturally have grey matter shrinkage and cerebral uptake change , it’s just normal Physiology. :) :):)

Like walking through the proverbial bond mine field. You don’t know where they’re at until you step on them, then you actually find it but its too late…

It looks like the smart money these days is buying gold. Thats saying a lot because gold doesn’t even pay any interest. Go figure. Perhaps interest rates must rise in order to get funded these days.

Gold is like cash.

Loan your gold to someone and you’ll earn interest.

ok so no vigilante skeletons popping up out of their graves but those long term yield charts are pretty scary. maybe dig a few more graves just in case.

I remember when Japan increased the consumption tax to 10%. It was politically unpopular and even though JGB yields were close to 0%, it was necessary to reign in government debt. It was a hard fought victory.

Now, Sanae Takaichi threatens to undo all the good work at the worst possible time. JGB yields are spiking and the fiscal situation is worse than ever.

Sanae Takaichi’s stance on immigration and China play well at home but will exacerbate Japan’s problems. Japan has elected a populist leader and it’s not going to end well.

As the saying goes, especially when it comes to purchasing bonds; “Full FAITH and Credit”…

I know that many of us were in “T-bill and chill” mode when the “market” was going sideways and the short of the curve was paying 5% or more, but the fact of the matter is that risk (faith) is being repriced globally. We are going back to a mercantilist world. The producers will make the rules again. Interesting times, gold passing $4,800 this morning… yikes….. 3% inflation? Yeah, we (america) should be so lucky.

Doesn’t Scott Bessent seem like he is taking over as the guy at every accident or calamity that is shouting “nothing happened, nothing to see here!”

That’s his job. #1 item on his job description. #2 item is selling bonds at the lowest cost possible. Those two go together.

I was thinking more if the sheriff in Blazing Saddles and the scene where he hold himself hostage. Maybe that’s just the vibe the Japanese bond market is sending…

The first domino to fall? When good and services stop crossing borders, troops will…

I wonder who has more troops?

Same as it ever was.

Ha, ha. Yes I can see him saying in an interview “excuse me while I whip this out.” Love to see him when the sit hits the fan.

The classical technical setup would be for the willshire 5000 to retest old resistance of 68912 and than sell sell sell, take out yesterday low than panic selling lower. Almost there on the upside or it may of ran out of gas right before or a tad higher on willshire 5000. Will find out shortly.

The European are great at the charts. When Mario Dragh announced whatever it takes bazooka it was at the exact moment the charts were breaking, than just like that everything was awesome. American retail investors just got fooled, the European are selling into their greed, pulled the rug on them. Perfectly timed. Todays rally is over!!! Sell before the crash

You can see the insider trading before the Trumps announcement of no tariffs. Blatant

Yeah, I was on a plane in April, in a short position and missed the “liberation” of a good time to buy stocks post by Mr. Truth social himself.

I am (struggling?) learning the danger of trying to short anything that is marketed by the bubble machine.

Shorting is dangerous business for your wealth, trailing stop loss is always advised and never meet a margin call, just fold your hand is my only wisdom to share. Speaking of margin calls, maybe they will be coming into season next week.

68.1t on the willshire if it breaches than large volume will sell. Bessent crew knew what would have happen yesterday if the Tarrifs were not called off, we were heading for a large drop….Willshire is still red for the week, $tnx is trending up on the weekly charts too. I was fool to have said sell before support was taken out 68.1t on willshire. Too much chutzpah!!! I am not trading I am just watching. Thanks

Greenland is all about the trillion in rare earth minerals absolutely nothing about defense. This pause will be thin. Venezuela wasn’t about drug trade it was about selling their Oil and taking a haircut of the oil money to put into a Quatar bank account. We are using an off shore bank account for the oil revenue that we took by force. Who is benefiting?