The expected rate cut gets complicated: A dovish Fed amid rising inflation can spook the bond market.

By Wolf Richter for WOLF STREET.

The Treasury market – and the mortgage market with it – has gotten a little ruffled since the tranquility of Thanksgiving week ended, despite the widespread assumption that the Fed will deliver another rate cut this week.

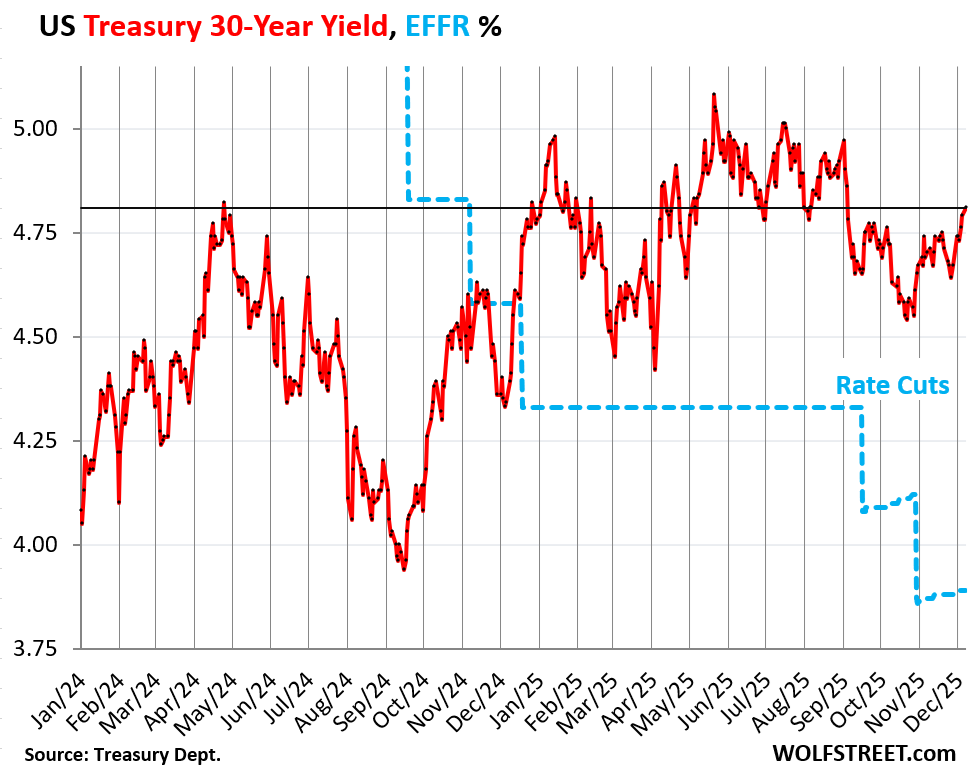

The 30-year Treasury yield has risen by 17 basis points since the day before Thanksgiving, including 2 basis points today, to 4.81%, the highest since September 4. Since the rate cut in October, the 30-year yield has risen by 26 basis points. Since the first rate cut in September last year, it has risen by 87 basis points.

The Effective Federal Funds Rate (EFFR, dotted blue line in the chart), an unsecured overnight rate at which banks lend to each other, and which the Fed targets with its monetary policy rates, has been drifting up ever so slightly after each rate cut, starting in September, amid tighter liquidity in the money markets, including bouts of turmoil in the repo market. And the 30-year Treasury yield is just ignoring the EFFR.

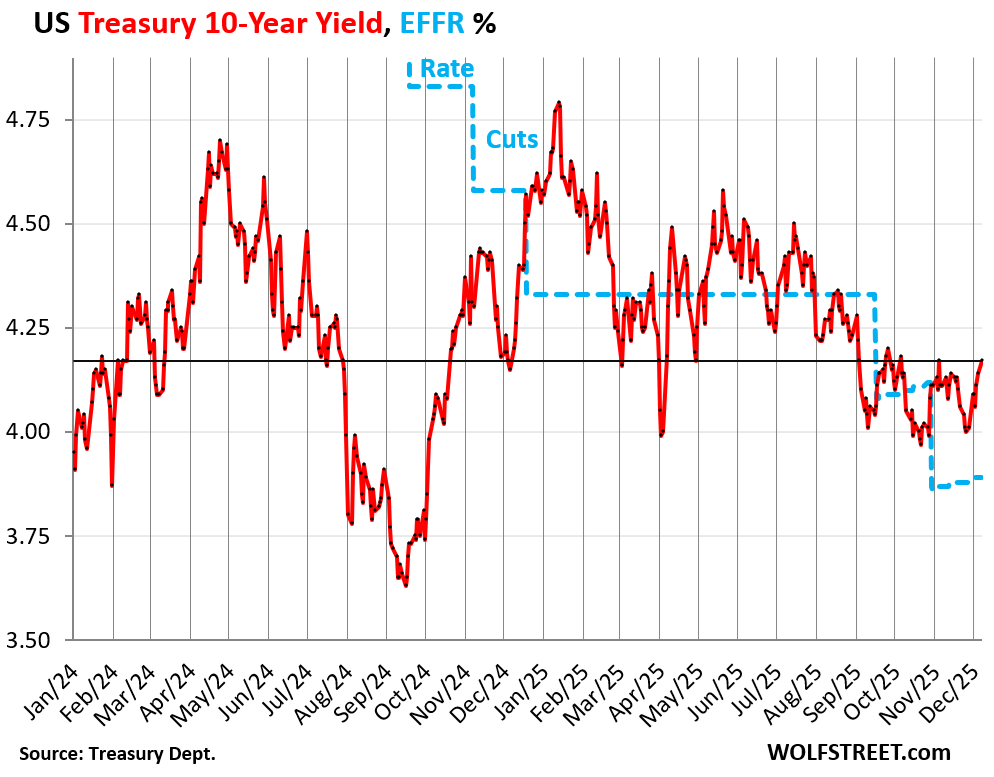

The 10-year Treasury yield briefly jumped nearly 6 basis points this morning to 4.195%, just a hair from 4.20%, but then edged back and closed at 4.17%, up by 3 basis points from Friday, and up by 17 basis points from the day before Thanksgiving, and the highest close since November 5 (also 4.17%), and both had been the highest since October 6.

Since the October rate cut, the 10-year Treasury yield has risen by 18 basis points. Since the first rate cut in September 2024, it has risen by 54 basis points.

The Fed’s short-term policy rates and hopes for rate cuts have only limited impact on the long end of the bond market, where yields are largely driven by fears of future inflation and fears of an onslaught of new supply of Treasuries that the market has to absorb by pulling in more investors, potentially with more attractive, thereby higher, yields — meaning lower prices for existing bondholders.

The inflation scenario is made worse if the market sees prospects of a lax Fed in face of inflation.

The Fed, at its interest-rate decision on Wednesday, will have to make do without much of the current data that is still tangled up in the after-effects of the government shutdown, including inflation and labor market data.

Markets now expect a “hawkish cut,” with several dissents and a hawkish tone of the “dot plot” depicting participants’ projections for rates, inflation, unemployment, and economic growth. The Fed may also provide more details on its balance sheet.

In addition, the market has to digest six Treasury bill auctions this week, two Treasury note auctions (3-year and 10-year Treasury notes) and the 30-year Treasury bond auction.

Today was already busy with three auctions, totaling $228 billion, including $90 billion of 3-month T-bills and $80 billion of 6-month T-bills, both pricing in a rate cut this week.

At the 3-year auction this morning, $58 billion of Treasury notes were sold at a yield of 3.614%. In the secondary market, the 3-year yields rose to 3.62%, the highest since November 5.

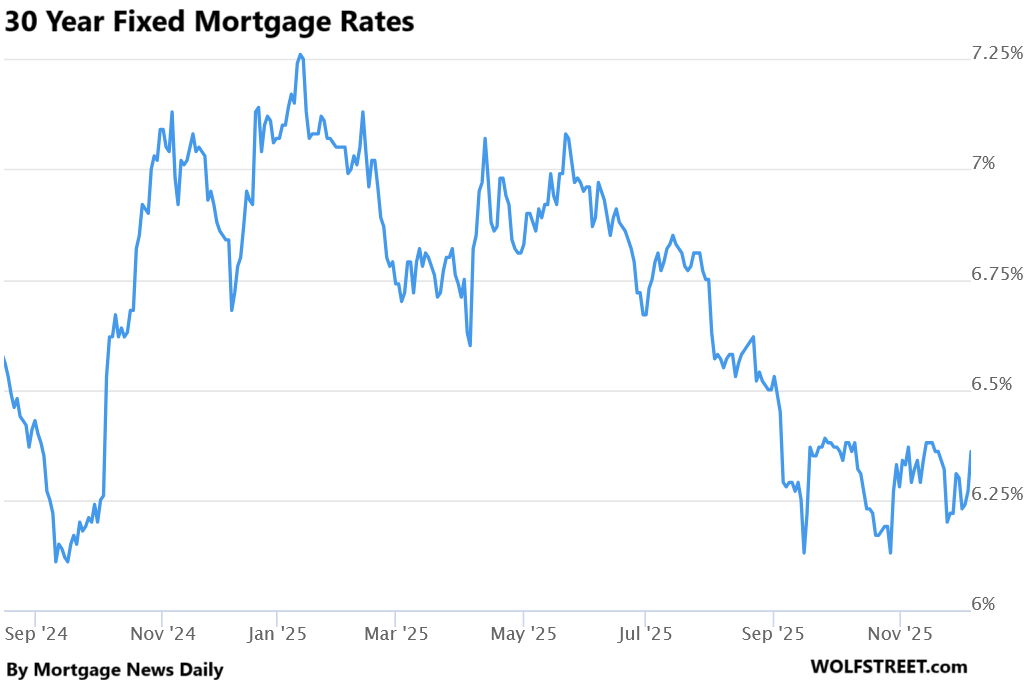

Mortgage rates got pushed up by rising long-term Treasury yields. The daily measure of the average 30-year fixed mortgage rate by Mortgage News Daily jumped by 9 basis points today, to 6.36%, the highest since November 20.

The average life of a 30-year mortgage is less than 10 years as mortgages get paid off prematurely via refis and sales of mortgaged homes. And so the mortgage market roughly tracks the 10-year Treasury yield, with mortgage rates being somewhat higher, and this spread varies over time.

Before the first rate cut in September 2024, the average 30-year mortgage rate had dropped to 6.11%. Rate cuts by the Fed do not mechanically translate into lower 30-year fixed mortgage rates. Mortgage rates are a function of the bond market.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The long bond market is starting to price in Trump’s replacement for Powell. This will be somebody who will kiss Trump’s heinie, and lower short term rates as quickly as possible, thus spurring inflation. I would be very nervous if I was buying long-term Treasuries (10, 20, 30 years).

If you go to the dictionary and look up the word sycophant

an ever smiling Kevin Hassett looks back at you.

I would be happy to join Kevin Hassett and drop interest rates 2%, and I am not a sycophant for anybody.

So… You want short-term rates below the inflation rate? You want negative real rates on your savings? You want to stoke inflation even more? You want a possible repeat of Tall Paul’s shift to 20% interest rates in order to eventually correct it?

I just see the market pricing in over sized govt debt going exponential

just $1 Trillion(fake printed money) for interest we can’t afford

gotta remember to also thank biden for $10T or so

and inflation thanks to his Inflation Production Act

Government debt has exploded and there isn’t a plan amongst both parties to fix it.

MS,

You want hyperinflation?

We have too much liquidity.

End the fed

Biden didn’t create the inflation. It’s primarily the result of things done to contain the GFC to manageable proportions and to prevent economic collapse during the Pandemic.

Those were both necessary actions by Gov and Fed, but not without cost, as we’re seeing today.

Maybe handling during the GFC was necessary, but they should’ve broken up any bank or business deemed Too Big To Fail while they could in the fat times, just for better market resiliency. Antifragility and all that.

A concept that the bond market is appropriately priced is absurd in the current environment of excess liquidity. Currently, the most under priced asset class is long term debt. I know, the 10 year, which has been squashed in it’s role as a totem of financial health, has been trending up.

The people who buy U.S. Treasuries have money to burn. Let’s not worry to much for them.

May be true for SOME folx who buy US treasuries MS, but definitely NOT true for others who have worked and earned and saved and now NEED some safe place for their savings.

Try to get out of your personal bubble and take a hard look at the majority of working people.

Yes, we keep our emergency fund in a t-bill ladder that has part of it rolling over at least once a week. MS is out of touch.

If you have a money-market fund for your “6-12 months of emergency savings”, you own U.S. Treasuries. (And are getting a better yield than a bank account, too.)

If your 401K is invested in a target-date fund or a bond index, you own U.S. Treasuries.

If you have a pension, it owns U.S. Treasuries on your behalf.

If you are drawing Social Security, or expect to, it has something like $7,000,000,000,000 (7 trillion) in Treasuries in a “trust fund” buffer, without which you (and millions of others) would not be getting as much from Social Security.

If you have house or car insurance, your insurance company has invested some of your premiums in U.S. Treasuries, as part of their financial reserves.

Treasuries are much, much more widespread than you might think. After all, there are $38 trillion of them!

I hate insurance…

It is a mandated legalized scam.

You make an agreement to pay, and they make an agreement to do everything in their power not to honor the agreement that was settled upon…

and the government backs them, because of lobbies and subsidies and such.

Junk… I pay bare legal minimum.

Who would one buy a 3 yr at 3.6?

Reminds me of those buying ten yrs at .5%

Every signal from free market action says the Fed should NOT cut.

Long end is wobbly and the SOFR in which there is a scrambling for money over 4% all say rates are NOT restrictive but attractive.

Add in stocks all time highs, prices all time highs for metals and cost of living. Inflation over the “target” for 4 years.

If you cut now, when do you raise rates?

What’s also interesting is that Trump’s economic approval among the people is in the toilet. Goes to show that for Trump as with Biden, the American people, as a whole, don’t care about stock prices.

But if you let the financial media dictate your view, you’d think that’s all that mattered.

It’s the toilet among Democrats. It’s still fairly high among the GOP.

It’s low among independents; that’s really what’s hurting him right now. The red and blue pom pom crowd just thermostatically flip sides like clockwork. Independents are who to watch.

What’s interesting is the fact that we *just* did this with the covid inflation and the “most reckless Fed ever”, and people were pissed. Trump comes in, wins the election, and says, “Let’s do that again!”

I knew this administration was going to be a disaster, but just about every facet of it has ended up turning into some kind of bizarre lose-lose situation. You have all the power in the world and this is what you come up with? Truly, the dumbest timeline.

The Oligarchs run the show now. They are all well positioned to take advantage of the coming collapse.

Well the real joke about free market economics is “assume a free market” which is exactly what my Dad, shop steward for the teamsters, argued.

That the wealth and health of this paradise relies on the most fragile human attribute, love.

It makes everything so much easier when you wave away the real complexities. It’s like playing blackjack and calculating the odds of your next play by assuming all 52 cards are equally possible to come next off the top of the deck.

Long-term money flows, the volume and velocity of money, could fall by 50 percent between now and April 2026. But that’s only likely if the FED doesn’t cut rates.

The FED should cut rates because short-term money flows are falling. However, this analysis is ephemeral as it hasn’t been back tested. It’s based on theory.

The 10 year bond should be at 10-20 percent. This would cause a recession, but then inflation would stop and prices might decline. Great, but jobs for poor college kids and the rest of us would be scarce and even scarcer because of AI. So which way does the FED go? I think for jobs. The hell with inflation, buy gold and silver and stay out of bonds.

Seems like gold and silver have been working pretty good for quite awhile…and may continue with cuts and inflation and such.

Question like all other investments, is when to sell. Buy low sell high ?

Jakob Fugger: “invest 25% each in stocks, bonds, gold, and land…expect to lose money in at least one at any point in time…. Rebalance periodically to keep the 4 equal.”

That…and some other stuff…worked pretty good for him.

But…Anyone that says they know for sure is full of…! Just educated guesses, and risk vs gain assessments. If it all goes, we all hosed.

The difference between stocks and bonds VS gold and land: you can hang on to the gold and land forever and valuation be damned.

The metal is a chaos hedge (and arguable store of value). The land has potential to fulfill most or all of a person’s basic needs (though water can be tricky, and food doesn’t grow itself).

I am looking for a viable agricultural plot (oh, and the money to obtain the “ownership”).

The concept of “This would cause a recession” is worthy of being intellectually dissected, in search of the truth.

I think that financial machinations to forestall the onset of a recession is the world that I live in. Nameless Harvard grads cashing in on the America that my Dad’s being shot in the face by a German sniper while driving a tank destroyer in coordination with Patton’s army.

That’s the way the Fed has gone for the last 30 -60 years, so that seems like a good bet, especially with Trump in the White House.

I figure if the 30yr hits 6% I can load up the truck and retire a few years earlier. Hopefully that’s not a dumb decision….

What do you think are the chances that inflation will kick-in bigly in the next few years ?

I agree. Six percent is the point where the federal government wakes up and says to itself

We call ourselves Republicans but we act as supplicants to an authoritarian form of government.

Let’s increase the marginal rate on the mega billionaires, the real free riders.

This assumes they give a hoot. Looking at the budget deficit and national debt ballooning whether Team Blue or Team Red is in office, I’m guessing they don’t do anything until it all blows up in their face.

the 30yr went to 15% in 1981

careful

I profess to know little about economics but I do know that in December of 1979 I bought a three year old, 1200 sq ft 2br 2ba single family stick built home in Ocala Florida for $42,500 with 10% down and a mortgage at 14.9% for 30 years. I think the piti with pmi was right at $550/mo. Sold it the first chance I got. The Zestimate today from Zillow shows the house at $230,000. In today’s society, I would not live in that neighborhood.

Nice to see that long-term yields and mortgage rates are rising just as expected they would.

OK but I think the long term rates are at least 25 pct too low and should be at least 5.1 pct. Because I think that monetary policy has been shit from the perspective of the working family. A category that determines presidential elections..

America is a beloved country that is jaundiced by the institutionalized corruption

DJT wants the market up for the midterms…..

but to your point, the working family that has little to no stock and expects the powers to guard the nation’s currency are the ones being harmed. These people are not on anybody’s radar, sadly.

Money earned, then saved, should not be a losing proposition….for those pushing for rates at or below the inflation rate. ( the poster pushing for 2% Fed Funds)

MW: Mortgage rates are surging ahead of the Fed’s expected rate cut. What gives?

We only have Sept. price data. Nov. should be the peak.

Not sure what prevents the Fed from mostly issuing short term and thus keeping it fairly low. Seems there are even people willing to buy longer term low rates considering more inflation is possible. I suppose I would do 10 year at 5% but that doesn’t seem like it will be happening.

Sets up a bit of a challenge of what to do with the money I have had in short term bills that will barely outpace inflation. Perhaps this is no longer the goal. Feels like bond markets will simply be unpredictable for foreseeable future.

Perhaps time to jump back into real estate!

The Fed doesn’t issue bills. The treasury does. The Fed can directly or indirectly influence the supply sometimes, but what is issued is entirely up to Treasury.

The problem with issuing mostly short term bills is that if inflation surges and investors demand higher yields, you don’t have any long term ones to rely on for a while, but you have to roll over that much more debt at those higher rates.

The FED has destroyed the borrow short, to lend long, savings/investment process. Now there is substantial substitutability of short vs. long term financing.

Real estate is way overpriced in the majority of markets. It’s hard for many to sell something when they think it’s worth more than it actually is. I think we need even tighter liquidity to stop funding dead weight and rebalance asset prices.

Well Glen I think it may be an awful time to jump back into real estate a category that is about to collapse, perhaps

The government is the decider

Ah, Great Expectations. Powell must know it would be foolish to cut rates now. The question is whether he can browbeat the majority of the committee into standing firm.

“Easing into an existing bubble…”

Nonfinancial corporate debt explosion, JGB yields, and the Chinese non-US export surplus seem to be the leading drivers of the recent global bond market volatility.

The best way to have investment and growth and full employment long term is with stable prices.

For now we are stuck in the boom bust inflation cycle.

A Fed chief with some credibility would not cut interest rates right now. A significant cut now will cause the 30 year long term bond market to crash and rise to over 5% and the 10 year note to go to 4.5% or higher. The housing market which is already in a recession will go into a depression. See if I am wrong.

To get a rate cut, 7 out of 12 FOMC members must vote for a rate cut. Powell is only one of the 12 votes. But he can try to schmooze, cajole, and persuade to build a majority.

The recent dissenting votes are an interesting phenomenon. I was reading a blurb by John Mauldin the other day that said the Fed’s unanimous rate votes are an artifact of the Greenspan era, and it might be better to have a more mixed vote which will give the market a better idea of Fed policy direction and what the voting members’ opinions really are, and where they think rates should be.

Doesn’t the Dot Plot achieve this?

Not saying you’re wrong, but the WSJ says regarding rate cut…

“…But the final call rests with

Chair Jerome Powell,..”

WSJ 12/10/2025

Is the FOMC just advisory to the Chairman, or is the WSJ wrong?

Just one more piece of bullshit in the WSJ. The WSJ is full of it.

Why anyone in their right mind would buy 10 year plus US debt at these low interest rates when the repayment of US 38 trillion is impossible and will either be defaulted on or defaulted away through inflation.

The Fed can lower rates to zero but bond rates will keep rising as foreigners off load treasuries and buy gold

This year I purchased a decent amount of 10yr. Why?

Returns on CDs and high yield savings are dropping and there’s state income tax on the interest, stock market is a casino, crypto is fraud, real estate is a mess, where exactly am I supposed to park my cash when I’m trying to retire in 8-13 years?

In private-sector bonds, “repayment” occurs through issuance of new bonds, such as Apple’s bonds. They’re not repaid from cash flow. They’re repaid by Apple issuing new bonds. Same with government bonds.

There are only two kinds of capital: equity capital and debt capital. Equity capital is permanent. At least part of debt capital is treated as de-facto permanent by rolling it over (issuing new bonds to repay maturing bonds).

There are real and big issues with the US government debt trajectory. But “repayment” of debt isn’t one of them. This notion of “repaying” or “paying off” the US national debt is just silly.

The thing you need to focus on is the sustainability of this debt. So in the government’s case, you need to keep your eyes on the ratios of interest payments to tax receipts and debt to GDP:

https://wolfstreet.com/2025/08/28/us-governments-fiscal-mess-interest-payments-on-the-treasury-debt-interest-rates-tax-receipts-and-debt-to-gdp-ratio-q2-2025/

Wise words,

Thanks

Thanks. Whaty the heck happened in ~ 1985 and 1992?!

The effects of Reagan’s tax cuts were kicking it, on top of a military spending spree, which caused the debt to balloon, on top of much higher interest rates that were filtering into the US debt as old lower-interest rate debt matured and was replaced by higher interest-rate debt. Plus some other factors. Those were iffy times.

Risk (trust) is being repriced globally. The faster the Fed lowers short term rates, the faster interest rates on bonds and interest rates in the real world will rise

Hyperstagflation in a country with 38+ trillion in debt.

Interesting times.

The Fed and the Federal Government are to blame in my mind for the huge amount of spending, but they are not the sole culprits in our inflation problem.

Inelastic supply and rising demand are seen in housing and medical costs. More people same number of homes and doctors.

The same is true for many other services, such as plumbing, excavating, etc.

For so long, high schools told Johnny to get a degree in political science and avoid trade school.

We now have a shortage of service providers in many areas.

Yes. The laws of physics and Nature (demographics) win. Almost 80% of equities and housing equity held by the aging boomers, many of whom built service businesses. Many of their children got rich as part of the great “financialization” and refuse to pay taxes or support the aging system that made them so wealthy. The irony all this and ignorance of this younger generation will be their undoing.

The same people that carried around pocket constitutions are now okay with one man implementing taxes/tariffs. This is in fact taxation without representation. One has to laugh. The rest of the world certainly is.

Hedge accordingly.

The Federal Reserve has nothing whatsoever to do with excessive federal government spending and has told Congress over and over to get its fiscal spending in line with its income via taxes.

The fed enabled the govt to go way overboard with debt and deficit spending by *buying* the debt with money printing. If the fed wouldnt have done QE, the higher rates that would result from less dollars being available to buy the debt would be a deterrant to govt overspending.

1234

You are correct. The Fed sheltered the Federal Govt from the discipline of the free market……one in which more supply depresses prices (higher yields). The Fed absorbed, at one point nearly $9 Trillion of debt from market forces.

Imagine, So Cal, if that debt had been looking for a home out in the market place? Where would rates have gone and what impact on deficit spending would it have had?

Now the politicians complain about rates that are historically normal when the national debt is 4 times what it was in 2009.

The most important jolt number of the year, 7.67M jolt job openings, 6 7 what does it mean? Ha Employment cost index will pop tomorrow. I am guessing not many people are short. Everyone on one side of the boat. What could go wrong?

Depending on when and how aggressive the Fed cuts, I think we will see a 20-30% drawdown in equities. Historically, markets decline after the Fed cuts, but then again do fundamentals matter anymore?

“ Debt is neither a good thing nor a bad thing per se. Likewise, the use of leverage in the AI industry shouldn’t be applauded or feared. It all comes down to the proportion of debt in the capital structure; the quality of the assets or cash flows you’re lending against; the borrowers’ alternative sources of liquidity for repayment; and the adequacy of the safety margin obtained by lenders. We’ll see which lenders maintain discipline in today’s heady environment.”~ Howard Marks Oaktree Capital~ this is great way to think of all debt, except as Wolf stated their is never repayment of Debt in sovereign or large scale corporation, just rollover with new debt issues.

I will only add that you must let bad debt actually clear and in that process actually reset asset prices. Repackaging bad debt and selling it to a greater fool simply makes a larger eCONomic bomb.

The recent price action just reinforces a

“normal yield curve “ with longer term rates reflecting more uncertainty than shorter term rates . Normal yield curves have been much more common than its cousin “inverted yield curves “in the past

Can the yield curve become even more upward sloping .Yes , since there is no low risk way to arbitrage long / short rates .

And unless the Fed starts QE again or institutes “yield curve control” , there is nothing ( even Trumps histrionics) that will prevent long term rates from moving even higher .

Given the Feds attitude towards letting its MBS holdings runoff without replacing them , there is good reason to expect the relationship between the 10 year note and mortgage rates to move even higher.

Correct. This will put additional pressure on CONgress as servicing the debt becomes more expensive.

Interesting times.

Where does Japan fit in? Carry trade has evaporated, YOY + 90 bips on their 10 yr, they own @ 13% of outstanding US debt. Their rates are beginning to move. They look like an indicator for the entire BIS eco system. Correspondingly, at some tipping point – cut vs hike does not look like a decision that can be made in the vacuum of US politics.

TIA

Japan has 3.0% inflation. The 10-year yield is only 1.97%, so a negative real 10-year yield of -1.03%. It SHOULD be 4%-plus, given where inflation is. The BOJ’s main policy rate 0.5%, LOL, with 3.0% inflation. The yen has collapsed against the dollar, impoverishing the Japanese people when it comes to imports (energy, foods, other stuff) and international travel. Their monetary policy has been totally f**ked up for decades.

Price of Beef in Japan is over $100/lb

That’s for Kobe Wagyu beef — that special super-fat intensely marbled Japanese beef from special cattle (Tajima cattle). I had some in Japan some years ago. It’s like eating flavored butter. It sort of melts in your mouth, you barely have to chew it. It’s kind of like the belly part (fatty part) of a fish, such as toro of tuna). I’m a free-range grass-fed steak kind of guy and like to chew my meat, so eating this buttery beef is not my thing. In addition to being hugely expensive in a restaurant.

Regular beef is about twice as expensive in Japan as in the US (such as Safeway prices). My wife works for a company that exports beef to Japan (chilled and frozen), so I get to hear the laundry list of issues that come with exporting beef to Japan. It’s part of Japan’s administrative barriers to entry (instead of tariffs) to protect local producers. Everything has to be preapproved to get into the country. US meatpackers have to butcher the carcass in a certain approved-by-Japan way, and produce special cuts, packaging, and labeling for exports to Japan, so they cannot mass-produce the shipment along with all other shipments. They have to do a special run for Japan-destined products. Then the company my wife works for has a sister company in Japan that gets this product painstakingly through customs, puts an approved label on it, and sends it on. All this costs a lot of money.

They know a thing or two about the futures market.

Thank you Wolf, and duly noted on your comments. What I don’t get (and maybe no-one [even Kyle Bass] knows) is what happens as Japan boosts rates to defend the Yen?

Graeber (The First 5000 Years) notes that we really haven’t had a period wherein ZIRP was employed. It is a modern concept.

At some point I have to believe the fantasy world of MMT / ZIRP / Extend and Pretend; combined with capricious 4.24.24 style seizures corners the $ and / or takes the decision out of US hands.

We’ll see.

Thank you for your articles – they prompt thought, which is refreshing in a sea of opinion and noise.

Take care.