“Many participants suggested that … it would likely be appropriate to keep the target range unchanged for the rest of the year”: FOMC minutes.

By Wolf Richter for WOLF STREET.

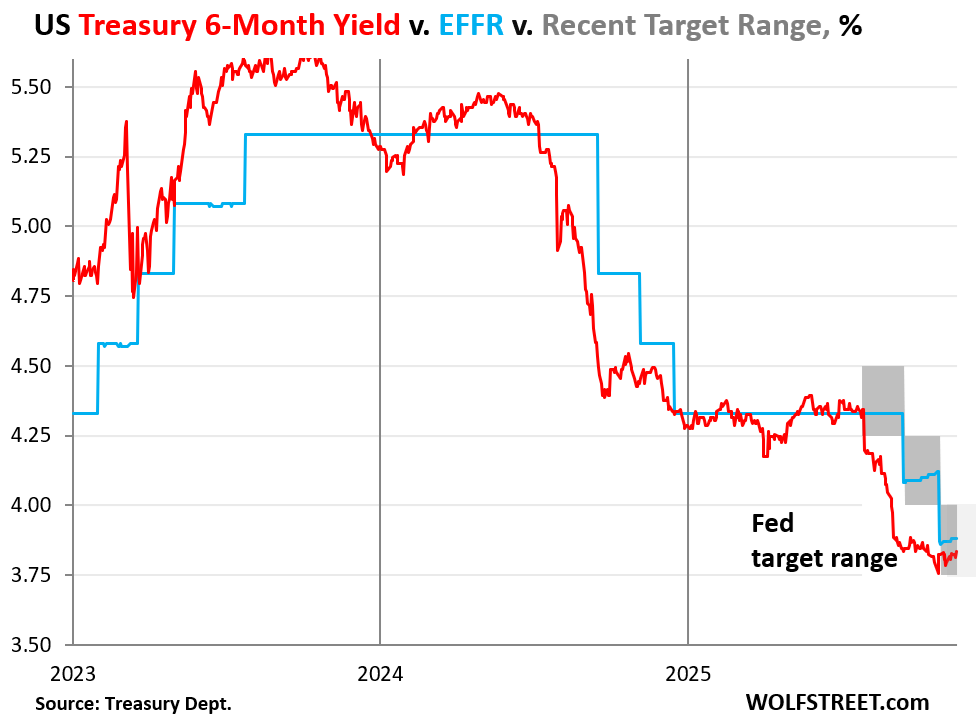

The minutes of the FOMC’s October meeting, released today, made official what a majority of Fed speakers have been saying for weeks: Unless the data changes drastically, there is not much chance of a December rate cut, and the Treasury market adjusted to it:

The 6-month Treasury yield rose by 2 basis points today and closed at 3.83%, well within the Fed’s current target range of 3.75% to 4.0% (shaded area). Just before the Fed’s October rate cut, it had dropped to 3.75% on a downward trajectory to price in the next rate cut in December, but then it reversed.

Traders and algos scrutinize everything that the Fed publishes, such as these minutes, and everything Fed speakers say in their speeches, and they trade accordingly. As a result, the 6-month Treasury yield reacts to expectations of the Fed’s policy rates over the next two or so months and is a good indicator where the Treasury market thinks the Fed’s policy rates will be within its two-month-plus window. And now, with the yield in the Fed’s target range, it predicts no change in December, and little chance of a rate cut at the January 27-28 meeting

The Fed’s FOMC is deeply divided, but with a majority on the side of likely no cut in December, while some members have been advocating for a cut:

“Most participants noted that, against a backdrop of elevated inflation readings and a very gradual cooling of labor market conditions, further policy rate reductions could add to the risk of higher inflation becoming entrenched or could be misinterpreted as implying a lack of policymaker commitment to the 2 percent inflation objective.”

“Many participants” expressed concerns that “overall inflation had been above target for some time and had shown little sign of returning sustainably to the 2 percent objective in a timely manner.”

The minutes depict a deeply divided FOMC, amid strong concerns about persistent and rising inflation and also strong concerns about a slowly cooling labor market, despite “solid” economic growth – and they fingered AI and automation, along with reduced immigration, among the factors for this combination of slow hiring but few layoffs amid solid economic growth:

“Participants generally attributed the slowdown in job creation to both reduced labor supply—stemming from lower immigration and labor force participation—and less labor demand amid moderate economic growth and elevated uncertainty. Many participants remarked that structural factors such as investment related to AI and other productivity-enhancing technologies may be contributing to softer labor demand.”

And the minutes reported on the stark division during the October meeting – apparently not even that October rate cut was an easy call:

“Many participants observed that the divergence between solid economic growth and weak job creation created a particularly challenging environment for policy decisions, requiring careful monitoring of incoming data to distinguish between cyclical weakness and structural changes in the relationship between output and employment.”

Amid upside risks to inflation and upside risks to unemployment, “many participants were in favor of lowering the target range for the federal funds rate at this [October] meeting, some supported such a decision but could have also supported maintaining the level of the target range, and several were against lowering the target range.”

Lots of disagreements even about the October cut:

“Those who preferred to keep the target range for the federal funds rate unchanged at this meeting expressed concern that progress toward the Committee’s inflation objective had stalled this year, as inflation readings increased, or that more confidence was needed that inflation was on a course toward the Committee’s 2 percent objective, while also noting that longer-term inflation expectations could rise should inflation not return to 2 percent in a timely manner.”

And about that December meeting:

“Many participants suggested that, under their economic outlooks, it would likely be appropriate to keep the target range unchanged for the rest of the year.”

So unless data shows some big changes until the December meeting, the majority of the FOMC members are in no mood to cut, in face of their concerns about persistent and rising inflation.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Deeply divided is what US does best so good to see it moving into everything.

This is not necessarily a bad thing. Extremely powerful institutions (and nations) are capable of doing extreme things when united. But being human, all too often they are unfortunately united in error.

Division, discussion and deliberation are important “checks and balances” guardrails to prevent errors of excess.

Put another way, I fear those who are overly certain far more than those who are thoughtfully uncertain.

VanEck Gold Miners ETF (GDX) $76.39 +0.76 +(1.00%) YTD 126.21%

The financial media is hoping that the warnings from retail earnings prompt a Fed rate cut so that NVDA can continue to cash out. It’s kind of entertaining.

Satanic

Why isn’t the Federal Reserve urgently moving to increase the Federal Funds rate and other short term interest rates?

Because that would be doing the right thing for the country, and they do not want their wrong decisions streak to be blemished

Rates on notes and bonds are what need to come up moreso than bills. But the Fed doesn’t directly control that.

Myrrh Resin Index ETF (MRI) $134.27 +$1.21 + (.88%)

The October jobs report has been canceled. The November one will come out too late for the Fed.

But we’ll get September tomorrow 🤣

Big data changes aside, we are now looking at March for the Fed to decide its direction. Will the stock market cope with the frustration or will it blow a gasket?

Notice how 2% went from ceiling to floor.

It’s neither ceiling nor floor, but a “target” that they try to get close to. Since inflation figures wobble up and down a lot, “close to” would be on either side. Alarm bells go off then it’s substantially below or above.

Hi Wolf, barely on-topic here: Could you give us your views about what’s happening in Japan and their rates.

Yen near the magic 160 line again. Long-term yields up a little, but still incredibly low, with the 10-year at 1.82%, way below the rate of inflation, it should be 4%+, and the 30-year yield at 3.38%, ridiculously low for 30-year paper in an inflationary environment and a gigantic debt load, it should be 5%-plus.

The BOJ should raise its short-term rates to at least 3.5% and speed up QT. But they’re not going to do it because there is too much debt out there. They’re engineering a currency and debt devaluation. That’s how they’re paying for the piper.

“The BOJ should raise its short-term rates to at least 3.5% and speed up QT. But they’re not going to do it because there is too much debt out there. They’re engineering a currency and debt devaluation. That’s how they’re paying for the piper.”

YES, just like The Fed will.

Hedge accordingly.

Interesting, thanks. But it did raise dome questions for me at least.

If a dozen years of negative real interest rates didn’t lift the CPI above 2%, what makes the FOMC think raising rates will lower the CPI?

What was the change in FOMC’’S average weighted interest rate and interest expense on the UST debt in FY 2020 versus FY 2024?

And one last question; what is the difference of the interest expense on a percentage basis of the Federal Government’s FY 2020 compared to FY 2024?

All you have to do is read it (through Q2 since we don’t yet have all of the Q3 data yet, such as GDP):

https://wolfstreet.com/2025/08/28/us-governments-fiscal-mess-interest-payments-on-the-treasury-debt-interest-rates-tax-receipts-and-debt-to-gdp-ratio-q2-2025/

Good observations that underscore the Fed’s ability to control the short end. Unfortunately, risk is being repriced in the bond market, globally. Anyone seen what is happening to Japanese bond yields lately?

Hedge accordingly.

There are an incredible number of moving parts in the US economy. Add in what’s going on internationally and it gets beyond complicated.

My gut tells me that the lower part of the K economy has stagnated….folks barely getting by, little room to save.

The upper part of the K economy is weathering better. They generally have better paying (have to have) jobs but also, as we know, financial assets that until now, have done really well. But even those gains are showing some strain; particularly real estate assets. Also Boomer retirees are starting to realize their savings is not going near far enough with the 25-30% inflation suffered over the past 3-4 years. So that spending is slowing up.

If inflation continues (albeit more slowly), that majorily hurts the lower K sector; thus the hestitancy to lower by some Fed members.

But keeping rates higher for longer is hurting a significant asset class: Housing. This probably impacts the upper K sector most.

Throw in tarriff impacts, government deficits, dollar hegemony challenge, China’s control over key industries and you have a veritable shit show going on.

Bottom line for me is ongoing stagflation in lower K and muddling through with upper K. Until something breaks.

It’s not higher rates but prices being too high that is hurting housing.

Yesterday Trump threatened to fire Bessent if he doesn’t get Powell to lower interest rates, during a speech at the U.S.-Saudi Investment Forum.

You know that Bessent will be working hard on that.

When are people finally going to quit posting every Trump-said BS?

When the BBC stops? ;)

its pretty easy to get TRUMP to change his mind or just come up w some other random plan. it wont be hard for Bessent ….it’ll just happen automatically .

All degenerate gambling fools should perish without any bailout.

The long-term rate of change in money flows, the volume and velocity of money, peaks this November. Inflation will be headed down from here. Short-term money flows were already decelerating. There could be a recession beginning in the 1st qtr. of 2026.

Crypto crashed again today. Crypto is heading for zero or below zero as the Swamp predicted in a previous post. Many investors refinanced on their homes and plunged the cash out funds into Crypto. They will soon be underwater on their Crypto portfolio and on their homes as well. The Crypto crash may also take the whole stock market down with it.

Anyone stupid enough to leverage their house for something so unstable as the crypto market deserves to be homeless. Even in the stock market, people are advised never to take margin debt, and that is much less risky.

The global economy never fully recovered from the 2008 crisis. The overall growth of the real economy has been muted and living standards in most countries have been stagnant or have gone into reverse. The main factors propping up global growth have been huge investments in infrastructure and housing in China, Western governments’ gigantic monetary and fiscal stimulus to their economies and a speculative frenzy in asset prices centered in the U.S. Of these three factors, only the third continues to this day.

The CPC has slowed the rate of investment in infrastructure and has burst the housing bubble, bringing the market into a depression. In response, the regime has invested massively in “new productive forces,” driving down the price of many industrial goods, including electric cars and solar panels. This massive investment has created a deflationary cycle in China and accelerated the tendency toward deindustrialization in other parts of the world. Across the globe, we can observe a slowing down of production and an oversupply of industrial goods.

On the monetary side of the equation, most major economies saw increased interest rates in response to the spike in inflation following the Covid pandemic. This marked a break with the ultra-loose borrowing conditions that had been in existence since 2008. The result is that borrowing is growing ever more expensive, pushing many governments to try to limit their deficits. Most imperialist countries now find themselves with historically high debt burdens, which threaten to cause great political and economic instability in the future. These problems are all exacerbated by the drive to drastically increase military expenditure.

As for the stock bubble centered on the U.S. market, it has continued to expand following the correction in the early days of the Trump presidency. This has enabled those who own stocks to continue consuming at high levels. Meanwhile, everyone else is struggling more and more to get by. The massive spike in tech stocks due to the supposed AI revolution has continued to be the main, and increasingly the only, driver of stock market gains. The stock valuation of the chip designer Nvidia recently hit five trillion dollars, which means the company is worth as much as the entire annual output of the German economy. Clearly this is insane. So far, the bubble has been able to continue growing by leveraging the rising value of AI companies to purchase more AI products, causing an upward spiral in valuations. This will necessarily end in a catastrophic collapse. When exactly this occurs can’t be predicted. But we can see that there is a decreasing number of factors supporting the stock bubble, which is reliant on the continued growth of a declining number of stocks.

When the music stops, we will get a glimpse into the true state of the world economy and the real balance of economic might between the great powers. In the first instance, a major shock will probably not lead to a rise in working-class militancy. Fear for the future and for self-preservation will probably be the prevailing attitudes, allowing governments to further squeeze working people despite their growing unpopularity.