The deficit doubled, as benefit payments spiked in part due to the expansion of Social Security, while income rose only slowly.

By Wolf Richter for WOLF STREET.

The new thing this year for the “Old-Age and Survivors Insurance (OASI) Trust Fund,” commonly called the Social Security Trust Fund, was the Social Security Fairness Act, signed into law on January 5, 2025, by President Biden. It expanded benefits to certain groups of retirees with careers in government, education, and law enforcement that are already covered under public pension plans.

The Act ended the Windfall Elimination Provision and the Government Pension Offset, which had reduced Social Security benefits for certain people who also received a public pension.

Retroactive benefit payments started going out in February 2025, and surged out in March, and benefit payments in March spiked by 13.5% from February, and by 20.2% year-over-year, to $130 billion for just March, a massive record. Those were just the retroactive catch-up payments. The regular monthly benefit payments also increased under the Act.

But the Act did not provide for any additional revenues or other tweaks. In addition, the growth of contributions slowed sharply as the labor market has been growing more slowly. And so, with income barely rising (blue in the chart), and outgo surging (red), the Social Security deficit doubled this fiscal year to $181 billion, according to the Social Security’s fiscal year income and outgo data, released today.

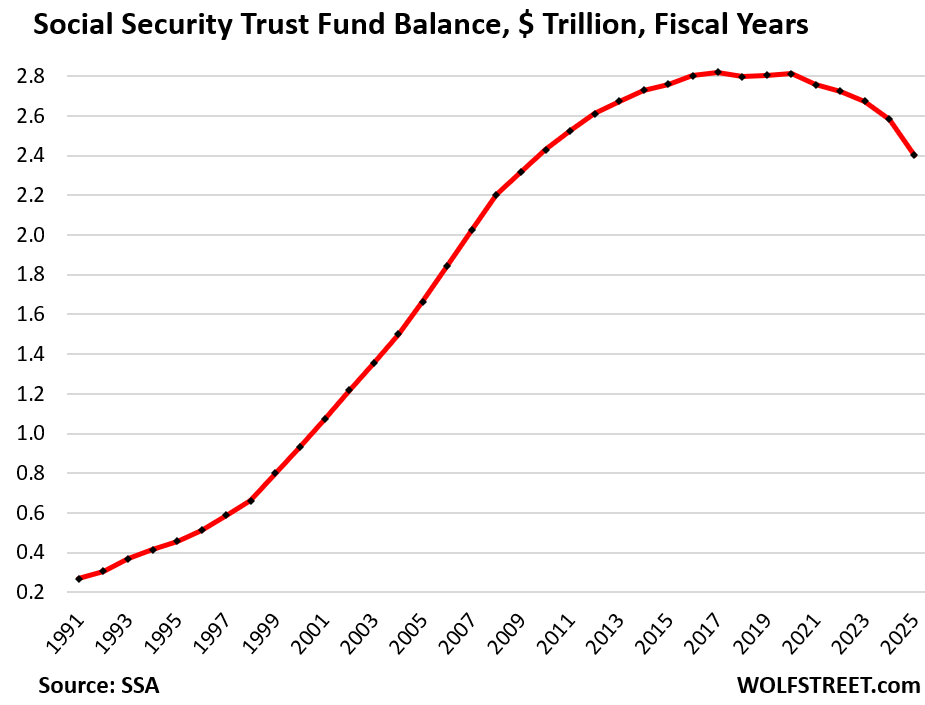

When the total income (blue) was above the total outgo (red), the Trust Fund ran a surplus which caused assets to accumulate and the Trust Fund to grow. When the red line rose above the blue line – this happened for the first time in 2018 – the Trust Fund ran a deficit and its assets shrank.

Congress needs to get serious about tweaking various aspects of Social Security, but this time to improve the financial aspects of the system, and not to make them worse, as it had done in January.

These figures do not include the Disability Insurance Trust Fund, which by law is a separate entity from the OASI Trust Fund, and is not part of this discussion here.

Total outgo (red line in the chart above) spiked by $117.2 billion in the fiscal year through September 30, or by 9.0%, to a record $1.42 trillion.

By category of outgo:

- Benefit payments spiked by $117.4 billion (+9.1%), to $1.41 trillion, attributable to more retirees drawing benefits, including through the Social Security Fairness Act, and to Cost of Living Adjustments (COLAs).

- Administrative expenses fell by $300 million to $4.5 billion (0.19% of the Trust Fund balance, 0.36% of total income).

- Transfer to Railroad Retirement Program rose by $100 million to $6.0 billion

Total income (blue line in the chart above) rose by only $27 billion (+2.3%) in the fiscal year ended September 30, to a record $1.24 trillion.

By category of income:

- Contributions rose by only $21 billion (+1.9%), to $1.12 trillion. The slow increase was due to much slower labor market growth.

- Taxation of benefits rose by $5.1 billion, or by 9.6%, to $58.2 billion.

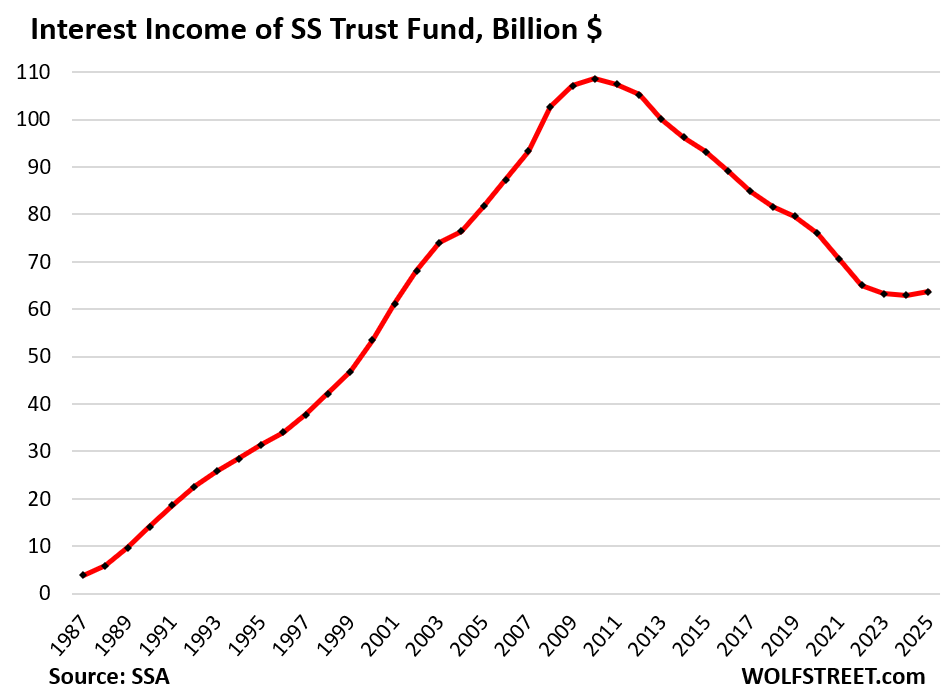

- Interest income from the securities in the Trust Fund ticked up by 1.4% to $63.7 trillion, on higher interest rates earned by the Trust Fund’s securities.

This first increase in interest income came after 14 years of declines that ravaged the fund though its balance ballooned through 2017. The Fed’s reckless interest rate repression (QE and ZIRP) from 2008 to 2022 is responsible for the plunge in interest income.

Social Security is not part of the general budget. Its surpluses through 2017 didn’t reduce the general budget deficits; and now its deficits do not increase the general budget deficits. And its surpluses and deficits have no impact on the size of the US debt. The Trust Fund doesn’t have debt and doesn’t borrow funds. It invests funds into US debt. It’s an investor, not a borrower. Cutting benefits will not reduce the general budget deficit nor the debt.

But the system needs to be tweaked in several ways to accommodate demographic changes, just like it was tweaked under Reagan last time.

The Social Security Trust Fund.

With spiking outgo and only slowly rising income, the deficit in the fiscal year doubled to $181 billion, from $91 billion in the prior fiscal year, the biggest deficit yet, and the fifth year in a row of deficits.

Over the past 36 years, 30 years had surpluses, totaling $2.6 trillion, which accumulated in the Trust Fund. Six years had deficits (2018, 2021, 2022, 2023, 2024, and 2025), totaling $429 billion, which reduced the Trust Fund.

The shortage between income and outgo is paid out of the Trust Fund, and in the fiscal year, the Trust Fund balance declined by the amount of the deficit, by $181 billion, or by 7.0%, to $2.40 trillion.

How the Trust Fund invests the $2.4 trillion.

The Trust Fund’s total assets of $2.40 trillion at the end of the fiscal year was split up between $2.23 trillion in interest-bearing special-issue Treasury securities and $172 billion in short-term cash-management securities (“certificates of indebtedness”) at the end of the fiscal year.

Similar to the Treasury I bonds and EE savings bonds that retail investors hold in their accounts at TreasuryDirect, these securities are not traded in the secondary market, and are not subject to the whims of the secondary market; so the value of these securities doesn’t fluctuate with the day-to-day prices in the secondary market.

The Trust Fund gets paid face value when its Treasury securities are redeemed. Day-to-day price fluctuations are irrelevant for the Trust Fund.

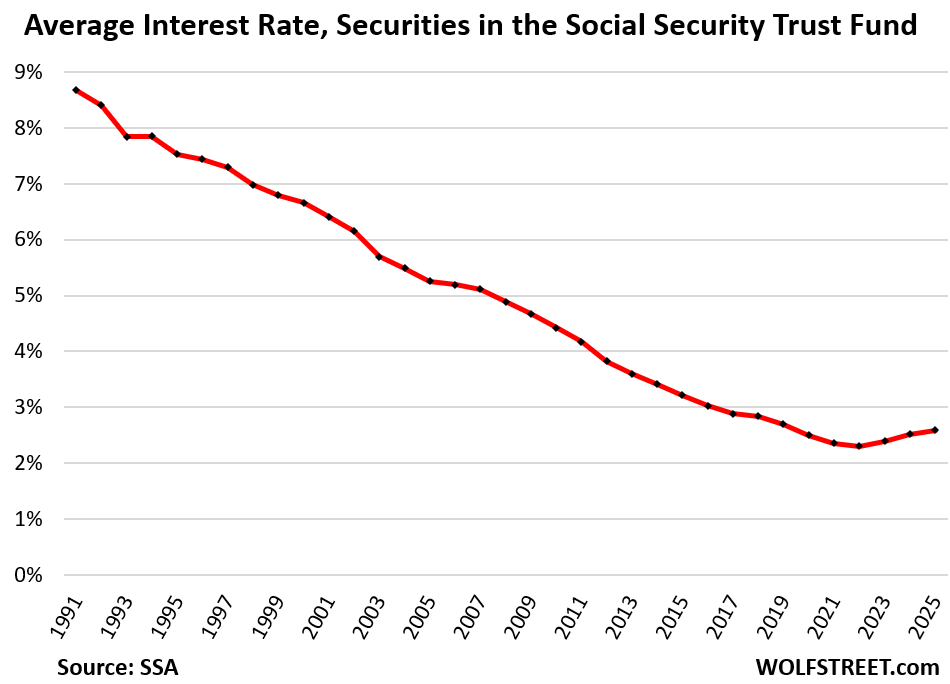

Investing in Treasury securities when they’re issued and holding them until maturity is a low-risk conservative investment strategy. But the Fed’s reckless interest rate repression from 2008 to 2022 crushed the cashflow from this investment strategy.

The average interest rate ticks up. The low-interest-rate securities from the QE and ZIRP era are maturing piece by piece and are being replaced with higher-interest rate securities with shorter maturities, which pushed up the average interest rate earned by the Trust Fund to 2.6%, the third year in a row of increases, after several decades of declines, but still woefully low.

For example, this fiscal year: If the Trust Fund had earned an average of 4.1% on its Treasury securities, instead of 2.6%, it would have earned $94 billion in interest income, instead of $64 billion. In the prior fiscal year, the deficit would have been one-third lower. Two fiscal years ago, it would have had a surplus.

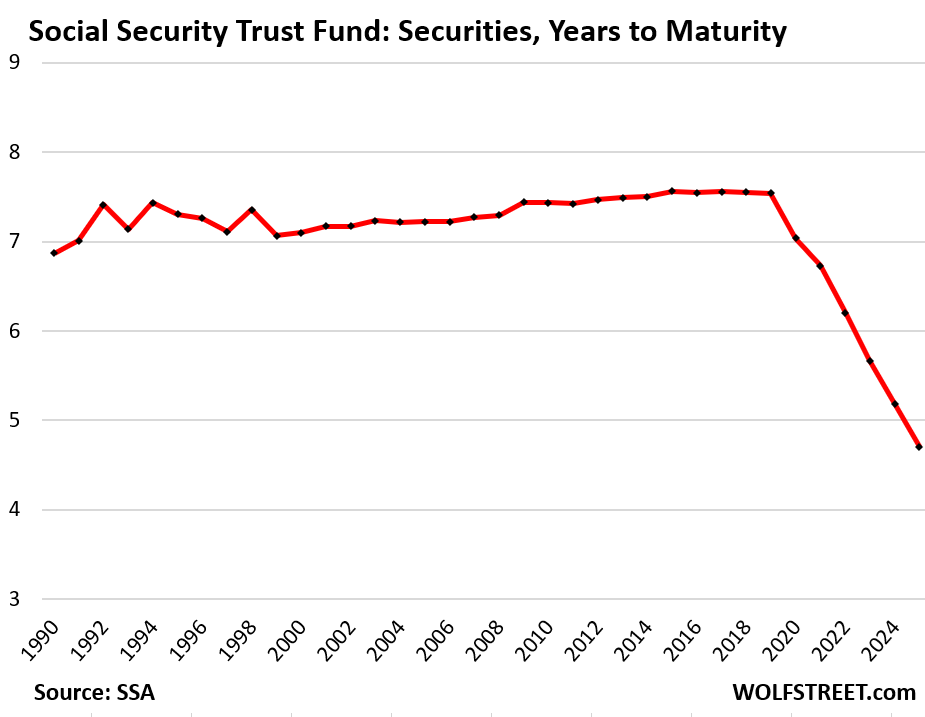

Shifting to shorter-term securities. The average number of years to maturity used to be around 7 to 7.5 years. But in 2020 it began to drop, likely a strategic decision by the SSA to not load up on the 0.5% longer-term securities issued at the time.

In the fiscal year through September, the average years to maturity declined to 4.7 years, the shortest on record.

Tweaking OASI is necessary. Various proposals have been floated in Congress over the years to tweak the system, but they have persistently gone nowhere. The only Act that was actually passed was the Social Security Fairness Act in January, which made the situation worse.

Generally, each proposal tweaks the system in several ways, and each tweak could be relatively small, but combined and over time, they’ll make a difference. It was done before under Reagan when the young boomers were told to retire later, and pay more for longer into the system. These reforms created the surpluses that caused the Trust Fund balance to rise from near nothing in the 1980s to $2.82 trillion by 2017. And it can be done again.

If no changes are made to the plan, if Congress doesn’t get its act together, the Trust Fund will be depleted in the early 2030s, and at that point, without adjustments till then, either the benefits would need to be trimmed to match the Trust Fund’s income on an annual basis, or the general budget would be used to make up the difference.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

This is awful Wolf…another thorn in America’s sound, responsible, ethical management systems. Doesn’t Good Judgement ever triumph over Reelection Prospects…ever!!!…PJS

Rarely. Maybe never.

Pete,

Good things and elections can go hand in hand. After all, The New Deal was really about getting the votes, even though it resulted in some good programs. We just need people to be smart enough to vote that way, which is likely a never situation!

Interesting connection to your previous post on fed rates. Perhaps some motivation for higher long-term rates is to shore up the Trust Fund a bit.

We could eliminate the income cap and tax all income,e, instead of the first 150k-ish. That would be a dramatic lift.

We could also treat capital gains as income, and apply social security tax to that as well.

Finally, we could also eliminate the congressional pension, converting their current pensions to 401ks, and I bet Social Security would be saved within 10 minutes.

Educated.

I did not realize that Social Security was not part of the general budget.

Probably should have know though !

When the adults were left in the room in the mid 80s, they did a responsible solution for all this stuff, including a tax reform that was essentially a tax increase, and delaying retirement for Gen X and late boomers. Without some of the stupidity that was done regarding benefits, it would remain solvent. The gummint double tax is finally being rectified, as no new plan members were allowed in the old closed systems after 1990 or so.

No adults now, so no solution until this administration is gone and a real accounting shows it benefits most of America. Which requires honest math, not fiction. The two deficits of social security and the us government require a real solution. The last one made 40 years. The next one should as well.

Or into the abyss we go. RED or BLUE we are all in this together, unless Peter Thiel is going to let you into his bunker.

The fund could easily be secured simply by removing the income cap on payroll taxes. Social security payments could also be means tested. After all, millionaires and billionaires probably don’t need these payments.

We could also add a payroll like tax on capital gains since those who own the vast majority of capital don’t have much in the way of taxable income.

But I know, this all smells like socialism which, in the USA, is something only reserved for the wealthy and for large corporations. Anything else risks the American people getting the erroneous impression that government can benefit the common man instead of only the wealthy.

The benefits to the ones who need them least, supported by the ones who can afford it least!

Sounds like our GubMint. Sounds like the adjustment they already made, in that they fully pay folks who already have a true pension?

“The only Act that was actually passed was the Social Security Fairness Act in January, which made the situation worse.“

Seems like the “new normal” for legislative action/ especially fiscal and monetary?

The average interest rate on the SS Fund’s securities is now less than the rate of inflation. Previous years (before 2020), the SS Fund’s interest rate was much higher than inflation. Looks like the fund will be burning through money a getting a negative real rate of return at least in the short term (few months) and have been the past four years or so.

I do not understand why benefits can’t be cut, particularly for those making >$100k in income per year. Even just a 5% haircut would help the fund. As someone less than 30 years old, I would appreciate being able to someday collect from the fund I’m paying into.