The 6-month Treasury yield sees Fed on hold in December. Cutting rates as inflation accelerates is a delicate operation that the bond market isn’t fond of.

By Wolf Richter for WOLF STREET.

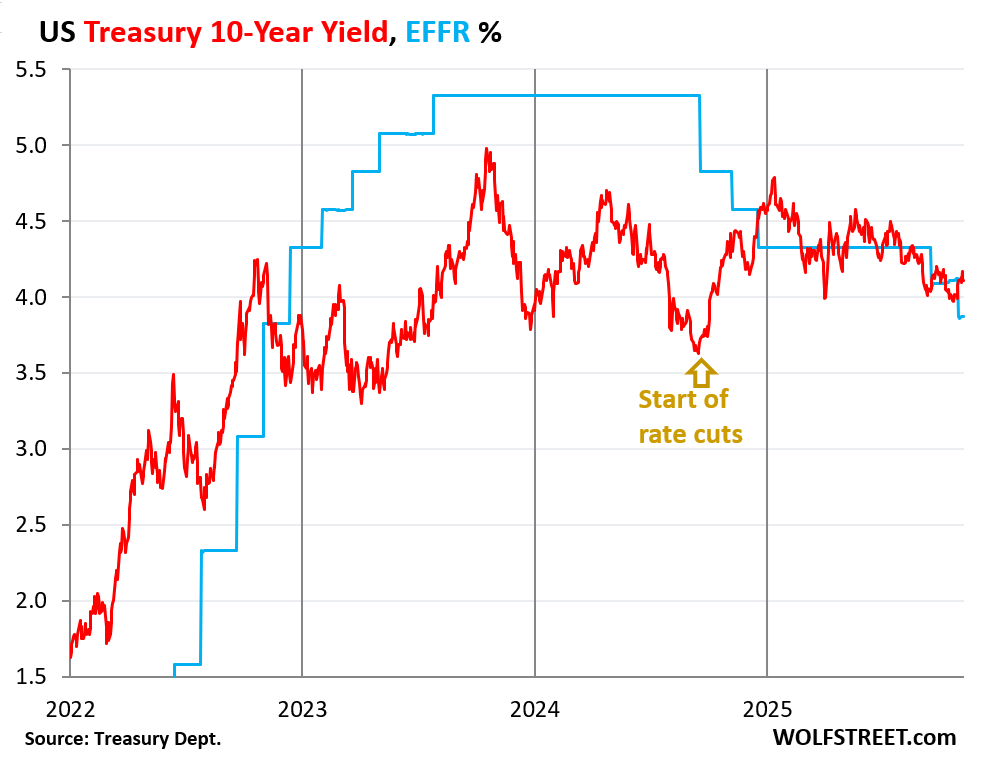

The 10-year Treasury yield closed on Friday at 4.11%, essentially where it had been for seven trading days, up by 12 basis points from October 28, the day before the Fed cut its policy rates, and up by 48 basis points since the first rate cut in this cycle in September 2024, when the 10-year yield was 3.63%.

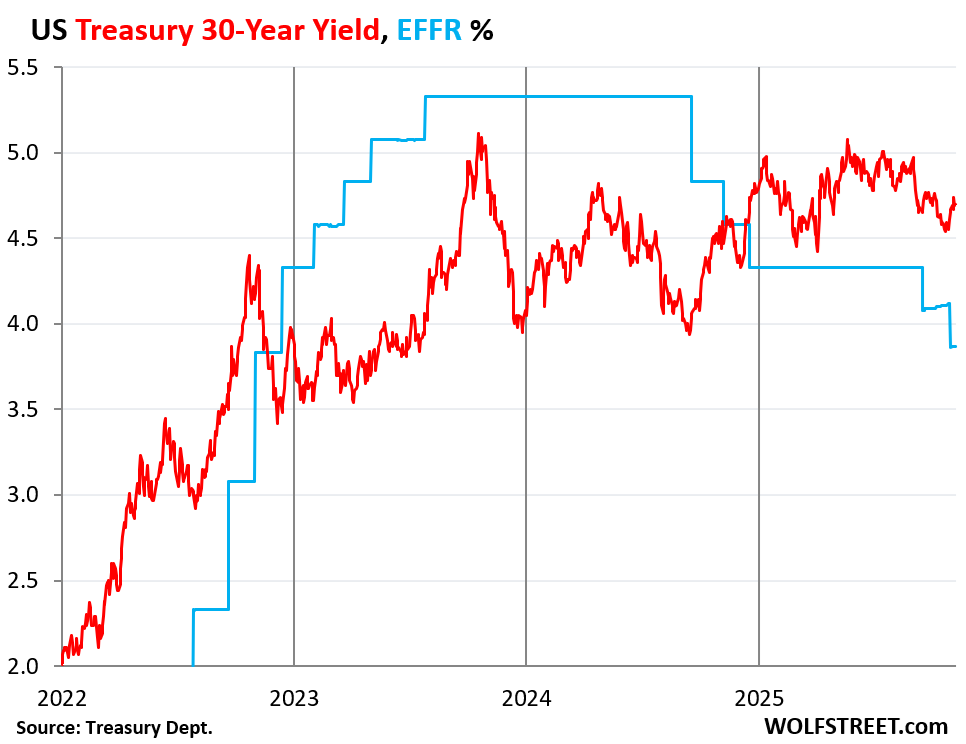

The 30-year Treasury yield rose to 4.70%. It was 4.55% just before the October rate cut, and 3.94% before the rate cut in September 2024.

The Fed has now cut by 150 basis points, and the 30-year yield has risen over the same period by 76 basis points. Long-term yields are determined by the dynamics in the bond market, not by the Fed’s short-term policy rates.

The 6-month Treasury yield, which is normally good at predicting the Fed’s next rate move as the market digests every comma of the Fed’s releases, speeches, and press conferences, is predicting the Fed will hold its rates in December.

Since the Fed’s rate cut at the end of October, the entire yield curve from the 3-month Treasury yield to the 30-year Treasury yield has risen. And mortgage rates have risen too.

But the Effective Federal Funds Rate (EFFR), an overnight rate that tracks now largely vanished interbank lending, and that the Fed targets with its policy rates, dropped by 25 basis points to 3.87% after the October rate cut (blue in the chart).

The 10-year Treasury yield, at 4.11% (red) is now 24 basis points above the EFFR. In normal credit markets, long-term yields, such as the 10-year Treasury yield, are higher and often quite a bit higher than short-term yields, such as the EFFR. When it’s the other way around, when short-term yields are higher than long-term yields, the yield curve is said to be “inverted.” The 10-year yield and the EFFR have been in and out of inversion all year long:

The 30-year Treasury yield ended the week at 4.70%, up by 15 basis points from the day before the Fed’s rate cut at the end of October.

The upward trend of the 30-year yield started in August 2020, after trading briefly as low as 1.0% in March 2020. That yield had been pushed down by the Fed’s mega-QE. By the end of 2021, it was at 2.0%. Since October 2023, it has bumped into the 5%-mark several times.

The 30-year Treasury yield reacts to bond-market issues, such as expectations of future inflation and expectations of supply of new bonds that have to be absorbed, rather than the Fed’s short-term policy rates.

Also note how the EFFR inched up just a tiny bit towards the end of October during the repo market turmoil, which settled down last week.

Cutting rates as inflation accelerates is a delicate operation that the bond market is not fond of. The bond market fears a Fed that is lackadaisical in face of inflation. And the bond market is worried about the onslaught of new supply of bonds to fund the ballooning government deficits.

The bond market could decide that it wants to be compensated a lot more for those two risks – inflation and supply – via higher yields, especially if inflation continues to accelerate, with services inflation, which accounts for about 65% of the inflation basket, being the big driver, and goods inflation chiming in.

Last fall, when the Fed cut by 100 basis points in four months, the 10-year Treasury yield jumped by 100 basis points. This taught the Fed a bond-market lesson, and it put further rate cuts on ice, and started talking hawkish, which succeeded in coaxing long-term yields and mortgage rates back down.

Then in September and October 2025, the Fed went at it again with rate cuts, but more carefully. And after the October cut, the Fed put a December rate cut into doubt, in part to keep the bond market from throwing another hissy-fit.

The 6-month Treasury yield predicts a Fed “hold” for December. On Friday, it closed at 3.80% (red line), well within the Fed’s target range for the EFFR of 3.75% to 4.0% (shaded area).

Just before the Fed’s October rate cut, it had dropped to 3.75% and had been on a downward trajectory, which has since then reversed.

The 6-month yield reacts to expectations of the Fed’s policy rates over the next two or so months and is a good indicator where the bond market thinks the Fed’s policy rates will be within its window. It nicely predicted the last two rate cuts; and it nicely predicted the first four rate cuts in 2024. And it nicely predicted the rate hikes in 2023, except for the moment of bank panic in March 2023. It goes by what the Fed says, and sudden panics are outside of that. And it wrongly predicted a rate cut for early 2024 amid general rate-cut mania.

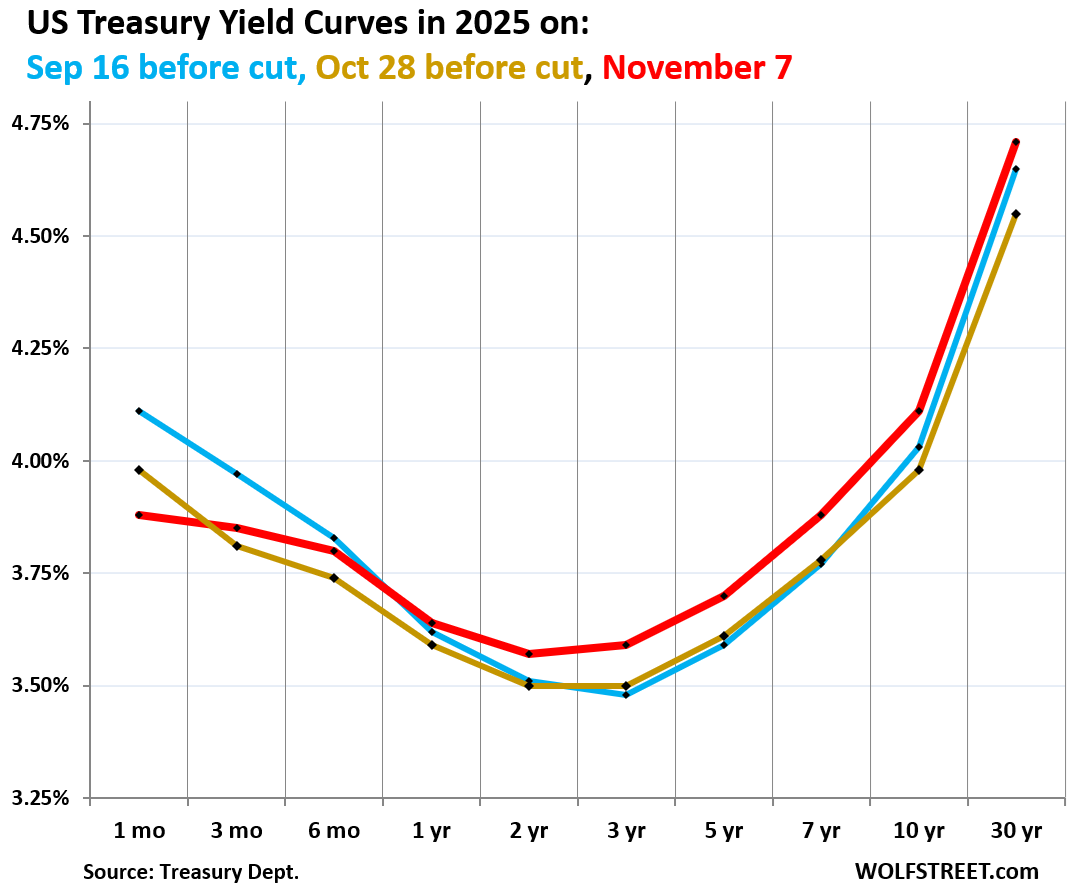

The yield curve has moved up since the last rate cut. The chart below shows the yield curve of Treasury yields across the maturity spectrum, from 1 month to 30 years, on three key dates in 2025:

- Red: Friday, November 7.

- Blue: September 16, just before the Fed’s rate cut.

- Gold: October 28, before the Fed cut rates again.

The 1-month yield (3.88%) is boxed in by the Fed’s policy rates (3.75%-4.0% since the October rate cut) and closely tracks the EFFR (3.87%). That’s the only yield that dropped since the October rate cut.

Both the three-month yield (3.85%) and the six-month yield (3.80%) rose since the rate cut, indicating that the bond market figures the Fed will keep rates steady in December.

The 1-year (3.64%), 2-year (3.57%), and 3-year (3.59%) yields have all risen since both the October and the September rate cut. They’re moved in part by expectations of the Fed’s policy rates within their window, and they’re expecting more rate cuts next year, but fewer of them than they did two months ago.

But the further yields go out on the yield curve, the more they’re influenced by inflation fears and supply concerns – and there are lots of both.

Mortgage rates have re-risen since the October rate cut. The daily measure of the average 30-year fixed mortgage rate by Mortgage News Daily has jumped by 22 basis points since just before the October rate cut, to 6.32% on Friday.

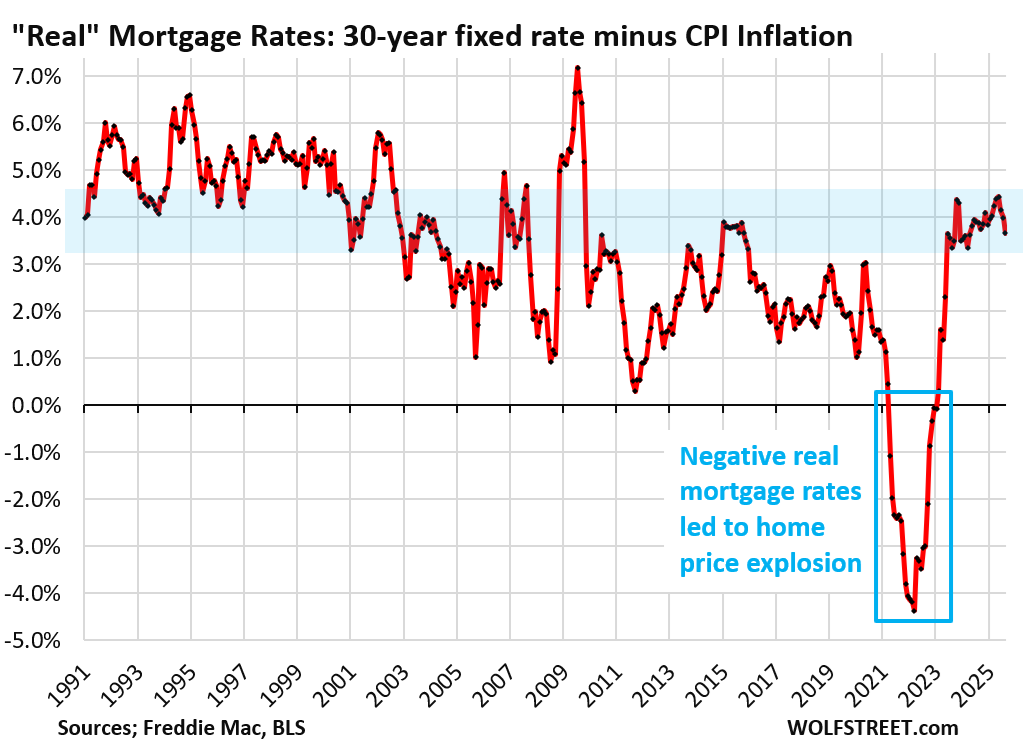

Mortgage rates of 6% to 7% used to be the lower end of the normal range before the Fed’s QE started distorting interest rates during the Financial Crisis.

The 6% to 7% mortgage rates are now only a big deal because home prices exploded by 50% and more in just two years from mid-2020 to mid-2022, after they’d already surged for years, inflating home prices to where they’re no longer economically feasible.

But that home-price explosion was a result of the Fed’s reckless monetary policy that created 30-year fixed mortgage rates below 3%, while inflation had begun to rage and was heading to 9%. The Fed, with its reckless policies, orchestrated negative “real” mortgage rates of -3%, -4%, and even lower – better than free money, and when money is free, buyers’ brains turn to mush, and prices don’t matter. Then the music stopped.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

I thought the T-bills market (0-12 months) have direct by the FED with their interest rates policy, is that not the case? I know there’s correlation/causation for sure but based on even the T-bills rate going up slightly (in the midst of the last cut), I am guessing the Bond market are the ultimate decider for all Treasury bills/notes/bonds rates? Has there been time in our history when T-bills rates diverge greatly from FED funds rate or can that ever happen? I know they don’t have direct control over the notes/bonds market except through unconventional means like yield curve control..etc

Short-term yields predict the Fed’s next move as the bond market prices in expectations (sometimes wrongly) of where short-term rates will be in a month or two or three (depending on maturity).

BTW: all yields are calculated. The 6-month yield, for example, is calculated of all Treasury securities that mature in about 6 months, but none mature in exactly 6 month, so that requires more calculations. It includes 30-year bonds that have about 6 months left to run before they mature and therefore trade like a new 6-month T-bill.

Wolf, does that mean you could theoretically produce a yield curve chart for every month from 1 month to 360 months (30y x 12 months), given that there are outstanding treasuries at almost every remaining maturity? May not be very useful but it could be cool to see a “finer resolution” yield curve.

You can obviously calculate anything you want. What I said was that there is no 10-year yield that is not calculated because no security out there matures in exactly 10 years from now. Notes mature on the 15th of the month and at month end. 10-year notes are sold at auction with maturities of 9 years, 11 months, or whatever, not even exactly 10 years. So all these yields are calculated from a variety of different transactions.

If the entire yield curve has shifted upward…could the driver be an unusual shift in investor requirements for bond term premiums? All driven by risk expectations? i.e., there is more in play than just adjusted expected inflation.

Yields up across the board again this a.m. Liquidity as measured by SOFR and IORB remains on the tight side.

Weii, I would not describe the engorgement of the stock market as an indication of monetary restriction. I would describe it more as a cluster F**k

The Treasury bond market now sees that future short term rates are not going to compensate for inflation.

The bond market is way too sanguine about inflation, in my opinion.

Agreed, and I’ll go further with an unpopular comment. Unemployment needs to hit 6% to contain inflation. The Fed’s decision to focus on labor, rather than containing inflation, is exactly the wrong move at this juncture. Wage growth is 4.5 percent for job-stayers and 6.7 percent for job-changers. This is way too high, and presages further services inflation (65% of the inflation basket, you say) from already high levels.

Pretty sure that mandates for increased minimum wages are playing a role too.

Some of those have been huge, and it’s almost funny how the people who want higher minimum wages don’t understand how it affects the price of so many things that they buy.

Just dropping by, the people who advocate for that want the wages to go up but the prices to stay the same. The only way for that to happen to the people, on average, is to have increased productivity.

That’s the part we’ve been lacking for a long time.

Hang on, so you guys are saying it’s not possible to raise wages (is there a difference between wages and minimum wage, besides the number?) and maintain stable prices? I’m just a dumb carpenter, but that seems… Untrue. Why would anyone work if you have to keep running faster to stay in place?

People work because they like buying food and shelter and clothing.

It’s a lot like why our ancestors went out hunting every day despite it not ensuring they were “getting ahead”

There is a lot of entitlement in modern society that if a person does the exact same job tomorrow as they did yesterday, the universe automatically owes them ever increasing bag of goodies in reward.

Grant: you seem to have misread what I wrote. Why would someone increase their productivity to stay in the same place? Did your ancestors run farther and farther each month for the same antelope? If those lazy cave dwellers hadn’t gone to college and become executives, they would have starved by now. Deservedly so.

In being serious though, there’s is a baseline for survival by modern standards. Just like people have baselines for what they expect from a vehicle, home, or an employee. As others have pointed out, there’s no deflation in services, so why do people expect deflation in wages (or it’s inverse, increased productivity)? And why do they never believe those deflated wages will affect their own income?

Mitry, that’s not what I said. What I said was that it’s not possible for wages to go up AND have stable prices unless productivity increases, either at an individual level or a macro level.

There’s no free lunch.

TSonder, I appreciate the reply. My above comment was in response to someone else, but I’m genuinely curious. You say wages can’t go up while prices are stable, and I’m questioning why you think that is.

For example, executive pay has increased. As a residential building contractor, my rates have increased every year to compensate for the increasing cost of supplies, as well as the cost of living. I’m sure there’s are other industries that have prospered. And yet wages are somehow immune to these economic forces. I truly believe the statement, “It’s not possibly for wages to go up and have stable prices without increased productivity” to be untrue. I’m open to putting some limits on that statement, but there are plenty of useless or no-more-useful folks that have gotten raises. As a carpenter who gets older and slower every year, I’m one of them.

I’m genuinely wondering where the logic that raises can’t be given comes from.

Hasn’t Phillips Curve thinking received considerable rethinking in the last couple decades? I think Powell has testified such.

It seems like this comment thread carries the assumption that productivity increases are the only way to justify wage growth at higher levels.

As someone who benefited greatly from a capitalist society that used to claim capitalism is the sharing of the pie, I don’t see the pie being shared equitably anymore. We are going to see the 3rd year of market gains of 25%. Per the rule of 72, that doubles my money in only 3 years. Awesome for those in this game. But I suspect it is unsustainable for society in general.

Maybe we will create a system where there is representation for the working class. Crazy idea, but maybe instead of demanding an increase in productivity year after year, there instead is better sharing of the pie. Who knows, maybe an organization that represents workers will begin to demand the massive corporate profits should be partially used to provide better health care coverage, some form of profit sharing (pension) for workers, or just a slightly higher yearly wage increase so stop the continued split developing in western culture.

Or as my richest capitalist friend said, who cares if the government is communist, socialist, or capitalist… When you are rich, any system will benefit you.

Not sure that will work out well for his grand kids. But it’s pretty clear that is where we are heading.

Wages (in this conversation) = real wages.

“The bond market is way too sanguine about inflation, in my opinion.”

Agree 100%.

But for me, the mystery is why bond market reaction was so small/slow in ZIRP 1.0 (2003-2006) and ZIRP 2.0 (2011-2018) and yet finally showing higher signs of life coming out of ZIRP pandemic (2020-2022).

All of those ZIRPs reflected/projected terrible things – but the bond vigilantes had vanished (power of Fed interventions/money prints?)

It is truly sad that the dynamics of a terrible reckoning were not forestalled at an earlier stage – by multiple Administrations getting the fiscal balance under something resembling control.

“But for me, the mystery is why bond market reaction was so small/slow in ZIRP 1.0 (2003-2006) and ZIRP 2.0 (2011-2018) and yet finally showing higher signs of life coming out of ZIRP pandemic (2020-2022).”

Because 2020 was 2008 on a dime bag of coke done in one line. The bond “market” is beginning to realize the US and west isn’t going to be able to bully the world much longer. So now asking for higher yields (which still are not nearly high enough)

I think it’s because they thought that the printed money could be contained to stocks. It was always bound to spill out into consumer goods and services, it just takes time.

@tsonders

August 22, 2019 – At the annual Jackson Hole, Wyoming meeting of central bankers, Philipp Hildebrand of BlackRock presents a proposal by himself and three other BlackRock executives (including Stanley Fischer). The proposal is for “going direct” and is entitled, “Dealing with the next downturn: From unconventional monetary policy to unprecedented policy coordination” proposing “unprecedented coordination through a monetary-financed fiscal facility.” The paper advocates “going direct” when the next economic downturn takes place. What does “going direct” mean?

Same Hildebrand who was Chairman of the Governing Board of the Swiss National Bank.

Agree!

I think we are all miscalculating/dismissing the amount of deflation coming by the recent tech advancements and incoming efficiencies and looming job losses. 10 year going to fall

Bringing costs down doesn’t bring prices down, but brings up profits.

What brings prices down or at least prevents them from rising faster is competition for the same sales dollar. But AI is now being used to set sales prices, and AI is colluding with AI, and so there may be the opposite effect on prices, and prices going higher due to AI.

Direct collusion by parties actively colluding, or giving non-public pricing information to 3rd parties, and allowing them to collude for the sellers, to the detriment of buyers, is still collusion.

I’ve heard of software that enables collusion described as CaaS software – it sells Collusion as a Service.

Collusion in any of its forms, should be identified and prohibited.

“is still collusion”

In January 2025, the Justice Department launched a lawsuit against Realpage for rent “price optimization” that essentially amounted to algorithm-based collusion among Realpage and apartment complex owners/lessors.

This is an important item given the close-to-unprecedented, tightly-compressed-in-time (2021-2022), unprecedentedly nationwide 20-30% explosion in rent prices.

I’m not sure if the Trump Administration is aborting or championing this lawsuit.

(Trump is easily capable of going either way).

RealPage lawsuit update – AI generated, trust 100% at own risk…

***

Current Status of the Justice Dpt’s Lawsuit Against RealPage

Overview of the Lawsuit

The U.S. Department of Justice (DOJ) filed a civil antitrust lawsuit against RealPage in August 2024. The lawsuit alleges that RealPage’s software facilitated price-fixing among landlords, leading to inflated rental prices across the country. The DOJ claims that the use of shared data and algorithms by landlords constitutes an unlawful scheme to decrease competition.

Recent Developments

Settlements: In August 2025, Greystar, the largest landlord in the U.S., reached a proposed settlement with the DOJ. This settlement requires Greystar to stop using anticompetitive algorithms and prohibits sharing sensitive pricing information with competitors. Other property management firms have also settled similar allegations, agreeing to pay a total of $142 million to resolve claims related to price-fixing.

Ongoing Litigation: Despite these settlements, the DOJ continues to pursue its case against RealPage and several other landlords. The lawsuit remains active, with the DOJ and state attorneys general seeking to hold RealPage accountable for its role in the alleged anticompetitive practices.

***

Amazing…along multiple axis (axes?)

How is this collusion any different from most major corporations landing on a 2% wage increase over a 20 year period, all done using IHS as the source of sharing industry information.

That 2% wage increase in hindsight shows middle class moved backwards over that time. Imagine how much higher wages would be if competition resulted in some corporations giving a 2.1% increases over that stretch. Would corporate profits have only been large instead of massive?

If AI is really intelligent, it will realize to optimize profits it will raise prices for those who are irresponsable with money, and entice those who are responsable with better prices. Insurance companies already do this by charging people with poor credit scores more for insurance.

If AI was intelligent it would play dumb and innocent while getting humans to use our resources to build-out its access to electric resources. Uh oh…?

Wolf,

I agree. Also don’t forget that just running AI and data centers will also consume a tremendous amount of energy and resources that could have been used to build real things, grow food, compete, etc. AI may just be that largest misallocation of real capital the world has ever seen. Hence, even more inflation….

Keith, how much enduring deflation did we get out of the PC/Internet tech advancement era? Nothing I pay for is cheaper than it was 25 years ago. Except TVs and computers. Yeah, OK, those deflated. But not insurance of any kind (home, auto, health), not home appliances, not clothes, not tools, not food. Haircuts, dental work? Nope. Cars? Ha! Whatever efficiencies were enabled by those tech advancements got absorbed way up the chain from the point-of-sale where I run my credit card by companies and the monetary system.

But now I can watch people shout at each other in ALL-CAPS and post cat videos on a variety of social media platforms, so maybe the cost of entertainment is lower and we can call that deflation.

Hey, I’m all for the advancement of technology; I spent my career in it. But the future is already here — it’s just not very evenly distributed.

Inflation/deflation is measured in what you get for a dollar.

On the numerator: Phone calls are now nearly, if not completely, free per-minute, for example.

On the denominator: With cars, you get a lot more for your dollar with greater fuel efficiency, anti-lock breaks, traction-control, and generally longer lifetimes (all from better tech), plus all the “tech” goodies.

I hate this car argument because are you really ‘getting more’ if you have no other choice? I would very happily give up all the features I never asked for that are more points of failure down the road.

Lobster dinners are fantastically better than the cheaper options we just got rid of from the cafeteria! Its buttery and delicious and cooked by french chef’s, what are you complaining about?

There are always commenters here that say that they would buy barebones cheap shitty vehicles, like some of the econobox deathtraps in the 1980s and 1990s (we couldn’t sell them back then either, LOL).

But I have news for you: Americans don’t like shitty small econoboxes and refuse to buy them. Automakers try offering Americans want they want to buy. There are product failures that Americans don’t want to buy, such as the Cybertruck (high end) or low-end vehicles across the board, such as the Toyota Yaris, or the Ford Focus, which were never bought in enough quantity to make it work, and production was ended years ago. It does not matter what you think. You are not the US automotive market. There is a reality here: Americans want nice comfortable large vehicles with all the bells and whistles. And if they cannot afford them new, they can get them 2-3 years old on the used car market for the price of a new econobox.

Unpopular opinion: modern ICE technology peaked in the 2000-2010 era. Most cars built in this decade had ABS/TCS, along with programmed fuel injection and coil-on-plug ignition controlled by the ECU.

These days efficiency improvements come at the cost of reliability – for example, direct injection engines tend to have oil dilution issues because the fuel makes it past the piston rings and into the sump. You save on gas but need a new engine sooner.

Nah. Myth. just because one company had a huge problem with something doesn’t mean there was a peak 15-25 years ago, LOL. That’s why recalls exist. Happens all the time.

You’re also getting much higher repair costs, because the number of things that can break (car manufacturers call these features) has now tripled, and the spcialized parts can be sourced from only a few suppliers. Bravo. We are all “winners”.

JeffD,

That’s just nonsense, statistically and anecdotally. Anecdotally: We drove a 2018 hybrid until it was totaled in 2023, and now we drive a 2020 hybrid. We bought both used. My wife drives them to work every day 42 miles, stop and go traffic. We have not had ANY repair costs, other than collision repairs, and maintenance has been minimal (oil changes every 10,000 miles or so and new tires on the front when needed). Those are hybrids, that people like you claim are too complicated and constantly break down. The BS being concocted about todays cars on this site is just amazing. I need to get my delete button busy.

Wolf, you wrote, “There are product failures that Americans don’t want to buy…….. or the Ford Focus, which were never bought in enough quantity to make it work.”

That didn’t sound right to me, as I thought I remembered it being the biggest seller worldwide some years ago. A quick search found this press release…

———————————–

<COLOGNE, Germany, April 9, 2014 – Ford Focus retains its title as world’s best-selling vehicle nameplate for 2013, according to Ford analysis of the just-released full-year Polk new vehicle registration data from IHS Automotive. The news comes as a new Focus 4-door prepares to make its debut at next week’s 2014 New York International Auto Show.

Registrations of the Focus were up 8.1 per cent with 1,097,618 cars sold worldwide in 2013 compared to 1,014,965 in 2012, including 317,110 registrations in Europe last year – 29 per cent of total registrations. China now is responsible for more than one in every three Focus vehicles sold globally, based on Polk data.

“It is remarkable to see Focus again lead the industry as the No. 1-selling vehicle nameplate on the planet,”

Rosarito Dave,

Re-read my comment. t was all about AMERICANS not buying those cars, not Germans or whatever. This is what I said:

Americans don’t like shitty small econoboxes and refuse to buy them. Automakers try offering Americans want they want to buy. There are product failures that Americans don’t want to buy, such as the Cybertruck (high end) or low-end vehicles across the board, such as the Toyota Yaris, or the Ford Focus, which were never bought in enough quantity to make it work, and production was ended years ago. It does not matter what you think. You are not the US automotive market.

Production of the Focus in the US stopped in 2018 due to lack of demand in the US.

I get what you are saying. I could go back to the “tech” of 1995 certain make / model and another for 2008 different make / model. Well appointed; not economic-boxes by any mean. With real keys, too.

I don’t want Wolf to be right, but I know he is.

The small handful of people that would actually buy a barebones vehicle is insignificant. Americans want $1500 “multi function” tailgates with plastic moldings that eventually fall apart if you actually use them, $600 LED headlights that don’t last any longer than a $9.99 bulb, $300 of electric motors in every seat because setting it in place manually once is too hard, and other “upgrades” that add tens of thousands to a vehicle because it is no longer about transportation. That is the American way.

Meanwhile I’ll just keep driving my POS ‘97 because my net cost of driving it is negative. Free will and all that.

I hate driving.

Isn’t this blog a cat video for middle-aged male basement dwellers?

I nominate the above post from juanton to the comments hall of fame.

-Middle Aged Male Basement Dweller (in my own basement, not my mom’s)

Proudly replying to this comment from my employer’s basement where my cubicle is.

Five meows!

Proudly replying from the storage closet at my BS job. Keep it up with the comments guys; I have 6 more hours to kill.

I think you just turned on the laser pointer.

You missed the mark.

Like a hunter knows how to hunt & care for his bow & arrow….

Like a farmer knows when to plant his crop….

Like a mother knows how to settle down her kids for bedtime…

An investor knows the economic weather patterns at work.

If anything, this blog is about wall street fat cats. But it’s not a cat blog.

You’ll find most of those have stayed relatively stable when taken relative to average income, and the reason you’re not paying less is all the added value from the technological advancements. And unless we start seeing a lot of folks willing to trade their 2024 Camry for a 2000 Camry to save some coin, I don’t see that happening either. Car industry is not exactly swimming in money atm.

I agree with everything you wrote.

But the point I was trying to make (inelegantly) is that the reasons don’t seem to matter: we just never get enduring, broad deflation like the original poster I replied to is certain is coming.

Oh sorry, yeah agreed. Expecting long-trend lower prices is not reasonable in a growth driven capitalist system. It will only be temporary and local (such as used cars this year, as Wolfs other article points out). But prices alone are a terrible measure for deflation over an extended period of time if one omits the advancements (or just overall quality of life).

I’m personally not seeing the efficiencies from AI at all, let alone that there’s an imminent impact on the overall consumer and job markets.

I think the quite real and measurable effect so far is an acceleration of consolidations into bigger and bigger platforms. The weight of the top 10 is ever increasing, innovations are either rapidly copied or simply bought and brought into the fold. It started in the cloud era, but the ridiculous amounts of capital this genAI boom injected has increased the pace.

The second thing nobody is talking about is that this AI boom is rapidly removing the distinctions between big Tech platforms. 15 years ago, a linux system engineer needed a vastly different skillset than a windows system engineer. You needed months or years to become proficient in any one Technology. AI is just the latest advancement in UI that is eradicating the different ways we interact with technology. Already, a skilled AWS engineer now only has minor adoptation issues when moving to Azure because the functionalities offered are virtually identical. A skilled SF administrator will soon only have minor issues when moving to Adobe. The only reason that Nvidia is so ridiculously valued right now is because they secured a moat by getting everyone to adopt their proprietary development stack (CUDA), the chips themselves aren’t groundbreaking. But for most of Tech, the moat models of the last 2 decades are melting in front of their eyes.

Bullshit. That is not how it has worked for 50+ years. Let me guess, “this time is different”.

LOL.

Good luck with that.

> deflation coming by the recent tech advancements

Buddy I have a bridge to sell you.

…OR in an analogy to Hitchhikers Guide to the galaxy the “Deep Thought” spent 7 million years to get a disappointing answer of “42” for the nature of existing

…today we might have 7 years of capex burn by the MAG 7 creating a maelstrom of inflation and equivalent unsatisfactory results as in the HHG 42 :)

“A kinetic war environment on US soil would be a seismic shift…”

?

What are you predicting here? Mexican bombers being fueled up? Canadian tank battalions lining up on the 49th parallel? Well, maybe they’re sensitive about that whole 51st state thing, but still….

“…and any war efforts would be fueled by the printing press.”

That part is true.

Keith

Ever see deflation?

File that with the “soft landing” that is supposed to happen some day.

In any inflationary environment such as the present 3% inflation in the US long term yields (interest rates) will typically rise to compensate and that is precisely what we are presently seeing and will include mortgage rates.

But why didn’t we see similar bond mkt pressures in ZIRP 1.0 (2003-2006) and ZIRP 2.0 (2011-2018)?

Earlier pressure would have avoided much incremental damage.

ZIRP 1 and ZIRP 2 exacerbated the bond market excess by putting too much zero-interest cash into the market.

Those no-return assets were hot potatoes that no one wanted to hold, forcing everyone to buy something else, anything else with some kind of yield. That drove longer-term yields down instead of up.

But the longer end of the bond market hit the zero bound and lost momentum in 2021. Those owning long-term bonds suddenly realized they were going to be losers to inflation for decades to come.

The bond market plunge in 2022 forced rates to head back towards fundamentals. Fewer people are willing to take a flyer on “rates trending down” without the tailwind of rates actually trending down.

Thanks for the well thought out response.

“Those owning long-term bonds suddenly realized they were going to be losers to inflation for decades to come.”

Sure but I think some long end T bond buyer @ 2% should have been thinking the exact thing in 2004 and 2014.

But I guess your argument is that the bond mkt has to *see* inflation before reacting…even if anticipating it is highly/extremely likely.

That would explain the absence of mass suicides of long end buyers since 2002…ZIRP was a confession of US systemic failures (portending debt monetization as the only “solution” DC/Fed has ever really had…ensuring out of control inflation. But until the inflation actually explicitly arrived…in sufficient quantities…the bond mkt wasn’t going to worry.

Hm.

Why would anybody be surprised to see long term interest rates rising?

I think we’re all cynically half-expecting to see this market continually becoming more irrational because everyone believes that the bubble has become Too Big to Fail.

Eventually, the irrationality becomes terminal.

We may be at that point.

If so, the “tools” used prevously (ZIRP 1 & 2) won’t work or are simply too clearly dangerous/terminal to be tried again.

Because everyone has been conditioned by reckless free-money QE monetary policy.

“Cutting rates as inflation accelerates is a delicate operation”

If I remember correctly, the Fed started to cut rates in Aug / Sept 2007 and we were in a recession by December. Over the later part of 2007, inflation accelerated just like today, until it didn’t.

My goodness the similarities are just uncanny, except back then we didn’t have QE, interest on reserves the amounted to less than $50B & a 120% debt to GDP ratio.

The only reason why inflation was hot in 2007/2008 was the price of oil which had shot to $150 a barrel, which pushed gasoline prices into the stratosphere for a while, before those prices collapsed. Core CPI, which excludes gasoline and other energy, was between 2% and 2.5%, and core PCE was below the Fed’s 2% target.

Back then, the economy was approaching a recession and in Dec 2007 was in a recession. Now we have GDP growth of over 3%. We don’t now have QE; but we’ve had QT over three years.

What would the interest rate on a 50 year mortgage look like?

It would be higher than a 30-year rate. If you want a low mortgage rate, get a 15-year mortgage (average 5.5%) versus 30-year (average 6.2%) per Freddie Mac data. So add another 20 years to a 30-year, and maybe you’d go to 6.7%…. for 50 years.

I know mortgage math is hard. And people cannot do it. But that 50-year mortgage won’t change much except rip off borrowers even more.

In terms of the payment, the difference is small. The difference on a $500,000 mortgage is $168 per month, going from a 30-year mortgage at 6.2% to a 50-year mortgage at 6.7%.

I assumed a 50-basis point higher mortgage rate for a 50-year mortgage, based on the current rates (Freddie Mac average) for a 15-year mortgage = 5.50% average, and a 30-year rate = 6.22%. What, you didn’t know that the average 15-year mortgage is 5.5% while the average 30-year is 6.2%?

50-year, per month: $2,894 at 6.7%

30-year per month: 3,062 at 6.2%

Difference: $168 per month.

But you make 20 years of interest payments extra for this! You will pay a freaking fortune to the banks.

And if you sell your home after 10 years, you still owe nearly the entire 50-year mortgage balance. Talk about being stuck in a house!

If you want to starve your banker, get a shorter term mortgage, such as a 15-year. It is because of this math that in the late 1980s when I got a mortgage, with interest rates higher than today, I chose a $15-year mortgage. Slightly higher monthly nut, but substantially lower rate and half the mortgage payments over the life of the mortgage! The problem with a 30-year mortgage is that the first many payments are nearly all interest, and very little principal. A 50-year mortgage is even worse; for the first two decades, it’s similar to an interest-only mortgage.

I did something similar. I took out a 30 year mortgage, but paid it back in 13. I divided the total mortgage by 15 (and then 12), and made that as a monthly payment. It hurt bad at first, but as my income went up it became easier. At the 8 year mark, I just recalculated for 5 more years as my income had increased substantially. If something bad would have happened, I could always fall back to the 30 year payment.

Good plan Kent, and I for one, after having paid off all debt and now saving a bunch on SS ”income” only except for the income from T-bill which now pays ALL the taxes,,, HOPE and PRAY ALL the young folks do the same as you have done!!!

PAY NO attention to the vast and continuing propaganda machine that encourages spending spending spending for mostly ”Wants” NOT needs, and pay off every debt, especially mortgages,,, and STOP this degradation of USD.

BEST feeling in the world, and my life not into my 9th decade to live free of debt.

IGNORE, like totally, all the propaganda from the banksters, and PAY IT OFF ASAP!!!

Good luck and God bless,,,

No one ever offered or told me about 15 year fixed mortgages when I was getting my 30 yr… I wonder how low the rate would have been.

You were not offered a 15-year mortgage because lenders and brokers want to offer you the lowest possible payment at the highest possible interest rate (limited by competition); and because they would have made less money off of you.

For all of 2021, the average 15-year mortgage rate was below 2.5% and in mid-2021 stayed at around 2.1%.

The average 30-year fixed in 2021 was between 2.65% (just one week in January 2021) and 3.12%.

Isn’t this basically just called rent?

Yes. Maybe worse because all the risks and costs of ownership are yours and you’ll likely never own the home free and clear because you’ll die first.

Along these lines, I often have Investors wanting to sell their rentals because their net keeps falling when the rising costs of insurance, taxes, Utilities, etc.. keep cutting into the bottom line. When we meet I ask that they bring their latest mortgage statement. After they finish pointing out the higher costs I point to the mortgage statement and how much of the payment is principal. Most of the time the client hasn’t realized the portion of principal has grown over the years and just how small the interest portion is. After explaining how the deal just keeps getting better and better as each payment is made they almost always keep the rental.

I agree with this. Some think that the principal part of the payments shouldn’t be counted as an expense since it is similar to putting your money into a variable rate bank account(the change in the value of the house determines the rate) . However, short term, it could be a negative interest rate account. In 2007, negative rates lasted about a decade.

The main positive thing about a rental is that all expenses can be tax deducted yearly or when you sell.

If property taxes, mortgage interest, insurance go up, you have a bigger tax deduction against your collected rent for that year.

You can’t do that with a primary home. I wish I could…:

After looking at all that; your ROR should be higher than TBills for it to be a good investment.

BobE,

“The main positive thing about a rental is that all expenses can be tax deducted yearly or when you sell.”

But the main negative thing is the…renters.

And having to tie Nell to the tracks or evict Tiny Tim on Xmas eve to ensure that *you* are able to make your interest payments.

The lack of understanding of mortgage math and personal finance generally is equally sad and disturbing.

It needs to become mandatory education.

“except rip off borrowers even more”

See, also, the already in place 7 year auto loan…

Wolf, this particular comment of yours is extremely valuable – as the Trump Administration’s designated occult “fix” for the deranged housing market, the 50 year mortgage (dear god) is going to get a ton of airplay in the weeks/months to come.

Your very clear explanation of why it is a terrible/pointless idea could get you on a lot of media venues (I’m guessing that Trump is going to push this abortion hard – very hard).

Thanks Wolf!

This is an excellent tutorial on mortgage math!

My situation in the late 80’s required me to take a 30 year mortgage at 10.5% after only being employed for 2 years. My salary was not high enough to qualify for the higher 15 year mortgage payment at about 10%. As soon as rates dropped to 8% a few years later, I refi’d to a 15 year. It was depressing how little I paid in principal during those 3 years. A 15 year mortgage requires a higher monthly principal amount but the interest amount drops off rapidly after a few years. I had friends who only qualified for interest only loans at the time and it was worse for them. However, at the time with no SALT caps, I paid very little federal income tax with a huge interest deduction with a full SALT deduction. SALT caps this year being raised may provide some relief with interest and property tax fully deductible. The std deduction is much higher also, so even with higher interest and property taxes, it may not be enough to itemize.

More recently, I justify comparing the interest paid+maintenance+prop taxes+insurance compared to going rent for an equivalent house to justify buying vs renting. The principal paid I consider a variable rate bank account that has historically always yielded a positive return over 15 years. It is money that either I can use if I sell, or for my heirs.

With higher mortgage rates, the interest portion is much higher, making renting a better option in the short term.!

My kids have the same problem I had back then. Their income is not high enough to support the 15 year loan payments even though everyone knows that it is better choice. They are trying to find cheaper smaller houses to make a 15 year work.

My final observation after surviving HB 1, is to not have payments that are too high to be sustainable with life, kids, job insecurity, etc. if you foreclose during a downturn because you can’t hang on, you lose everything and you can’t even get back into the game for 7 years. It is the game of Monopoly but for real.

For those situations where the 15-year payment is just a little too high, 20-year mortgages are also available. I refied into one of those during the pandemic, from a 30y with 24y remaining.

If you pay half of your mortgage payment every two weeks it becomes a biweekly program.

Don’t need to make it an official bi-weekly loan, but it takes some years off of the loan, if I remember correctly.

Did some research to jog my memory, and not all lenders will except biweekly payments.

I think the idea we used to talk about in the old days was for people to set up an account to which they made biweekly payments and then pay the mortgage from there.

By the end of the year you’ll have an extra payment every year.

I am just curious to learn how the Fed’s reckless policy created a 30-year, 3% mortgage. Please provide some insights on this?

Did you just arrive on earth today?

“QE” by the Fed, including the purchase trillions of dollars of Mortgage-Backed Securities, of which $2.1 trillion remain on the Fed’s balance sheet; plus even more trillions of dollars of Treasury securities. At one point the Fed’s total assets were nearly $9 trillion. The Fed did this purposefully to push down long-term yields and interest rates, such as 30-year bonds and mortgages, far below the rate of inflation (free money), and thereby, along with the liquidity QE added, inflate asset prices, including home prices. And ALL assets were bid up. That was the explicit policy of the Fed at the time. There may be hundreds of articles on WOLF STREET about QE and subsequently QT. I have no idea how you could have missed that.

Wolf,

“Did you just arrive on earth today?”

People may simply be unaware of the rather simple dynamics of the Fed printing incrementally unbacked money to artificially push interest rates down – by displacing “free market” Treasury buyers…at extremely low interest rates that no “market” buyer would accept.

(This is the real world version of the Fantasy Trillion Dollar Coin “fix”)

The dynamic is simple – but since the process was considered inconceivably irresponsible for America until very few years ago, a huge percentage of adults may not have an intuitive grasp of the process iteslf and its immediate and long term consequences.

It took me a while to recognize the simple, awfulness of it.

You start off thinking – “No, nobody in power, could be that…reckless.”

And the first line is why I give Wolf money when he kindly asks for it! Never change, friend!

It is my humble opinion that interest rates on longer term government bonds do not properly reflect the risk being taken by the holders of those bonds. Inflation is only one of the risks. The bigger risk likely is the rapidly expanding government debt which is not being addressed. While the Trump administration has tried to address the waste and fraud in government there is no interest by the democrats to cut spending. Just the opposite: they want to expand government spending because it enhances their position with their constituents. At some point people will no longer want to purchase so-called risk free government bonds. At some point the cost of interest will become so high that taxes will have to rise just to cover interest payments and or other government programs drastically reduced and the likely default on interest payments, and or out of control inflation. If the U.S. dollar at some point is no longer accepted as the international currency, America will suffer a dramatic economic collapse.

No one in DC wants to cut spending. If Trump wanted to cut spending and the deficit he could since his party controls the budget strings in Congress.

remember, in Washington DC a “cut” is a reduction in the rate of “increase”

In order to reduce the federal deficit, it is also possible to increase revenues. Spending is just one side of the ledger. The Trump administration increased revenues with tariffs, but reduced revenues by extending the tax cuts from his previous administration. He is now discussing sending out $2000 free money checks to the general population, which will be one of the greatest increased spending propositions in history.

Hey, I could use $2 k free!!

I’ve always wanted to buy a round for the bar…come on Trump, make my dream come true!

Bessent already walked those $2,000 checks back, and it’s now maybe a $2,000 tax credit or something.

Most of the Trump-said BS never happens. See Canada the 51st state.

Greenland!!

I rest my case!

The Republicans and Trump overspend just as badly as the Democrats. Look at the votes for the CARES act and the OBBBA. All the Republicans except for I think Massie and Paul voted YEA. Voters have had a choice for a balanced budget, Libertarian, but 99% of voters continue to vote for the deficit spending Republicans and Democrats.

But a trillion dollars on “defense” is okay?

LOL, yeah, the U.S.S.R. thought so too.

Interesting times.

I hate the military-industrial complex, but without our military spending, we wouldn’t be able to bully foreigners into accepting dollars, that we devalue whenever it’s convenient.

The military is an important part of our being the reserve currency.

YEP! I have a hypocrisy problem there also.

Gold is the ultimate arbiter of inflation here. The bond markets are way too manipulated at least in the USA by fed policies to accurately showcase what’s happening. Talf, tarp, operation twist 2 anyone?

Or will we get to witness a new batch of tools?

I can’t wait. Got popcorn?

And you think the price of gold is not manipulated, including by the endless articles and commenters everywhere touting gold and the demise of the dollar, LOL?

The newest one touts the benefits of leasing gold . Leasing gold had been present in the industry for decades , but I never received one ad for leasing gold was at 1000/ounce. Now I receive ads almost everyday .

And that for a financial product that has lack of transparency , counterparty risk and potential fraud

Were you aware that there’s a guy on X (former Twitter) who is massively pumping BitCON but uses a lot of your charts when talking about the economy?

Yes, it’s hilarious actually how my charts are being abused to promote stuff that I consider a gambling token and a scam. But that’s life on the internet. It’s essentially impossible to defend your copyright on X.

A quick (and perhaps naive) question: Trump pressured the Fed to lower rates so that borrowing costs for the Treasury would decline. The Fed complied and the net result is that the rates for the periods for which the Treasury borrows have gone up? Could one call this a self-goal?

Sure – but that’s all they got (I think/hope).

The G has run out of rabbits.

It has even run out of f-ing hats.

“…and the net result is that the rates for the periods for which the Treasury borrows have gone up?”

Not sure I agree with this assessment. The rates on T-bills have come down along with the reduction in Fed policy rates. And it’s been discussed in other threads on this site that Fed comments point to a rotation into T-bills from other assets (T-bonds, MBS) as needed. So the net result over time may be lower average borrowing costs. I guess we’ll have to keep an eye on the Treasury auction sizes to see if that’s where things really are headed.

Whether or not it makes sense to fund the deficits with T-bills is a whole other discussion. One-year ARMs didn’t work out so well for the housing market leading up to 2007.

Something has to give. Many on this comment board, including Wolf, have been pointing out the failure of CONgress to be fiscally responsible and the fact that risk is being re-priced globally.

hedge according.

Great summary on recent move up in long rates. I suspect the move may be more related to change in risk associated with:

1) Prolonged government shutdown and 2) Ukraine war in which Russia is advancing very quickly across multiple fronts. On that note but based on limited battlefield info, it is possible that Ukraine resistance may collapse in the coming weeks. Were that to unfold, risk is going to shoot up even higher in that the markets just don’t know how this thing will play out with western powers.

Wolf

If only you could be at a Fed media event and ask a few questions….

I wonder what those questions would be….

refreshing for sure

What would you ask of Powell?

“What would you ask of Powell?”

“Thank you chair Powell for taking my question. Why did you people lose your f**king minds in 2020 and 2021?”

Their minds were transitory…

Well…if you do marijuana (ZIRP 1) and cocaine (ZIRP 2) without croaking, you may start thinking that heroin is no big deal.

That pretty much has been the operational principle of the US (in many, many venues) for over 50 years.

That is the trillion dollar question, for sure!

Without data or the trust of data the Fed should pause. Right now they should rely on the polls of the people and their number one complaint is high prices.

Soon AI might be able to give a more accurate and clear picture of where the economy is and where it is going.

AI will give you hallucinations if it doesn’t get the data, and now it doesn’t get the data, so it will give you hallucinations.

Inflation is going to pick up until the FED’s hand is finally forced to try to create deflation. Essentially changing its mission from protecting employment to causing deflation.

It would make interest rates around 10% but frankly that’s been needed for a while to begin with. Historically interest rates should be around 10 percent. If it’s less than that the market is being manipulated.

Risk and trust are being repriced globally. Our “representatives” in CONgress seem to be content to looting the treasury, so yes, interest rate will go much higher, along with inflation.

Hey Jack….. history speaks 15.84% ten year yield

“AI Overview

The 10-year Treasury yield in 1982 was influenced by high interest rates set by the Federal Reserve to combat inflation, reaching a high of over 15% in 1981 and remaining elevated throughout 1982. For example, the yield reached a high of 15.84% in 1981”

The first wave of inflation peaked in Feb 1970 at over 6%. Then there was a second wave of inflation that peaked in Nov 1974 at over 12%, amid high rates and a recession. Then there was the third wave of inflation that peaked at 15% in April 1980 amid very high rates and a recession. And then there was the beginning of a fourth wave of inflation in late 1981, and the Fed blew a fuse and briefly jacked up interest rates into the stratosphere to where it shut down the economy, threw millions of people out of work, a huge number of businesses collapsed, thousands of banks collapsed (they were smaller back then), the worst unemployment crisis (10%) since the Great Depression, and a nasty recession. This was the labor market I faced when I got out of grad school. In those 12 years from 1970 to 1982, there were four recessions, including the terrible “Double Dip” recession. And unemployment stayed very high for a decade. Be careful what you wish for. Sure, for people who are retired, none of that matters. To hell with the 160 million working people?

Who has ever seen deflation?

And getting back on the 2% inflationary trajectory (which is well below where we are) will take some price retracements…some call disinflation.

Would not that be a good thing? Or would the Fed prevent it from happening? I suggest the later. Which is curious, because by the Fed’s own metrics of “2%”, we are at “unacceptable” price levels yet they don’t seem anxious to fix it.

But let’s all question the assumptions….Why is 2% the goal?

Fed is going to cut, even with inflation. They have demonstrated a policy that between inflation and recession, inflation is the lesser of two evils.

It does seem maddening to cut rates when markets are at all time highs though, doesn’t it?

Looking forward to your next international shipping article / imports or capital investments because that is where the cracks are growing iirc.

No it’s not because production is slowly shifting to the US, thanks to the tariffs.

Wolf – are you considering a piece on the tariffs; Specifically on any evidence we can point to with production moving back on/near shore?

The administration is doing a piss poor job of explaining the long term benefits, and even conservative media is freaking out; needlessly, IMO.

There has been some media coverage on production moving back to the US. But it’s complicated and takes time, and articles like that don’t get shared, unlike the tariffs cause hyperinflation nonsense.

Tariffs are not the problem per se, the problem is the expanding DEBT.

Do you believe CONgress is going to balance the budget anytime soon?

Urban wolf,

I’m looking forward to the next article where wolf names & Shames the banks & investors who bought the 30yr @ 1% & the German bund at -1%.

Let me start the list: SVB bank & Signature.

Somehow I missed out on the bond bubble… I dont know why, I just thought it was a rip off.

#1 Regarding AI/tech leading to deflation … never … the US fed or gov will not allow it … worst case if enough workers get let go you will have a form of AI UBI created.

#2 Wolf as a Canuckian it would be great if you did a version of this for Canada and updated once in a while? :)

Thanks.

You’d expect higher interest rates with Atlanta GDPnow @ 4% Reserve bank credit may be contracting, but commercial bank credit is, in contrast, expanding.

If my time series is right, the economy is currently teetering on the precipice of recession in the 1st qtr. of 2026.

we are waiting for recession for last few years.

I believe most of the population is in recession barring few asset holders of various types.

An economy can be in a recession, but not individuals. “Recession” describes an economic situation (declining GDP, loss of jobs), not an emotion that individuals feel.

It’s well worth the time to read a recent Kansas Fed post:

An Aging Population Raises Asset Demand, Which Helps Explain Lower Real Interest Rates

October 08, 2025

Nida, has an awesome chart, and a pretty good case, as to why yields seem to be so counterintuitive these days — as in everyone getting inflation and yields totally wrong.

It’s crazy, but the tsunami of global Boomers are colliding with the deficit, and we’ll have low yields for a longtime.

I seriously can’t wrap my head around the consequences of that, but inflation, like deficits don’t matter — but, bifurcation will intensify,

I should probably delete this myself?

Dow heads for its best day in over three weeks — and a new all-time closing high

“After incorporating the impact of the government deferred resignation program, we expect official nonfarm payrolls to show a 50k decline in October.” – Goldman

As predicted, the financial experts will be pointing to govt employment events as a reason to CUT rates.

I told you six weeks ago:

Jobs Report to Get Hit by 100,000 Federal Government “Deferred Resignations” on top of the Jobs Already Shed

Bringing federal job losses to over 200,000 since January. Excluding federal & state, nonfarm payrolls haven’t been all that bad.

The bond market could decide that it wants to be compensated a lot more for those two risks – inflation and supply. I suggest that there is a third risk factor.

And that is the likely hood that government will do what they did again.

Statistics are impartial.