The new & improved SRF begins to serve its purpose of allowing the Fed to push QT as far as possible without blowing anything up, unlike last time.

By Wolf Richter for WOLF STREET.

That banks are starting to use the Fed’s Standing Repo Facility (SRF) occasionally and with relatively small amounts has in recent days been twisted into headlines about banks facing a funding crisis and running out of cash or whatever.

A primary purpose of the SRF is for banks to step into the repo market when repo market rates rise enough above the Fed’s policy rate for repos, 4.25% since the rate cut. Banks borrow at the SRF’s policy rate of 4.25%, and lend those amounts to the repo market at the higher rates in the market, and make money on the spread. This douses the brushfires in the repo market before they get big.

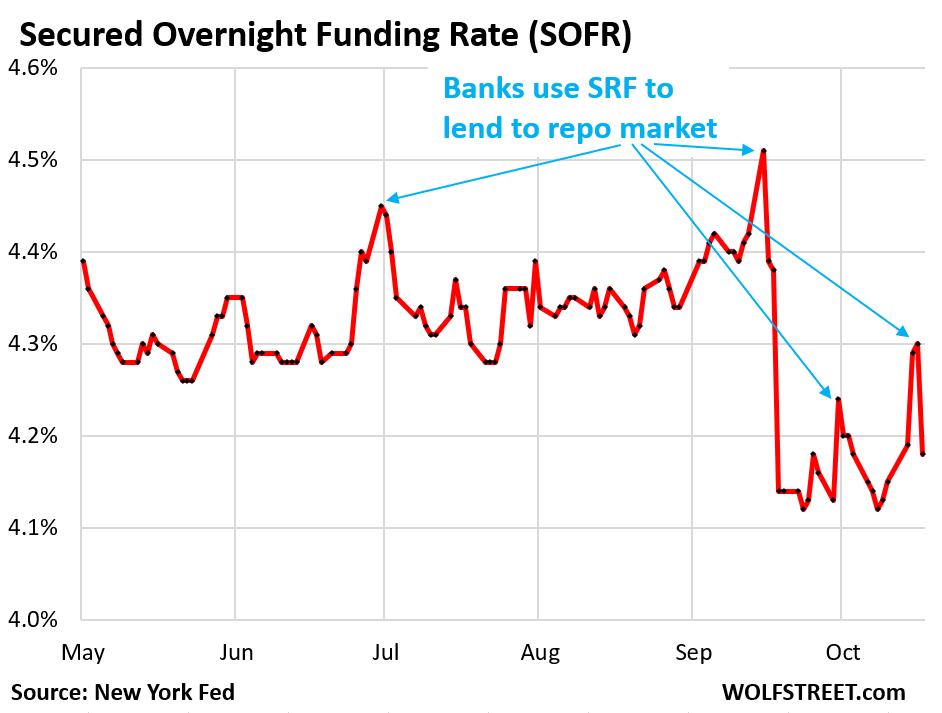

Last week, the Secured Overnight Funding Rate (SOFR), which tracks a $3-trillion-a-day segment of the repo market, had risen intraday as high as 4.39% on Wednesday and 4.41% on Thursday, with the average SOFR at 4.29% and 4.30% on those days, and some banks jumped in, borrowed at 4.25% at the SRF and lent overnight to the repo market at the higher rates that they could get there, and made some easy risk-free profits.

It had the desired effect. By Friday, the majority of the trades were below 4.20%, and the average SOFR was 4.18%, and the banks did not borrow from the SRF on Friday to lend to the repo market, and the SRF balance reverted to zero.

Today, repo trading is still going on, and the SOFR rates haven’t been released yet.

Repo market rates fluctuate quite a bit now that the Fed’s QT has wrung $2.4 trillion in excess liquidity out of the market. And the SRF activity when banks stepped into the repo market matches the high points of SOFR. The chart shows the final repo rates for each day, as released by the New York Fed, not the intraday highs:

The repos at the SRF are overnight repos that mature the next business day, when banks pay back to the SRF the amount they borrowed and get their collateral back. They don’t stick on the Fed’s balance sheet for years or decades, unlike QE bonds. Which is why the balance of the SRF goes to zero on days when it is not used. Which is exactly what happened on Friday.

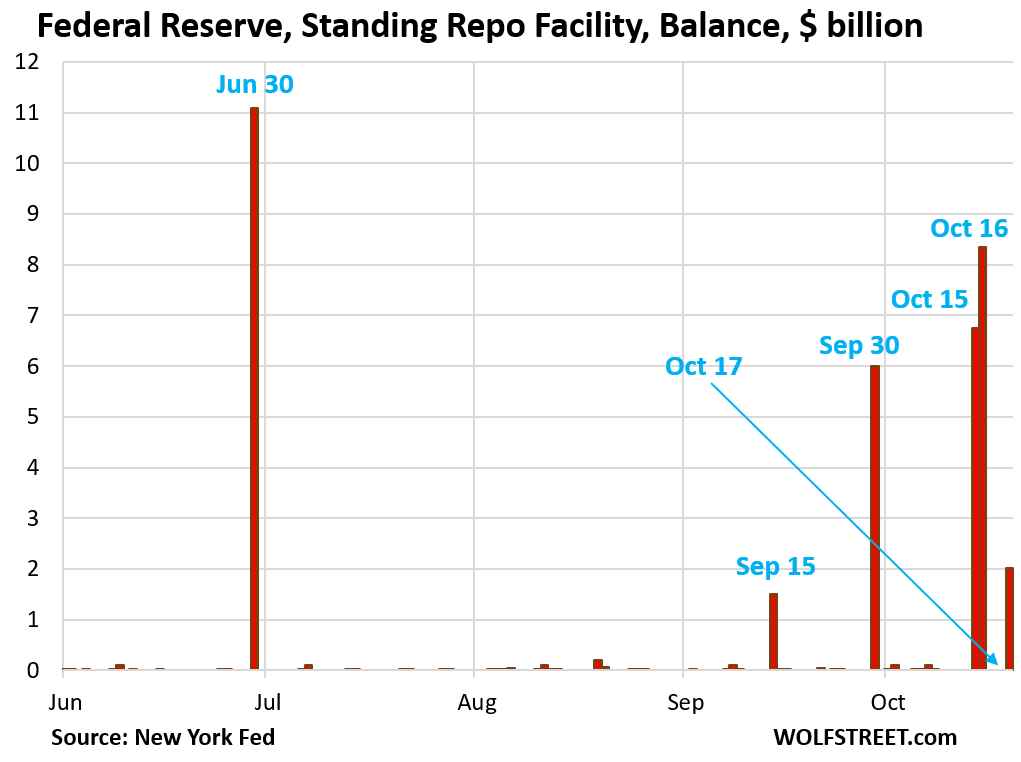

On Wednesday and Thursday last week, repo rates had risen to the point that it was profitable for banks to borrow at the SRF at 4.25% and lend to the repo markets at higher rates and make money on the spread, and this lending to the repo market helped repo market rates to calm down. On Wednesday, the uptake at the SRF was $6.75 billion and Thursday $8.35 billion.

On Friday, the balance was back to zero and there was no activity at the SRF.

At the auction this morning (Oct 20), there was no activity. At the auction this afternoon, $2 billion were drawn and the total balance today ended at $2 billion:

The purpose of the SRF is to prevent repo market rates from blowing out again, as they had done in September 2019, which had caused the Fed to step directly into the repo market, undoing a big part of the QT it had done over the prior two years. And it learned a big lesson.

In July 2021, in preparation for withdrawing liquidity through QT, the Fed re-established its Standing Repo Facility that it had shut down in 2009, and that it then didn’t have in September 2019.

The banks are using the SRF exactly how the Fed has long exhorted banks to use it: to keep a lid on the interest rates in the vast repo market. If the SRF had been in place in the fall of 2019, the few brushfires would have been doused before they exploded into a firestorm.

The Fed has improved the SRF this year, including by adding a morning auction, so now there is a morning auction and an afternoon auction to match the daily liquidity flows of the markets.

The new and improved SRF has now begun to serve its purpose of allowing the Fed to push QT as far as possible without blowing anything up. And it has been praised as such in Fed communications.

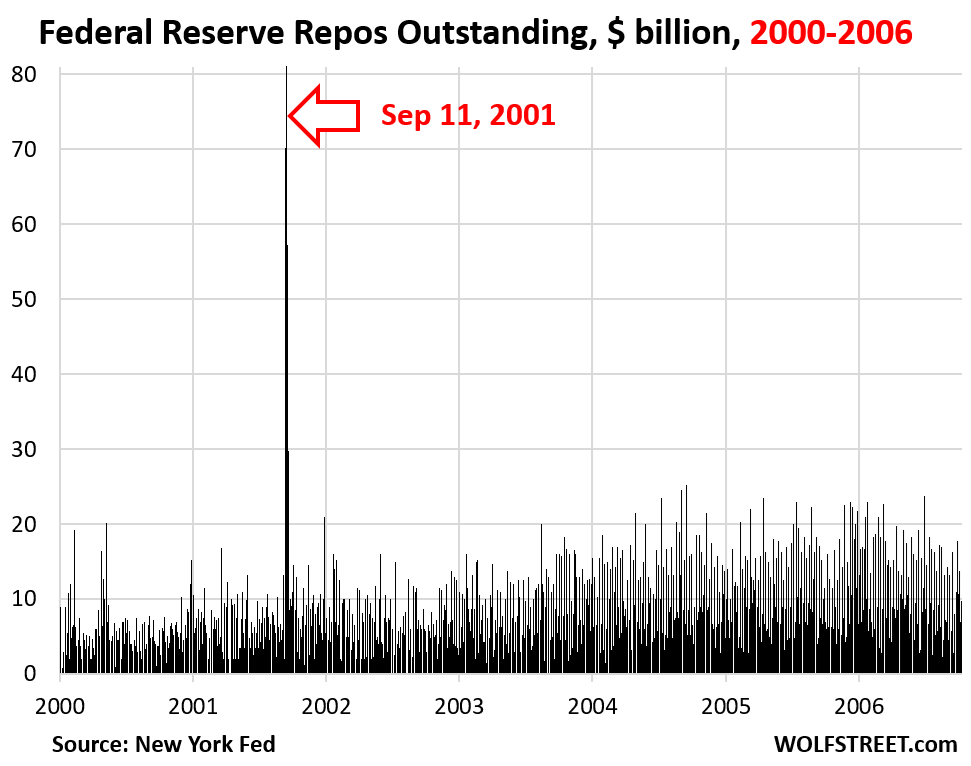

In the days before 2009, before the Fed inflated its balance sheet with QE, the SRF was constantly in use, and when a market problem arose, such as in the days following September 11, 2001, as markets were shut down because some of the infrastructure for electronic trading had been destroyed, banks used the SRF to provide liquidity to the markets, and within two weeks, as liquidity flows had normalized, the repo balance was back to normal, no QE needed:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

What’s the net effect of the SRF? It seems that it adds more liquidity and will inevitably be abused.

The net effect is that QT can go on for longer, and has continued to go on.

There is zero liquidity added on days when the SRF is zero, such as on Monday, Tuesday, and Friday last week. The liquidity it added on Wednesday and Thursday was removed again on Friday.

The line goes up and to the right.

https://fred.stlouisfed.org/series/SOFRVOL

And that is tightening???

That’s overnight financing VOLUME, now at $3 trillion. Note that it’s just a shift of funding as the Fed’s overnight reverse repos were drained. The increase in volume started rising from about $1 trillion after QT started as more funding shifted to the repo market while the Fed’s ON RRPs were drained ultimately by $2.4 trillion, which is why repo market volume rose by over $2 trillion over this period.

Don’t overthink this and always remember eCONomics is a SOCIAL “science”…

As Wolf points out “ON RRPs were drained ultimately by $2.4 trillion, which is why repo market volume rose by over $2 trillion over this period.”

So it appears the Fed is indeed always there to provide the necessary “grease” to keep the gears turning in financial markets.

I think the larger, more important, question is how much the financial markets and the stonk market really matter to the actual “boots on the ground” in the real productive economy. What is happening in American agriculture is a point of concern IMO.

Interesting times…

without looking at the details, I speculate that this is what Fed does to help banks escape the worst fate of gambling. Maybe there will be some ill effect in longer term but in short term, this is just to lubricate inter-banking businesses. At some point though, whatever warts that led this mini-panic will cause major problems.

No activity at the SRF today (Wed.), neither at the morning auction nor at the afternoon auction. The SRF balance is back to zero. That’s how it is supposed to work.

How does zero liquidity on one day remove liquidity added on previous days?

Learn what overnight repos are.

They’re rolling $5B off per month. Let’s not be cute about this. It’d take them 1200 months at this rate to get that balance sheet back into any responsible level.

This isn’t really QT. This is just printing money at a rather slow pace (as they are of course still buying tens of billions in US Debt every month).

Ignorant stupid BS. Last month, they rolled of $21 billion of MBS ($17 billion) and Treasury securities ($4 billion).

read this:

https://wolfstreet.com/2025/10/02/fed-balance-sheet-qt-15-billion-in-september-2-38-trillion-from-peak-to-6-59-trillion/

Designed to prevent a 2019 repo spike…The interesting thing right now is that the Fed has this liquidity framework–1. Abundant 2. Ample 3. Scarce. They rolled out this tool that was designed to warn when the risk of a 2019 repo spike was likely. It has utterly failed. It is caalled Reserve Demand Elasticity (50%). When designed post 2019 it seemed to fit the data perfectly, but recently as these liquidity issues have shown unwanted spikes, it has not done its job. For me the best things to watch are either reserves to bank liabilitues (12% level is a threshold) or Waller’s simple on which is bank reserves to nominal GDP (10% is the number to watch there, and we are there)

Did you mean to say that “QT can go on for longer”?

Yes, thanks.

Lots depends upon the distribution of bank reserves in the system.

“Concerns have been raised about the concentration of reserve balances among a few large banks, particularly following rounds of quantitative easing (three addressing the 2008 financial crisis and one addressing the COVID-19 pandemic). These programs injected substantial reserve balances into the banking system to finance the Fed’s purchase of government securities, potentially amplifying concentration concerns.”

“Note that banks’ excess reserve balances can be negative.”

A few individual insufficient liquidity buffers can distort the whole picture.

The 4.25% number caught my eye. When I was at my Credit Union today they had a large sign in the lobby advertising their interest rate paid on checking accounts was 4.25%.

I wonder if this is related to what the Fed was paying ??

It reflects the upper end of the Fed’s policy rates. It’s pretty good. Money market funds are now about 4.0%. The one-month Treasury yield is 4.02%. CD offerings are all over the place, but 4.25% is good for anything short-term, especially checking accounts.

It’s now extremely rare to find a report of something the government did working exactly as intended. I guess it just doesn’t draw in the clicks.

Just imagine what would have happened on 9/11 without the SRF.

So thanks for adding that balance and educating us, Wolf.

Beginning with Black Monday it was called the Greenspan put.

I think you mean QT can go on for longer?

It can, for sure. I don’t know for how long it will go on. But the thing is, it CAN go on. Last time, it couldn’t because the $5-trillion-a-day repo market was staring to lock up.

The SRF is one massive penny placed in the circuit breaker box… not an individual breaker, but the main breaker.

Sure QT can continue and the distortions can be covered a little longer, but then we know how this ends.

The SRF is doing exactly that for what they introduced, and when some “analysts” decalare the repo facility usage with small amounts as problem, they didnt understand the system. Liquidity facilities are in my view the better way in comparsion to the heavy expanding balance sheet through QE.

God forbid we let the market work. Oh no, we’re still suppressing interest rates by giving free money ( the spread) to the banks when it goes above our centrally planned number. This whole liquidity argument is nonsense. There is plenty of money available, just not at that price. The market says (on those days), there is more risk, we want more return, but instead our centrally planned economy overlords said “no, no more return for you”.

Good thing all these centrally planned economies have always worked out so well.

The repo market is not to be trifled with because it’s a $5-trillion-a-day market where funding occurs. Companies borrow in the repo market short-term (overnight) and lend/invest long-term, which is inherently risky. If they cannot borrow that amount every day because the market locks up (market not functioning), which it started to in 2019, then there are trillions of dollars of funding that might not take place, and all kinds of stuff starts to implode in a chain reaction. It would be like a huge run on the bank. I know that some people here would love to see that.

An argument can be made that such a market should not exist because it’s too risky without backstop, like banks are too risky without backstop. But that’s an argument we should probably have had 100 years ago, not now.

“But that’s an argument we should probably have had 100 years ago, not now.”

“One might expect that those in charge of banking policy in the United States would celebrate the concept of a “narrow bank.” A narrow bank takes deposits and invests only in interest-paying reserves at the Fed. A narrow bank cannot fail unless the US Treasury or Federal Reserve fails. A narrow bank cannot lose money on its assets. It cannot suffer a run. If people want their money back, they can all have it, instantly. A narrow bank needs essentially no asset risk regulation, stress tests, or anything else.”

— from “The Safest Bank the Fed Won’t Sanction” in Chicago Booth Review

1. Something like that should never have the Fed’s backing. A bank that doesn’t make loans is useless. It should never have the Fed’s backing.

2. If the Fed reverts to not paying interest on reserves (as it did pre-2009), that bank would collapse.

The SRF provides another important tool that lets the market run freely. There is no “free money” in the sense you’re thinking. Banks still have to post collateral, good collateral, to borrow that cash.

“The market says (on those days), there is more risk, we want more return,” No, there is not necessarily more risk. You really think these banks can price risk down to a few basis points? There’s a lack of liquidity at that price. Big difference.

LGC

I agree.

It seems like this mechanism is hiding the true levels at which interest rates should exist.

Understood that the Fed wants rates to be no higher than the 4.25%, but it is clear that they are tampering with free market forces.

Which leads me to ask a greater Fed policy question….

Powell says rates are restrictive……WHAT is being restricted, exactly?

Gold, Stocks, Cost of living, Insurance?

J J Pettigrew

“It seems like this mechanism is hiding the true levels at which interest rates should exist.”

Good lordy. By definition, and since its beginning, the Fed’s job is being accomplished by controlling short-term interest rates. That’s the primary tool it has. That’s what its FOMC policy meetings are all about. Remember: rate hikes and rate cuts? That’s what the Fed’s five policy rates are all about: controlling short-term interest rates. This includes the overnight repo rates. There is no “free market” in short-term interest rates, and there hasn’t been in over 100 years.

I find myself burdened with the weight of never knowing the truth, concerning the current favorite .

Thank you for highlighting and educating us!

The new tricks on the block have seemingly no end… i guess it works until it doesn’t… wonder what the next one will be when this one stops working. isn’t it in effect just continuing risky behavior? i’m asking for a friend;-)

Risk is relative. Banks have to assume a lot of trust with their business partners: from their borrowers, lenders, and investment partners. Lower trust means less borrowing, lending, and investing; a weaker economy with fewer jobs and less income (see Mexico). Higher trust does the opposite. Risk is simply a function of trust. The SRF increases trust at almost zero cost.

When will Mr. Wolf recommend shorting NVIDIA?

Never. In my opinion, shorting individual stocks is too risky. I learned that in November 1999. I was right but about three months early.

Which stock if I may ask?

Just shorted Tesla, couldn’t help myself. Probably too early, but earnings have sobered up a lot of folks lately, although temporarily…

DoubleClick and RealNetworks 🤣

DoubleClick was eventually acquired by PE firms for a fistful of dollars, which later sold it to Google for a huge profit. RealNetworks was eventually taken private for less than $1 a share. When I shorted them, both were trading in the several-hundred-dollar a share range.

Shows how hard it is to short stocks!, so If I get out of Tesla short on top I will make a donation!

Thank you! Good luck!

So is there a safer way to short the entire market os specific sectors? It just seems like the market is unsustainable at these valuations.

This is a bubble, and it will burst. But people lose lots of money betting against bubbles because they’re off in their timing.

As Wolf said, timing is everything. A couple weeks or months can have massive consequences and bubbles are great at perpetuating themselves just long enough to burn you on bigger risky trades.

Easiest bet to safely short this bubble is reduce stock positions and move heavier into cash or equivalent. Buy back heavier when prices are attractive again. Still some money to be made in the market, but I’ve cut way back for the near term. Just playing with some pretty safe options trades.

We’ve surpassed dot-com valuation levels in terms of PE, CAPE, Buffet Indicator, margin at brokers, price to book, and price to sales.

Wolf, what are your thoughts? You might need to do an article on the subject because there’s so much evidence of a bubble.

The financial incest in the AI industry that was recently reported by Bloomberg is also concerning, as this represents borderline accounting fraud IMO.

Maybe time to get into gold? That’s what chinas doing

“Maybe time to get into gold? That’s what China’s doing” was rock-solid advice in 2014/5 after gold was done plunging by 50% to around $1,000.

Right now, there is a real chance to buy high and sell low.

Andy.

Andy!

Andy!!!!!!!!!!!!

Hurry up, the toaster’s about to pop.

It’s over there, go.

idiot

What is causing the rise in the repo rates?

1. the rise is small, just a few basis points.

2. Liquidity is not distributing smoothly because there is less liquidity due to QT.

3. Some fluctuations are normal as liquidity distributes, up and down, and you see that in the chart.

4. Higher rates now bring in more lenders, due to the SRF.

The fed wants to decrease its balance sheet as much it can do easily. Personally i believe that a few months of average uptake of over $100 Billion would be a sufficent signal that liqudity is scarce enough in the banking sector. But until then QT could and should go full steam ahead. Or is there something that i am not seeing?

The Bank of England is doing exactly that: it is SELLING its long-term bonds, not waiting for them to mature decades down the road, which is pretty aggressive, but it exhorted the banks to use its repo facility to keep rates under control, and they’re going it, and the BOE’s repo facility usage has jumped over the past 12 months. So the BOE is shedding its bonds by selling them at a pretty good clip, and any liquidity needs come out of repos, which was the classic pre-QE way of doing it.

To SRF Man?

Wolf…..

what parties seek money above the SRF rate?

It would seem to me that banks would borrow at 4.25% from the SRF and lend at 4.26% all day long…….locking in the .01……why do the rates get higher, like 4.3%?

There are some costs involved in these trades. So it may take more than 1 basis point spread to make this a profitable deal.

What parties?

Remember the repo market is not just banks. So, commercial businesses do not have access to SRF directly . These companies have to get their cash and do their repo with a bank, which then that bank can do the repo and get the cash from FED

It still amazes me that the SRF was done away with in the first place. It boggles the mind.

From what I understand, it was the usual anti-government/anti-system nuts who pushed the narrative that banks were making free money off of the taxpayer because the would borrow cheaply from the taxpayer and then lend it out for a higher rate therefore making free money.

What they failed to realize (or ignored) was that these banks were providing a service, a very valuable service. They were providing liquidity when it was desperately needed.

Unfortunately there are those who think that the victims of liquidity deserved to go under and be destroyed. Fine in theory, but it ignored the real world consequences of an interconnected world where the destruction of one entity can ripple accross the economy. Liquidity crisis suffered by one company can cause liquidity crisis in other entities, and so on and so on, rippling throughout the economy causing huge amounts of damage.

The semi-rational thought they discovered a new tool to handle liquidity crisis: QE/QT. So they gave into the anti-government/anti-system nuts and abolished SRF.

What everyone (collectively) failed to realize is that liquidity is first and foremost a short term problem. So solving it with QE/QT (which has long term consequences), isn’t a good fit. It is a terrible fit.

SRF is perfect for solving short term liquidity problems. Getting rid of it was stupid. I am glad it is back.

Thanks Wolf for these insights on the Repo market.

There seems to be a concerted effort right now to bring long rates down. I believe the Treasury is doing this through purchase of longer bonds and with reissuance at the bill end.

This seems to be creating a convergence of the two ends of the rate curve.

Lower long term rates will help restart a moribund housing market, as planned. Not sure what slightly higher short term rates will do.

Long term goal of Bessant Treasury and Trump seem to be to try and run the economy as hot as possible and accept higher inflation rates. All this to decrease the debt nominally.

Sure, the government is always trying to keep a lid on long-term yields.

But…

“doing this through purchase of longer bonds and with reissuance at the bill end.”

The buybacks, which were started under Biden, are minuscule. They have no market impact. For example, at the buyback auction last week, only $192 million with an M were bought back. That’s not even a rounding error in the $38 trillion in debt outstanding and in the issuance of $400 billion to $800 billion with a B a WEEK.

MW: GM’s stock is soaring toward its best day in five years. Why investors are cheering.

GM +14.72%

Revenues down, costs up (eats the tariffs), net income plunged by 65%, stock jumps by 14%.

They’re learning a lesson from Tesla 🤣

Gold prices are having their biggest single one day drop in the entire history of gold and are now down more than $220 per ounce.

it’s off 5% from it’s all-time high – not a big deal yet.

Are repo rates the same as SOFR?

SOFR tracks a $3 trillion segment of the $5 trillion repo market. So it represents repo rates in that $3 trillion segment of the repo market.

When is the Fed going to learn that it’s got to let things fail if they want to keep their jobs?

You can’t just bail everyone out and expect there to not be inflation.

If we’re lucky, someone with a lot of money will buy Congress to tell the Fed to quit bailing people out, let things fail, and have a deflationary target. But I doubt that’s ever going to happen.

There is no bailout here. It’s just “rate control.” The Fed is in charge of short-term rates, and sets them in its FOMC policy meetings (rate cuts, rate hikes), and then it has to try to control short-term rates to conform to its policy rate decision.

Unless I’m mistaken the Fed just said they will probably stop QT soon.

One thing I haven’t been able to find is Powell or someone else saying explicitly that they will continue to let MBS roll off and then replace with T-Bills. I thought they said that but I can’t find the quote now.

Maybe best case is the Fed still lets five or ten billion roll off each month, but it does seem like we’re now seeing near the smallest balance sheet for the rest of time.

I bought a 18 mo CD at 4.05, 24 months cd at 4.20 yesterday. I am happy with that yield! Liquidity is running dry on the street, precious medals sold today to keep the equity bull direction intact. $vix above 20 spy below 666 the machine will sell with gusto, for being near highs the charts scream danger. CPI MOM .4 or .5 maybe higher? Friday could be fireworks paradigm shift day.

You know, I believe this guy. I have a feeling he’s right. Friday guys. Be ready. It’s gonna blow.

1:04 PM 10/21/2025

Dow 46,924.74 +218.16 0.47%

S&P 500 6,735.35 +0.22 0.00%

Nasdaq 22,953.67 -36.88 -0.16%

VIX 17.63 -0.60 -3.29%

Gold 4,119.50 -239.90 -5.50%

Oil 57.86 +0.34 0.59%

What’s the difference between things “blowing up” as mentioned in the title, which every thing the FED is doing is designed to prevent, and that is ostensibly a good thing – and a “bubble bursting”, which can also be a good thing?

Unless there is a difference between things “blowing up” and a “bubble bursting” it seems the FED’s job is to “blow up the bubble forever”

A bubble bursting means asset prices (stocks, real estate, etc.) go down.

“…without blowing anything up, unlike last time” in the subtitle refers to the repo market issues in September 2019, when within 5 days, repo rates spiked from 2.2% to 10% as liquidity had suddenly dried up, and banks were not lending to the repo market because they had to deal with the huge liquidity flows from corporate tax payments in mid-September. Companies and financial institutions that borrow in the repo market must borrow every day anew since these are overnight loans. If some day there suddenly aren’t enough lenders to the repo market, then it’s a HUGE issue. This is where the SRF comes in which provides liquidity to the banks to provide liquidity to the repo market, and make money doing it.

Repo lending is nearly risk-free since the collateral is Treasury securities. It’s just a liquidity issue.

It’s good to see the SRF starting to work as intended. Two questions.

First, for a bank, wouldn’t it be simpler to withdraw some of their excess reserves from the Fed and use that to lend to repos? I suppose that if we start to see consistent activity in the SRF, to the point where banks are consistently lending on a near-daily basis, then some banks might very well do that?

Second, if the SRF is starting to get some action, indicating that liquidity in the regular markets is adequate-but-not-ample, isn’t this a good time to start reducing the interest paid on reserves, to get banks to shift some of their excess reserves back into the market? This, IMHO, would give the Feds a much larger cushion to continue to carry out QT than just the SRF alone.

1. “First, for a bank, wouldn’t it be simpler to withdraw some of their excess reserves from the Fed and use that to lend to repos…”

Yes, and they did that for years. But now QT has reduced the excess reserves and has emptied out the Fed’s ON RRPs (excess cash from money market funds), and so there is not that much excess cash floating around there among banks and money market funds to put into repos when repo rates spike. This is what tripped up the Fed in September 2019.

2. There are many voices saying that the Fed shouldn’t pay interest on reserves at all. So phasing out IOR might be one way. But IOR is one of the Fed’s tools to control short-term rates as per its policy. In addition, if the Fed cuts the IOR, it will also have to re-impose the minimum reserve requirement for each bank, which it eliminated in 2020. So this would get complicated very quickly. There is good reason to do it, but carefully.

Wolf:

In your opinion, has the FED been successful the last 110 years. They were legislated mandates, some obviously conflicting The overall concept of which is to buffer the business cycle. Please address these specific mandates:

Full employment?

Stable US Dollar value?

Lender last resort?

Buffer business cycle?

Mananage an economy such that wealth can be created?

Thanks!

Whatever one makes of Powell, the re-start of the SRF will stand the country in good stead for some time to come, and should amount to at least one entry in his pro column.

Yes.

No activity at the SRF today, neither in the morning auction nor in the afternoon auction. Its balance is back to zero. That’s how it is supposed to work.