Its holdings of commercial paper & corporate bonds are nearly gone. The BOJ is cleaning up its balance sheet.

By Wolf Richter for WOLF STREET.

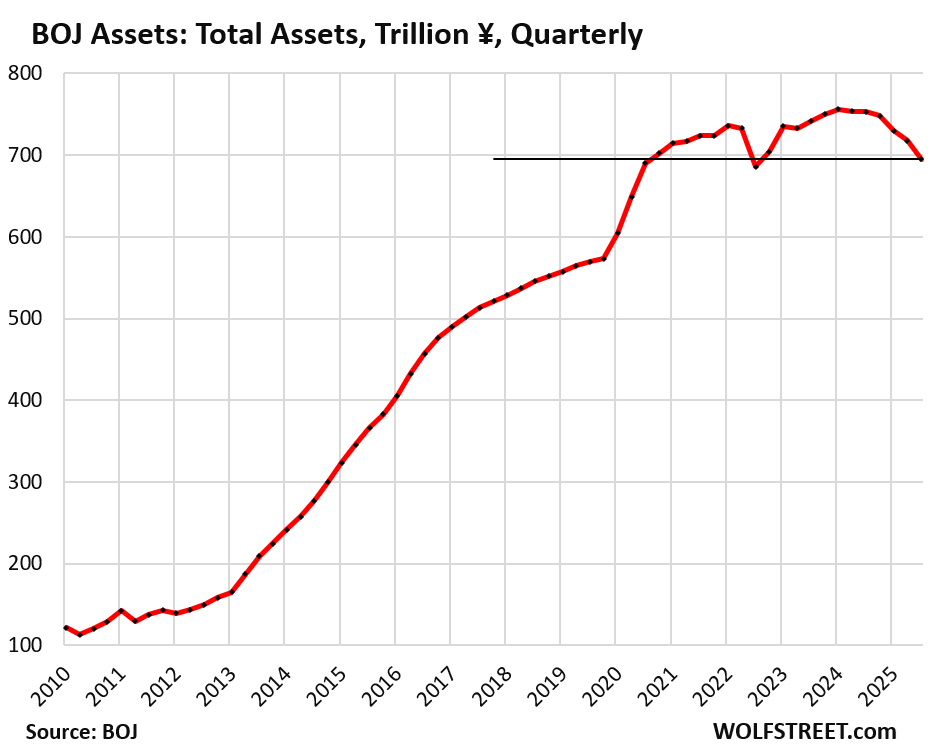

The Bank of Japan further accelerated its quantitative tightening: Total assets on its balance sheet fell by ¥22.3 trillion ($148 billion) in the quarter through September, the biggest quarter-over-quarter decline since QT started in early 2024.

Since the peak in the quarter through March 2024, total assets have fallen by ¥61.2 trillion ($407 billion), or by 8.1%, to ¥695 trillion ($4.62 trillion), back to where they’d first been at the end of 2020, according to the BOJ’s balance sheet.

The BOJ fiscal year ends March 31. For the sake of simplicity, all quarters here are expressed calendar quarters (quarter ended September 30 = Q3).

Back in the QE days, the BOJ conducted QE in several forms:

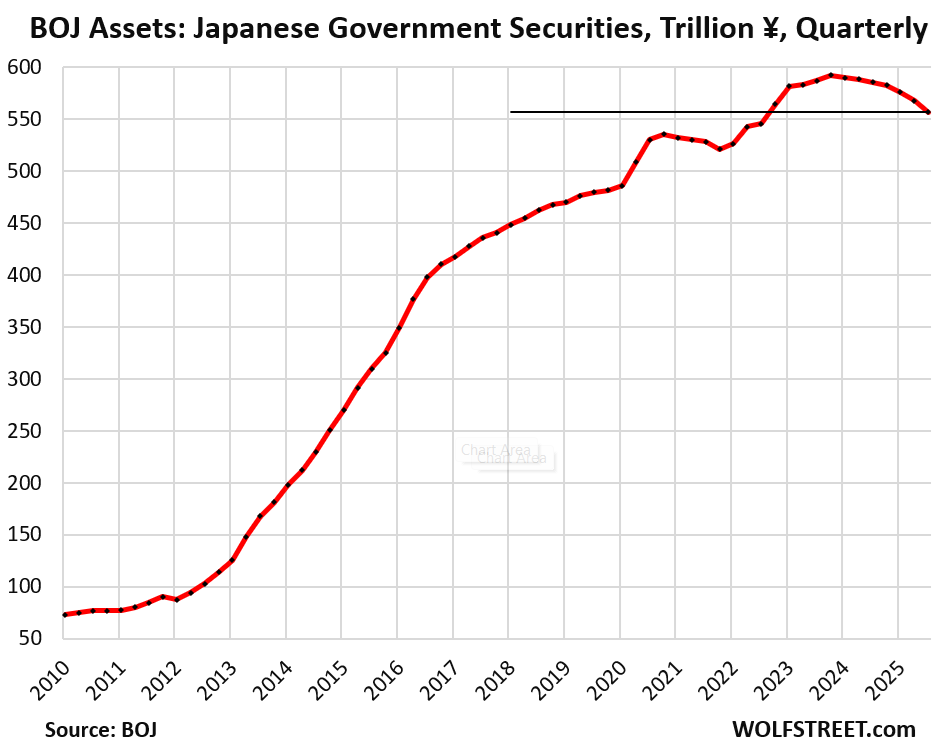

- Japanese government securities (now 80% of total assets).

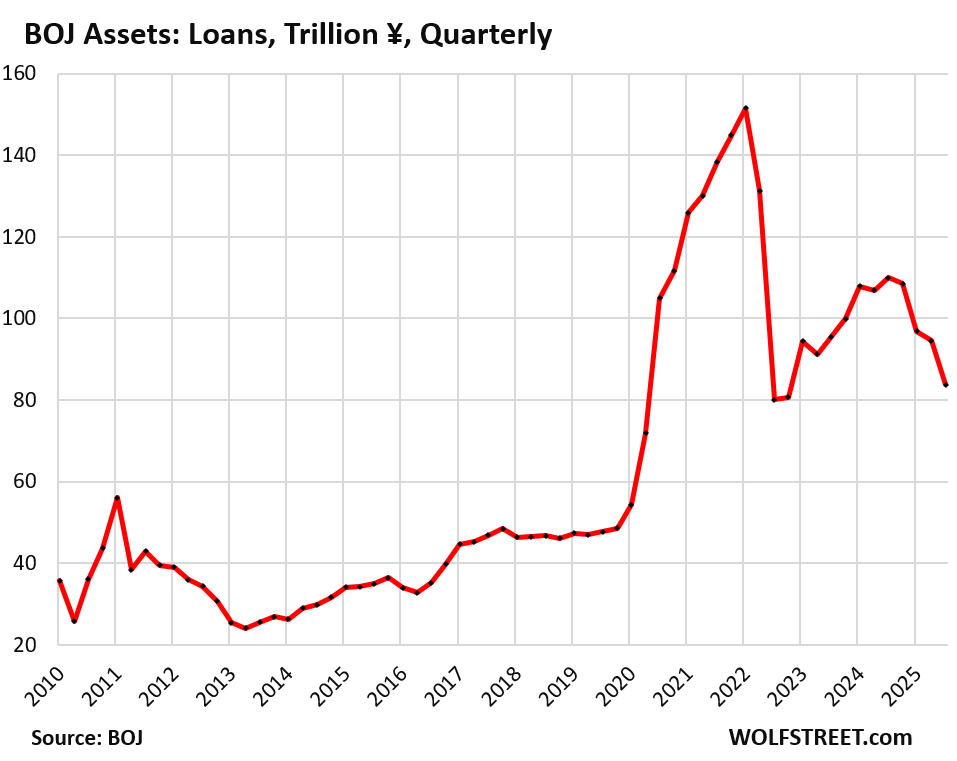

- Loans (now 11% of total assets).

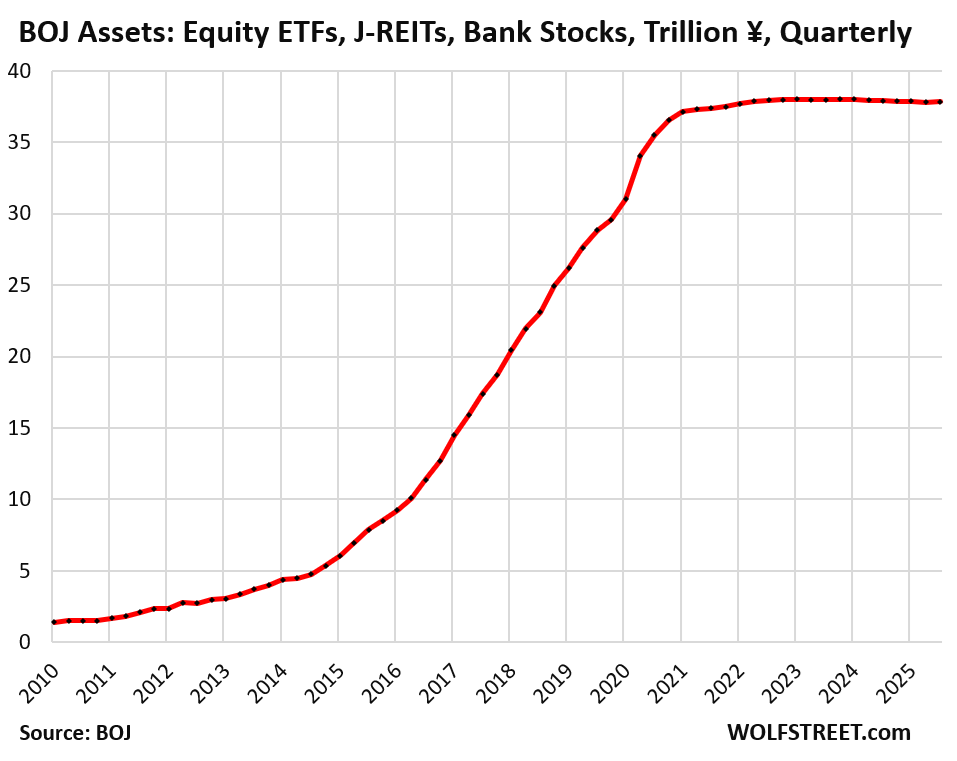

- Stock-market traded equity ETFs and Japanese REITS (now 5% of total assets)

- Commercial paper and corporate bonds (down to 0.6% of total assets).

- Bank stocks purchased in 2000 and 2009 (sold the last ones in Q3).

Japanese government securities declined by ¥10.8 trillion (-$71.5 billion) in Q3, to ¥567 trillion ($3.66 trillion), the lowest since Q4 2022, down by ¥35.5 trillion (-6.0%) from the peak in Q4 2023.

Nearly all of them are longer-term Japanese Government Bonds (JGBs); its holdings of short-term Japanese Government Treasury Bills were unchanged at just ¥1.7 trillion ($12 billion).

The acceleration of QT, in terms of the quarter-over-quarter declines of its holdings of Japanese government securities:

- Q3 2025: -¥10.8 trillion

- Q2 2025: -¥8.4 trillion

- Q1 2025: -¥6.4 trillion

- Q4 2024: -¥3.1 trillion

- Q3 2024: -¥3.0 trillion

- Q2 2024: -¥1.2 trillion

- Q1 2024: -¥2.6 trillion

- Q4 2023: end of QE

The BOJ’s holdings of Japanese government securities move in three-month cycles due to the timing of when long-term bonds mature and when they’re replaced with newly issued bonds of the same type. The BOJ also makes quarterly data available and refers to quarterly data in its balance sheet discussions, which iron out the three-month cycles.

Loans declined by ¥10.8 trillion in Q3 from Q2, and by ¥26.1 trillion year-over-year, to ¥83.8 trillion ($555 billion).

Since the peak in Q1 2022, the outstanding balance has fallen by ¥67.7 trillion, or by 45%.

These loans now account for 11% of the BOJ’s total assets. The BOJ provided loans to banks and other entities under several programs, including the pandemic-era loans that caused the total amount of loans outstanding to more than triple in two years:

BOJ’s equity ETFs, Japanese J-REITs, and bank stocks.

Equity ETFs, Japanese REITs, and bank stocks don’t mature, and therefore the BOJ can’t get rid of them by letting them mature without replacement, unlike Japanese government securities, commercial paper, and corporate bonds. To get rid of its equity ETFs, Japanese REITs, and bank stocks, the BOJ has to sell them outright.

The BOJ is preparing to sell its ETFs and Japanese REITs, it said at its September meeting. It will start selling them at an initial pace that is very slow: equity ETFs at a pace of ¥330 billion per year ($2.2 billion) and Japanese REITs at a pace of ¥5 billion per year ($33 million).

It said that it could review the pace of those sales at future policy meetings. It said the sales would start when the operational preparations are completed.

The BOJ carries them at acquisition cost and didn’t write them up as market values rose since it started buying them in 2012. It stopped buying in Q4 2023 when they’d reached ¥37.8 trillion ($250 billion) at acquisition cost.

Equity ETFs and J-REITs only account for 5.0% of the BOJ’s total assets. They were always only a small part of the BOJ’s QE operations, but the hype around those purchases in the US QE-promoting financial media was enormous.

The BOJ sold off its last bank stocks in Q3. It had purchased them in the early 2000s and then again in 2009. The purchases of bank stocks ceased in 2010. In 2016, the BOJ started selling them and said at the time that sales would be completed by March 2026. As of the end of September, the last of the bank stocks were gone. This process can be a guideline for how the BOJ will sell its ETFs and J-REITs.

The BOJ’s total stock-market-traded assets combined – bank stocks, equity ETFs, and J-REITs – have declined since the peak in Q4 2023 at a microscopic pace, totaling 0.9%, due to the sales of the bank stocks. The decline is so small it gets lost in rounding.

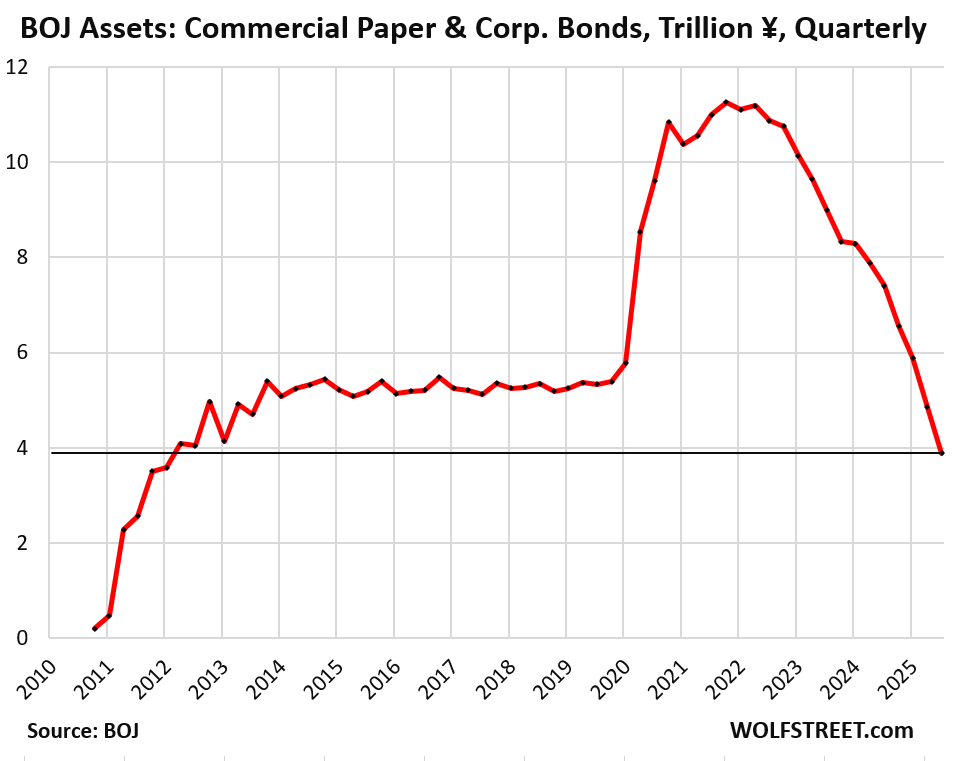

Commercial paper and corporate bonds fell by ¥1.0 trillion in Q3 to just ¥3.9 trillion ($26 billion), the lowest since 2012.

Since the peak in Q4 2021, they have plunged by 57%. The BOJ stopped buying commercial paper and corporate bonds in early 2022, and its holdings have been running off the balance sheet as they mature.

They were never a significant part of the BOJ’s QE operations. At their peak in Q4 2021, they accounted for only 2.2% of the BOJ’s total assets, and their share is now down to just 0.6%.

In case you missed it: Fed Balance Sheet QT: -$15 Billion in September, -$2.38 Trillion from Peak, to $6.59 Trillion.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

What have they done with the BoJ’s Gold reserves??? (if any)

Why would such a trivial little asset class like gold matter at all?

LMFAO! love the sarcasm.

“Full faith and credit”

The BOJ lists ¥441 billion of gold at cost on its balance sheet (about $2.9 billion). It has been unchanged since 2000.

According to World Gold Council, the BOJ has 846 tonnes of gold. So that’s about $109 billion at today’s price.

But now a female PM? There goes the country!

To be serious, both the UK and Germany have had good female leaders: Thatcher and Merkel.

I know a lot of lefty Brits didn’t like Thatcher but they forget the basket case she took over. Example: incredibly, the press unions had negotiated a ban on the intro of modern tech into printing newspapers. They were still melting hot metal being cast into letters on Linotype machines. After a page had been assembled in a box, a proof was taken. One man would roll ink over the letters, another would place a sheet of paper, a third would press the sheet. None could do another’s job: that would cause a strike.

Similar conditions in auto plants: one important plant only had two weeks of uninterrupted production in a year. Meanwhile, in 1974, W Germany, VW had its first strike. It lasted for one day.

Both women were scientists, Thatcher worked with X ray diffraction and did research for 3M, before becoming a lawyer, before becoming a politician. Merkel did nuclear physics as applied in reactors.

Let’s hope a female PM helps other women to breakthrough Japan’s very thick ‘Glass Ceiling’ in its business world.

Thatcher gutted UK industry by massively overvaluing the pound with high interest rates when the oil started to flow. Then threw away the oil revenues on tax cuts and selling off state assets on the cheap. Her time was an utter disaster. It was only the Falklands War that saved her in 1983. Merkel was also a complete and utter disaster, and facilitated the rise of the other disaster von der Leyen. Nothing to do with their sex, just the usual types of leader we have had in the past few decades.

Looks like the equity sales could continue for as long as the market keeps going up. If the sales aren’t big enough they are just selling the annual profits

“If the sales aren’t big enough they are just selling the annual profits”

No, by definition, because the amounts are at their acquisition costs at which they carry the ETFs on their balance sheet. They never write them up to market.

So selling ¥330 billion per year means ¥330 billion at their acquisition costs. The actual sales proceeds could be far higher, depending on when they bought those particular ETFs that they sell; for the early purchases, the sales proceeds can be four times their acquisition costs. So actual sales would be far higher. But their balance sheet would drop by the amount of the acquisition cost.

Also note how they started out slowly with their JGB reductions and then sped up. There is a table in this article with quarterly JGB roll-off amounts so you can see the acceleration.

Start out slowly, then speed up. That’s how they do it. But even after accelerating the pace, they will still take decades to sell those ETFs, just like they took 10 years to sell their much smaller position in bank stocks (which was tricker because those were the stocks of individual banks).

Wolf -really appreciate your periodic scrutiny of Japan, knowing that you’ve indicated in the past that it’s not one of your more-popular arenas…

may we all find a better day.

thanks. Yes, I’d be out of business if I did a lot of it. I’ll post a quarterly ECB article on Wednesday, same thing there. This stuff about the big central banks is really important, yet few people read them. However, my monthly Fed balance sheet articles are big. It’s like there’s an army of people out there just waiting for it, and if I skip it one month, my inbox blows up with people asking where it is.

Initially I was very interested when the BOJ said it would sell its index ETF and REIT holdings. Then I read the fine print: it will likely take more than 100 years! Maybe they don’t want to scrare investors and the actually rate of selling will be higher than they indicated.

Like I said in the article, this is the initial pace. Look at the initial pace of the JGB roll-off in the table in the article. It started out in Q1 2024 at ¥2.6 trillion. And then it accelerated from there every quarter. In Q3 2025, it accelerated to ¥10.8 trillion. That’s how the BOJ works. People like you also laughed at the JGB roll-off in Q1 2024. And after 7 quarters of acceleration later, the BOJ’s QT is faster than the Fed’s.

Are there any other countries accelerating QT?

Good question. Yes. The ECB has further accelerated its bond QT this year. During QE, it had purchased all kinds of bonds, including the sovereign bonds of its member states, corporate bonds, asset backed securities, mortgage bonds, etc. a huge pile of bonds. When QT started, it put a cap on the amount of the roll-off, at first at a fairly low level on one of its portfolios and no roll-off at its other portfolio, and then it raised the cap on the first and started the roll-off on the second, and this year it removed the last cap from the bond roll-off. So whatever matures in both portfolios comes off its balance sheet. The amounts of the bond-roll-off are now quite substantial.

Article coming with the latest figures, including the mark-to-market of its gold holdings, in less than 24 hours.

We are in uncharted waters with such substantial QT, I would guess. Is this a concern as to creating a global slowdown or recession inadvertently? Any wisdom being expressed on that?

QE caused a huge amount of damage. Now they’re trying to unwind some of that damage. But they still have a long way to go. The balance sheets of all the big central banks are still swollen with QE assets. They need to shed those. And they know it. That’s not going to cause a global slowdown. But when the AI investment bubble implodes, that will cause a recession in the US for sure – unrelated to QT.

This could be the implosion that ignites the explosion.

“ Jefferies Financial Group Inc. sunk nearly a quarter of its $3 billion trade finance portfolio into receivables tied to auto parts supplier First Brands Group Inc.”

No more bailouts?

bailout LOL. you people crack me up. Jeffries is indirectly exposed to $715 million in Frist Brands receivables factoring, secured by collateral. So they may take a haircut and lose maybe a couple of hundred million on this deal, or they may not lose anything. But they also made lots of money on this deal, so no biggie. For a company the size of Jeffries, that’s peanuts. Jefferies booked a net profit of $252 million in the last quarter, so the loss from this factoring deal, if any, might dent one quarter’s income.

There are unsecured creditors though, and they will get crushed.

I wonder how EU QT is affecting the worrying rise in French bond yields?

Perhaps a pause is on the way?

No. Where does all this end-of-QT stuff come from? It’s just an effort at market manipulation.

Bond yields in France are still too low, and are a lot lower than in the US and the UK. They’re just higher than in Germany. The reason they’re higher in France than in Germany (more than normal) is because France is stuck in political chaos that prevents it from passing a budget.

10-year yields in:

Germany: 2.67%

France: 3.52%

US: 4.11%

UK: 4.71%

Merkel was a terrible leader, particularlyduringthe last half of her yearsin power. Her immigration and energy policies are why Germany has the economic problems it is currently facing. Plus, she relied on Russian gas while claiming Russia was a threat, and kept defense spending at about 1.2% of GDP during most of her years in power. The chickens are coming home to roost, and as is often the case, it takes years, sometimes a decade or more, to see just how bad policies really were.

AI Overview

Before the Ukraine war, numerous countries bought Russian oil and gas, including all EU member states, which imported significant amounts of Russian oil and pipeline gas.

So she had company in the EU,,,everyone.

Yes, cheap Russian natural gas has been a huge factor in Germany and other countries, and all German politicians had to pray at the altar of cheap natural gas from Russia.

When I was a kid, living in Germany in the 1950s and 1960s, we had coal gas, produced at the local gasworks from coal. It was toxic and expensive. We used it in the kitchen stove and oven. We also had a big coal-fired boiler in the kitchen that heated the hot water that heated the entire apartment. We had a coal gas fired tankless water heater in the bathroom. Then during the Cold War, Germany helped fund the first natural gas pipeline from the USSR to Germany, and it brought about huge changes, adios household coal and coal gas. It gave Germany access to cheap clean fuel. Cheap clean fuel is addictive.

Having lived in Kaiserslautern and then on to Sembach for the A-10’s, I had many fond memories of Germany and the amounts of money that were being used and invested gave Germany great pride, and now I weep for what has become of Germany. Very different from when I was there, and we move on.

It would make sense for an energy-poor region like Western Europe to go all-in on renewables. Their high energy prices were the reasons for desperate dependency on Russian gas and now it is the cause for their industrial malaise, including in the IT area. Imagine running a data center or an aluminum smelter at >100 Euros per Mwh!

Meanwhile, solar panels from China have become the cheapest energy source in the world, and can be expected to keep producing for 30 or more years (so no dependency). If the politics could be set aside, it would make sense for European leaders to set zero tariffs on solar equipment, set up generous net metering regimes, and flood the zone with private investment that could reduce peak costs and create a un-disruptable distributed supply system.

Yes Europe is cloudy, blah blah. You just add more panels, which are the cheapest components of a solar energy system. The economics support this because of the high cost of electricity. Until they run out of flat roof space and south-facing hillsides, there’s no shortage of opportunity.

Chris B,

What do you do at night? You’d need a massive network of battery storage for that to work.

The problem with too much solar is it can create pricing distortions, e.g. prices can go negative during the day which is a problem for net metering. You need to overproduce during the day to avoid paying for what you use at night. But what if daytime electric prices go negative and now you’re paying the grid operator to take the extra electricity off your hands? Remember /everyone/ with panels is following the same dynamic.

I spent $15k on my PV system so I’m not “anti-solar” but I have no delusions about it being a valid form of baseload power (it just isn’t). Solar can only AUGMENT the grid.

Chris B: Germany had just finished re-furbishing a big nuke reactor when the Tsunami hit Japan and they had their big nuke disaster. Merkel went into the tank, hold all calls for a week, and when she comes out, Germany is out of nuclear power. Newly refurbed nuke demolished. Buys a lot of power from France’s reactors, which have big issues of their own but still deliver power.

Now everyone is talking about a potential nuke renaissance maybe Germany will get back in.

If this AI play keep chugging at this pace, we won’t have much choice other than to get into nuclear. That alone might be worth all the hype from this AI cycle

It takes many years to build a nuclear power plant, and many years longer than planned. And cost overruns are standard. And the Small Modular Reactors are already falling into the same trap.

To build power plants fast and low cost, they cannot be nuclear.

Only if you let China build the nukes, everyone else is way more expensive and takes way longer to build them. 1GW in China US$3 billion, the US two to two and a half times that. The UK GBP 15 billion!

1GW in China 6 years, in US one and a half decades, in UK two decades!

The Chinese offered to build those nuke plants for the Brits, but the Brits got all Orientalism on them.

Yep, so much of that clean renewable energy went on replacing clean nuclear energy. Germany would be much closer to net zero electricity and be able to handle the lack of Russian gas better if it had kept those nukes; which were supplying about a quarter of Germany’s electricity. Good reliable base load power.

When I look at they are selling I ask how and why did they buy all this. All this manipulation of a market and market economy. All the ways to to manipulate price discovery and allow markets to clear, clean and wash out the problems if they would have had price discovery and no intervention. It is sickening.

Wolf? Has the BOJ over the years been a positive or negative for the country and Japanese people?

The Japanese people got away with the BOJ’s money printing for a long time. But that’s over. the yen has plunged, including against the USD, making the Japanese feel poor when they travel overseas or buy imports. And for the past four years, they’ve experienced inflation similar to the US inflation rates, but wages aren’t rising fast enough, and price increases really bite. The Japanese hate price increases just as much as Americans do. And they hate the plunge of the yen. So that’s new. The BOJ has tried to stay in the background, but it got some bad attention. So there is pressure to not let this get out of hand.

Yen devaluation was long overdue. Having lived in Japan when USDJPY hovered around 80 and a cab ride from Narita to Tokyo central cost 250 USD, their currency devaluation was a long time in the making.

In my last trip to Tokyo, everything seemed so much more affordable and reasonable. <10 USD Ramen shops were everywhere and I didn't have to worry about cash in my wallet while hailing a cab randomly.

Yes, BOJ screwed up and tried to solve structural deflationary issues using persistent and nonsensical monetary experiments. But this plunge in yen is one good thing they have achieved out of all this. As Yen devalues further, their strong external surplus means that servicing their local debt becomes more affordable.

“In my last trip to Tokyo, everything seemed so much more affordable and reasonable.”

Yes, if your income is based in the US. Since the yen plunge, Japan has become a budget traveler destination. That’s a bad sign.

For Japanese people earning Japanese wages, Tokyo is not at all “more affordable and reasonable,” and foreigners piling in (including from China/Hong Kong) to buy homes in Tokyo has driven up real estate prices in the Tokyo area, and locals trying to buy are now having a hard time.

I think Japan’s domestic wages will naturally go up as Yen collapses. It was always an export-dependent economy and it endured decades of stagnation and abysmal growth as Yen strengthening from 200 to 80 made it give up a lot of its exporting prowess to China. USDJPY at 150 is not a historically high rate to be honest, it is just mean reverting on a longer time cycle.

Japan was never a super innovative economy but they excelled at efficiency and cost management – qualities which came unstuck as their exports lost their competitiveness and made them move their factories elsewhere. With this plunge, hopefully things will start looking up again. And Nikkei is showing why it is generally good for the country. Of course they can’t beat demographics unless they shed their reservations on immigration but that is a long topic and better discussed separately.

Mayank – you neglected to mention another, vital aspect at which the Japanese excelled, high Quality Assurance of their export goods, resulting from their conceptual innovation and subsequent oversight of the MITI…

may we all find a better day.

It’s strange to see the Japanese stock market hitting new highs even as the central bank is removing liquidity from the markets by selling bonds (and collecting yen). You’d think with fewer yen in circulation to chase assets, that liquidity would go down and prices might go down too. Well, nope.

In hindsight the same thing happened in the US when the US was doing QT. The usual prognosticators were worried about various markets running out of buyers or yields rising, but it didn’t happen. During QE, people were reassured that a deflationary recession wouldn’t happen because the government was pumping cash into the system. During QT, people were reassured that inflation wouldn’t go up and necessitate higher rates, because the government was removing cash from the system. Together these methods addressed whatever was the main concern at the time, justifying investments into risky assets either way.

I suppose the point is, it’s futile to try to predict asset prices from central bank QE/QT actions. Supply and demand work differently on the scale of entire nations / currencies.

Wolf,

What percent of the JGB market does the BOJ now own? At one point I think I recall it being >50% but must be less now.

At the end of September, central government long-term bonds outstanding rose to ¥1,112 trillion. The BOJ holds ¥567 trillion, or about 51%.

This percentage is coming down gradually as the BOJ reduces its JGB holdings, and as the amount outstanding increases.