The rise of the “non-traditional reserve currencies.”

By Wolf Richter for WOLF STREET.

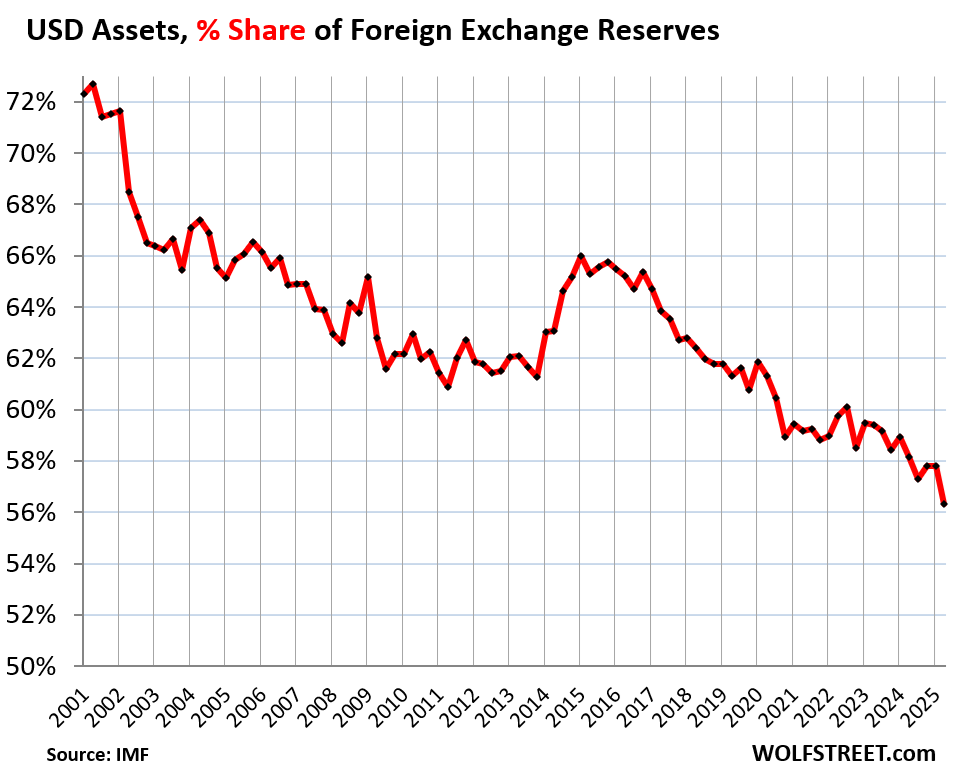

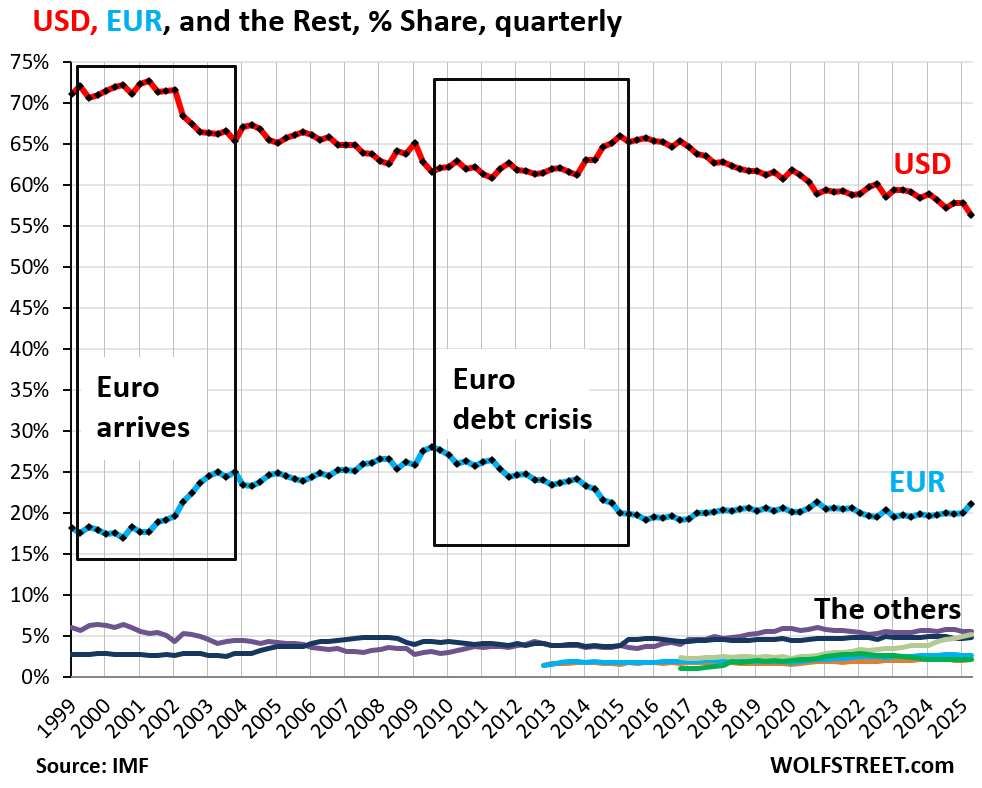

The dollar’s status as dominant global reserve currency just took another steep dive. The share of USD-denominated assets held by other central banks plunged to 56.3% of total foreign exchange reserves in Q2, the lowest since 1994, from 57.8% in the prior quarter, according to IMF’s new data on Currency Composition of Official Foreign Exchange Reserves.

At the pace of the past five years, the dollar’s share might fall to 50% in another five years. Even at 50%, the dollar would still be the largest reserve currency, as all other currencies combined would weigh only as much as the dollar. But the long-term trend is clear – and this has significant long-term consequences for the US.

USD-denominated foreign exchange reserves include US Treasury securities, US MBS, US agency securities, US corporate bonds, and other USD-denominated assets held by central banks other than the Fed.

Excluded are any central bank’s holdings of assets denominated in its own currency, such as the Fed’s holdings of Treasury securities or the ECB’s holdings of euro-denominated bonds.

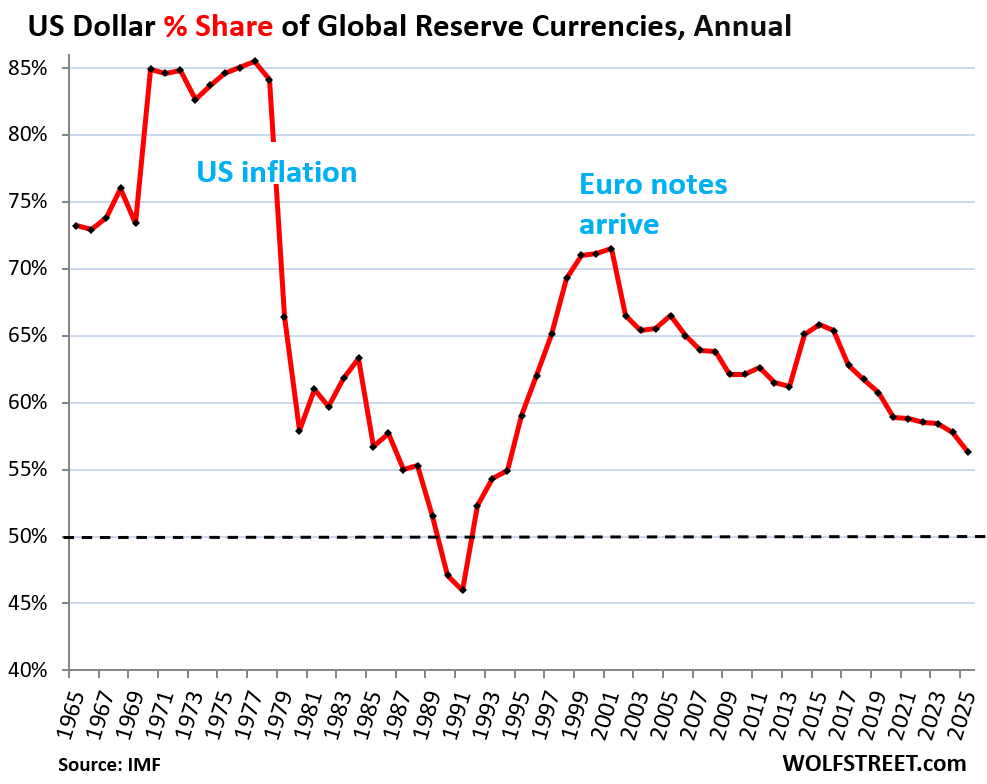

The dollar’s share had already been below 50% (dotted line in the chart below) in 1990 and 1991, at the final leg of its long plunge from a share of 85% in 1977 to 46% in 1991, after inflation had exploded in the US in the 1970s and into the 1980s, and central banks lost confidence in the Fed’s will to get this inflation under control.

But the Fed did bring inflation under control, though it took years, and by the 1990s, central banks loaded up on dollar-assets again, until the euro came along. The dollar’s share at the end of each year (2025 = Q2):

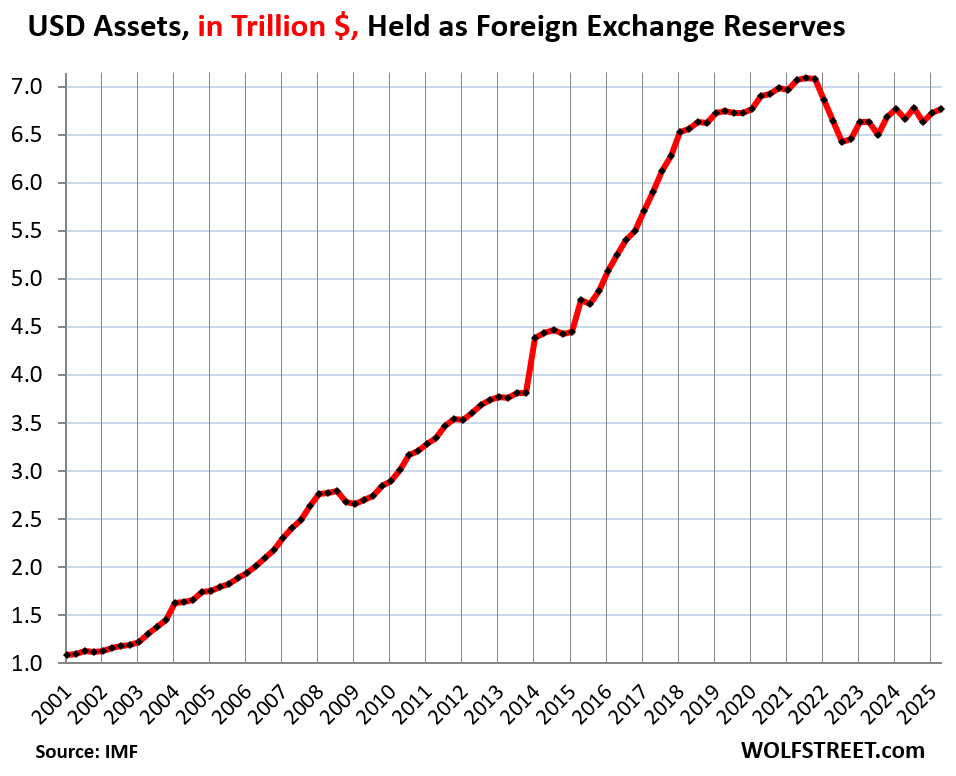

They didn’t dump USD-denominated securities.

Well, they did dump USD-denominated securities for three quarters in a row in 2022 when inflation exploded in the US; they dumped $660 billion in USD assets in Q1, Q2, and Q3 2022.

But when the Fed got serious about inflation and pushed up interest rates and started QT, the dumping stopped and the buying started again. And they increased their holdings of USD assets in Q2 2025 to $6.77 trillion, but that remains below the peak in Q4 2021 of $7.09 trillion.

Instead, what caused the share of USD assets to decline over the years is the growth in total foreign exchange reserves, driven by the growth in assets denominated in other currencies, including many smaller currencies, that outpaced the growth in USD assets, as central banks have been diversifying away from the USD.

So these are the USD-denominated assets – US Treasury securities, US agency securities, US MBS, US corporate bonds, etc. – held by foreign central banks:

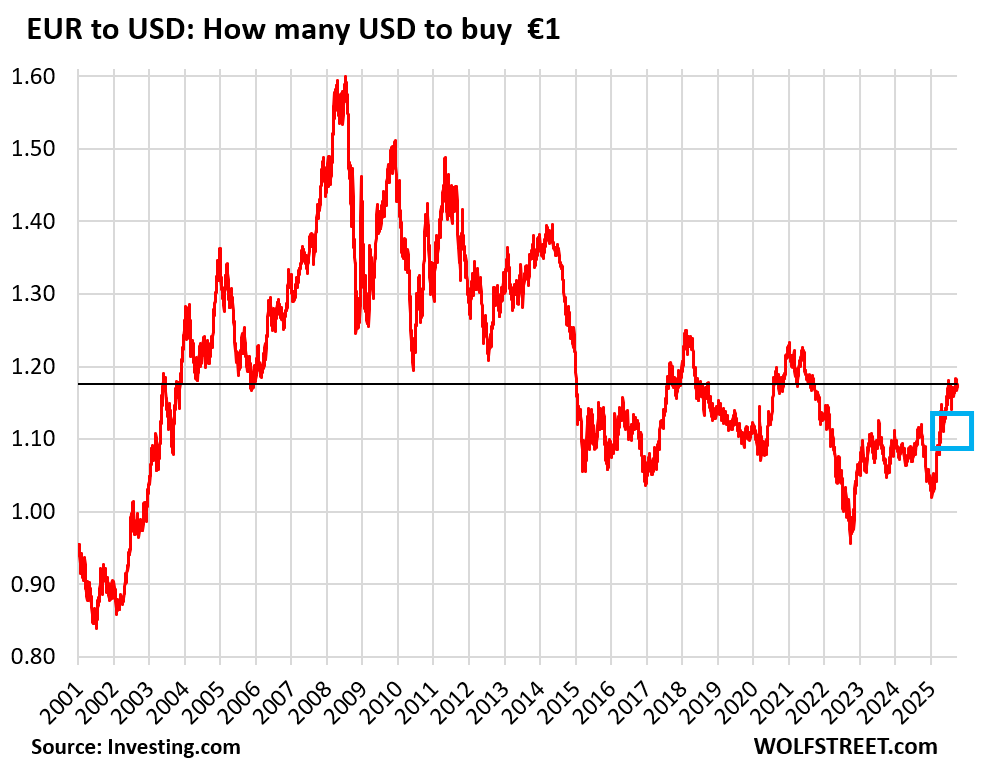

But the dollar tanked in Q2.

The IMF expressed all foreign exchange reserves here in USD. So all USD holdings are reported in USD obviously. But the value of EUR-denominated assets is expressed in USD at the current exchange rate; the value of all assets denominated in other currencies is expressed in USD at the current exchange rate.

Big movements in exchange rates change the value of the non-USD assets that are expressed in USD, but don’t change the value of USD assets. This shifts the share of USD assets against these non-USD assets.

The USD plunged 8.3% against the EUR in Q2 (blue box in the chart below). The euro is the second largest reserve currency with a share of over 20%. It moves the needle.

As the value of EUR-assets is then expressed in USD via that lower exchange rate, the value in USD of the EUR-assets increases, and the euro’s share of total exchange reserves rises while the dollar’s share declines.

Despite all the dollar-collapse theories, those exchange-rate movements were nothing special over the long term, with bigger and faster moves in the past, and the exchange rate between the USD and the EUR is in the middle of the range since the EUR’s existence (data via YCharts):

The USD also declined against the other major reserve currencies, but since their share is much smaller than the euro’s share (more in a moment), they had less of an impact.

The IMF estimated that most of that steep decline in Q2 was due to the drop of the exchange rate of the USD against the other major reserve currencies. If the USD exchange rates had remained unchanged in Q2, the dollar’s share of all global exchange reserves would have still declined, continuing along the trend, but the decline would have been much smaller.

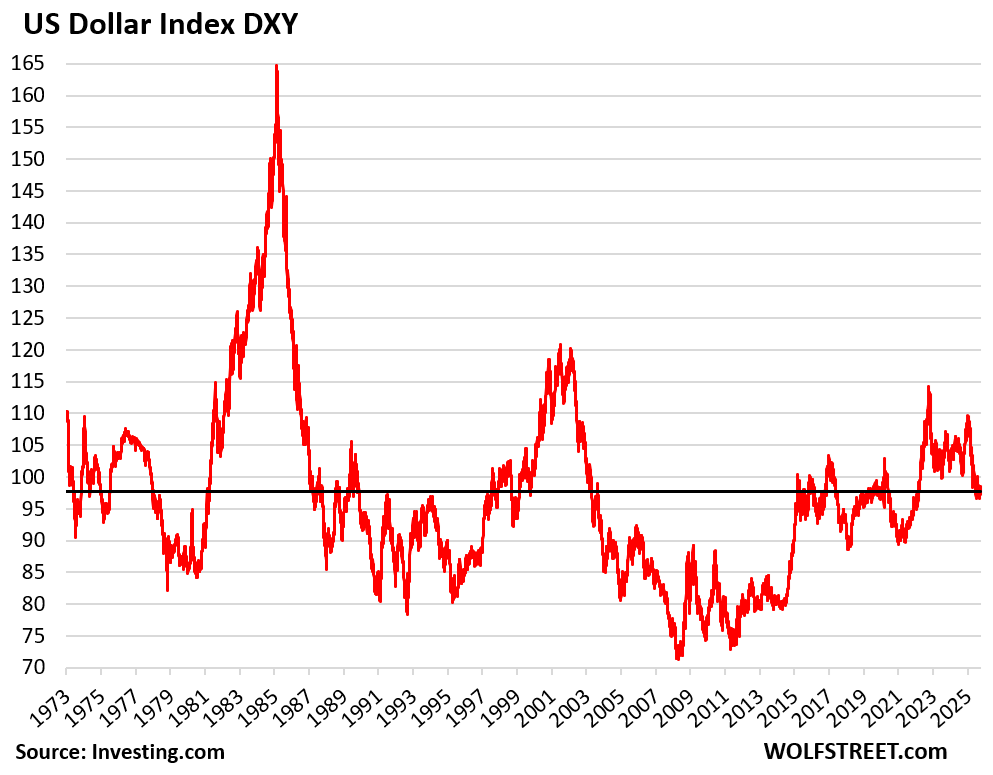

Over the long term, the DXY dollar index – it tracks the exchange rates of the USD against the currencies of the Euro Area, Japan, United Kingdom, Canada, Sweden, and Switzerland – has been, well, unchanged from 1973, despite huge fluctuations in between.

Also note the massive rally of the USD from 2009 through 2022, and how the recent decline of the USD has retraced only a small portion of that rally.

The other foreign exchange reserves.

Central banks holdings of foreign exchange reserves ins USD and in other currencies (expressed in USD), rose to $12.9 trillion in Q2.

Top holdings, expressed in USD:

- USD-denominated assets: $6.77 trillion

- EUR-denominated assets: $2.54 trillion

- YEN-denominated assets: $0.67 trillion

- GBP-denominated assets: $0.58 trillion

- CAD-denominated assets: $0.31 trillion.

The euro’s share, #2, jumped up to 21.1% in Q2. The entire surge in Q2 was due to the surge of the exchange rate of the EUR against the dollar, as the value of the EUR-assets were expressed in weakened USD (blue in the chart below).

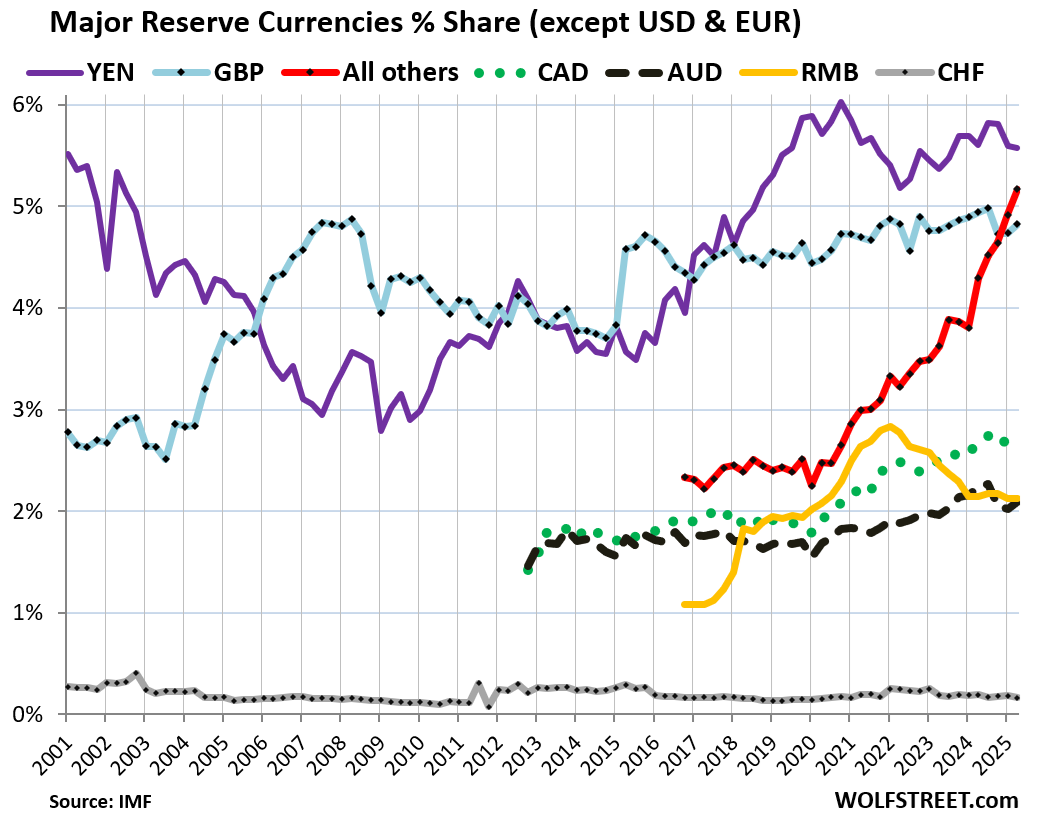

The other currencies are the colorful tangle at the bottom of the chart (more in a moment). Combined, they have gained share over the years, at the expense of the dollar, while the euro’s share has remained roughly stable since 2015.

The rise of the “non-traditional” reserve currencies. What is stunning in this tangle at the bottom of the above chart, once we look at it under the microscope, is the surge of “nontraditional reserve currencies,” as the IMF calls them (red line in the chart below). These are dozens of smaller currencies, and central banks have been gobbling up their assets.

What is equally stunning is the decline of the Chinese renminbi (RMB, yellow), that became an official reserve currency in 2016 amid immense hoopla and was supposed to catch up with the USD. It made a little headway early on. But starting in 2022, its share has plunged amid ongoing capital controls, convertibility issues, and a slew of other issues.

The two currencies that gave up share to the “non-traditional reserve currencies” are the USD and the RMB. The world is diversifying away from them.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

For the first time in decades central banks own more gold than Treasuries as a percentage of reserves.

Gold is “reserve asset” on a central bank’s balance sheet, not a “foreign exchange asset” (securities denominated in foreign currency), which are a subsect for reserve assets. So gold doesn’t fit into here since this is about foreign exchange assets.

But yes, some smaller central banks have been buying lots of gold (not the Fed, ECB, and BOJ though)

Clouds with gold lining: The Central Banks diversifying into Gold has been the best news ever to a gold investor. After living the 1970s inflation, reading Roman history of debasing currency, etc. all over the world throughout history, leaves the conclusion people had halfway to the Ice Age of what to invest in. Gold to $6,000 a troy ounce; and going to a gold standard would put it in the 10s of thousands. Looks like time to roll up to a country club community in a tax free state.

With tariffs and much action to bring all forms of manufacturing home what might the outcome be in terms of who we would trade with?

Selling military hardware? China is using the economic for warfighting and for now seems to be close behind????

Many of the forms of making money will change with a high degree of knowledge and sophistication will preclude many here with good choices available in the past.

Amazing will be how the Baby Boomer 19 trillion wealth transfer will occur….