Bond market reacts to inflation expectations and supply of new bonds, not the Fed’s policy rates.

By Wolf Richter for WOLF STREET.

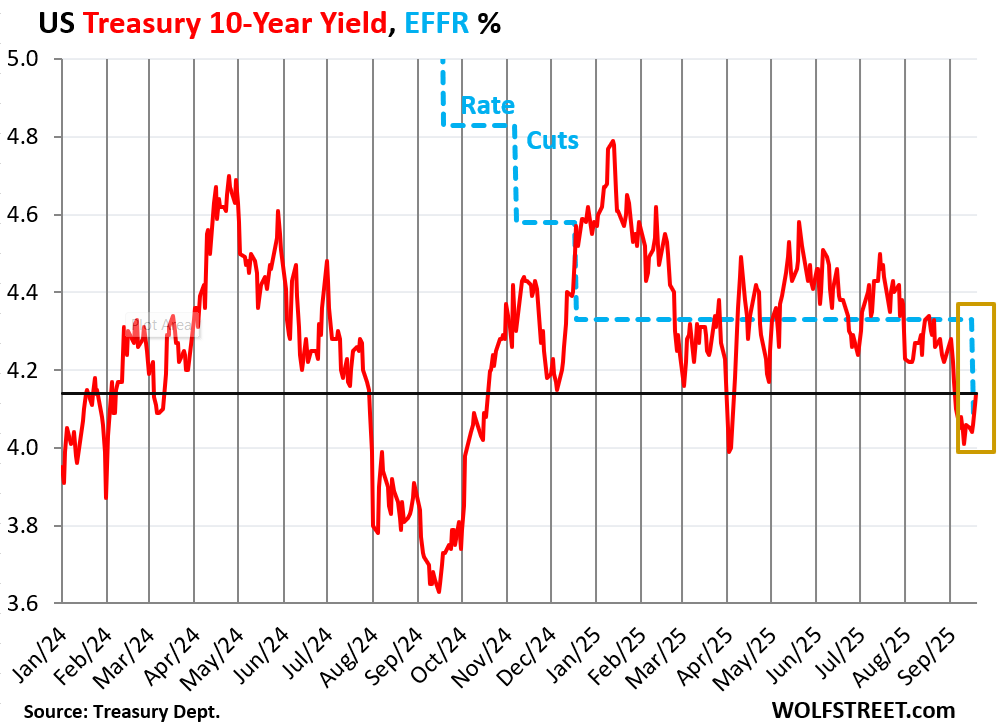

The 10-year Treasury yield closed at 4.14% on Friday, after having dropped briefly below 4.0% on September 11 (closing at 4.01%). On Wednesday last week, during an algo-driven moment, it also dropped to 4.0%, from 4.05%, then jumped right back to 4.05%, and ended the day at 4.06%, after the Fed had released its statement of a 25-basis-point cut. It then continued to rise to end the week at 4.14%.

The Effective Federal Funds Rate (EFFR), which the Fed targets with its five monetary policy rates, dropped by 25 basis points to 4.08% after the cut, from 4.33% before the cut (blue in the chart). The EFFR is now once again below the 10-year Treasury yield.

This phenomenon of rate cuts causing long-term yields to rise is rare – but we had it before, namely a year ago, when the Fed cut by 50 basis points at its September meeting, and the bond market got spooked by the sight of a lax Fed amid accelerating inflation. By the end of the year, the Fed had cut by 100 basis points, and the 10-year Treasury yield had jumped by 100 basis points, and the Fed, having learned a lesson, put further rate cuts on ice, and started talking hawkish, which succeeded in coaxing long-term yields – including mortgage rates – back down. But then the Fed went at it again with another rate cut.

This time, the Fed was more careful, less dovish: It cut only by 25 basis points, and Powell was less dovish than the statement even, and so the bond market’s reaction to the rate cut might have been a little less pronounced than it was a year ago.

But if the next few batches of inflation data continue along the worsening inflation trends, it could still spook the bond market further and lead to higher long-term yields despite the rate cuts.

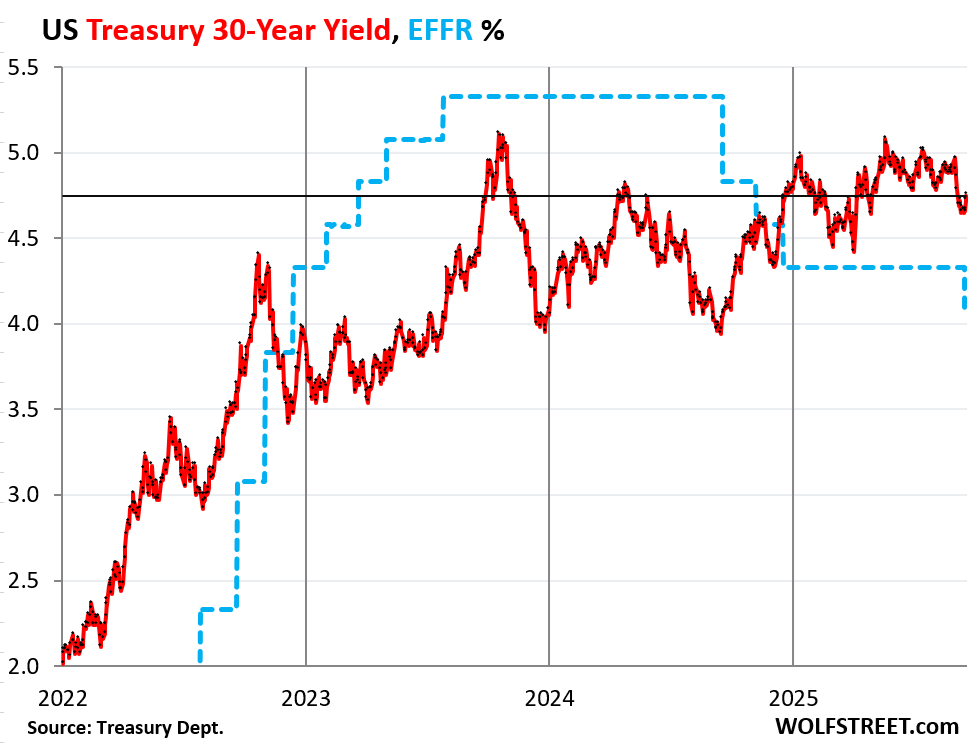

The 30-year Treasury yield ended the week at 4.75%, up by 10 basis points from the day before the Fed’s rate cut.

The upward trend of the 30-year yield started in August 2020 at 1.25% (after trading briefly at 1.0% in March 2020). By the end of 2021, it was at 2.0%, and by the end of 2023, just under 4%. It went over 5% in October 2023 and a few times briefly since then.

Note the divergence of the 30-year Treasury yield and the EFFR, as the 30-year yield reacts to bond-market issues, such as expectations of future inflation and supply of new bonds that have to be absorbed, rather than the Fed’s policy rates.

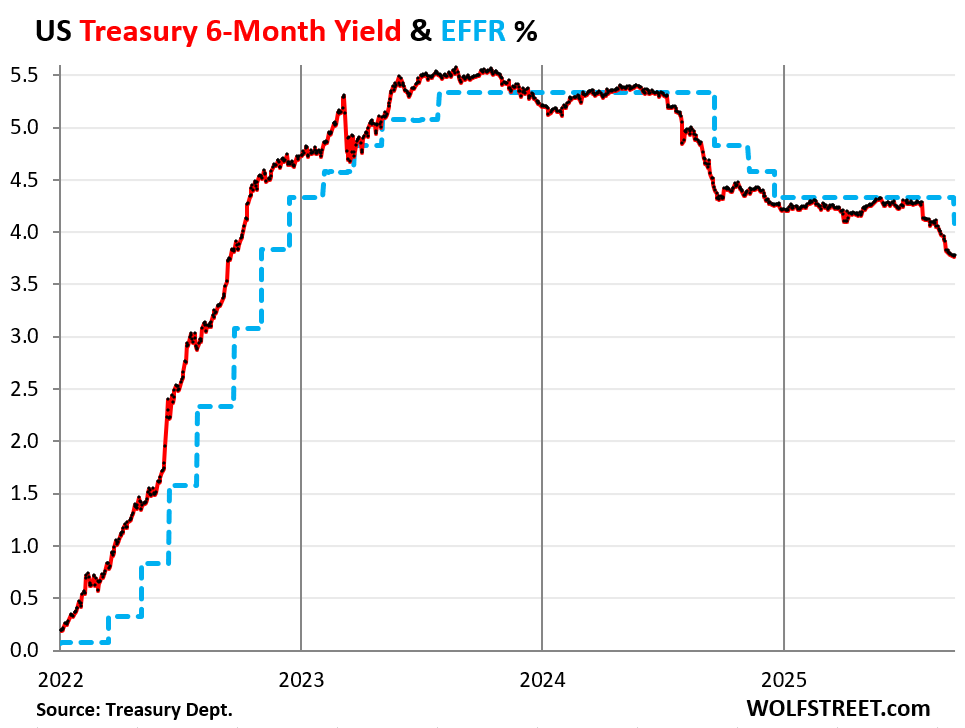

But the 6-month Treasury yield reacts to expectations of the Fed’s policy rates over the next two months or so and is a good indicator where the short end of the bond market thinks the Fed’s policy rates will be within its window. It currently expects another 25-basis-point cut over the next two months.

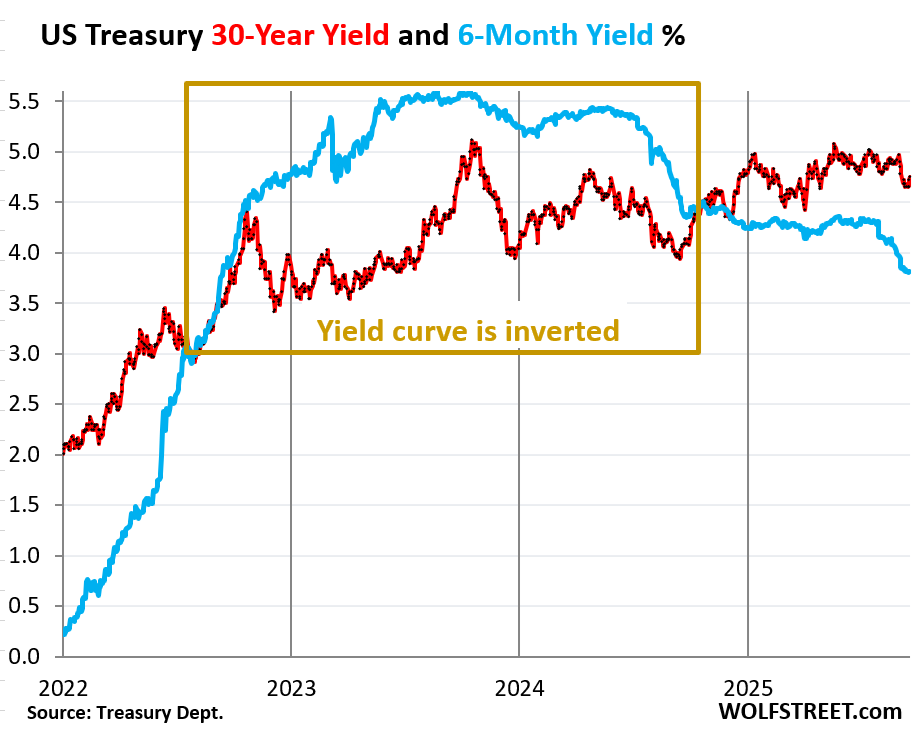

So the 30-year Treasury yield – which reacts to the bond-market issues of inflation expectations, supply of new bonds, etc. – has diverged dramatically from the six-month Treasury yield, which reacts to expectations of the Fed’s policy rates over the next two months.

That part of the yield curve – the 30-year yield and the 6-month yield – inverted in mid-2022 as the Fed was pushing up policy rates in 75-basis-point increments, and the 6-month yield stayed ahead of them, while the 30-year yield was only slowly disabusing itself from the Fed’s concept that this inflation was transitory.

But as the Fed was cutting rates in late 2024, the 6-month yield stayed ahead of those rate cuts and fell, while the 30-year yield surged, driven by an edgy bond market, and that part of the yield curve un-inverted in October 2024 and has steepened since then.

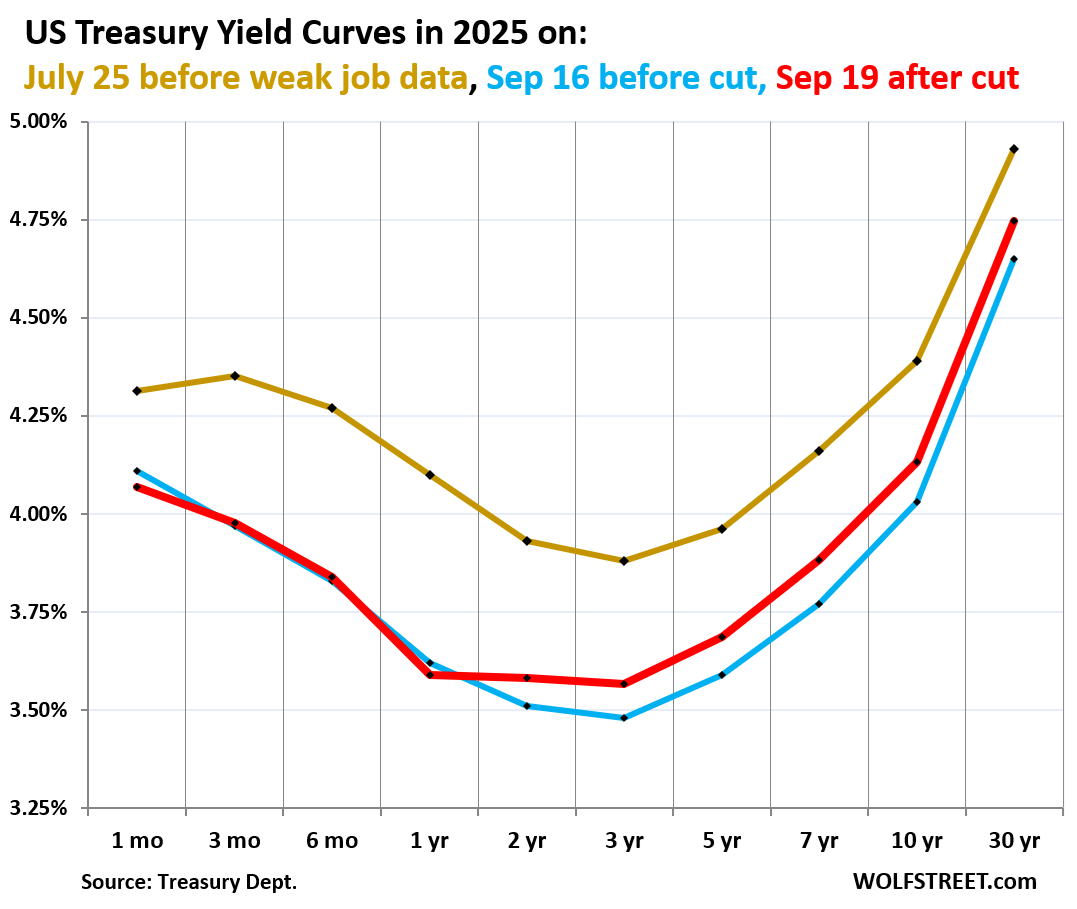

Yield curve steepened at longer end after rate cut.

The chart below shows the yield curve of Treasury yields across the maturity spectrum, from 1 month to 30 years, on three key dates:

- Red: Friday, September 19, 2025.

- Blue: September 16, 2025, just before the Fed’s rate cut.

- Gold: July 25, 2025, just before weak labor market data overpowered hot inflation data.

The 1-month yield is boxed in by the Fed’s five policy rates (from 4.0% to 4.25%) and closely tracks the EFFR.

The shorter-term yields are moved by expectations of the Fed’s policy rates, and they’re expecting more rate cuts this year and next year.

But the further yields go out on the yield curve, the more they’re influenced by inflation fears and supply concerns, with the 30-year yield being the ultimate test of them.

So from the two-year yield on out, yields have risen since just before the rate cut by:

- 2-year: +7 basis points

- 3-year: +9 basis points

- 5-year: +10 basis points

- 7-year: +11 basis points

- 10-year: +10 basis points

- 30-year: +10 basis points

Cutting policy rates during inflationary times is a delicate operation that has the potential of turning the bond market into a scourge. If inflation settles down in the 2% range, no problem. But if it continues to accelerate as it has done over the past few months, with services inflation being the big driver, and goods inflation chiming in and making it worse, then the bond market’s reaction to a lackadaisical Fed could get ugly.

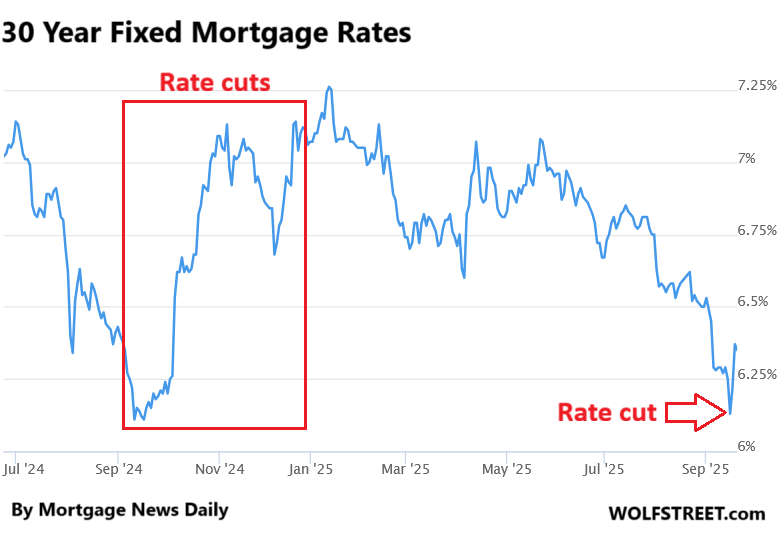

Mortgage rates have jumped more than Treasury yields: the daily measure of the average 30-year fixed mortgage rate by Mortgage News Daily has jumped by 22 basis points since just before the rate cut, from 6.13% on September 16 to 6.35% on Friday.

This is about double the increase of the 10-year Treasury yield over the same period, a replay of what happened a year ago after the Fed’s big rate cut.

These mortgage rates of 6% to 7% are now only a big deal because home prices exploded by 50% and more during the two years between mid-2020 and mid-2022. This home-price explosion was caused by the Fed’s reckless monetary policy that created 30-year fixed mortgage rates that were far below the raging inflation rates – better than free money, and when money is free, prices don’t matter.

But that’s a bubble-pricing problem now that should have never occurred, not a rate problem. The rates are fine. They’re historically at the low end of the normal range. The 5% and below mortgage rates were a creature of massive QE during the Financial Crisis and after, when the Fed loaded up on trillions of dollars of Treasury securities and MBS to push down long-term rates. But the Fed has been doing the opposite since the second half of 2022 and has shed $2.4 trillion of those securities as QT continues.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Ugly it is. So many factors at play. Afraid this 4 quarter will be dicey.

Was that a pushmi-pullyu interest rate move?

Right now the real estate market is dead here in the Swamp. The only houses on the market are dogs, (S$hit ass properties that nobody wants). No one in their right mind will give up their 3% mortgages and trade them in for a 6 to 7% mortgage unless they have to. Some Condos are coming on the market from investors who have finished converting rental apartments to condos. That’s it. Realtors here may as well start looking for a new career as nothing is going to change anytime soon. They are SOL (S$it out of luck)

Very understandable and predictable.

The US economy needs the bubble to burst.

It was wrong to inflate a bubble

It still is wrong for the FED to protect the bubble with lower short term rates.

All assets are priced too high

70% of the population owns a nominal amount of these assets

They lose no direct wealth from letting the bubble deflate on its own. The small job losses and future lower wage rate gains are worth deflating the assets.

The wealth effect, which used to increase spending by 50-60% of citizens, now only affects about 20% of citizen spending.

GDP, which is the wrong way to measure the health of US economy, will go down.

Who will be damaged by letting the bubble burst? The top 20% of households who own 90% of the wealth.

Stock market…..who should care. The owners who own on margin knew the risk, same for their lenders.

Bond market will be fine. Maybe true price discovery helps guide bond market; and stock market.

The housing market needs to drop 50% in most markets. Older, long time owners lose only the fake gains they thought they may have had.These owners are not leveraged.

The recent young buyers will be screwed. But some of them knew the risk.

The banks, who have loaned far too much on bubble asset values will have to eat the losses as the real estate market resets. Regulators, who are knowingly allow extend and pretend must stop this. Force the legal remedy of foreclosure, get the foreclosed housing stock back on the market, let Mr Market clear the excess with pricing. Many banks should fail and clear that market as well. No FDIC payoff of uninsured depositors either.

The CRE market is ripe for its own clearing.Developers and investors are big boys and girls, just like the foolish bankers who loaned the money.

The pensions and 401k accounts will be devastated, but the bubble values were fake gains. People will need to save more and spend less to build their nest egg.

Speaking of saving, why have the powers to be (deep state control of Congress ) felt it was correct or fair to put the thumb on the scale to help borrowers at the expense of savers. The savers are good people. We need to encourage savings so we have a pool of funds to loan to developers and entrepreneurs, instead of printing money at the FED.

and the Fed, how much worse could they perform on their duty of price stability and preventing currency ($$$) devaluation. The $ dollar of 1971 now with a penny! High school students throwing darts could have done better.

Do not open up the federal housing agencies from their current government control. Do not re-privatize. Actually, liquidate them. Let the private market fill in and grow. By the way, how many countries have a fixed rate 30 year mortgage guaranteed by their governments. This product helped create the housing mess.

The US economy needs real, transparent,unsubsidized markets and price discovery. Price discovery emanating hundreds of thousands of players each attempting to improve their lot in life, is a system that investors and the public a look to for stability.

All the government fixes, crony capitalism, GREENSPAN puts, do-gooders attempting to lower housing costs for the masses via subsidies, etc have ruined our economy. And do not try to say our economy is healthy.

Let’s go folks, support taking our medicine. Let’s get off the debt drug. Let’s get off socialism and crony capitalism. Let’s take our pain we have coming…AND GIVE OUR CHILDREN A CHANCE.

Just as expected. Just as predicted. Don’t these people ever learn?

The world changed on “Liberation Day”, Wed. 2 April 2025 and there was an immediate panic, but it has taken until the start of Q4 for the cracks in the whole system to really start to show. Are we in for a boiling frog or a Wile E. Coyote future?

Date that rate right? LOL, I’ll be lying if I say I am disappointed to see these RE agents and MSM will continue to loose steam on this narrative. Guess whoever they were able to sucker into this narrative recently with the drop in mortgage rates, better enjoy it while it last. At least for the mortgage brokers, they got some uptick in refinance business.

NAR, please be creative with your next BS narrative to drum up FOMO…these same old rate drops and never ending price increase talking points is getting really stall and lack any effort.

They’ll say something ridiculous like mortgage rates are high because there’s so much demand for them.

Wolf, I’d say some solid steepening is good news, but I fear that will encourage the administration to put even more of the debt they’re racking up and refi’ing on the front end rather than distributed around.

Damn, we DID create a FrankenMonster!

What’s next is anybody’s guess.

It’s not nothing that Fed still holds $3 trill Treasury securities and MBS.

Old job just cut 5 bids, the drivers on them are working whatever piecemeal crap comes down the line.

Landlord’s son just got placed on hold for work. Had to drive 200 miles for his last 3 weeks of work. At least 2 weeks with no jobs lined up.

I and a few others at my new job are going to 4 day work weeks since we are a common carrier and just lost a contract we were fulfilling because the other company has slowed down.

Like everyone says, housing won’t drop dramatically until the job market goes to crap. Over here in the trucking world, things have been a mess for years but it’s actually starting to get pretty bad now. Might be a long cold winter.

I still think a lot of younger people are sitting on the sidelines waiting for prices to come down enough for them to qualify for a mortgage. Until they are out of work in large enough numbers to chill demand, I don’t see much in the way of a major housing correction. The low end of the market is still selling like hot cakes here.

It USED to be, the DJT (Dow Jones Transportation Index/ NOT the meme stock) was a forward looking indicator of overall economic activity.

Now that the most valuable things are bits and bytes (including NFTs, Crypto and OnlyFans), we shall see how it plays out.

The index hit the ATH on a spike in Nov. ‘21, and failed to make an attempt to close higher than that day in question, until Nov/ Dec ‘24.

I imagine it rose then, in anticipation of the “stimulative rate cut.” The effect was unseen and by liberation day had slumped to hover above the pre-pandemic high range.

The 5 years of sideways movement sums up the consensus of the ”real economy.” We continue to wait for:

The Recession that Never Came