Result of withered demand: Days on the market in Los Angeles, San Diego, Orange County, Riverside, San Francisco, San Jose & Silicon Valley, Sacramento, Fresno.

By Wolf Richter for WOLF STREET.

The situation is this: Inventories are high, sales have plunged, frustrated sellers are pulling their homes off the market in large numbers, new listings are low because what’s already on the market is very slow to sell, and the number of days that a home sits on the market before it gets pulled off the market, or before it sells, has been soaring and in August hit the highest level for any August in the data from Realtor.com going back a decade. This situation is spread across all major metros.

This jump in the number of days a home spends on the market is occurring despite the surge in delistings where frustrated sellers throw in the towel and wait for better days, rather than cut the price and make a deal. Three of California’s markets are in the top 10 nationally on the list of Realtor.com’s ratio of delistings to new listings: the Riverside-San Bernardino-Ontario metro in the #3 spot (behind Miami and Phoenix), Los Angeles in the #8 spot, and San Diego in the #10 spot.

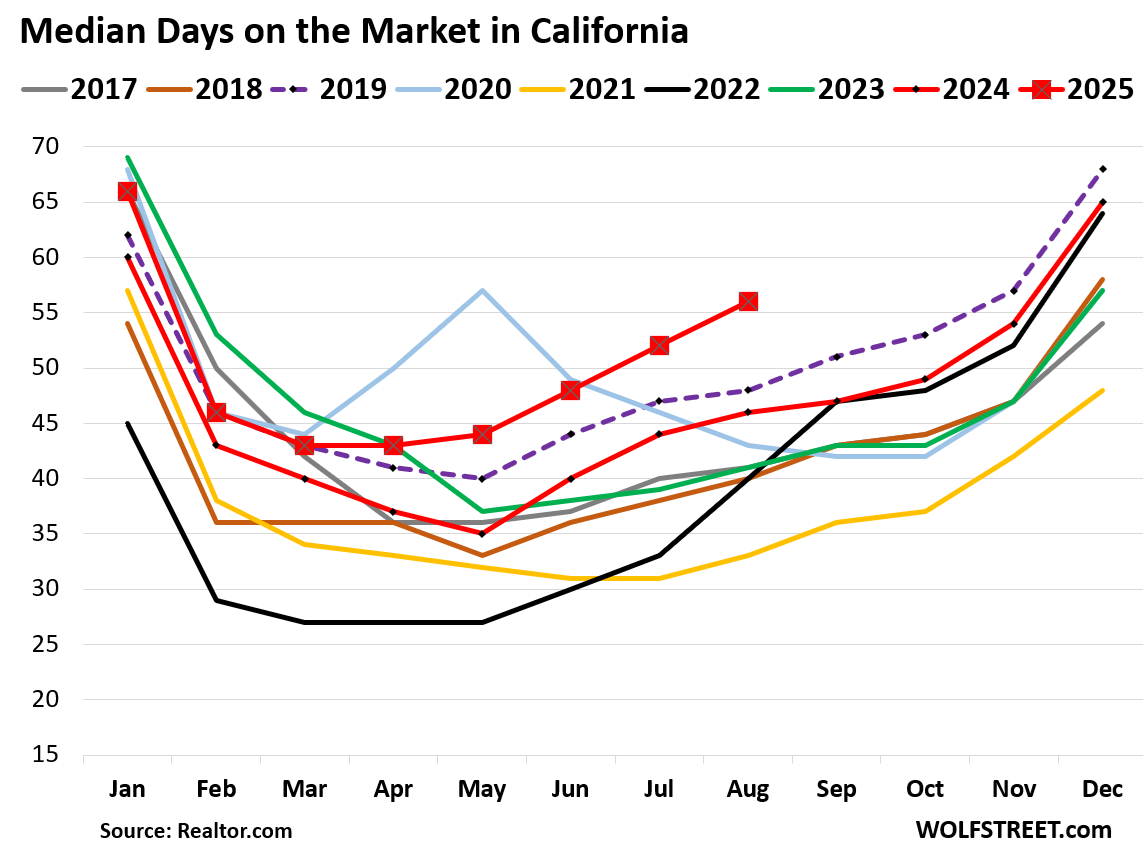

In California, the median number of days a home spent on the market before it was pulled off the market or sold jumped to 56 in August, by far the highest for any August in today’s data from Realtor.com going back to 2016, and up from the runners-up of 48 days in 2019 (dotted purple) and 46 days in 2024 (red).

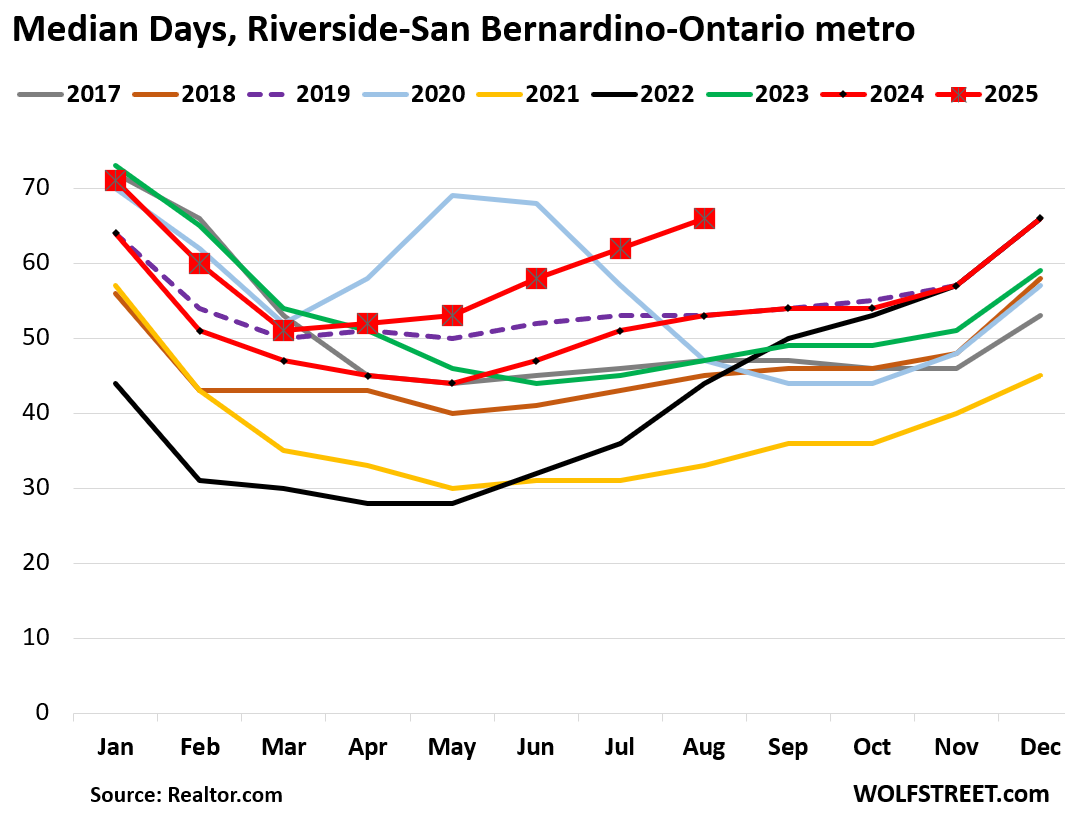

In the Riverside-San Bernardino-Ontario metro, the median number of days on the market before a home got pulled or sold jumped to 66 days in August, by far the most for any August in the data going back to 2016.

In the Augusts of 2017 and 2018, homes sat for 47 and 45 days. In 2019 and 2024, the two runners-up, they sat 53 days.

In terms of delistings, the metro was the third-highest in the US, with 34 delistings for each 100 new listings, up from 30 two months ago, and up from 18 in May 2024.

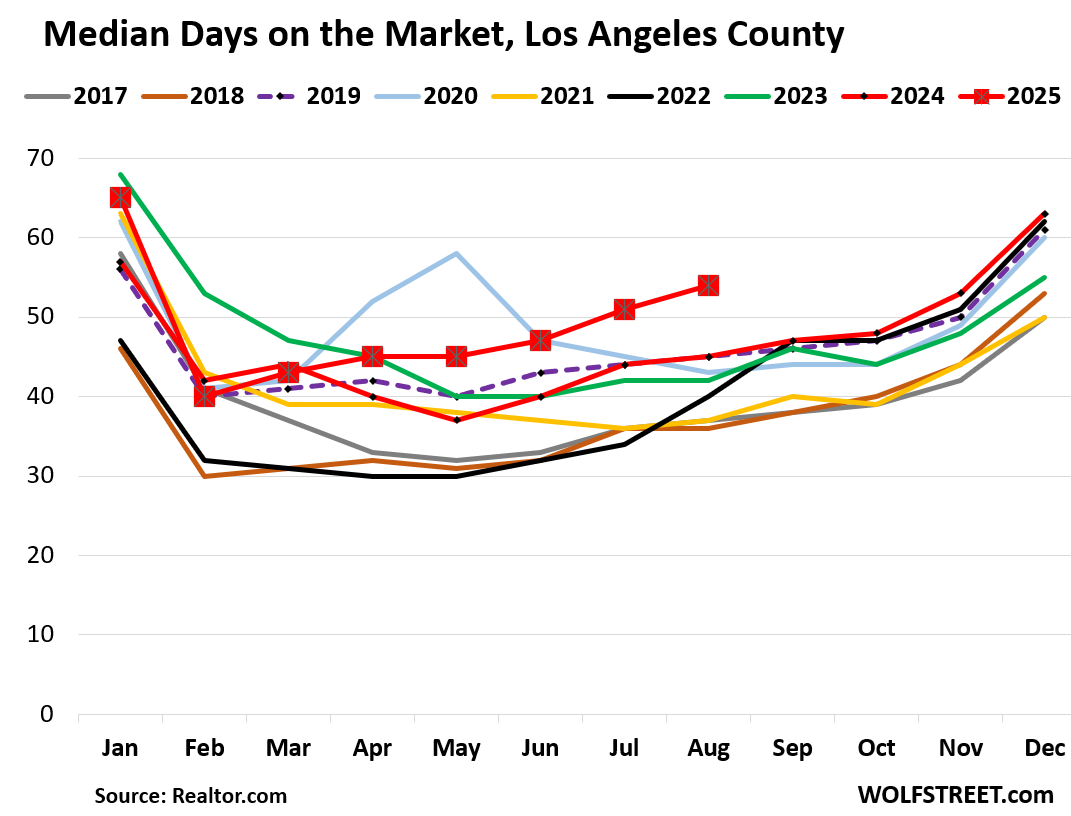

In Los Angeles County, the median number of days a home spent on the market jumped to 54 days in August, by far the highest for any August in the decade of data.

The second-highest August in the decade was 45 days in 2024 and 2019.

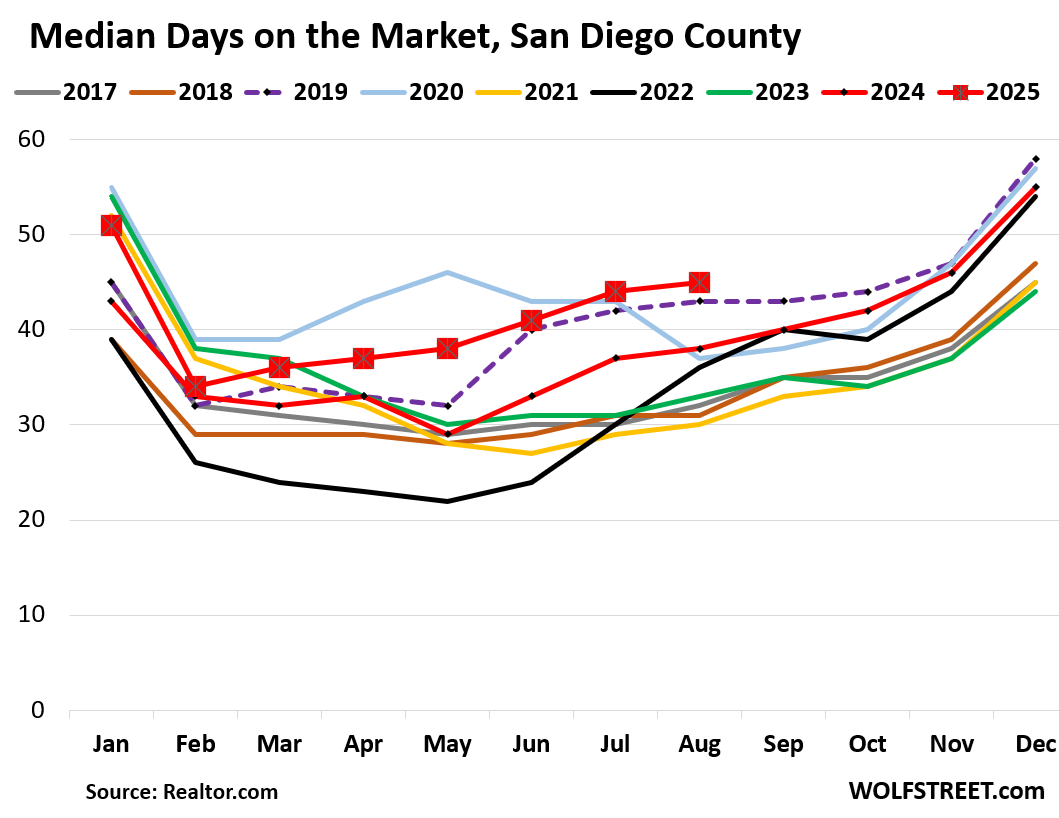

In San Diego County, the median number of days on the market rose to 45 days in August, the most for any August in the decade of data:

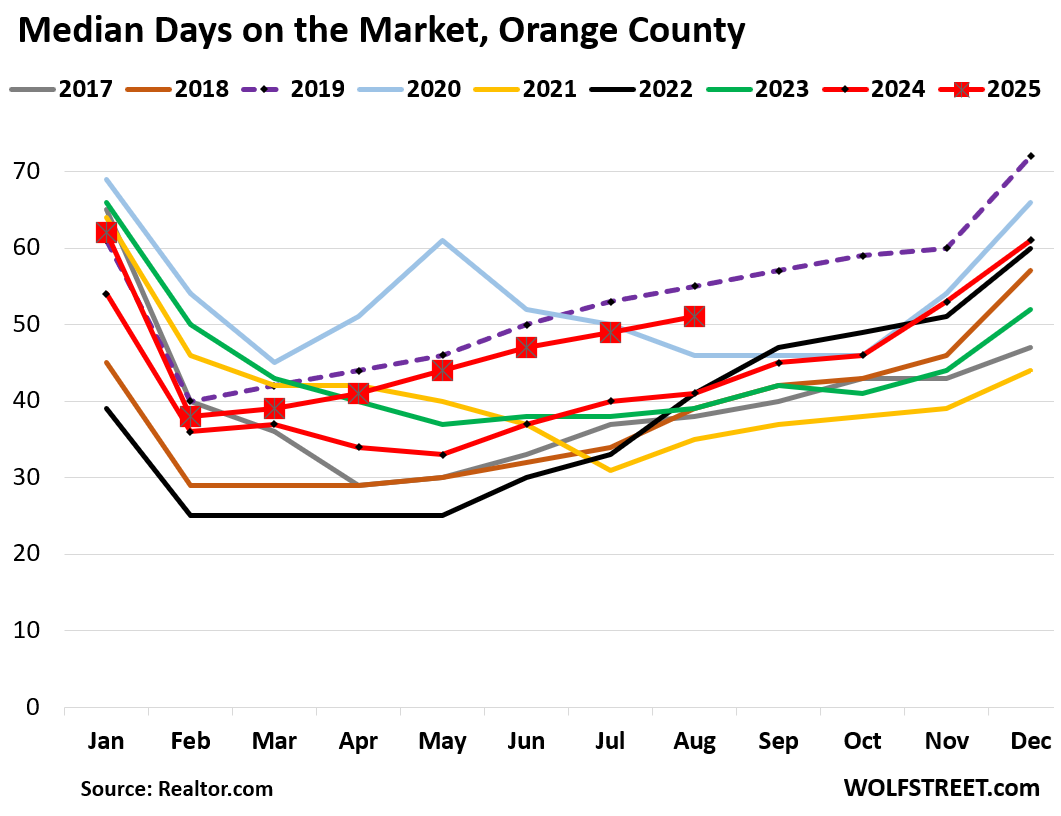

In Orange County, the median number of days on the market rose to 51 days in August, the second-highest for any August in the decade of data, behind only 2019.

Orange County is the only major market in California where days on the market has not yet reached a decade-high, due to the high readings in 2019 (dotted purple):

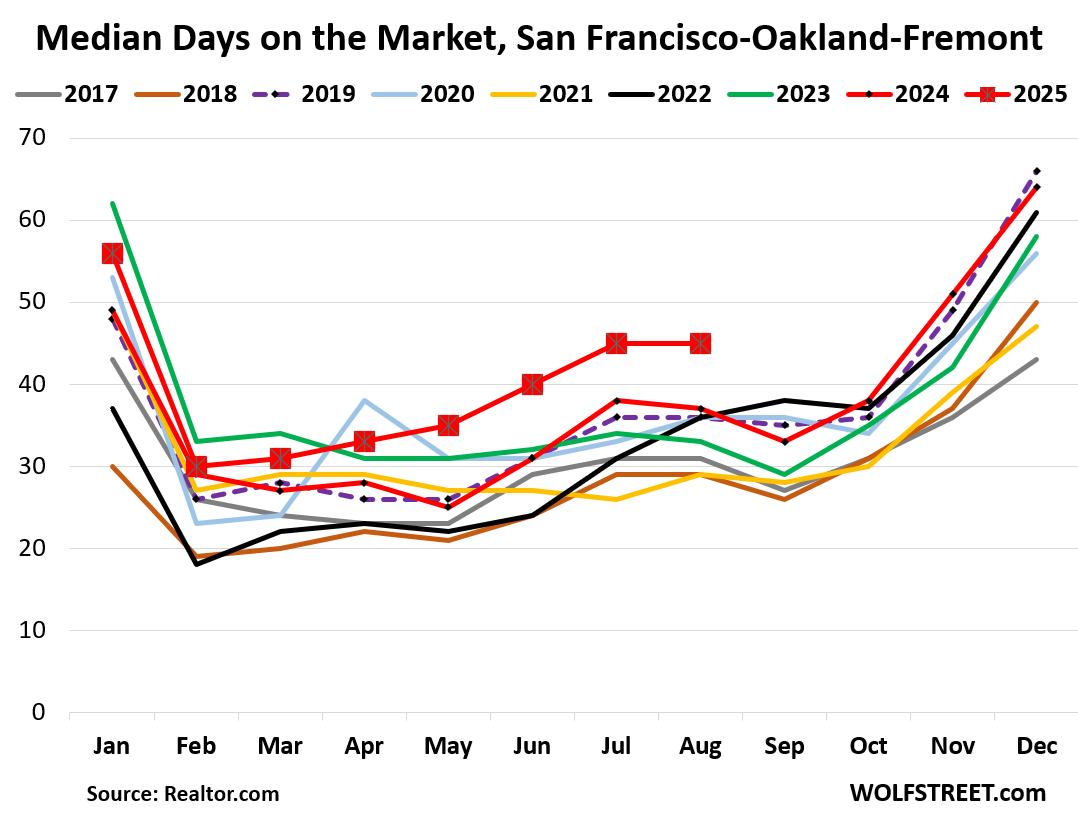

In the San Francisco-Oakland-Fremont metro, the median number of days a home spent on the market remained at 45 days in August, same as in July, and by far the highest for any August in a decade of data.

The runner-up was August 2024 with 37 days. In 2017 and 2018, homes sat for 31 days and 29 days respectively before they were pulled or sold.

This metropolitan statistical area (MSA) includes the counties of San Francisco and San Mateo (northern portion of Silicon Valley), part of the East Bay, and part of the North Bay.

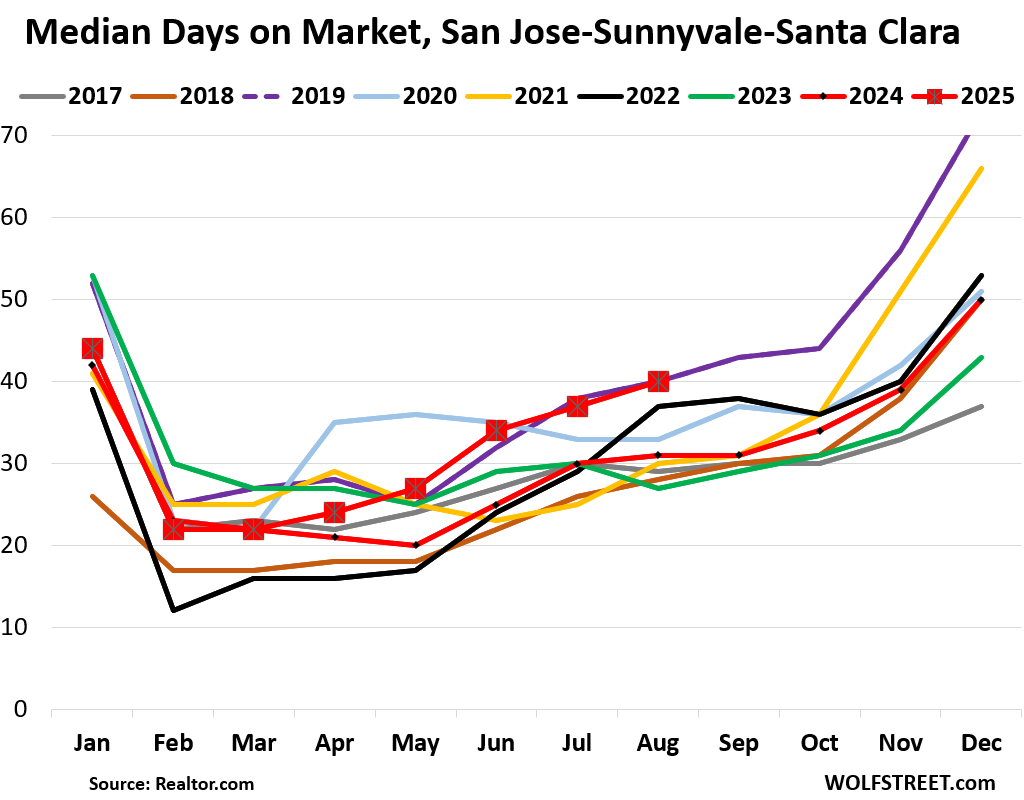

In the San Jose-Sunnyvale-Santa Clara metro, median days on the market rose to 40 days, along with August 2019, up from 31 days a year ago, and along with 2019, the highest August in the data.

The MSA includes Santa Clara County (San Jose and the southern part of Silicon Valley) and San Benito County, which extends south into rural areas.

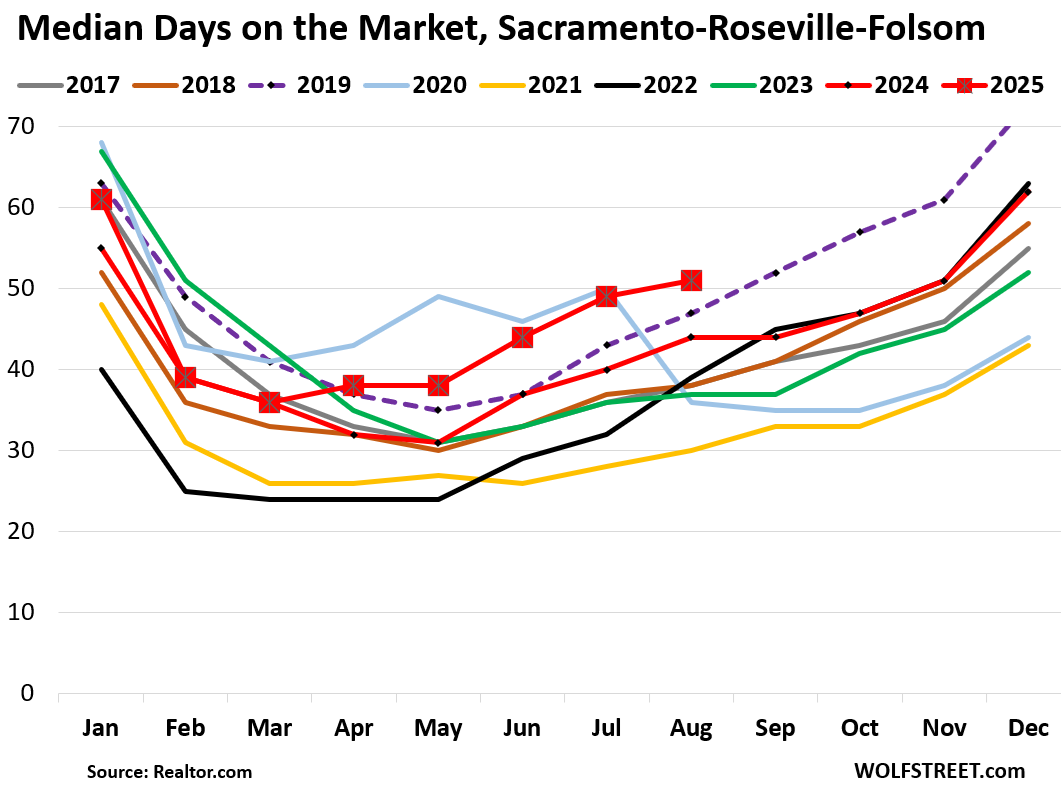

In the Sacramento-Roseville-Folsom metro, median days on the market rose to 51 days, the highest for any August in the decade of data, up from 44 days a year ago, and up from 38 days in the Augusts of 2017 and 2018.

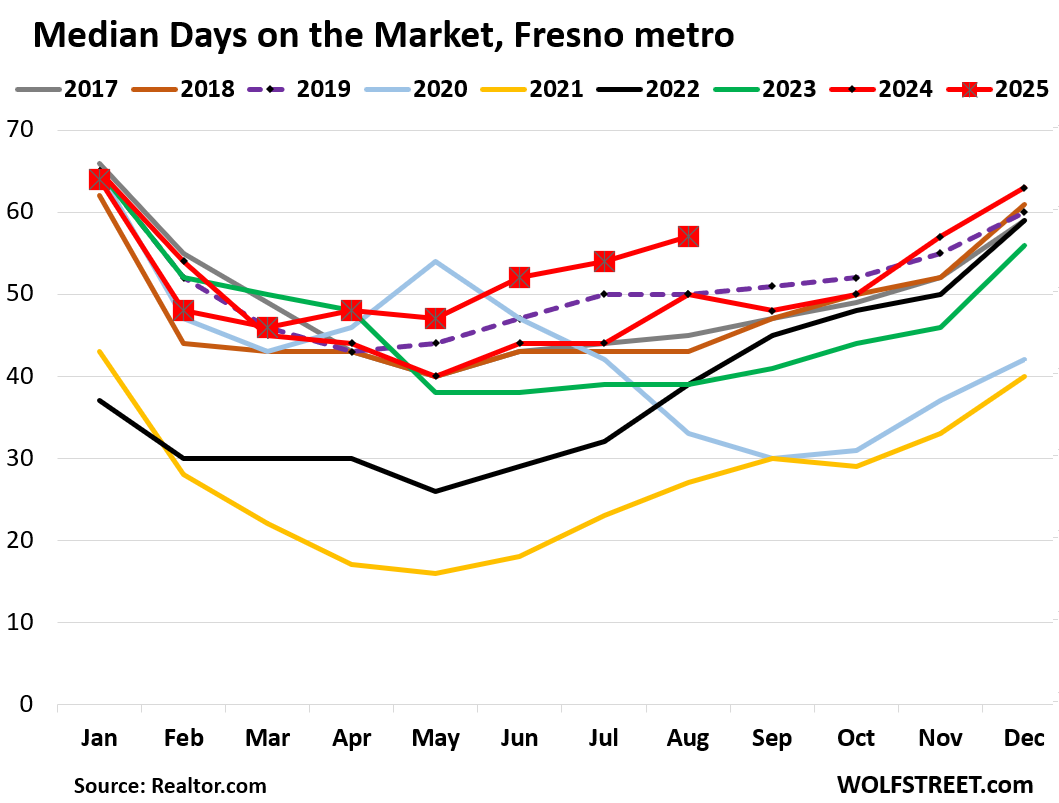

In the Fresno metro, the median number of days a home spent on the market jumped to 57 days, the highest for any August in a decade of data, and up from 50 days in August 2024 and 2019, the second-highest Augusts in the data.

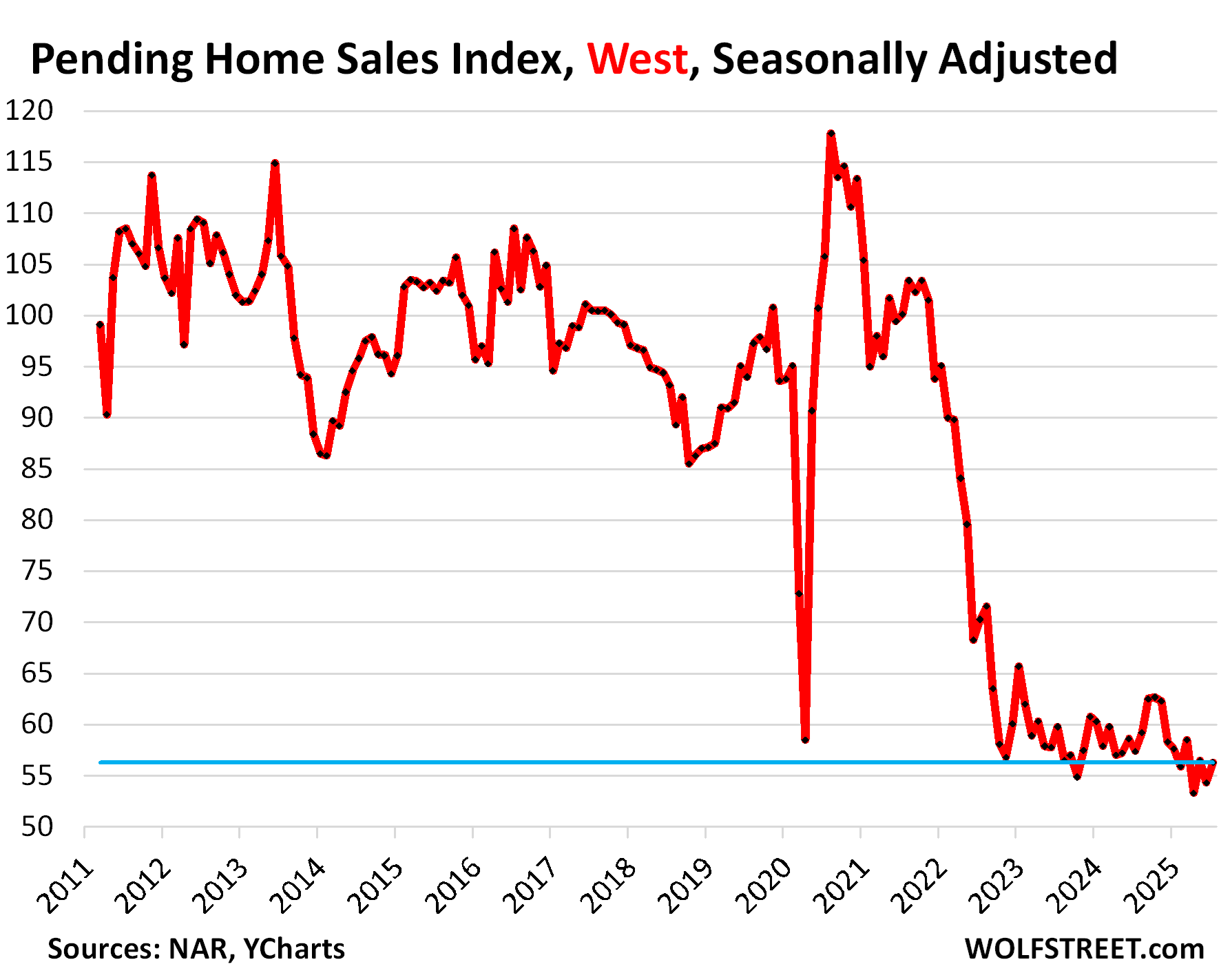

Because demand has plunged. Pending sales of existing homes in the West – which is dominated by the huge housing market of California – were down by 40% from 2019, according to the National Association of Realtors at the end of August. This is what persistent demand destruction from too-high prices looks like:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Time to pump the market then

You know MSM is busy trying to bouce that deadcat as much as possible…saw a new headline this morning….oh better get in now before it’s too late…lol

“Mortgage demand jumps to the highest level in three years, as interest rates drop sharply”

Hopefully this trend will keep up so I don’t have to continue to see every old crapshack listed in Long Beach or OC for minimum $1M as the baseline.. a lot of them have no business asking for more than $600k before the insanity of 2021 to now, they can play these delist and hope for a better day tactic but I hope they just end up chasing the market all the way down ..

The too-high listing prices are the reason demand has plunged and homes sit so long before the get pulled… To make a deal, sellers need to be realistic.

100% its the real estate agents blowing smoke up everybody’s skirt! Some of these homes that are only 1200 square feet. Our priced in the six and sevens, it’s ridiculous!

In Reno NV,Carson City area its even worse if the home has 1 acre..but its a shitshack that needs updating. Minden area? Laughable prices! And then they reduce by 1k or 5k to boost it back in everyone’s email.. sorry.. come down to reality. Especially with rates in 6’s. Oh there’s buyers, Im one of them, but Im not dumb enough to over pay. So, waiting…..

Come on down to low cost markets, where $200k still buys you a very nice, large house. A little Zillow tourism will reveal the places I’m talking about.

Is it the RE agents or sellers being unrealistic? Combo of both maybe?

I imagine that coaching sellers to accept lower prices is a tough conversation… “my neighbor got $xxx,xxx last year after multiple offers, why do I need to cut my price?”

The agent gets diddly squat from the property just sitting, so in theory they should be motivated to bring the seller back to reality.

My auntie lives up north around Sacramento. We encouraged her 3 yrs ago to sell. She refused. She now refuses to lower her price (her asking price is unrealistic) AND she is disabled. She is now asking family to start helping her …….financially. We’re not. She’s pissed.

Oh good old greed and a little bit of FAFO…still not too late now if she is more serious about them price cut…

Completely agree Wolf. My hope is that people in SoCal are not so easily sway into FOMO again if sellers drop a tiny 3-5% or if mortgage rate dips another 1-2% and all of a sudden even above million, because of some drop, they plow into the market again…

Two couples I know recently bought at $1.2 and $1.3M despite the homes being “mid” as what my kids would call it….so I am not holding out that much hope that people will now JOMO instead of FOMO and truly wait for some serious price correction before piling back in, hope I’ll be wrong on this.

Phx, one problem is there are boatload of people exactly like you all waiting for the same thing, at different degrees of anger/angst/desire. If their buy in levels are higher than yours, you’re going to be in for a long wait. Especially if you trim your bid down as prices fall.

I was you for 20, maybe 30 very long RE years.

Sentiment can change very quickly. If it’s clear prices will be lower next year for the same property, people will wait. This is already happening in Austin and Denver and SF, SoCal is probably next.

I live in a cul de sac of 1 to 2 acre homes at about 800k to 1 million. We are right next to 1 acre newer homes at 1 to 1.5 mil. About 13 of the 20 homes have people between 60s to 80s. It looks like there will be an onslaught of homes being sold in the event rates go down. This are properties that offer much due to large desirable lots near freeways, shopping in Riverside. Still, it looks strange to see no clear path ahead with all the chaos. Inflation makes it hard to gauge the value of buying or selling. Even those like my wife and I have excellent retirement and the potential of generational wealth transfer and still the uncertainty gives pause as we have a great home on a horse ranch with all needed within a short drive. The houses being put on the market are desperation sales and although the sales are taking longer the good stuff goes fast. The flippers are gnashing their teeth like the coyotes that scour the region.

Much of the grumbling here sounds like grumpy men who just hate the reality of what is going and still none of us have any clear picture and likely this will turn into turgid waters for sure…

“…this will turn into turgid waters ” – or, perhaps turds in the water – time will tell. (user name checks out)

Welcome to the “suck” +

It’s very simple. Prices are too high. I am in Southern California and am actively in the Ventura, LA and Orange County – and a little of San Bernardino county markets. When a property is priced correctly, it sells quickly. We saw such large upward price moves – particularly in more Covid friendly geos (like the desert) that sellers are unrealistic. In addition insurance costs – or the inability to access viable insurance – seem to finally be influencing pricing – which is long overdue. That issue will get worse once we pass January 7, 2026 – the date the moratorium is lifted for insurance to cancel policies post the palisades and Eaton fires.

“Too high listings price” is not the cause of this demand plunge but the consequence of other changes.

Is it really so hard to admit what is causing this demand plunge or too inconvenient or unpleasant political truth?

Too-high prices destroy demand. That’s how markets work. Sellers cut prices until buyers are interested again and demand picks up again. When there is lots of demand and not enough supply, prices rise again. That’s how a normal market functions and balances out.

But the housing market is sick. It doesn’t function like a normal market anymore. Prices are too high, but instead of lowering prices, sellers hang in there, pull their homes off the market, eat the costs and inconvenience of holding on to the home, and potential buyers just stay away, and transaction volume collapsed.

By contrast, in the office sector of commercial real estate — these are all professionals — the market has completely reset after being completely frozen for a year. Depending on the market, prices have plunged by 40-70%, and now there are lots of transactions at these much lower prices. And it’s clearing up the mess.

Yes, high prices do this. the complexity of all this is astounding. I am a builder, the trades are becoming a big ripoff. The insurance companies are leaving because the government fire agencies cannot guarantee the response necessary for insurance companies to assess risk (given this info by Costco offer of home insurance). I am looking to build east of San Diego County in Alpine, Julian, Pine Valley, or Descanso. If you build, the fees are outrageous and you CANNOT get fire insurance in many cases due to being out in the country where there is acreage to buy, the fire hazard is at the highest. I will have to build high cost fireproof home with major clearance of plants and trees away from the house and good luck with my need for a shop and a horse barn with no fire hydrants in proximity. California purposely does not want anyone to build except in the 15 minute cities, in apts, with no car. Sure, I will send my wife and 3 grand kids on a bus so they can be attacked by a crazy nut homeless person. California is the problem. Good luck with fixing it.

In the end, CA has 40 million people 95% of whom want to live in that 30 mile (+/-) wide coastal strip that makes California…California.

(Go much further inland and the weather can approximate LV or Phoenix…with insane taxes and hour long commutes each way to job centers).

(And that coastal strip *really* only runs as far north as SF…and not so much if Mark Twain is to be believed – “The coldest winter I ever spent was a summer in San Francisco”).

These kinds of comments are ubiquitous and insane. These forests haven’t burned in a hundred years *because* people keep building out there and now they’re overgrown. There is absolutely nothing stopping you from building your house in a lake of gasoline if you want to. Instead, the problem is not that the state is telling people like you that you can’t build out there, it’s that the state won’t use the city-dweller’s tax money to subsidize those who choose to live in the forest with their own personal power lines, water mains with hydrants, their own firefighting force, as well as to absorb all of the risk of loss on a structure that the private insurance companies won’t touch. Meanwhile, the services that the state does provide because they are cost effective, such as public transit, are somehow unacceptable. At some point, people who want to live the libertarian lifestyle out in the country need to realize that they can’t have it both ways.

Sounds like you want all the people living in cities to subsidize the installation of hydrants & fire stations out into the wilderness so you can save a few bucks on a box-of-kindling home in a wildfire zone.

Fire hydrants aren’t even installed by the state- they’re a city or county responsibility. If you want more hydrants in Alpine, Julian, Pine Valley, or Descanso, then you need the local governments to raise the taxes to pay for it.

@grant The cities used to have redevelopment agencies that handled that before CA had pulled that money to weather the Great Recession in the 2000s.

Banks always screw it up for the rest of us…

Even if something else is causing the demand plunge then that still means that the listing prices are too high based on the new demand.

Any other stupid statements?

It isn’t complicated. Prices went up 30-50% during QE because mortgage rates were ridiculously low. We are now 2 years into QT, mortgage rates have normalized, and prices are falling.

What do you think accounts for the decline in new listings?

It was mentioned multiple times in the article: “new listings are low because what’s already on the market is very slow to sell, and the number of days that a home sits on the market before it gets pulled off the market, or before it sells, has been soaring”.

Prices are too high, plain and simple.

Some people are sitting on interest rates that they got when they weren’t real,like 2 and 3 %. We will never see those again

1. Why list when there isn’t enough demand to sell what’s already on the market?

2. People with 3% mortgages aren’t moving. They’re not buying, and they’re not selling. See my story about the divorced couple with young kids living together — he in the house, she in the Airstream trailer taking showers in the backyard — because they have a below-3% mortgage and want to preserve it.

In a way, the divorced couple example goes against what many of us have said in the comments: that “life happens” and some people are forced to move. Granted, this example is very likely rare because it made the news as a single example, not dozens of couples like this. So divorces will still unlock homes available for sale. Although with fewer people getting married historically within the past couple decades, this method of unlocking homes is decreasing.

With the labor market fairly locked up, it looks like primarily death and some divorces will unlock homes available for sale.

“Although with fewer people getting married historically within the past couple decades, this method of unlocking homes is decreasing.”

Works both ways though – marriage/kids are one of the primary drivers of SFH *demand* – no marriage, no kids…let me have my cheap studio apartment…

I would chime in that you stating that couples who get divorced and have to make “alternative life style changes” in housing is not rare, given that a great number of people were affected by the Ponzi scheme of inflated home valuations in the Countrywide loan debacle (2008) that continues to effect the real estate market. I was there doing pro bono work for the families that were destroyed by the pump and dump scheme. At least someone went to jail.

Makes sense. I guess the potential sellers go to the realtors and are discouraged from listing because of the glut sitting there?

Haven’t some of these areas become uninsurable? That takes those buyers who need mortgages out of the equation in many cases.

And creates gunshy cash buyers…

Insurability is only a part of the unaffordability calculus in California. Under-insurability plays a much more significant role in creating sales barriers. The CA Insurance commissioner, cowtowing to carriers, has permitted exhorbatant rate increases affecting all areas of the State.

No, not really. There are very few areas in San Diego or SOCAL that are uninsurable.

The reality is no one wants to pay $1.5M at 7% interest for a normal 30 year old house in the suburbs.

People like you are hilarious. You’ll come up with every excuse besides the price.

“The reality is no one wants to pay $1.5M at 7% interest”

7% is low. Over the last 53 years – US 30 year home mortgages have averaged 7.71%.

Correct, Mark. But prices are historically high. So they will fall.

“The reality is no one wants to pay $1.5M at 7% interest for a normal 30 year old house in the suburbs.”

Of course.

And a reflection of how much ZIRP induced insanity was created at 3-4% mortgage rates.

Anddd…this is the second go round of the massive insanity since just 2004…

Yes i’m a californian native, the insurance is absolutely insane, and that did for a while. Drive some prices down, or the seller was more willing to make concessions.

Now it’s a triple whammy insurance, taxes, and interest rates.

Some places Northern California, I have dropped into a more reasonable market. But then you’ll see some that are priced very outrageous. So you could say it’s all over the map. Listing agent should be more reasonable, but most of them will just take a listing and let their seller drive the train instead of educating them. They lose control of their client.

Not “uninsurable,” but expensive to insure, like in lots of other places.

One reason insurance is more expensive is that home prices have soared so much, so the cost to the insurance company in case of a loss is so much higher. There are no free lunches. Higher home prices = higher insurance.

And for buyers in CA, higher home prices also mean much higher property taxes.

And higher home prices also mean higher transaction costs: 6% of $1 million is a lot more than 6% of $500,000.

Too-high home prices suck the bejesus out of the economy.

I neither live in California nor understand fully how typical single family home property insurance works. But perhaps insurance rates aren’t just increasing because of wildfire risk. How much of the premium increases are due to earthquake and tsunami risk? The latter two are low-probability but high-cost disasters. With each passing year without a “big one”, the annual risk of it happening increases.

Of course there are other factors at play too, like cost of material and labor, which have increased exorbitantly in recent years.

Earthquake risks play ZERO role in dwelling and homeowner insurance as they are completely and categorically EXCLUDED from any coverages which is available on on separate CEA (California Earthquake Authority) policies at very high premiums and with very high deductibles. This has been the case since 1994.

Tsunami’s are also EXCLUDED from coverage on dwelling and homeowner policies and would only be covered by a separate NFIP (National Flood Insurance Program) flood insurance policy as such damage would be caused by external ground water.

In California, earthquake and tsunami insurance are not part of standard homeowner’s insurance and need to be purchased separately. So those risks aren’t a factor in the increase in the cost of standard homeowner’s insurance policies which cover wildfire risk. I’m starting to wonder if wildfire risk should also be separated from a standard homeowner’s policy in California so it can be more flexible regarding the deductible and coverage.

It doesn’t help that California has an insurance commissioner as compromised as Ricardo Lara. I realize that you seek to avoid political discussions, Wolf, but Lara’s a major reason why insurance is so out of whack in the state.

Honestly, I was skeptical of your claim considering it is political, as you mentioned. However, investigations into his tenure have shocking results.

Wolf, I know you generally block hyperlinks but this investigative piece by ABC7 Bay Area really drives HollywoodDog’s point home. The level of absence and fraud is astounding.

https://abc7news.com/post/ca-insurance-commissioners-attendance-record-in-question/16045912/

May we all hold our elected officials accountable to not generate these sorts of taxpayer-funded expenses.

“Too-high home prices suck the bejesus out of the economy.”

Heh…isn’t this point where the Fed starts lecturing about optimal employment level paths and wealth effects?…no free lunch indeed.

57 days to wait it out in Fresno might seem like a lifetime.

The question to me is who capitulates- buyers or sellers and when that happens.

If rates drop, then demand should increase due to better affordability. If rates stay where they are, sellers may need to drop the listing prices. Hard to see a scenario where the status quo stays that way.

“The question to me is who capitulates- buyers or sellers and when that happens.”

Maybe nobody capitulates. The path of least resistance is that builders keep taking a larger share of transaction volume from existing home sellers by reducing prices outright and through incentives.

Warren Buffet seems to think so. He started buying builders.

Our vacation home in Glendale, AZ (our main home is 85 miles away in Prescott) that we owned for 10 years took 5 months and 5 price reductions to sell. I am a REALTOR-active.. and I understand the market. Our decision was to get out; to turn a non-performing asset we were not using much to cash. Yes, we took a beating compared to a few years ago but we also enjoyed a reasonable profit. Sellers need to gain perspective; the market is not what it was; there were false highs and false gains; on paper. Get realistic and move on. Holding out achives only one thing; you use up time. Time is one thing you cannot buy.

One of my saved Zillow homes sold for ~385k in April, was just relisted ~525k. What was upgraded? Well they pull all the door jams, the outlets and other electrical fixtures and cut a few holes in the walls.

It won’t sell for the foreseeable future so I’m going to wait, and lowball tf out of them in 6mo. Or a year if it’s still up. You reduce homes value then bump the price up 50%+ in a few months? Nah.

Yes, exactly. The 2021 and 2022 bubble pricing was due to a confluence of factors that all came together in a perfect storm, from remote work, to low interest rates, to QE and MBS purchases, to general FOMO manias.

It was a temporary blip. That wasn’t what things were worth. It was paper gains that disappeared as fast as they came. It was like people who were reselling ammo or toilet paper during the shortage in 2020. You had a very small window of opportunity to get out at the peak, and most people didn’t, but hung on thinking prices would continue to go up. They didn’t, and that’s exactly what happened with housing prices.

@TSonder305 wrote: “Yes, exactly. The 2021 and 2022 bubble pricing was due to a confluence of factors that all came together in a perfect storm, from remote work, to low interest rates, to QE and MBS purchases, to general FOMO manias.” I don’t hear many people talking about it but a BIG reason for many areas spiking in price is that remote work allowed thousands of high paid workers to move to lower cost areas where they bid up prices that still seemed “cheap” compared to where they were moving from (there are examplae all over the country but in CA this happened with many people moving from the Bay Area to Tahoe and LA/OC to the desert)

I monitor N. Boise. The market in that area is very strong. It is however, a niche area. Micron, ag, gov’t jobs…nearby skiing, beautiful infrastructure, good medical, pretty nice climate, good schools.

Compared to SV or LA it is ‘living the dream’ at less than half the price. It’s still about location. When the location has it all, there is typically no way to replace it. People will pay up.

Yes, I’ve written about that extensively. Remote work temporarily caused housing prices in desirable areas to reset to the incomes of the highest paid parts of America, like NYC and the Bay Area.

That was never going to last.

Great points and a taste of reality.

Multi units in select areas of the Bay Area are now reasonably priced. The challenge is insurance at any price.

@David Where are you seeing “reasonably priced” multi-unit properties in the Bay Area? What cap rate and price per unit do you feel is “reasonable”? I still see deals that are showing a 4% cap rate but with “real” vacancy and “real” expenses (including “real” capx reserves) the cap rates are closer to 1%. P.. l am starting to see some “reverse FOMO” where both residential and investment brokers are trying to get people to sell “before prices go even lower”…

There is a 10 unit in unincorporated alameda county right now that I’m trying to negotiate. It’s priced at 10x GRM which is well below the typical pricing. 10% gross yield. Subtract taxes and insurance (if obtainable) and it’s 7%, subtract repairs and it’s 5% or so, unlevered. And mostly tax free with depreciation.

Last time I saw 10x GRMs was 2010 ish.

5%? Let’s not forget managing that is a job and a headache, so the ROI effectively is 0% or negative. Why bother with this hassle when you can get a 30 yr risk free T bond that yields the same considering no state tax obligation? Appreciation potential on the RE? Could be an unfulfilled wish.

David,

I’m wondering the same thing as Dr. Ben. How can a 5% return (absent appreciation) justify owning this 10 Unit?

What about Management time/expense and what about capital improvements/replacements? 2% might cover maintenance but I can’t see how it covers maintenance AND any needed capital improvements/replacements and/or a reserve for future capital improvements/replacements?

As you are probably aware, Depreciation isn’t tax free (it’s recaptured via a tax of 25% at time of eventual sale), but it does defer the tax for as long as you own the property (and potentially longer if one does a 1031 exchange).

Curious on your thoughts?

@Kile I don’t want to answer for David and I won’t be buying any investment property at 10x gross rents today but when I was younger (and single and basically working two full time jobs) I would have since (doing ALL the work myself) I would have had positive cash flow and the levered cash on cash return on real estate investment was crazy high. All those years when Bay Area Real Estate went up by 5%-10% a year I was getting a 20% to 40% return on my 25% down payments (plus the positive cash flow). Looking back I might have done just as well if I got my contractors license and worked the same hours for others managing and renovating apartments on nights and weekends and invested all the money I made in the S&P 500 (that has gone up even more than Bay Area Real Estate). At the end of the day I’m happy since I have been able to work an average of 20 hours a week for the past 22 years since I got married and spend more time with my kids than most people, thanks to 1031 exchanges I have never had to pay capital gains taxes or recapture depreciation. I’m on track to have $0 debt by the time I turn 70 and even with the worst managers in the world my property will spin off enough cash to support me, my wife and kids even if all of us become disabled and need to live in a home.

Thanks wr for this report.

Prices need to fall 50 percent to bring sanity and I am confident this wont happen

Rates are trending downwards anyway

“Prices need to fall 50 percent to bring sanity and I am confident this wont happen”

Prices fell 50% in some CA markets during ZIRP Bubble Bust 1.0 (2008-2012).

“Then the Gods of the Market tumbled, and their smooth-tongued wizards withdrew,

And the hearts of the meanest were humbled and began to believe it was true

That All is not Gold that Glitters, and Two and Two make Four—

And the Gods of the Copybook Headings limped up to explain it once more.

As it will be in the future, it was at the birth of Man—

There are only four things certain since Social Progress began:—

That the Dog returns to his Vomit and the Sow returns to her Mire,

And the burnt Fool’s bandaged finger goes wabbling back to the Fire;”

(Otherwise known as the Fed interest rate cycle…)

Wolf,

I am starting to see the main stream financial media (i.e. MSNBC, Bloomberg, MarketWatch, etc.) party line mentioning high home prices in articles about affordability. Previously, affordability was always blamed on high interest rates.

I am also seeing more articles about underwater mortgages, high insurance costs, and high local taxes coming into the discussion.

Very little discussion about home prices actually dropping in some areas. I guess this is still a “taboo” topic per order of the National Realtors Association. LOL

There seems to be a 3-6 month lag between your reporting and the big boys. Interesting that a one person operation can outperform a large business operation. It makes you wonder, “what the hell are all these analysts and consultants doing at these places”?

@BruceP most of the mainstream media is struggling and they don’t want to get any of their advertisers mad, so don’t expect any negative real estate, car company or drug company stories anytime soon…

To become a media “big boy,” you have to sacrifice both currency and accuracy. First, trust your own eyes. Then trust another’s eyes. But never trust a corporation’s eyes.

“It makes you wonder, “what the hell are all these analysts and consultants doing at these places”?

Lying.

The fact this is sold *or delisted* makes me think the actual picture is even worse. I would expect delisting to be faster now as internet advertising dominates, and agents are seeking to avoid the poor optics. Is there any data on that?

As an aside on the games they play, one local house on a corner lot that’s been sitting on the market overpriced for a year as the owner chases the prices down just managed to “change” street. Result: an apparently brand new listing without that pesky history. (It’s still overpriced, so the problem is likely to repeat)

Phoney markets/Valuations pump buy phoney over printed paper since 2008.

I sold my condo in late 2020. Denver market. Bought it in 2013 so it was a decent return, even in real terms, on top of being a place to live. The guy who bought it attempted to sell it this year for 100k more than he bought it for. Sat on the market for several months, he cut the price a bit, then finally delisted. Probably has to sell it for what he paid, frankly.

It’s funny because the person I bought it from went through a similar experience of buying it on the up swing in 08 and having to sell it to me for what she bought it for years later.

Owners in CA have the benefit of lower property taxes ( long term owners) and 3% mortgages. Little incentive to sell unless one has to, and apparently most don’t have to. Even paying cash, prop taxes reset to current rates when they buy. If one doesn’t want to cashin by moving to another state, there is little incentive to sell unless one really wants new digs, in which case a significant financial penalty. The stalemate really hinders the ability for folks the adjust their housing for family size, preference, etc. (such as a retiree who wants to downsize).

Is this a realistic scenario?

Existing home market remains largely in stalemate. Builders continue to take a higher share of total housing transactions, thereby increasing total supply of homes on the market. The market stabilizes several years down the road with lower prices caused by permanently higher inventory from new builds.

New builds could be facilitated by zoning changes and other changes the Trump administration plans to introduce this Fall.

In my opinion, we need incentives to build and buy a NEW home. Incentivizing the sale of existing homes does not permanently increase inventory or create jobs.

Seems likely to me.

Home builders get to keep building so long as existing-home sellers keep doing drugs with regards to prices.

Home builders are willing and able to drop effective price and so can make up margin reductions with increased volume until existing homes are priced low enough to sell again.

It’s already happening in a lot of areas. And because existing-home sellers are doing drugs with regards to prices, refusing to believe their precious overpriced homes could possibly fall in price, home builders get to eat their lunch until existing home sellers sober up.

The way the market is going is already incentivizing more building even as effective prices fall, because builders are throughout businesses and right now they as a sector can massively increase building without undue pressure on prices that drive margins negative, because existing home sellers are eating the volume cost and existing home sales are usually 2-4x new home builds.

When existing sellers do finally sober up then you’ll have a crash in home building. But until then – builders have zero competition as a sector because their prices are lower even if just a bit.

The problem with new builds is that they are often not ideally located. Outer suburbs in many cases. I would never buy; middle of nowhere, no nearby shops, have to drive everywhere, endless rows of copycat homes. They are ideal for first time buyers, and any additional housing lowers overall demand. So they help, but the the inner suburbs will remain at a premium. Also, the build quality sucks. I can’s imagine what shape these homes will be in, in another 20-30 years… I’ll stick with my brick home, with copper pipes and solid wooden beams…

The other problem, at least in CA, is most new homes have near 2% tax rate plus HOAs because of Mello Roos and the fact that local govts haven’t built out any infrastructure.

Nice way to hurt younger buyers while ensuring boomers get their 1% tax rates…

Reporting from the north central valley California it has become an established pattern to list a house high, reduce the price 10k two weeks later, sometimes one more reduction, then delist shortly after.

The house reappears a month later as a new listing. It’s pretty funny, and stupid.

I’ve seen exactly one house that was well-priced and it went pending fast and sold for 30k over asking.

Any thoughts on the impact of a housing crash in California (given its about 20% of the total in the US)?

Or will the bubble not pop unless there’s a meaningful increase in unemployment, and we’re instead facing a long term malaise in housing transactions until prices fall bit by bit?

Even without big unemployment, prices are going down.

One hot markets like Austin and SFO are down more than 20% from peak and nothing big bad happened because of this.

Home prices going down over time is not a malaise, it is a needed for healthy society.

I agree, poor wording! Purely I meant a gradual decline, which isn’t really good for anyone. Sellers can’t sell, buyers can’t buy except at inflated prices.

It would be nice if house prices could fall as fast as they rose but I supposed we can’t choose the laws of economics (or sociology?).

I think people should begin to understand the nature of assets. They gyrate in terms of what flavor is in favor at any given moment. If everyone says to buy one thing, then sell it, and buy what they hatz. So, now the herd is beginning to understand that it trampled the market flat. And now if you need to sell, you need to find a willing buyer. Which is getting hard, so prices go down as the few buyers compare multiple properties with no bidding warz. LoL. This time it’s different, the biggest lie of humanity.

It’s not that the herd is wrong, but they trample everything in their path. Like selling gold right now, everyone is doing it, in spite of higher prices, because the herd is arriving.

Now when they throng the LCS stores to burn their money out of their pockets, then sell everything, and buy what they hate.

I suggest stamp collections, they are going into the trash, along with fancy dinner plates. Just not beanie babies, or Labubus….

List your California property at what it was going for at this time in 2020. Any value above that, more than the 4% historical appreciation rate, was a market abnormality caused by the COVID-related stimulus. Lower the price, sell your house. You simply can’t get top dollar for a used air conditioner in January.

Wolf,

So do we have enough information to make a diagnosis yet?

Will we see another 2008-like housing market crash?

By many metrics, it appears Housing Bubble 2.0 is bigger than 1.0.

In my experience, history does not repeat itself. It always dishes up some new surprises.

“History doesn’t repeat itself.

But it rhymes.”

If you look at the buying numbers (at least pre 2021-2022 peak insanity), the number of home sales transactions was maybe 60% of 2002-2006 ZIRP 1.0 insanity.

So at least we have that going for us.

(And even the 2021-22 “Mass Death is Good for SFH RE Boom” was fairly thin transaction volume wise and, heh, short lived.).

But the very thin-ness of transaction volumes (while ultimately a good thing), points up the intrinsic delusions of “wealth effects” (see also, market caps.).

Just because a thin slice of buyers are willing to foolishly overpay *does not mean* those over-valuations are widely shared (and therefore long-term sustainable).

Every seller has to find a buyer – and as over-valuations become more absurd, more and more potential buyers snort and drop out.

Yet…the absurd over-valuations are *reported* as though 100% of asset owners could immediately liquidate and realize the full value of the over-valuations.

Not true, unless 100% of buyers suddenly become lobotimized.

Or juiced with Crank and ZIRP.

Ok, so the real estate market in the world’s 5th largest economy has seized up. This is due to ONE reason – prices in the statosphere.

Most people buying now are setting themselves up for disaster/loss, which will worsen the enormity of the bust.

On top of a real estate crisis, there is a cost-of-living crisis. The cards do not look good. It’s time to fold and walk away. I believe that very few can see the enormity of this disaster waiting to happen.

Time to fold was two years ago. Those still sitting at the table are along for the ride at this point.

@Oh, Shitake the real estate has not “seized up” it has “slowed down”.

“Some” buyers will get in over their head and take a loss, but “most” buyers (even more than the past average) are repeat buyers coming in with big down payments so they are not “in over their head”.

We have always had “some” people struggling with the cost of living and with the recent inflation I’m guessing that it is also “more than the past average”, but “most” people seem to be doing fine (I was shocked to hear what a neighbor paid to fly his family to see the 49ers play in Seattle this past weekend).

I am happy prices are coming down although we have long way to go.

Hope houses become homes for families to have shelter, not a financial instrument to make money.

As a landlord, you are also providing good service.

“This time is different. There won’t be a repeat of 2008-2013. We don’t have all the liar loans and the no-income, no-asset loans.”

This time is surely different! This is the Great Housing Abomination. Prepare accordingly.

Anecdotal…somewhat related: traveled to Ormond Beach (in FL near Daytona and Orlando). Friend has been building a vacation home there on the ocean – taking over three years obtw. Anywho, the beach is really a strand, Atlantic on one side, inland waterway on the other maybe a half mile away. For first time in the trips I have taken down there to assist friend, there are for sale signs all over the place – all for very nice homes.

Hi again. Might you be able to share the stats of the top 10 markets? I saw the link to realtor.com but was not sure where those details would be posted. It was not obvious to me. 😱

You have to download the data from Realtor.com from the page I linked. You need spreadsheet software to do that. And then, once you have the data on your computer, you build the charts for whatever markets you want. You also need something like a laptop to do that. You cannot do it on a smartphone.