Turns out, free money is a toxin. And now the housing market has cancer.

By Wolf Richter for WOLF STREET.

The WSJ had two anecdotal stories back-to-back about the fallout from the housing bubble and from the artificially repressed mortgage rates.

A story today about a chap in Atlanta who’d bought at the peak in mid-2022. A year ago, he put his home on the market at a price well above his purchase price, perhaps on the notion that prices always go up. Two price cuts later to below his purchase price, he still hasn’t had a single offer, even as expenses are racking up. He is learning the hard way: He who panics first, panics best.

And a story over the weekend about a divorced couple with young children whose big problem is the below-3% mortgage that they refinanced into, and that now forces them to live together, as a divorced couple, because… well, they could sell because they have massive but shrinking gains in their house that they bought in 2017, but they then cannot buy two houses, after price exploded due to the low mortgage rates, and they don’t want to rent.

Similar stories and lamentations have cropped up in other publications and in the social media. And they have replaced the breathless hype about bidding wars that were in part responsible for FOMO — this fear of missing out that leads to hasty decisions.

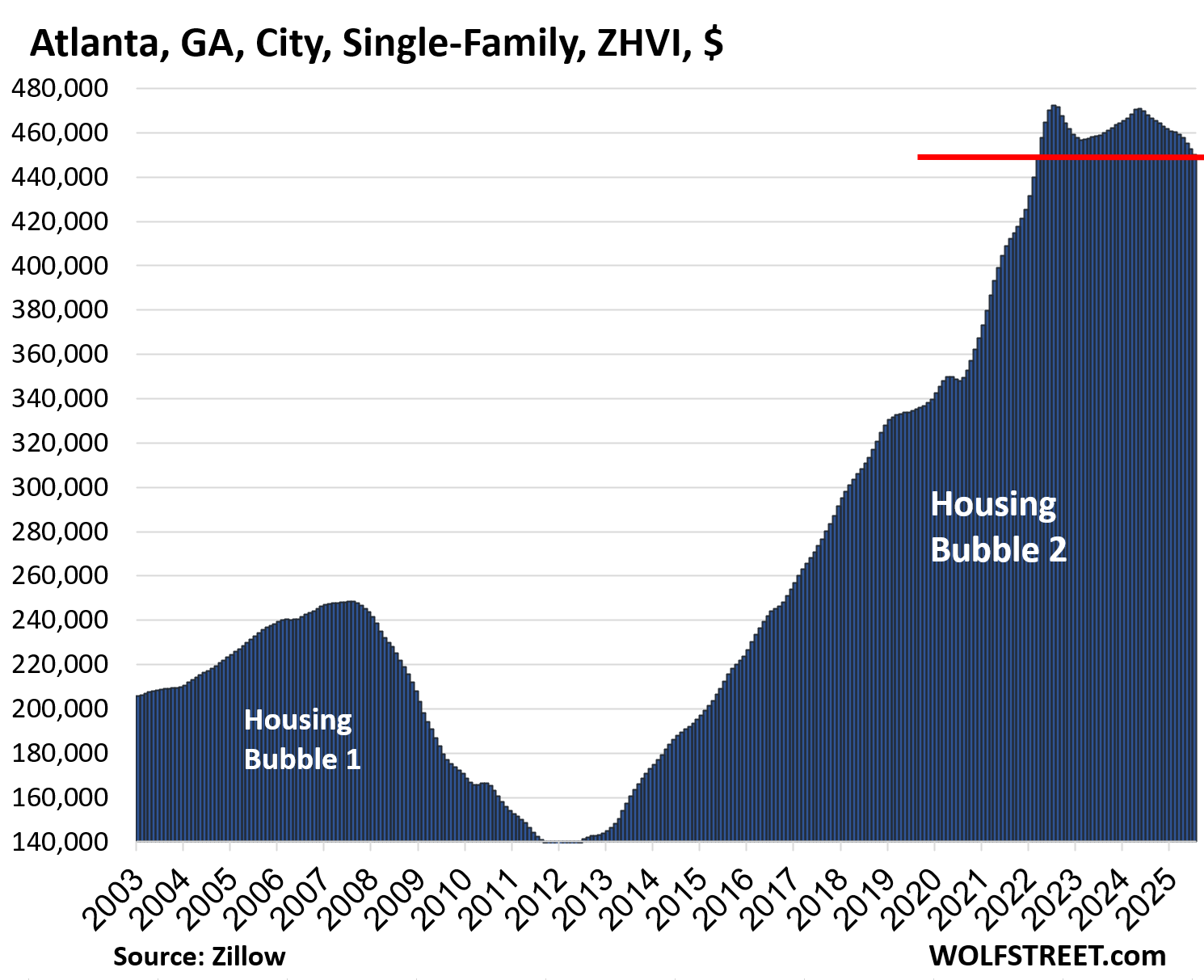

The hapless chap in Atlanta had bought the 1,600 square-foot house in mid-2022 for $399,000, the WSJ said. He signed the contract within two days of looking at the house and waived the inspections, which came to haunt him with a sewage pipe repair.

Prices in the city of Atlanta peaked in mid-2022, after having spiked by 38% in two years and by 52% in four years, and it didn’t occur to the real estate professionals who extracted lots of money from this deal, to warn the chap that such a historic price explosion, caused by the Fed’s reckless monetary policies, might end in tears. Instead, they did what they could to fuel his FOMO, including feeding the media an endless series of hype that the media turned into clickbait about bidding wars and what not, and this chap fell for it.

And his costs are racking up. There is the monthly nut of $2,950, which includes mortgage payment, homeowner’s insurance, utilities, and lawn care, compared to $1,200 when he was renting. In addition, there was a $13,000 bill to fix that sewage pipe that hadn’t been connected, which a proper inspection might have found.

Prices of single-family homes in Atlanta have since then skidded lower by about 5%, most of it over the past 12 months, according to the Zillow Home Value Index. And price declines have been accelerating in recent months.

The chap then decided to rent again to shed the costs and “headaches” of homeownership and save some money. He put the house on the market at $430,000 a year ago, and then cut the price twice and is now asking $387,500, below his purchase price in mid-2020 of $399,000, and still hasn’t had a single offer.

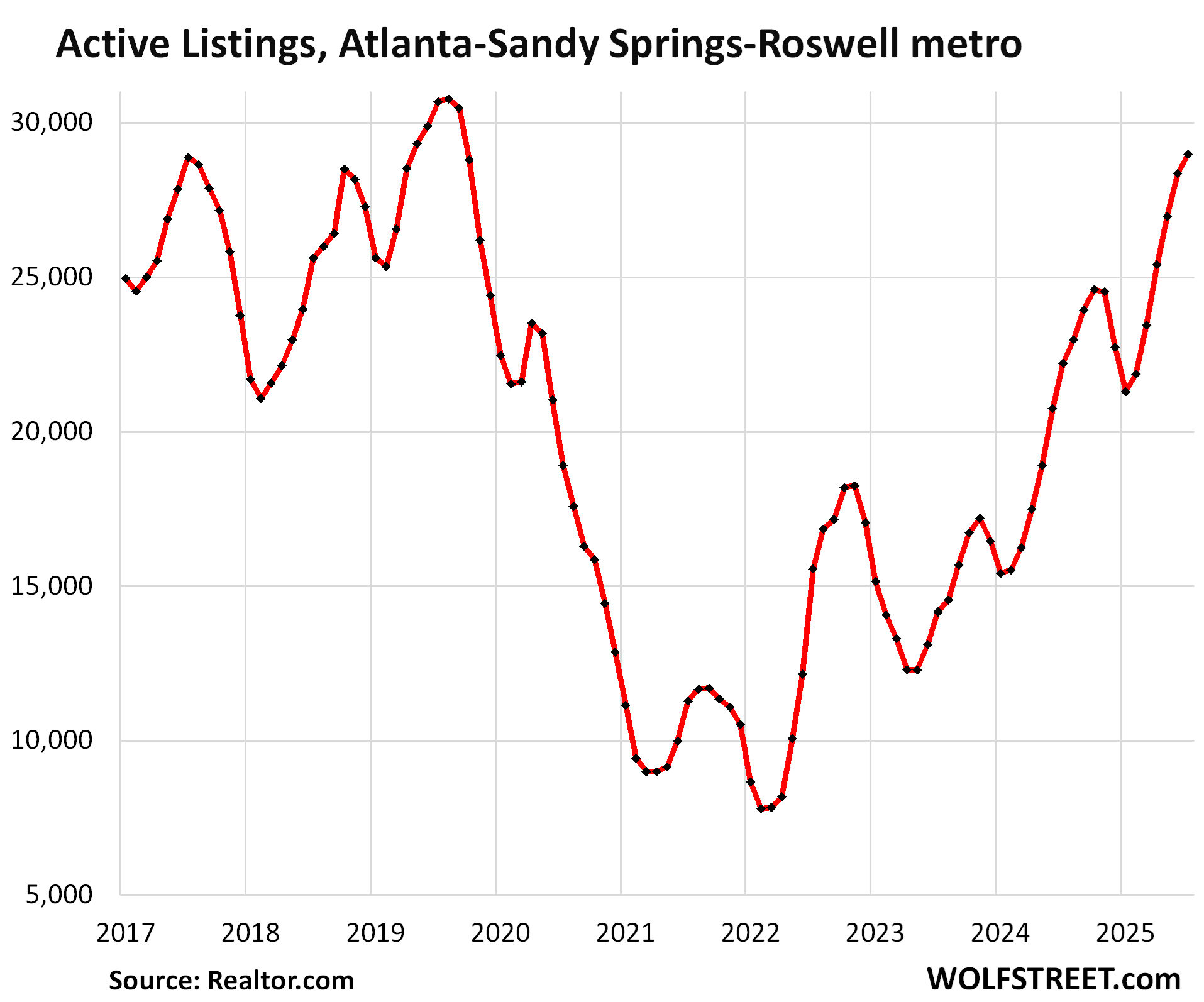

Here is the inventory situation in Atlanta that he is facing:

He who panics first, panics best.

He should have listed it a year ago at $387,500 and would have been able to sell it at the time, and maybe for a little more, but the real estate industry had polluted his mind with the mantra that prices only go up, and he couldn’t grasp that he was being manipulated to enrich others when he bought in a fit of FOMO.

He told the WSJ that he might need to drop the price again. That’s a good bet, given that he has had no offers. He is making a classic move: chasing the price down. By the time he adjusts his asking price down further, reality will have moved away from him again.

So now, depending on where he is on his mortgage, and how much longer he chooses to dilly-dally around, he may have to come to the closing with some cash.

The Richmond Fed described this issue in its Beige Book for August: “A North Carolina agent said, “it feels like we are living in two markets, those listing at the right price or those listing like it is 2021.”

These prices from yesteryear are a widespread problem and in part responsible for the plunge in sales volume and soaring inventories.

The fallout from the most reckless Fed ever.

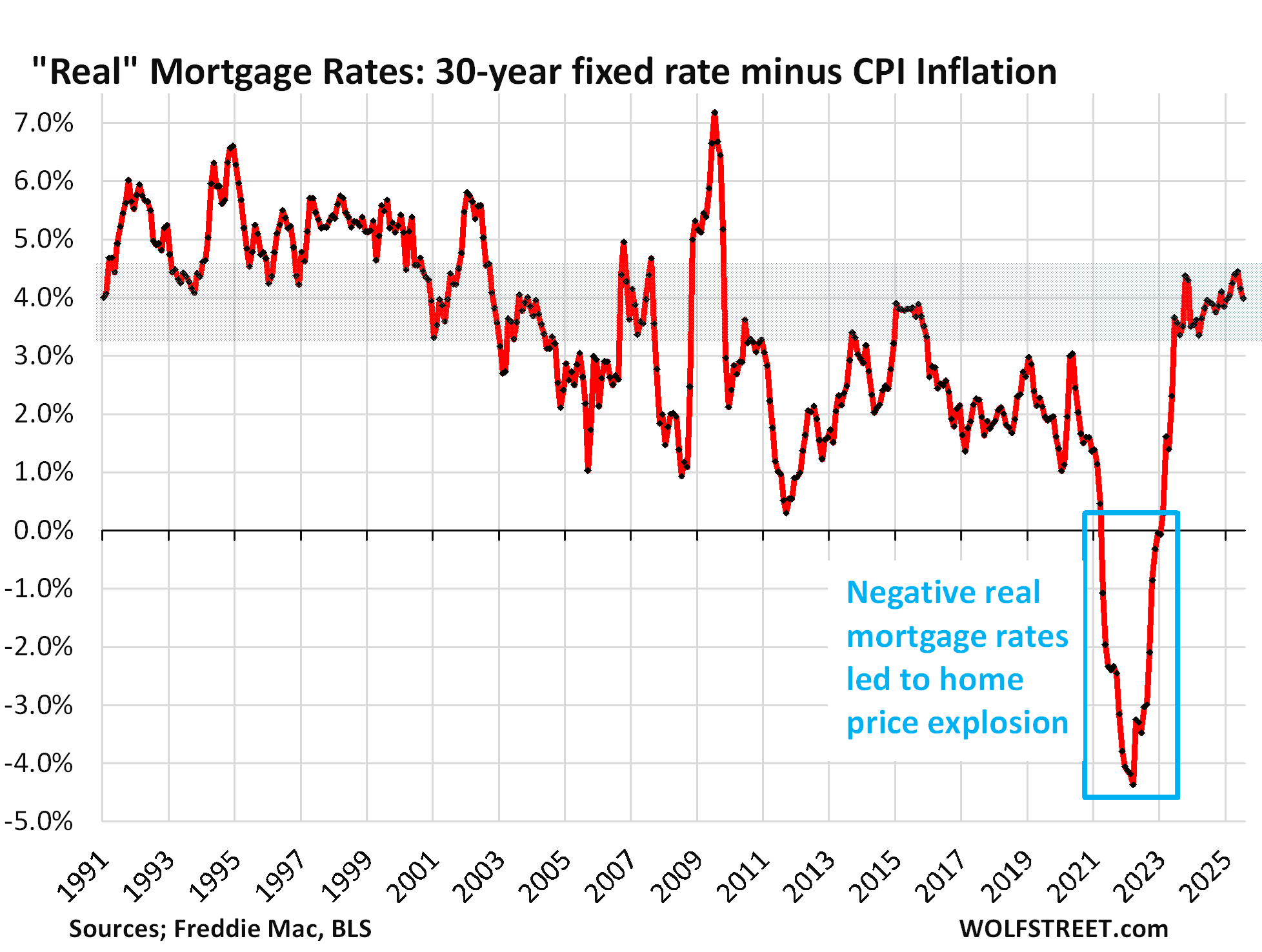

The below-3% mortgages – and even below 5%-mortgages – were a product of the most reckless Fed ever when it repressed interest rates from early 2020 through early 2022, with massive amounts of QE and 0% policy rates.

As a result, in 2021 and into 2022, CPI inflation was spiking and reached levels far higher than the repressed mortgage rates. In other words, “real” mortgage rates (inflation-adjusted mortgage rates) were massively negative. It was, or seemed, better than free money, and when money is free, price doesn’t matter, and home prices exploded.

Turns out, free money is a toxin, and now the housing market has cancer, and the treatment is painful.

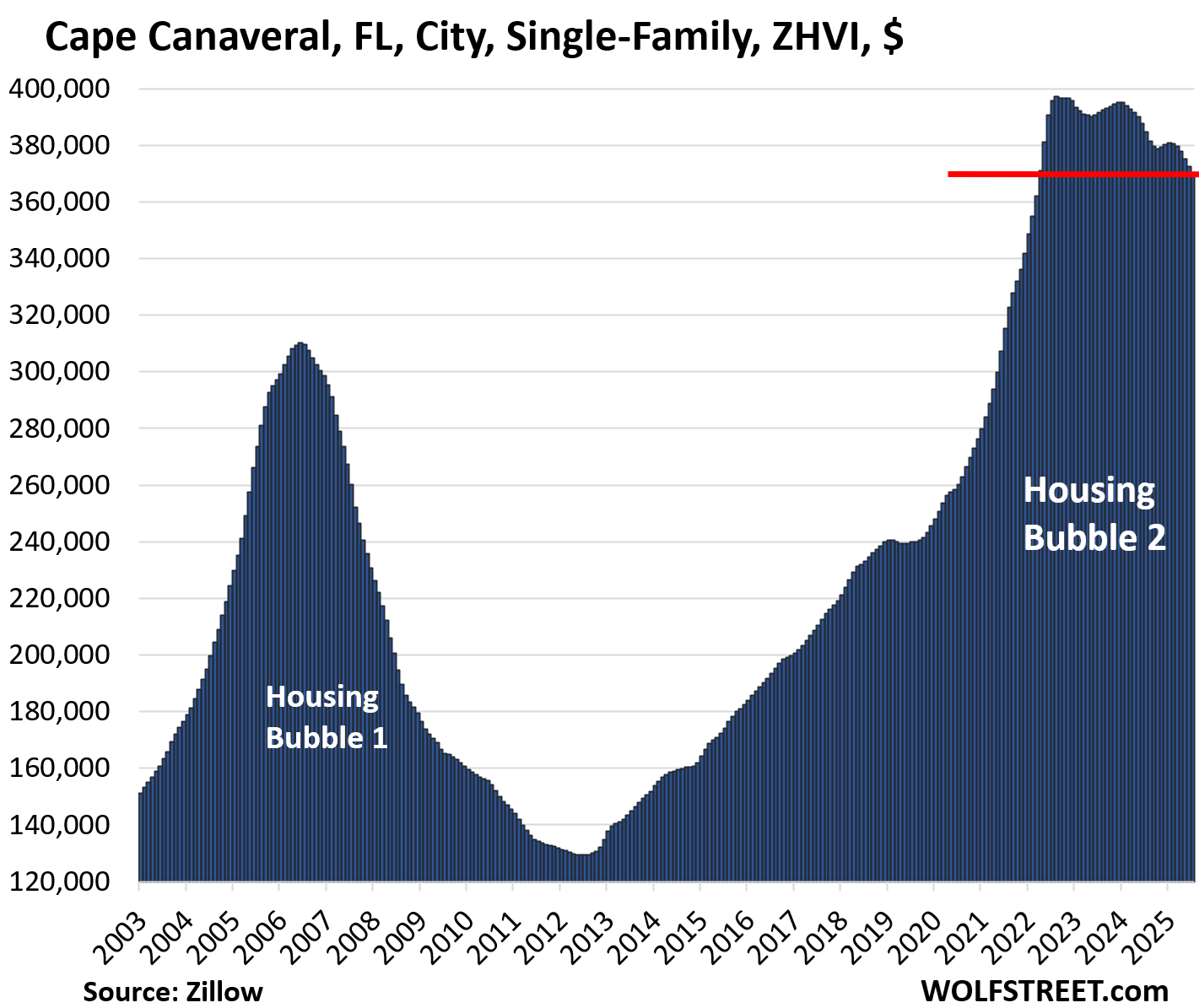

And now there are stories of the fallout from the below-3% mortgages cropping up in the media. In the WSJ’s story, a couple with young children finalized their divorce in April but decided, because they have a below-3% mortgage they refinanced into, that they have to to live together but separate: he in the house and she in their Airstream trailer in the backyard, with an outdoor shower – luckily, in Florida, not in Minnesota.

They’re part of that lock-in phenomenon because of that mortgage and because home prices have spiked so much due to those mortgage rates.

Luckily again, they bought the house in 2017 for about $265,000. Prices of single-family homes in Cape Canaveral peaked in mid-2022 and have since then declined by 7%. But in the two years to the peak, prices exploded by 54%. And despite the price declines since that peak, prices are still up by 77% from 2017, when the couple bought the house.

So unlike the chap in Atlanta, they could obviously price their house aggressively and sell for it for a still very substantial gain after prices had exploded by 77% since 2017. But what they then cannot do is buy two houses because prices had exploded by 77% since 2017, and mortgages are now back in the normal-ish range. And renting is not an option for them.

Meanwhile, as they go through their daily arrangements, home prices in Cape Canaveral continue to skid lower, by another 0.7% in July.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Turns out, free money is a toxin. And now the housing market has cancer

I like this analogy….from the looks of it, certain markets are already in Stage II, and other markets like SoCal probably barely got the news they got stage I and it’s still in denial….judging from the charts you regularly publish, seems like one are in stage IV yet, although Texas/Austin are heading that way pretty quick and some markets I am not so optimistic it ever will, though just like cancer, time will tell.

“But what they then cannot do is buy two houses because prices had exploded by 77% since 2017, and mortgages are now back in the normal-ish range. And renting is not an option for them.”

Why is renting not an option for them? Too much shame going back to renter class and the judgemental stares they might get from friends and families for going throwing money at rents again? If that’s the case have fun living with someone you just divorced, I am sure that’s fun, extra fun if it’s a nasty divorce and someone you can’t stand the sight of but hey you are still a homeowner sitting on a gain for now..

The story is a bit more complicated… she owns a vacant lot next door (all this is is 3 blocks from the beach) that the ex is making payments on for several years as part of their settlement and she wants to eventually build on the lot and in the meantime saves a ton by living in the Airstream rather than renting somewhere.

In any case, their biggest ‘asset’ is their sub 3% mortgage, which at the same time binds them in all sorts of ridiculous ways. This whole situation is insane, just like the insane Fed that adopted the crazy policy that led to those rates (and kept them there for way too long).

I don’t feel bad for the hapless chap in Atlanta, either.

It takes two to tango, and how did he get approved for the loan if he couldn’t afford nearly $3k/month?

And the Fed chairman who dreamed up the carcinogen received the Nobel Prize in for “”for research on banks and financial crises”.

And his 2 successors carried on metastasizing the monetary system.

The Fed is and has always been the cause of monetary evil in our economic system. They mess things up then become heroes when the rescue us from their mess.

ZIRP and QE and the rescuing of banks and then corporations was a joke leading us to where we are today with inflated asset prices.

Debtor corporations got fat by using cheap $$ to buy out competition. Bankers could hide bad loans, the national debt ballooned by the Fed purchasing trillions of debt at negative real rates as they stripped retirees with savings of their wealth.

The Fed needs to be returned back to its original functions, that is making the discount window only available to solvent banks and strict banking regulation. The dual mandate of of inflation and employment is a political farce. They backed derivative trading without regs and repeal of Glass-Stegall, rescued Harley Davidson, bailed out the money center banks and let the bonuses roll. But then receive millions in speaking fees from Wall Street upon retirement.

Have been subject to their messes since 1972 and damn tired of it.

Good summation A.

Paying Interest on Reserve Balances: It’s More Significant than You Think – Scott Fullwiler Date Written: December 1, 2004

See Fed Paying Interest on Reserves: “An Old Idea with a New Urgency”

https://www.wsj.com/articles/BL-REB-1411

April 29, 2008 11:02 am ET

Paul Volcker was quoted in the WSJ in 1983 that the Fed: “as a matter of principle favors payment of interest on all reserve balances” … “on rounds of equity”. [sic]

These guys would have flunked KU’s Money and Banking class.

Saver-holders need high and firm real rates of interest.

An accurate assessment!

As Cavett Robert once said, “Since ninety-five per cent of the people are imitators and only five per cent initiators, people are persuaded more by the actions of others than by any proof we can offer.”

I’d add to that Wolf’s point: “Instead, they (the RE agents) did what they could to fuel his FOMO….”

Now he receives a not-so-warm welcome to the underwater financial world. Nothing quite like the joy of having your home’s market value be less than your mortgage loan balance. A real picnic. But I’m short on pity. His situation could have been avoided with common sense (and reading Wolf Street.)

It is the old joke about lawyers rewritten: “How can you tell when a real estate agent is lying? Their lips are moving.”

Sitting on a massive (non-taxable) gain and don’t want to rent. Boo Hoo Hoo. They sell at a profit, then rent when renting is advantageous. Save up and buy homes when prices drop to reasonable levels. Not a terrible position. Life gives us curves at times and one just has to roll with it. They are doing pretty well compared to those that never got onto the housing bandwagon and have always rented and may always rent. Likely one or both will remarry and end up in a home. What sad looks like – the folks who lost jobs in 08 and had to walk away from their underwater homes with nothing to show for it but debt collectors calling them constantly. Not to proud to rent as it was their only option….

leverage = price to high

I just got off webinar about NEW 102 unit apt complex in Scottsdale

10% occupancy and priced at $35,000,000 or $343k per unit

rent is $2,500 per unit

negative cash flow is $2mil 1st year and another $1.3 2nd year

we repriced it at $20,000,000(this is new in $100k annual avg income market)

soon we’ll have more to come

I work across from one these in Scottsdale. We all watched the construction from the office, all of us were way off on what the asking prices were going to be.

Optima we know is expensive af but this place looks nice but it ain’t $350k for a one bedroom nice.

From my anecdotal experience, people don’t want to buy 1-bedroom apartments. Rent, yes, but not buy, because it doesn’t give flexibility to have a home office, to have a significant other move in, and so on.

I have seen nice buildings where the 2 and 3 BR units get snapped up relatively quickly, while the 1 BRs sit. That can’t be a coincidence.

Are there any credible econometric models that tell us when the bottom will be in, and what pricing ?

No.

I continue to watch Wolf’s excellent chart showing the home price index and Owners Equivalent of Rent. OER was rising with wage inflation and the house price index was flattening the last time Wolf posted this graph. It is was still about 35% more to buy than rent. They were converging slowly.

When the lines intersect, it is the bottom. It means renting is more costly than buying and it makes sense to buy. They intersected in 2012 at the last bottom and diverged after 2014 thanks to FOMO, ZIRP and QE.

When they converge again, investors will start jumping in to make easy money. FOMO for happy complacent renters may take longer to increase. 2012 was strange. It was cheaper to buy than rent but potential homeowners must have been shell-shocked from all of the foreclosures from 2008-2012 and were not buying. Housing Bubble blogs were still predicting further declines. Big investors were buying.

My son is waiting for this great convergence (or within 10%).

It’ll be worse than that, actually.

CRE has already fallen by more than 30 percent.

Other costs are going up much much faster – food, insurance (home and car), trade services (plumbers electricians etc.), and if those keep rising less can be spent on housing.

With rates and those other costs being what they are, housing nationally needs to fall 80% to be affordable. 90% in the worst areas like NYC, Los Angeles, etc. 30% drop won’t cut it. And rents will collapse right alongside SFH because rise in SFH drove rent increases, and as owning continues to fall in price, so will rents. Then add in the less immigration (legal and illegal) and housing will crash and stay low for a lifetime.

Housing can’t even try to recover until the cost of living gets so cheap for young people that they start having large families again. That will take at least 20 years even to begin, and another 20-25 years for those children to grow to become homebuyers. The apocalyptic wording from Wolf is very much justified.

I don’t see birth rates rising either way. All the data in prosperous first world economies shows otherwise. Reasons are more existential than economic.

I’d hazard a guess and say the 1st qtr. of 2027.

I am not entirely sure what could’ve been different for the divorced folks if we were still in 2022 or even 2020 – if they bought their house at the edge of affordability with TWO incomes, there’s probably a fat chance they could’ve been able to “convert” their “one mortgage @ two incomes” situation into “two separate mortgages @ two incomes” situation at virtually ANY point between the time they bought their house till now without resorting to renting or otherwise supplementing their incomes (e.g. by remarrying). In other words, it’s definitely fair to say that they may be screwed now, but I doubt they would’ve been much better off if they had divorced at 2022 or 2020 with the same assumptions…

Turns out, free money is a toxin. And now the housing market has cancer.”

Wolf man – these are the MOST GRAPHIC words you have EVER used to describe the housing market so far. You’re letting the cat out of the bag!

And yes, this is the Great Housing Abomination.

“Turns out, free money is a toxin. And now the housing market has cancer.”

Sheer poetry ….. the best

The Americans I grew up watching in movies and series/sitcoms were very tolerant to change. They would complain about it, make fun, but adapt.

Now, it is showing, that it is hard for some chaps out there to change their status quo, and move on.

Makes me recall a statement I read or listened to somewhere. Many people are afraid of very little, but almost everyone is afraid of appearing “poor”.

Long time back, I liked idea of Independent FED but then I realized they screwed us after 2008. Reality is FED hasn’t delivered on their inflation mandate for last 5 years straight . There is no accountability about it in FED. But I also don’t want President in charge of them then they will be mere puppets.

QE was sin. I could understand after 2008 for sometime. But even after 12 years, they didn’t learn their lesson. On top of Himalayan stimulus in 2020 an even small child could tell FED housing market was skyrocketed, they kept on buying MBS.FOMC must have been smoking weed or something to ignore this but obvious fact.

Unless we have recession and unemployment rise, I don’t see huge correction happening in markets like Bay area. After prices tripled in last 12 years, going down 15% from Peak is not a big deal. We need at least 50% correction to bring back those prices to earthly level.

I personally know who did so much cash refinance in 2021, 2% rate era. Smart people invested wisely or hold on their cash.

Best case scenario for people to not panic and introduce market discipline is to have a slow drip of price degradation. That way the speculation and bad behavior is beat out of the market. But that will not introduce shellshock. The realtors need to take it in the chin for awhile and the propaganda needs to be hung out to dry.

The part that galls me is not only did the Fed make egregious mistakes that were obvious even without the benefit of hindsight, but the establishment continues to applaud Powell/Yellin and apologize for their mistakes. “They had to move quickly and did the best with what they knew at the time” or “They prevented a depression! A little inflation is worth that!”

Don’t let that troll Bernanke off the hook. He is the real criminal. He blatantly lied to congress on multiple occasions. What would happen to you or I if we lied to congress?

Oh he’s a huge POS. But I don’t hear people applauding him quite as much.

The Atlanta chap must feel like he’s pulling out his own teeth to mark down his house an entire 3% from purchase price.

Imagine how he’ll feel when that 3% drop turns into a 53% drop.

Or an 80% drop!

For Americans to be able to afford housing in this current environment housing will have to drop by about that much.

Great read as always! Wolf. I was pushed the same article this morning of that 48hr Atlanta guy, but not falling for click bait or anything pay-walled, I did not know of the juicy sewage details… On Reddit though one commenter suggested more likely that “Gio” is tying to FOMO out of this house, whereas he could just get a roommate…. interesting lives people have for sure…

What is happening with house prices in the US, Canada, Western Europe and China has not yet reached Eastern Europe. Here people are still under the influence of FOMO. The boom continues. It is happening because governments are borrowing and supporting domestic consumption. But cracks are already appearing in the economies.

Countries like Romania, Poland, and Hungary already have deficits that are difficult to manage. Economists warn of a ballooning economy, but central banks and governments are ignoring it.

What is happening in the US will also happen here, but with much worse consequences, because a lot of people are buying at these ridiculously high prices, while in Us, these people were not so many.

I just got a full upgrade of the waste pipe system for my single house (1901) rental in rural Colorado, including a 40 foot new line dug out to the street to connect to city, for about $1,400. So feel very lucky I always had FOBI (fear of buying into) impossibly bloated cost-of-living areas.

… “they refinanced into, that they have to to live together but separate: he in the house and she in their Airstream trailer in the backyard, with an outdoor shower – luckily, in Florida, not in Minnesota.”

Next on channel 6 evening news, cops say they apprehended the suspect after a 9-hour standoff outside his ex-wife’s airstream trailer in Canaveral. Local leaders blamed FED Chairman Powell for the situation.

To think that pipe issue would be found on an inspection is pretty funny. Gave me a good laugh.

The pipe wasn’t connected and it smelled of sewage.

Housing price delusion can be shared by municipal governments as well as homeowners trying to sell. The city government where I live has approved and aggressively defends a zoning change to allow construction of a big foot “luxury” condo development that was approved in 2022, but to date struggles for financing. The city administration sees the development as a much-needed property tax windfall and has used our state’s enabling zoning act to override the NIMBY objections of adjacent homeowners. There are similar laws in most states that make it difficult to sue, and NIMBY often losses. Our city fathers and mothers stubbornly refuse to recognize that this is no longer 2022 as the graphs such as the one in this and other recent Wolf’s articles show.

He who doesn’t FOMO doesn’t buy at the peak. Gambling rarely wins.

Thank you Wolf for the piece of comedy from the WSJ this morning. Next up, an article of sympathy for the bag holders when the AI stock boom pulls back.

“Won’t anyone think of the asset holders!”

What’s happening is the transfer of wealth from the asset holders to income producers. Asset holders are going to get screwed. Income producers (like manufacturers) are going to do very well for themselves.

The crash of the asset bubbles will simply be the final straw for this.

The FED is a Serial bubble blower or arsonist, firefighter depending on when the credit bubble burst…you know greenspan said on record in housing bubble 1 to burn the excess inventory giving us insight to his worped mind like many of our overlords…Boom and Bust, is a banker controlled planet…amongst other unnatural things they do shown in the movie eyes wide shut…

There is a street by my house that I pass through on my walks. About 4 months ago I saw a house for sale. It was the only house on the street for sale. Yesterday I walked down the street, the house was still for sale. Then, I noticed that there were 4 more houses on the street for sale, and another with a rent sign in front. I’m in Ventura County, CA. Interesting.

Awesome! Let the bad debt clear already, and let the bad actors suffer the consequences of their decisions.

Thanks Wolf, another classic to forward to all my “never a better time to buy” realtor friends!

Housing listings are piling up where I am too.

Everywhere you go in my metro area there are listings for houses on signs and stuff but no buyers. So the listings stay, and pile up. For months, and now years.

Huge amount of cheap apartments were built here between 2018 and 2024. Population growth is there but not so much as to justify all the building. You simply can’t build 5000 housing units a year when the population isn’t going up more than 1000 a year.

Just on my tiny street there’s 3 or 4 listings, one for $1.3 million, the others around $700,000. If they sell at half those prices they ought to consider themselves lucky in the extreme. It’s forced selling too since some of the people who lived here were older people who died.

Wolf is correct that the housing market now has cancer. Idiots believe that housing will always go up and that right there is the biggest indication of any bubble.

Housing prices are soon to fall by 80%. Real estate market will not recover for 4 decades even at moderately high inflation rates (2-5% a year). This happened in 1926. Prices spiked 4x where they should have been, and then a huge crash after 1929 that left all those real estate speculators penniless. It will happen today, too.

Fact is, there are two ways to make money off real estate: you can build and sell, or you can rent it out. Capital gains are not a sustainable way to make money, a fact that real estate owners are about to find out all too well. Even if you have the sustained cash flow to hang on, you’ll be dead before you recover the inflation-adjusted value of your investments even if you’re in your 20s now.

The 1920s are calling, and their message is simple: if you own real estate as an investment, get out now or you’ll never get the chance. If you rent out real estate right now and you can’t handle your rents going down by 80%, might be best to sell now. If you have a mortgage and you can’t handle your housing price falling by 80%, sell now and walk away you’ll end up just as penniless as the bankers of the 1920s who believed real estate would go up forever.

And the ultimate lesson? Bubbles always crash – hard. There is no soft landing. There is nothing but absolute, total, and quick devastation for those who participate in bubbles.

Happy note. Look at the situation; gold up housing down. Now, what to do. Old Chinese say,”Time to sell gold and buy home”.

“Free money is a toxin” – W.R.

I grew up around wealthy kids who had cars and cash thrown at them by the Parents.

A large majority trashed the cars and blew the cash carefree.

When We earn and purchase We respect and understand the sacrifice.

60% of those kids from My past are broke drug addicts without a pot to piss in.

Have a fantastic day W.R. and company. 🍻

So that’s what justifys a housing bubble by having someone’s life ruined by the drug rackets which support corrupt government officials of cops, Lawyers, dea know cartel bribes, pensions, rehab centers, Medicaid fraud billings…all because the empire is flooded with dope on Purpose…dark money…

Wolf, Your post reminds me of a speech made by the character Will Robertson in the movie Margin Call,

“Jesus, Seth. Listen, if you really wanna do this with your life you have to believe you’re necessary and you are. People wanna live like this in their cars and big fuckin’ houses they can’t even pay for, then you’re necessary. The only reason that they all get to continue living like kings is cause we got our fingers on the scales in their favor. I take my hand off and then the whole world gets really fuckin’ fair really fuckin’ quickly and nobody actually wants that. They say they do but they don’t. They want what we have to give them but they also wanna, you know, play innocent and pretend they have no idea where it came from. Well, thats more hypocrisy than I’m willing to swallow, so fuck em.”

…A lot of truth in that speech.

Sold my house January 2024 in a suburb of Chicago. Just checked the Zillow value and it is up 25%. I just jokingly told my son I got screwed and we laughed. He reminded me I just wanted out. And it was a young couple with a baby that bought it. I hope they are enjoying it and hope they are doing well.

Buyers in 2022 paid ~2032 prices. They won’t be upside down forever but if they need to sell before then it will be painful. People that bought before 2021 and refied at 3% are in a great position ASSUMING they didn’t pull any cash out. Of course this is America and that shiny new car that you deserve costs $60k…

“luckily, in Florida, not in Minnesota”

Just be able to dodge those thunderbolts of lightning dear.

Job growth revised down by 911,000…

Economy on shakier footing than ‘realized’…