Turns out, free money is a toxin. And now the housing market has cancer.

By Wolf Richter for WOLF STREET.

The WSJ had two anecdotal stories back-to-back about the fallout from the housing bubble and from the artificially repressed mortgage rates.

A story today about a chap in Atlanta who’d bought at the peak in mid-2022. A year ago, he put his home on the market at a price well above his purchase price, perhaps on the notion that prices always go up. Two price cuts later to below his purchase price, he still hasn’t had a single offer, even as expenses are racking up. He is learning the hard way: He who panics first, panics best.

And a story over the weekend about a divorced couple with young children whose big problem is the below-3% mortgage that they refinanced into, and that now forces them to live together, as a divorced couple, because… well, they could sell because they have massive but shrinking gains in their house that they bought in 2017, but they then cannot buy two houses, after price exploded due to the low mortgage rates, and they don’t want to rent.

Similar stories and lamentations have cropped up in other publications and in the social media. And they have replaced the breathless hype about bidding wars that were in part responsible for FOMO — this fear of missing out that leads to hasty decisions.

The hapless chap in Atlanta had bought the 1,600 square-foot house in mid-2022 for $399,000, the WSJ said. He signed the contract within two days of looking at the house and waived the inspections, which came to haunt him with a sewage pipe repair.

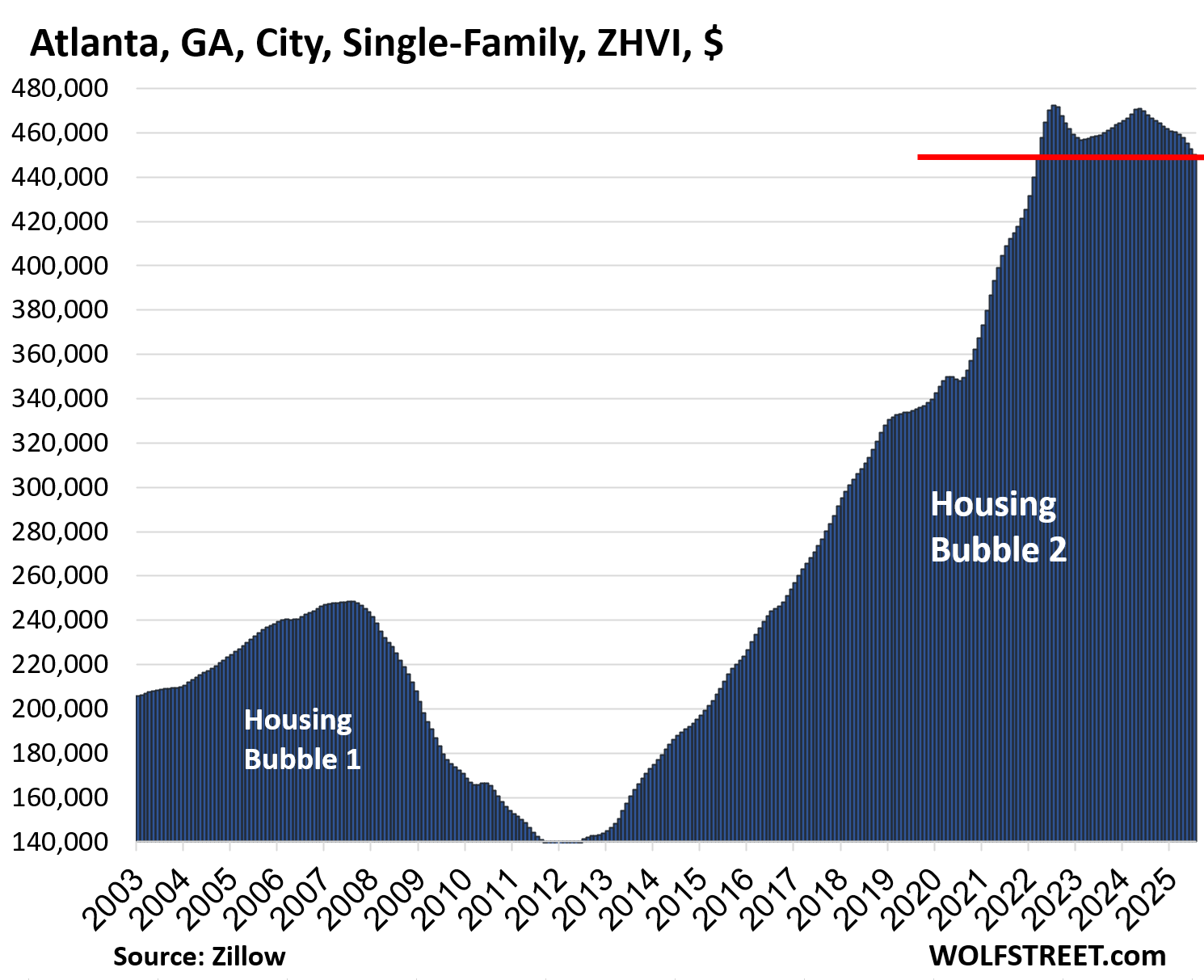

Prices in the city of Atlanta peaked in mid-2022, after having spiked by 38% in two years and by 52% in four years, and it didn’t occur to the real estate professionals who extracted lots of money from this deal, to warn the chap that such a historic price explosion, caused by the Fed’s reckless monetary policies, might end in tears. Instead, they did what they could to fuel his FOMO, including feeding the media an endless series of hype that the media turned into clickbait about bidding wars and what not, and this chap fell for it.

And his costs are racking up. There is the monthly nut of $2,950, which includes mortgage payment, homeowner’s insurance, utilities, and lawn care, compared to $1,200 when he was renting. In addition, there was a $13,000 bill to fix that sewage pipe that hadn’t been connected, which a proper inspection might have found.

Prices of single-family homes in Atlanta have since then skidded lower by about 5%, most of it over the past 12 months, according to the Zillow Home Value Index. And price declines have been accelerating in recent months.

The chap then decided to rent again to shed the costs and “headaches” of homeownership and save some money. He put the house on the market at $430,000 a year ago, and then cut the price twice and is now asking $387,500, below his purchase price in mid-2020 of $399,000, and still hasn’t had a single offer.

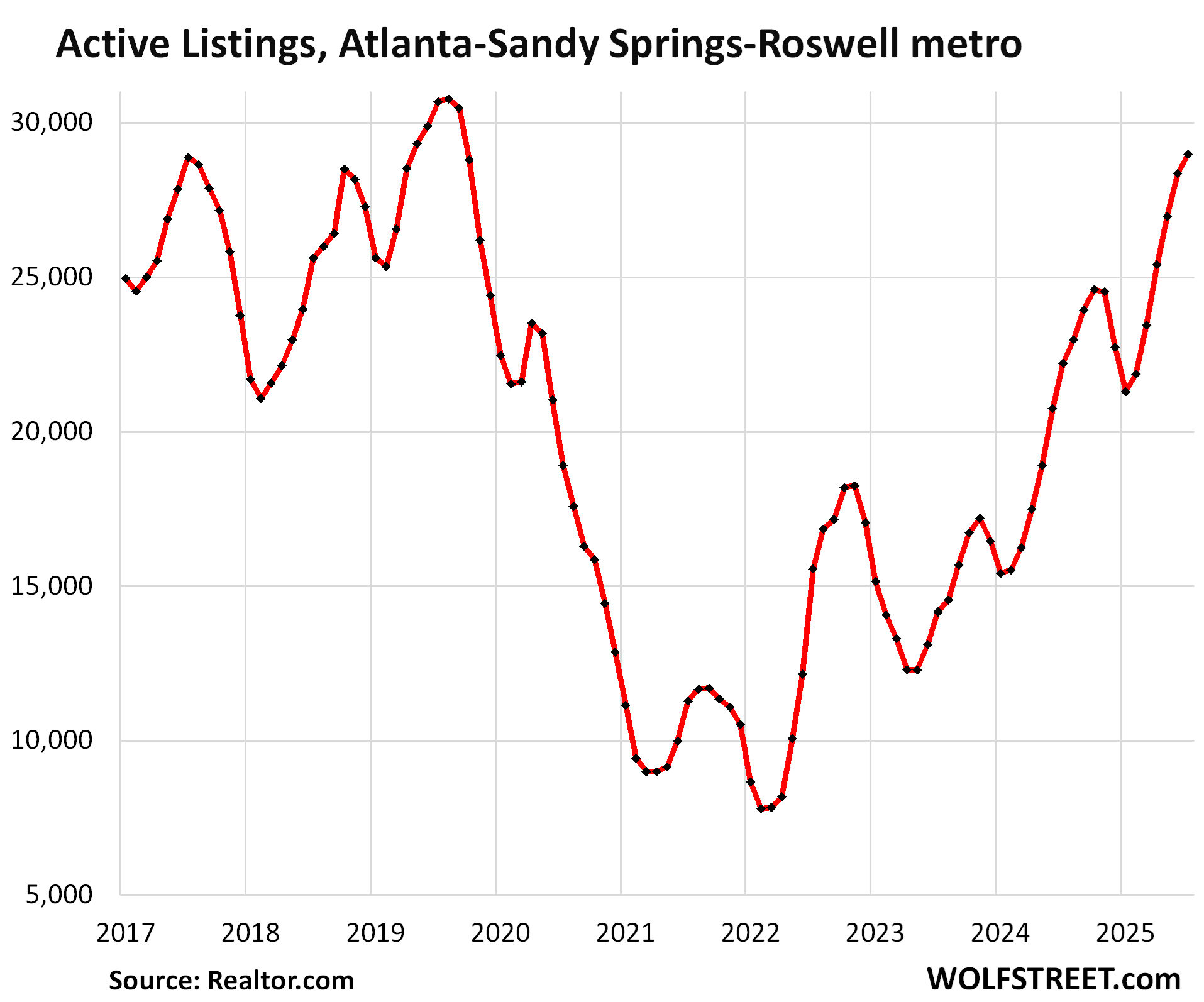

Here is the inventory situation in Atlanta that he is facing:

He who panics first, panics best.

He should have listed it a year ago at $387,500 and would have been able to sell it at the time, and maybe for a little more, but the real estate industry had polluted his mind with the mantra that prices only go up, and he couldn’t grasp that he was being manipulated to enrich others when he bought in a fit of FOMO.

He told the WSJ that he might need to drop the price again. That’s a good bet, given that he has had no offers. He is making a classic move: chasing the price down. By the time he adjusts his asking price down further, reality will have moved away from him again.

So now, depending on where he is on his mortgage, and how much longer he chooses to dilly-dally around, he may have to come to the closing with some cash.

The Richmond Fed described this issue in its Beige Book for August: “A North Carolina agent said, “it feels like we are living in two markets, those listing at the right price or those listing like it is 2021.”

These prices from yesteryear are a widespread problem and in part responsible for the plunge in sales volume and soaring inventories.

The fallout from the most reckless Fed ever.

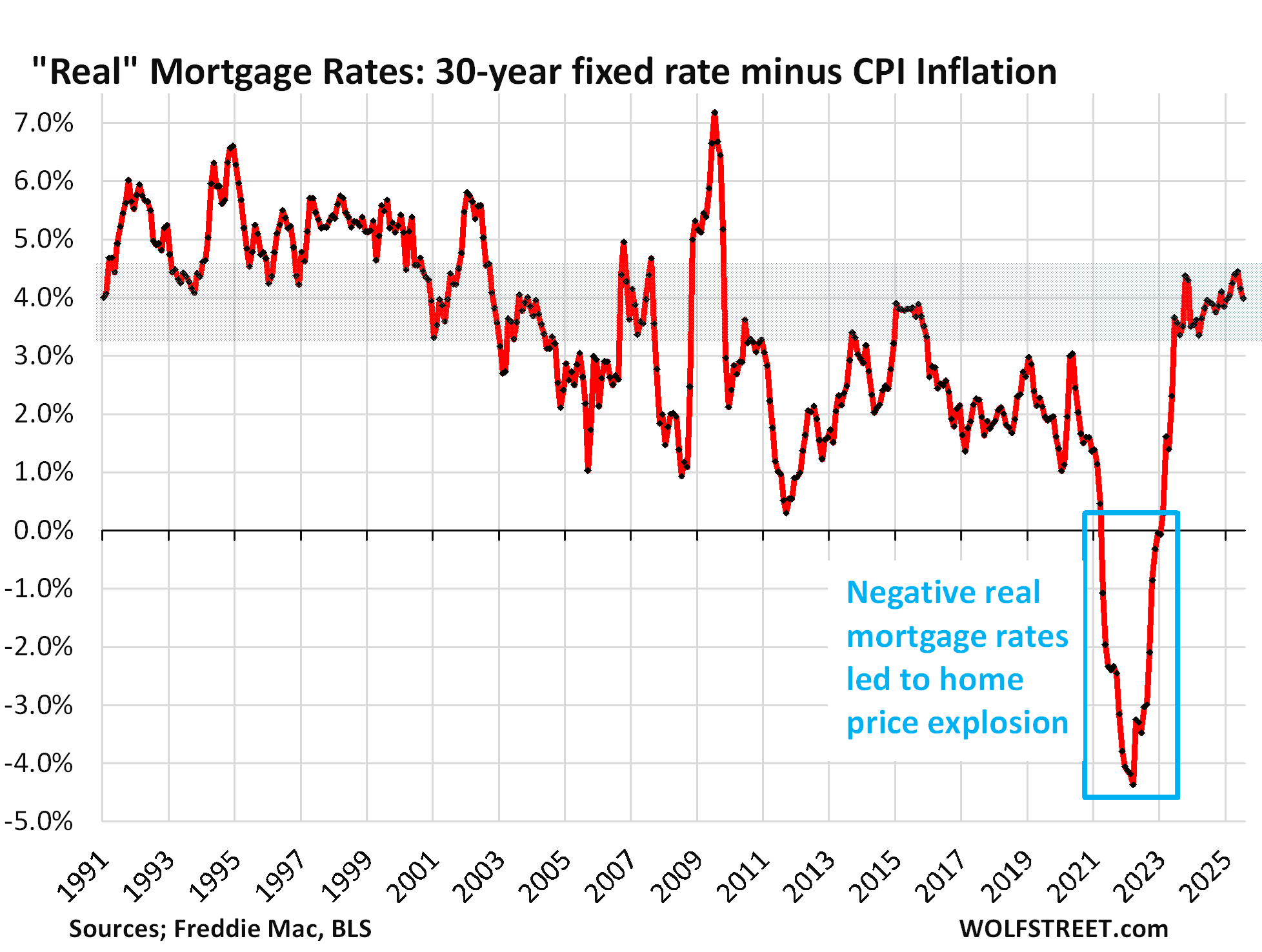

The below-3% mortgages – and even below 5%-mortgages – were a product of the most reckless Fed ever when it repressed interest rates from early 2020 through early 2022, with massive amounts of QE and 0% policy rates.

As a result, in 2021 and into 2022, CPI inflation was spiking and reached levels far higher than the repressed mortgage rates. In other words, “real” mortgage rates (inflation-adjusted mortgage rates) were massively negative. It was, or seemed, better than free money, and when money is free, price doesn’t matter, and home prices exploded.

Turns out, free money is a toxin, and now the housing market has cancer, and the treatment is painful.

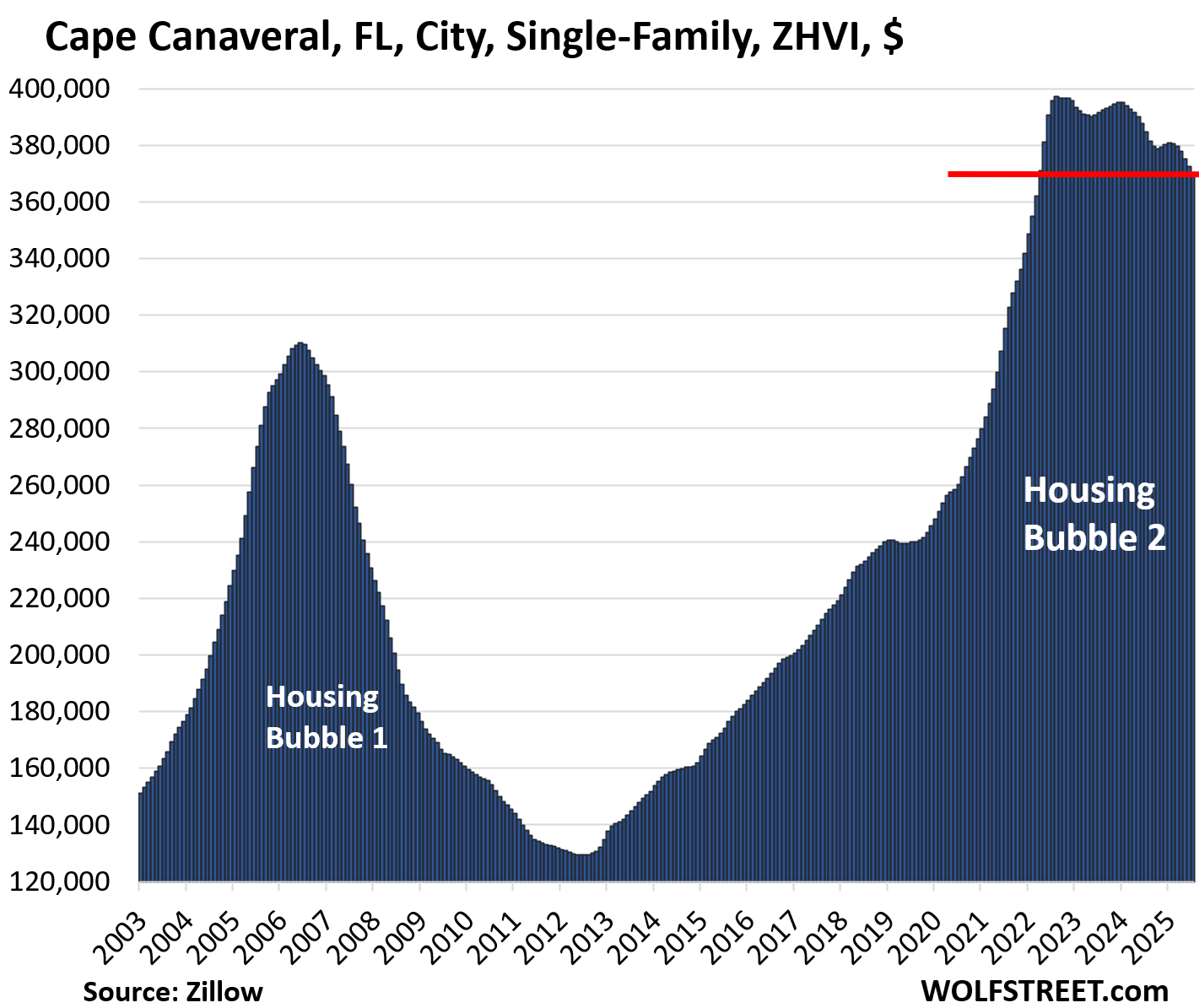

And now there are stories of the fallout from the below-3% mortgages cropping up in the media. In the WSJ’s story, a couple with young children finalized their divorce in April but decided, because they have a below-3% mortgage they refinanced into, that they have to to live together but separate: he in the house and she in their Airstream trailer in the backyard, with an outdoor shower – luckily, in Florida, not in Minnesota.

They’re part of that lock-in phenomenon because of that mortgage and because home prices have spiked so much due to those mortgage rates.

Luckily again, they bought the house in 2017 for about $265,000. Prices of single-family homes in Cape Canaveral peaked in mid-2022 and have since then declined by 7%. But in the two years to the peak, prices exploded by 54%. And despite the price declines since that peak, prices are still up by 77% from 2017, when the couple bought the house.

So unlike the chap in Atlanta, they could obviously price their house aggressively and sell for it for a still very substantial gain after prices had exploded by 77% since 2017. But what they then cannot do is buy two houses because prices had exploded by 77% since 2017, and mortgages are now back in the normal-ish range. And renting is not an option for them.

Meanwhile, as they go through their daily arrangements, home prices in Cape Canaveral continue to skid lower, by another 0.7% in July.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Turns out, free money is a toxin. And now the housing market has cancer

I like this analogy….from the looks of it, certain markets are already in Stage II, and other markets like SoCal probably barely got the news they got stage I and it’s still in denial….judging from the charts you regularly publish, seems like one are in stage IV yet, although Texas/Austin are heading that way pretty quick and some markets I am not so optimistic it ever will, though just like cancer, time will tell.

“But what they then cannot do is buy two houses because prices had exploded by 77% since 2017, and mortgages are now back in the normal-ish range. And renting is not an option for them.”

Why is renting not an option for them? Too much shame going back to renter class and the judgemental stares they might get from friends and families for going throwing money at rents again? If that’s the case have fun living with someone you just divorced, I am sure that’s fun, extra fun if it’s a nasty divorce and someone you can’t stand the sight of but hey you are still a homeowner sitting on a gain for now..

The story is a bit more complicated… she owns a vacant lot next door (all this is is 3 blocks from the beach) that the ex is making payments on for several years as part of their settlement and she wants to eventually build on the lot and in the meantime saves a ton by living in the Airstream rather than renting somewhere.

In any case, their biggest ‘asset’ is their sub 3% mortgage, which at the same time binds them in all sorts of ridiculous ways. This whole situation is insane, just like the insane Fed that adopted the crazy policy that led to those rates (and kept them there for way too long).

The true insanity is that this is the *second* go round of the identical insanity within *very recent* living memory (*not including late 70’s/early 80’s*).

The Fed ran ZIRP 1 from about 2002-2005 and created Housing Bubble 1.0 – which started imploding in 2007/2008 (after a year or two of unZIRP rate normalization).

Home prices collapsed from at least 2009 though 2012 and didn’t crawl out of the blast crater until 2017/2018 (and never fully recovered in some places…from the *first* bubble).

And yet the worthies at the Fed more or less ignored the lessons of 2002, 2006, 2009, and 2012.

This isn’t coherent policy making – it is the desperate improvisations of a country in a death spiral.

so our commercial group(not realtors) did webinar on ‘sale’ of 102 unit(new 2025) in Scottsdale AZ, 10% rented with rents of $3k on 600SF 1 bedroom

asking $35,000,000 (spec)

Lots of new class A in McCormick Ranch

55+ for top $$$ folks

after doing spreadsheet and looking at 3 years to fill after huge concessions

bank bridge loan at 8% with 30% down + 2 years interest reserves($12 mil)

felt price should be $20,000,000 – doubt get it for that(unless they default)

heard of another large apartment in default

bank was willing to take immediate $8 million haircut to move it off their books

Correct.

That is what’s most galling about this.

We just did this 2008.

I assume they will do it again.

I’m watching the long bond as a new rate cutting cycle starts.

I don’t feel bad for the hapless chap in Atlanta, either.

It takes two to tango, and how did he get approved for the loan if he couldn’t afford nearly $3k/month?

he ought to just default

cause he’ll have to come to close with $30-50k or more

hit his/her credit and move

And if he defaults, he’ll probably be able to keep living in the house another year or more before being evicted. At 3k per month that’s $36,000 per year back in the pocket! Lots of people don’t EARN that much.

And the Fed chairman who dreamed up the carcinogen received the Nobel Prize in for “”for research on banks and financial crises”.

And his 2 successors carried on metastasizing the monetary system.

The Fed is and has always been the cause of monetary evil in our economic system. They mess things up then become heroes when the rescue us from their mess.

ZIRP and QE and the rescuing of banks and then corporations was a joke leading us to where we are today with inflated asset prices.

Debtor corporations got fat by using cheap $$ to buy out competition. Bankers could hide bad loans, the national debt ballooned by the Fed purchasing trillions of debt at negative real rates as they stripped retirees with savings of their wealth.

The Fed needs to be returned back to its original functions, that is making the discount window only available to solvent banks and strict banking regulation. The dual mandate of of inflation and employment is a political farce. They backed derivative trading without regs and repeal of Glass-Stegall, rescued Harley Davidson, bailed out the money center banks and let the bonuses roll. But then receive millions in speaking fees from Wall Street upon retirement.

Have been subject to their messes since 1972 and damn tired of it.

Good summation A.

Paying Interest on Reserve Balances: It’s More Significant than You Think – Scott Fullwiler Date Written: December 1, 2004

See Fed Paying Interest on Reserves: “An Old Idea with a New Urgency”

https://www.wsj.com/articles/BL-REB-1411

April 29, 2008 11:02 am ET

Paul Volcker was quoted in the WSJ in 1983 that the Fed: “as a matter of principle favors payment of interest on all reserve balances” … “on rounds of equity”. [sic]

These guys would have flunked KU’s Money and Banking class.

Saver-holders need high and firm real rates of interest.

An accurate assessment!

Ooh, I know: Let’s fix this with MORE Government intervention!

Declare a “housing emergency” invent a brand new hammer to pound the screw.

Make different and unforeseen problems and blame the next guy when it doesn’t work!

I thought the so called “Nobel Prize” that Bernanke won was the imitation one issued by Sveriges Riksbank. It was created in 1968 to reward Oligarch toadies for their contribution of scientific sounding pieces of propaganda to the news media.

As Cavett Robert once said, “Since ninety-five per cent of the people are imitators and only five per cent initiators, people are persuaded more by the actions of others than by any proof we can offer.”

I’d add to that Wolf’s point: “Instead, they (the RE agents) did what they could to fuel his FOMO….”

Now he receives a not-so-warm welcome to the underwater financial world. Nothing quite like the joy of having your home’s market value be less than your mortgage loan balance. A real picnic. But I’m short on pity. His situation could have been avoided with common sense (and reading Wolf Street.)

It is the old joke about lawyers rewritten: “How can you tell when a real estate agent is lying? Their lips are moving.”

Sitting on a massive (non-taxable) gain and don’t want to rent. Boo Hoo Hoo. They sell at a profit, then rent when renting is advantageous. Save up and buy homes when prices drop to reasonable levels. Not a terrible position. Life gives us curves at times and one just has to roll with it. They are doing pretty well compared to those that never got onto the housing bandwagon and have always rented and may always rent. Likely one or both will remarry and end up in a home. What sad looks like – the folks who lost jobs in 08 and had to walk away from their underwater homes with nothing to show for it but debt collectors calling them constantly. Not to proud to rent as it was their only option….

leverage = price to high

I just got off webinar about NEW 102 unit apt complex in Scottsdale

10% occupancy and priced at $35,000,000 or $343k per unit

rent is $2,500 per unit

negative cash flow is $2mil 1st year and another $1.3 2nd year

we repriced it at $20,000,000(this is new in $100k annual avg income market)

soon we’ll have more to come

I work across from one these in Scottsdale. We all watched the construction from the office, all of us were way off on what the asking prices were going to be.

Optima we know is expensive af but this place looks nice but it ain’t $350k for a one bedroom nice.

From my anecdotal experience, people don’t want to buy 1-bedroom apartments. Rent, yes, but not buy, because it doesn’t give flexibility to have a home office, to have a significant other move in, and so on.

I have seen nice buildings where the 2 and 3 BR units get snapped up relatively quickly, while the 1 BRs sit. That can’t be a coincidence.

Are there any credible econometric models that tell us when the bottom will be in, and what pricing ?

No.

I continue to watch Wolf’s excellent chart showing the home price index and Owners Equivalent of Rent. OER was rising with wage inflation and the house price index was flattening the last time Wolf posted this graph. It is was still about 35% more to buy than rent. They were converging slowly.

When the lines intersect, it is the bottom. It means renting is more costly than buying and it makes sense to buy. They intersected in 2012 at the last bottom and diverged after 2014 thanks to FOMO, ZIRP and QE.

When they converge again, investors will start jumping in to make easy money. FOMO for happy complacent renters may take longer to increase. 2012 was strange. It was cheaper to buy than rent but potential homeowners must have been shell-shocked from all of the foreclosures from 2008-2012 and were not buying. Housing Bubble blogs were still predicting further declines. Big investors were buying.

My son is waiting for this great convergence (or within 10%).

It’ll be worse than that, actually.

CRE has already fallen by more than 30 percent.

Other costs are going up much much faster – food, insurance (home and car), trade services (plumbers electricians etc.), and if those keep rising less can be spent on housing.

With rates and those other costs being what they are, housing nationally needs to fall 80% to be affordable. 90% in the worst areas like NYC, Los Angeles, etc. 30% drop won’t cut it. And rents will collapse right alongside SFH because rise in SFH drove rent increases, and as owning continues to fall in price, so will rents. Then add in the less immigration (legal and illegal) and housing will crash and stay low for a lifetime.

Housing can’t even try to recover until the cost of living gets so cheap for young people that they start having large families again. That will take at least 20 years even to begin, and another 20-25 years for those children to grow to become homebuyers. The apocalyptic wording from Wolf is very much justified.

I don’t see birth rates rising either way. All the data in prosperous first world economies shows otherwise. Reasons are more existential than economic.

Jack,

I see your point with CRE, however I believe it is a different market. My perspective is based on my experience with a Silicon Valley tech job.

1) From 2018-2020; the tech economy was booming and all of the up and coming tech companies needed office space. Older tech companies wanted newer and bigger office space. This caused a massive CRE building boom. The older buildings had less demand so were abandoned. Also, retail saw a decline due online shopping so retail CRE had less demand and malls were left abandoned.

2) Now, tech is not growing as much and most are working from home so there is less demand for even the new office space.

The supply of both new and old office space has caused a glut due to overbuilding.

The demand for office space has drastically decreased due to work from home.

It is a Perfect Storm.

Everyone needs a home to live in and now to work from whether it is owned or rented. The demand for homes is still high. Wages have been increasing and unemployment is at record lows. However, the ZIRP and QE effects had driven prices to record unaffordable highs. Nobody wants to sell their house unless they get their perceived high price. They have record low payments due to QE and ZIRP and good paying jobs so they don’t have to sell.

A major job loss recession would “fix” this like in 2008. If people lost their income and couldn’t afford to make even the low payments(and insurance/taxes), they will have to sell or foreclose like in 2008. This hasn’t happened and it doesn’t look like it will happen soon. People can still afford their low mortgage payments

If there is another Depression, then people will sell or foreclose. If is terrible enough, they won’t even be able to afford rent. Rents will drop but landlords may have to sell or foreclose if rents don’t cover expenses. Plywood Hoovervilles may start popping up just like in the 1930’s.

I wanted to add one more thing.

The company I work for has downsized office space since 2020 and encouraged WFH 3-4 days per week. They closed the majority of the field offices with the big company logo signs. This has rippled into at least 10 major cities which used to benefit from at least the lunches and late dinners that were driving local restaurants (and the flowers/gifts which were required for working so many hours away from the family).

I also know many local independent contractors/consultants who run their businesses from home now. They used to drive the local office space because they used to think that having a local office with a logo on the door helped promote business and provided a meeting space. Now they use Teams or Zoom and meet at coffee shops if needed. Customers who are also working from home prefer this.

It is a huge shift away from office space which has rippled into big city shops and restaurants.

Office space is now much cheaper here. At least until the current owner defaults because they can’t cover expenses. Supply will reduce to meet demand.

The opposite has happened with homes. The demand for houses with office space along with living space has grown.

I’d hazard a guess and say the 1st qtr. of 2027.

I am not entirely sure what could’ve been different for the divorced folks if we were still in 2022 or even 2020 – if they bought their house at the edge of affordability with TWO incomes, there’s probably a fat chance they could’ve been able to “convert” their “one mortgage @ two incomes” situation into “two separate mortgages @ two incomes” situation at virtually ANY point between the time they bought their house till now without resorting to renting or otherwise supplementing their incomes (e.g. by remarrying). In other words, it’s definitely fair to say that they may be screwed now, but I doubt they would’ve been much better off if they had divorced at 2022 or 2020 with the same assumptions…

Turns out, free money is a toxin. And now the housing market has cancer.”

Wolf man – these are the MOST GRAPHIC words you have EVER used to describe the housing market so far. You’re letting the cat out of the bag!

And yes, this is the Great Housing Abomination.

“Turns out, free money is a toxin. And now the housing market has cancer.”

Sheer poetry ….. the best

The Americans I grew up watching in movies and series/sitcoms were very tolerant to change. They would complain about it, make fun, but adapt.

Now, it is showing, that it is hard for some chaps out there to change their status quo, and move on.

Makes me recall a statement I read or listened to somewhere. Many people are afraid of very little, but almost everyone is afraid of appearing “poor”.

Long time back, I liked idea of Independent FED but then I realized they screwed us after 2008. Reality is FED hasn’t delivered on their inflation mandate for last 5 years straight . There is no accountability about it in FED. But I also don’t want President in charge of them then they will be mere puppets.

QE was sin. I could understand after 2008 for sometime. But even after 12 years, they didn’t learn their lesson. On top of Himalayan stimulus in 2020 an even small child could tell FED housing market was skyrocketed, they kept on buying MBS.FOMC must have been smoking weed or something to ignore this but obvious fact.

Unless we have recession and unemployment rise, I don’t see huge correction happening in markets like Bay area. After prices tripled in last 12 years, going down 15% from Peak is not a big deal. We need at least 50% correction to bring back those prices to earthly level.

I personally know who did so much cash refinance in 2021, 2% rate era. Smart people invested wisely or hold on their cash.

Best case scenario for people to not panic and introduce market discipline is to have a slow drip of price degradation. That way the speculation and bad behavior is beat out of the market. But that will not introduce shellshock. The realtors need to take it in the chin for awhile and the propaganda needs to be hung out to dry.

The part that galls me is not only did the Fed make egregious mistakes that were obvious even without the benefit of hindsight, but the establishment continues to applaud Powell/Yellin and apologize for their mistakes. “They had to move quickly and did the best with what they knew at the time” or “They prevented a depression! A little inflation is worth that!”

Don’t let that troll Bernanke off the hook. He is the real criminal. He blatantly lied to congress on multiple occasions. What would happen to you or I if we lied to congress?

Oh he’s a huge POS. But I don’t hear people applauding him quite as much.

Powell dug a hole for himself. As I said: “The 4th qtr. 2019 is not the problem. The 1st qtr. 2020 will be negative.” Nov 26, 2019.

Bernanke in his book The Courage to Act “Monetary policy is a blunt tool” and “Unfortunately, beyond a quarter or two, the course of the economy is extremely hard to forecast”.

Totally agree. The revisionist history for how the media now treats Janet “Inflation is Only Transitory” Yellen is sickening.

The FED can never claim victory until their balance sheet goes to zero. And with their current balance sheet they’re not even at halftime.

The Fed’s balance sheet was NEVER zero. NO balance sheet can EVER be zero. From day one, the Fed had a balance sheet of a substantial size. The Fed’s balance sheet always grew roughly in line with nominal GDP (largely driven by its then biggest liability, currency in circulation). Starting in 2008, the Fed’s balance sheet grew because of QE and because the federal government switched its bank account from big commercial banks (primarily JP Morgan) to the New York Fed.

Read this, it will give you a better understanding:

https://wolfstreet.com/2024/03/23/the-feds-liabilities-how-far-can-qt-go-whats-the-lowest-possible-level-of-the-balance-sheet-without-blowing-stuff-up/

I watched a long video about the history of the FED. If it is correct, the FED has a long history of not being independent going back to the 1930’s.

Like Argentina a few years back, they use silly statistics such as Home Rents to determine the inflation rate. Their inflation rate only makes sense if you rent out your house, don’t eat, don’t drive, and don’t have children. So, it’s useless.

The Atlanta chap must feel like he’s pulling out his own teeth to mark down his house an entire 3% from purchase price.

Imagine how he’ll feel when that 3% drop turns into a 53% drop.

Or an 80% drop!

For Americans to be able to afford housing in this current environment housing will have to drop by about that much.

Well, if that happens you are in the Great Depression #2 ( and, nobody will still be able to afford a home ) !

Not really.

The Great Depression happened because US created a general investment surplus in the 1920s. It wasn’t merely the stock market – it was manufacturing, electric utilities, and yes, real estate that all booked far in excess of American demand. US proportion of GDP that was net exports in 1929 was at least as high as China in 2007. Until demand could recover to use up the investment surplus, economy went into the toilet, not helped along by a trade war (net exporters lose most in any trade war) and gov’t policy that prevented increases in wages.

This is not possible in US economy today as indicated by our trade deficit. If anything we have a demand surplus. The pain of less housing investment will fall onto foreign countries that produce imported supplies for US housing construction, not Americans so much. Any housing investment downturn will be more than taken up by increased manufacturing investment as a result. No demand shortage means no halt to investments in general – just changes what exactly is invested. Less housing, less stocks, more bank loans to open new factories. To make a demand shortage would require ending Social Security and Medicare at the least. Probably also Medicaid.

Yes, some people will be badly hurt. But because there is no demand shortage, housing may be in the toilet as per prices, but increased buyers and redirected investment towards other areas of the economy will more than make up for it. There’s not any government policy preventing wage increases either, though there are many preventing deflation. But as long as there is one there will be a correction mechanism that prevents a problem like the extreme demand shortage that caused the Great Depression.

Great read as always! Wolf. I was pushed the same article this morning of that 48hr Atlanta guy, but not falling for click bait or anything pay-walled, I did not know of the juicy sewage details… On Reddit though one commenter suggested more likely that “Gio” is tying to FOMO out of this house, whereas he could just get a roommate…. interesting lives people have for sure…

What is happening with house prices in the US, Canada, Western Europe and China has not yet reached Eastern Europe. Here people are still under the influence of FOMO. The boom continues. It is happening because governments are borrowing and supporting domestic consumption. But cracks are already appearing in the economies.

Countries like Romania, Poland, and Hungary already have deficits that are difficult to manage. Economists warn of a ballooning economy, but central banks and governments are ignoring it.

What is happening in the US will also happen here, but with much worse consequences, because a lot of people are buying at these ridiculously high prices, while in Us, these people were not so many.

The insanity behind 🇨🇳 RE development (economic) & cultural revolution (political) are two sides of the same coin. It is scary to see the quality, safety & environmental impact. Policies makers are too naive or incompetent to understand what was coming – the only beneficiaries are those who controls the $$ creation & flow, not Chinese elite nor ruling class for sure since 🇨🇳 print out money based on how much 💵 they receive from exporting. Connect the dots who decide … Youngsters understand it so they are the rational generation – no mortgage, no car loans & no marriage (aka kids). Those who were born before 90’s were part of that FOMO bunch. Imagine – per sf price went up every hour 🤯🤨😂 type of craziness when this RE started in late 1990’s lasted about 15 years …

I just got a full upgrade of the waste pipe system for my single house (1901) rental in rural Colorado, including a 40 foot new line dug out to the street to connect to city, for about $1,400. So feel very lucky I always had FOBI (fear of buying into) impossibly bloated cost-of-living areas.

… “they refinanced into, that they have to to live together but separate: he in the house and she in their Airstream trailer in the backyard, with an outdoor shower – luckily, in Florida, not in Minnesota.”

Next on channel 6 evening news, cops say they apprehended the suspect after a 9-hour standoff outside his ex-wife’s airstream trailer in Canaveral. Local leaders blamed FED Chairman Powell for the situation.

To think that pipe issue would be found on an inspection is pretty funny. Gave me a good laugh.

The pipe wasn’t connected and it smelled of sewage.

I’ve bought 3 houses and had each inspected by a licensed professional. The things they missed included:

1) Termites ate out the entire sill plate and band joist under a bedroom, and a PO had placed a cover board over it.

2) A thumb-sized hole in the roof.

3) A tilting foundation support pier.

4) Wood subfloor completely rotted out under a toilet.

5) Wood subfloor completely rotted out under a tub (different house)

6) Roof slope below code, causing leaks.

7) A broken window.

Housing price delusion can be shared by municipal governments as well as homeowners trying to sell. The city government where I live has approved and aggressively defends a zoning change to allow construction of a big foot “luxury” condo development that was approved in 2022, but to date struggles for financing. The city administration sees the development as a much-needed property tax windfall and has used our state’s enabling zoning act to override the NIMBY objections of adjacent homeowners. There are similar laws in most states that make it difficult to sue, and NIMBY often losses. Our city fathers and mothers stubbornly refuse to recognize that this is no longer 2022 as the graphs such as the one in this and other recent Wolf’s articles show.

He who doesn’t FOMO doesn’t buy at the peak. Gambling rarely wins.

It doesn’t just work with panic, though: He who FOMOs first, FOMOs best.

I was fomo-ing at the bottom of the GFC. When other people started fomo-ing I stopped.

…too often, I notice foam gently dropping onto my lap…

may we all find a better day.

Thank you Wolf for the piece of comedy from the WSJ this morning. Next up, an article of sympathy for the bag holders when the AI stock boom pulls back.

“Won’t anyone think of the asset holders!”

What’s happening is the transfer of wealth from the asset holders to income producers. Asset holders are going to get screwed. Income producers (like manufacturers) are going to do very well for themselves.

The crash of the asset bubbles will simply be the final straw for this.

The FED is a Serial bubble blower or arsonist, firefighter depending on when the credit bubble burst…you know greenspan said on record in housing bubble 1 to burn the excess inventory giving us insight to his worped mind like many of our overlords…Boom and Bust, is a banker controlled planet…amongst other unnatural things they do shown in the movie eyes wide shut…

There is a street by my house that I pass through on my walks. About 4 months ago I saw a house for sale. It was the only house on the street for sale. Yesterday I walked down the street, the house was still for sale. Then, I noticed that there were 4 more houses on the street for sale, and another with a rent sign in front. I’m in Ventura County, CA. Interesting.

I’m seeing this as well. It’s like the masses now realize the bubble is over and are making their mad dash to sell, not realizing they’ve missed the rush. I’m in an outlying Nashville, TN area.

Awesome! Let the bad debt clear already, and let the bad actors suffer the consequences of their decisions.

Thanks Wolf, another classic to forward to all my “never a better time to buy” realtor friends!

Housing listings are piling up where I am too.

Everywhere you go in my metro area there are listings for houses on signs and stuff but no buyers. So the listings stay, and pile up. For months, and now years.

Huge amount of cheap apartments were built here between 2018 and 2024. Population growth is there but not so much as to justify all the building. You simply can’t build 5000 housing units a year when the population isn’t going up more than 1000 a year.

Just on my tiny street there’s 3 or 4 listings, one for $1.3 million, the others around $700,000. If they sell at half those prices they ought to consider themselves lucky in the extreme. It’s forced selling too since some of the people who lived here were older people who died.

Wolf is correct that the housing market now has cancer. Idiots believe that housing will always go up and that right there is the biggest indication of any bubble.

Housing prices are soon to fall by 80%. Real estate market will not recover for 4 decades even at moderately high inflation rates (2-5% a year). This happened in 1926. Prices spiked 4x where they should have been, and then a huge crash after 1929 that left all those real estate speculators penniless. It will happen today, too.

Fact is, there are two ways to make money off real estate: you can build and sell, or you can rent it out. Capital gains are not a sustainable way to make money, a fact that real estate owners are about to find out all too well. Even if you have the sustained cash flow to hang on, you’ll be dead before you recover the inflation-adjusted value of your investments even if you’re in your 20s now.

The 1920s are calling, and their message is simple: if you own real estate as an investment, get out now or you’ll never get the chance. If you rent out real estate right now and you can’t handle your rents going down by 80%, might be best to sell now. If you have a mortgage and you can’t handle your housing price falling by 80%, sell now and walk away you’ll end up just as penniless as the bankers of the 1920s who believed real estate would go up forever.

And the ultimate lesson? Bubbles always crash – hard. There is no soft landing. There is nothing but absolute, total, and quick devastation for those who participate in bubbles.

Happy note. Look at the situation; gold up housing down. Now, what to do. Old Chinese say,”Time to sell gold and buy home”.

“Free money is a toxin” – W.R.

I grew up around wealthy kids who had cars and cash thrown at them by the Parents.

A large majority trashed the cars and blew the cash carefree.

When We earn and purchase We respect and understand the sacrifice.

60% of those kids from My past are broke drug addicts without a pot to piss in.

Have a fantastic day W.R. and company. 🍻

So that’s what justifys a housing bubble by having someone’s life ruined by the drug rackets which support corrupt government officials of cops, Lawyers, dea know cartel bribes, pensions, rehab centers, Medicaid fraud billings…all because the empire is flooded with dope on Purpose…dark money…

Lots of wealthy families manage to pass money through mutlplie generations. It’s about teaching character and restraint…

Wolf, Your post reminds me of a speech made by the character Will Robertson in the movie Margin Call,

“Jesus, Seth. Listen, if you really wanna do this with your life you have to believe you’re necessary and you are. People wanna live like this in their cars and big fuckin’ houses they can’t even pay for, then you’re necessary. The only reason that they all get to continue living like kings is cause we got our fingers on the scales in their favor. I take my hand off and then the whole world gets really fuckin’ fair really fuckin’ quickly and nobody actually wants that. They say they do but they don’t. They want what we have to give them but they also wanna, you know, play innocent and pretend they have no idea where it came from. Well, thats more hypocrisy than I’m willing to swallow, so fuck em.”

…A lot of truth in that speech.

Best part of the movie and very applicable.

Yeah, that flick has some gems.

“Maybe you can tell me what you think is going on here. And, please, speak as you might to a young child. Or…a golden retriever. It wasn’t brains that got me here, I can assure you of that!”

Sold my house January 2024 in a suburb of Chicago. Just checked the Zillow value and it is up 25%. I just jokingly told my son I got screwed and we laughed. He reminded me I just wanted out. And it was a young couple with a baby that bought it. I hope they are enjoying it and hope they are doing well.

Buyers in 2022 paid ~2032 prices. They won’t be upside down forever but if they need to sell before then it will be painful. People that bought before 2021 and refied at 3% are in a great position ASSUMING they didn’t pull any cash out. Of course this is America and that shiny new car that you deserve costs $60k…

“luckily, in Florida, not in Minnesota”

Just be able to dodge those thunderbolts of lightning dear.

Job growth revised down by 911,000…

Economy on shakier footing than ‘realized’…

As a longtime RE investor, I do have to say that your garden variety $600 home inspection is not going to catch a sewer line problem. That’s a bummer and waiving the inspection is a stupid move for most people (if you’re a GC or have a GC buddy, waiving it and doing your own is a great move) but the sewer line issue would not have come up in the report.

Walt,I am a carpenter and have friends in other trades,would do my own inspection along with paying for one,feel short money for a extra pair of eyes,would also pay for septic inspection,well output can measure meself.

As for FOMO,all I can say is FAFO.

It’s somewhere between 4000x and 9000x cheaper to live in a tent based on national median home price (vs purchasing a home for cash or 30yr mortgage), and the tent doesn’t have thousands of dollars in annual recurring costs, more like $120 in annual costs, tops, to buy a new tent. I live in Irvine, not in a tent, but the life choices that people make are absolute madness, and mostly based on image.

I just can not wrap my head around WHY the FED created this mess?

Incompetence? Stupidity? Exigency?

If they aren’t old enough to remember the 70s, surely they studied it.

We are just in the beginning stages of a lot of pain for a lot of people, unfortunately and completely unnecessarily.

The real estate market is having its sunk cost fallacy mokent. Those who bought at the peak and many of the people with large equity gains price too high because they have too much emotional attachment. If you’re underwater, the loss could be huge including commission and fees so it’s hard to accept. If you have equity, it’s difficult to let go of the old price. Their emotions cause them to list at a higher price than the market can bear and then take the listing off the market when no one buys. It isn’t a loss until you pull the trigger.

1 couple can’t buy 2 houses after owning a single house for only 8 years? Shocking! That scenario would be true in about every time period in history.

A different person waived inspections, buys a bigger house than he needed as a single man, and pays for lawn work instead of doing it himself. From the article, it sounds like he also bought “stuff” just to fill his empty rooms. And then he tries to sell 3 years later. He was bound to lose money. Selling within 3 years has always been ill-advised, with the expectation of losing money since you’d be paying Realtor fees so soon, and having paid so little principal.

These stories are of people making bad choices. Bad choices that would be bad no matter what time in history they would have been doing it.

Do you think there’s a point where you’ll begin to see a mass exodus out of major metro areas to more rural communities and towns of <100k people?

Living in Houston and comparing with my hometown in BFE, Kansas, you can get a larger house on a lot 5-6x larger for about 75k less. They’re not the cookie cutter homes built in masturba- masterplanned communities… they’re generally “safer” areas and the only thing missing are the entry level jobs that require college degrees. Labor pool is probably employed at a higher rate even though wages are likely lower compared to the big-city types.

I guess my thing is this: if folks fled unlivable states for lower prices… how much longer before folks leave unlivable cities for smaller towns? Sort of a de-suburbanization.

Jobs, all jobs. I doubt it

Remote work is slowly dying so it’s actually likely more people return to the city

Remote work, including on a hybrid basis, is dying an amazingly slow undeath. I just got the last batch of data on it. It just edges down in tiny increments. It’s really astounding how it hangs in there, despite all the big companies coming out with ultimatums.

Times change and many homes for sale are not what is wanted or needed.

I look at my fathers home and thank god, I no longer own it, but know the guy who does.

It is a money pit waiting to happen. Replacement is over 900k in todays dollars and he would be blessed if he could get 300k.

We need housing average people can afford to buy and own.

Much of the current inventory for sale will never fill that need!

That might be a good option for people who like to live out in the sticks. But rural life or small-town life is not for everyone. Lots of people love living in big vibrant cities with lots of stuff going on and with lots of opportunities.

Thankfully we can choose where we want to live.

Big vibrant cities also have medical care options which may not exist in small towns or rural areas. That’s another consideration.

I live in a small town (30k in the valley). It’s the biggest “city” in 100 miles in any direction. The biggest employer is probably the hospital with the “college” and the big Ag industry. Lots of people move in for 2 years and then leave. They just don’t like the small town. They “need” more to do, more restaurants to go to, more nightlife, more something. (I bet a lot is Doctor’s spouses needing more “status”).

I have a saying, either you’ve been here for 2 years or 30 years, there’s not much in between.

BTW not only is housing dramatically cheaper but everything else is too. You don’t drive anywhere (cuz the town isn’t very big) so car expenses go WAY down. There’s not a 1000 over priced restaurants and after a while you’ve been to all the local ones so you stop going out as much. Beer is way cheaper at home. It’s not JUST housing costs are way lower.

There aren’t enough jobs in most of small town America for this to work. Big cities, for all their problems, are excellent places to find work of all kinds, and there are ways in many of them to live a little cheaper, usually by means of a long commute.

Have a local subdivision built in early 2000 that went from selling at 150k in 2019 to 400k at the peak. Lennar came in and is dropping 300 similar cracker boxes right beside it selling at 320k starting last year. Destroyed the value of the older subdivision which is back to selling in the 250-300k range. Haven’t seen any of those that sold ’21-23 come back on market, but I know they have to be sweating up a storm.

One would expect that there are many similar situations around the country as the big builders still have to sale and will do what is necessary.

Destroyed the value? Sounds like the houses built in 2019 are still up 66-100% in six years which is great! A few people who bought at the absolute peak are probably underwater, but they have extremely low mortgage rates.

Lennar figured out they could put up cardboard boxes for cheap and sell them at a premium. I’d be interested to see what the twenty-year lifespan of those houses actually is… and how those older subdivisions with the newer cookie cutter houses fare.

The housing market has cancer, yeah, but what about equity markets and crypto fantasy coins and everything else.

They have created a monster that is used to getting what it wants.

Time for chemo, reality is here and would like a word with all the buyers since 2020. As for cheap money, we are going to get a few shots of “stimulus” that will provide get out opportunities (see 30 year bond rates declining on fed cut anticipation). But if you have to sell, sell quick and be aggressive on your price (uh less than those stale idiot listings). About 15% off the recent highs here in Portland, and Phoenix is doing about the same. I would add that the west side of Portland, Nike/Intel country, is beginning to experience layoffs, and houses are going to go splat in short order.

Panic first, or just hang on through it.

Or, as I told the inheritance unit, housing will be a lot cheaper in 5 to ten years in real terms. In coupons, welp, I think lower over the next 4 years. Business will be dealing with shrinking sales versus the infinite horizons they are used to projecting. Unless you are a precious metals refiner. Then you see nothing but insane demand for your services.

I wonder how the USPS, FedEx, DHL are going to make up for lower revenues as international packages undergo major shrink.

I see lumber is doing a brutal roundtrip…..now up next big agriculture with the fall harvest.

Earlier this year, Lawrence Summers stated that the U.S. could lose two million jobs as a result of T – Rump’s tariffs. 😲

Time will tell.

Yeah, Summers, the mastermind behind Clinton’s disastrous offshoring and globalization drive. The economy hasn’t lost any jobs at all, it has gained jobs, but it has gained fewer jobs than previously estimated.

Never listen to Larry summer’s. Go read Nakedcapotalism’s series of articles on why he’s wrong.

By far, the most pain was (and is) felt by renters trying to purchase a home at a reasonable price. Many of them chose to stay out of the overheated market to maintain financial security. Because of ridiculous and stubbornly applied Federal Reserve policies, they watched their savings dwindle in comparison to down payment requirements. They watched as home prices went from 3-5X salary to 6-10x salary in many locations, while the Federal Reserve continued to buy MBS and repress rates. On the coasts, many of them are now locked out of home ownership, maybe for life, assuming the Federal Reserve is not reformed.

But many don’t want to buy. Why should they? Just a hassle. It’s a fallacy to think that everyone wants to own a house out in the burbs. Not true.

“ And now the housing market has cancer.”

Did Wolf accidentally let that slip, or is he seeing a change for the worse now? Or did his superiors tell him to print that?

No ambiguity in that statement. Many patients die from cancer. Will the hoising market?

Read my articles on the housing market lol

https://wolfstreet.com/category/all/housing/

Epic!

I love it when we get to 4 chan levels!

I do love those autist nutcases!

Look in the mirror. 🤪

Intellect is rare commodity after all 😂

In Orange County, California everyone from realtors to friends who were born in this area that housing price never go down in this area because everyone wants to live here for the gorgeous weather. Comparing the listing Px vs Sale Px, I wonder when 🍊 County (part of LA in Wolf’s data analysis) will catch up the rest of the country. $1.2M condo with around 1,500 SF goes under contract fast. Single family sold over $1k per sf in an either run down condition or 60’s 70’s original work out condition. Maybe time gap in consumer psychology? In 2008 CA fell out 1st 🧐 interesting

So in my inventory data, I separate Orange County from LA. You will see this later today or earlier tomorrow.

In my metro-based “Most Splendid Housing Bubble” series (prices), LA and Orange County are in the same metro.

I have a city-based series on prices, but I might add Orange County into that because otherwise I can never cover it on its own.

Greatly appreciate it 🙏 👍

…and the Fed buying MBS’ hand over fist!

Living in Spring Lake Michigan nestled between Grand Rapids and Muskegon with water everywhere including pristine beaches on Lake Michigan. One would easily not be swayed to think there was anything wrong with the economy or real estate market. Spring Lake has more condo’s (52+% Owned by Corporations) than single family homes. Starting at $400K on up past an Easy Million $$’s. The turn around is affecting them, you see more toys for sale, fewer leased vehicles, and used car lots without enough room for the inventory. But the Real Estate Agents and Local Banks continue to Push Ultra Low Closing Costs loans to the misplaced greed that they will always be able to sell at a premium to value. Many owners are now using the Vacation Rental Business like Airbnb’s, to rent out space to help pay for elevated expenses. Soon will come the time when more Sales Signs dot Spring Lake than Buyers. Maybe just around the corner.

Just wait until the HOA’S outlaw VRBO’s. Over here in SW Michigan there are some nice places for sale at old pricing. Without the “extra Income” it is not so much fun to own lakefront anymore. A few more years of this and it might be time to start buying again. As they say, money talks & BS walks.