The Treasury market counts on the tariffs to slow the supply of new debt and could throw a hissy-fit if they end while the Fed cuts rates into accelerating inflation.

By Wolf Richter for WOLF STREET.

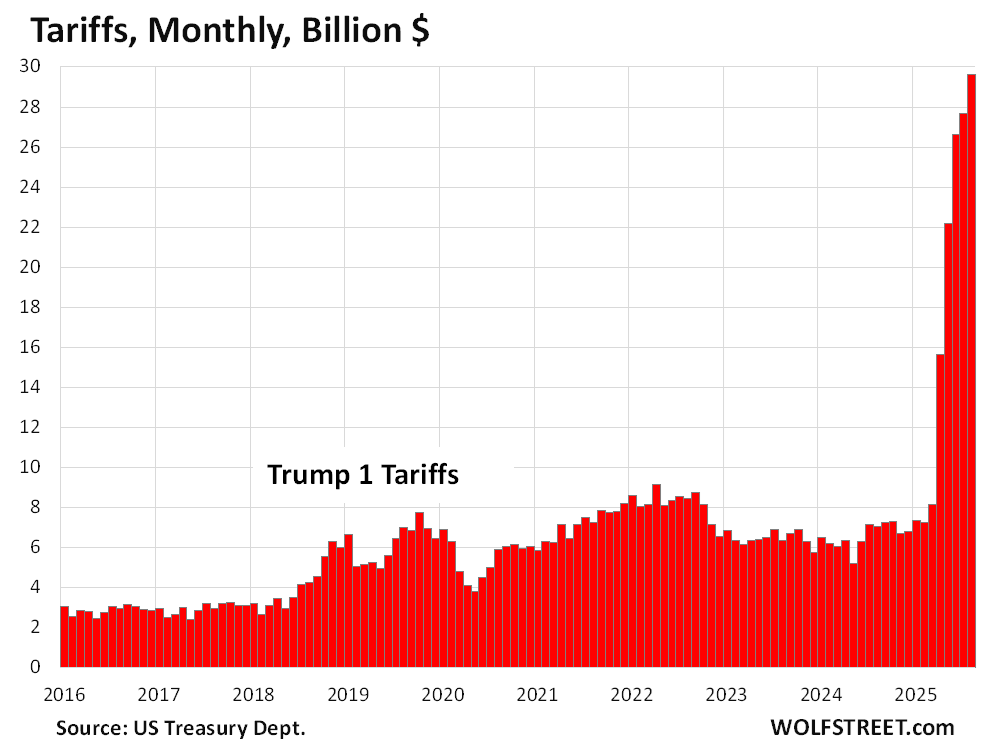

Revenues from tariffs soared to about $30 billion in August. Tariffs have always existed. What’s new is the amount. The new tariffs started taking off in April. Before then, revenues from tariffs amounted to about $7 billion a month. So in August, about $23 billion come from the new tariffs. Revenues from tariffs have increased every month since March.

If revenues from the new tariffs level off at $25 billion a month, they would amount to $300 billion in new revenues a year, and would lower the amount of the would-be annual deficit by $300 billion a year, thereby slowing this Mississippi River of new debt that the market has to absorb.

The Treasury market is counting on this additional revenue to slow the vast supply of new debt that investors have to absorb, amid worries about a lax Fed that is getting ready to cut short-term interest rates despite rising inflationary pressures.

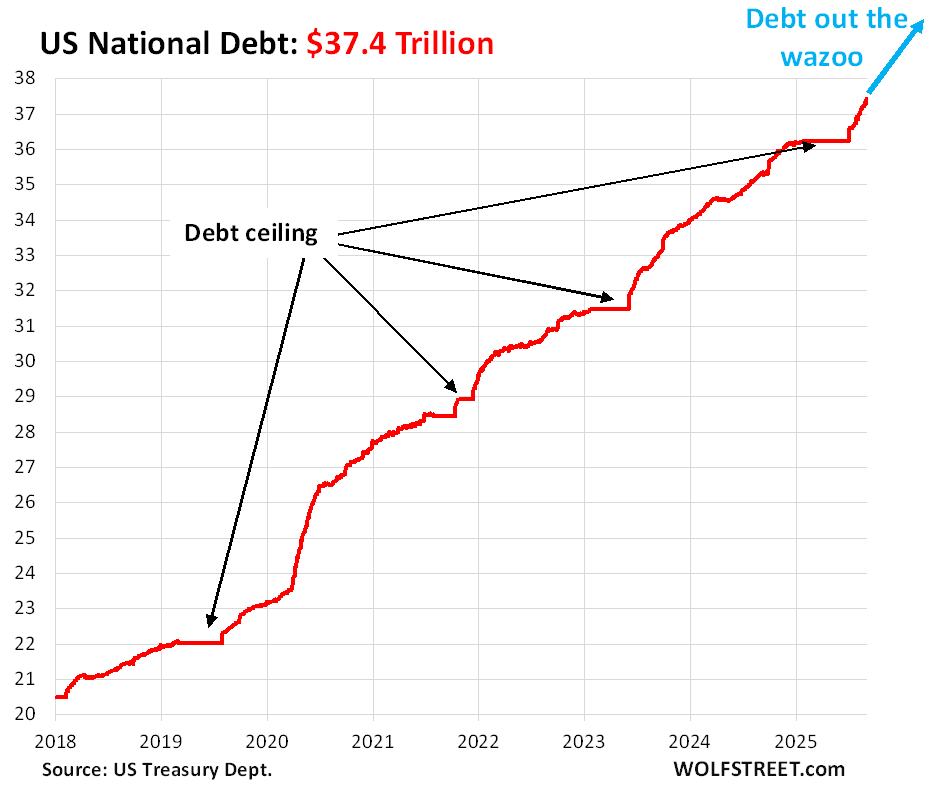

The US gross national debt has soared by $1.2 trillion in the two months since the debt ceiling, and also by that much since the beginning of 2025, to $37.4 trillion currently.

By calendar year, the total Treasury debt increased by:

- $2.2 trillion in 2024,

- $2.6 trillion in 2023.

Obviously, the debt will continue to grow, but the tariffs are slowing that growth and have a chance of slowing the increase of the debt in the calendar year 2025 below the $2 trillion mark – assuming continued economic growth. In a recession, the deficit will blow out because income-tax revenues plunge.

If the new tariffs don’t continue, the Treasury debt would grow by about $300 billion a year more than it would otherwise, year after year, which would further drive up the interest expense on the debt. Over 10 years, this would amount to $3 trillion in additional debt.

This could happen if the Supreme Court sides with the appeals court’s ruling that the imposition of most of the new tariffs was an illegal use of an emergency powers law, and if then the White House’s “Plan B,” as Bessent called it, fails in reestablishing the tariffs.

Investors have to absorb this Mississippi River of new Treasury debt flowing into the bond market. To accomplish this, new funds need to be enticed into the market, and if they’re worried about inflation and about this Mississippi River of new debt, investors would require more attractive yields to be enticed into this market – meaning higher yields.

And those new tariffs are the only thing currently reducing the flow of the Mississippi River of new debt.

Last week, the Treasury market took comfort in the labor market data. Employers added only 22,000 nonfarm jobs in August, June was revised to a net decline of 13,000 jobs, and July was revised up to a net gain of 79,000 jobs.

Without the 28,000 job losses at federal and state governments, the remaining employers added 50,000 jobs in August and 144,000 jobs over the past three months. So it was slow job growth, dragged down further by continued government job losses. And the unemployment rate rose to 4.3%, still historically low, but up from the range of 4.0% to 4.2% over the prior 14 months [more in My Thoughts about that August Jobs Report].

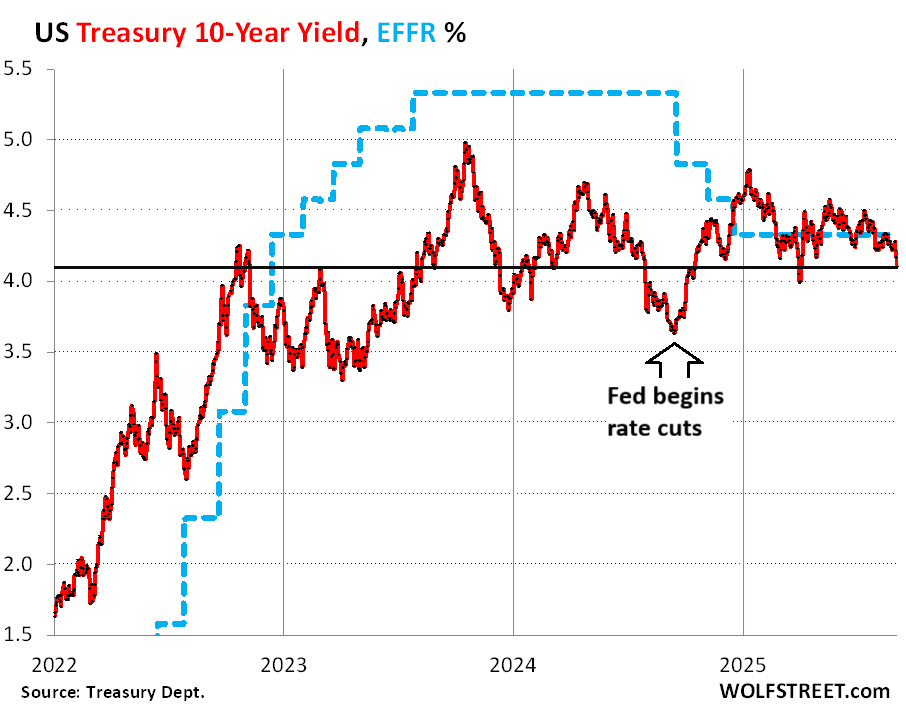

In response, long-term yields fell across the board, with investors expecting slowing economic growth and lower rates. Over the last two days of the week, the 10-year Treasury yield fell by 14 basis points to 4.08%.

The low point in the 10-year Treasury yield in 2024 was September 16, on the eve of the FOMC rate-cut decision, when it dropped to 3.62%.

The rate cut announcement then caused the 10-year yield to rise, and by mid-January 2025, it had risen by 118 basis points to 4.80%, on fears of a lax Fed amid accelerating inflation, which taught the Fed a lesson, and it put further rate cuts on ice, and replaced them with hawkish talk. The 10-year yield then stared declining again. But this will be changing under Trump’s push for lower short-term rates.

This week, two big inflation reports for August will be released: PPI and CPI. The last inflation reports were bad, with core services inflation sharply accelerating in the CPI, the PPI, and the Fed-favored PCE price index (my analysis for each: CPI, PPI, and PCE).

If core services inflation continues to act up in the PPI and CPI this week and later this year, the bond market is faced with rate cuts amid accelerating inflation – the same scenario that played out in September through December 2024, when the Fed cut by 100 basis points and the 10-year Treasury yield rose by 118 basis points.

But this time, a third element could be on the table: the loss of revenues from the tariffs – in addition to a lax Fed and accelerating inflation.

Tariffs are slowing that river of new debt, and the Treasury market is relying on it to continue, and these new revenues have helped keep a lid on long-term yields in recent months.

But if the revenues from the new tariffs don’t continue, and the supply of new debt therefore increases, while the Fed cuts short-term rates amid accelerating inflation, the Treasury market could throw a real hissy-fit.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

If the SC over turns the tariffs..the probability of recession also goes down which means the probability of income-tax getting suppressed is also goes down. Income tax recenues far exceeds tariffs – so scrapping tariffs would appear to be beneficial overall.

..just to add avoiding a recession is perhaps more important for the majority..like keeping the fed rate high and deflating the housing market a bit. …so needless to say they (SC and fed) will likely fuck the majority over.

This SC is completely captive to the ruling party. There is NO chance that they will rule anything else than to declare that an “emergency” is in the opinion of the president alone.

They should be ruling that Congress giving up its Constitutional taxation authority in the first place was unconstitutional, but these are Federalist Society originalists, right?

Actually, gambling sites think there’s only a 45% chance the Supreme Court rules the tariffs are legal.

Damn, I might take that bet.

I know the difference between should and will!

The Constitution places tariff authority squarely on Congress, and this court has been skeptical when Presidents try to lever obscure laws into massive pseudo legislation (see the student loan forgiveness debacle). SCOTUS is definitely not looking for confrontation with the Pres, but I would not be surprised at all if the tariffs are overturned.

Recession?

How many years have we been told a “soft landing” is coming?

Charts straight up to upper right corner in everything

The billionaires and hundred millionaires have rigged the system so that all assets go straight up and to the right irrespective of fiscal and economic realities.

If anyone thinks the tariffs will have no negative effect on US business, or that their pluses always outweigh the negatives, look into the situation facing ALCOA. the Aluminum Company of America.

Tariffs are a tax on business. Been saying that from the beginning. You’re finally catching on after denying it for months. Businesses can dodge them by producing in the US, such as Alcoa.

But business have been getting huge tax cuts, including another one in the OBBB via the investment tax credits and accelerated deprecation for tax purposes. My heart goes out to them.

I submit that the riskiest financial asset of the last 10 years is arguably the long term government debt. Pick your major western country, the US ?

Holders of 30 year bonds lost around 50 pct of their retirement money, invested in the gold standard, US Treasuries.

Great article, thank you. I think that all long term debt is overpriced by at least 25 pct. Interest rate policy is a poison no matter whose ox is gored.

If the Supreme Court doesnt overturn is there any hope of Congress getting their act together to keep the tariffs in place?

Who set the tariff rayes in days of old? Were they set by acts of Congress in the olden days?

In the days of old there was a document called the Constitution that stated Congress shall have Power To lay and collect Taxes, Duties, Imposts and Excises. Now I’m wondering if your comment is sarcasm…

Not sarcasm, but I am a sleep deprived parent. I just wanted to check that back in the 1800s/early 1900s it was actually Congress that set the tariff rates.

Notable tariff set by Congress: “The Smoot-Hawley Tariff Act, passed in 1930, was a protectionist U.S. law that raised tariffs on over 20,000 imported goods to their highest levels in U.S. history. Its goal was to protect American farmers and industries, but it sparked a global trade war, causing retaliatory tariffs from other nations that severely reduced both U.S. imports and exports, contributing significantly to the worsening of the Great Depression.” from Wikipedia

The US was the largest EXPORTER in the world at the time. Now the US is the largest IMPORTER in the world. People who cite Smoot-Hawley either microwaved their brains or are willfully spreading manipulative BS propaganda that only morons would not see as such.

Bravo!! … to Wolf’s comment above.

Very unlikely given the Democrats will not want to give the GOP any wins before midterms, or generically speaking, neither party wants to give wins to either side. The idea has always been laughable our elected officials act for the betterment of your average citizen.

So what do you consider a “win”? Higher tariffs? Or lower tariffs?

I’m of the opinion that regardless of what Congress does, the side in the majority calls it a “win” while the opposing side calls it “the end of civilization as we know it.”

There is no win in our current system. The flaw is seeing a solution on either way it goes and thinking that picking a side matters. We have either Dumb or Dumber running the country and you can choose which label to assign to either party as doesn’t matter. This continues until working class wakes up which super unlikely.

“is there any hope of Congress getting their act together?”

Hahahahahahahhahahahahahhaha good one !

The obsession with the Fed lowering rates is what will kill us. We have now heard that the Fed will lower rates soon for years. The market and economy is perfectly fine with Fed rates around 5% and mortgages around 6 7%. The hangover of no more free money is the new recession I guess.

With respect, what’s killing us is a feckless Congress and imperial presidents for the last 20-years or so.

Except for the growing housing and commercial real estate mess.

Which always leads the economy downward.

There’s that.

The Federal Circuit affirmed a declaratory judgment that the parties to the suit do not need to pay IEEPA tariffs on the imports in question. It vacated the lowet court injunction.

If affirmed in its current form by the Supreme Court, the judgment wouldnt actually do anything right away. Instead, the precedent set would be used as the basis for calculation of future tariffs and as support for refund applications, which would be processed in due course like any other refund application. Note that interest runs at 6% for corporate tariff payers and 7% for others, so there is no benefit to the government dragging its feet (since those rates are higher than short term treasury rates).

Aha! Thanks for this. Illuminating.

Back when Volcker’s CPI was somewhat truthful…..

“The 10-year Treasury yield in 1981 reached a high of about 15.82% in September 1981, driven by high inflation that the Federal Reserve was trying to control. By the beginning of 1981, the yield was already around 12.57%, increasing to its peak later in the year.”

There was never a “Volcker’s CPI.” It exists only in the wild imagination of some people.

I think he meant CPI during Volcker’s term, not that it was his data. Alas, he’s not the only one who questions the accuracy of the BLS. I believe they intentionally manipulate it lower. Hedonic this, mothertrucker.

There was nothing in the CPI during the Volcker era for laptops, home network equipment, smartphones, streaming subscriptions, broadband subscriptions, wireless subscriptions, flat panel TVs; cars with 8 airbags, 10-speed automatic transmissions (standard now on F-150s), antilock brakes crumple zones, side-impact protection, backup cameras, responsive cruise control, automatic windshield wipers and lights, etc.; cars back then were POS death traps compared to what we have now. And those quality improvements are not free and have to be reflected in CPI. These simplistic CPI comments are just bullshit.

I’m curious what the “refund channel” would look like if the Supreme Court does rule to force a return of the newly collected tariffs. As one huge slug all at once out the TGA that’s only just getting refilled? Or could Treasury slow-roll the outgoing in some way? Seems like the path could have implications for the composition of the Mississippi River of new debt, i.e. T-bills vs. -notes and -bonds.

I can imagine very slow walking if that is the case. “my dog ate it”, “that person was let go”, ‘we are out of checks’, etc…If refund channel is needed, expect very slow movement of any money….Meanwhile courts will be involved to help slow it down.

There’s a supreme-er court that could help slow it down?

Well, one thing’s for certain: it’ll be infinitely faster than the refund process for end consumers.

I still think long duration Treasuries are a relatively attractive investment (given the paucity of other good opportunities). Short duration bond yields have declined sharply and low credit spreads make the yield offered by relatively low risk bonds unattractive. The US government will always pay its debt and given its hard to imagine any scenario where inflation exceeds 5% pa over the next 30 years, the real return will be positive.

It’s easy to imagine a scenario where consumer and asset prices exceed 5% pa over the upcoming 30 yrs. Also the after-tax return on Treasuries is the important measure, and is likely to be negative over that horizon if yields remain where they are.

There are some attractive munis out there that are worth taking a look at – particularly in the 7-10 year to maturity range (if you are looking to shield income).

How do you stop a mad, crazy drunkard from spending (on a credit card, of course) like there’s no tomorrow ? Not by the bartender saying he’ll buy two of the drunkard’s drinks per night. That doesn’t stop the insanity.

Do you stop an out of control freight train by putting a few marshmallows on the track? I don’t think so.

The Great Housing Abomination

The Great Everything Bubble

The destruction will be one for the history books!

Unfortunately, the destruction this time will be more inflation, and greater divide between haves and have nots.

Tax the rich, replace fossil fuel with renewables, increase legal immigration – all things that won’t be happening to fix the debt, inflation and growth problems.

“replace fossil fuel with renewables”

Utopian fantasy.

Oh it will happen. It has to happen. The only questions that remain are how soon, and how much damage will we do to the planet before it happens. Seems like a lot of people are fine with the “as long as the planet isn’t destroyed in my lifetime, I’m good with it!”

You people have no clue what the costs actually are and don’t give a shit about rates going up 6-8% because of the renewables.

Have you seen what the Europeans have done? They’re up to 24% renewable, in cloudy Northern climates. And they’re replacing more every day.

Europe pays a lot more for its electricity than we do in USA.

My own rooftop solar system cost me over five figures even with all the gov’t tax credits – this isn’t cheap energy by any means.

But your electricity and gas bills are not cheap either, if PG&E is your provider, because among other reasons, you’re paying for the many billions of dollars in claims related to wild fires that PG&E equipment was ruled to have caused, plus you’re paying for the interest on PG&E’s debt, its dividends to shareholders, its huge executive compensation packages, etc.

ShortTLT I too paid five figures for a rooftop solar PV system. The vast majority of the cost is in the labor to retrofit one single house and the inverter, not the panels. Thus, solar farms are far more economical. The most recent data say PV solar is currently the 2nd cheapest source of electricity next to offshore wind. At the time I installed, I estimated a 6% IRR. That was a pretty good return at the time, and uncorrelated with other assets. As electric prices rise (thanks AI) our returns on our investments might increase by a lot.

https://ourworldindata.org/grapher/levelized-cost-of-energy

Acting as if fossil fuels will last forever is worse.

LOL!

Details matter.

Fossil fuels (hydrocarbons) are not being produced using algae, so technically, they will last forever (hell, if you are fat, then you are a walking bag of reduced hydrocarbons).

The issue is flux. How fast can we replace the hydrocarbons being burnt. But to you real point, if there are no calories/joules/watts available for consumption, you cannot have an economy, period.

Sorry, that should read “NOW” being produced using algae. Lots of companies are getting this right.

It’s a bit silly though, use the sun to fix CO2 back into reduced hydrocarbons to be oxidized back to CO2…

50 years oil, 50 yrs gas, 100 plus years coal, based on no new discoveries. Given AI, which may unpopulate the planet and nuclear energy, close enough to forever for me.

Ask Europe how that energy transition is working out for them !

Make sure you ask them, and not ZH.

I actually was in northern Italy last week and I have never seen so many high dollar cars on the road along with an obsession over renewable energy and climate change. Coming back to the US was like time traveling – and not in a good way!

Transition is well in progress, which comes at a cost. But the (western) european countries have at least had the foresight to understand that the electrificiation is not going to slow down, and that fossil fuels won’t magically replenish. Yes, they are paying more due to the required investments in the grids, but their costs will only be going down while the rest of the world’s go up. Sure it’s expensive, but it’s future proof as well.

Norway: 90+% of all cars sold being EV, domestic energy completely covered by hydro and wind power

Netherlands: 34% of all owned houses equiped with solar panels, 180k public EV charging stations

France: 75% domestic power from nuclear sources

Denmark: 58% domestic power from wind turbines

Now, for a fair comparison we should be looking at EU averages, which come in quite a bit lower than these individual markets, but substantially higher than the U.S. in all sectors except for… biomass.

Replacing fossil fuels would probably have the opposite effect.

Love the idea of increasing legal immigration. This simply has to happen.

Renewables increase the deficit inasmuch as the government pays subsidy for them. Green energy may be good for the planet but it is irrelevant to the Federal deficit.

Taxing the rich always always always means more taxes on the middle class. Just look at the history of the income tax in the US, and the total tax burden on the middle class in Europe. Remember income tax in the US started as a tax of 7% on what was the equivalent of 11 million in today’s dollars.

Look how far away from that we are now! Net taxes on the middle class are more than on billionaires.

In the long run, the government must cut social and defense spending. There is no other way out of the deficit problem.

I’ve been seeing posts about people getting hit with huge fees (e.g. extra $1047 charge on $517 of parts from UAE ) at the point of delivery of packages from overseas. Some say it’s a system glitch with UPS. Any idea why this is happening? Will UPS get to pocket any of that if tariffs get overturned?

Right now, if you try to order anything international on eBay, (bike parts, etc) you will see a huge pop-up banner saying that your purchase will subject to tariffs, and that the shipping carrier will charge you. Last time this happened to me, it was for a purchase that exceeded the $800 de minimis limit, and DHL left a bill on the package as it was delivered. Not sure what would have happened if I didn’t pay it – because I did. But now the question would be – if I did pay it, and the tariffs are reversed, would DHL refund me? How? And would the Federal government refund DHL? Sounds like total chaos.

Wolf: below the second chart, should that be $300 billion / year?

Yes, thanks.

How much M1 is being siphoned out of the “economy” via River of debt ? crowding out all else.?

Buy some gold/silver and forget it.

And yes, the US will always print enough money to pay t-bills holders.

This is one awful mess. VAT tax anyone?

Those commodities are headed for their biggest plunges in history.

well they would need to go down by approx 80% if your prediction comes to pass; I don’t see it but, the NASDAQ could ( it’s done it before in the not too distant past ). And, don’t forget to put your commodity shorts on ! LOL

For the first time since 1996,. gold holdings by central banks exceed US$ assets, RE: treating gold as a commodity. like pork bellies, OJ, copper etc, is ridiculous. It is a Tier One Asset for the Bank of International Settlements.

It is not just money, it is big boy money.

A nothing burger at best! Oh my another 300 billion to print out of trillions of new debt.

Just like all the bs of a small interest rate cut will fix housing. If you cannot afford a 500k house, all cheaper interest does is prolong your agony.

You need to include the value of the dollar in your risk profile! Even a few percent adds up over the years.

There’s no sign of a recession in the near future.

1) The job creation stats are notoriously volatile, and you have to squint to see any increase in initial claims or unemployment on a 10 year scale.

2) Financial liquidity is high, as judged by the NFCI and other metrics.

3) Durable goods spending is only down because it was up, due to tariff front-loading.

4) Wages are growing faster than inflation and real estate prices, particularly in the services sector. The drunks are getting more money to spend.

5) The 2/10 yield curve has been uninverted long enough to call the inversion a false alarm.

6) Residential investment is higher than it was in 2024.

So these are inflationary times, and the Fed is about to be manipulated into cutting rates.

SHORT TLT

Inflation is TRANSITORY!!!! This has to be a one-time-shock from tariffs, so we need to lower rates.

How many times will we hear this story as the rich get richer, and housing becomes more and more unaffordable, and car payment go to 7 years.

The middle class will soon be indebted for the entirety of their lives, with lifetime car loans and lifetime mortgages.

Go long hamster wheels.

Hi!

The TLT just jumped 4.67% in 4 days, first time above the 200 day average since April. I’d buy it on a pullback.

Sorry, that was advice, not attempting to call you. Lol.

Is there a ShortZROZ in the house?

Increasing QT would reduce the supply of new debt if tariffs are discontinued.

In fact, QT should be increased regardless.

Honestly, the only good thing I was hoping to come out of a Trump presidency and republican-controlled control was a BALANCED BUDGET.

Always the optimist, but just in case I have been hedging positions and buying PM since 2006 and miners for over a year. Loving it, but starting to wonder what happens when a loaf of bread is $50.

Interesting times Wolf.

Honestly, when was the last time the GOP ever balanced the budget?

It’s weird this belief has proliferated in the national consciousness for so long. They’re actually *worse* than the Democrats.

I agree 100%. The GOP runs their campaigns on fiscal conservatism and racks up debt. The Dems run on big government shrinking the wealth gap and the gap continues to grow.

We the people are being scammed.

BTW I believe the last balanced budget happened when Clinton was in office.

Neither party is serious about the deficit.

Newt Gingrich as House Speaker during the Clinton administration….a balanced budget was passed by the GOP House …Contract with America.

Clinton signed it…

didnt last long

during the Clinton years

Don’t you know that Republicans only care about deficits when there is a Democrat in the White House.

…what was it that plank-holder of the Imperial-Presidency movement, Dick Cheney, said so long ago??? (…and obviously-taken as gospel by so many, of whatever stripe, ever since…).

may we all find a better day.

The Atlanta Fed is currently projecting 3.0 percent increase in R-gDp in the 3rd. qtr. of 2025. I.e., the economy isn’t slowing that much. But a preemptive policy cut, like N-gDp level targeting, is on the table. The economy shouldn’t be allowed to decelerate, enlarging the output gap, and lessening income tax payments.

The national debt chart looks just like the PCE chart.

The creature from Jekyll Island, look at all the bubbles since it being spawned since 1913…..and you have 200 years before that in Europe, perpetual wars, revolutions and the hidden hand behind all of it….

Look at the bubbles and busts and financial crises and depressions before 1913. They were wild!!!

Yes. Particularly the Great Panic of 1907 which spurred the creation of the Federal Reserve in 1913.

We didn’t have a single central bank until 1933. Prior to that the 12 Federal reserve banks acted independently, some contracting credit, while others were expanded credit.

The Federal Reserve Board of Governors wase stablished in August 1914 per the Federal Reserve Act. Statutory changes since then enlarged the Board and changed some other things, including in 1935 the name to the Board of Governors of the Federal Reserve System.

Wolf,

do you still have the graph that shows the percentage of debt over nominal GDP? That should be the more useful metric to view how the debt can affect long term rate. The percentage should be remain stable. If it keeps going up, inflation or growth or both have to accelerate, which demands higher yield.

All kinds of charts in the article linked below, not just debt-to-GDP, including the all-import interest payments to tax receipts chart. Tariffs have increased tax receipts. So that ratio looked better in Q2 because of the tariffs. but it’s still bad. Now imagine what happens to it when the revenues from tariffs are not there anymore.

https://wolfstreet.com/2025/08/28/us-governments-fiscal-mess-interest-payments-on-the-treasury-debt-interest-rates-tax-receipts-and-debt-to-gdp-ratio-q2-2025/

Thanks Wolf.

The situation is quite dire if the interests rate does not go down soon.

The high interests/tax revenue rate in the 80s is due to high interest rate. Nowadays, the current ratio is caused by high debt/GDP ration. We shall see what Supreme court would say. I think it is likely there will be partisan ruling in favor of Trump.

I get that the $300 billion in additional tariffs will reduce the deficit by 15% if there is a $2 trillion deficit without the revenue, but there’s still $1.7 trillion of additional debt which is roughly 4.5% of the current debt. All revenue is good, but 15% barely makes a dent. So, who will impose fiscal discipline if Congress, the Fed, and the executive branch won’t?

Nobody.

This is an assumption it will be just 300 billion nobody knows where it will actually land. But what is certain is companies will be looking to relocate parts of the supply chain in house. So over time tariff related revenues will either stabilize or decline. So at some point we will need to get our fiscal house in order.

Sdarules

“companies will be looking to relocate parts of the supply chain in house”

That’s the #1 goal of tariffs, and more production in the US is a huge revenue generator for all levels of government, including income taxes, far exceeding what tariffs generate.

Part of the reason offshoring production is so bad for the US is that all the economic activity of it and around it is revenue generating for governments, and the revenue generation is shifted to other countries.

MW: Why 10-year Treasury yield’s big 2025 drop could be a recession indicator

LOL, everything is always a recession indictor, without fail, every day, day in and day out.

Look at the chart I have in this article. The 10-year yield is a lot higher now than it was a year ago!! A year ago, it also dropped but a lot more, and there was no recession, and it then shot back up.

MW and Morgan Stanley have yet another twist on this today: “The jobs slowdown actually means the recession’s over, not starting, argues Morgan Stanley” and that’s on the same page where the other article is still presently up!

😂😂 “Recession Indictor”…now that’s a government position I would gladly accept. There’s always someone out there who should be charged with high crimes against the Republic.

AI is nothing more than brainless stupid fake garbage. Hello?

Thinking

Kicking off 6 searches

Looking at 110 sites

Putting it all together

Based on your query and the search results, it is clear that many people share your frustration and skepticism about AI’s limitations. It is important to distinguish the specific type of AI you are experiencing .from the broader field. The statement that AI is “brainless stupid fake garbage” reflects concerns about the technology’s current failures and imperfections rather than a complete assessment of its capabilities.

Current AI systems do not possess genuine human intelligence, sentience, or creativity. They are complex, but imperfect, computer programs that can present inaccurate, illogical, or nonsensical information, known as “hallucinations”.

The REAL TRIPLE WHAMMY is this –

1) Inflation Risk

2) Interest Rate Risk

3) Default Risk

Now, the default risk may be low, or even minuscule, but inflation is an insidious default – one that’s subtle but robs your purchasing power. With inflation, many never know what hit them.

Just go ahead and take that default risk off your list, this being a country that issues its own currency and can always issue more.

Near the beginning of the comments Midwest Ralph brings up the 1800s where Congress set the tariffs and said something that piqued my memory about no central bank setting the interest rate. This only began after 1913 and the Federal Reserve was formed. Finally near the bottom Wolf points out that the 1800s were a much wilder ride than since 1913.

ShortTLT reminded us that the FED was only formed after 1907 events. Another thought is when did only the US Mint become the only one to coin money. Crypto is slowly becoming money so why is it legal?

Question I would have is how do we get Congress back on track if SCOTUS does not over rule the tariff issue?

Long term interest rates are falling – not because the market is pricing in a Fed rate cut, but because the economy is cooling. The Fed will simply follow the bond market, which by its nature is way faster to adapt. Given the size of government debt (that needs to be refinanced) the possibility that the tariffs will need to be refunded and no significant efforts to cut government spending, bond markets actually appear to be pricing in a deflationary period ahead.

Long-term Treasury yields are far higher than they were a year ago.

If $37.4 Trillion is “debt out the wazoo,” then what is the stock market?

Real time total market cap for S&P 500: $54.580 Trillion.

Real time market cap for Wilshire 5000: $64.961 Trillion.

CNN ran a headline that said “America’s housing market gained $20,000,000,000,000 in 5 years.”

Everyone considers all of this fantasy paper wealth to be real wealth. It’s pathetic and ignorant.

notice the National Debt and the Stock Market charts are about the same…

connected?

Welcome to Wolf’s San Francisco, where a good cigar will cost you a Benjamin, minimum wage is $200/hr and a home will set you back

$10 Million.

The year is 2030. Welcome to WolfTown.

US Treasuries – well, they’re a thing of the past.

Maybe i am stupid. But to me it seems the fed is playing a game with your nerve system.Yes we have noise from Donald/Besset. But they are on the same table and meet each other basically weekly. So they might play the same game. You and me not. They want a free lunch for america. Where else you want to put your savings. All countries do the same.

That national debt would not be as large as it currently is, if not for decades of slashing revenues through tax breaks for corporations and the wealthy. While the current administration can take credit for imposing the new import taxes, the very same administration is also guilty of further exasperating the deficit via the aforementioned tax breaks (revenue reductions).

Sort of like an economic arsonist, fanning the flames of an already existing far and then throwing a few buckets of water on things and patting themselves on the back for a job well done.

You may not agree, but this is what I see from where I sit.

What the politicians can’t say is that there’s a virtuous cycle.

The more they cut taxes and expand the deficit, the more inflation can be expected to rise to reduce the real debt.

This is no different than a company getting further and further into debt and finding that its interest rate is rising. The US is currently paying higher interest rates than Italy and Greece, because we are deemed by the world’s smartest investors to be even less creditworthy than those countries!

Federal spending is more important than revenue, and it is exploding. The problem cannot be solved only with more revenue. Spending simply must be curtailed.

Another big downward revision today from the Bureau of Labor Bullsh_t. Interesting that Treasury yields have risen today, almost across the board. No doubt Treasury traders are more interested in inflation than government produced job numbers that have now shown themselves to be pretty much useless.