Services are where two-thirds of consumer spending goes. And that’s where inflation is. But it’s no longer in rents.

By Wolf Richter for WOLF STREET.

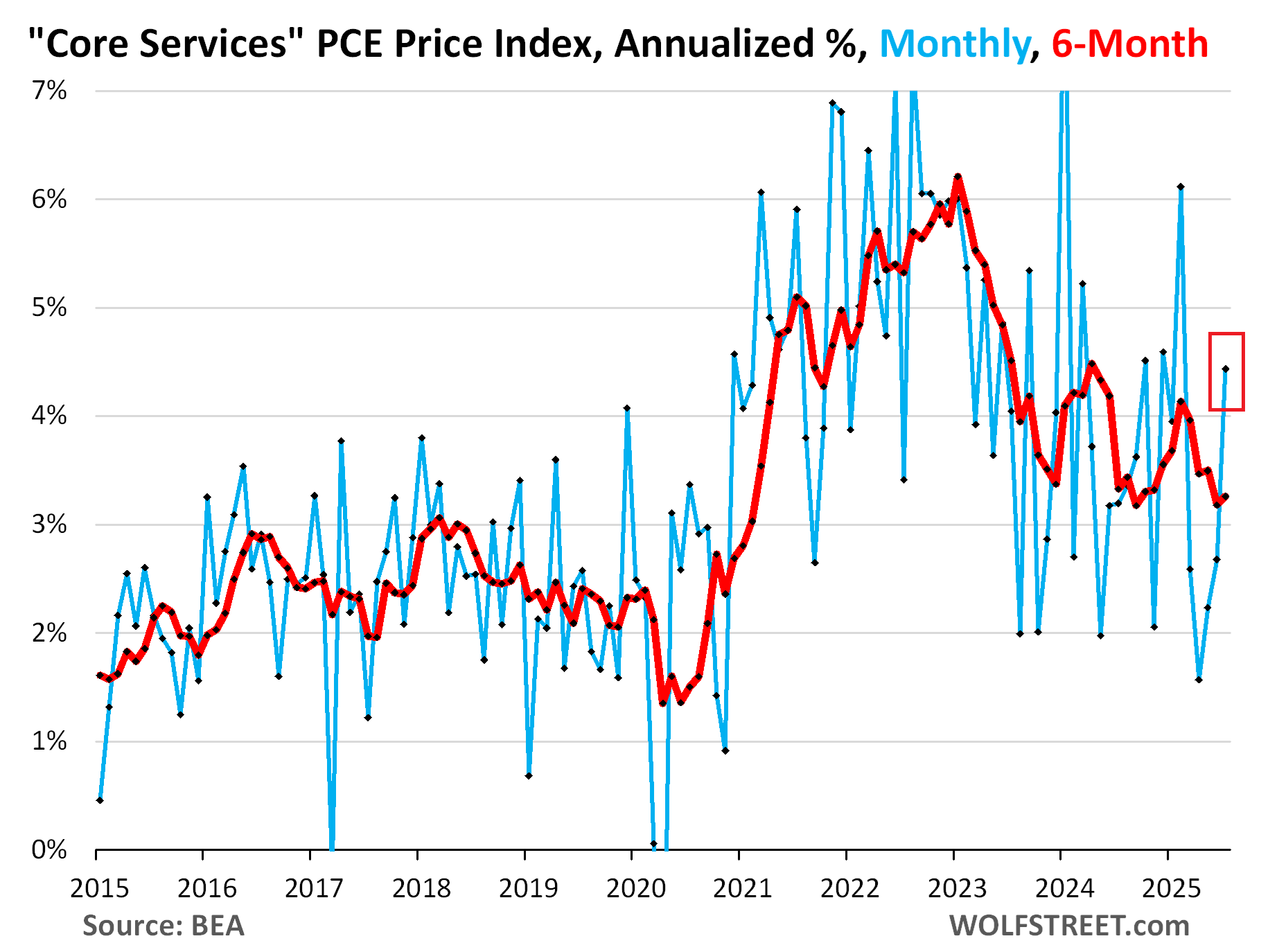

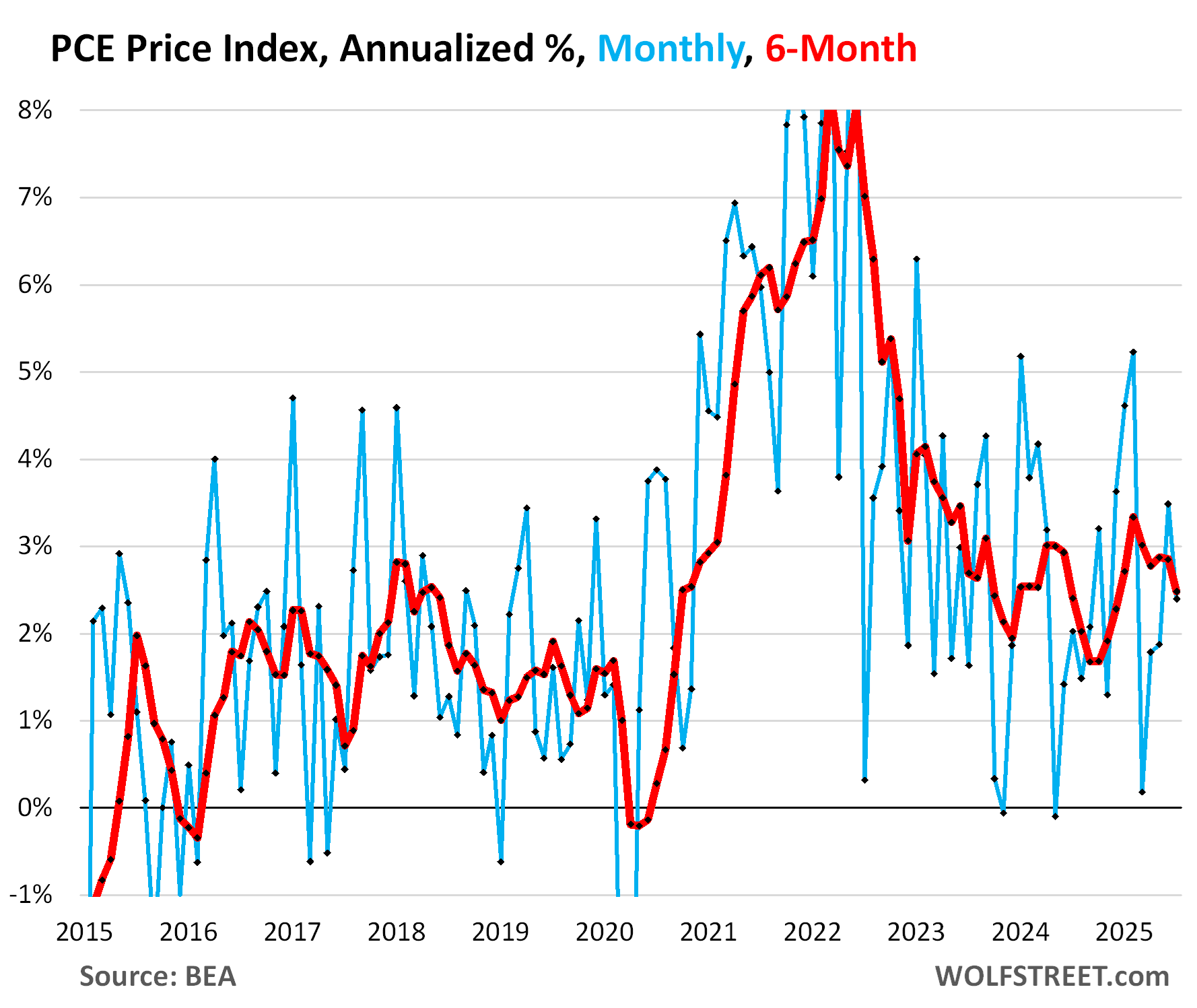

The core services PCE Price Index, which excludes energy services, accelerated to +0.36% (+4.4% annualized) in July from June, the third month in a row of acceleration. The increase was driven by non-housing services; rents continued to decelerate.

This caused the 3-month core services PCE price index to accelerate to 3.1% annualized; and it caused the 6-month index to accelerate to 3.3%. Services are not tariffed.

We have already seen this trend of sharply rising services inflation in the CPI for July, and in the PPI for July, both released earlier this month. The PCE price index here is favored by the Fed as yardstick for its inflation target and usually runs lower than the CPI – and did so for July.

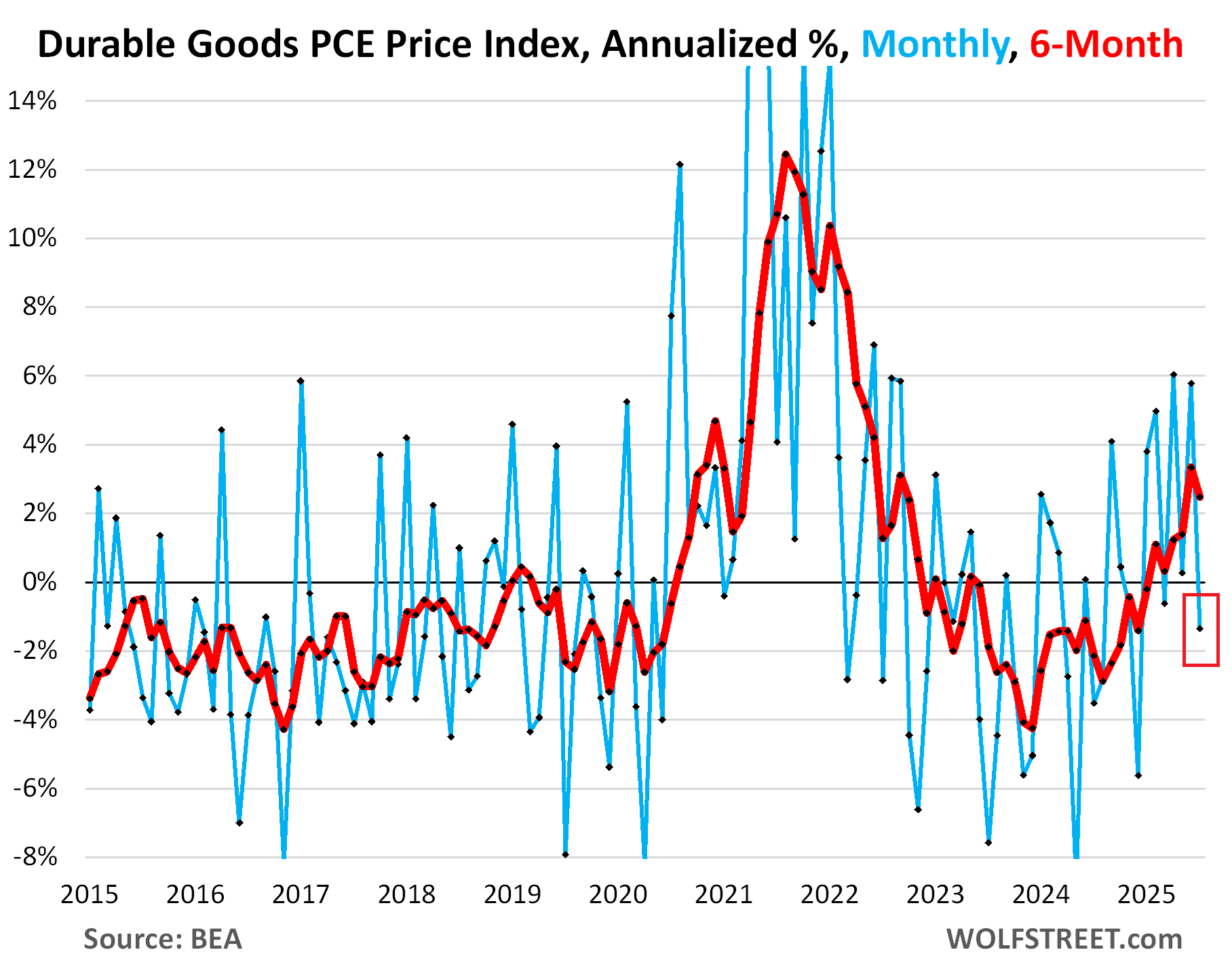

But the durable goods PCE price index fell by 0.11% (-1.3% annualized in July from June). Many durable goods are imported, or their components are imported, and many of them are tariffed.

Durable goods include all motor vehicles, appliances, furniture, bicycles, phones, audio and video equipment, etc.

This is where a big part of the tariffs would show up. But whether or not companies can pass on these taxes depends on market conditions – whether consumers keep buying products at higher prices, now that the free money is gone, or whether sales fall, and companies have to cut prices to get the sales they want.

Durable goods prices spiked massively starting in 2020 and into 2022, and then consumers came out of their pay-whatever stupor, and as resistance to higher prices set in, companies were forced to cut prices and offer deals in order to sell their goods, which is why the durable goods PCE price index turned negative in late 2022. It turned positive for much of 2025 but fell into the negative again in July.

The 6-month index decelerated to +2.5% annualized, from +3.4% in the prior month.

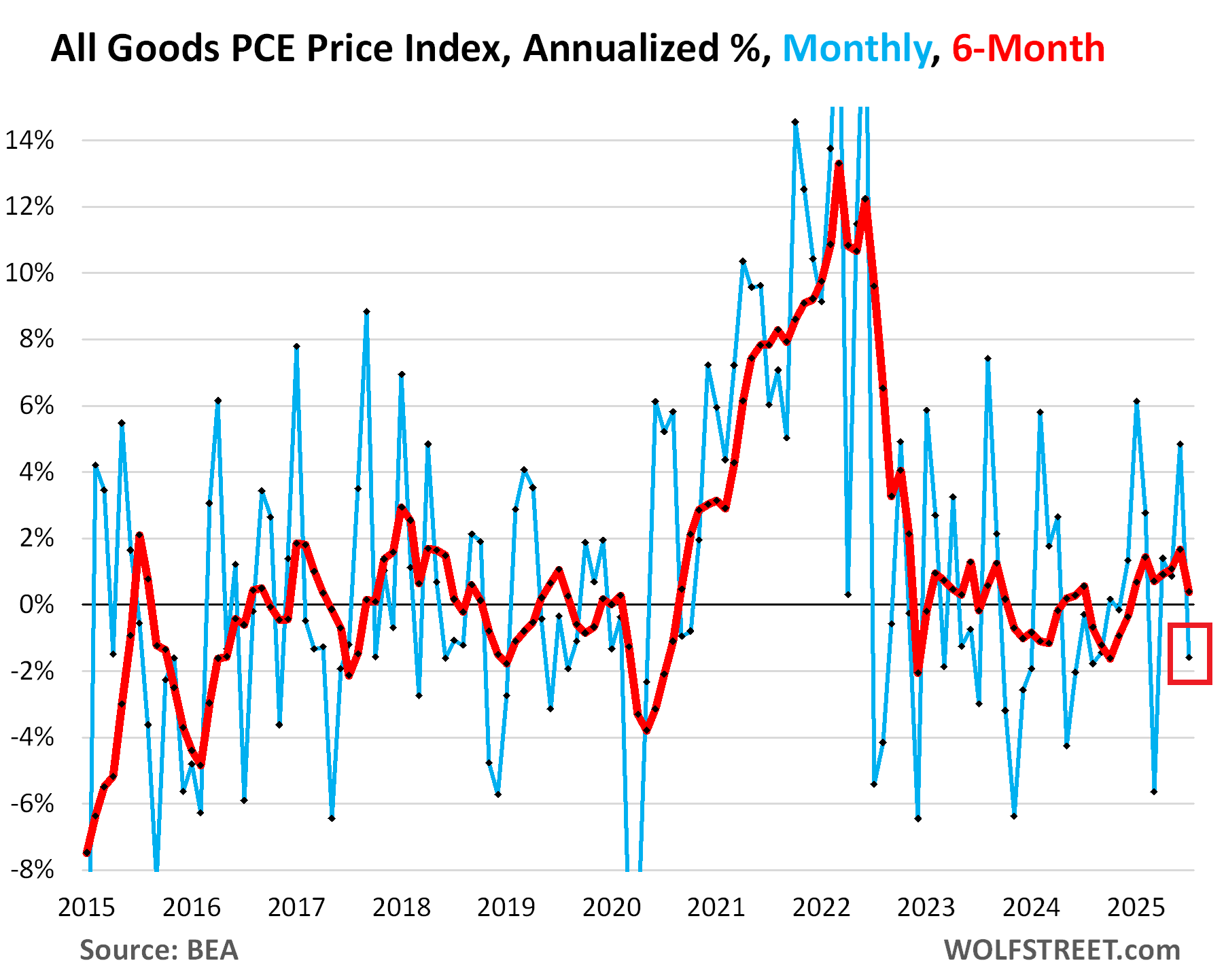

All goods inflation – durables plus nondurables such as food, gasoline, clothing, shoes, supplies, etc. – fell by 0.13% (-1.6% annualized) in July from June.

The 6-month all-goods PCE price index decelerated to +0.4% annualized.

Services inflation is where the action is. Services account for about two-thirds of consumer spending. And services inflation is very hard to squash, as we can see now.

While folks were bent over looking with their big magnifying glasses for micro-traces of tariffs in some cherrypicked goods prices, services inflation blew out behind their backs.

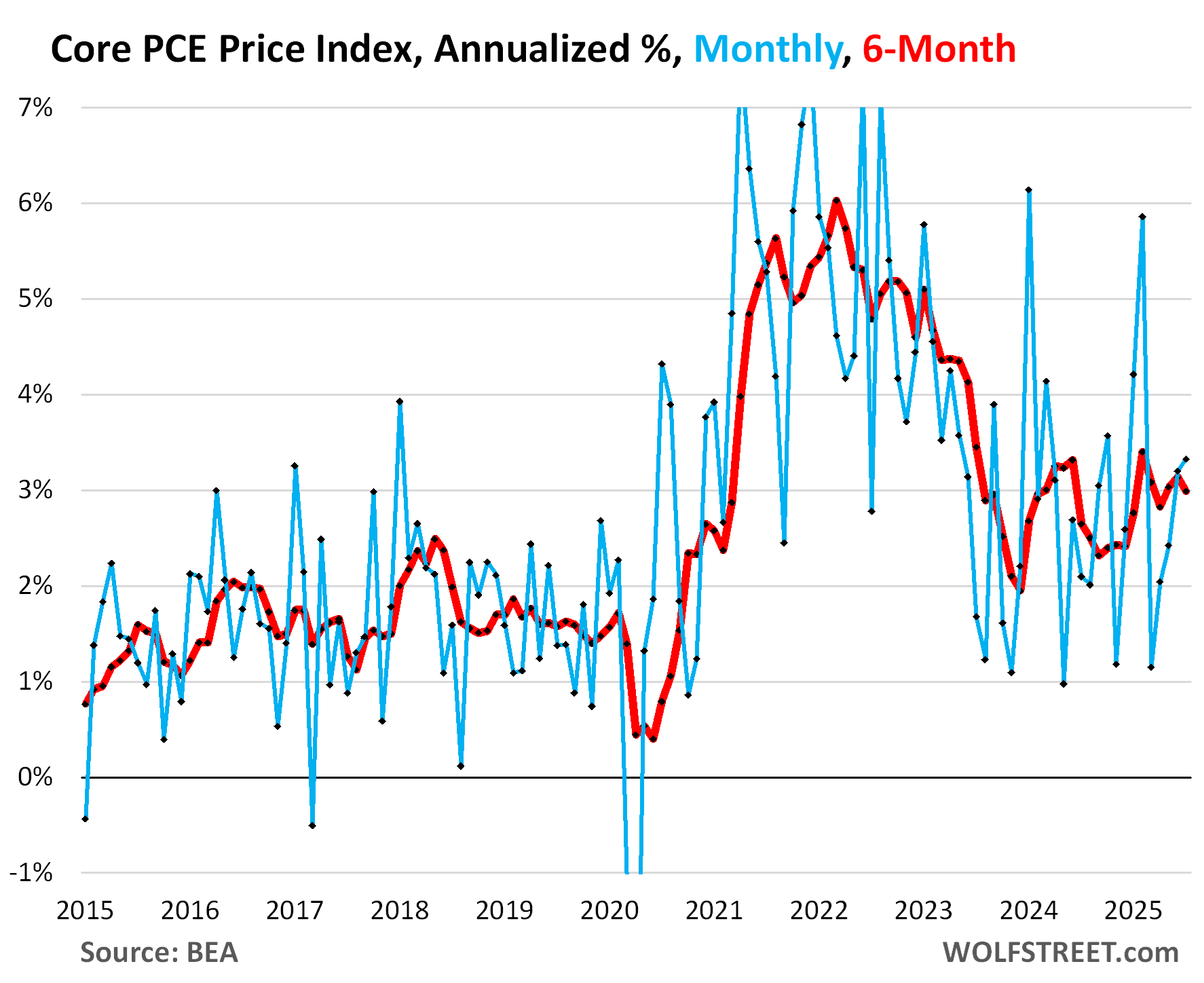

The core PCE price index accelerated a little to 0.27% (+3.3% annualized) in July from June, on this mix of much higher core services inflation and negative durable goods inflation.

The 6-month index decelerated a little to 3.0% annualized in July, from 3.1% in June.

The headline PCE price index decelerated to 0.20% (+2.4% annualized) in July from June, pushed down by the continued plunge in energy prices (-1.0% not annualized) that overpowered the acceleration in core services inflation (+0.36% not annualized).

The 6-month headline index decelerated to 2.5% annualized.

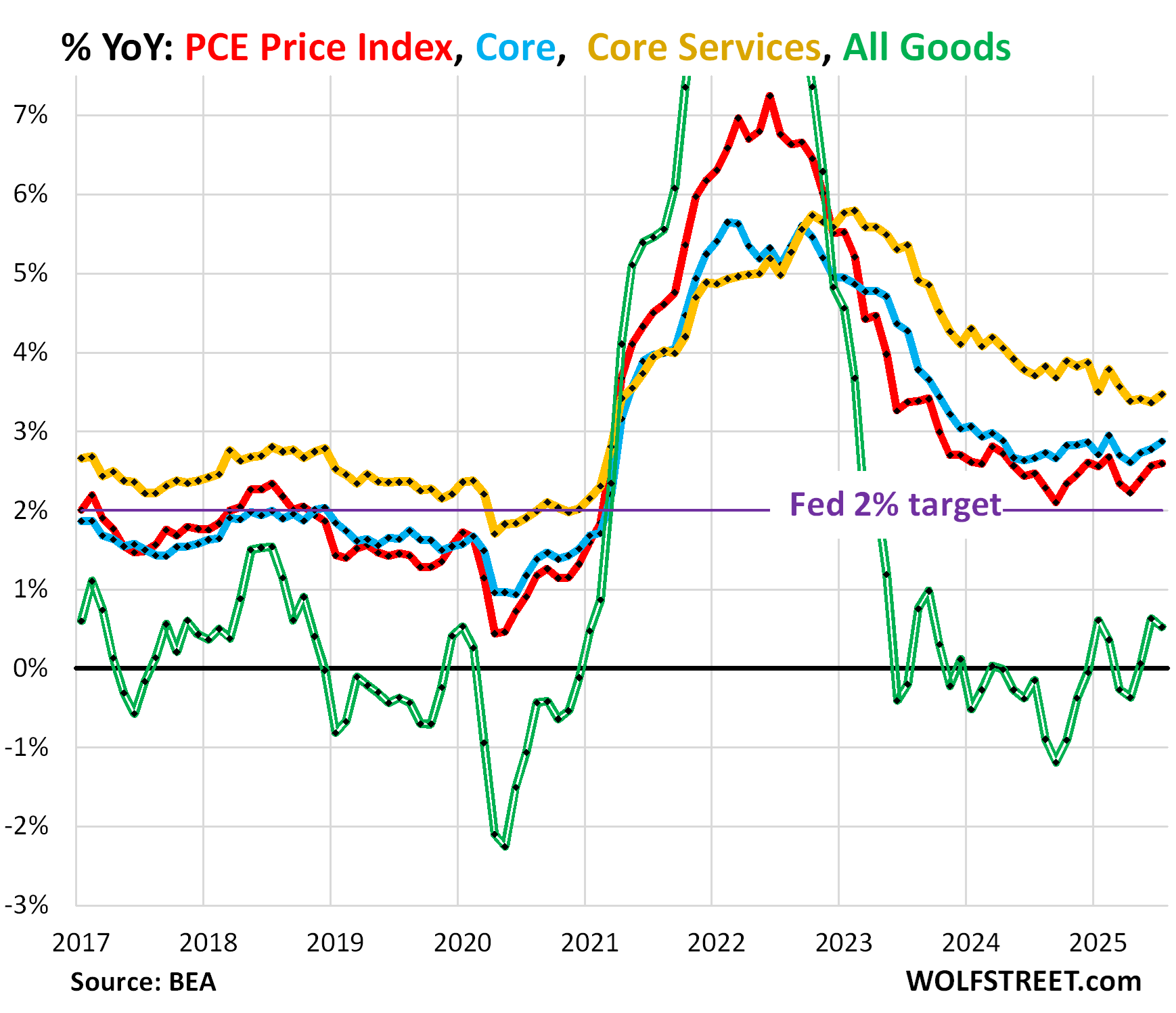

Year-over-year and the Fed’s 2% target.

The year-over-year overall PCE price index and the year-over-year core PCE price index form the yard stick that the Fed uses for its 2% inflation target. Both are well above the 2% target and moving further away from it.

In addition, core PCE and headline PCE were worse in July than they were a year ago. In other words, inflation is now worse than it was a year ago.

Headline PCE price index accelerated a hair to 2.60% in July, worse than a year ago (2.47%), and the third month of acceleration in a row (red in the chart below).

Core PCE price index accelerated to 2.88%, worse than a year ago (2.67%), and the third month of acceleration in a row (blue in the chart).

Core services PCE index accelerated to 3.47% (yellow).

Goods PCE price index decelerated to 0.52% (double green line) and remains very low.

Raising prices is tricky and profits are still huge.

All companies want to raise prices all the time. The reason they don’t is that sales plunge when they do. That is particularly true for companies selling goods, which can be easily comparison-shopped online.

But in 2021 and 2022, as free money was floating around, companies saw that they could raise prices, and by a lot, and sales didn’t plunge because consumers were willing to pay whatever.

When money is free, prices don’t matter. And that’s the phenomenon we saw at the time. But that time is over. The free money is gone. Prices matter a lot.

Whatever part of the tariffs will eventually make it into consumer prices may end up being a one-time bump in the price level of those goods.

But services prices are much harder to tamp down on, in part because many essential services are hard to comparison-shop, and because some big important services don’t have a lot, if any, competition.

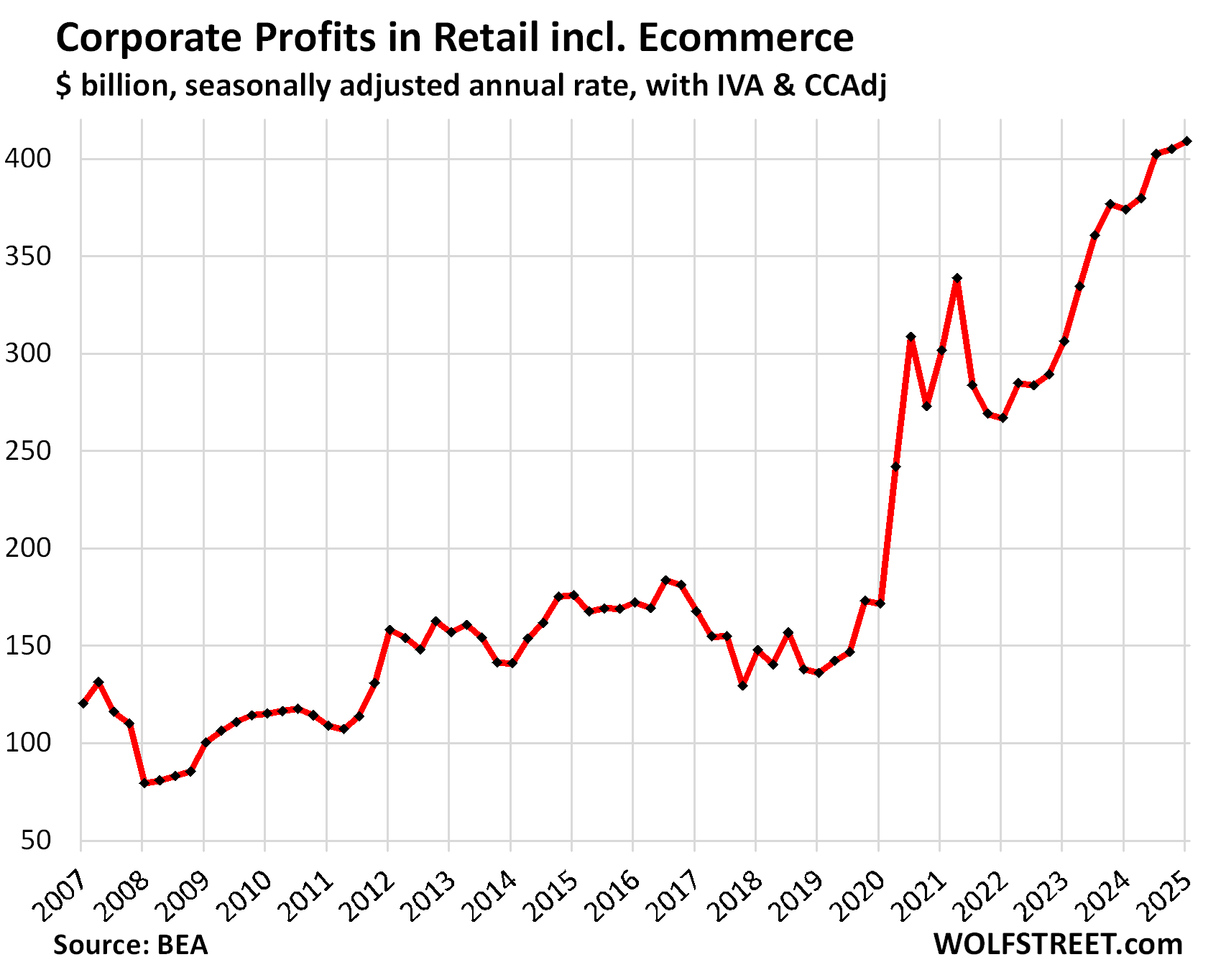

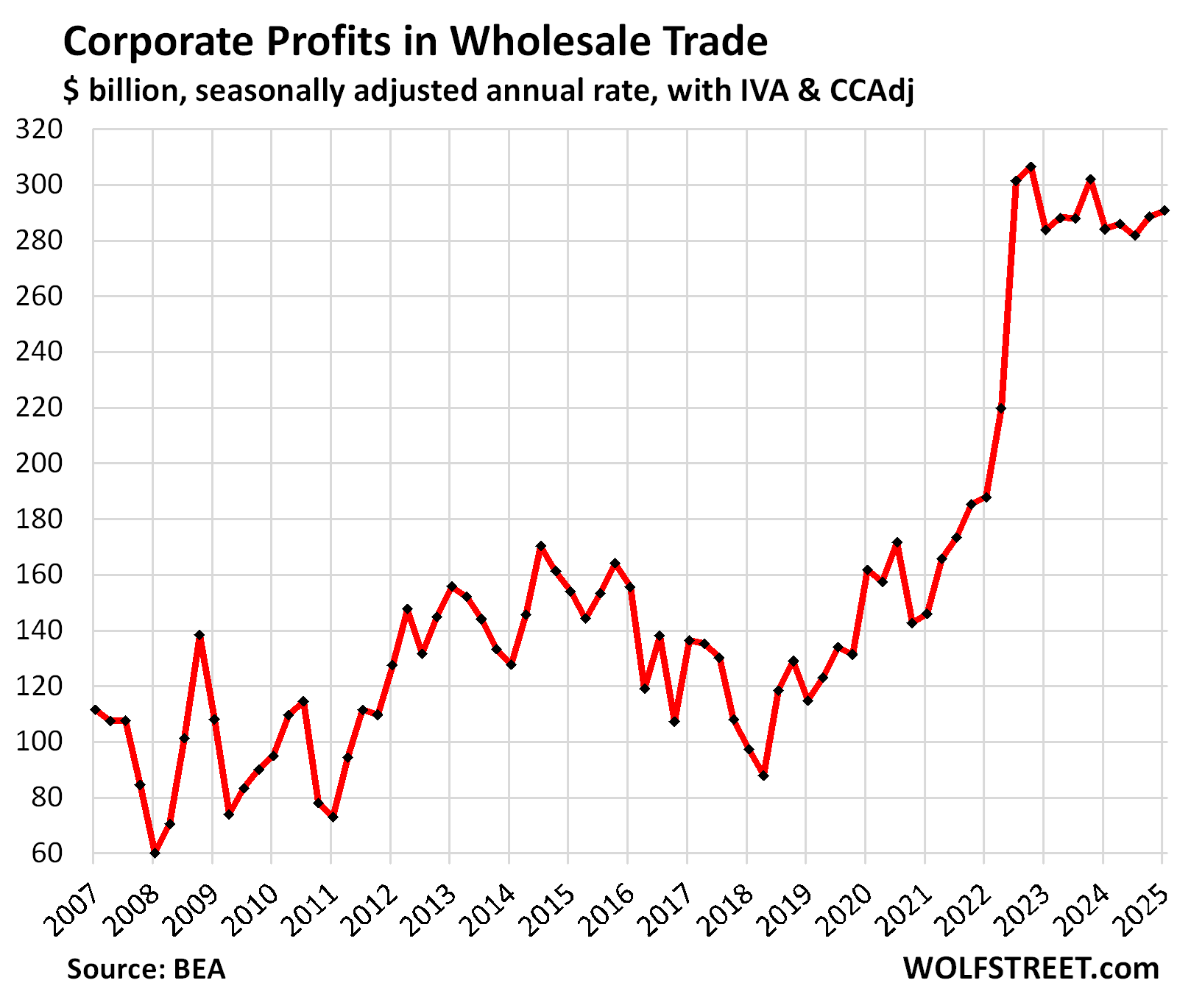

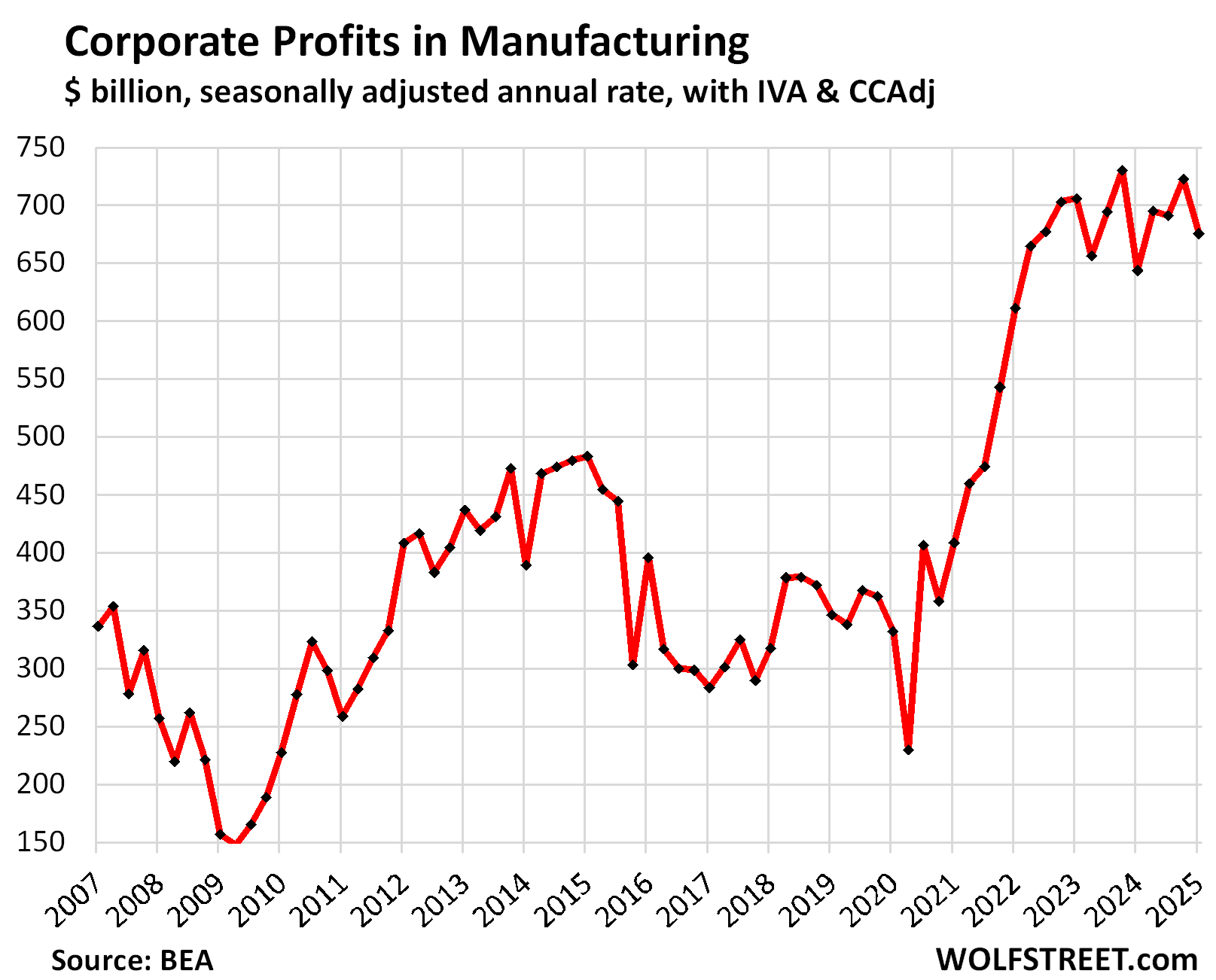

Companies now have lots of room to eat the tariffs after they jacked up their prices during the high-inflation years far more than their costs rose. We discussed the details of those profits by industry here. Some morsels from that report:

At retailers, including ecommerce, profits rose by 138% since Q1 2020:

At wholesalers, profits rose by 80% since Q1 2020:

At manufacturers, profits rose by 100% since Q1 2020:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Companies can eat tariffs, but at the same time, they have a literal fiduciary responsibility to maximize profits. There is continual pressure that last years net income isn’t good enough. Tariffs will bite against that pressure, and any pricing power they can have, they will 100% take. God knows valuations mean they need to keep showing increased net income.

As inventories deplete, we’ll either see corporate new income erode, or prices go up. It may start as the former then transition to the latter. Add in substitution effects and we won’t really know the net effect on either for a solid couple years.

Services makes total sense. In many areas wages don’t support whats needed for housing (despite these starting to soften). So to get local workers, companies are having to raise wages and pass these costs on to customers. This ain’t stopping any time soon. Some areas have a solid 50%/100% gap between CoL and average prevailing wage.

The goal of a company is to charge all they can, as you said. If they can charge more simply because they have an import tax, they were failing to charge all they could before that. The import tax brought no added value to the customer.

You’re missing the impact of competition. In theory, an infinite number of players can sell a commodity. Players will enter the game until the marginal profit margin falls to 0. If one player tries to set a higher price, they will simply lose market share.

If the base cost to get the item to the shelf raises for all players, the cost to consumers goes up.

“If the base cost to get the item to the shelf raises for all players, the cost to consumers goes up.”

No, it doesn’t. At least not for goods because some consumers will choose to not buy those goods, and do without, or delay buying it, and then revenues will slump, and then the company has to roll back the price hike.

For example, people switch from wanting to buy a new car to buying a used car. They delay purchasing appliances after a price increase, and many say forget it. Sure, if an appliance breaks, people replace it. But lots of appliances are bought because people want something new, nicer, fancier, maybe they moved, etc. even as the old stuff still works. Same with cars, bicycles, motorcycles, skis (ask me!), the latest smartphone, laptop, etc. They could still use the old stuff, but want something new.

The US economy is huge on satisfying the consumers WANTS. The goods that people actually NEED are a relatively small portion. For example, you can commute to work in a $5,000 used car (a basic car is a NEED in the US), but you WANT an $80,000 new vehicle. So that $80,000 vehicle price is subject to you deciding that it’s too expensive, and the revenues of the dealer and automaker drop, and they end up rolling back the price increase.

Services can be different. Some services are essential and consumers cannot do without them, but many do not have alternatives or competition. And consumers end up having to grit their teeth and pay for them. Or changing the service is costly and time-consuming: for example, if you get a rent increase and you don’t like it, you can move out, but you need a roof over your head, so it’s hard to just forgo renting, or delaying it, and moving is expensive and time consuming, and so people don’t do it easily, especially if they have lots of stuff, and instead they pay the rent increase. This is why services inflation is tough to get rid of.

You’re missing my word “commodity” wolf….

Of course luxury goods have different price elasticity and depth of competition.

I think you’re greatly underestimating how much the US consumer spends on needs, not wants, particularly in the bottom 50% income bracket.

Not to mention intense price competition in commodities means these are what have been pushed offshore for fixed cost savings….

I don’t care what happens to luxury goods.

Of course…very unlikely that perfect market conditions apply in many markets…especially in the context of global oligopolies cutting deals (or being forced) with foreign gov’ts.

I’m not even sure what profit maximization means in the real world. It’s obvious that many companies do not manage their cost side with profit maximization in mind.

The only thing that’s clear, to me, is that repeated annual losses lead to eventual bankruptcy. Capital can, and does, eventually move to better opportunities.

Look for the standard cost cutting measures (hiring freezes, buyouts, reorgs, job cuts, etc.) to be exhausted before any serious pricing action.

Simplistically there are two main ways to grow ebita and valuation; topline revenue growth via increased pricing and/or sales volume, or bottom line efficiency through increased productivity per headcount. I’m betting on the latter which will show up in hiring numbers first, assuming it hasn’t already done so.

The $800 de minimis exemption ended today. That cements my forecast.

finally. That was the most abused loophole ever — abused also by HUGE foreign retailers selling direct in the US.

I would think that could impact Amazon, but it is a pretty ruthless marketer and uses all kinds of tricks. One product I buy locally for my orchard is $184/5 lbs. Amazon sells it for $225! I save huge buying locally.

So with today’s numbers and recent tone from Pow Pow, do you expect rate cuts is still on track in Sept or do you expect Pow Pow to lean in on these numbers and pause again? If you’re betting on Polymarket, would you change your original bet?

Jerome Powell as Chairman of the Federal Reserve does not make any unilateral decisions by himself but listens quite carefully to the full 12 member FOMC of which he is a member and which makes all policy interest rate decisions. Most of those 12 member are not in favor of lowering the present FOMC interest rates and are carefully watching the inflation numbers which continue to accelerate.

LOL, I get it and I got it many months and years ago. Pow Pow is not a one-man show. When I say Pow Pow it’s already implied it’s the entire FED governing body’s decision. But let’s not forget, Pow Pow does hold a lot of sway. Plus, until recently, Pow Pow is the only open target to the Dwayne Elizondo Mountain Dew Herbert Camacho, to the not into the detail public, wrongly so, he is face of interest rates or why I have to pay more to finance a car, buy a house…etc

Today was just a different version of the July CPI report released earlier this month.

The new thing will be the CPI report for August, coming out just days before the meeting.

But given how much pressure they’re under from Trump, I think they will cut by 25 basis points no matter what — there will be dissenters, maybe in both directions, for bigger cuts and no cuts, and it might be a narrow vote.

A cut will give them some breathing room. If inflation spikes in the fall, they have more ammo to defend not cutting further.

Agree. Even if it’s hidden to the level of being better described as subconscious. Everyone is political.

Losing the battle and giving a small win to the outside pressure can be a win in the longer term war.

The practical implication of a 25 basis point cut are minimal. Debt yield/prices with duration longer than 6 months have already moved in whatever direction the market feels appropriate to respond to a small September cut.

If Cook is made into Crook by then, the Fed will want some good press. But it’s not political[wink!].

4 Guvs sent packing in 4 years is not a good look.

Wolf, do you think the Fed will acquiesce and raise rates if the next CPI and PPI reports are above estimates?

I’ll just repeat what I said above, emphasis added:

“I think they will cut by 25 basis points no matter what — there will be dissenters, maybe in both directions, for bigger cuts and no cuts, and it might be a narrow vote.”

A cut may be followed a by a rise in long rates like last fall. That might take the pressure off the Fed for additional cuts.

Inflation report won’t matter unless it’s way cool which seems unlikely.

Clearly from this and past inflation reports were running closer to 3% then 2% or maybe 4% lol

It’s all about Jobs market!

Weak report and 50 bps will be the discussion.

No way to justify these crazy valuations if people are losing jobs😬

The whole thing is silly tho. Jobs are usually a lagging indicator and if the labor market is weakening and if rate cuts also allegedly take months to work through the economy… what is 25 or 50 bips gonna do? it’s all reactionary 😴

Per usual the Fed and the market will be to late and we’re probably further down the rabbit hole then we are aware of.

Get prepared for some serious inflation in your home insurance costs, even if you live in a low risk state. I have three people in my circle, 2 neighbors and one lawn man who just told me they have been informed that their insurance may go up 40% or more. Drones are flying over their houses looking for mold on their roof. They have been told to replace a perfectly good roof or face a large premium increase. I also got a letter from USAA threatening me with a home inspection to renew my policy. We are going to fight back against this extortion. These insurance companies are trying recoup all their losses from the fires in California, hurricanes in Florida & LA, floods in North Carolina by going after low risk policy holders.

Wolf, since you mentioned here the surge in profits enjoyed by American companies over the past 4 years (in fact, you’d reviewed this matter in a previous piece), I’m curious to know your opinion on something.

During and after the 2021-2024 inflation spike, there was no shortage of commentators claiming that inflation was a reflection of “corporate greed”. The accusation was that many companies “took advantage” of market conditions (trillions in government stimulus, combined with heavily impaired supply chains), raising prices far beyond any actual increase in costs; copious profits and sinister twirling of executive mustaches ensued.

I took this as nonsense, at the time – the sort of thing that only the most extreme, anti-business activist might say. Yet, seeing the surprising trend, post-Covid, in corporate profits, I wonder whether I might not have been a little too dismissive of those claims.

I’m still skeptical of the “greed” analysis, but I have to admit I’d struggle to explain away the burst in profits in a debate with, say, Bernie Sanders.

What’s the right way to think of this?

Look, I worked in business for much of my life, and every single day, you try to figure out how to raise prices. It’s very hard because you lose sales if you do. But if you don’t, you lose money and go out of business. You cut your costs so you can sell more items for less and push up your revenues. But that has its limits too. Call it greed, or call if free market. Whatever.

The hard reality is that in a functioning market, the buyers set the prices. The seller can ask for a higher price, but if the buyer doesn’t want to pay it, there is no sale, and if there are no other buyers at this price, the seller cuts the price until there is a sale to some buyer. Buyers compete with each other, which is what keeps prices from collapsing. That’s the ancient mechanism. And it works well.

What happened during the pandemic was free money. When money is free, prices no longer matter. And it broke the market mechanism. Buyers were suddenly willing to pay whatever, and astonished sellers (my car dealer friends were flabbergasted by this whole thing) tried to figure out how far buyers would go paying whatever, and for two years, buyers went very far paying whatever because free money had destroyed the pricing mechanism.

That was a very unusual phase – I have never seen anything like that before. So call it greed from sellers; or call it stupidity from buyers. Call it whatever. But that’s how it worked.

Free money is like a virus that turns brains to mush. Putting out all this free money from the government and the Fed was a destructive thing to do – and among the things it destroyed was the pricing mechanism, including in the housing market.

As predicted, a Federal appeals court ruled the IEEPA tariffs illegal.

Smart companies knew this was coming and chose to eat the tariffs rather than lose market share, knowing that any tariffs paid will soon be refunded with interest.

LOL, irrelevant. The only thing to watch in these Trump cases is the Supreme Court. The rest is just decoration. Everyone knows that.

Some smart people believe it takes 6 months to 2 years for Fed interest rates adjustments to show up in the real economy. I imagine Tarrifs effects to the economy would be a similar timeline except for the revenue that is collected from the tax, that’s in real time. Pay now; play(boast to domestic) or pain(inflation) later. 2027 we will know, unless the Supreme Court rules them illegal.

I thought the biggest news in today’s data was wage and salary income saw a significant increase of 0.6% MOM, that’s 7.2% annual. That’s red hot indicator where inflation is going.

Bloomberg was shilling today that “goods prices are going to put pressure on inflation”. They also seemed to infer that they agreed that IEEPA tariffs were illegal. Its a shame most people never see these charts and just read headline info.