Services are where two-thirds of consumer spending goes. And that’s where inflation is. But it’s no longer in rents.

By Wolf Richter for WOLF STREET.

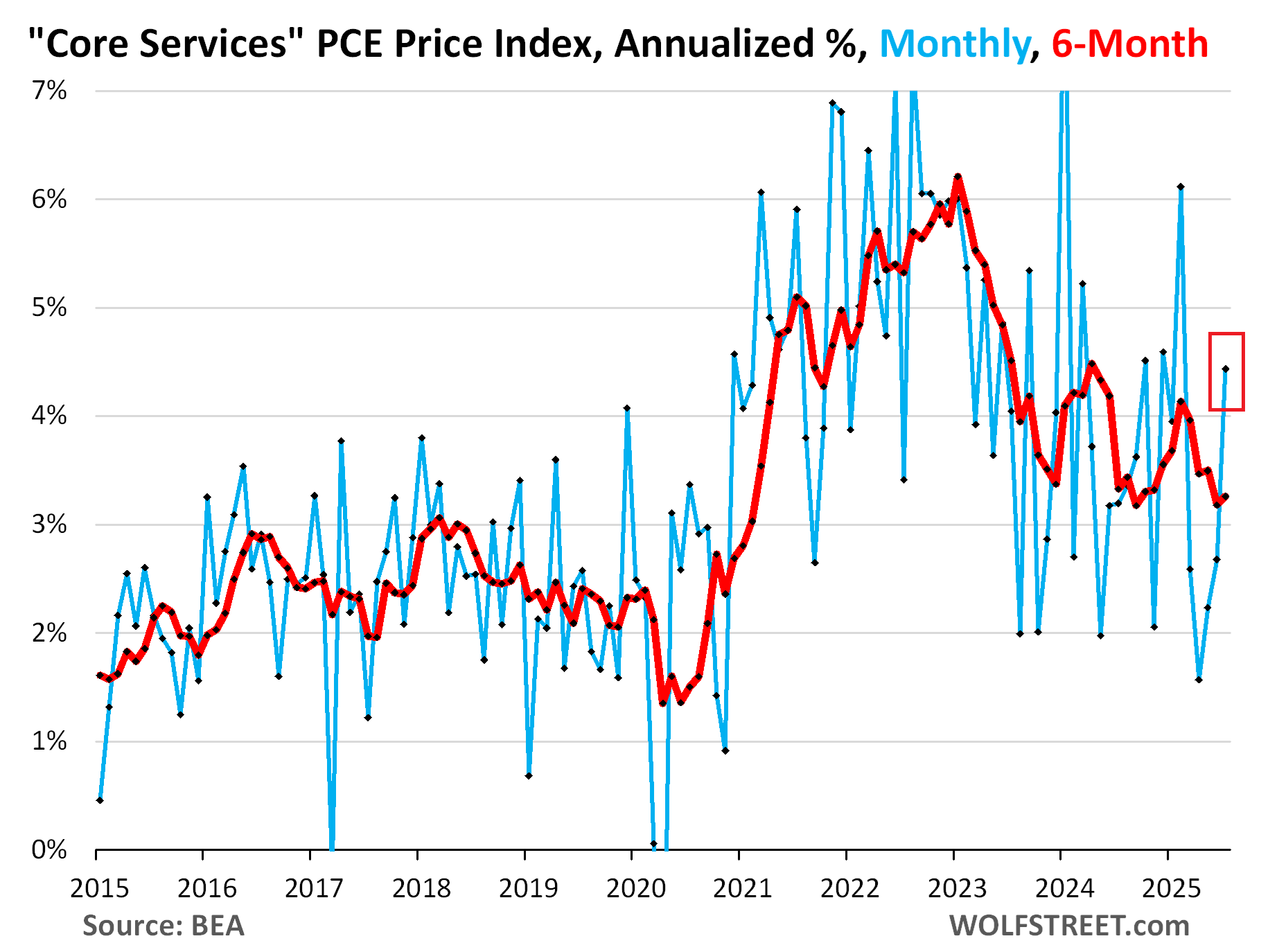

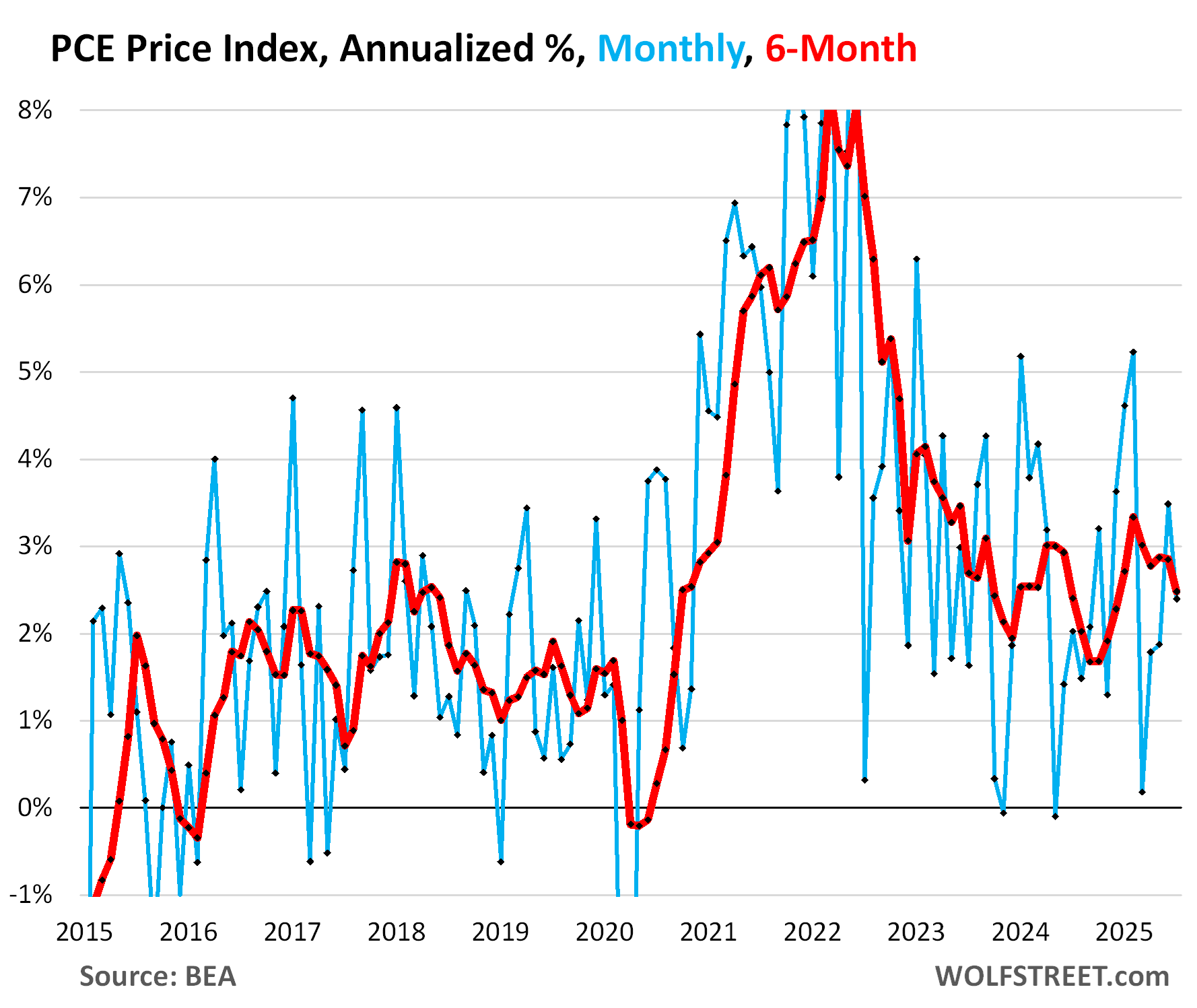

The core services PCE Price Index, which excludes energy services, accelerated to +0.36% (+4.4% annualized) in July from June, the third month in a row of acceleration. The increase was driven by non-housing services; rents continued to decelerate.

This caused the 3-month core services PCE price index to accelerate to 3.1% annualized; and it caused the 6-month index to accelerate to 3.3%. Services are not tariffed.

We have already seen this trend of sharply rising services inflation in the CPI for July, and in the PPI for July, both released earlier this month. The PCE price index here is favored by the Fed as yardstick for its inflation target and usually runs lower than the CPI – and did so for July.

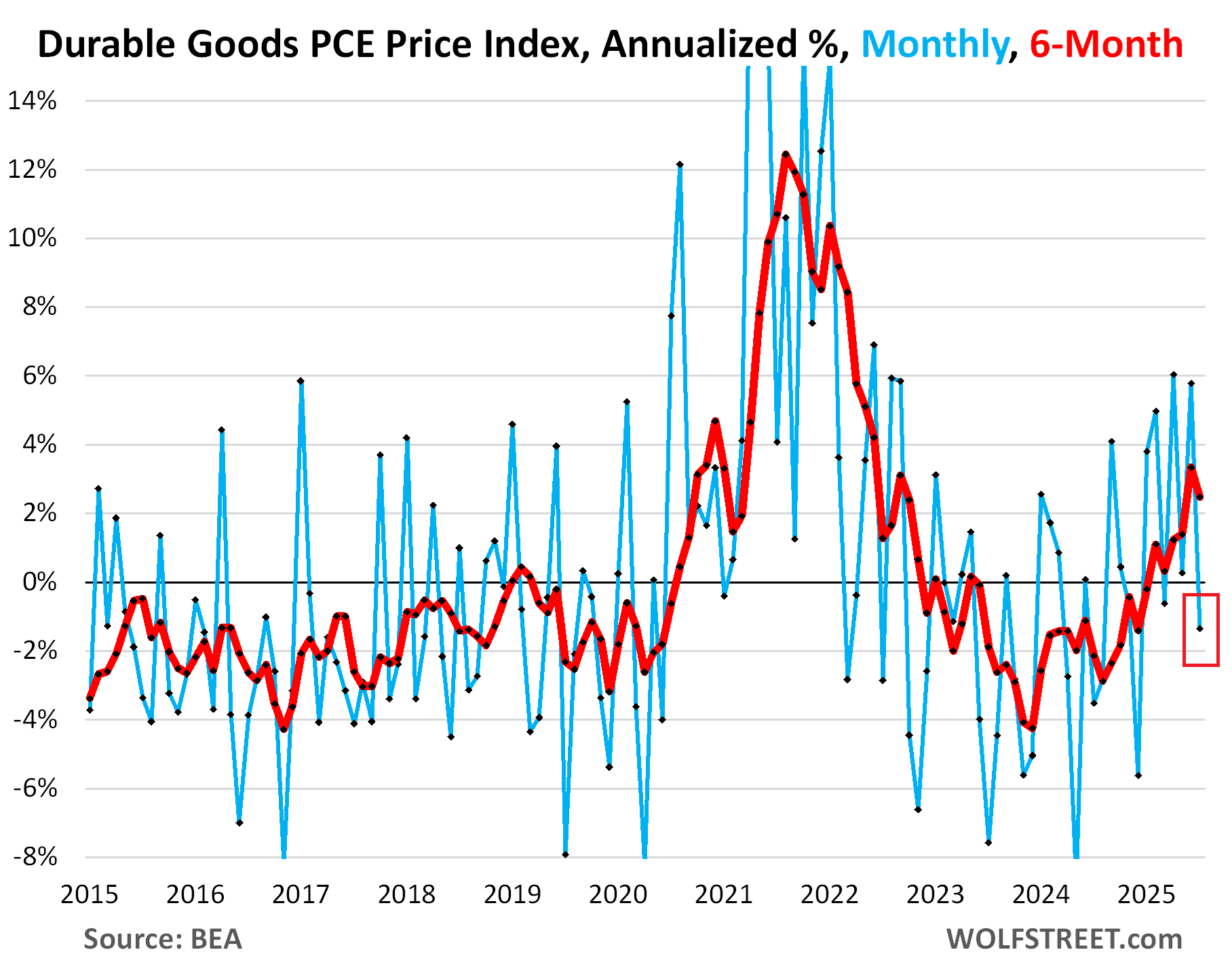

But the durable goods PCE price index fell by 0.11% (-1.3% annualized in July from June). Many durable goods are imported, or their components are imported, and many of them are tariffed.

Durable goods include all motor vehicles, appliances, furniture, bicycles, phones, audio and video equipment, etc.

This is where a big part of the tariffs would show up. But whether or not companies can pass on these taxes depends on market conditions – whether consumers keep buying products at higher prices, now that the free money is gone, or whether sales fall, and companies have to cut prices to get the sales they want.

Durable goods prices spiked massively starting in 2020 and into 2022, and then consumers came out of their pay-whatever stupor, and as resistance to higher prices set in, companies were forced to cut prices and offer deals in order to sell their goods, which is why the durable goods PCE price index turned negative in late 2022. It turned positive for much of 2025 but fell into the negative again in July.

The 6-month index decelerated to +2.5% annualized, from +3.4% in the prior month.

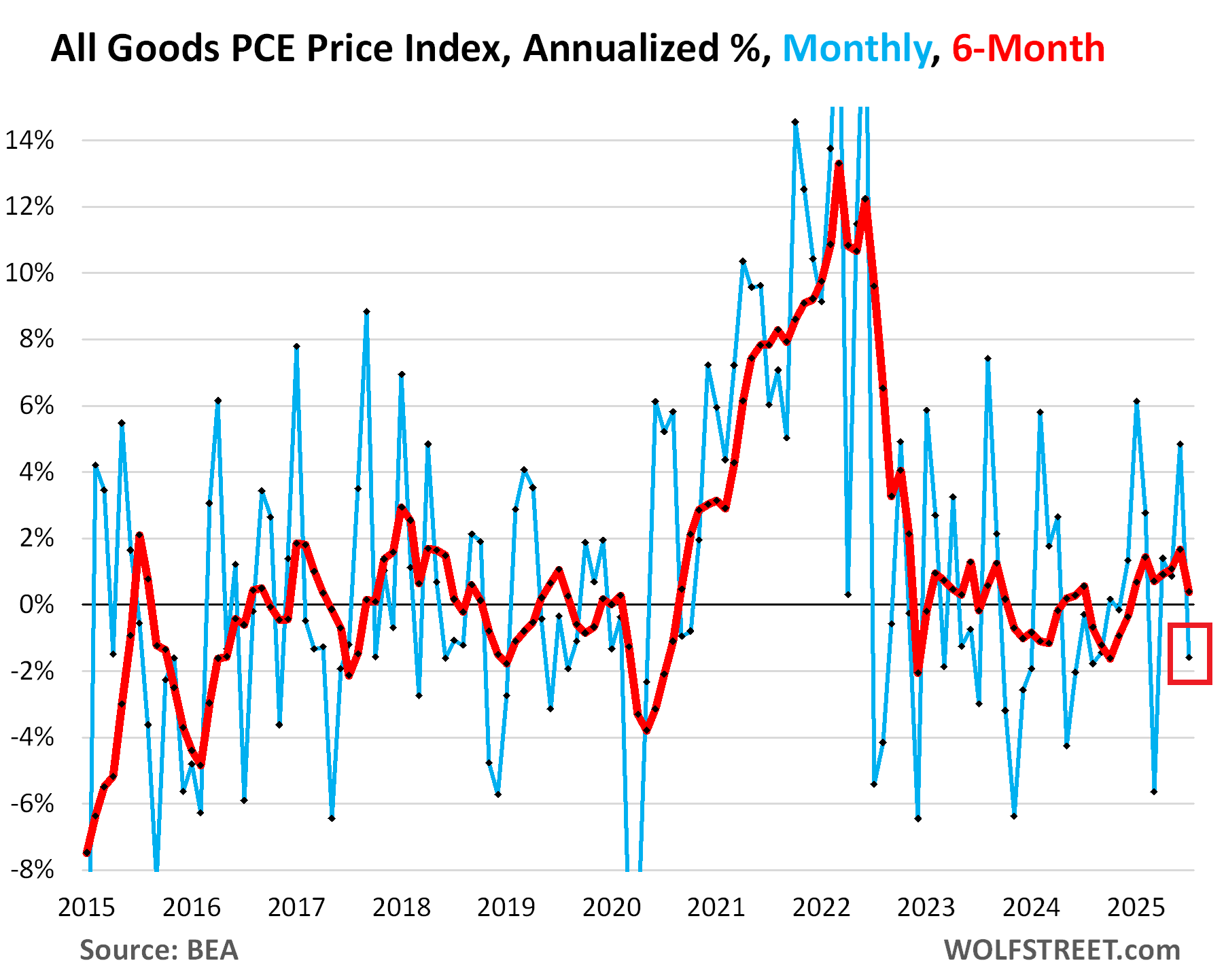

All goods inflation – durables plus nondurables such as food, gasoline, clothing, shoes, supplies, etc. – fell by 0.13% (-1.6% annualized) in July from June.

The 6-month all-goods PCE price index decelerated to +0.4% annualized.

Services inflation is where the action is. Services account for about two-thirds of consumer spending. And services inflation is very hard to squash, as we can see now.

While folks were bent over looking with their big magnifying glasses for micro-traces of tariffs in some cherrypicked goods prices, services inflation blew out behind their backs.

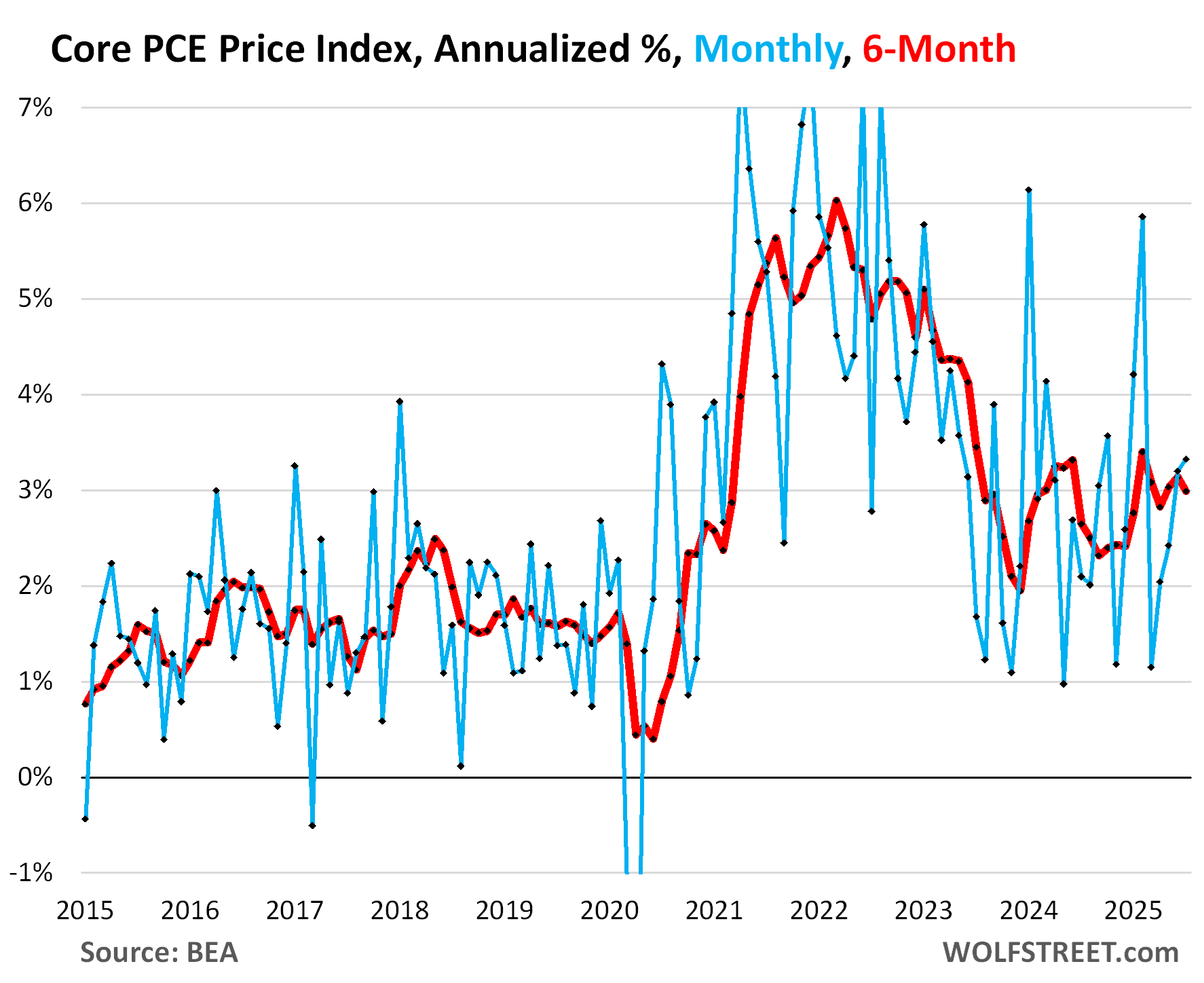

The core PCE price index accelerated a little to 0.27% (+3.3% annualized) in July from June, on this mix of much higher core services inflation and negative durable goods inflation.

The 6-month index decelerated a little to 3.0% annualized in July, from 3.1% in June.

The headline PCE price index decelerated to 0.20% (+2.4% annualized) in July from June, pushed down by the continued plunge in energy prices (-1.0% not annualized) that overpowered the acceleration in core services inflation (+0.36% not annualized).

The 6-month headline index decelerated to 2.5% annualized.

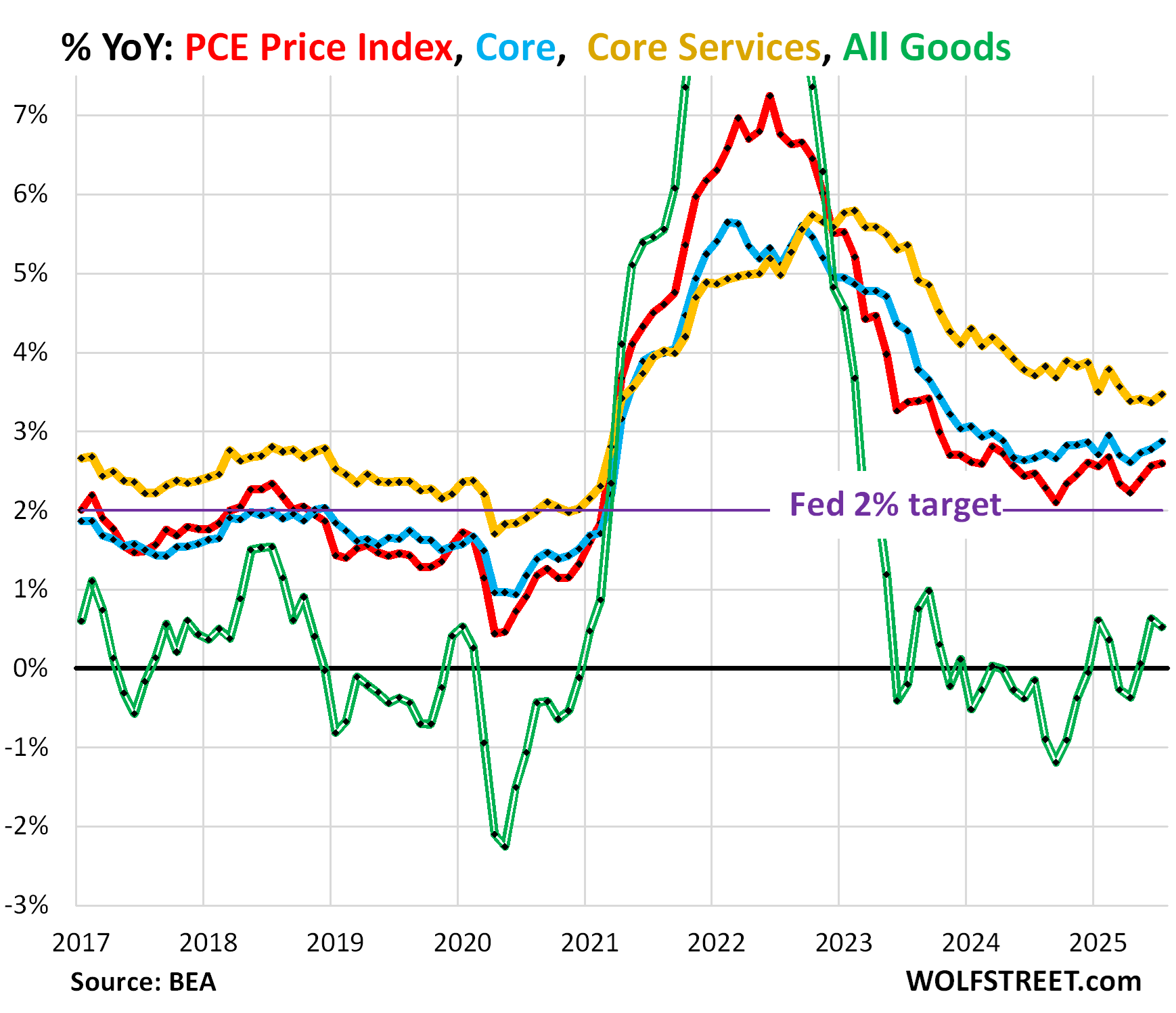

Year-over-year and the Fed’s 2% target.

The year-over-year overall PCE price index and the year-over-year core PCE price index form the yard stick that the Fed uses for its 2% inflation target. Both are well above the 2% target and moving further away from it.

In addition, core PCE and headline PCE were worse in July than they were a year ago. In other words, inflation is now worse than it was a year ago.

Headline PCE price index accelerated a hair to 2.60% in July, worse than a year ago (2.47%), and the third month of acceleration in a row (red in the chart below).

Core PCE price index accelerated to 2.88%, worse than a year ago (2.67%), and the third month of acceleration in a row (blue in the chart).

Core services PCE index accelerated to 3.47% (yellow).

Goods PCE price index decelerated to 0.52% (double green line) and remains very low.

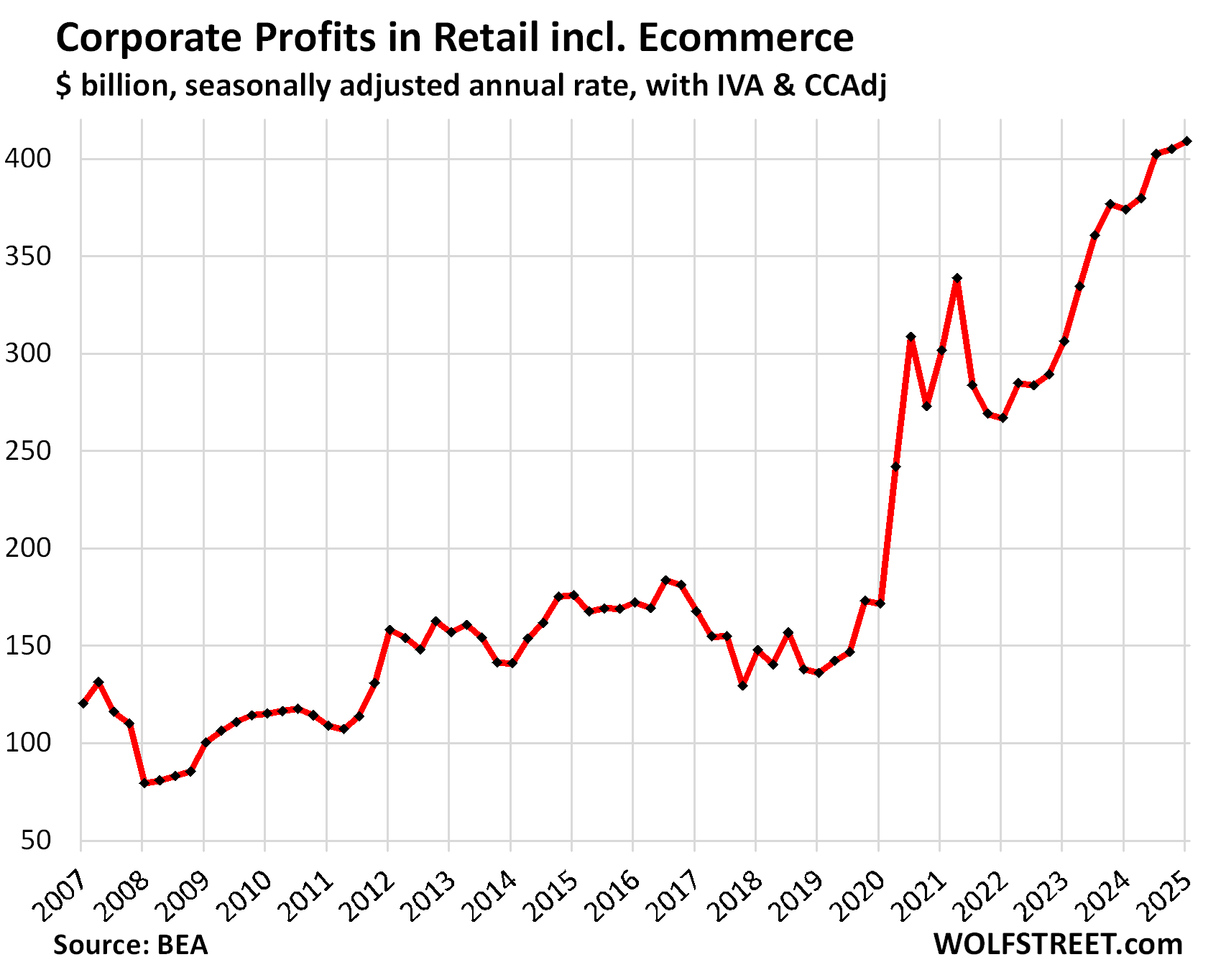

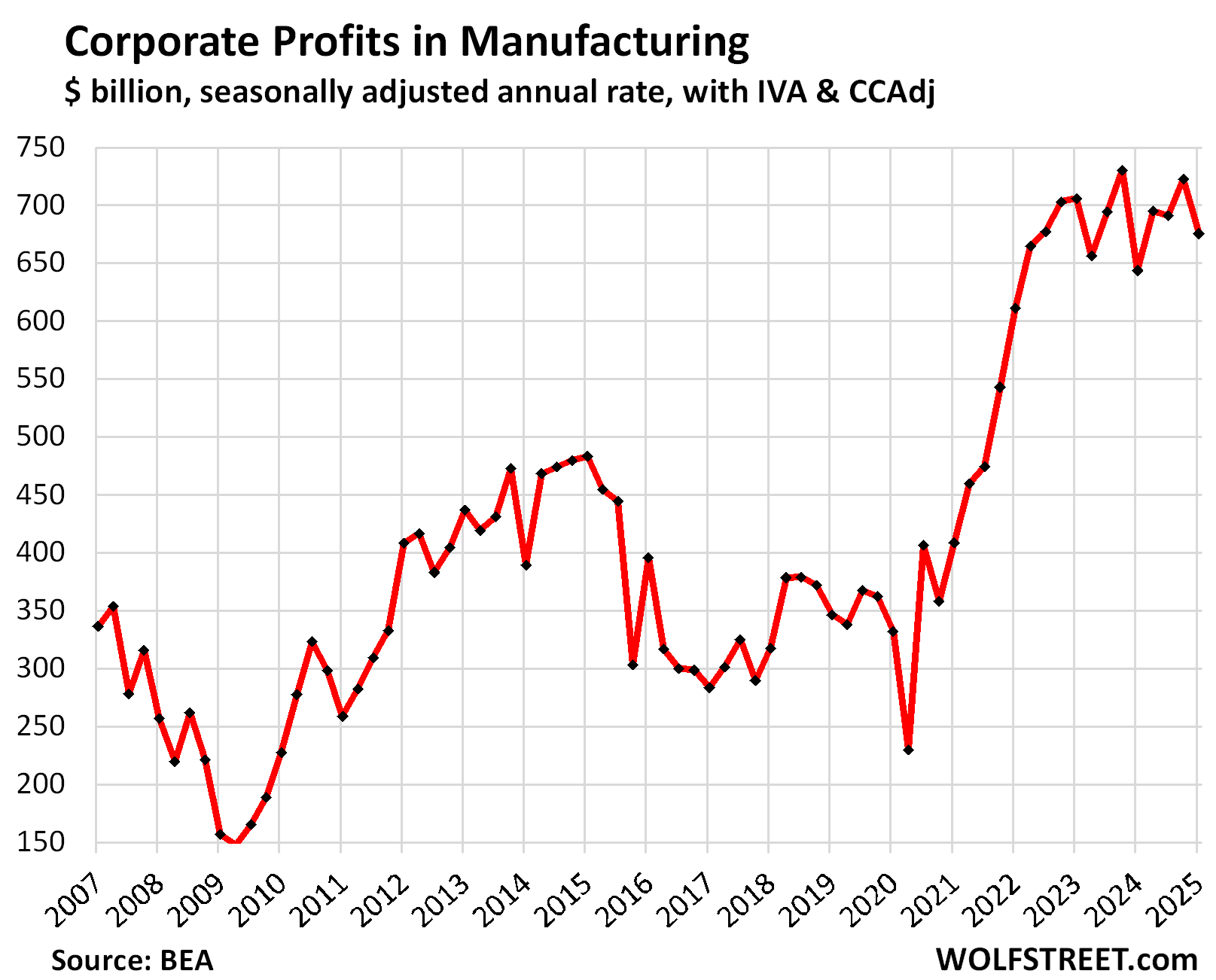

Raising prices is tricky and profits are still huge.

All companies want to raise prices all the time. The reason they don’t is that sales plunge when they do. That is particularly true for companies selling goods, which can be easily comparison-shopped online.

But in 2021 and 2022, as free money was floating around, companies saw that they could raise prices, and by a lot, and sales didn’t plunge because consumers were willing to pay whatever.

When money is free, prices don’t matter. And that’s the phenomenon we saw at the time. But that time is over. The free money is gone. Prices matter a lot.

Whatever part of the tariffs will eventually make it into consumer prices may end up being a one-time bump in the price level of those goods.

But services prices are much harder to tamp down on, in part because many essential services are hard to comparison-shop, and because some big important services don’t have a lot, if any, competition.

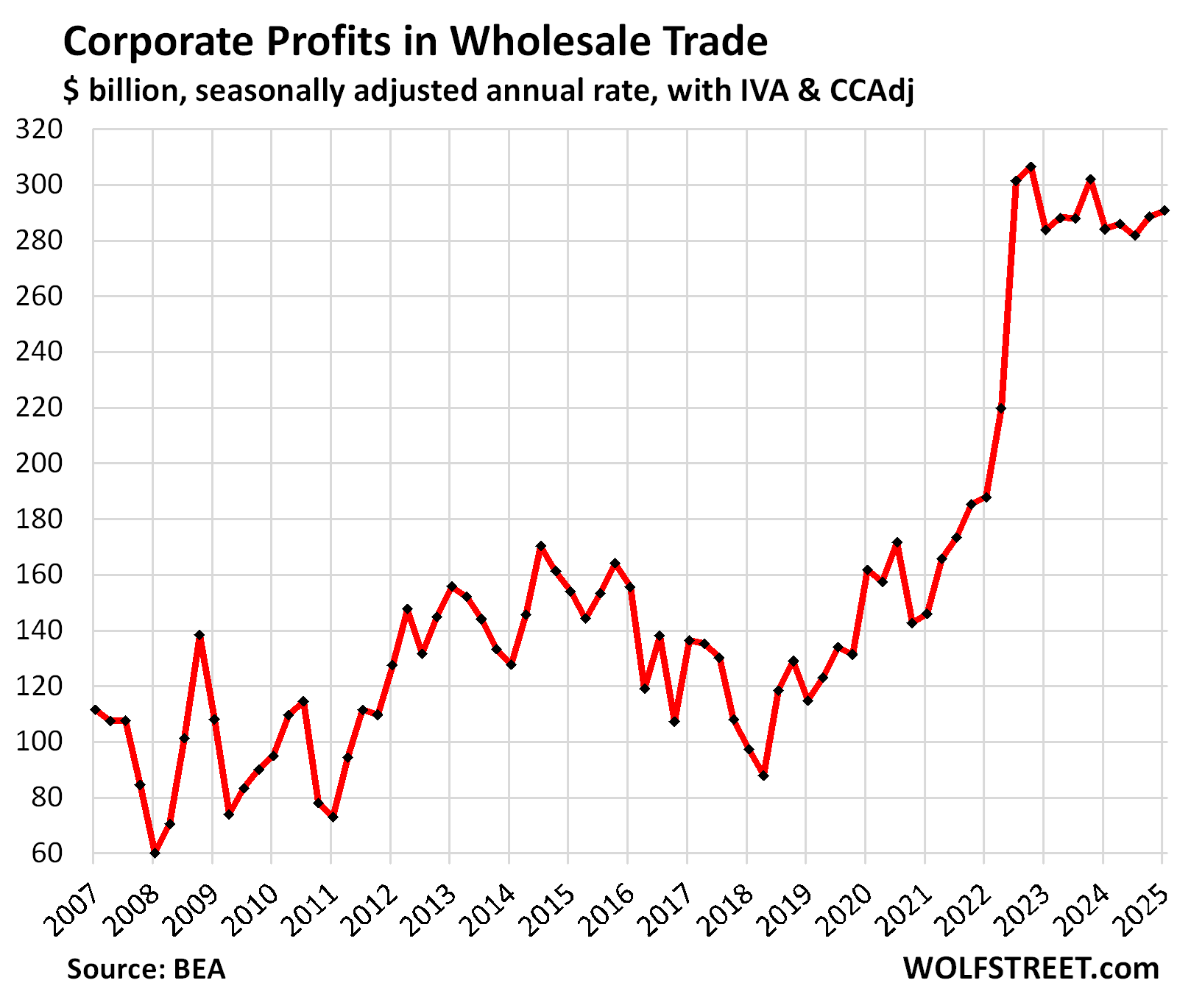

Companies now have lots of room to eat the tariffs after they jacked up their prices during the high-inflation years far more than their costs rose. We discussed the details of those profits by industry here. Some morsels from that report:

At retailers, including ecommerce, profits rose by 138% since Q1 2020:

At wholesalers, profits rose by 80% since Q1 2020:

At manufacturers, profits rose by 100% since Q1 2020:

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Companies can eat tariffs, but at the same time, they have a literal fiduciary responsibility to maximize profits. There is continual pressure that last years net income isn’t good enough. Tariffs will bite against that pressure, and any pricing power they can have, they will 100% take. God knows valuations mean they need to keep showing increased net income.

As inventories deplete, we’ll either see corporate new income erode, or prices go up. It may start as the former then transition to the latter. Add in substitution effects and we won’t really know the net effect on either for a solid couple years.

Services makes total sense. In many areas wages don’t support whats needed for housing (despite these starting to soften). So to get local workers, companies are having to raise wages and pass these costs on to customers. This ain’t stopping any time soon. Some areas have a solid 50%/100% gap between CoL and average prevailing wage.

The goal of a company is to charge all they can, as you said. If they can charge more simply because they have an import tax, they were failing to charge all they could before that. The import tax brought no added value to the customer.

You’re missing the impact of competition. In theory, an infinite number of players can sell a commodity. Players will enter the game until the marginal profit margin falls to 0. If one player tries to set a higher price, they will simply lose market share.

If the base cost to get the item to the shelf raises for all players, the cost to consumers goes up.

“If the base cost to get the item to the shelf raises for all players, the cost to consumers goes up.”

No, it doesn’t. At least not for goods because some consumers will choose to not buy those goods, and do without, or delay buying it, and then revenues will slump, and then the company has to roll back the price hike.

For example, people switch from wanting to buy a new car to buying a used car. They delay purchasing appliances after a price increase, and many say forget it. Sure, if an appliance breaks, people replace it. But lots of appliances are bought because people want something new, nicer, fancier, maybe they moved, etc. even as the old stuff still works. Same with cars, bicycles, motorcycles, skis (ask me!), the latest smartphone, laptop, etc. They could still use the old stuff, but want something new.

The US economy is huge on satisfying the consumers WANTS. The goods that people actually NEED are a relatively small portion. For example, you can commute to work in a $5,000 used car (a basic car is a NEED in the US), but you WANT an $80,000 new vehicle. So that $80,000 vehicle price is subject to you deciding that it’s too expensive, and the revenues of the dealer and automaker drop, and they end up rolling back the price increase.

Services can be different. Some services are essential and consumers cannot do without them, but many do not have alternatives or competition. And consumers end up having to grit their teeth and pay for them. Or changing the service is costly and time-consuming: for example, if you get a rent increase and you don’t like it, you can move out, but you need a roof over your head, so it’s hard to just forgo renting, or delaying it, and moving is expensive and time consuming, and so people don’t do it easily, especially if they have lots of stuff, and instead they pay the rent increase. This is why services inflation is tough to get rid of.

You’re missing my word “commodity” wolf….

Of course luxury goods have different price elasticity and depth of competition.

I think you’re greatly underestimating how much the US consumer spends on needs, not wants, particularly in the bottom 50% income bracket.

Not to mention intense price competition in commodities means these are what have been pushed offshore for fixed cost savings….

I don’t care what happens to luxury goods.

Of course…very unlikely that perfect market conditions apply in many markets…especially in the context of global oligopolies cutting deals (or being forced) with foreign gov’ts.

I’m not even sure what profit maximization means in the real world. It’s obvious that many companies do not manage their cost side with profit maximization in mind.

The only thing that’s clear, to me, is that repeated annual losses lead to eventual bankruptcy. Capital can, and does, eventually move to better opportunities.

Actually, a firm seeks to make as much PROFIT as possible. The ideal price is the one at which:

1. raising the price would result in a reduction in sales that more than offsets the added contribution per unit and

2. lowering the price would result in a reduction in contribution per unit that more than offsets the benefit from increased sales.

A rise in supplier cost from any source raises the ideal selling price described above.

In Econ 101 terms, the supply curve shifts up and to the left.

That’s precisely why econ classes of the 101 type are worthless. They have no idea what goes on in the real world. It’s all just a theory of how economic participants might react under certain simplistic theoretical conditions.

Look for the standard cost cutting measures (hiring freezes, buyouts, reorgs, job cuts, etc.) to be exhausted before any serious pricing action.

Simplistically there are two main ways to grow ebita and valuation; topline revenue growth via increased pricing and/or sales volume, or bottom line efficiency through increased productivity per headcount. I’m betting on the latter which will show up in hiring numbers first, assuming it hasn’t already done so.

The moral of the story is free money is bad. Democrats had the president and Congress for two years and went nuts with giveaways. It caused massive inflation and massive defecits. They rightly were thrown out of office. Trump may actually be right on Tarrifs. It will cause companies to eat the Tarrifs for a bit then seek American suppliers to bring back the profit you speak of. Win win. Higher tax revenue lowering the deficit resulting in more jobs in the USA

What Biden did with free money was stupid. We know…. But you seem to forget the fights and promises from Trump at the end of his first presidency where he floated COVID relief packages even over $2 trillion. Remember the “go big or go home”? He even delayed signing the $900B relief bill unless it included the $2k checks (which he finally signed and was part of what Biden handed out).

The BoD/CEO/whoever has zero fiduciary responsibility to maximize profits. I hear this often, but it’s not true, and never has been.

Crappy business decisions are continuously being made and are numerous. Maybe more bad decisions than good, who knows.

If there is personal gain to the detriment of the company, now that is a breach of fiduciary duty. Actionable? Who knows

The $800 de minimis exemption ended today. That cements my forecast.

finally. That was the most abused loophole ever — abused also by HUGE foreign retailers selling direct in the US.

I would think that could impact Amazon, but it is a pretty ruthless marketer and uses all kinds of tricks. One product I buy locally for my orchard is $184/5 lbs. Amazon sells it for $225! I save huge buying locally.

Amazon.com doesn’t generally ship packages from abroad but rather from US fulfillment centers which would no impact at all from this de minimum package shipping situation.

Yes and if exemption was not ended it would have hurt Amazon very much.

So that one million dollar gift to Trump’s inauguration fund paid off.

So with today’s numbers and recent tone from Pow Pow, do you expect rate cuts is still on track in Sept or do you expect Pow Pow to lean in on these numbers and pause again? If you’re betting on Polymarket, would you change your original bet?

Jerome Powell as Chairman of the Federal Reserve does not make any unilateral decisions by himself but listens quite carefully to the full 12 member FOMC of which he is a member and which makes all policy interest rate decisions. Most of those 12 member are not in favor of lowering the present FOMC interest rates and are carefully watching the inflation numbers which continue to accelerate.

LOL, I get it and I got it many months and years ago. Pow Pow is not a one-man show. When I say Pow Pow it’s already implied it’s the entire FED governing body’s decision. But let’s not forget, Pow Pow does hold a lot of sway. Plus, until recently, Pow Pow is the only open target to the Dwayne Elizondo Mountain Dew Herbert Camacho, to the not into the detail public, wrongly so, he is face of interest rates or why I have to pay more to finance a car, buy a house…etc

Remind us how often even just two people on the Fed vote against the Chair? Yeah, it’s about once every 15 years.

Me thinks correlation is not causation. It could also be Powell is voting in line with the others.

Today was just a different version of the July CPI report released earlier this month.

The new thing will be the CPI report for August, coming out just days before the meeting.

But given how much pressure they’re under from Trump, I think they will cut by 25 basis points no matter what — there will be dissenters, maybe in both directions, for bigger cuts and no cuts, and it might be a narrow vote.

A cut will give them some breathing room. If inflation spikes in the fall, they have more ammo to defend not cutting further.

Agree. Even if it’s hidden to the level of being better described as subconscious. Everyone is political.

Losing the battle and giving a small win to the outside pressure can be a win in the longer term war.

The practical implication of a 25 basis point cut are minimal. Debt yield/prices with duration longer than 6 months have already moved in whatever direction the market feels appropriate to respond to a small September cut.

If Cook is made into Crook by then, the Fed will want some good press. But it’s not political[wink!].

4 Guvs sent packing in 4 years is not a good look.

Wolf, do you think the Fed will acquiesce and raise rates if the next CPI and PPI reports are above estimates?

I’ll just repeat what I said above, emphasis added:

“I think they will cut by 25 basis points no matter what — there will be dissenters, maybe in both directions, for bigger cuts and no cuts, and it might be a narrow vote.”

A cut may be followed a by a rise in long rates like last fall. That might take the pressure off the Fed for additional cuts.

Dang it, I have been betting for no change on Kalshi based on inflation headed the wrong direction.

Since they are all under investigation by Trump they might need the breathing room.

“In addition, core PCE and headline PCE were worse in July than they were a year ago. In other words, inflation is now worse than it was a year ago.”

Cutting now goes against the logic of the steady prices portion of the fed’s dual mandate. Hold rates steady. If the fed cuts, I hope long term yields spike 100 basis points.

Inflation report won’t matter unless it’s way cool which seems unlikely.

Clearly from this and past inflation reports were running closer to 3% then 2% or maybe 4% lol

It’s all about Jobs market!

Weak report and 50 bps will be the discussion.

No way to justify these crazy valuations if people are losing jobs😬

The whole thing is silly tho. Jobs are usually a lagging indicator and if the labor market is weakening and if rate cuts also allegedly take months to work through the economy… what is 25 or 50 bips gonna do? it’s all reactionary 😴

Per usual the Fed and the market will be to late and we’re probably further down the rabbit hole then we are aware of.

Get prepared for some serious inflation in your home insurance costs, even if you live in a low risk state. I have three people in my circle, 2 neighbors and one lawn man who just told me they have been informed that their insurance may go up 40% or more. Drones are flying over their houses looking for mold on their roof. They have been told to replace a perfectly good roof or face a large premium increase. I also got a letter from USAA threatening me with a home inspection to renew my policy. We are going to fight back against this extortion. These insurance companies are trying recoup all their losses from the fires in California, hurricanes in Florida & LA, floods in North Carolina by going after low risk policy holders.

What losses? Sure they have to pay out claims, part of the business. But I thought insurers for the most part are enjoying record profits.

They are increasing their profit margins by raising rates on low risk policy holders.

Interesting about the roof comments. I’m getting a class 3 new roof in about 2 months but my roof is 20 years old and the asphalt shingles were rated at 20 years then. Installed new in 2006.

My insurance rates were raised 30 percent last year . As a retired person these fixed costs are not dropping and no income to offset. That’s life . Our economic system is not set up to getting old but neither are our minds or bodies .

Spending Labor Day weekend in Branson MO and the place is packed . People dropping money on food drinks and high cost low quality stuff. Baby Boomers and Millennials with kids. The STR craze has cooled off with a few STR sales that have dropped 30 percent .

wow its worse then what you say there is no effective competition in these markets. guess what happens to prices in those cirmstances.

yup

USAA doesn’t write new policies for homes in Florida. I just got my renewal for hurricane insurance and it was $600 per year LESS than last year. My hurricane insurance is now less than it was before Ian and Milton. This company required a home inspection before writing a policy. It’s not a bad idea and it was pretty painless. Mainly they are looking for leaky pipes. And yes, many insurance companies aren’t willing to take on a new policy when the roof is over 20 years old.

Insurance rates through the roof, whilst insurance industry banking record profits. Almost makes you wish for good legislation or actual collective insurance. Instead we’ll get a bigger and bigger jungle of smaller insurers that seek to get in on the feast with marginally lower rates, with all overhead and default risks that comes with that.

…insurance rates further increasing due to roof punctures caused by rates ‘going through’ it, perhaps?

may we all find a better day.

Wolf, since you mentioned here the surge in profits enjoyed by American companies over the past 4 years (in fact, you’d reviewed this matter in a previous piece), I’m curious to know your opinion on something.

During and after the 2021-2024 inflation spike, there was no shortage of commentators claiming that inflation was a reflection of “corporate greed”. The accusation was that many companies “took advantage” of market conditions (trillions in government stimulus, combined with heavily impaired supply chains), raising prices far beyond any actual increase in costs; copious profits and sinister twirling of executive mustaches ensued.

I took this as nonsense, at the time – the sort of thing that only the most extreme, anti-business activist might say. Yet, seeing the surprising trend, post-Covid, in corporate profits, I wonder whether I might not have been a little too dismissive of those claims.

I’m still skeptical of the “greed” analysis, but I have to admit I’d struggle to explain away the burst in profits in a debate with, say, Bernie Sanders.

What’s the right way to think of this?

Look, I worked in business for much of my life, and every single day, you try to figure out how to raise prices. It’s very hard because you lose sales if you do. But if you don’t, you lose money and go out of business. You cut your costs so you can sell more items for less and push up your revenues. But that has its limits too. Call it greed, or call if free market. Whatever.

The hard reality is that in a functioning market, the buyers set the prices. The seller can ask for a higher price, but if the buyer doesn’t want to pay it, there is no sale, and if there are no other buyers at this price, the seller cuts the price until there is a sale to some buyer. Buyers compete with each other, which is what keeps prices from collapsing. That’s the ancient mechanism. And it works well.

What happened during the pandemic was free money. When money is free, prices no longer matter. And it broke the market mechanism. Buyers were suddenly willing to pay whatever, and astonished sellers (my car dealer friends were flabbergasted by this whole thing) tried to figure out how far buyers would go paying whatever, and for two years, buyers went very far paying whatever because free money had destroyed the pricing mechanism.

That was a very unusual phase – I have never seen anything like that before. So call it greed from sellers; or call it stupidity from buyers. Call it whatever. But that’s how it worked.

Free money is like a virus that turns brains to mush. Putting out all this free money from the government and the Fed was a destructive thing to do – and among the things it destroyed was the pricing mechanism, including in the housing market.

This is the most level-headed, plain-spoken, accurate, and clear explanation of the free market economy that I have read in many years.

Agree with all of this. Another contributor is that free money was handed out to local governments, to schools, to states, to big corporations, to small businesses (through forgivable PPP loans), to individuals, and many more. So at all levels, you had people and organizations with tons of free money willing to pay whatever.

Hopefully our “leaders” learned their lesson, and next time there is a crisis, whether a recession or whatever, and at the very most, only dole out money on a targeted basis and not so that people have more than they started with.

Yep, you had greed and stupidity happening simultaneously. An unusual combination.

It seems to me that Covid forced many businesses to have workers work from home. Restaurants, hotels, and travel saw big declines in revenue. Thus, all those folks who didn’t spend money on those things had extra money to spend on home upgrades including setting up a home office where they could work more comfortably and efficiently. They weren’t stupid in paying more for goods that were in short supply to meet their needs. They were saving money on transportation and eating out and travelling and they simply reallocated that money to make their home environment more conducive to riding out the pandemic in their homes.

The free money analysis that I read here today for the first time ignores that much of the world also saw substantial inflation partly due to Covid supply chain disruptions and partly due to the decline of Russian oil and natural gas and Ukrainian grains and vegetable oils on the international market. The US economy continued to grow while many other countries saw their GDP drop or stagnate. Our GDP growth during Covid can be attributed partly to that free money, so free money wasn’t all bad.

According to a Fed report about 40% of our peak inflation of 9% in 2022 was taken by corporations as increased profit while our nation was going through a Covid pandemic that killed over 1 million Americans. Supply and demand may justify that increase in corporate profit, but corporate leaders could have sacrificed some of that profit for the good of the public in a time of a killer pandemic.

Luther – …the term: “good corporate citizen” has been a non-sequitir for many, many years, I fear, now…

may we all find a better day.

As predicted, a Federal appeals court ruled the IEEPA tariffs illegal.

Smart companies knew this was coming and chose to eat the tariffs rather than lose market share, knowing that any tariffs paid will soon be refunded with interest.

LOL, irrelevant. The only thing to watch in these Trump cases is the Supreme Court. The rest is just decoration. Everyone knows that.

The Federal Circuit is not irrelevant since it is the appeals court that hears all tariff related appeals.

The Supreme Court will get the final word since it was a 7-4 en banc decision and the 7 couldn’t all agree on reasoning. This is the kind of case that the supreme court likes to take.

Yes. And that’s exactly why they stayed their own ruling, to allow Trump to appeal to the Supreme Court. This way, they can make the political statement they wanted to make without causing chaos.

The stay was based on the equities and courteay to the supreme court.

There is no irreparable harm to the plaintiffs from leaving the tariffs in place, since importers will be able to eventually recover their money with interest. Giving the supreme court time to consider the matter is just good judicial manners.

If the Supreme Court sides with the lower courts, what happens to all the tariff revenues that have been collected so far? Are they given back to the companies that were taxed?

If the sun doesn’t rise tomorrow, what happens to my garden? Do I worry about that? No.

I will love to see Congress squirm when faced with the Treasury returning $200+ billion in tariff revenue. They’ll choke on their knuckles before agreeing to it.

In fact, they’ll pass legislation to make them permanent before turning off that cash spigot. I think Trump knows this.

100%! In fact they they love that they can wait to see if the court will side with them. They can get a sense for that. And will delay actually having to codify that into law. Because besides they are as equally greedy as they are lazy.

Some smart people believe it takes 6 months to 2 years for Fed interest rates adjustments to show up in the real economy. I imagine Tarrifs effects to the economy would be a similar timeline except for the revenue that is collected from the tax, that’s in real time. Pay now; play(boast to domestic) or pain(inflation) later. 2027 we will know, unless the Supreme Court rules them illegal.

I thought the biggest news in today’s data was wage and salary income saw a significant increase of 0.6% MOM, that’s 7.2% annual. That’s red hot indicator where inflation is going.

Bloomberg was shilling today that “goods prices are going to put pressure on inflation”. They also seemed to infer that they agreed that IEEPA tariffs were illegal. Its a shame most people never see these charts and just read headline info.

“inflation is now worse than it was a year ago” Wolf.

It’s time for the Fed, in all its bloated wisdom, to cut again.

Obviously, it is time for the Federal Reserve to RAISE its policy interest rates to counter rising inflation.

Pardon my sarcasm. I forgot the /s, but I thought it was obvious.

So it seems that the US companies are taking it on the chin for now. Import price index is relatively flat. Original thought came from Lyn Alden Newsletter.

Powell should NOT cut interest rates in September. None of the data supports a rate cut. Inflation is going up. The economy is overheated and needs some hard medicine to cool it off. If he cuts rates, then the long term bond market will crash like it did last year at this time and kill the housing market which is already in a recession.

You have commented perceptively a number of times on how the flow of money offshore for imports of physical goods cancels the multiplier effect benefit we would have gotten from the wages paid to U.S. workers had the goods been made here.

It occurs to me that this is equally true of the importation of worker-hours through off-shoring — and that not only is the tariff rate on imported worker-hours currently 0%, but also that Trump’s tariffs include none whatsoever on those imports.

The flip side is you stop using less labor through off shoring or H1B visas you will see pressure for wages to further increase. That is a good thing for the working class but obviously can hit inflation or simply increase the rate at which jobs are eliminated through AI and automation, but that is not an if but a when. I still think the key challenge is how mostly essential goods and services are priced such as health care and insurance as we move down the road. People talk about how much Europe pays extra in taxes but they also don’t pay 10s of thousands a year for health insurance either, admittedly on my case 80% covered by my employer but that is an entirely separate issue.

But sending money offshore for.imports drives the dollar down at the margin which makes exports more affordable to foreigners. More imports enable more exports and thus the so -called multiplier effect is preserved.

You have a weird fantasy.

The US has been sending money offshore and importing more than exporting to an ever-larger extent for 40 years, and the only thing it did was get worse. And in the process, it destroyed US manufacturing capacity, infrastructure, expertise, jobs, and tax revenues, and destroyed the secondary and tertiary benefits of manufacturing, and made the US critically dependent on countries like China. It’s hard to believe that there are still people out there who think this is somehow good. Good for what? China? Your stock portfolio?

Wolf man – you know as well as I do that when the F-Ed lowers interest rates, that inflation is going in one direction (not down), which will mean more inflation in goods and services. Report back to us all in a few months. I could write the headline right now for you, if you like.

I have to wonder about the sudden doubling – sometimes even more – of corporate profits in the last few years. Wondering what those profit margins are as a percent of revenue. Are there any economic relationships showing any negative or positive consequences where “profit margin” % would be the y-axis on the graph? For example would higher and higher macroeconomic margins be correllated with macroeconomic inflation or deflation or unemployment or whatever? Can those margins be maintained?

Bloomberg: Bessent Warns of US ‘Embarrassment’ If Tariffs Ruled Illegal

Trump cabinet officials told a federal appeals court that ruling president’s global tariffs illegal would seriously harm US foreign policy, with Treasury Secretary Scott Bessent warning of “dangerous diplomatic embarrassment.”

The administration on Friday filed statements by Bessent, Commerce Secretary Howard Lutnick and Secretary of State Marco Rubio in the US Court of Appeals for the Federal Circuit in Washington. The court is expected to decide soon whether President Donald Trump exceeded his authority to impose tariffs under a 1977 emergency powers law.

Bessent, Lutnick and Rubio’s statements were filed in support of a request that any ruling against the administration be immediately put on hold until the US Supreme Court issues a final decision. Failing to do so would have “devastating and dire consequences,” Lutnick said.

During July 31 oral arguments before the Federal Circuit, the administration’s claims of broad tariff power were met with skepticism, suggesting the judges might side with separate challenges filed by a group of small businesses and a coalition of Democratic-led states. Friday’s filing seems to suggest the administration is worried about precisely that outcome.

Trump has loaded the Supreme Court. However, Barret and Roberts sometimes do not toe the line. It would be amusing if the Supreme Court sh_tcanned Trump’s tariffs, but I doubt they will.

The Supreme Court generally disdains tax cases. Perhaps they will stay out of this one, notwithstanding the fractured appellate ruling…

A rate cut right now would be grossly irresponsible, so I expect the FED to do it.

The Fed has made so many mistakes in the past, the best strategy is to assume they will make another one. So it is almost certain they will cut. Not sure how to play it. Maybe an inverse 20 or 30 year Treasury bond ETF.

They will cut by .25%, and the long bond will go up by the same amount. Goodby housing recovery. Instead of cutting by .25 or .50 Powell should do us all a favor and use the next Fed meeting to announce his resignation

Many companies forced through price increases in 2020 due to what ultimately proved to be a very short lived but substantial inflation crisis for many basic commodities. When those prices largely came back down many of the prices did not, hence your profit chart. It is difficult, as a manufacturer, to force price increases. You will not have an easy time with your customers who are typically not end user or consumer, they are retailers or some such. So, there is an understandable reluctance from a manufacturer perspective to reduce prices. Likewise, the retailer margins increased by doing the same and then leveraging their position against the more competitive/saturated product markets and keeping the extra. Point being there has been a larger than average margin for a lot of food and other commodity sensitive items that will probably absorb a lot of the tariffs. Though that sounds nice, it will not be so nice on the market. I am curious to see who will try pushing through price increases to preserve those margins and what kind of backlash they will see.

“When money is free, prices don’t matter. And that’s the phenomenon we saw at the time. But that time is over. The free money is gone. Prices matter a lot.”

Do you mean to say that “free money” is no longer being handed out by the government? Or do you mean to say that all the “free money” that was handed out has now been completely incinerated by the Fed via QT?

I don’t know how much “free money” was given away, but I do know from your articles how much the Fed has incinerated, to date, via QT.

There were several aspects to this free money, and we talked a lot about it at the time. It includes being able to borrow for 30 years at below 3% when inflation was between 6% and 9%. This was more than free money.

If the bulk of the cost of tariffs is being absorbed by large publicly traded corporations, then we’re likely to see these earnings begin to decline from their current highs.

Likewise, if current stock valuations hinge on these elevated earnings, then we’re also likely to begin seeing cracks form in current stock prices as well.

Maybe. Those that pay the tariffs aren’t particularly important to the stock market anymore. Most of the largest cap stocks are primarily services or domestic producers (obviously not all).

Did a quick comparison of my Amazon purchases since 2023 and I paid $588 and today it would cost $526.

Amazon prices change by the hour.

Local sales, competition, sellers needing some profit, sellers getting rid of inventory, etc etc.

There are sites that send you price alerts.

Mr. Wolf writes: “The core services PCE Price Index, which excludes energy services, accelerated to +0.36% (+4.4% annualized)…”

Perhaps if the Federal Reserve aimed for 0% inflation in their process, they would hit 2% in actuality; because, the error in what they think they are doing and what actually happens seems to be around 2% of inaccuracy.

“While folks were bent over looking with their big magnifying glasses for micro-traces of tariffs in some cherrypicked goods prices, services inflation blew out behind their backs.”

Yes, the media is definitely bordering on being completely insane along with a plethora of so called economists…