Despite big waves of delistings.

By Wolf Richter for WOLF STREET.

It’s not that there are a lot of homes coming on the market – there are not – but that the homes that are on the market don’t sell because prices are too high.

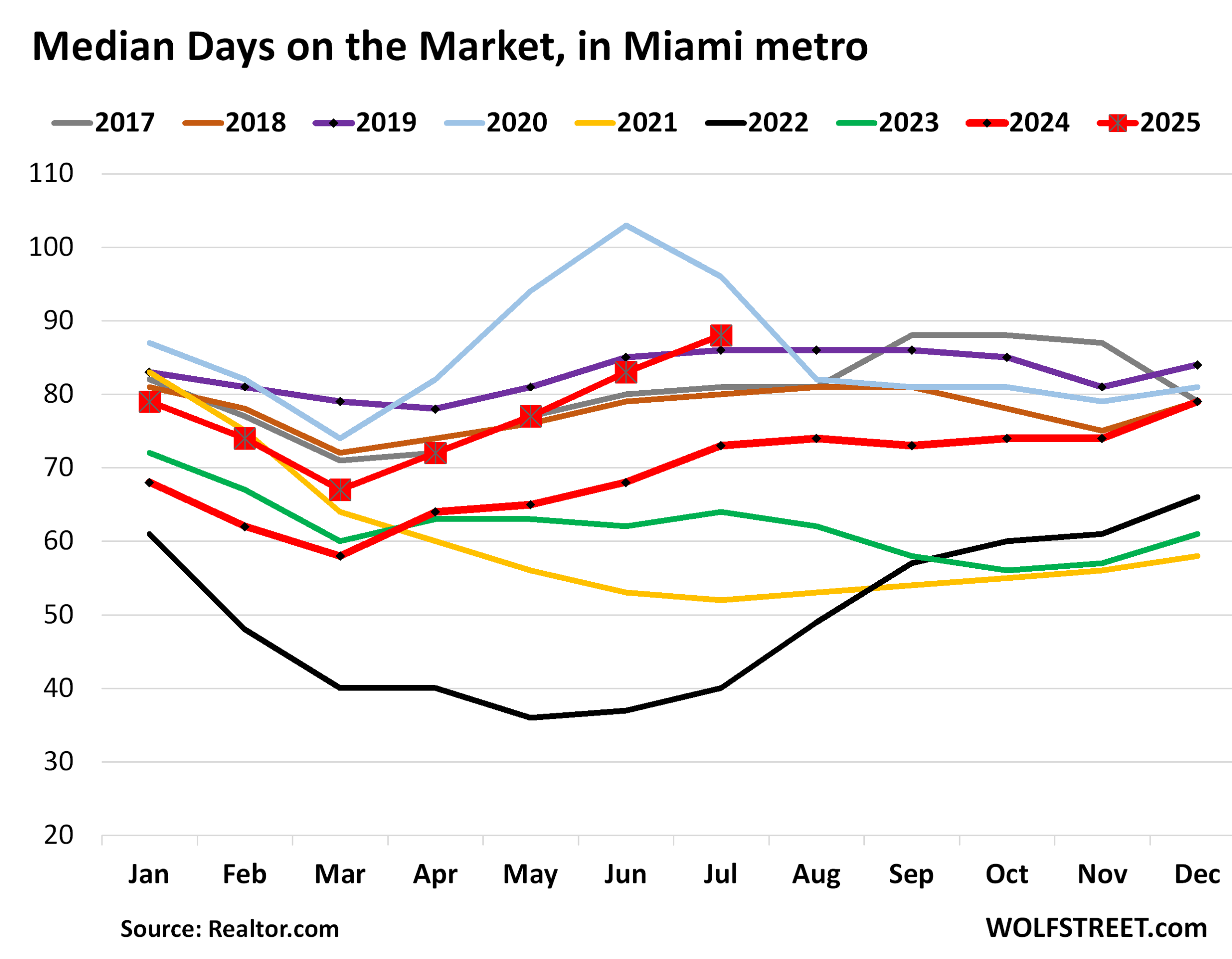

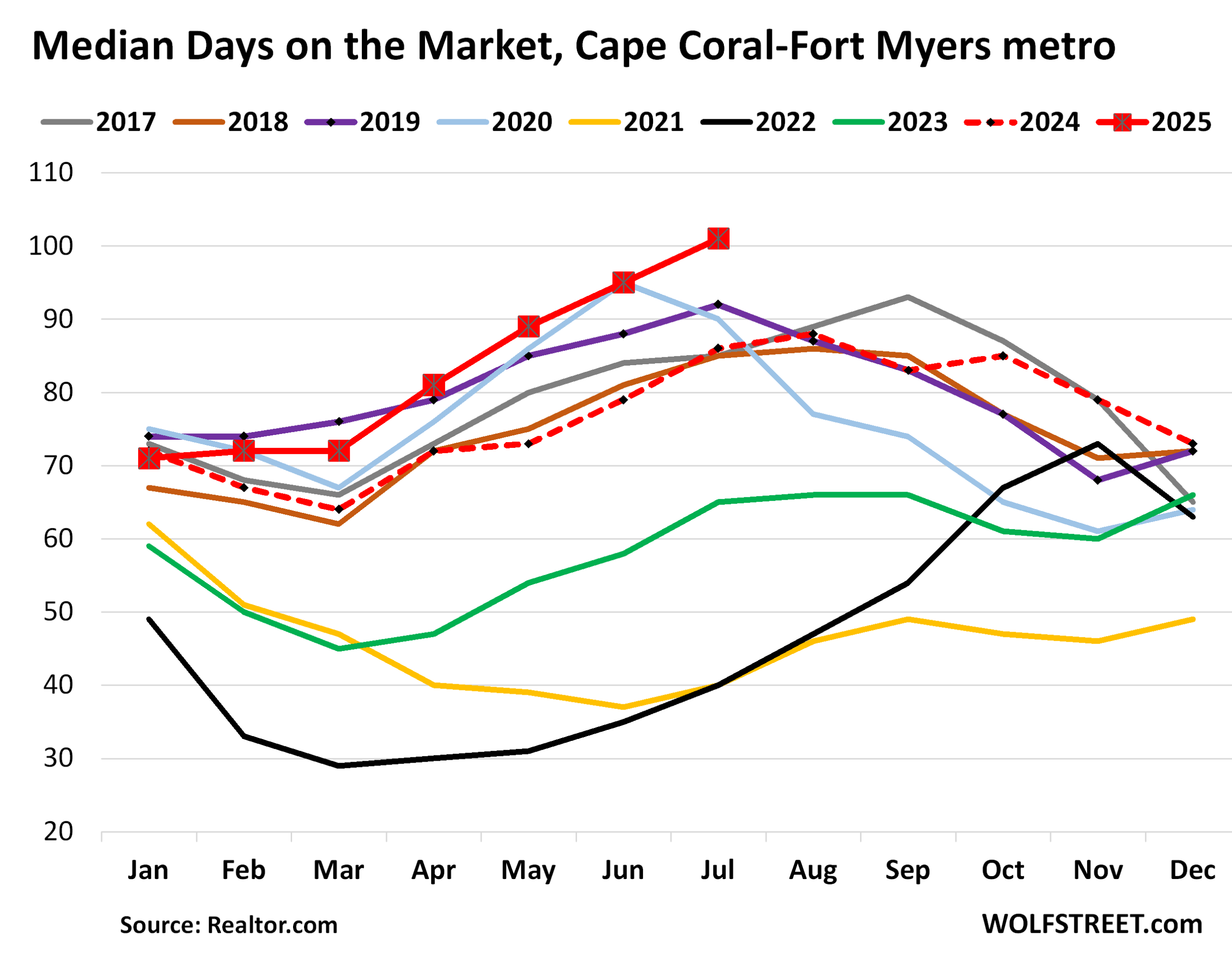

The number of days that homes sit on the market before they get delisted or sold is blowing out in the biggest metros in Florida. The Cape Coral-Fort Myers metro hit it out of the ballpark with a new high for at least the last decade of 101 days. In the Miami-Fort Lauderdale-West Palm Beach metro, despite being the market in the US with the highest ratio of delistings, time on the market jumped to 88 days.

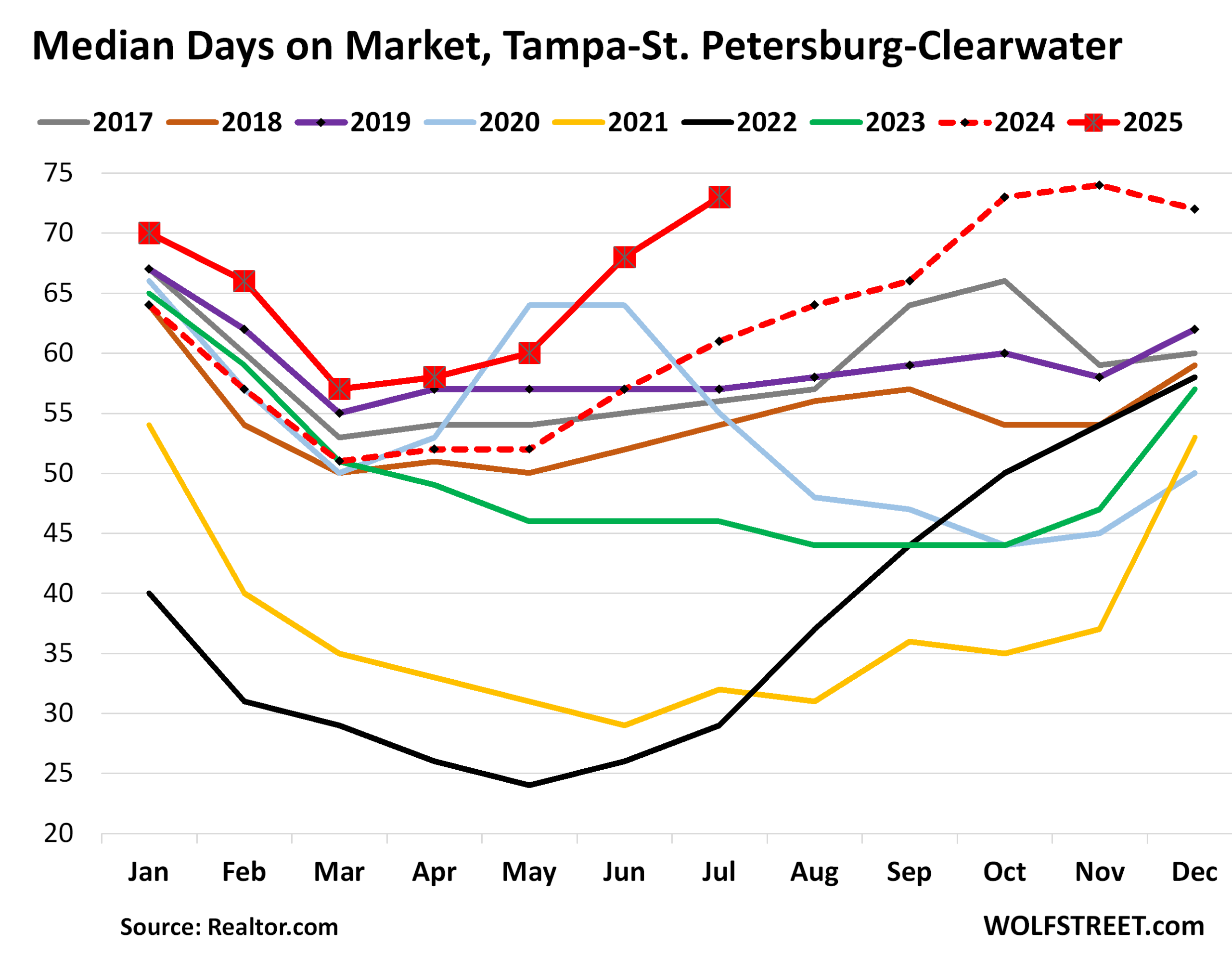

In the Tampa-Saint Petersburg-Clearwater metro, the median number of days homes sat on the market before they got pulled off the market or before they sold spiked to 73 days, the highest for any July in the data from Realtor.com, whose data go back to 2016. In July 2024, it was 61 days, in July 2019, it was 57 days.

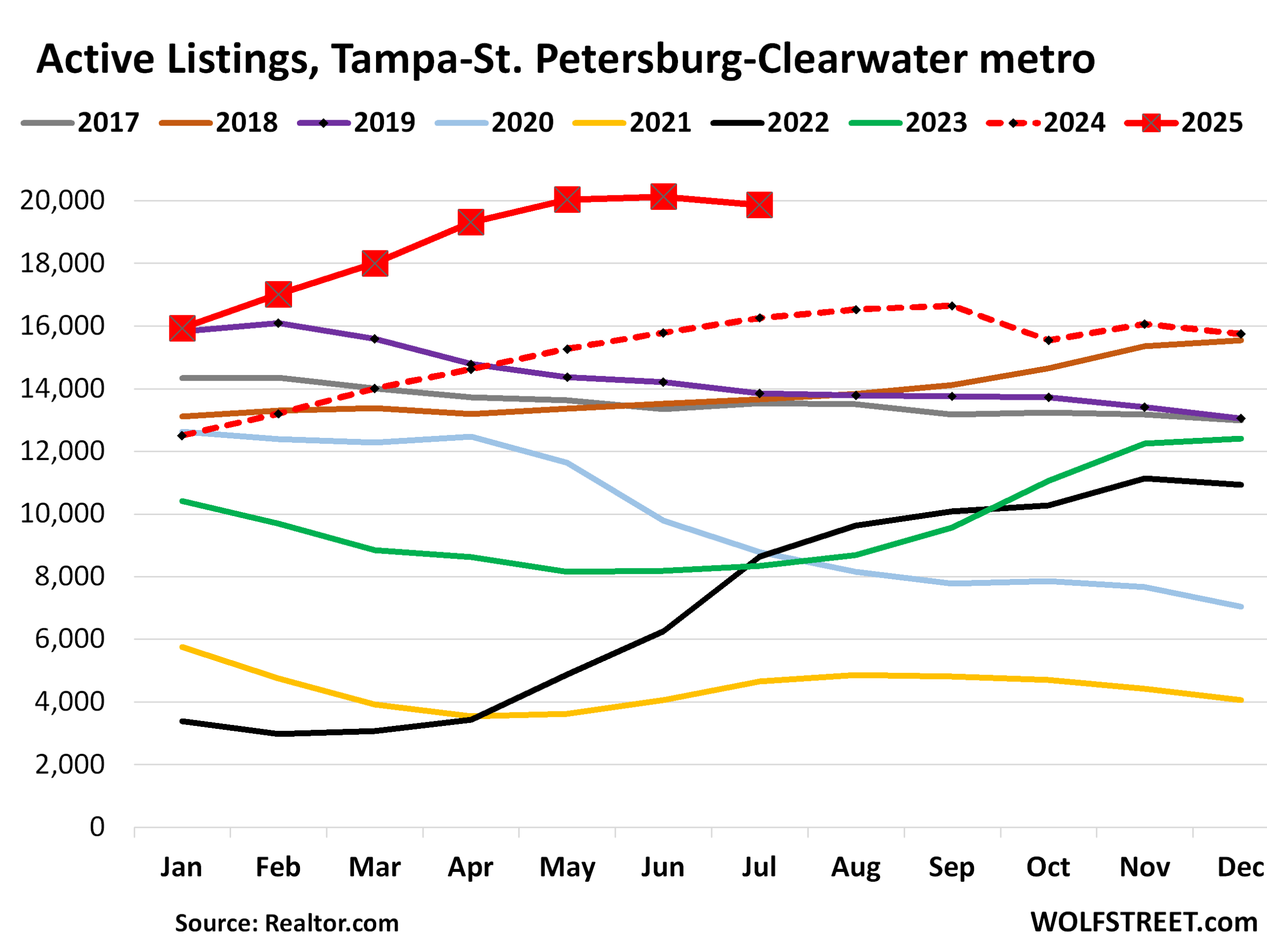

Active listings in the Tampa-Saint Petersburg-Clearwater metro jumped by 22% year-over-year in July to 19,862 homes for sale. Compared to 2019, listings were up by 43%. The listings over the past six months all have been the highest in the data going back to 2016. As days on the market indicate, these are big inventories at a time when sales have plunged.

In the Miami-Fort Lauderdale-West Palm Beach metro, median days on the market before the homes were delisted or sold jumped to 88 days, up from 73 days a year ago, and up from 86 days in 2019, and the highest for any July in the past decade except July 2020, during the pandemic.

And it would have been a lot higher if sellers hadn’t delisted their properties on a massive scale: For each 100 new listings, sellers pulled 59 listings off the market, the highest ratio of delistings to new listings in the US, and more than double compared to a month earlier, according to Realtor.com.

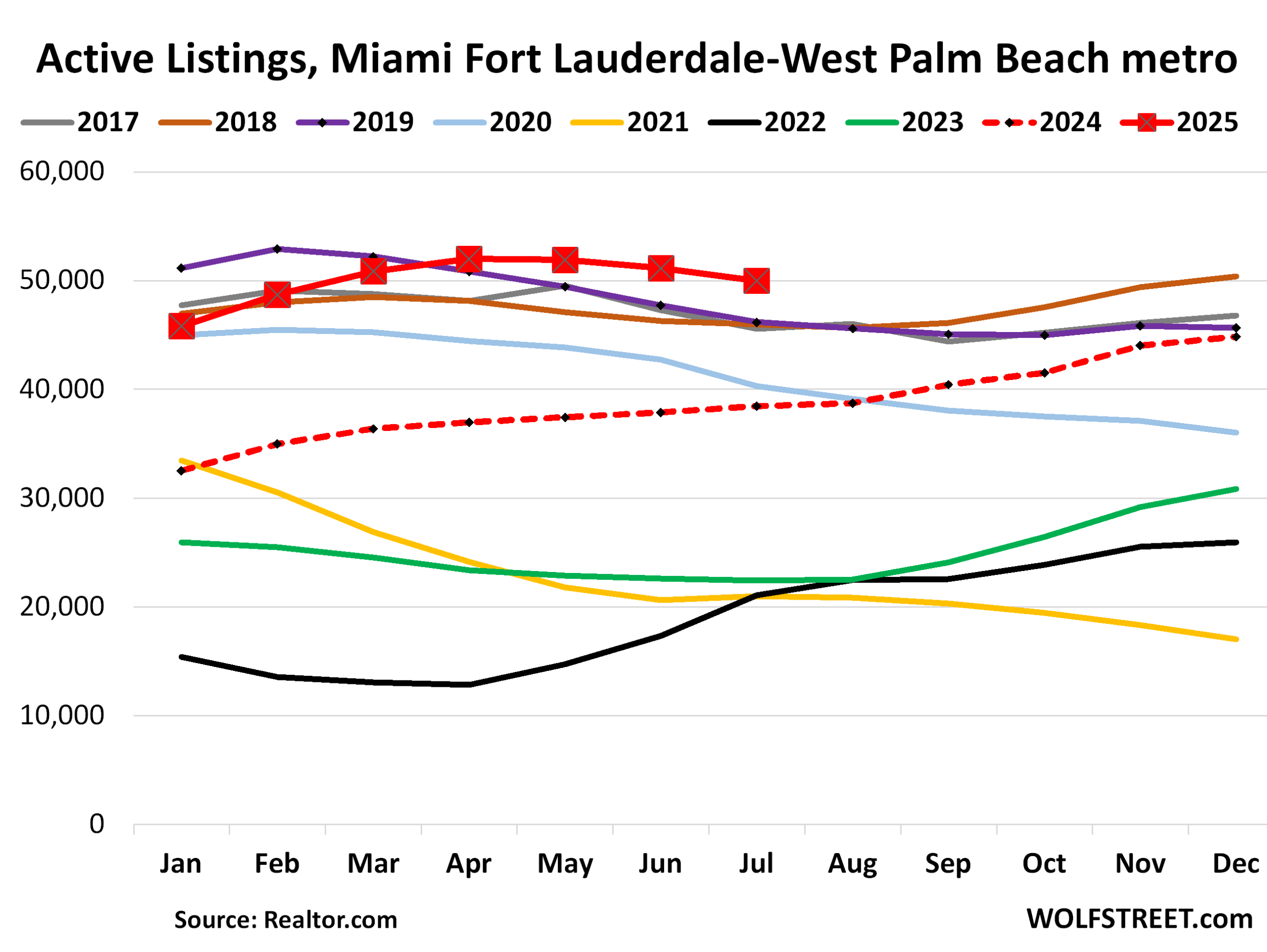

Active listings in the Miami metro jumped by 30% year-over-year to 49,980 homes, the highest July in the data from Realtor.com, which goes back to 2016.

The runners-up were the Julys of 2017-2019, in the range of 45,500 to 46,200.

In the Cape Coral-Fort Myers metro, days on the market spike to 101 days, up from 86 days a year ago, the highest in the decade of data from Realtor.com.

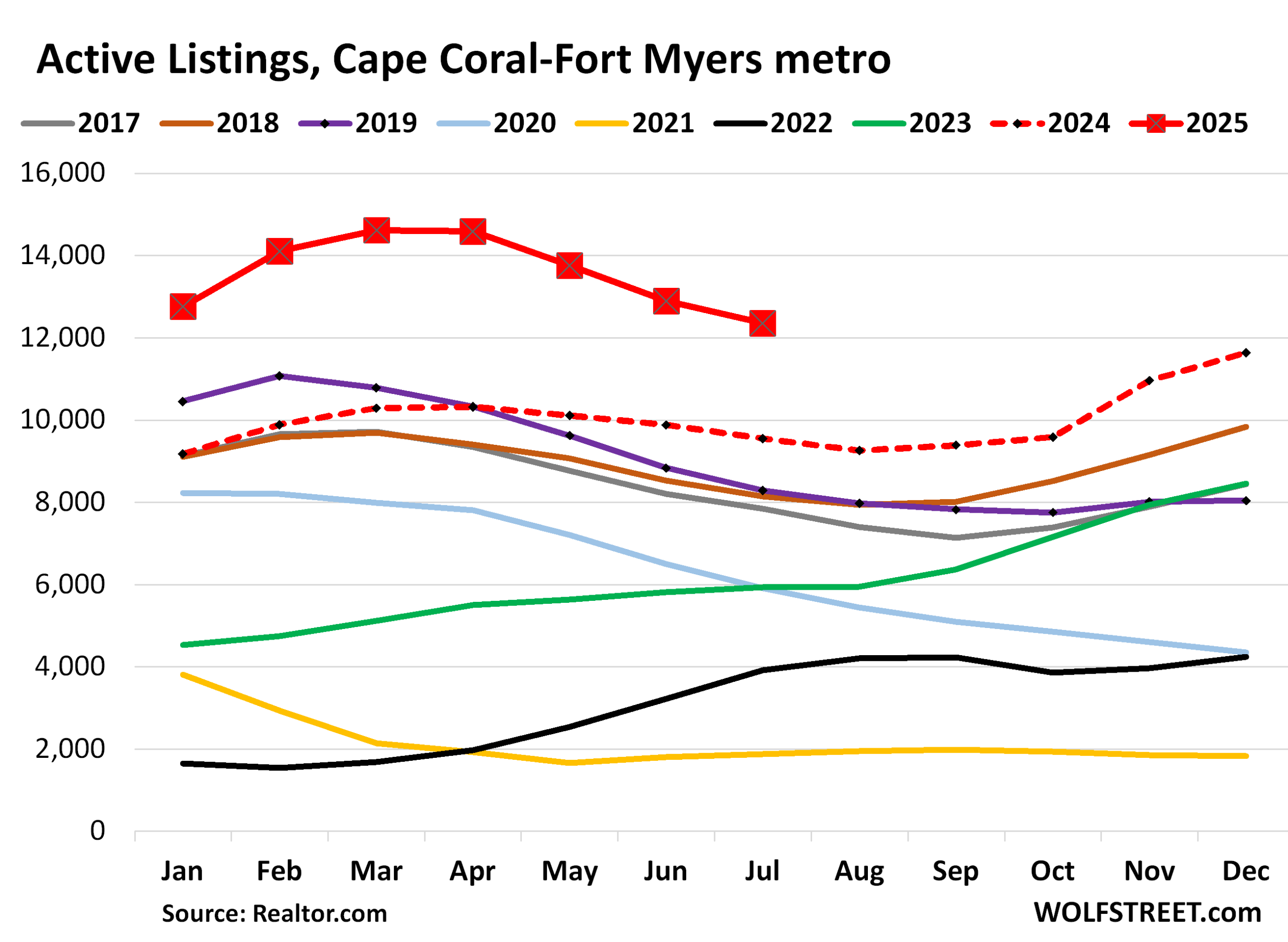

Active listings jumped by 29% year-over-year, and by 49% from 2019, to 12,353 homes. The entire year, listings have been the highest in the decade of data.

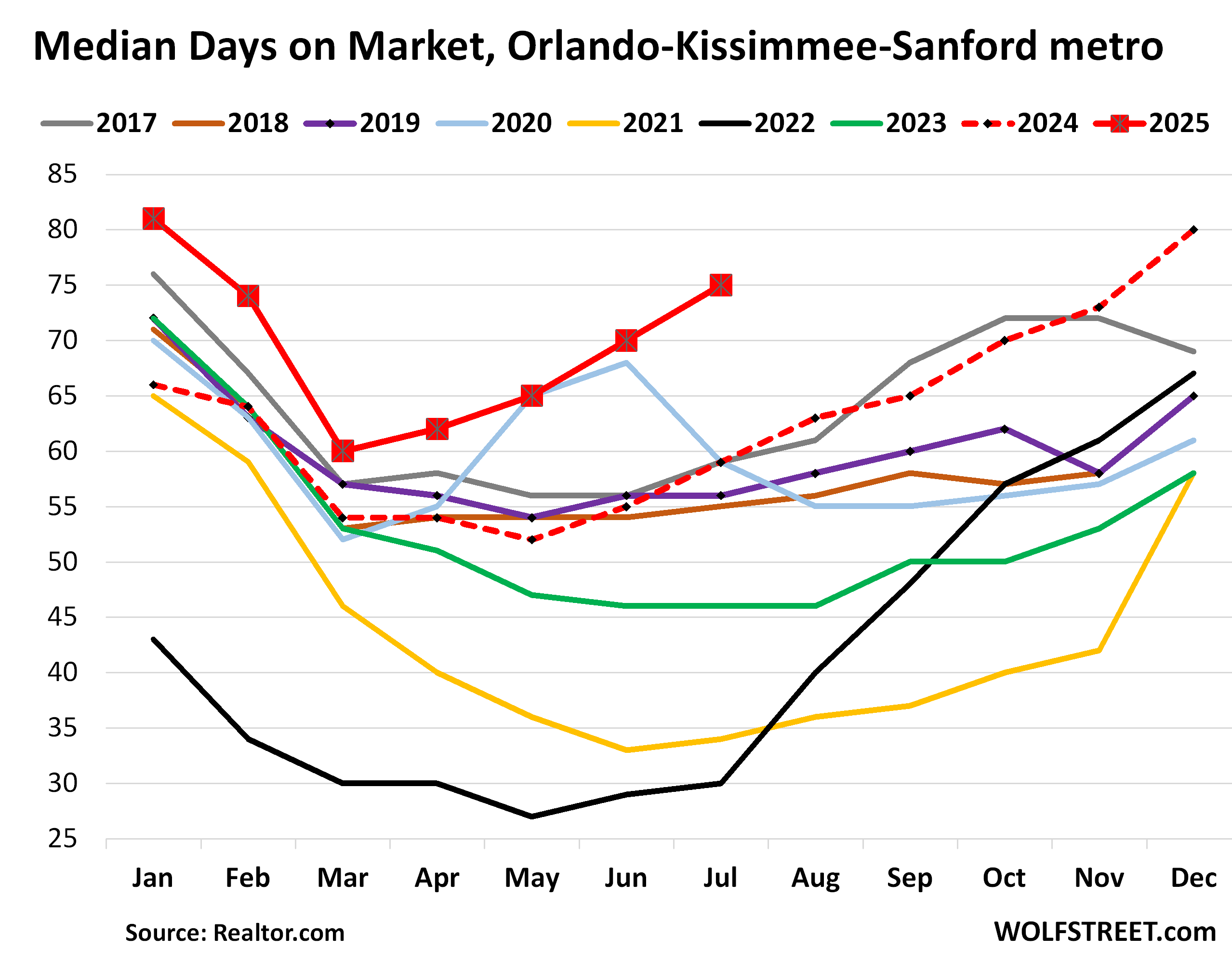

In the Orlando-Kissimmee-Sanford metro, days on the market spiked to 75 days in July, up from 59 days a year ago and up from 56 days in July 2019. There is a distinct seasonality in this market, with the spring being the trough, and January being the high point, which is still six months away:

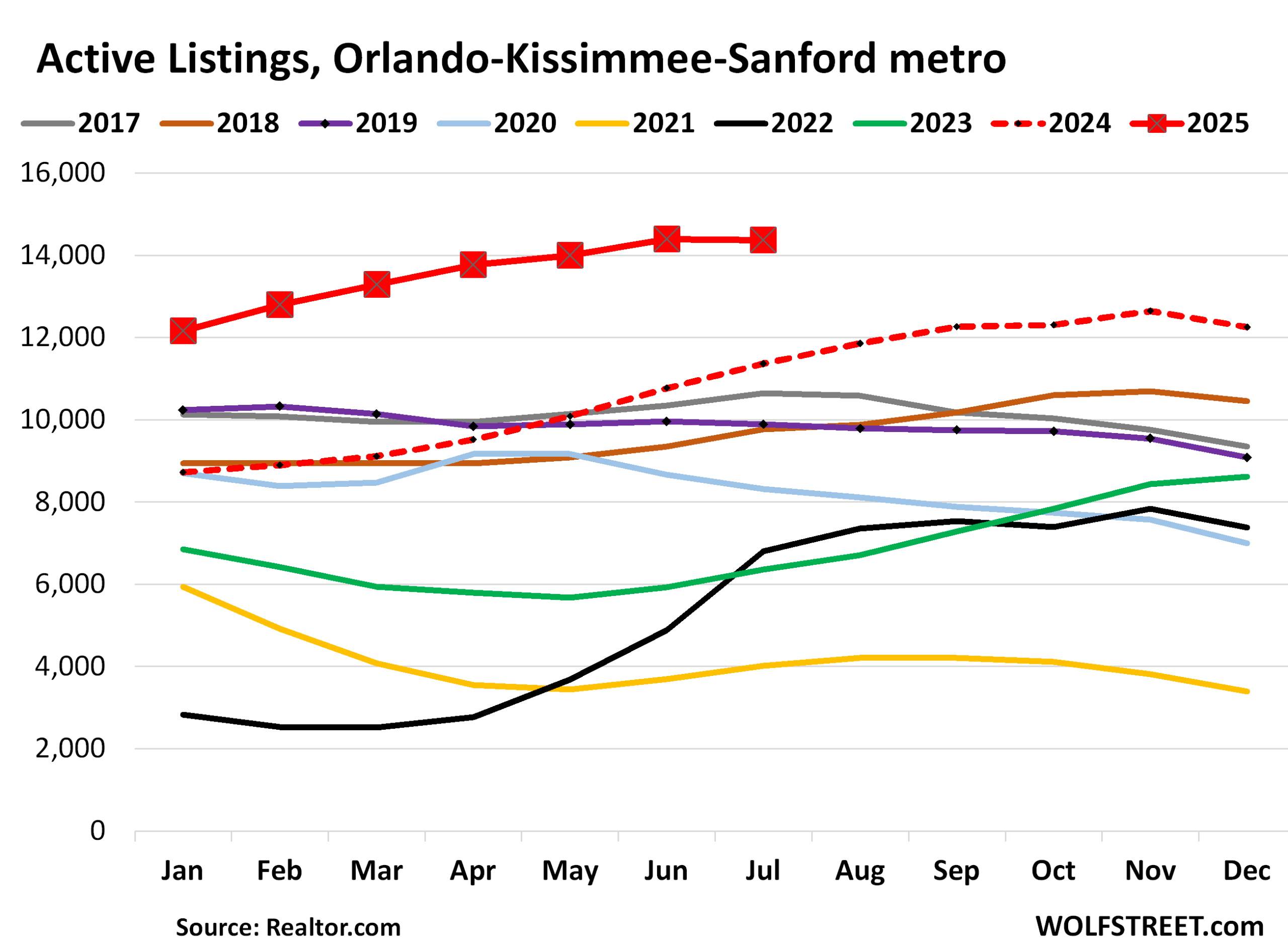

Active listings jumped by 26% year-over-year and by 45% since July 2019, to 14,364 homes. Over the six months, listings have been the highest in the decade of data.

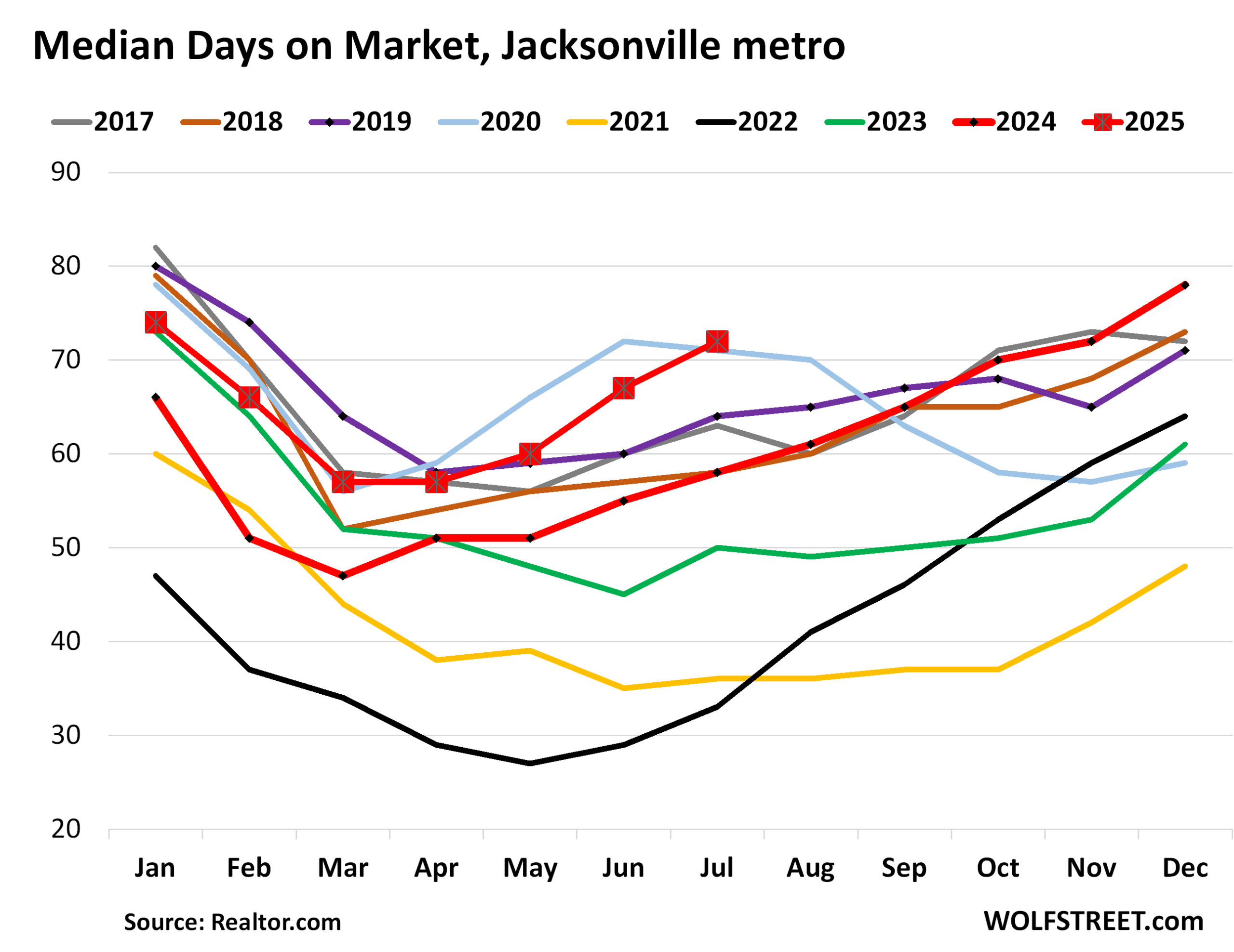

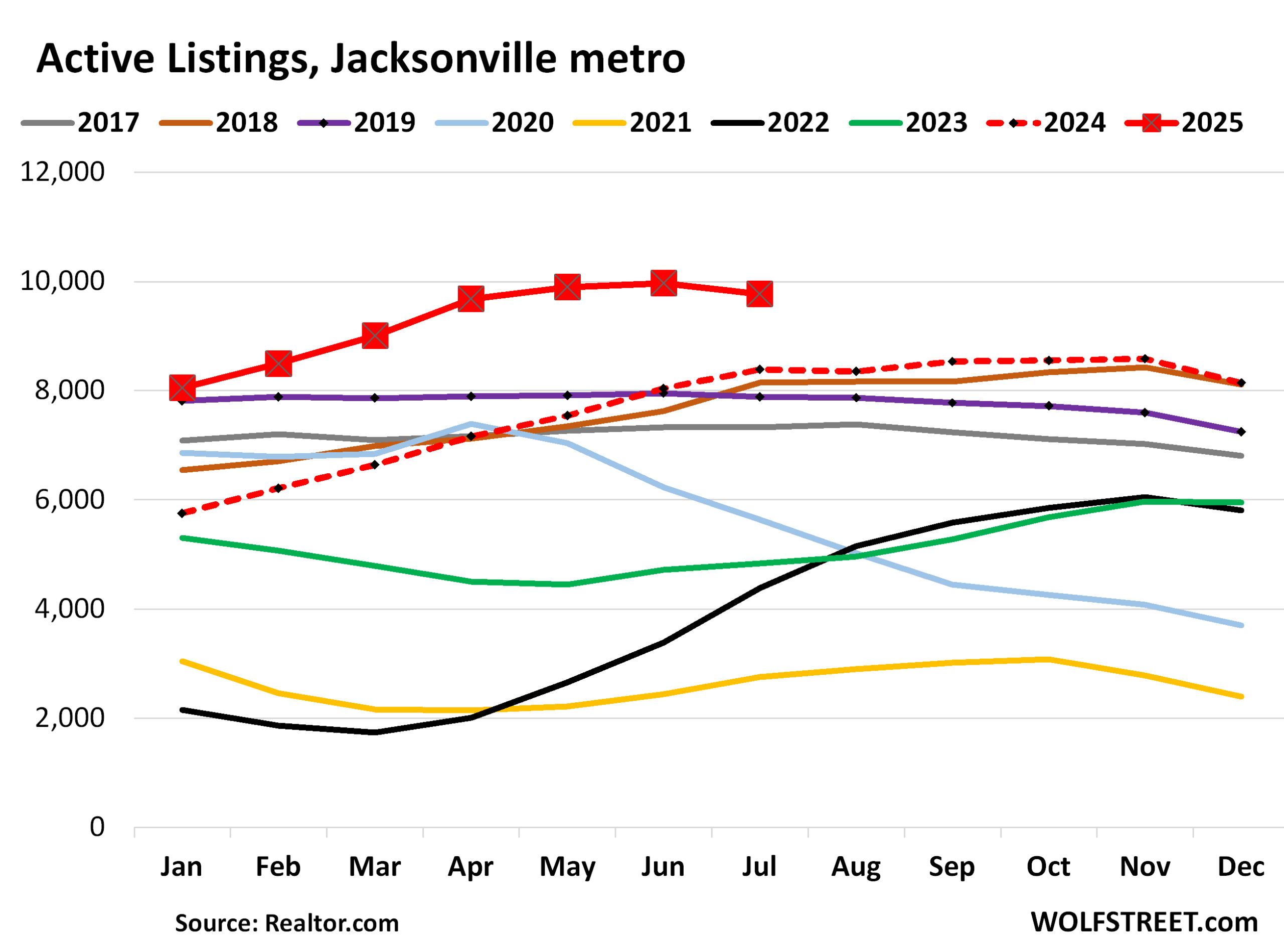

In the Jacksonville metro, days on the market jumped to 72 days, the highest for any July in the decade of data, up from 58 days a year ago and from 54 days in 2019.

Active listings jumped by 16% year-over-year, and by 24% from July 2019, to 9,767 homes. The past five months were the highest in the decade of data from Realtor.com.

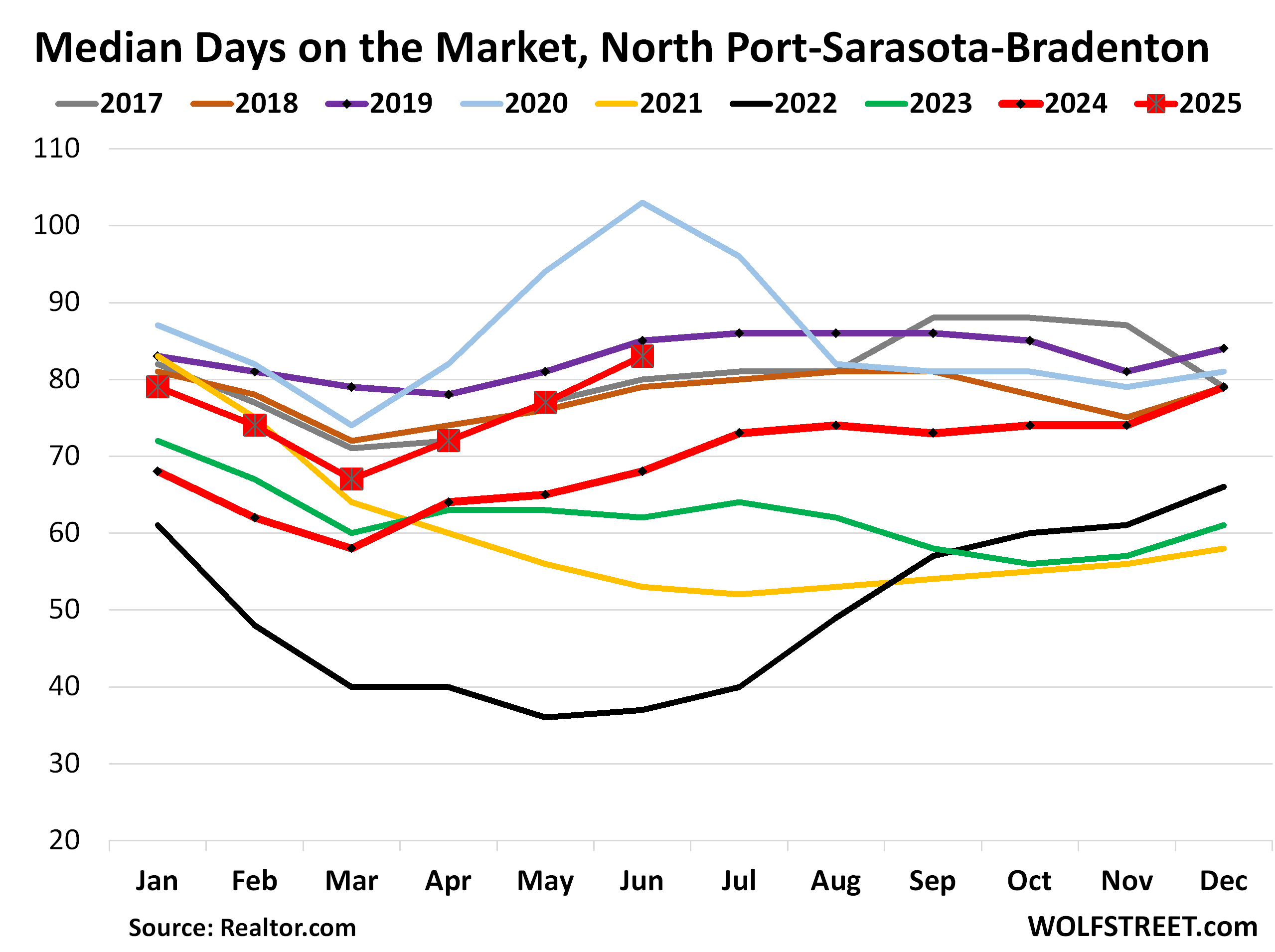

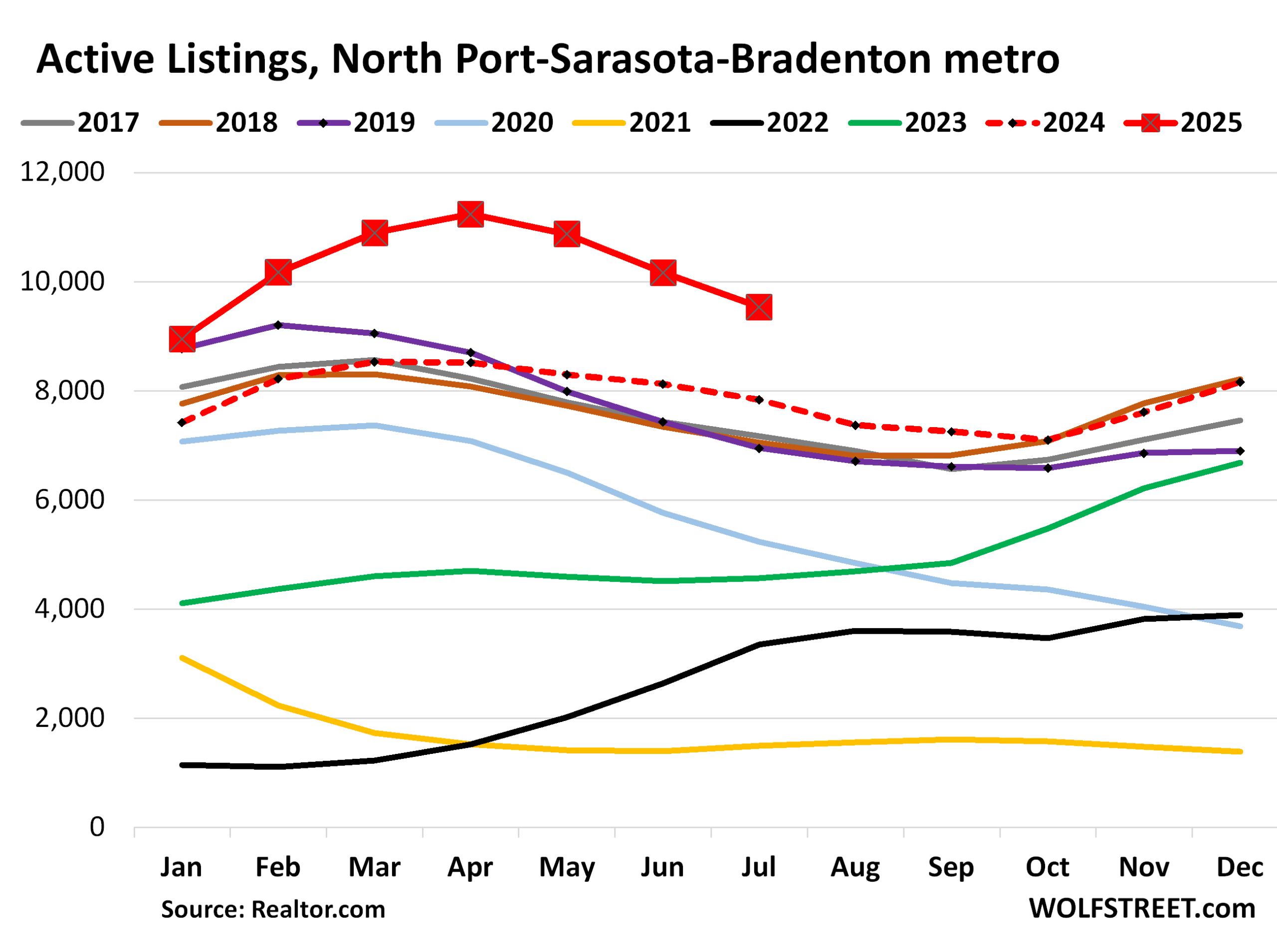

In the North Port-Sarasota-Bradenton metro, time on the market before homes were delisted or sold rose to 83 days, up from 68 days a year ago, but still before July 2019 (85 days) and July 2020 (103 days).

Active listings rose by 22% year-over-year and by 37% from 2019 to 9,533 homes. The past six months have been the highest in the decade of data.

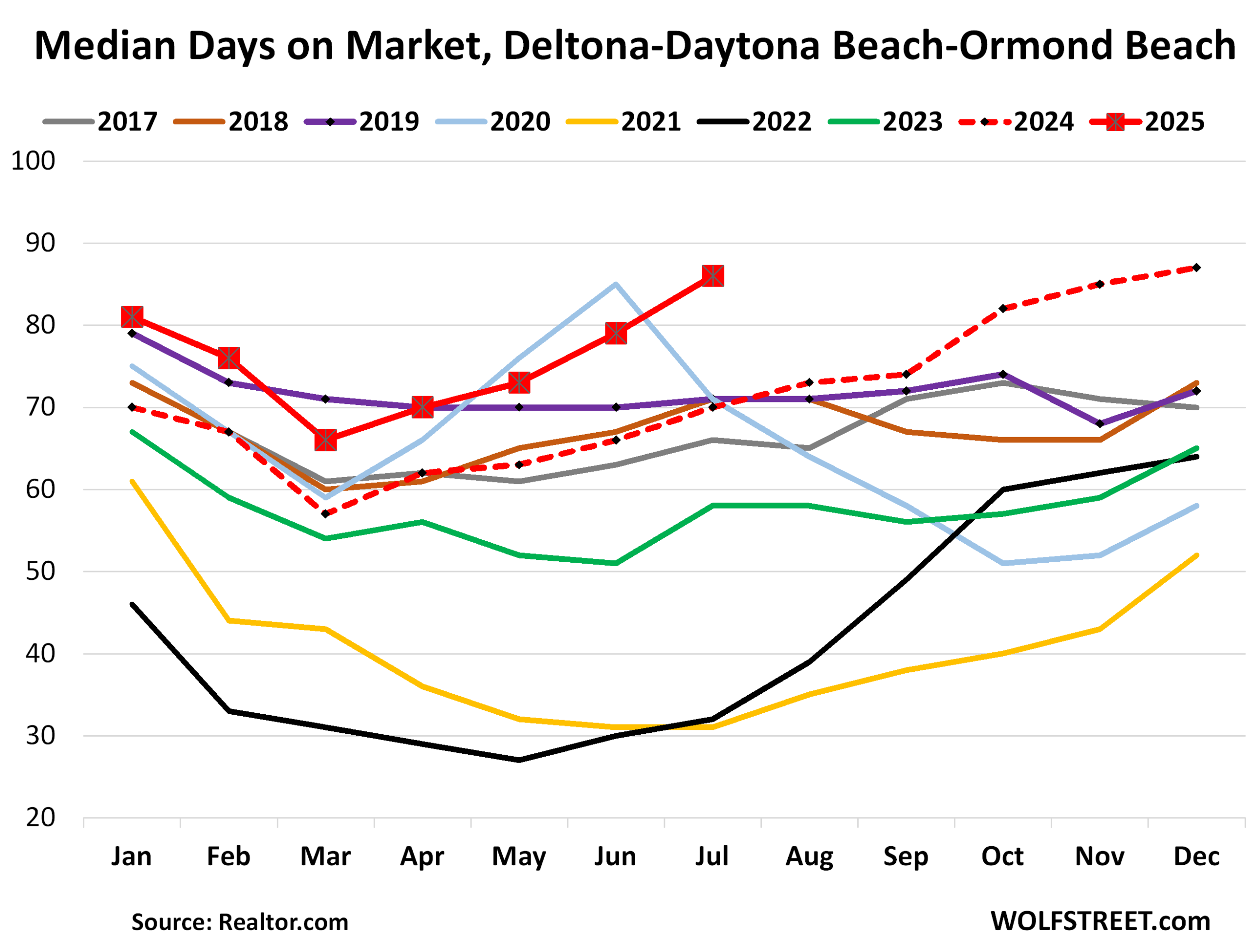

In the Deltona-Daytona Beach-Ormond Beach metro, median days on the market jumped to 86 days, by far the highest July in the data, up from 70 days a year ago, and up from 71 days in July 2019.

Active listings rose by 20% year-over-year, and by 38% from 2019, to 6,868 homes. Listings over the past six months were the highest in the decade of data.

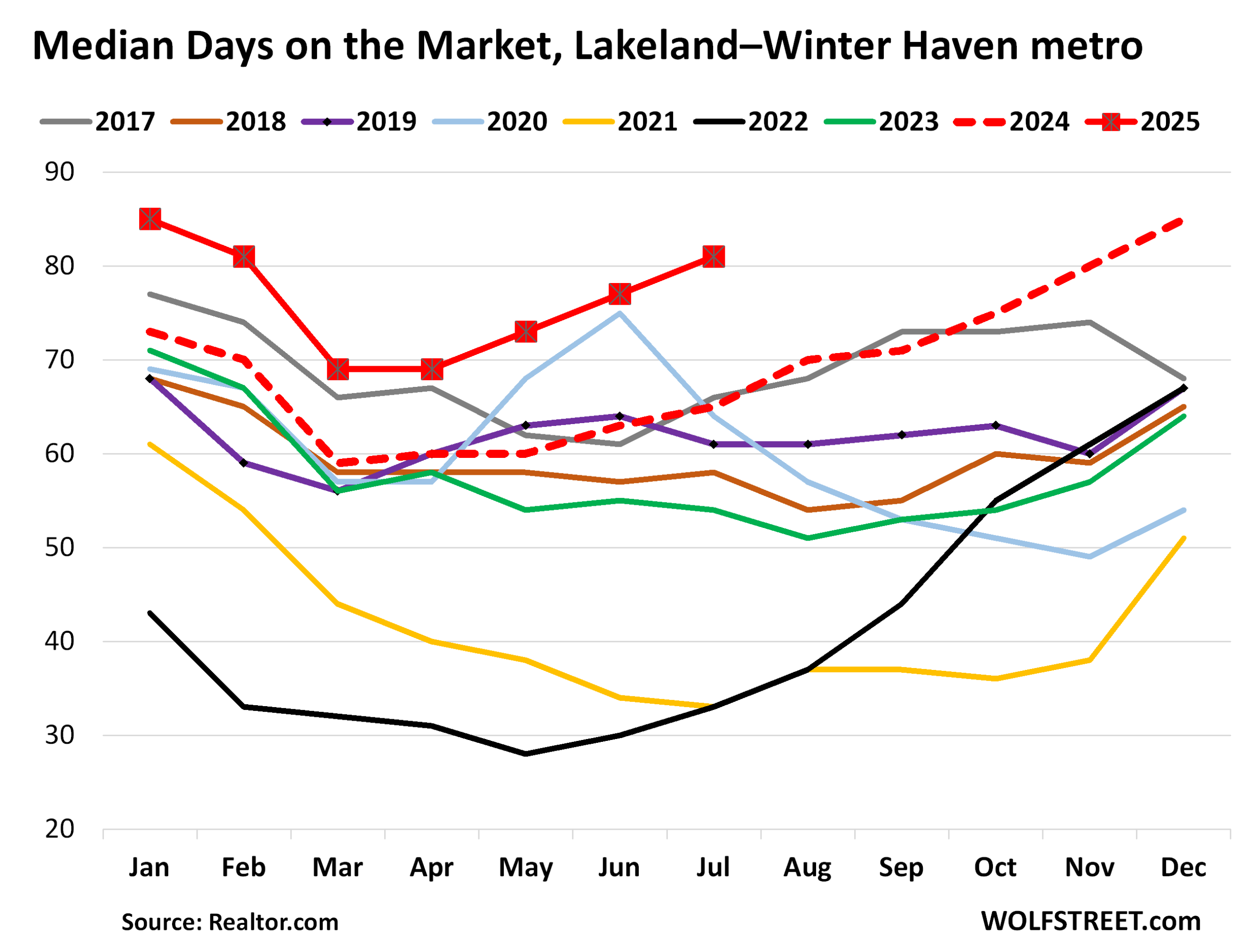

In the Lakeland-Winter Haven metro, days on the market jumped to 81 days, from 65 days in July 2024, and from 61 days in July 2019:

Active listings had already been soaring in 2024 beyond anything over the past decade of data, and all of 2025 has been even higher than 2024. In July, active listings rose by 14% from July 2024, by 80% from July 2019, and by 105% from July 2017, to 5,057 homes.

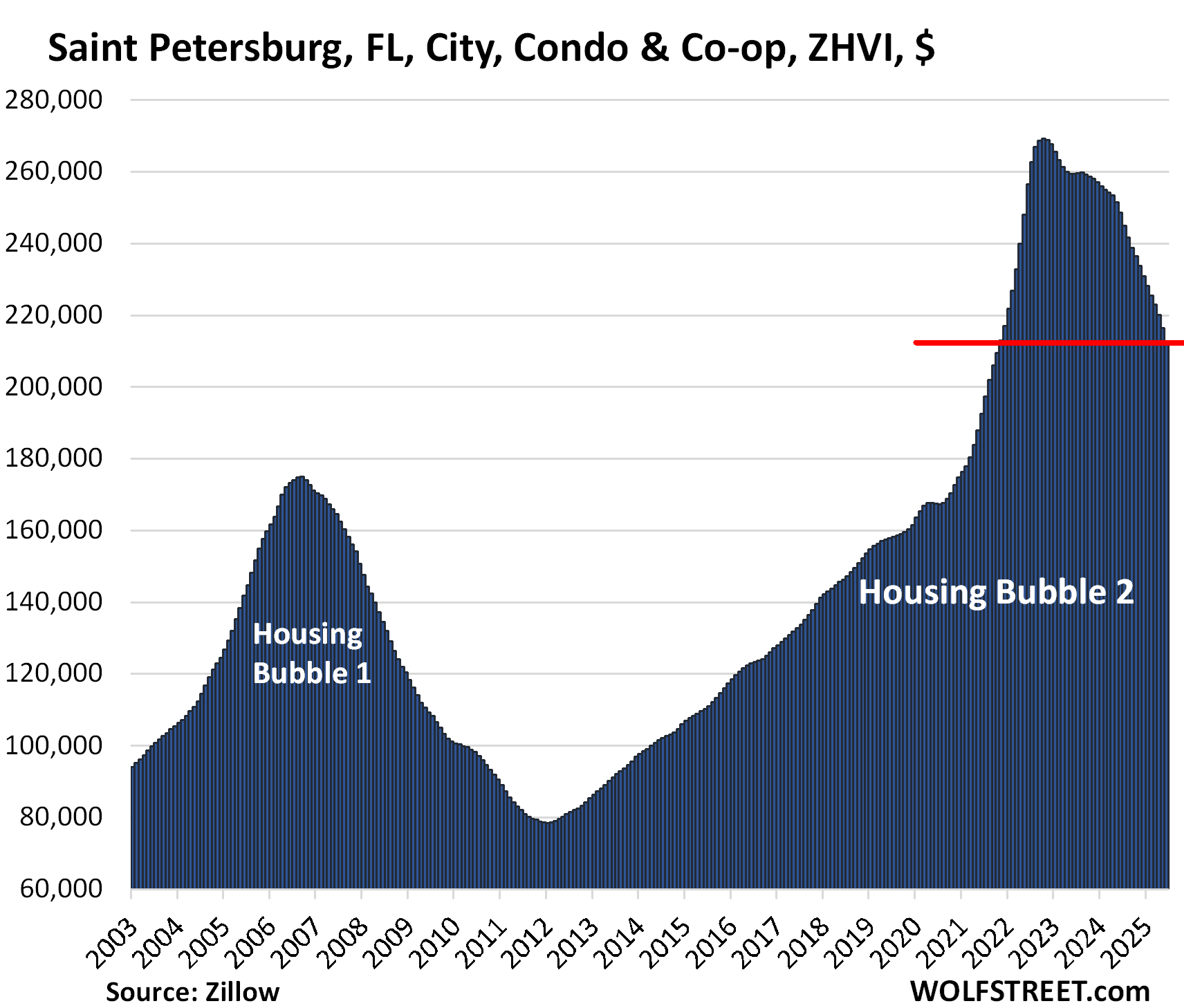

Prices have been skidding downhill in the major Florida markets, particularly condo prices, for example in St. Petersburg (-21%), Fort Meyers (-17%), Sarasota (-17%), Jacksonville (-14%), Tampa (-13%), and Naples (-13%). They’re part of the 19 bigger condo markets in the US with price declines of 12-23%, discussed here.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

As Wolf says low prices solve any sales problems. So lower prices.

Big 100 billion 4 week note sale today. Could be interesting for mortgage rates.

Mortgage rates flex with the 10 year Treasury not the 4-week.

From marketwatch:

The government is about to take a step on Thursday that it has never taken before to meet its financing needs, by using a single auction to sell a record $100 billion of Treasury bills that mature in four weeks.

While observers expect this sale to go smoothly, a continued reliance on short-term bill auctions is not without risk. The issue is that such auctions might eventually expose the government to sharply higher financing costs for any number of uncontrollable reasons. Thursday’s $100 billion sale represents an increase of $5 billion from last week’s $95 billion auction of similar bills.

Off quote;

Quite possibly when the treasury starts having trouble selling all the debt me thinks long term rates may go up thereby affecting mortgage rates. First news on results of this auction say demand was soft.

I think we’ve already gotten hints about what’s going to happen with those 4-week bills. At some point just to maintain “ample/adequate” reserves in the banking system the Fed is going to start increasing the size of the balance sheet again – and it could likely be short term TBills. Let’s say the Fed continues the $15-20B per month MBS rolloff, but adds $20-30B of treasuries. Not really QE, just normal operations…

Now on the other hand I’m really wondering who exactly buys the 30-year. Pensions, insurance companies..the Fed..but boy that’s a long time to lock in.

Ol’B

The Fed will start replacing maturing long-term Treasuries with T-bills long before QT ends. They’re ready to do that, they’ve been talking about it. Waller and Warsh, who might become the next chair, have been talking about it too. But there are currently not enough T-bills out there to do that in any significant way, given the Fed’s huge figures. So the Treasury is increasing T-bill supply so that the Fed can rotate out of long-term Treasuries into T-bills. And they might sell MBS to speed up QT. Waller mentioned that too. The Fed will shift a big part of its portfolio to T-bills to replace a big part of the long-term bonds.

Short rates didn’t budge but long rates are up due to weak demand for 30-year auction. Nothing to do with 4-week bills.

Good to be worried about skittish market pushing up long rates, but I think weakening labor market may override that?

4 week bill is up, those issued 7/22 yielded 4.23

Those issues the last two weeks 4.30

https://www.treasurydirect.gov/auctions/results/

Also they only yielded about 4% during tariff market fear in april.

The writing is on the wall in the land of the flying cockroach and hurricanes. It’s now smarter to be a renter than a buyer with a 7% interest rate and escalating insurance premiums. The next round of government QE and subsidized housing may happen under Trump just be patient and don’t cut your throat to blow your nose. Men only need a place to Shit, Shave, and Shower. Real estate $FOMO fever is on a 3 year decline, the pot of goal at the end of the rainbow has quickly turned to shit.

If you are a renter, then all of those costs are included in your rental payment each month. They’re not paid for by a magic fairy.

Rents are determined by what tenants are willing to pay, not by what the landlord wants, which is why so many recently purchased rental properties have steeply negative cashflows, and which is why the multifamily CRE sector is in deep trouble with lots of defaults and landlords walking away from their buildings, because landlords cannot get the rents they need to cover their expenses. If they hike the rent, tenants leave, and new tenants don’t materialize, and the unit sits empty and drains the lifeblood out of the landlord.

Yep. There’s so many potential sellers who say “If I don’t get my price (which is double 2019 pricing), then I’ll just rent it out.”

Good luck to them.

Costs must be passed on if a landlord wants to maintain cash flow and get a consistent return. That is not happening today. Landlords are accepting cap rates well below treasury bill and bond rates. Some are sitting on significant price appreciation and therefore don’t care about cash flow. They are consciously or unconsciously accepting low operating returns in hope of continued home price appreciation.

In the mind of a landlord, maybe rent levels are tied more to past performance and faulty impressions of home price appreciation than actual costs. Note, large firms that know what they are doing are selling out. It’s the Ma and Pa landlords that believe in miracles and realtor hype, which probably helps to keep rents low.

Plus, many landlords are sitting on low rate mortgages. Landlords that don’t have that benefit can’t compete and won’t be able to pass on their mortgage interest costs.

As I’ve written here before, there is no geography I can identify where newly purchased rentals “pencil out.” Even assuming you’re in the highest tax bracket and your rental income (unlike your T-bills) is untaxed.

There is however the move up 1031 exchange where even though the yield is low, you’re collecting a lot more net rents via the exchange and your stepped up value so it could make sense in certain situations. But generally, I’d rather buy other things right now than rental real estate. Still looking for some decent 1031’s if they exist!

You probably think tariffs cause inflation too. You need to get a clue.

Loose shoes, tight _____, and a warm place to shlt. That’s all men need, and the middle one not so much any more (too much baggage).

I would settle for a warm _____ at this rate my wife left me and I am thinking of trying the AI girlfriends

Realistic sexbots will put most women out of business. Women will still be needed to develop a fetus, but I imagine that will go the way of the horse and buggy too.

Wolf. I really hope that the government does not view this as a problem; and then try to solve it. They will. Make it worse. Low rates will make it worse. We need to let the market clear. We need housing all across the country to drop 40%. Let the chips fall. Then younger people and middle class people may. E able to buy. Let the market work.Agree?

Maybe the Fed can come in and buy some MBSs and drive long rates down? /s

FL is one hurricane away from being uninsurable….IMO.

The FDIC can lower its deposit guarantee, $250,000 per depositor, per insured bank, for each account ownership category, back to 100,000. That will increase the supply of loan funds, but not the supply of new money. It will lower long-term interest rates. And it will not reduce the size of the commercial banking system or bank credit.

The “Taper Tantrum” is prima facie evidence, where transaction’s deposit insurance was reduced from unlimited.

The shifts might not work out that way. If they lower the limit to $100k:

Either, you will see some of those suddenly uninsured fund balances of $150k-$250k (I don’t know how much that would amount to in total) shift to money market funds and T-bills.

Or, you will see that depositors will rely on the now (since SVB) effective implicit guarantee by the government of ALL balances at any bank that isn’t minuscule, and not move their money at those larger banks at all. And any remaining larger deposits at small banks will shift to regional or larger banks that might qualify for the implicit guarantee of all account balances.

The depositor bailouts of 2023 stabbed the policy implications of deposit insurance in the back.

The deceleration in LSAPs drastically increased the real rate of interest, the exchange value of the U.S. dollar, and decreased the rate of inflation. All of this was due to the increase in the supply of loan funds, vs. increase in supply of new money.

My bank farms out any amount over $250,000 to other banks, but keeps paying me the same rate as if all my money was in my bank. It’s called IntraFi Network Deposits DDA-MMDA Deposit Placement. You have to sign up for it. In any case, we saw with Silicon Valley Bank that the FDIC can declare an emergency and bail out ALL depositors, as they did.

U.S. Treasury Bills, Bonds, or Notes*

*These investments are not insured by the FDIC, but they are backed by the full faith and credit of the U.S. government.

Money would then flow THROUGH the nonbanks.

Im familiar with the industry. Everyone is well positioned for this storm season. Rates have finally become adequate and many homeowners are seeing decreases in their rates due to increased competition. The talking points of Florida’s insurance industry in distress are 2 years outdated.

Not Wolf, but this ancient RE/construction guy who’s been in it w dad and grandad for eva totally agrees country.

About damn time the folx in DC and even various state capitols STOP already with the manipulation of markets and let the chips and houses and cars fall where they do.

Actually quite shameful that SO many hard working folx cannot afford to buy a home these days, and it’s apparent the demographics are showing us that quite clearly.

I’m of the opinion that the only way this works out is through a massive amount of new housing construction. I’m surprised that at these prices it isn’t exploding everywhere, and I live in Florida. One of the changes I’ve noticed in the last couple of decades is the lack of individual lots for building. In my younger days, developers would buy huge swathes of land, throw in roads and utilities and sell the individual lots for significant profit. Nowadays, the developer won’ sell the lot individually. You have to buy one of the 5 models they have designed and let them build at a massive markup. The result is to keep prices high and competition low.

100% agree. We have a pricing problem, not an interest rate problem. Lower rates drive demand up which drives prices up. High prices were the result of low rates. Most government intervention increases demand, not supply.

That 40% drop could very well be in the form of flat prices for a decade while inflation compounds at 3%. People pulling listings means they don’t have to sell and they’ll wait until next year or so to try again. Anyone who HAS to sell lowers the price repeatedly until they do, or they foreclose and walk away. Right now there seems to be a lot of “testing the waters”.

But the prices are trending lower event with historically very low un employment rate and strong economy.

Think what would happen when and if recession hits which would come for sure unless the business cycle has been upended by Govt manipulation.

My friends who are deeply invested in real estate think that either prices stay stagnant or it would go higher. Prices going down is not the situation they have in their book.

How about a different government solution: if a house is unoccupied for a year or 2, the city can buy it (eminent domain) at last appraised value and use it in an affordable housing program, etc. I’m not serious, but wouldn’t that light a fire under those stockpiling houses as investments!

No gov solutions that’s what led to this stupidity even if some of us had massive windfalls.

I’m just sad we can sell our last property as a family member needs it. Would have been a 9 or 10x. Not the most money wise but I would have framed it just for keepsake.

Better idea. If a house is not owner-occupied, tax it like a commercial property, as that’s effectively what it is. You’re either using it for commercial purposes (renting it out) or you are leaving it empty, holding it as an “investment.” No reason they shouldn’t bear higher property taxes.

Utah very deceptively labels long-term rentals as “primary occupancy” on its property tax statements, with a 45% exemption reduction. In tourist towns, these are claimed “primary occupancy” and rented as short-term rentals. The state is also not transparent in public records of sales prices, so county assessors are guessing at a value.

Theocratic corruption runs deep and distorts real estate markets.

One primary residence tax free. Kind of like a homestead so Americans can actually realize true ownership. As long as the government can tax your primary residence you never really own it. Vacation homes taxed at a slightly higher rate. Rentals should be taxed at a higher commercial rate.

Minnesota does that. Property tax rates are different depending on either homestead or non homestead classification.

To have a homestead property:

You must own the property.

You must occupy the property as your sole or primary residence.

You must be a Minnesota resident.

(Many Minnesotans have their legal residency in Florida as Florida has no state income tax; versus a 9.85% top rate for Minnesota.)

“The homestead classification in Minnesota significantly impacts property taxes through the reduction in assessed value that directly influences the tax bill. Homesteaded properties are assessed at lower rates compared to non-homesteaded properties. This reduced assessment translates into lower property taxes, creating a tangible financial benefit. The logic behind this preferential treatment is to ease the financial burden on those using their property as a primary residence, encouraging homeownership and community stability.”

“Beyond tax reductions, homestead status provides legal protections against creditors. Minnesota Statutes, section 510.01-510.02, exempts homesteaded properties from certain types of debt collection, safeguarding the homeowner’s residence from being forcibly sold to satisfy debts. This protection extends up to a value of $450,000 for most properties and $1,125,000 for agricultural homesteads. The exemption ensures residents have stability in their home ownership, even amidst financial challenges.”

On that note, I dropped a check off at the Post yesterday for the second half of 2025; ‘Hennepin County Treasurer’ (due by 15 October). Free and clear until 2026!

Off topic:

For months I (& Mr. Market) thought the FED wouldn’t cut rates but currently these 2 persons have changed their mind. Mr. Market now predicts a rate cut of 0.50% or (more likely right now) 0.25%.

Not sure who your “Mr. Market” is but the 3-month bill says no cuts at the next two meetings.

Doesn’t matter who Mr or Ms market is, because the entire ”financial” world has become both irrational and clearly the whimsy/manipulations of paid political puppets.

To think or especially to ACT otherwise these days is to at least invite, if not certify, allegations of incompetence.

Certainly I, and I suspect many ”rational” folx would hope otherwise, and maybe, at some point in time,,, WE, the rational investors WE, will be confirmed…

But, please don’t rely on any such thing happening soon…

Who cares. Fed cut rates by 100 points last year and mortgage rates went up. Powell got caught with his pants down and can only sit around and hope for the best.

Condos crashing now. Next up – single family homes. Great for younger families trying to get into a home. Bad for assets rich, cash poor boomers

“Who cares. Fed cut rates by 100 points last year and mortgage rates went up.”

Exactly! If they cut again, long rates and inflation will spike. Also, i think we’ve seen the last of QE. 2020 was the event horizon. Think about it. We had 0% rates from end of 08 until 2015. If they could do it then, but they can’t do it now, what has changed?

The ‘markets’ have been ‘demanding’ all year and longer that the Federal Reserve cut its overnight short-term rates. Just what do they ‘think’ that would do to long term rates such as mortgage intertest rates? Didn’t the long-term rates rise a full 1% when the Federal Reserve cut short-term rates by 100 basis points?

I’m not disputing that all over the US, real estate is stalling in sales; however, Florida’s real estate may be worse due to a larger number of factors (some unique to Florida) converging on that state:

1) Hurricanes. Recent, multiple hurricanes along the west coast and inland to the central part of the state have convinced many that it’s time to move. Note: This direct hurricane experience impact has not hit south Florida….yet.

2) Homeowner insurance for everyone in the state is getting difficult due to weather impacts.

3) Tower condo owners across the state seeing huge increases of HOA fees for inspections/repairs; especially for older buildings. This has been evolving since Surfside collapse in 2021 and is now baked into all of these type residences across the sate.

4) Boomer retirement wave is ending but those remaining no longer see Florida as the perfect retirement. More affordable, mild climate and protected inland states/locations in SC, NC, TN and elsewhere are being sought.

5) Foreigners own a lot of property in Florida, including Canadians and Brits who vacation there in the winter. Their attitudes about the safety of their US investment in Florida may be changing?

As mentioned above, wait until the “big one” hits south Florida.

Ehh, I live in Florida, and I’m not that worried about hurricanes. My house has a new roof, impact glass, and is not that close to the ocean.

The houses that were destroyed on the Gulf Coast were old ramshackle houses.

As for 4, I don’t think it’s climate change, but the run up in pricing in 2020-2022 that has turned many new retirees away. They’ll be back if prices drop.

Just remember that Florida doesn’t really get a winter, whereas SC, NC and TN absolutely do.

The Insurance Industry is Quietly Making Record Profits

April 1, 2025

“According to AM Best, property casualty insurers made a record $169 billion in profit in 2024—even as they raised prices and pushed for laws to avoid paying more claims, all while claiming the industry was in trouble.1

The $169 billion profit amounted to a 90% increase from the previous year and a 333% increase from 2022.”

We’re living in a time of unprecedented corporate greed which is wholly unchecked.

I’ve lived in both locations for a number of years and by far, the climate in the mid-Atlantic states as well as SC and TN is far better all around than Florida. Florida is too hot in the summer. Winters in the areas I’ve called out are really not that bad. Much less severe than further north. Most folks have figured this out.

I’ve posted here before about a recent study where they had government officials up and down the chain in South Florida saying essentially that they should probably be planning for a post-insurance future there, but nobody can talk about it because the second you say that, you destroy everyone’s property values and now they’re mad at you.

At the same time Wolf posted this article, ProPublica posted a story from Oregon about the uproar over their fire risks maps there and how people think that the existence of those maps is what’s causing their insurance cancellations – cue the conspiracy theories and everything else you’d expect.

What I HOPE is that the trends Wolf is talking about here indicate that people are starting to engage with reality, at least in Florida… although what am I saying…

The alternative way that these trends play out was described pretty well on a recent Substack article:

“I have written a number of times about the way that the climate change crisis in America will manifest itself as an insurance crisis, which will then cause an economic crisis and a political crisis. Increasing climate risks will cause home insurance prices to rapidly rise towards unaffordability; homeowners in risky areas unable to afford the (actual) price of home insurance will clamor for relief; policymakers unwilling to confront the underlying problem (climate change) will react with a series of increasingly desperate maneuvers to delay and paper over the issue; increasingly pricey disasters will cause state and local politicians to run to the federal government for bailouts; in time, this will lead to a political confrontation between those who are receiving aid, and those in safer areas who are paying for it. The end of this process will be a retreat from areas that have become untenable to live in due to climate change. Instead of carrying out this necessity in a managed and rational way, our political system and economic system, absent some deep changes, will cause it to unfold in a cutthroat, childish, maximally destructive way, with millions of Americans frantically trying to step on the heads of everyone underneath them to jump into the metaphorical lifeboats, which will be controlled by capitalists looking to extract maximum profits from the spreading crisis.”

– Hamilton Nolan, “Cheap tricks for hard problems.”

see my post bove

…bottom of the ninth, game tied (the best, it seems, it can ever be in an ‘Anthros’-‘Planets’ series), Planets’ always-strong battery coming up against an apparently-weak Anthros’ bullpen…

may we all find a better day.

The Anthros played a really different sort of game, for maybe 6M to 13,000 years (depending on which part is of interest to ya, that’s for sure! And that is saying a lot for a 4+ Billion year overall game. I’m glad I got to play so many different positions and absorb so much of the Anthro’s playing skills and strategies during my “gooey rock” organism time.

Good comments here…well…..”good” in the sense of accurate, anyway.

Hope PD stablehand all else ok.

Oh, I cut it off at 13K because it is all just Anthro language and culture now…sorta like “natural” evolution got put on hold…..the two don’t mix well, that is for DAMN sure.

Oh well, bottom of the 9th, like you said, at least for those nearer the bottom…maybe all.

“Instead of carrying out this necessity in a managed and rational way, our political system and economic system, absent some deep changes, will cause it to unfold in a cutthroat…”

In other words, free markets work. Our $37T national debt (ignoring state and local government pension overhangs which are also substantial and also ignoring the rapidly approaching Social Security disaster) and the results of past government attempts to “fix” things in a supposedly “managed and rational way” all suggest that government “solutions” are likely not to be a better answer. Political solutions are often not “rational” – except from the POV of politicians who are buying votes and rent seeking special interests who benefit.

Regardless of what one believes about climate change, it’s not something that is going to be dramatically impacted by government action in a timely matter as it’s a global rather than local or national problem. Globally we can’t even get dictators to not invade sovereign countries (Putin) or be preparing to in the longer term (Xi) – there’s little hope that these same miscreants will allow their domestic popularity to suffer because they diverted resources to climate change for the “global good”.

And for the record I will not be responding to the MAGA warriors and idiotic climate deniers that always reply to my comments. I’m trying not to waste more of Wolf’s column space than I need to. If anyone wants to engage in a BS political knife fight with me then you can find me where that sort of thing belongs: in the YouTube comments section.

“Talk to the hand, sista, talk to the hand”

“Climate deniers” is a peculiar phrase. I doubt if anybody denies there is climate.

@Omnopotent Haha yeah if this website was able to fold replies and Wolf didn’t have to moderate everything then I would argue with them. Instead, this comment section is like an old school mailing list.

All of a sudden,

everyone is an atmospheric scientist.

So much like a climate alarmist.

Always trying to dictate terms

while hurling ad hominen attacks.

No wonder the children are scared.

Global Cooling>Global Warming>Climate Change>Climate Crisis

Keep escalating the verbiage.

So tiring, and quite banal.

Florida is hot in summer and has hurricanes.

Must be a man made problem,

Get outta here with that.

The climate has always been changing. We can’t control it. People have been building homes that are in high risk areas. Florida has always had hurricanes and the West Coast has always had fires. Just more people living there. Wake up man!

Correct. We always have hurricanes. What’s making it so expensive is the unnatural pricing bubble we’re in. Crash prices and insurance rates will follow

Climate change has almost nothing to do with the increasing price of homeowners insurance. There has been no increase in the number or intensity of hurricanes or severe weather in North America in the last century, and the number and size of forest fires in the American West is a tiny fraction of what it was prior to 1900, look it up, fires the size of European countries were frequent in those times.

What has changed in the last hundred years is that 10s of millions of people have moved to hurricane prone coastal areas in the southeast and the gulf coast, and 10s of millions in the American West, particularly CA, have moved into wildfire zones that existed for millennia.

The narrative you are promoting is from people who wish to control individual choice and taxation in ways that make people feel virtuous but have no impact whatsoever on climate change.

…as always, consider local planetary physical conditions (and any available history) before placing one’s short and long-term bets. Gather too-many, high-resource consumptive members in an any area, with a climate that always-varies on a longer wavelength than the one of an average lifespan, and a ‘climate-crisis’ of some sort awaits that population, human or not. Looking forward, realistic observations of supply and demand on resource availability/resilience and climate variance are now at constant odds with ‘eternally-subservient’ resource and climate memes across current human civilization…(…and yet, the (necessary, well-attended/curated and mission-stated/specific) time we spend here in Wolf’s most-excellent establishment, in the quest for a more-prudent management of our mostly-self-generated economic resources…).

may we all find a better day.

Happy1,

Respectfully,

It is good to control people’s right to individual choices when people’s choices have adverse consequences that affect everyone else, are difficult to redress or reverse, or will lead to rampant environmental damage and depletion of resources.

As an example, if you choose to believe that chlorofluorocarbons don’t damage the ozone layer, that should not entitle you to use them because you want that “personal freedom” for yourself and to force everyone else to deal with the consequences of increaed skin cancer and damage to crops because you refuse to accept reality.

If you choose to believe that lead is not harmful, that shouldn’t entitle you to drive around with leaded gasoline spraying lead particles everywhere from your exhaust or paint your apartment with lead paint and rent it out to someone else because that “freedom” has real consequences that restrict another individuals freedom to not be exposed to lead.

The tragedy of the commons is a real and well documented phenomenon. The government should absolutely be empowered to regulate selfish and greedy behavior in order to allow other people the freedom to not be harmed by another person’s personal choices.

Regulation and rule of law is critical to any well functioning society and part of the social contract is that everyone in society gives up some freedoms in order to secure some others.

Mirage,

You outline a slippery slope, that ultimately leads to totalitarianism/communism. One nice thing about the US, it is so big and complicated that it is difficult for government to play dictator. We have many laws. Many of those laws are ignored. The US will likely be the last country to succumb to the fascist-wannabes.

I dont think the big increases in house and house related costs such as insurance would have been nearly as much without all the govt QE zirp policy creating a speculative mania and that’s much more the cause of the problem than climate changes. Not everyone thinks high property values are good because that leads to high insurance or dropped coverage, high taxes, housing being very expensive or unaffordable for people who might want to start a family.

Re: “For each 100 new listings, sellers pulled 59 listings off the market”

From my experience, after selling my house, the new owner put the house on the market for a month, then delisted— but, what was curious, and still a mystery, is that his MLS effort was totally wiped off the map, in a scrubbing effort —- to obfuscate his failed attempt to sell.

He’s recently delisted at a higher price, but if someone searches Zillow, or any site, that prior failure to sell, isn’t there.

So, with Florida and this delisting trend, I’m curious if these failed efforts to sell are similarly scrubbed?

I can understand that, if, there’s not a legal transaction, there’s not a requirement to modify property records for a non-event.

My situation may be unusual, but how are these delisting quantified and are they notated in sales history??

The scrubbing really annoys me these days. Now I have to go to the assessor to find the past sales price? Yes, it’s a for-profit real estate site that can mislead anyone they want, but leaving buyers to take extra minutes for research does not make me generous to the agent or seller.

Transparency builds trust in real estate transactions. Hiding things builds lawsuits. Florida has a lot to hide with all the flooding, shoddy post-destruction renovation, and other alligators in the closet.

Rest assured the goverment will step in and make it worse. The problem is much greater than just home price and interest rates.

Most americans are getting poorer and will never be able to afford an average home. How this plays out none of us know.

In 2010 my financial advisor told me I was in the top one percent based on income and assets. Today just in the top 10 percent. I have more assets, but the target has moved.

The big issue for most folks is service inflation and that is going through the roof. I can easily control what I buy, but I have little control over services I need.

Perhaps Wolf could post a chart on what it takes to be one of the pretty people! Just might wake a few folks up. A few million just ain’t what it used to be.

Perhaps that is one reason many are not willing to sell property they own and do not need? If I sell then what? Earn little on a safe investment or buy into a overpriced market?

Finally bought a new pickup last week and paid cash. I bought the most no frills I could find and got an extended service and warrenty contract. I could have paid cash for any pickup on the lot, but uncertanty does drive consumer choices. I would expect this to effect retail sales and the general economy for a long time.

Everyone has control of what services they need laugh.

Welcome to the laland of living beyond the skies. Things become stupid in terms of thoughts and sayings like a few million isn’t what it use to be.

A wine club member last year remarked that 25M isn’t much because someone else in our group sold a company at over a billion dollars and has the real $.

The best question on a new meeting with friends from other laland members is “where do I summer?”

Enjoy laland I know I do sometimes.

You and Bear are funny.

But you guys can’t glow in the dark and so many other animals can….hundreds of species, many as yet unknown, like in the very deep ocean.

Unique to this bubble (?) is that sellers feel no urgency to lower prices. Job changes, divorce, etc. force a sale, so these pending sales must be predominantly investment homes, vacation homes, etc. so these owners just keep on renting or otherwise can afford the carrying cost of continued ownership.

From the price history, I can see a lot aren’t rented out or being sold. They’re just sitting vacant.

There’s only so long before they’ll tire of owning a money pit, solely so they can get “their price.”

I often wonder about the impact from having to decision-makers involved instead of just one.

Take a married couple for instance – the assumption is often that just one person is making the call on when to buy or sell a home, but there could actually be a lot of emotions and stress involved in that decision making dynamic.

If one decision maker is dead set against selling below a certain price, not much the other one can do other than agree to that price, but maybe put in a stipulation that they will definitely sell next year.

Historically house prices have pretty much only gone up, so there could be a very real fear that, if they go up again, the spouse would poke at them for years and decades to come (if they were to leave substantial money on the table).

Relationships can be complicated, and money can make that a lot worse. Will be interesting to see what happens in a year or so…

This dynamic may happen and is always present in the market, however given the significant number of homes that are sitting and/or pulled from the market there is something else going on. Why now? Why are so many choosing to not lower their price? Unique to this bubble, they have the option to pull their homes from the market, so the decision is not forced (unlike the 08 bubble).

“to decision makers” = “two decision makers”

Government just stay out. Let people and companies fail. Let the 500 year business cycle work its magic. This solution will create more stability. People can rely on a market more so than 13 people at FED or a President. Huge clearing out will happen, not by an authority stepping in, but by authority stepping away Correct?

Yes I totally agree, the manipulation is bad and makes things worse but the uniparty loves manipulation. If we voters don’t want that, weve got to not reward what we think is wrong by reelecting the bad policy makers. The Libertarian party that has been on the ballot policy is a balanced budget and free markets. But every if they won, the people would need to watch to make sure they follow through.

DM: Tech giant Intel’s stock plummets after Trump demands CEO resigns over China links

Once America’s crown jewel tech company, a struggling producer has drawn the ire of the President.

I looked over Intel, fairly close last year, because it seemed like it might have been undervalued— and that was right around when Qualcomm backed off — it came down to mediocre products and poor management and a disastrous board of directors — and realizing it was pointless to invest in.

Then along comes Vance pumping it up in early spring — and now, we get presidential market manipulation.

INTC kinda has the potential to have a decent foundry, but, after years of being directionless, they were totally caught off guard with AI — nonetheless, seemed like they could recover in time and find a way to supply a useful wafer for something, but their 18A test chips were relatively flawed and quality yields were awful.

So, with that background and the addition of presidential political manipulation, it’s clear to me, to not own stocks, especially during this early chaotic tariff stage. Instability and risk make this into an insane casino.

Intel does have a magnificent cash burn rate and if they don’t gut the BOD and majority of headcount they’re heading towards delisting (had to include that word somewhere).

The stock is back where it had been in 1997. At least, it’s still around, unlike a bunch of others of that time.

Great numbers/info, but somewhat skewed, because a lot of the pulling off the market is followed by a quick relisting simply to keep the listing “fresh”

Who do they think they are fooling? In my view, it creates a level of mistrust, via reduced transparency. I’m less inclined to purchase a home from somebody into game playing.

Home owners who refuse to the lower prices are an excellent example of the sunk cost fallacy. They are unwilling to let go of a losing investment because they have too much invested. Eventually they will have to capitulate if they need capital.

If you want Exhibit A of how out of whack Florida’s market is, check out 12137 Boca Reserve Lane, 33428 (Wolf doesn’t allow links, so I’m just giving the address).

Owner purchased it in 2016 for $725,000, and has been renting it out (or attempting to) since 2020. He listed it for sale a few weeks ago, for $1,995,000, before dropping the price to $1,900,000.

You’ll see that he has it listed for rent at $7,900, and it’s not flying off the shelf.

In no universe should something that supposedly costs $1.9 million only rent for $7,900/month. This is why people don’t want to buy. Zillow projects the cost of ownership at $13,280, and to be honest, that’s probably a little low given the situation with insurance.

Why would anyone buy?

Let’s assume that the “seller” can cover his costs with $7,900 (which may be true given that he paid only $715,000). How long is he going to spend $3k a month in carrying costs, until it’s rented? At some point, these people will realize they just need to sell and be done with it.

In the most bubbled markets, like Austin, Florida, Nashville, Denver, and so forth, there was a short temporary demand for rentals and sales. That is gone. This owner has been trying to rent it out for nearly 3 months now. At what point is enough enough? The “If it doesn’t sell, I’ll just rent it out” sometimes is easier said than done.

There is a psychological cost to losing money each month.

Here is a typical scenario when the market rolls over:

Seller is in denial and lists too high.

A series of failed escrows and relisting with “better” agents ensues, often over several years(I’ve seen this play out for even 6-8 years in the ’08 bust).

The property is always listed too high(or “in line” with similar properties).

Finally the seller throws in the towel and a low baller buys it way below the last listed price and waaa—-ay below what the seller could have sold for if he had gotten in front of the downward price cascade at the very beginning by undercutting all of his competition.

This is the case in so cal/san Diego as well.

A house would cost 1.5 million to buy but one can rent it for $7k or less.

Got you beat. All over Seattle, a person can rent a $2M home for less than $5k/month.

Federal Reserve, Using Non-Compliant Accounting, Hides Over $100 Billion a Year of Losses and Resulting Negative Equity, Due to Illegal Bank Subsidies

Posted on August 7, 2025 by Yves Smith

William Bergman, who was an economist at the Chicago Fed for 14 years, has published a bombshell analysis for the Institute for New Economic Thinking, which describes in depth how the central bank has been hiding large losses and what should be shown as negative equity via its own irregular accounting. Bergman’s finding of a loss rate of $100 billion a year is based on the subsidy to banks provided by the payment of interest on reserves, whose costs has risen considerably due to comparatively high interest rates in recent years. We’ll later unpack a second unaccounted-for source of losses, which Bergman mentions but doe not attempt to estimate, which is unrecognized losses on securities purchased during QE, whose value has fallen in a higher interest rate environment. As we’ll explain, QE by design was a “buy high, sell low” scheme, so this outcome should not be surprising.

This is ignorant bullshit. The Fed has NOT been hiding any losses, it is putting its losses in plain view, for all to see, both its operating losses, and its losses on securities (“unrealized losses”). All you have to do is read its annual report, or read my articles about its losses, instead of dragging this stupid-ass ignorant bullshit into here.

For example, in its annual report for 2024, the Fed reported an operating loss of $77.6 billion. For 2023, it reported an operating loss of $114 billion.

And in its annual report, it reported cumulative “unrealized losses” on its securities holdings of $1.06 trillion at the end of 2024, you goofball.

Click on this link and read the article to learn the details where the operating losses and losses on securities holdings came from, and never ever post this stupid-ass bullshit again. Adios.

https://wolfstreet.com/2025/03/21/feds-operating-losses-declined-to-78-billion-in-2024-unrealized-losses-rose-to-1-06-trillion/

Yes. Yet my posts still await moderation.

You were QE mongering again.

What’s this post have to do with Florida homes?

I’m starting to think there’s a conspiracy that the RE industry complex doesn’t want Wolf to keep running his website anymore. So they have their critters flood Wolf’s website and spread all this bs to rile him up and mess with his blood pressure. It’s diabolical I tell you. Long live Wolf!

“It may take until mid-2026 for rent inflation in the consumer price index to subside toward its pre-pandemic norm, according to research by the Cleveland Fed.”

That would coincide with long-term monetary flows, the volume and velocity of money.

Loved living in Florida – all kinds of nice fun things to do, beaches, outdoor activities in winter, cosmopolitan stuff in Miami, Space stuff, Redneck stuff in Jacksonville, crazy Florida Man in the news with something truly bizarre every week. Even hurricanes are incredibly entertaining if you live a couple miles from the ocean on high ground in a brick house. But, unfortunately – I was raising two boys and needed to get them out of the FL education system, so moved back to Farmville, MN 6 years ago this month. I can promise I will never again own property in FL unless someone gives it to me, at which point it will be immediately for sale.

Florida is an untenable state in the intermediate term. It should not be legal to build there, as long before the whole state will be underwater from sublimation and sea-level rise there will be no more drinking water due to salt intrusion in the aquifer. Insurance companies know this, and are intentionally pricing themselves out of the FL market. Soon enough, a big direct hit from a Cat5+ hurricane, like Andrew or the one in 1935 that lifted locomotive engines off their tracks is going to flatten a city, and it won’t make sense to rebuild.

Still it’s a lovely, fun place to vacation.

Respectfully Tom H, reverse osmosis water treatment systems can supplant ever-turning brackish aquifers in Florida, especially coupled with (but only if) wide deployment of solar array systems. Reverse osmosis systems are very energy-intensive relative to treatment for surface water like from the Great Lakes. But it’s feasible.

If you’re going to desalinate water, you might as well do it with ocean water rather than pumping the aquifer. But all of this depends on having basically free electricity, which is only possible if solar becomes ubiquitous, which will take a long time even discounting the fact that the party in power in Florida is hellbent on avoiding renewables.

But even if everything somehow works and you can cheaply desalinate water, ground water salinity will still ruin farming , which is still a large part of the Florida economy, not to mention have incalculable effects on the local ecosystem.

Bottom line is that desalination is a narrow solution to the problem of drinking water, or maybe household use at most. But Florida needs a lot more than just that.

Florida added more solar capacity in 2024 than California, per a CNBC article last week.

Give me a break. You left wing loons have been saying is FL supposed to be under water decades ago. You have a Better chance of freezing to death in MN so enjoy…

I see FL was ranked #2 in education by US news as well.

Is that you Tim??

I used to watch pro Wrasslin. But now I just come here. Much more entertaining and educational. I can just imagine these errant commenters getting slammed into the mat.

😂😂😂

Wolf is the Hulk Hogan of the cyberspace.

The current real estate market is the largest financial bubble in history. Imagine if you inflated a car tire so much that it became four times larger than it is supposed to be. It would be a disaster waiting to happen. What would happen? Oh yeah – it would burst, or

X-plode. When the housing market does burst, it will leave a lot of devastation in its wake. It is the largest financial bubble in all of history. It NEVER should have happened. We’re going to have to deal with its’ consequences.

Nobody mentions the ugly long term side of the real estate argument

DEMOGRAPHICS

Each year an increasing number of Boomers die or are forced to sell their houses. As a whole boomers have had the largest % home ownership of any age group in US history . And some of the more affluent boomers own more than one house.

This INEVITABLY creates INCREASINGLY large SUPPLY of these boomers houses .

Birth rates are the lowest in decades for various reasons . Women are delaying having children in order to get better established in their careers and freezing their eggs . This means smaller families and results in LESS DEMAND for the larger houses that the boomers own.

What happens when you have increasing SUPPLY

AND less DEMAND . LOWER prices .

Given the runup of the last 5 years , this will translate to much lower prices .

Well, you forgot the Millennials and GenXers — they’re now the largest generations, larger than the boomers, and they’re big home buyers.

Generations are a constant flow.