At the long end, the bond market is nervous.

By Wolf Richter for WOLF STREET.

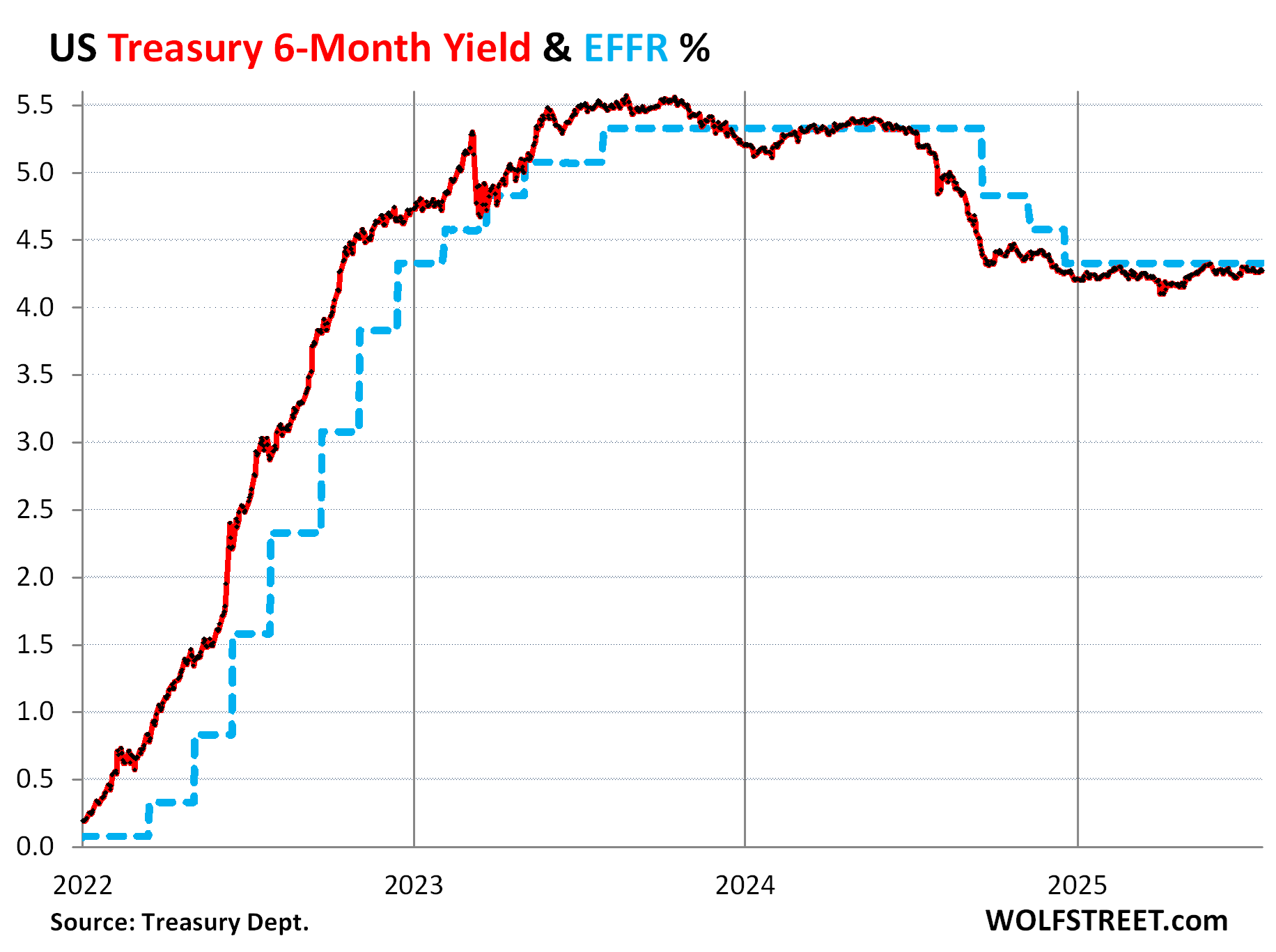

The 6-month Treasury yield, which is a good indication of rate hikes and rate cuts by the Fed within 2-3 months, is still glued to the underside of the Effective Federal Funds Rate (EFFR), which the Fed targets with its policy interest rates, and is thereby not yet predicting rate cuts within its vision of 2-3 months.

Last year, on June 26, the 6-month Treasury yield (then 5.33%, matching the EFFR) started skidding in anticipation of the 50-basis point rate cut that the Fed announced on September 18. By July 25, so exactly a year ago, it had dropped by 18 basis points to 5.15%. By August 28, it had dropped by 50 basis points to 4.83%, having fully priced in the 50-basis-point rate cut.

Today, July 25, the 6-month yield is still glued to the underside of the EFFR, and so it has still not begun to price in a rate cut at the September meeting, despite the public spectacle of Trump keelhauling Powell on a daily basis to get the Fed to cut its policy rates.

This 6-month Treasury yield is a summary depiction of the short end of the bond market where traders and algos look at millions of data points, and at everything the Fed says and does not say, to take bets on what will happen with interest rates over the next few months. And it still says, nothing will happen.

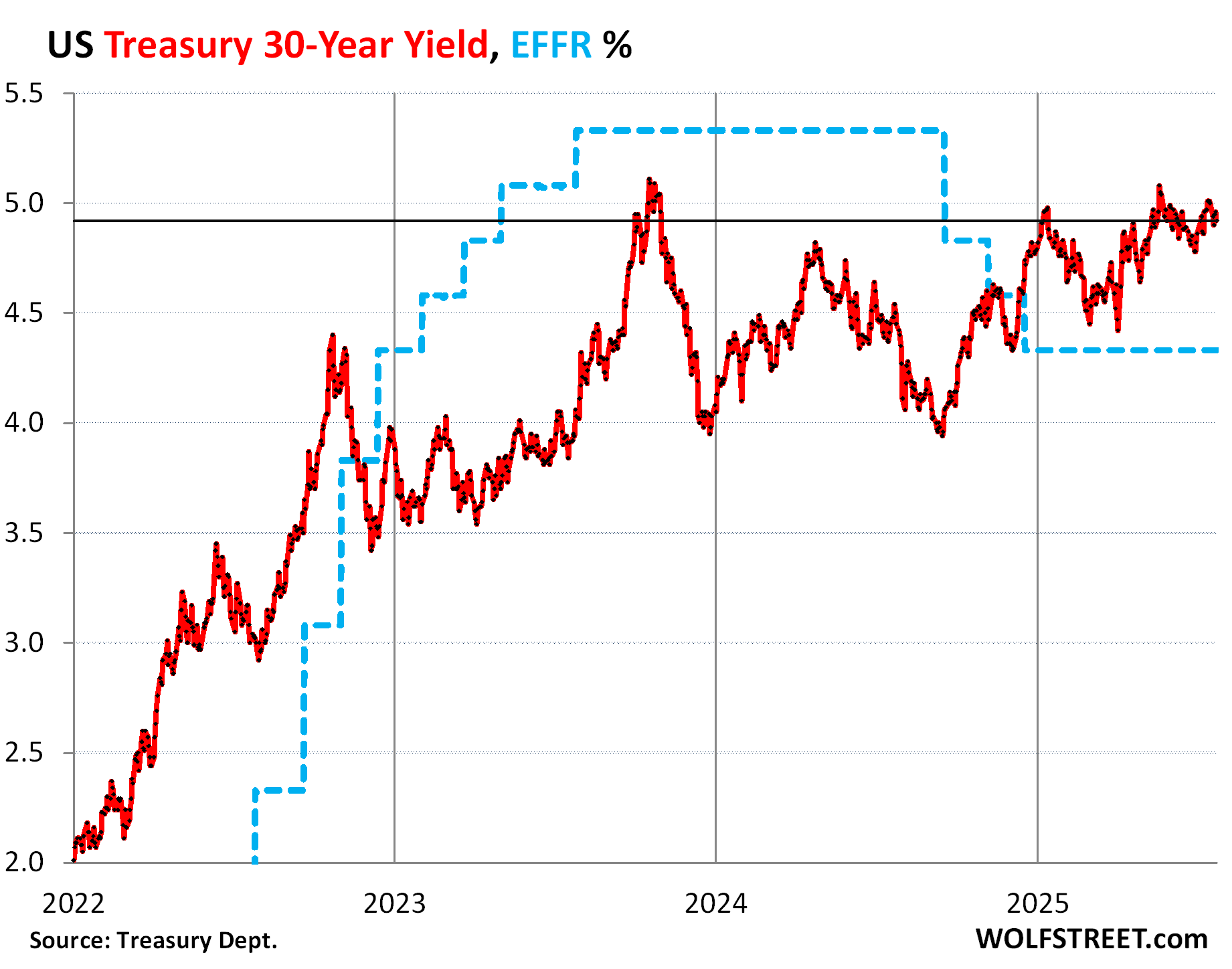

At the long end, the bond market is nervous.

The 30-year Treasury yield spent all week in the 4.90% to 4.96% range. On Friday, it ended at 4.92%, 59 basis points above the EFFR. Last week, it was at 5.0% for four days. So far in July, it has risen by 14 basis points.

Since the Fed cut by 100 basis points starting in September (dotted blue line), the 30-year yield (red line) has risen by 99 basis points! That was a massive move by the bond market against the Fed. And it has taught the Fed a lesson about spooking the bond market. It has since then switched to wait-and-see.

In this inflationary environment, the secret question is: How many rate cuts would it take to spook the bond market into pushing the 30-year yield to 6%?

The government has been trying actively to push down long-term yields, or at least keep them from rising further. It said that it would only slowly replenish its checking account, the Treasury General Account – which had been partially drained during the debt-ceiling period – by increasing the issuance of short-term Treasury bills, and taking it easy with the issuance of long-term notes and bonds.

Since mid-2024, the government has also been engaging in buybacks, where it issues new debt and uses the proceeds to buy back Treasury securities that had been issued some time ago. Some of the buybacks of long-dated securities – such as 30-year bonds issued in 2020 through mid-2021 with coupon interest below 2% – occur at massive discounts, whereby investors lock in their losses and the government reduces its outstanding debt. This is another effort, initially engineered by the Yellen-Treasury and continued by the Bessent-Treasury, to push down long-term yields.

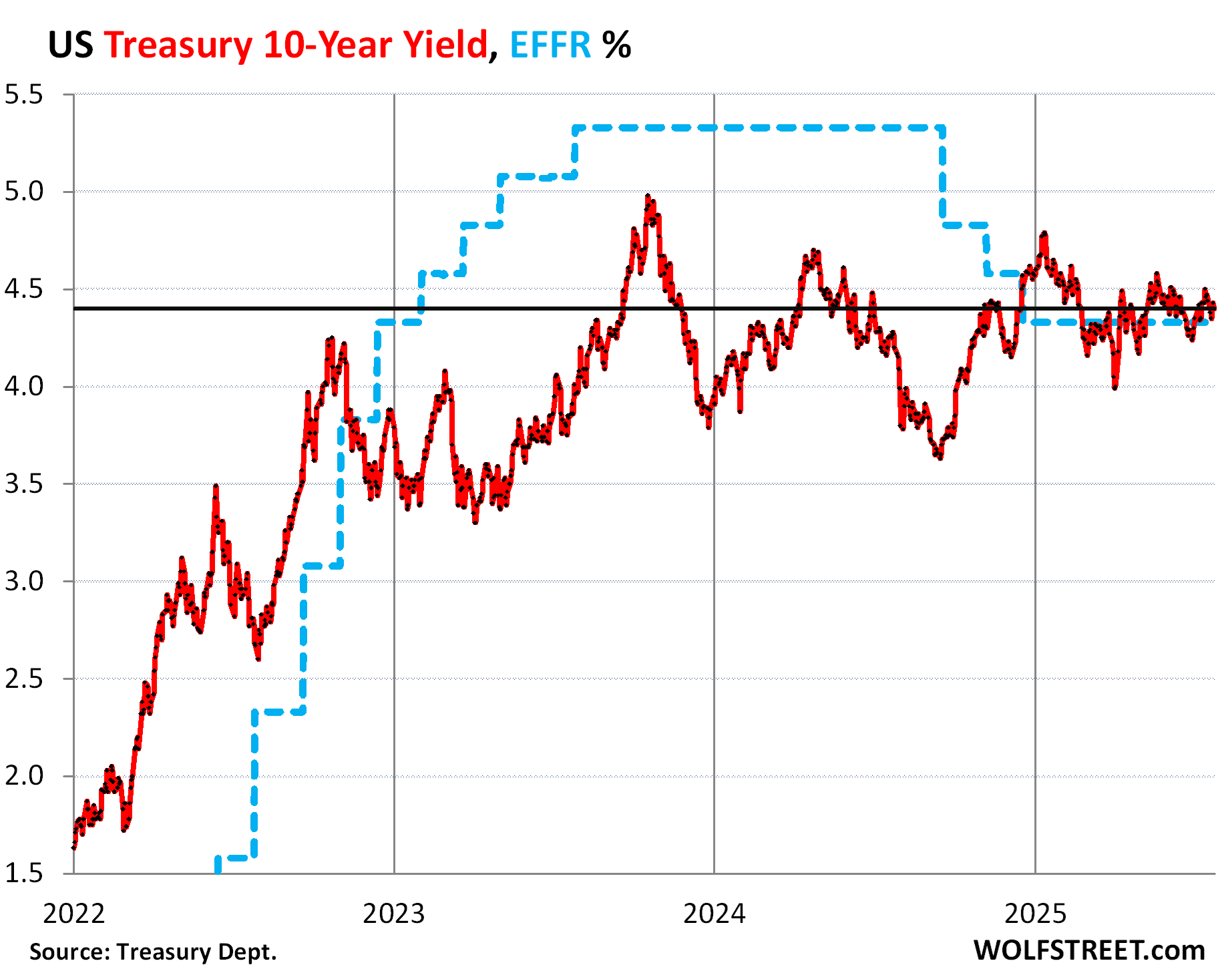

The 10-year yield ended Friday at 4.39%, just above the EFFR. Despite some ups and downs, it hasn’t gone anywhere over the past five months.

The bond market is nervous about inflation. Inflation, enemy #1 of holders of long-term Treasury bonds, has been accelerating, driven by inflation in services. And the bond market is nervous about a lackadaisical Fed in light of this or potential future inflation.

And it’s nervous about the swelling Mississippi River of new Treasury debt flowing toward the bond market that it has to absorb, possibly with higher yields to draw in more buyers. Higher yields mean lower bond prices; that’s attractive for future bond buyers, and that’s what it takes to pull more buyers into the market to absorb the Mississippi River of new debt. And it means more bloodletting for existing bondholders.

But short-term yields up to six months haven’t budged much and remain glued to the EFFR of 4.33% as rate cuts are still on ice.

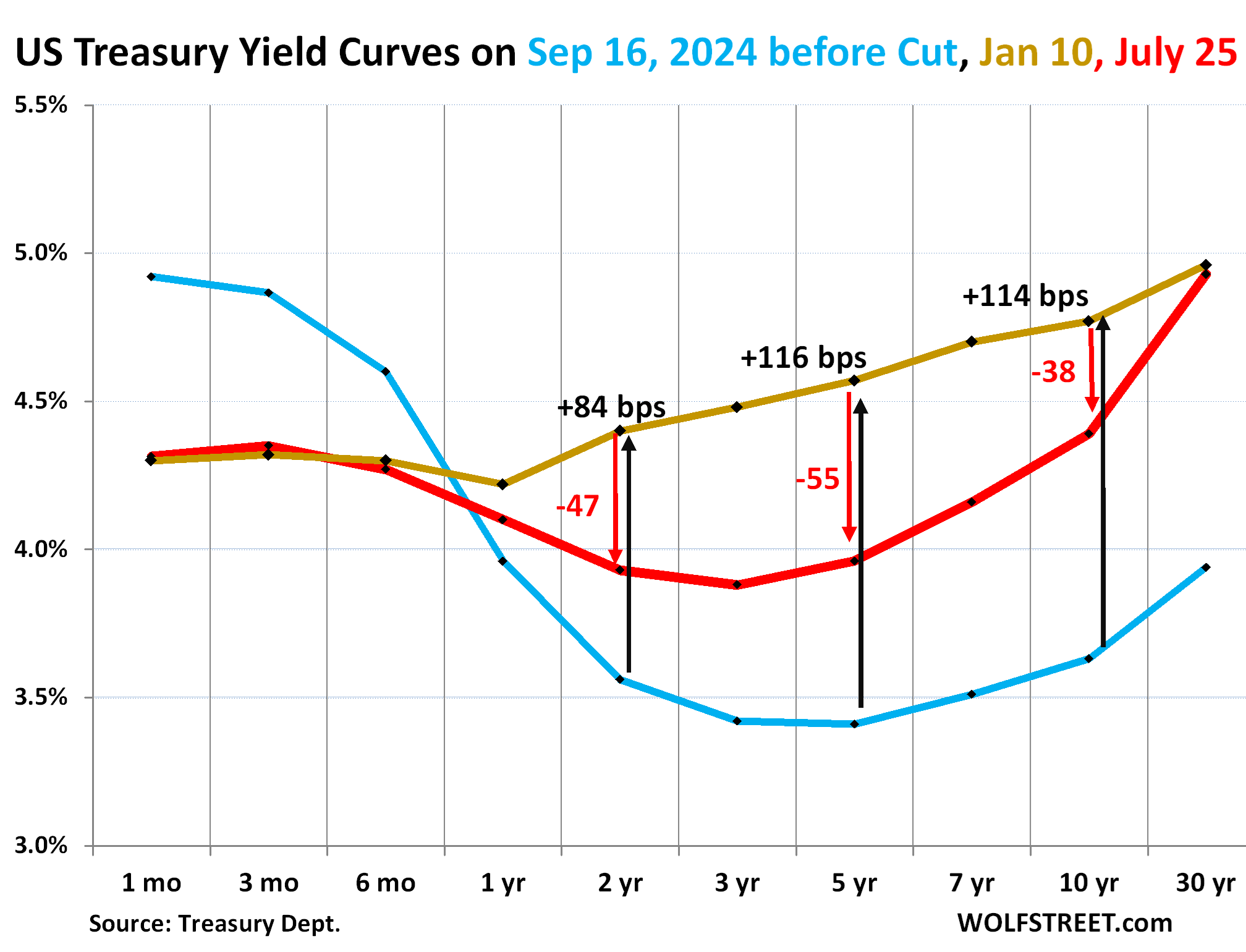

Expectations of rate cuts further down the road have pushed down yields over six months and into the five-year range.

The yield curve chart below shows the yield curve of Treasury yields across the maturity spectrum, from 1 month to 30 years, on three key dates:

- Red: Friday, July 25, 2025.

- Gold: January 10, 2025, just before the Fed officially pivoted to wait-and-see.

- Blue: September 16, 2024, just before the Fed’s rate cuts started.

The nervousness at the long end, rate cuts on ice at the short end, and rate-cut expectations for the next couple of years caused the yield curve to sag in the middle.

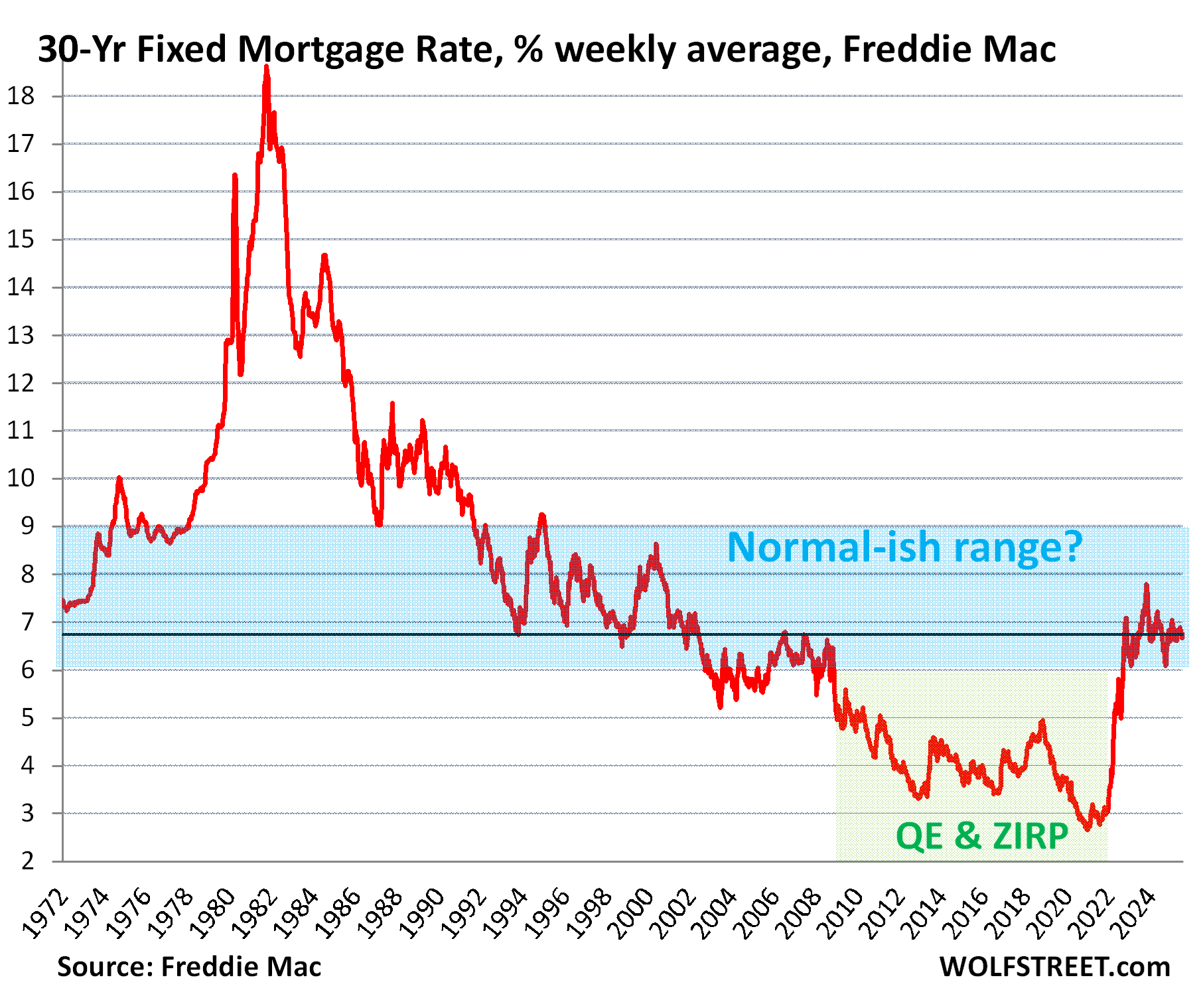

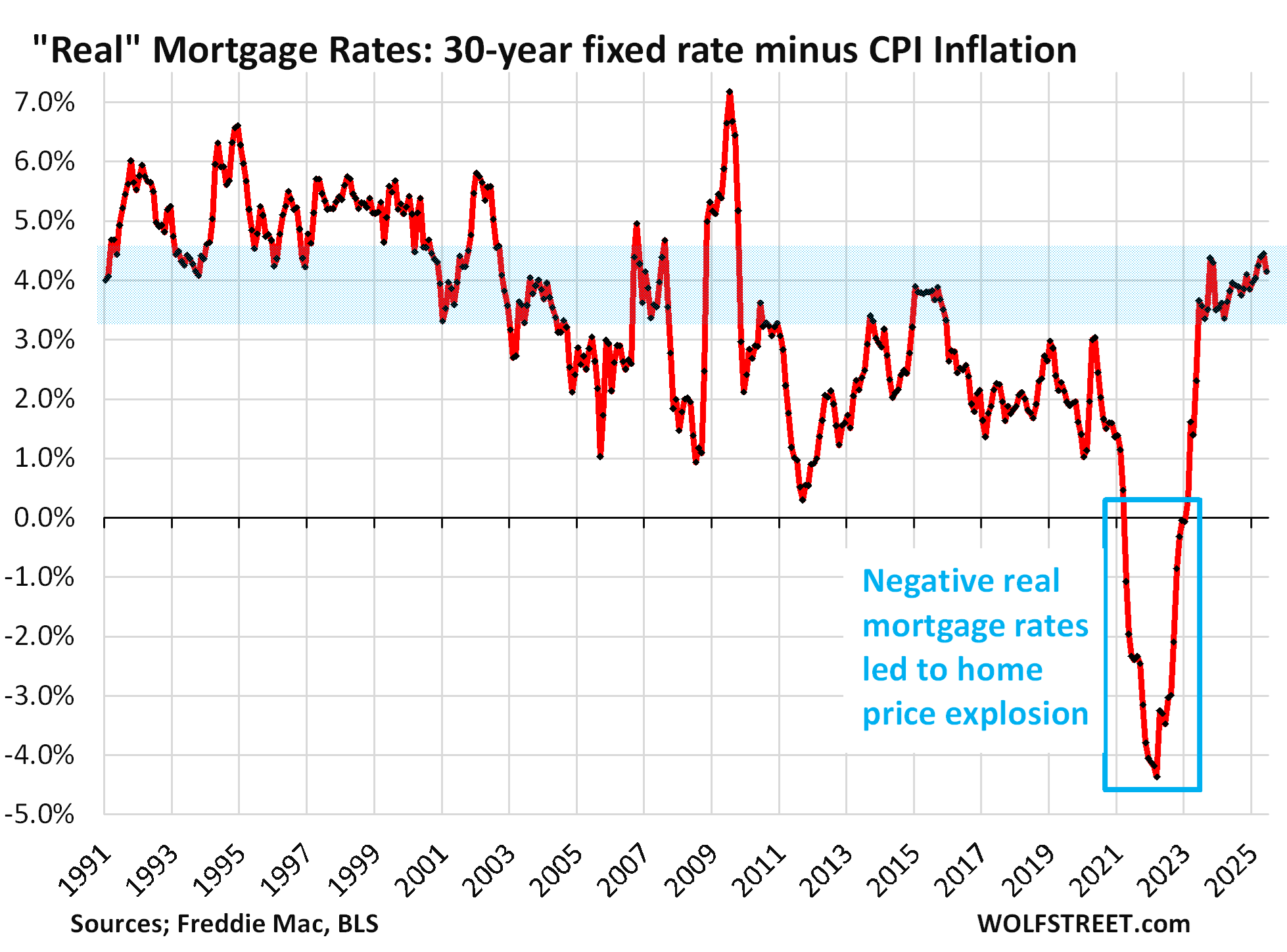

“Real” mortgage rates are back to pre-QE normal.

Mortgage rates of government-backed 30-year fixed mortgages run roughly in parallel with the 10-year Treasury yield, but are higher, and that spread varies.

In the latest reporting week, the average 30-year fixed mortgage rate ticked down to 6.74%. It has been in that range near 7% all year.

The super-low mortgage rates during the Fed’s mega-QE – when it bought trillions of dollars of MBS – were an anomaly of history that has caused the biggest explosion of home prices ever, along with raging inflation, into mid-2022. What’s left over now is a massive hangover, huge housing debt, and a frozen housing market.

“Real” mortgage rates – mortgage rates adjusted for inflation – have been back in the pre-QE normal range since the second half of 2023: The average 30-year fixed mortgage rate minus CPI inflation was 4.15% in June (average mortgage rate for June of 6.82% minus CPI for June of 2.67%).

The home-price explosion – home prices spiked by 50% and more in a couple of years – occurred from mid-2020 through mid-2022, driven by deeply negative “real” mortgage rates, when raging inflation far outran the Fed-repressed 3% mortgage rates. Borrowing at a 30-year-fixed rate of 3% while inflation was far higher was better than free money, and people went nuts because price suddenly didn’t matter anymore because money was better than free. This episode has caused this Fed to go down in WOLF STREET history as the “the most reckless Fed ever.”

Since then, the Fed has backed out of this recklessness, and “real” mortgage rates are back to normal, but home prices are way too high, and the housing market is suffering from a massive hangover.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Just how high will long term US Treasury yields rise in the months ahead?

Likely to go to 6. The probability that debt is in service mode is high. Debt to gdp 125%. If rates are dropped, it won’t help mortgage rates, or the 30.

SoCal,

Depends. How high will hyperinflation be?

One day you will be as cynical as me. You have a long ways to go till your in Rabid Perma bear country.

I shall keep an eye out for you.

@SoCalBeachDude

When I graduated from college, Treasuries were at 16%, and clearly headed up. This was 1977.

Those of us who remember the 70s are not easily fooled about inflation and the bond market:

-Federal Deficits cause inflation, typically after an 18-month delay.

-Inflation causes high bond yields, typically after a 12-month delay.

Considering that we have a Federal Deficit of around 4% per year, current bond market rates are low. The current budget means that this will continue for at least another 3-4 years.

Great piece

My thoughts too…

Classic wolf.

More valuable than all of WSJ.COM

I’m surprised they haven’t bought him out, just to shut him up

The WSJ has really changed for the worse, in all regards. From misleading headlines to content.

I found a bond that I had never heard of before. It is a AA+ government backed mortgage financing bond. It is a 20 year bond paying 6.05%. The catch is that it is callable. It will certainly get called if we ever reach the point where the fed is satisfied with the level of inflation. Until then, I don’t mind getting over 6%.

So it’s essentially a Fannie Mae bond?

My memory was bad, it is only paying 6.02%

FEDERAL HOME LOAN BA SER BQ-2045 6.02000% Jul-07-2045

Most government “agency” bonds are callable, and they do get called.

Interesting, I’d prob just go 4.5 to 5% with a treasury.

Bonds are fun tho.

Careful. This is not a great bond. You essentially lose out if rates drop as your bond doesn’t go up in value since it’s called. If, however, interest rates go up, you do take the loss.

Look up what the duration and convexity of a bond are. This type of bond has an S-shaped convexity that limits your gains, but leaves you with losses if rates go up.

The duration on this bond is likely around 14 years, depending on the coupon size. A 0.5% rise in long-term interest rates will cause you to lose 7% of its value, or about 13 months of interest. Conversely, if rates drop, you get a call notice.

But even if rates go up, a person doesn’t lose if they hold to maturity. They still get the 6 percent and then their principal at maturity.

The number one threat to bonds is inflation. If rates go up, in all likelihood the bond owner has lost purchasing power due to inflation. The longer the maturity of the bond, the larger the risk. Hence, longer-term bonds carry what’s called a term premium and have higher yields most of the time.

Long-term bond holders in the 50’s, 60’s, 70’s and 80’s took a bath on their bonds, despite the bond yield being guaranteed.

so all the downside but no upside. You might as well buy some high yield stocks.

The Fed, which will only act aggressively in abnormal, drastic conditions in the North American home market, where the world economy takes its lead for future conditions, is an institution of unhelpfully conservative bent. Its policies affect other world banks, not only in the Americas, but also across the developed First World. In acting conservatively, the Fed is lowering the bar on a range of future actions, hindering the fight against inflation and ignoring creative solutions that may present themselves. The Fed needs less bureaucratic thinking and more out-of-the-box thinking.

The LAST thing anyone needs is for the Fed to think out of the box. QE was a result of out-of-the-box thinking, the aftermath of which has turned into a nightmare. The Fed needs to stick to rate hikes and rate cuts and providing liquidity to the banking system when needed via repos and the discount window, and leave everything else alone.

“We will be data dependent” J Powell

“We will see through the data when appropriate” J Powell

Doublespeak typical of an” operation” hiding in plain sight

How is it that the Constitution gives Congress the power to create money (mint), yet the Federal Reserve has that power? At least Congress answers to voters.

The constitution gives the federal government the right to make coin money and regulate its value. Banks in the US traditionally created paper money. Congress had the Federal Reserve Bank take over that role from individual banks in order to better regulate banks and control the money supply.

The Congress gave that power to the FED and can take it back. But if they took it back it would be the Congress that would be accountable, not the FED. The last thing any politician wants is to be held accountable.

This way, the congress can appropriate spending without having to take responsibility for creating the money that is spent.

If money creating were explicitly in the hands of Congress I wonder what the value of USD would be ?

J J Pettigrew

“How is it that the Constitution gives Congress the power to create money (mint), yet the Federal Reserve has that power?”

I see this a lot but it’s nonsense.

The Federal Reserve Board of Governors, the employer of Powell and of which Powell is chairman, is a government agency, and its seven Board Members, including Powell, are nominated by the President and confirmed by the Senate. Only the regional Federal Reserve Banks are private institutions.

Congress creates and passes legislation. It doesn’t execute the instructions in the legislation. It’s up to the government (the “executive branch”) to do that, including the Federal Reserve Board of Governors.

Money creation is a fundamental process in a modern capitalist economy. Many people contribute to it (borrowing to buy a home, for instance) while commercial banks effectively create large amounts of money. The constant denigration of the Federal Reserve is exhausting!

danf51 nails it. The charade of central bank “independence” is a con perpetrated by your electoral representatives to evade responsibility for economic outcomes which are at least as much a function of their fiscal policy as monetary policy (and I would argue that fiscal policy is vastly more influential than monetary policy, but that is a view which is not widely held, I know) in devious attempt to undermine the democratic system of accountability.

“Independent” central banks are, by design, essentially aristocratic institutions inimical to labour. As such I would prefer a return to the consolidated treasury — a very heterodox position, I readily acknowledge.

The Fed was granted the power to create money in banking crises, but now it does so in a frivolous manner, denying free market cycles to occur….cycles which flush excesses. Excesses build, then there is a crisis. The Fed intervenes, the Fed accrues more power.

Hear, Hear !!

Wolf, well said. The Fed causes more problems than they solve.

The Fed used to expand the money supply to meet the demands of an ever growing economy.

It seems now, IMO, that it grows the money supply to give the illusion of an ever growing economy.

I used to have a cat that would shit outside-of-the-box, it was the worse thing ever. The way I see it, there’s no difference, thinking inside the box is always better

I initially read “the most reckless Fed ever” as “the most feckless Fed ever”.

When Trump talks about lowering interest rates, he should tell us what kind of interest rates he is talking about. The Fed can only lower short term rates, which can drive long term rates higher, as we are seeing now. Long term rates are determined by the market. Right now, it is not possible to lower all interest rates (short and long) at the same time. If Trump really wants to lower long term rates, he should be jawboning Powell to raise the Fed Funds Rate.

Indeed.

Trump is wrong in this matter. He has an inherent hate of the Fed as it put him out of business in 1981. He hates interest rates as all do in the real estate business.

If he inserts a “dove” and we get rate cuts with the inflation rate STILL above the false target of 2% and stocks, Cryptos, Gold at all time highs, the long end will spank him.

Replacing JPow won’t mean rates drop. FOMC still has to vote unless Trump fires half the voting members and replaced them with loyalists. If that happens we have a cataclysmic economic future that will have severe global consequences. I really doubt this will happen.

I’m also wondering home much of the housing slump is from people waiting out the market. Literally everyday I hear from people saying the rates are gonna fall and they are going to buy. I never respond but always think, “Just how much time do you have?”

I have a 6-digit down payment sum working for me from the sale of my former house, $1,500-$2,000 less — at a minimum — in housing costs per month by renting the equivalent house (which is also being put to work), and can be liquid in an instant.

I can wait a very long time — forever even, given current math.

and tariffs WILL PROVE to raise prices, but will they call it “inflation”?

Un-tariffed services have been raising prices. Not tariffs. Maybe someday, tariffs will raise prices a little bit, while services prices (67% of what consumers spend) blow out? And you’ll still be looking at the tariffs with your magnifying glass while services inflation is blowing up your budget in front of your eyes?

https://wolfstreet.com/2025/07/15/feds-nightmare-cpi-inflation-in-services-reheats-not-tariffed-while-inflation-in-durable-goods-apparel-footwear-tariffed-remains-cool/

RBC bank quoted a day or so ago, thinks there has been so much front- running in some stuff the full effect of tariffs won’t hit until late fall. I was surprised to read that, but then considered a product like Sketchers shoes, a high value, low volume item.

Let’s say Walmart orders monthly. If it thought it might be looking at a 50% tariff in a month, it would make sense to triple the order. This might result in extra cost to expedite the order. but you can get a lot of shoes in a shipping container, and it’s feasible to warehouse on arrival.

This option doesn’t work for most commodities: high volume, low value.

“The Fed can only lower short-term rates, which can drive long-term rates higher, as we are seeing now. ”

If the Fed chose to replace maturing short-term debt with 30-year treasuries, wouldn’t it affect long-term rates?

The Fed CAN and DID control long rates, to a great extent, with the QE and the massive purchases of MBSs (2.5 Trillion?)

They drove long rates to 4000 yr lows!

The history of the Fed is to stay out of the long end, but they jumped in big, and now sit on a nearly $1 Trillion paper loss.

Right on. There are two government bond markets. The short end where the FED operates to keep rates low and finance government debt, and the long end where rates represent reality. Reality says, inflation and default are real possibilities in 10-30 years.

Inflation yes, default no. Default is technical impossible. Inflation is a reality. And it does the same thing softly.

I watched an interesting interview by the Carlyle economist yesterday .

He stated that due to the massive A.I. capital spending programs by the dominant Mag 7 companies, they are no longer huge free cash flow creating companies.

As partially a result of that phenomenon as well as our enormous budget deficits, the projected government deficits demand on the private sector savings is expected to be 40%, up from 20% roughly a decade before .

Back in the bad old Bond Bear market years of the late 70s, chatter about the %of private savings needed to fund the government was spoken of widely.

I think this new development of the Mag 7 losing their free cash flow is another reason for the Bond Bear market to continue.

I actually agreed with some of the things the current president has done.

Trying to force down short term rates is NOT one of them. In this case, the Fed is right.

Amen!

I agree also. Trump doing a lot of things right economically, but trying to cut interest rates is not one of them.

Regarding residential real estate (and I am a long time professional REALTOR), ‘timing the market’ is folly. One cannot buy time. Reasonable and smart people learn one thing about life– move on. Fine— sit in your home with your 3-4% mortgage and ‘wait it out’. I’ll see you in Heaven and your kids will sell the home in a nano-second.

Right on—because housing only goes one way. Up. Up. Up. If you try to buy real estate at even a slightly reduced price you’re sure to miss out on the best investment opportunity ever.

And, don’t even think about transaction costs. They get lost in the rounding. Real estate and mortgage brokers add value beyond their fees. You couldn’t do it without them.

This is funny. I hope you meant it to be funny.

well – i sold my house in texas in 2022 through OPEN DOOR – no agent, no broker, no open house, no inspection, no hassle, picked my close date, closed on time, $ in my account in 24 hours – sold it for my price…what’s not to like?

Yes. I’ll let my death pledge run through its natural expiry in 2035 (I refi’d j to a 15 year, sub 3% in 2020). If I’m dead before then, the kids can do what they want. If I’m alive which I expect to be as I’ll be 60, well, I have a paid off house that’s quite pleasant to live in.

Fannie Mae stock was under a buck for many years and now it’s almost $9 a share.

What’s the reason for this, Wolf?

Speculation that they will be taken privately is the reason

From sheep, not wolf…

Fannie and Freddie are making money today and paying dividends to the Treasury. Big hedge funds believe Trump will privatize Fannie and Freddie which will unlock perhaps $150B in new shareholder value. If privatized, shares might go for upwards of $35. More so because the privatized company will still have tacit backing of the American taxpayer for bailouts of a private Fannie and Freddie like in 2008.

“More so because the privatized company will still have tacit backing of the American taxpayer for bailouts of a private Fannie and Freddie like in 2008.”

Wonderful – the US can continue to be a casino for the very wealthy

The ultimate in privatized gains and socialized losses.

History will definitely repeat itself if Fannie and Freddie go private again. They will overreach (because of their ignorance and arrogance), get in trouble, and will be bailed out.

Privatization. They might do it. They’ve clamoring for it for years.

My guess is the new Fed chairman will be a “low interest rate” guy appointed by Trump with the objective of getting rates down.

We’ll see how the bond market reacts. My gut tells me to bet on more inflation and irreversible fiscal & monetary policies.

Will continue to hold precious metal investments.

The chairman cannot set policy rates. The FOMC votes, and flipping the chairman just changes the chairman. Powell’s term as Chairman ends in May 2026, but his term on the Board ends in January 2028. So if he stays till January 2028, he continues to vote till then, and a new chairman, such as Waller, might not even change the votes. But there could be messy dissents by the chairman.

Wolf — what would you expect to see happen to inflation if the Treasury shifts bond issuance from long duration eg 20+ years to T bills?

Presumably this would cause long duration bonds to spike, yields to tumble and further stimulate borrowing and spending. Bessent is already talking about doing this bc the gov realizes the inconvenient truth about leaving it to the market on long duration bonds.

That shift started under the Yellen Treasury.

One thing the Fed will likely do – it has been talking about for a long time — is shed a big portion of long-term Treasuries and all of its MBS, and replace them with T-bills. This will absorb $3-5 trillion in T-bills, and shift $3-5 trillion in long-term securities into the market. So right now, there aren’t even enough T-bills to do that. And I think a shift by the Treasury to T-bills will match the Fed’s shift to T-bills.

What this means is that the proportion of T-bills will increase, but the Treasury will still replace the long-term maturing Treasury debt with new long-term debt.

I don’t think there is any impact on inflation of that.

Wolf – I didn’t really understand your response, aside from the FED replacing long-term debt with long-term debt.

If the Treasury needs to issue say $5T in a given year, what’s to stop them from offering all or most of that in T-bill auctions as opposed to 20 or 30 year bonds? And IF that were to happen, wouldn’t that effectively mean less supply of 20/30 year bonds and ergo lower long-run rates and everything that comes with that?

Having re-read your response, your view is that the shift from the FED will match the shift in duration from the Treasury aside from the fact that someone will need to absorb the $3-5T in long duration bonds. But what happens after that? Wouldn’t there still be demand for treasuries at 20, 30 years and therefore push the price of those bonds way up? Or is your view that no rational investor will want to buy those 20/30 year bonds if the yield falls to say 3% because of a dearth of supply because of this shift in issuance mix?

They can’t control the yield curve.

They try and sometimes it works sometimes not.

No reason to sell with rates under 5 percent on 80 percent existing mortgages and those lien free…Trump’s big number is 88 and Too late is 88 in gemetria so it’s just a script, like most things in the USA it’s scripted by paid actors…I call it the military industrial political entertainment complex…

They aren’t part of the show. They are the show. I’m thinking to try to make “money” as a “investor” following the script is necessary.

Most reckless Fed and Treasury….

“ According to the guidance released for the third quarter of Fiscal Year 2025 (April–June), Treasury anticipates borrowing $1,068 billion in the upcoming six months, which would be $72 billion more than it issued during the same period last year”

Many long moons ago, yardeni had a lengthy post, implying the 2yr treasury rate, was a good barometer of where the 10yr treasury rate would drift to, in the span of one year.

Even though so much seems broken in forward thinking, that’s within the realm of possibilities, like a10y around 3.95% — but, that measurement, like so many others, is being distorted by unprecedented treasury issuance, for unprecedented debt and servicing costs. I guess, if that plays out, mortgage rates decline, maybe — seems like recent relationships are not in sync.

Maybe there’s a continuation of Schrödinger Cat ambiguity, where speculators lust for cheaper yielding treasury debt, but, whatever that stupid demand is, there’s a huge supply of people that won’t support the stupidity. Betting on the equilibrium of volatile chaos seems like a sure way to burn cash.

I can’t shut up — think of this backdrop — we’re apparently supposed to run a hot economy, with tax cuts, biblical deficit with massive interest payments, wait for tariff outcomes, which in one way or another, will increase inflation, and then we execute an aggressive Fed rate cut program, to help stimulate demand, while the dollar falls and treasury yields decline.

Kinda seems like a Great way to bankrupt the casino.

This is exactly what I see happening to be honest.

In every possible scenario the answer seems to be inflation inflation inflation.

You all keep predicting tariffs will cause inflation and ignoring that virtually all of inflation today is in services which have no tariffs whatsoever. There is a whole host of low to no information drive-by commenters here who never even read the posts and just post whatever nonsense, backed up by nothing.

The Fed should do nothing for a few years. 5% long bonds are fine. 6.5% mortgages are fine. People need time to adapt to the situation and let prices clear. The constant picking and fidgiting leads everyone to say “just wait until..” and that leads to frustration and anger. Housing prices will find their equilibrium in a steady rate environment. Over time short rates might drop a bit on their own as people see a smooth yield curve and can plan for more than the next quarter or two.

How about no Fed chair after Powell for a while??

Like it. No one, but no one else has this Board, whose multiple members chime in with different views every week. You have to have a head of the Fed, which is the US central bank, but he doesn’t have to head a talking shop. One negative effect; media lay offs, as there wouldn’t be 12 (?) cups of tea leaves to read every week.

The Federal Reserve does a vast array of things other than to set a few very short term policy interest rates. Are you not aware of that?

Are TIPS a useful tool to look into the bond market?

It was just pointed out to me that the “real yield” on 30-year TIPS was in the 2.6% range. If I read the charts right, that’s something like a 20-year high.

TIPS have been a pretty good deal for new buyers recently, better than in decades. 10-year TIPS ran through the auction this week at a yield of 1.99% (interest to be paid), plus CPI-based inflation compensation. So if CPI is about 3% over the long term, the TIPS will yield 5%. In a year when CPI is 6%, the TIPS will yield 8%. In a year with CPI at 0%, they will yield close to 2%.

The interest yield used to be negative for many years. I’m not sure what this 2% interest yield indicates, maybe overconfidence in the market that inflation will go away, and so there is less demand for TIPS now than in the years before, and so they’re not bidding them up the prices (which pushes down the yield) like they used to? We couldn’t resist and nibbled on those TIPS at the auction (in tax-deferred accounts so we don’t have to mess with the tax situation that TIPS produce).

There seems to be close to a consensus that it would be a disaster if Trump gets his wish and forces the Fed Chair out. In any other context if the CEO’s wish is considered a disaster, he is not a desirable CEO.

Or is the rationale: ‘It’s just the economy’?

Nick – mebbe more akin to: “…forget it, Jake. It’s just…Chinatown…”.

may we all find a better day.

The power of the US dollar is in its reliability and predictability. People rushed away from emerging markets in 2008 and into dollars for this very reason. The stability of the currency is wholly reliant on the feds ability to use said rate cuts/increases as a tool to protect its stability. Politicizing rate cuts is his goal and it removes the most important tool they have. This is why forcing out the fed chair would be a disaster, it puts the future stability of USD into question.

I think Trump wants to drive us all out on the risk curve, into the casino. Deregulation of stock disclosures, crypto, gambling (“event contracts”), plus loosening rules on retirement account investments, are other signs of this. Lower rates would fit this like a glove.

Seems like for foreign buyers there is always some element of currency exchange risk present. What might be a good rate today might be different 10 years from now, but only matters I guess if they want to get money back in their currency eventually.

The Fisher Effect, “tendency for nominal interest rates to change to follow the inflation rate” is at play. The distributed lag effect of money flows, the proxy for inflation, peaks in September, but doesn’t materially fall until the 2nd qtr. of 2026.

In the last couple days T- Rump was on camera answering journalists’ questions and said exactly this: “We have no inflation. We wiped out inflation”

He truly is clueless! I guess that’s much easier to fool yourself into thinking when you’re a billionaire!

Just like the Dems found out… You can’t spin inflation!

People see it almost every day. Saying it doesn’t exist just kills overall credibility… Which isn’t in abundance in Washington.

Appreciate and 100% agree with the first few paragraphs wolf. The Fed has no reason to cut rates if you look at the data and the bond market is telling them the same thing. No cuts yet!

Could that change as early as Friday? Possibly, but no definitive signs of labor weakness yet!

Inflation is a rich man’s grift!

Love my fixed rate debt at 3% indeed.

There are some lush yields out there. Private mortgages yielding 10%+, etc.

would rather own that than the stock market.

Home values have dropped by millions of dollars over the last three years in the Greater Toronto Area, a new analysis found.

Ten neighborhoods saw the median sale price of a single-family home fall by 40 percent or more since 2022, according to new research by Wahi, a Canadian real estate listing website and app.

Houses in Canada reached their peak values in April 2022, after two years of historically low supply and rock-bottom interest rates spurred by the COVID-19 pandemic.

‘Prices for single-family homes have held up better than condos, but Wahi’s latest analysis shows how much market trends can vary from neighborhood to neighborhood,’ Wahi CEO Benjy Katchen said in a statement.

Four neighborhoods in Brampton, the third largest Toronto suburb, were in the top ten in terms of largest percentage drops in value.

They included Huttonville (-53 percent), Vales of Humber (-50 percent), Northwood (-44 percent), and Westgate (-40 percent).

These areas are among the hardest hit, but the downward trajectory is widespread, with 289 of the 344 neighborhoods that Wahi analyzed having lower prices this year than in April 2022.

Windfields, an upper-middle class area northeast of downtown Toronto, had the biggest home price decline as a raw number.

The median sale price of a Windfields home declined by $3.1 million since 2022, when a property cost a whopping $6.3 million.

Windfields saw a $1 million bigger drop than Wanless Park, the next biggest loser at a $2.2 million decrease over the same period.

I did some back to school clothes shopping for my kid yesterday and prices have definitely risen. I’m talking places like Old Navy, Target, Macys, etc. I talked to other people who were also shopping and we all noticed the higher prices. Maybe hasn’t shown up in the government charts yet, but it will. We weren’t all having a collective delusion.

We just came back from eating out, and prices of all-American foods have definitely risen at that restaurant compared to three months ago when we were there last time, and by a lot. My electricity rate has jumped for the second time in less than 12 months. My broadband jumped by 60% last month. None of this is tariffed, it’s just plain old inflation in services where consumers do nearly 70% of their spending and it’s blowing away the inflation in a few imported goods that even have price increases. New vehicle prices are still going down, and some of them are tariffed. That’s also a biggie, far bigger than shoes and apparel. Spending on goods outside of food and gasoline is just a small part of consumers spending. Motor vehicles is the majority of that. So go take out your magnifying glass and look for tariffs on T-shirts while services inflation is blowing up your budget right in front of your eyes.

But picking up nickels in front of the steamroller is fun. I’m quite adept at it……………… and it’s a really hard habit to break.

I think it’s more of a last straw thing. I too am paying more for all of those other things as well, including groceries. I shudder to think what the new health insurance premiums for 2026 are going to be.

If your electric bill went up, you’re witnessing inflation in goods and service.

Your electric bill varies depending how much of their product you use. They also bill you for delivery of that electricity (a service).

Inflation is rampant in products as well as services. New vehicle prices are only deflating because they went through the roof (just like housing did) starting five years ago, to the point of no longer being affordable.

Wolf,

US Treasuries is issuing more and more T-Bills. This is helping them to keep long term rates in check. Even FED is talking about moving their balance sheet towards more Bills than Notes and Bond.

My question is: Can FED can control shorter end of the curve for UST? Similar like Operation Twist except for Short Term.

I understand FED sets overnight rates (one of those 5 rates they set). But when FED participates in T-Bill auction, do they expect UST to pay them at FED Funds Rate or Market rate? Are they competitive buyers or non-competitive buyer?

What if FED says we will lend to UST at 1% for all T-Bills, it will save lot of money for UST. I mean what will stop UST from making most of new issuance to T-Bills and FED will buy those Bills at very low rate. I am sure Warsh and Bessent will come up with creative thinking in order to screw us all. that’s what Warsh is indirectly proposing.

Till Powell is there, I have some hope of doing the right thing. I know some people may jump on this. Sure FED made mistakes. But QE didnt start after Powell took over. Even he tried to raise rates in 2019. It boom rang. But after inflation went crazy, this FED has deviated from their inflation goal. Most important he has clarified 2% goal remains same, Speed and urgency can be all debated. Very few even believed FED will do this much QT too. Still they did. In spite of all the political pressure, he has done right thing so far.

The Fed has for months been talking about getting rid of all its MBS, including by selling them, and reducing its holdings of longer-term Treasury bonds and notes; and after the balance sheet drops to the desired level, replacing the MBS and the notes and bonds with T-bills. That would take $3-5 trillion of T-bills, and the market will have to absorb $3-5 trillion in MBS and Treasury notes and bonds. But now there aren’t even enough T-bills out there to do that. So the Treasury department would have to issue $4 trillion in additional T-bills over the next few years so that the Fed could use those to replace $4 trillion in MBS and Treasury notes and bonds.

Two candidates for the the chairman job – Waller and Warsh — have already talked about it in those terms.

If the Treasury is buying back long term securities at a discount, wouldn’t this cause the overall debt level to decline? Basically booking short term gains at the expense of loosing the future lower interest expense.

Yes, buying back debt at a discount to face value reduces the overall debt by the amount of the discount. But the amounts are small, usually in the hundreds of millions per bond issue they buy back per auction. They buy back usually several bond issues. And so the total amount bought back per week ranges between $2 billion and $8 billion or so, minuscule, compared to the $36.7 trillion in total debt outstanding. And yes, they’re replacing the low-interest rate debt at a discount with higher-interest rate debt at face value, so the interest expense stays about the same. But the fact that there is a buyer out there for small portions of this otherwise fairly illiquid debt helps push down long-term yields.

Ok, forget (for the time being) what Uncle Wolf posted— overall it’s better information than anything, anywhere, but what UW is missing, is the far bigger theoretical snapshot of what’s actually unfolding:

“ Just as in a tornado, where debris is often found spinning about the vortex, so in a black hole, a dust torus surrounds its waist”

That’s the multi-generational, multi-transnational journey that money is.

As the deficit black hole expands, it needs more fuel, which is drawn from the dust torus (treasury issuance) — and as the black hole — which brings us back to overall real world accounting logic:

“Increased Accretion: A larger black hole with a stronger gravitational pull can draw in more material from the torus, increasing the accretion rate”

Hence, as our deficit black hole expands, it needs more treasury issuance fuel, which is why the future value of treasury returns is diminished — obviously, dilution is the result of deficit expansion, which is why the speculators obtaining treasuries, will require more future cash return.

The idea of a dust torus is interesting, because what we’re witnessing, is a case of wool being pulled over the sheep’s nose — it’s as if, were to believe, that by increasing the amount of dust torus fuel (treasury issuance) that fuel will smoother the expansion of the black hole deficit —- versus, proving a larger amount of fuel to encourage the black hole to expand at a faster rate.

Looks like you’d be better off not using theories of astrophysics for guidance in finance.

Redundant, way too many metaphors. Just speak your mind clearly and concisely. One of the most useful things I learned in college is not to use physical science to try to understand social science. Actually there is little science in the analysis of social action. The “law” of supply and demand is about all we have, and that can be perverted. Social “science” is just a bunch of statistics.

GDPnow on 7/25 is @ 2.4%. M2 is growing at a 5 percent rate. But that masks the composition of the money stock. Means-of-payment money is growing at a 9 percent clip. The FED is not tight.

If you reduce policy rates lower than NIMs then bank credit will accelerate.

If the government isn’t growing both GDP and employment will look weaker than reality. Private sector looking just fine.

Great piece again Wolf – you’re killing it with these posts, and generally the discussion is civil and non-political which I love!!!! Keep going!!!

‘At the long end the market is nervous’. As it damn well should be! I feel like all the action is going to be at the long end and I have my eyes glued to the US 10/20/30 and JGB 30 year daily. Any stress is going to show up there first.

Some commenters remarked that the Fed can not influence the long end, only the short end. I beg to differ.

The Fed indeed can only control the long end via rate hikes/cuts, but it very much controls the long end via it’s balance sheet holdings aka QE/QT.

The 30 year is almost at 5%? Really? That’s with almost 7T of all sorts of holdings on the Fed balance sheet! What would that rate be if it didn’t suck up those worthless bonds noone wanted at the time.

Trump will get his lower rates by hook or by crook.

The Fed is the enabling parent who let’s the kids spent. With the ‘Mississippi’ level of debt issuance coming, who is going to absorb it? Is the Fed really going to let rates spike to ‘teach the government’? Then, why this time? Not.Going.To.Happen!

We are getting QE before any rate cut ever sees the light of day.

I ask my friend what would have happened in 2003 when the US declared war on Iraq. Fellow countrymen where shouting ‘USA USA USA’. What if the cost had been calculated upfront, and rather than inflate it away via debt issuance, the tax man would knock on everyones door to collect $6,300 for every person living there. How many would be changing USA USA then?

That’s my point – with the Fed, we have a system where we can have AND social spending AND a warfare state AND do massive tax cuts. It’s all courtesy of the Fed, without it it would not have been possible, and like any normal house hold it would have to make hard choices about OR food OR medicine OR that vacation, but not all.

There should be no Fed at all, and if there is one, they should only be allowed to set interest rates.

I still prefer Jim Grant’s take: The demand for money should set interest rates, interest rates should not set the demand for money.

Disclosure: Hard assets only. Can’t wait for this to implode.

No, Trump is not going to get lower short term rates from the Federal Reserve at any time soon when the risk of inflation keeps increasing.

Money has a time cost. That time cost is called interest. That time cost determines the demand for money.

From the socialist commies at IMF:

“At the start of 2025, the consensus forecast among economists was predicted 2.6 percent global growth this year. That number is now down to 2.2 percent, nearly a third lower than the average that prevailed in the 2010s.”

Moar and more energy going into debt servicing, versus output into stuff for humans — which is probably fine, since we’re heading into a robotic future — maybe that’s where everything balances out, with wealthy people accumulating robots, while everyone else goes by the wayside.

The Fed is caught between a rock and a hard plate. It they lower short term interest rates now, the ones they control, like they did just before the election to try to help the Dems win the election, the long term rates will go up including the 10 year Mortgage Notes, 30 year notes, and further hurt the housing financing market, CMBS refinancing, etc. If they stay pat they will be get pounded by the current administration like there is no tomorrow. They are in a LOSE LOSE situation. J Powell put us in this position. He should do the country a great service by announcing his resignation. A new Fed chief should immediately be appointed. There are plenty of excellent candidates. The first task of this new Chair of the Fed should be to fire half or more of the Federal reserve staff that put forth these failed policies and put us in this no win situation.

No.

I agree. Fire them all & let Newsom put them to work on his high speed rail boondoggle. Should be able to get that out of the billions & into the trillions.

Never got a good explanation as to why we had to go to negative “real” mortgage rates and goose the housing market. Totally unnecessary terrible policy.