Homebuilders cut prices, bring on supply; profits plunge back to earth. Medicine this overpriced housing market needs.

By Wolf Richter for WOLF STREET.

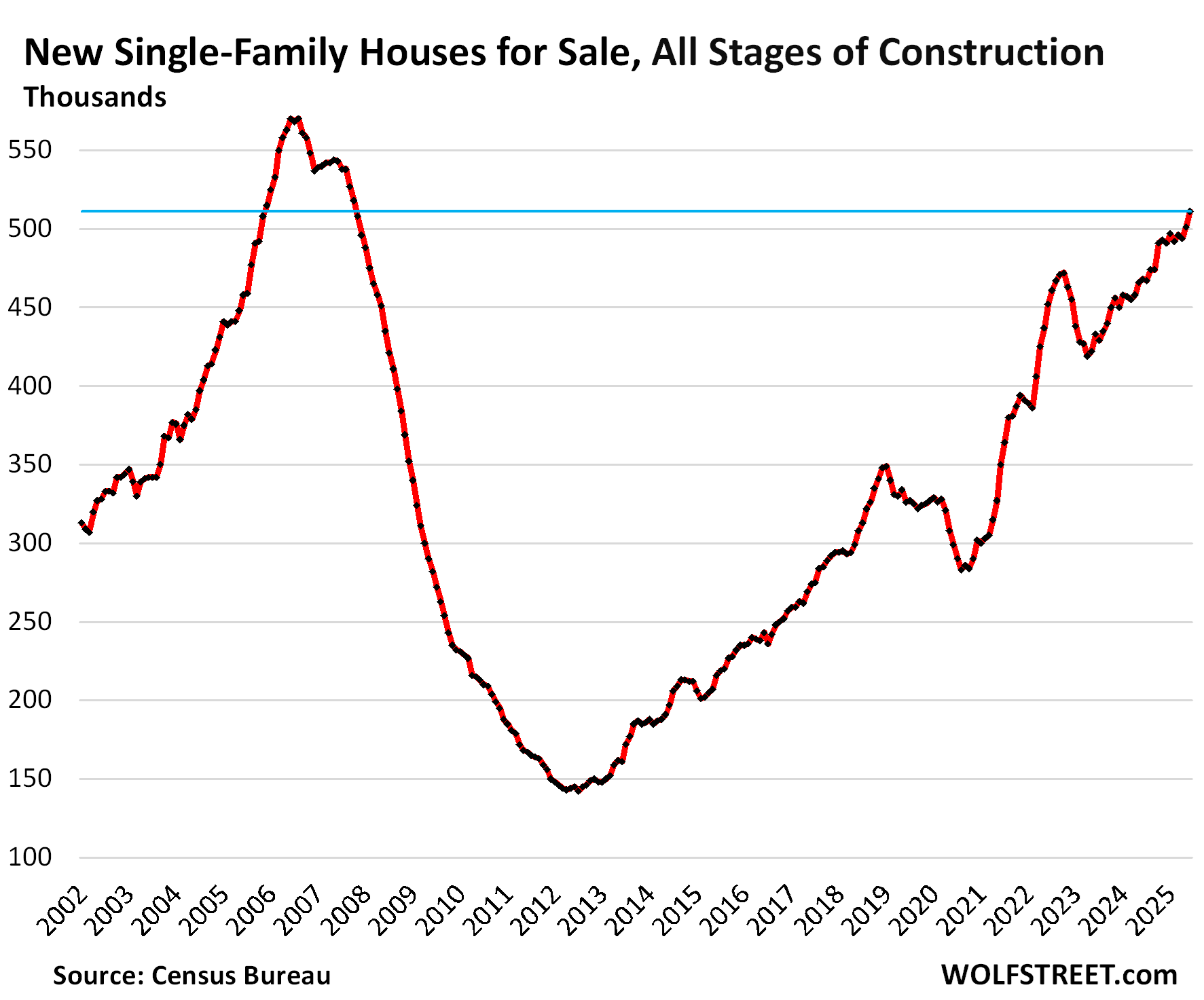

New single-family homes for sale at all stages of construction spiked to 511,000 homes in June, the highest since October 2007, when inventory was falling during the Housing Bust as homebuilders, struggling to stay alive, were cutting back construction.

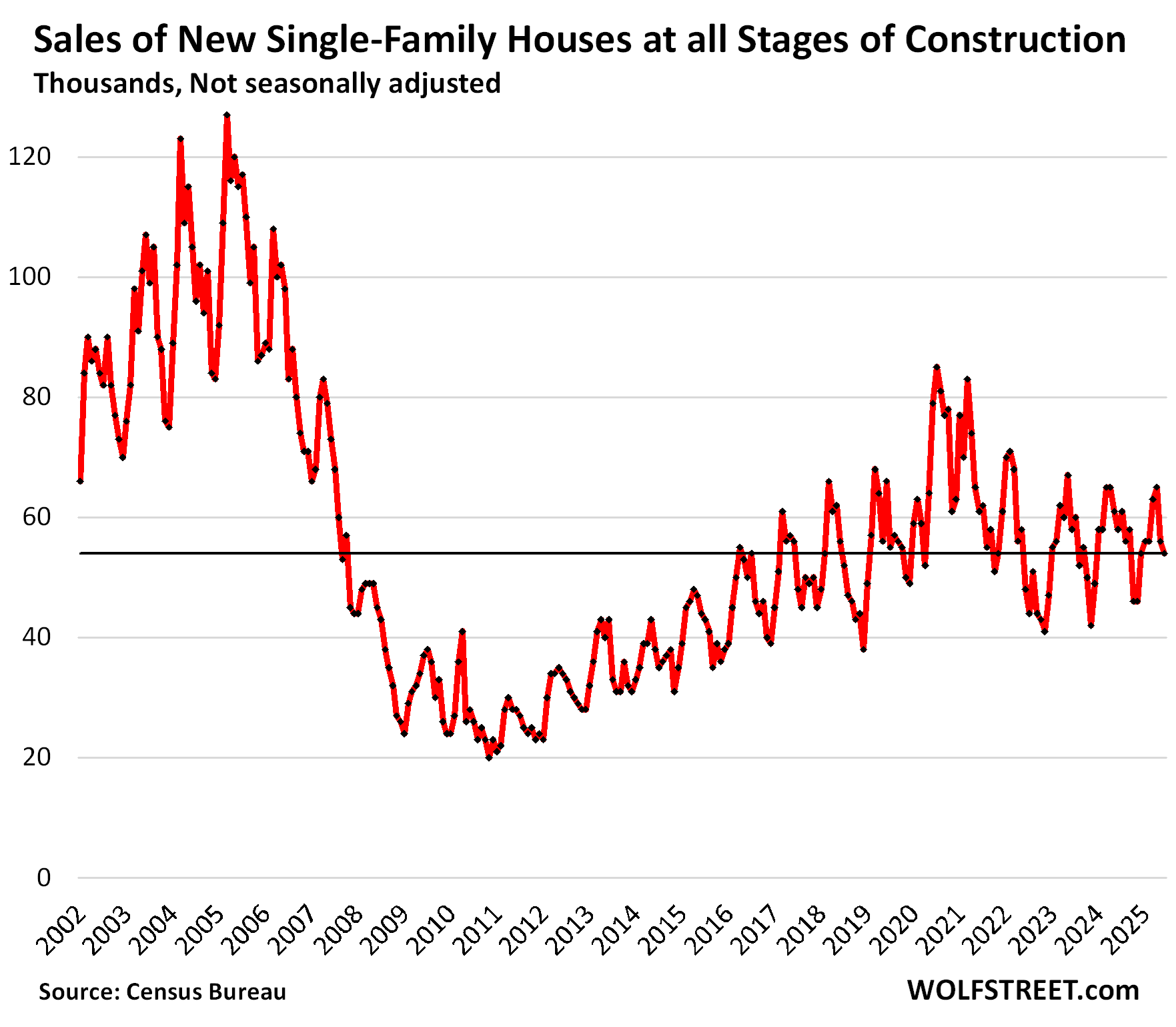

Prices fell, according to Census Bureau data today, and sales fell too but were still in a decent range, unlike sales of existing homes, which plunged.

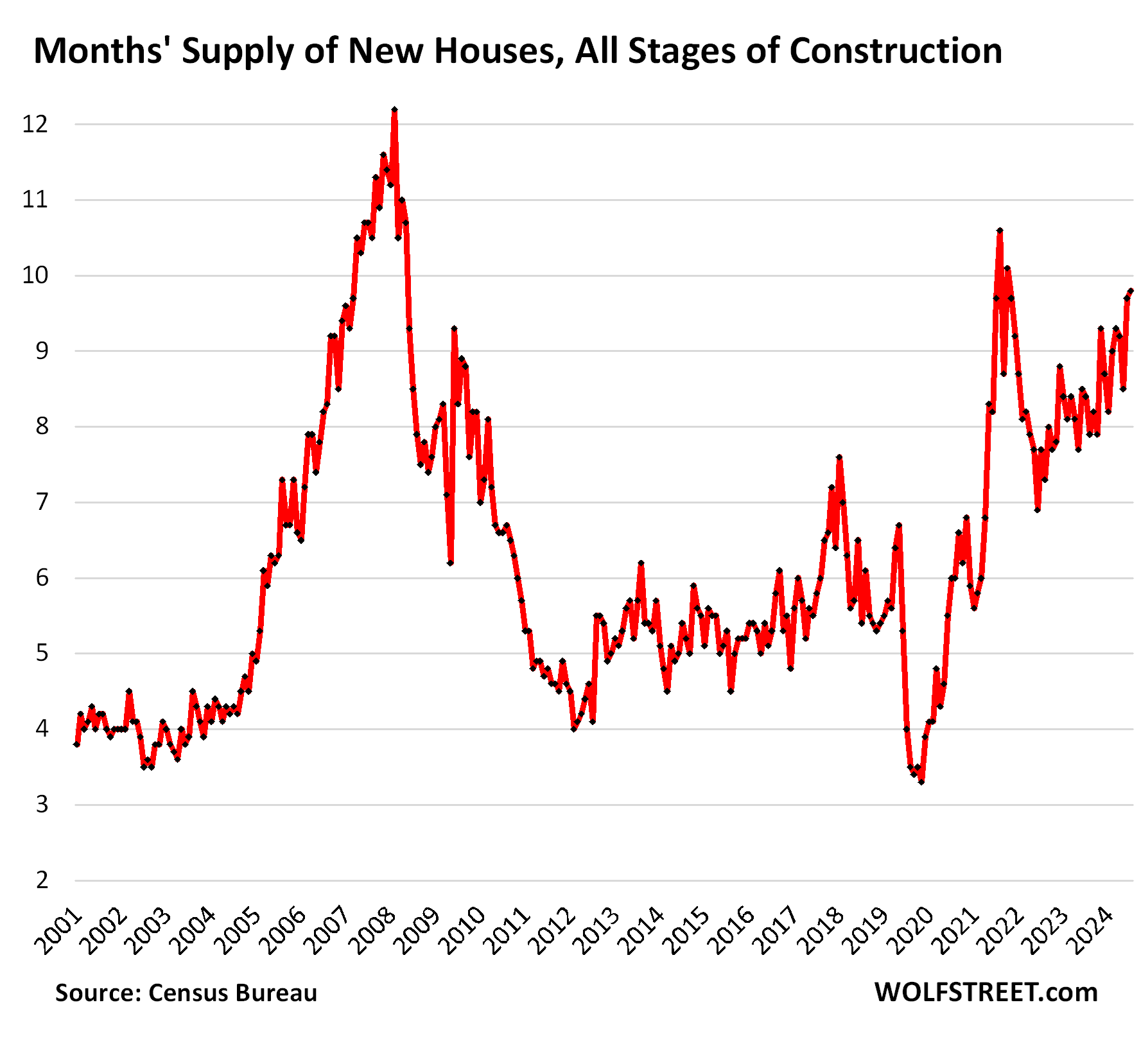

Supply of new homes hit 9.8 months in June at the current rate of sales. A glut of new houses on the market is exactly the medicine this overpriced housing market needs. Bring on the supply!

The fictitious real-estate-hype meme that there is a “Housing Shortage,” bandied about endlessly in the media to pump up prices, needs to be flushed down the toilet, where it belongs, with a double-flush to make sure all of it goes down.

Sales of new homes fell 6.9% year-over-year to 54,000 contracts signed in June, and were down by 1.8% from June 2019.

So compared to existing homes, where sales have plunged because prices are too high, sales of new homes are still in a decent range. Homebuilders cannot decide to not build and not sell while waiting for better days. They have to maintain their businesses, and they have to find the price points at which they can sell, and they sacrifice some of their big-fat profits to get there.

These sales are tracked by signed contracts, not closed sales. A substantial portion of these deals will fall through before closing. For example, D.R. Horton disclosed when it reported earnings two days ago that 4,837 orders were canceled in the quarter, while it booked 23,071 new orders in the quarter.

The publicly traded homebuilders have been singing the blues in their earnings reports. And their shares have sunk from their highs last fall: DR Horton [DHI] -27%, Lennar [LEN] -41%, KB Home [KBH] -37%, PulteGroup [PHM] -21%, etc., despite the blistering surge of the overall market over the same period.

In the earnings calls, homebuilders have been talking about stimulating demand with big incentives and costly mortgage rate buydowns; about bringing costs down; about lower sales, lower profit margins, and much lower net profits.

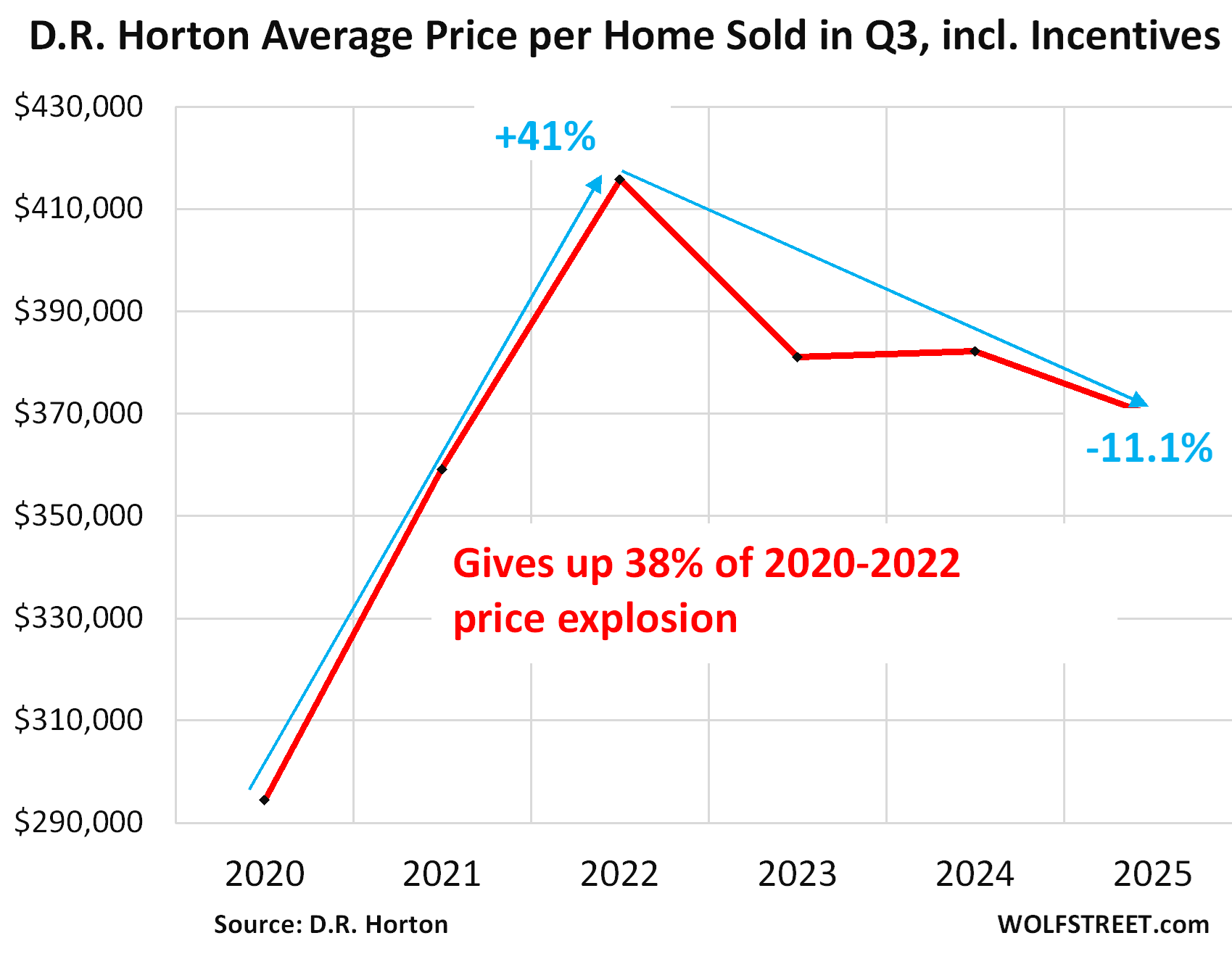

D.R. Horton, the largest homebuilder in the US, reported earnings on July 22 for its fiscal Q3 ended June 30. Net income plunged by 24% year-over-year to $1.02 billion. Compared to Q3 2022, the peak of the price-spike era, net income plunged by 38%.

Order backlog fell 16% year-over-year to 14,075 homes; in dollar terms, the backlog plunged by 19%. Closed sales declined by 7% year-over-year to $8.56 billion.

And the average selling price per home sold declined by 3.3% year-over-year, and by 11.1% from the peak in its fiscal Q3 2022, to $369,600.

But during the home price explosion between its Q3 2020 and Q3 2022, D.R. Horton had jacked up prices on average per home by $121,000 or by 41%. At the time, homebuyers were eager to pay whatever, the Fed’s free money acting like a virus that had turned their brains to mush.

Since that peak, D.R. Horton has reduced the average price per home by $46,200; meaning it gave up 38% of the 2020-2022 price spike. Average selling price includes the incentives:

D.R. Horton still made over $1 billion in net income in the quarter, so there’s plenty of room left to give up more of that price spike. And it said as much in the quarterly filing: “We expect to maintain an elevated level of incentives to support demand and may increase them further…”

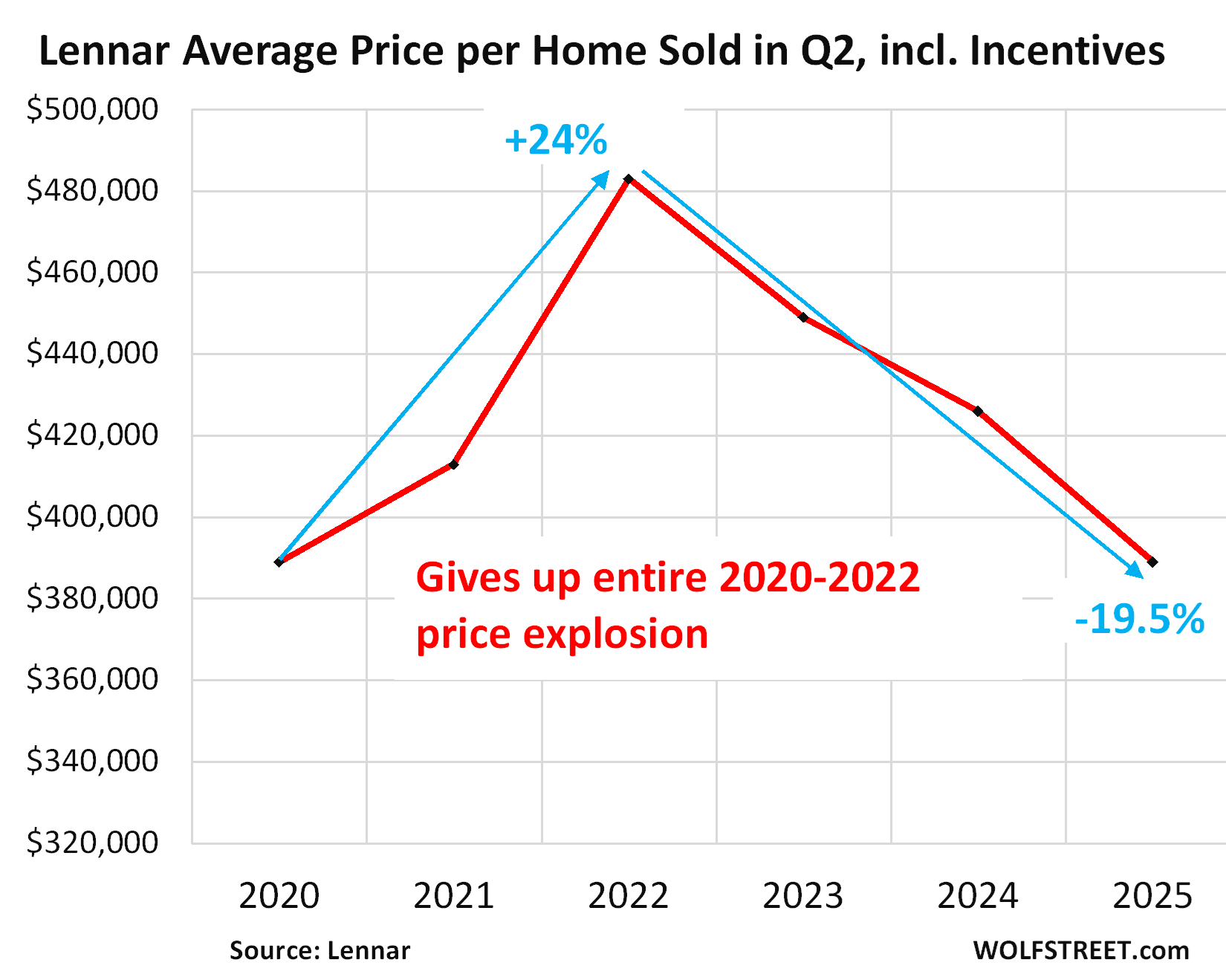

Lennar, which reported its fiscal Q2 earnings in June, disclosed that its incentive spending jumped to 13.3% of revenues, “primarily” due to mortgage-rate buydowns, the highest incentive spending rate since 2009.

Lennar’s average sales price dropped by 8.7% year-over-year, to $389,000. Compared to the price explosion peak in Q2 2022, it dropped by 19.5%, and is back where it had been in Q2 2020, having given up the entire 2020-2022 price explosion.

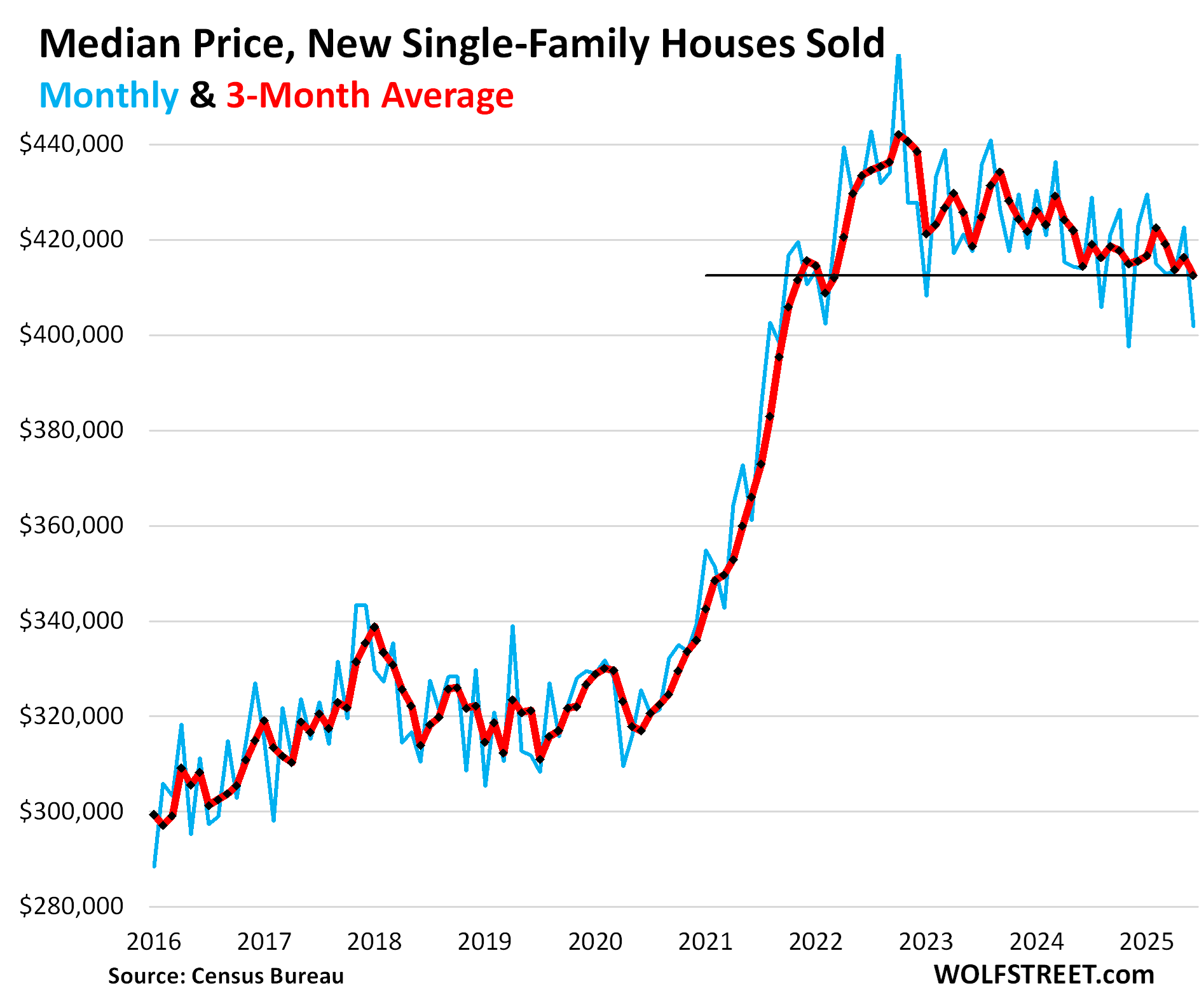

But incentives are not included in the median price.

The median contract price dropped by 2.9% year-over-year to $401,800 in June (blue in the chart below).

The three-month average, which irons out some of the month-to-month squiggles dropped to $412,600 (red), down by only 0.5% year-over-year and by 6.7% from the peak in late 2022.

But the Census Bureau tracks sales prices of new houses by the prices in purchase contracts that buyers signed, which do not include the costs of mortgage-rate buydowns and some other incentives, and thereby overstate the effective sales prices and understate the effective price cuts.

Inventory for sale by region.

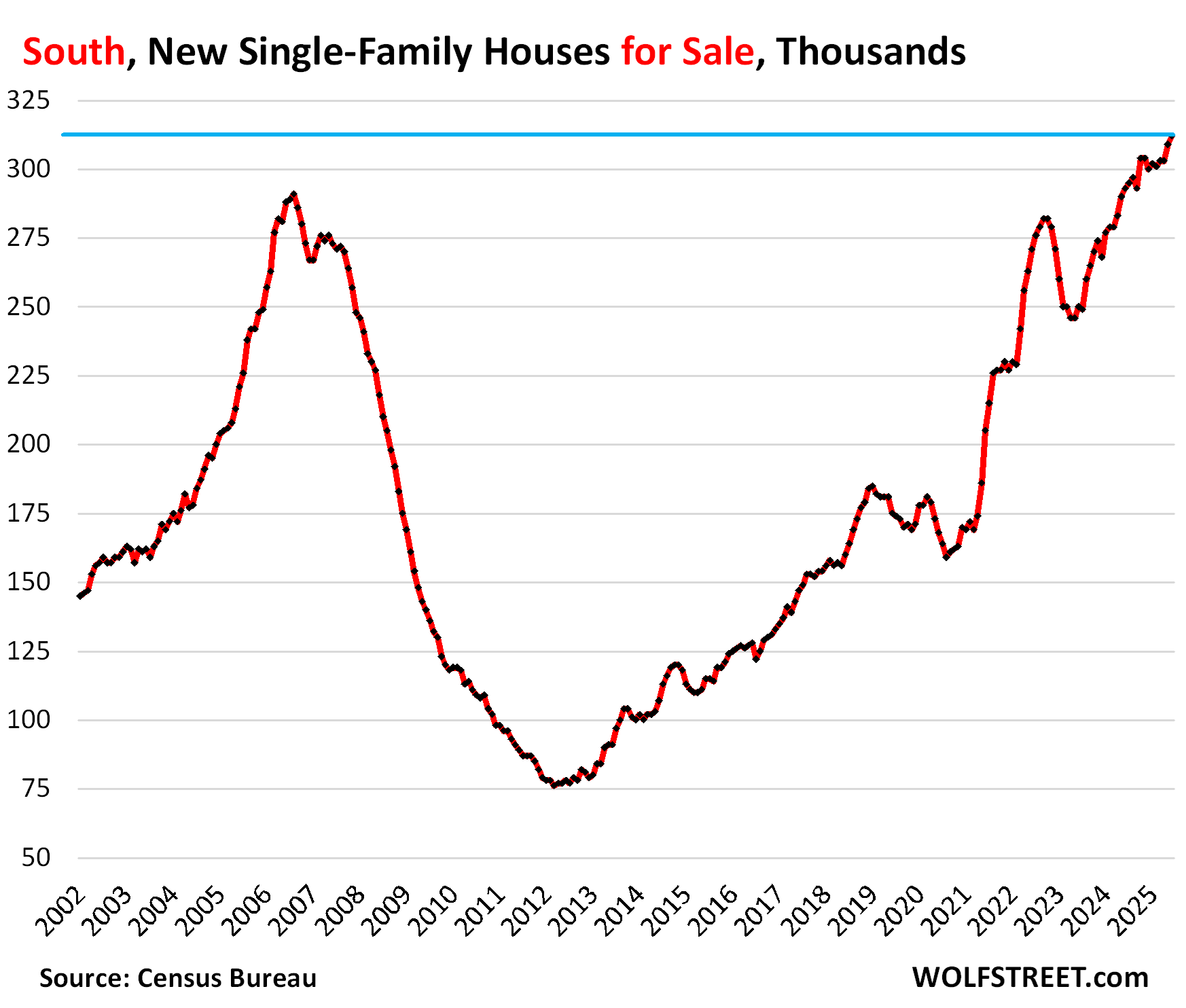

In the South, dominated by Texas and Florida, inventories of new houses for sale spiked to a record of 312,000 in June, up by 6.5% from the already above-Housing-Bust-peak level a year ago, and up by 78% from June 2019.

The Census region accounted for 61% of total US new-home inventory, and also for 61% of total US new-home sales (a map of the four Census regions is below the article at the top of the comments).

Sales dropped by 6% year-over-year to 33,000 new homes, and by 15% from June 2019, despite the massive incentives by homebuilders.

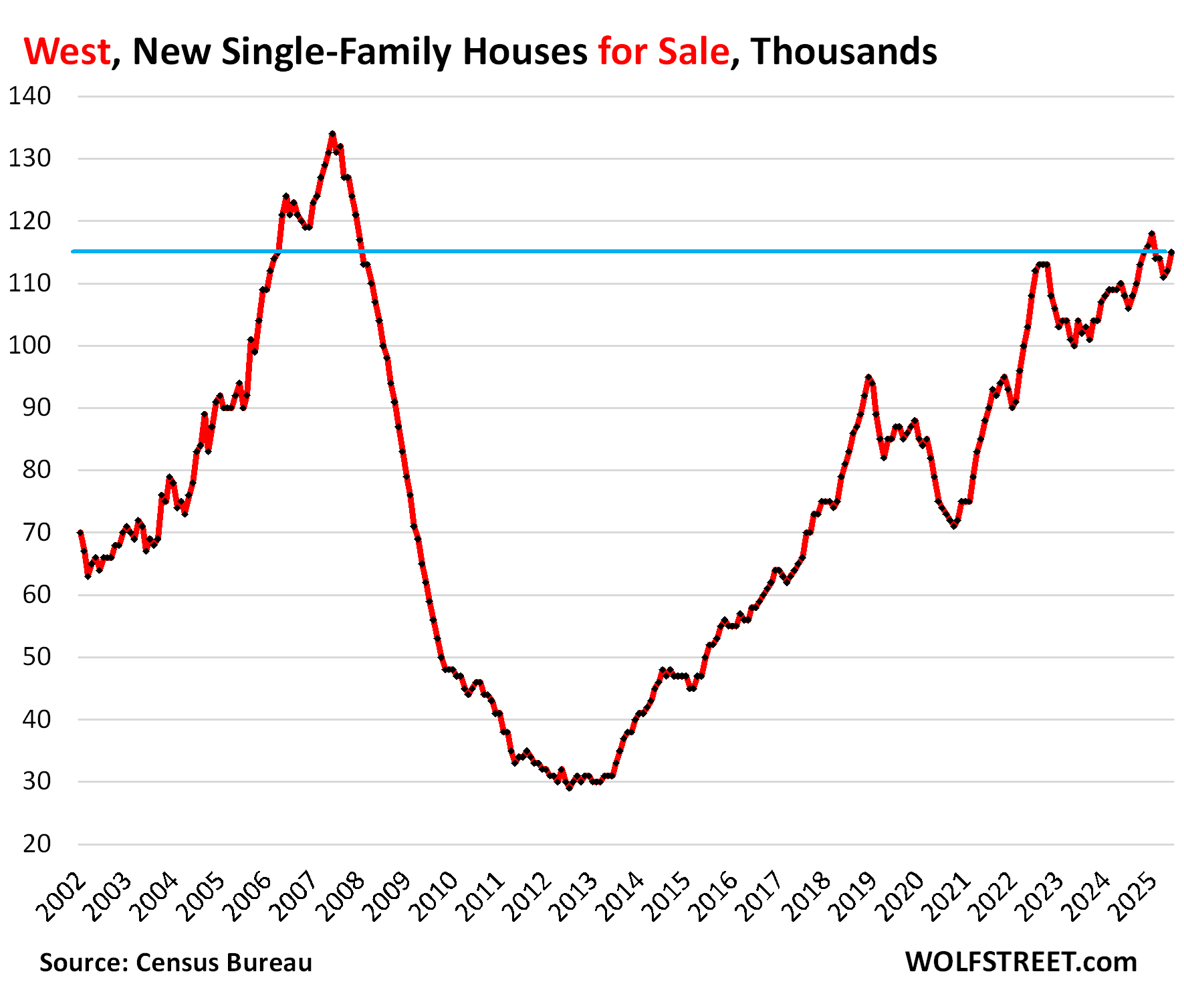

In the West, dominated by California, inventories of new homes for sale jumped by 6.5% year-over-year to 115,000, up by 35% from June 2019.

Sales in the West fell by 14% year-over-year and by 33% from June 2019, to just 12,000 new homes. The West accounted for 23% of the total US inventory and for 22% of total US sales.

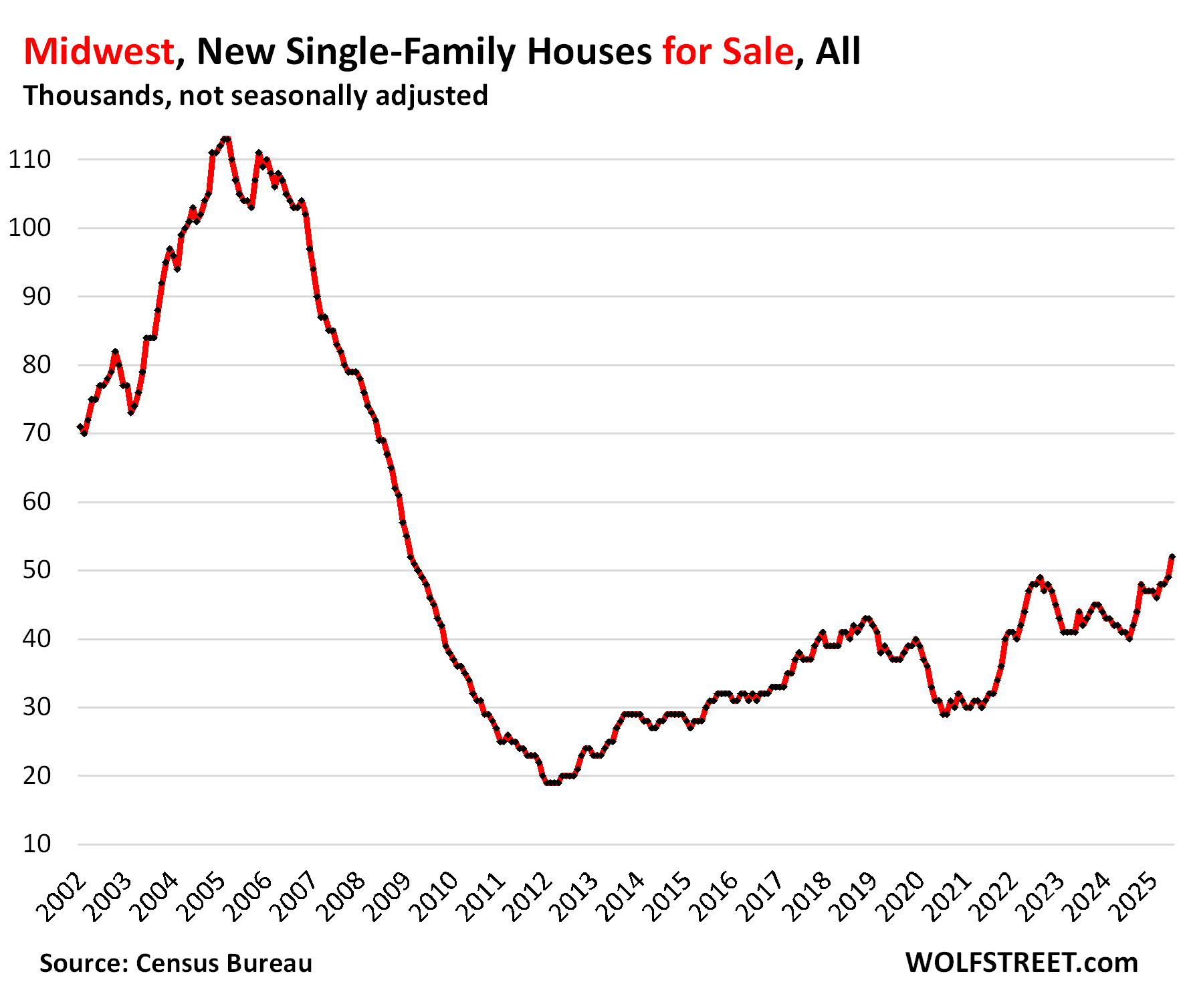

In the Midwest, inventories of new homes for sale spiked by 26.8% year-over-year and by 41% from June 2019 to 52,000 new homes, the highest since February 2009:

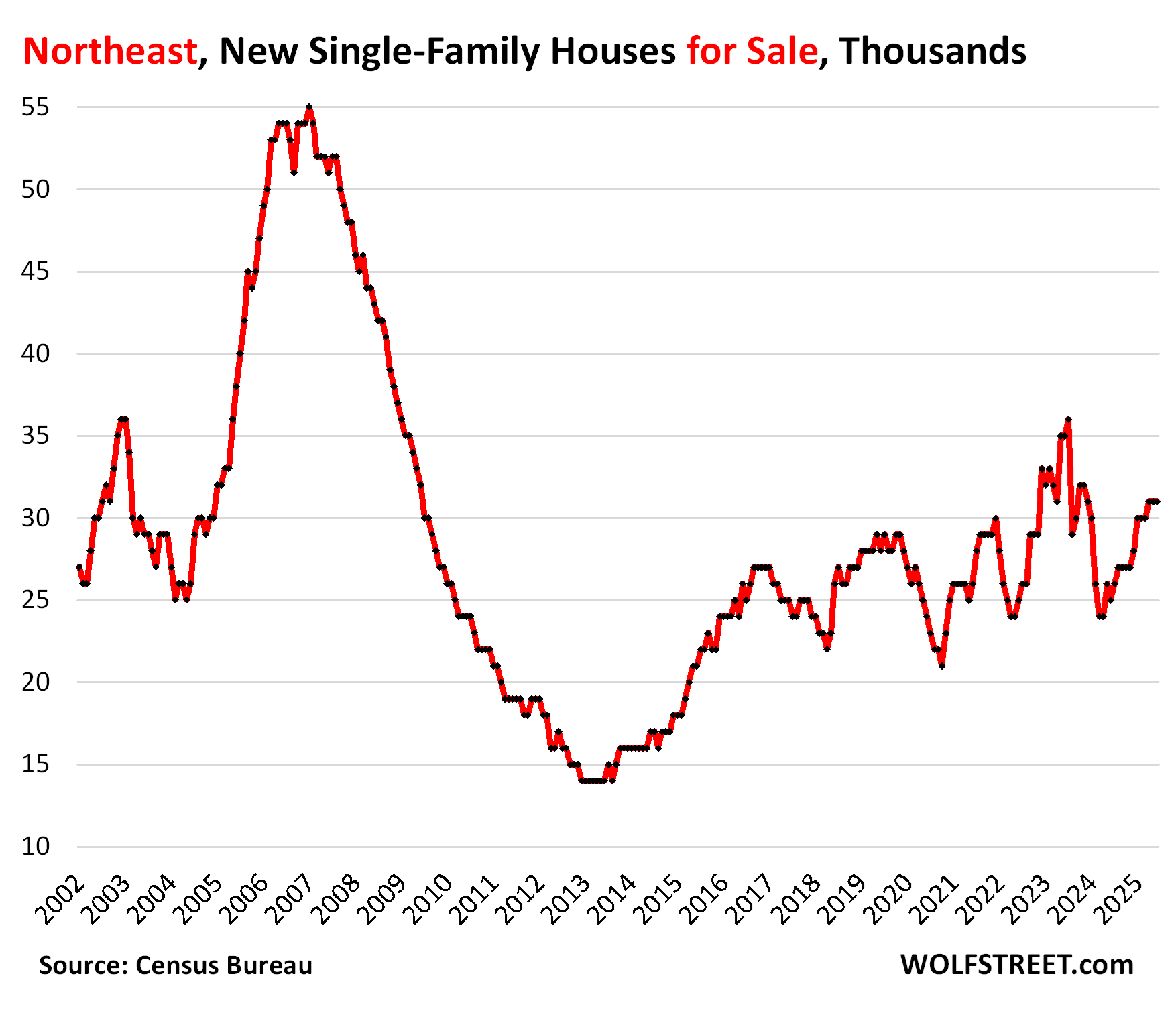

In the Northeast, inventory jumped by 24% year-over-year and by 11% from June 2019, to 31,000 new homes.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The promised map of the four Census regions of the US:

I suppose if you add in all the commercial real estate price reductions, it really needs a slow triple flush ;^). Any (wise-ass?) guesses about how all this excess real estate value swirls down the drain into the black hole of nothingness? How long might it take? When/where might it end?

Seriously, this stuff just keeps getting more and more frightening. Thanks again.

Ehh. This will be a blip. Americans are spending more and the stock market keeps pushing ATHs. There is plenty of money to soak up these homes without it craterin

Why do people think the stock market has anything to do with the housing market?

Historically It’s definitely correlated for luxury housing. The definition of luxury houses changes by zip code. In park city Utah, under 3M is still selling and over 30m(expensive houses for the zip code) still has interest and showings, but the 4m to 15m range not selling so fast and not many showings. In April when the stock market plunged people backed out of housing contracts/deals. During Covid people moved to ski resort towns now some of those people are getting called back to an office in a big city and listing/selling. If the wealth effect rolls over in housing it may trigger a sell off in the stock market, watch market, Porsche gt3s, Birken purses and all the nonsense that people use to stay addicted to this materialistic world of building wealth. In my eyes, Essentially it’s a credit bubble that produced too much liquidity that needed a place to be stored to keep values going up to satisfy the credit obligations and for people’s egos. So many Smart people are obsessed with building wealth instead of making a difference in this world. When the liquidity tide goes out the follies will be evident. Bubbles may last over a decade but eventually they run out out of fuel. All assets are like mountain climbers roped up to one another on a rock face, when one falls eventually others get pulled down. Free soloist are free, no ropes to make them slaves. Simply, Attached to being kind to fellow humans and living a good and aware life. Ha lol. I don’t know why we are the way we are. Peace in your mind, heart, soul, feeling connected that’s true wealth.. May we all enjoy and find the reason we are here.

Look at the 2009 experience. When stocks drop, people have less wealth to buy RE, and vice versa.

I think a better question is, why do people think RE is a stand alone asset not impacted by wealth effect?

As long as investors have a strong say in both markets, it seems they will be somewhat correlated with some lag time.

Dan

Right, interest is the price of credit, not the price of money.

So why is inventory stacking up as we see all time highs in the stock market? Your idiotic theory implodes on itself – try using your brain next time

I think the thing to look at is inventory piling up despite all time highs. What will inventory look like if the stock market tanks?

Don’t worry Greg. The current USD system is designed to print USD into existence at multiple levels with no reserves required whenever people swipe credit cards, get mortgages, or the US govt issues debt. Even if the USD prices of houses crashes the govt officials will borrow a quadrillion dollars and hand it to their buddies to buy up all the properties at lower rates than consumers are ever offered “save us” from low USD housing prices. They have your back don’t worry.

Thank You for the report. Prost 🍻

It would be interesting to have that first graph showing the total inventory of homes for sale with the median home sale price to visualize the relationship between those two data points. Seems like prices are still stubbornly high regardless of 7% mortgage rates and record breaking inventory.

1. Homes are not cryptos. They don’t plunge 50% overnight (usually). You people have zero patience with the real world. Home prices take years to come down.

2. Effective price drops are far bigger. See the homebuilder charts I included, of the average prices of homes sold by homebuilders. Lennar’s average price is down by nearly 20%; D.R. Horton’s by 11%, including incentives. But the Census Bureau’s median price chart does not include incentives; it’s based on contract prices, which don’t include the incentives. I made a HUGE deal out of this in the article. And you missed it. So go back upstairs and read that section carefully.

Effective selling prices of existing homes, too, are being distorted by non-inclusion of incentives.

Here in my suburb northwest of Chicago I see multiple houses in the over-$600k range with Zillow closing prices $40k or more above the listing price. Almost certainly interest rate buydowns rather than fevered competition.

On point 1 – markets are made up of individual buyers and sellers each of whom have different perspectives. With respect to “used” homes (not new build), look in your area at what is for sale and the last sale vs. current ask, particularly for homes bought at the peak (between mid 2021 and late 2022). Some are slightly below the 2021 purchase price, some are slightly above, others are substantially higher (as much as 25% above a purchase from 3 years ago – which can translate into 200k or more). Many sellers still want double or more than what they paid in 2018 or 2019.

Also consider how many properties are pending and then back on the market (analogous to the cancelled sales). Why are the deals failing? Inspection issues, financing issues, insurance issues, or other reasons.

Individuals have “anchor” prices (e.g. “my place is nicer than my neighbor’s who got $XXX in 2022 so I deserve 20% more”). These sellers will chase the market down or simply not sell.

Finally, and just an anecdote, I recently saw a listing description that started with, “Seller is highly motivated—bring all offers!”. The asking price is $125k (10%) ABOVE what they paid in October 2022 (and the property was build/bought for pure speculation – it’s been on and off market for 3 years and never lived in (no W/D or Refrigerator)

Patience, grasshoppers.

One thing is clear. The FOMO of of 2021-2024 has largely subsided, and an expectation of price drops is beginning to arise, largely due to prices actually dropping in many markets. Plus, there are tons of new build condos and apts coming to market. Those will be occupied.

If the stock market drops for many months or recession hits, the RE price decline would likely accelerate.

Could stock and RE prices plateau for many years as wages catch up? IMO, not likely. On the current fiscal course, there is a reckoning ahead.

No kidding. I’ll add the following;

I am seeing more layoffs in my sector, nationally. As unemployment, eventually ticks up. There will be a reckoning. Being a person with several properties and rentals I am more concerned with the county assessments, which have followed prices up. In my experience, when people get in trouble financially they tend to stop paying their rent before they stop buying food or paying their utilities. Landlords can lower rents, depending on their margins, but a smaller tax bill definitely helps.

Interesting times.

@Wolf

Some people just have a short attention span. . .

Just a random thought, but average price would look more realistic at $330k….

Hmmm — as with oil drilling, there’s a certain break even price range, to be profitable — so, with home builders saying they have lots of cushion, that implies more inventory buildup, as they cut more deals. There’s a reliance on past performance that makes that forward guidance euphoria suspicious. Costs increasing, while they sell fewer units for less cash, seems like shares have further to drop.

You only speak of big market areas. Talk about the midwest, year over year appreciation. Look and ohio, indiana, kentucky and surrounding states. The article makes it sound like this is the entire United States. This isn’t the whole truth.

1. This is about new houses sold by homebuilders, not existing homes sold by homeowners. You’re talking about prices of existing homes sold by homeowners. You’re trolling in the wrong article.

2. Those states you mention are included in this article, either in the “South” (Kentucky) or the “Midwest” (Ohio, Indiana), each of which has its own chart and data. So go ahead and actually look at the article, not just the headline. In fact, read the article, it does NOT bite.

Wolf you are The Troll. He made a valid point, and you responded with insult. Look at Tennessee or The South beyond Texas Florida. I’ve purchased 3 homes in Knoxville area financed by my sale of a home in Brockton Massachusetts and the rental income has benefited my life and I expect home value appreciation in the long run even if there is a pause in that, or not. Your incessant characterization of The South as being Texas and Florida is shallow and insulting. And on a completely different topic, your blatant disregard for growing income inequality by your dismissive comments directed at anyone who brings this up is part of why your analysis lacks depth.

What was D.h’s valid point? The article discusses the inventory of new single-family homes by region. Wolf noted Florida and Texas dominate the South region, but I assumed that’s because those states have a combined population over 50 million and their sheer size dominates the South region. That’s vastly different than asserting the South is only Texas and Florida, which is not what the article says.

Can you not read, timbers?

Wolf has addressed wealth disparity in articles where he is talking about the data that illustrates it. He just likes to stick to the topic, from what I’ve seen the last 3 years or so that I’ve been here.

Brockton? Yikes.

When did you buy? I assume not recent because rents are far cheap than mortgages these days even in Knoxville. Hope you’re not over leveraged because prices are down in the south – and yes, that includes Knoxville

Really appreciate someone like Wolf providing such comprehensive analysis backed by data.

Before I switched my profession, data is everything to me for analyzing & managing investment risks.

It takes tremendous time & effort.

He is sharing this without forcing us to pay.

For that, agree or disagree, let’s be grateful & respectful.

Let’s acknowledge his time, effort & contribution.

In this day & age, it is rare to see a source staying objective & not being bought to disseminate misinformation or even disinformation to manipulate the public.

It is understandable that as a landlord one would want to see all articles reinforcing one bought @ the right time with the right price & most importantly this investment is a one way elevator never comes down.

We humans are biological not logic, fact of which has made it possible for market manipulation & for gambling type of behavior in purchasing like home or stock.

Often the combination of both has brought to us each of the crisis.

That being said, it is possible that one just expresses frustration derived from the fact that subconsciously one knows market is turning though slowly.

Article is well composed & easy to read. Shouldn’t miss the main point.

In the field of investment, one thing check @ the door before entering – your feeling.

It doesn’t matter how you feel. It is all about what #s tell you for #s don’t lie.

“Brockton? Yikes.”

Brockton, city of crack…

Reported selling prices of existing homes are being held above true price by sellers buying down interest rates in same way as new home builders.

I know prices are falling but it is important to remember that since new home builders also know prices are falling they have been working to build cheaper homes to meet the market and still sell homes in this tough envionment. Porsche sold less than half as many 911s in 2011 than they did in 2006 just as the last RE bubble popped, but they sold more cheaper SUVs in 2011 than 2006. Many of the homes sold today for less cost the builders less since they don’t have the outdoor kitchen or cocktail pool that they did a few years ago.

Good, USA need more affordable homes.

I don’t want garbage product at the price of a nice house in 2018, I want 2018 nice now. So many bad looking townhouse developments where I live that are garbage product at the top of normal affordability. Zero land, which is where the value is.

Is this the canary in the coal mine?

It’s a comin’ around.

The tune sounds different but the song remains the same.

The trajectories on those charts are nearly identical.

The slowdown with agents and bankers is very real.

NE/Midwest maybe distorted due to slow population growth,

slow demand for new vs. existing, lack of investment, etc..

Related, external thing:

“Newly constructed homes in June were also far cheaper than existing homes. The median sales price of an existing home rose to a record high in June of $435,300”

Regardless if that’s 100% accurate, I think the increase in inventory, by both home builders and existing homeowners, is the early stages of a price war and a glut of overpriced homes that need a significant haircut.

The builders think they have leverage, but apparently existing homeowners are not financially stressed, as in GFC — so, seems like the frozen mkt may become more competitive, but stay gummed up with high prices.

Ultimately, I think existing homes face an uphill battle, more so than existing, because a lot of money pit shacks were bought at top dollar, then fixed up— making expensive homes, into totally unaffordable, unattainable assets.

On the other hand, new builds are by and large in crappy areas, built on small lots, screaming cheap shoddy overpriced crap — more affordable but less desirable.

That’s gonna be a very ugly price war, with a tsunami of junk pounding the shoreline.

Howdy Lone Wolf. Your latest articles make me think the RE downward trend is accelerating. Keep reading here Youngins, could get real interesting real fast??????

Ah so you are part of the income inequality problem by being able to buy 3 fucking homes by selling your NE home.

Have been watching this site for all the real estate stories, fantastic perspective, thank you Wolf.

Thankfully I just sold a second home three weeks ago- a 125 year old 4 square in a tiny town where my family lived while building a new home on rural family farmland. We had to put a new roof on it before we sold, otherwise the new buyer could not get insurance. This facilitated the deal, and the price went up by the price we paid for the roof. I’m hearing the market is starting to freeze here in Southern MN, where still there isn’t a huge inventory, but it usually turns over fairly fast. I’m also seeing big price drops starting on other local listings. I talked to a friend who owns a lumber yard and he says new construction is grinding to a halt.

Meanwhile, agricultural land is holding strong. (with corn at $4 and soybeans around $10/bu we could be seeing trouble ahead) Right now there is almost nothing of farmland for sale.

I feel pretty lucky right now- free and clear new house and land, no mortgage, not carrying an empty house. Credit this site for bringing clarity and focus to the reality of the market, helping to make these decisions.

Farm land prices are sitting on epic bubble. This too shall go down!

Just have patience.

I’m a farmer. It hasn’t been this bad since the 80s. It’s a complete nightmare. We are losing our shirts and no one seems to care.

Don’t know how common this is, but here’s an anecdote about a couple who live in a house across the street from my parents.

They are getting divorced. Don’t know what the initial purchase price is, but the husband says he’s going to sell it for at least 1.3 million.

If he doesn’t get that, he’ll just sleep on the couch for a year and sell it next year for 1.7 million.

You can’t make this stuff up… Talk about an inflationary mindset!

I don’t know how many people in this country get divorced but, if this kind of mindset happens in even 10% of the divorces, could be a pretty big pipeline of potential sales coming. And, unfortunately, even more reason for people to be upset and angry with each other if it doesn’t work out…

There are always “life events.” Don’t think divorce is any more common recently. In fact I think it’s dropped (also might be because fewer people are married)

The point wasn’t about divorce rates.

The point was that the guy getting divorced was expecting a significant amount of money for his house.

If he didn’t get it, he was going to stay in the house for another year (“on the couch”) and expect to collect $400,000 more just for waiting around.

I don’t remember the initial purchase price, but I’m pretty sure that the value has gone up by at least 300,000 since they bought it a handful of years ago.

The expectation of any appreciation in this market seems optimistic (to me), but $400,000 in a year seems ridiculous. And to stay on your ex’s couch for a year trying to collect??

It may be crazy, but I doubt he’s the only one doing this…

And yet even with the life event he’s a voluntary seller or he’d be cutting the price right now.

LOL why sleep on the couch for only 1 year and make only $400K when you can sleep on the couch for 2 yrs and make $800K?

Reminds of the mindset of ’05-’06. Prices only go up. Oops.

Reminds me of my friend who chased down the market in 2008.

Listed for 780K originally, kept on reducing prices, got many offers on the way down but sold after 3 years for 460K.

Those who panic first, panics best!!

Falcon, kind of reminds me of the supermodel in the 90s who said she wouldn’t get out of bed for less than $10,000 a day.

Seems like he’s being kind of a housing diva…😀

Oh, he’s not. Realtor.com has an article up “Delistings Surge Nearly 50% as Sellers Who Can’t Get Their Price Quit the Market in Frustration” (just search for it) that tells the tale of woe from sellers who can’t get their expected price. They think if they just wait for another year the rates will drop and buyers will be beating down their doors with offers above list.

I’d feel bad for them, but just can’t make myself do it.

I agree that expectations are high for existing homeowners where new home builders as Wolf points out has to sell homes to stay in business and smaller homes with incentives are still creating sales and inventory is growing so maybe builders increase their incentives to increase sales though margins will be lower

Happened right next door to my parents. House was offered at a price similar to the one cited by Profit Margins.

And it sat there. For years.

Sounds like a wonderful guy with that kind of mindset, maybe his wife has a good reason to divorce him..

Not a marriage therapist here but delusional mindset certainly isn’t a plus in maintaining a healthy marriage 😅

I have known several listing in my area because of divorce.

Maybe don’t wanna bad memories, maybe no one can afford the entire home on its own or maybe when marriage falls apart @ lease make some hefty $$

Who knows … divorce stats certainly explains the supply side just like # of baby boomers who are in God’s waiting room

Things are getting interesting

From what I’ve heard that mindset gets pretty messy in divorces, hope he has the liquid cash to buy his wife out of her half and then pay the mortgage all on his own

The complaints about mortgage rates being too high are lame.

Only are they too high when one looks to the manipulation of the Fed, QE, and the FORCING of rates to ALL TIME LOWS.

IMO, rates never went where they should have…….. the constant increase in debt proves that they were not “restrictive”.

$400k loan to buy a 450-500k house at 7% is $2661. Let’s say average T&I is 1.5% (2.5% in Midwest and northeast hellholes of course), or about $7500, $625/month. That’s around $3300/month, necessitating around a $100k household income. Median household income for 35-44 year olds (prime age homebuyers) is $101k. (As of 2023, so it’s higher now).

The housing crash so fervently hope d for here will not happen.

Nominal prices will drop a little here and there and continue to lose to inflation and that $500k house will still be $500k in 2030 but you won’t be buying it for $350k in 2028.

Ok assume 5% pretax to 401k this household has around 6k a month minus 3300 for their home…. 2700 left over for everything else. Car payment? Food? Savings? Even with perfect job security that down payment and an extra 1k a month saved by renting and they get a measly 3% and they are ahead ~1300/month. Why assume the risk if the home will sell for the same amount in 5 years when you will have 180k saved vs 60k (assuming no major repairs). Try adding a child into the mix. If you don’t have any safety net (i.e. avg wolf street dad with 12 rentals) it is a very uncomfortable position and seems to the the financially wrong choice.

Doesn’t matter what you think about the rest of the budget. The household easily qualifies for a house if they want to buy it. With no special underwriting or anything. That’s plain vanilla A paper.

why do you think that home prices wont crash ?

So called once hot market Austin has fallen more than 23% and falling more and more. The median income in Austin is also quite good.

Crash is already happening and unless rates go below sub 4, this ain’t gonna stop.

Median household income for 35-44 year olds (prime age homebuyers) WAS $101k.

Oh sorry, laid off. Bye bye income. Feel free to compete for entry level work with uncounted millions of lightly legalized immigrants.

Hahah average taxes and insurance is 1.5%. That’s hilariously wrong. Also, go find your grade school math teacher and tell him or her that your education was an abject failure. You need at least a household income of $150k to purchase a $500k home even with 20% down.

David is obviously an investor or realtor and is high on hopium.

Ok dude. In my house in California, the T&I is precisely 1.5% of the current value.

In, say, Arizona, the property taxes are around 0.75% (at most) of value, plus insurance.

You obviously live in some over-property taxed area east of the Mississippi.

And, no, 1/3 your income, gross on P&I is pretty standard “A” paper for a mortgage.

You obviously don’t own a house or 2.

1/3 is really to much of your income and gets a lot of people in trouble. Principle of Wolf Street: Live Below Your Means! We try to live by 1/5. This has helped greatly during layoffs, illness, and emergencies. Plus you have more cash and freedom. A home should not be a liability.

“Ok dude. In my house in California, the T&I is precisely 1.5% of the current value.”

What’s the point of % of “current value” (a theoretical number)? Why not do % of total carrying costs?

My taxes and insurance (at my house that I own) are about 40% of my total carrying costs. That’s a huge chunk.

For anyone curious… monthly P+I is $980, monthly taxes are ~$525 and insurance is ~$66. That doesn’t include water, sewer, electric, or gas bills.

Admittedly I live in a high property tax state (NH), but you’re also bias living in CA with your lovely prop 13. For many, taxes and insurance are a huge part of the carrying costs.

Median numbers seem a bit off. Denver median household income for that age range is 90k – ish and median single family homes price is $580k.

Additionally even if median family household income is $100k. That’s 70k ish, about $5.8k after tax. Throw in $2k month for daycare. That’s $3.8k for housing. So at $3300, that leave $500 month to cover electricity, wifi, food, cell phone, groceries, car insurance. Throw in a car payment and/or student loans they’re definitely in the red.

For this reason I know lots people in that age range making significantly above the median income who have no desire to buy at current prices.

Personally I think it’s all marketing from the zirp era – the public opinion will change soon as the media narrative changes and buyers will disappear even more so than they have today.

Time is the hardest part. In 2005, it was obvious to me that we were going to have a crash, but even I only expected 20%. The epic crash was obvious in 2007, yet the bottom was still two years away.

As dear old Tom Petty said, the waiting is the hardest part. And this time it’s not different.

So much damage yet to happen, so much denial again. Economics has truly proven to be a dismal science in my experience.

Crypto has truly trained another generation to BTFD. So the crash will be toxic, again.

Yeah except this is nothing like the great recession

Stocks bottomed with money flows in March 2009. But Bernanke remunerated interbank demand deposits at the FED inducing nonbank disintermediation where the nonbanks shrank by 6.2 trillion dollars. That process didn’t end until Bernanke bankrupt half the home builders.

Yeah this feels like our 2006 moment. We know things are overpriced, we know there’s a ton of inventory, but most people keep saying prices won’t drop.

I mean this time will be slightly different. It’s never identical. But the market never goes straight up forever and typically reverts to the mean

Given enough time, homes only do go up. My parents bought a house at the peak in 2006 but now 19 years later it’s still valued way higher than it was at the previous peak.

30 years from now any house you buy today will be worth a lot more than it is today.

Yes, there are peaks and valleys along the way, but typically you’re better off not waiting for some magic low price to come along.

“typically you’re better off not waiting”

“typically” doesn’t apply here. We never had a 50-70% price explosion in two years. Nor did we have 3% mortgage rates when inflation was 9%. This were huge distortions that will take many years to work off.

In local markets, which is where you buy a home — not in the national median market — home prices can wobble down for decades and not get back to their prior values for decades. I know about Tulsa because I bought a condo there in 1989, well after the housing market had massively crashed. I bought from a bank that had foreclosed on it (I paid about 60% below the defaulted mortgage issued in the mid-1980s). Then the bank collapsed, and the FDIC took over. My neighbor bought his unit (same as mine) from the FDIC for 20% less than I’d paid. So that was the bottom. I sold in 2000 at a big gain, but still below the defaulted mortgage balance of the mid-1980s. Then prices plunged again, and the buyers sold my condo in 2014 at a big loss from what they’d paid me, far below the 1980s mortgage balance. It took the home-price explosion of 2020-2022 to get the condo (and meanwhile additional improvements) to sell last year for more than the mid-1980s mortgage balance. That’s 40 years to get back to where you were!

Over those 40 years, the dollar has lost 62% of its value. So that property adjusted for the loss in purchasing power of the dollar, last sold for something like 50% below the mid-1980s mortgage balance.

Beautiful condo, 1,800 square feet, I’d put in gorgeous red granite on the kitchen counter and floor, in the entry way, and in the master bath floor and counter. Endless views west and south, 24 foot long balcony…. sunsets, tornados (saw two), floods (the building is just a couple blocks up from the Arkansas River which went over the embankments periodically), hailstorms… the whole drama of nature right in front of you. That was my forever-bachelor-pad 🤣. I still miss the place (a little).

Wolf,

For the most part it may lack flooding, tornados, and hailstorms, but at least SF does have sunsets for you to enjoy.

This is all happening while the dollar falls and other assets (stocks, gold) inflate. No doubt home prices are facing the same upwards pressure. Makes me wonder how bad home prices would be if weren’t for this.

Dan

Right, something isn’t kosher.

lol why you fools keep comparing homes to investment like the stock market is beyond me. They have nothing to do with each other. Younger generation priced out probably doesn’t own any stocks outside their 401k.

People buy homes to live in and raise a family… Not as an investment.

A home isn’t an investment, but it’s an asset. Not all assets are investments. Stocks are both an investment and an asset. Homes and gold are assets.

While a bit too slow to adjust for the instant gratification crowd, (actually a good thing) a free market system is doing its job.

Free market Capitalism, it’s just the best!!

Love the articles!!

I borrowed this idea from Sven H and let my AI friend help, but seems legitimate:

“Based on the data available, the total homeowner equity, while having dropped slightly from its peak in 2024, remains substantial and is on a scale comparable to, or even exceeding, the estimated annual U.S. GDP in 2025

U.S. households hold a collective value of homeowner equity that is near record levels, estimated at $34.5 trillion at the beginning of 2025”

As with, Buffett indicator, it’s almost impossible for any segment of the economy, to outperform the aggregate cumulative performance of national GDP —- which helps explain the unrealistic notion that the housing market will continue exploding into a second staged rocket.

Also, keep in mind, with that unsustainable backdrop, there’s the absolute unsustainable equity bubble exploding — as the global deficits explode, especially USA insanity.

The only way to grow housing, equity and crypto bubbles is with exponential debt — this entire world is absolutely stupid!

Money is something that is simultaneously liquid. Real estate isn’t.

Stupid? Nah, it’s the new norm, we’re the stupid one trying to look at things with any kind of underlying fundamentals. Search around for this article, yeah totally normal, nothing to see here. All for a currency that you can’t even use at Ikea or Starbucks to buy common goods but hey there’s a use case there somewhere…

“A Bitcoin whale just sold $9.5 billion in crypto that was originally acquired for $54,000 in 2014 — recent 80,000 BTC transaction nets an 18 million percent return”

Phoenix: That bitcoin whale is going to have to write a large check in capital gains taxes.

I bet if he asked the guy getting divorced that thinks his home will be worth $400K more next year he would have told him to wait a year and sell the Bitcoin for $13.5 Billion next year…

P.S. To @Patrick I could be wrong but I’me guessing that the “average” wolf street dad has less than12 rentals…

Tech giant Intel stuns Wall Street with 25,000 layoffs as jobs crisis deepens

Silicon Valley titan Intel will slash 25,000 jobs this year as it battles to turn around its flagging fortunes.

The chipmaking giant — which makes processors that power millions of Dell, HP, and Lenovo computers — will shrink its workforce from about 99,500 to 75,000 by the end of 2025.

Bosses said the layoffs come alongside plans to abandon factory projects in Germany and Poland, slow the pace of construction on major facilities in Ohio, and consolidate operations in Costa Rica into bigger hubs in Vietnam and Malaysia.

So most of those layoffs are overseas?

I don’t know the US/foreign breakdown, but Intel is really hurting and getting hit hard by AMD making better, cheaper, faster CPUs.

Agreed.

Not to mention Apple using homegrown M chips is biting into additional profit.

Interesting

On WeChat a widely used Chinese social media it is advertised that anyone with a degree in tech related fields is desired by tech company in Bay Area. In addition, company will sponsor H1 visa or facilitate immigration process under the category of highly desired talented individuals.

I also saw other info such as newly graduated foreign students from 🇨🇳with master degree makes average $250k a year & buy a home built in 80’s just in one year. Employers are among Apple, Google, Nvidia, etc.

So who are they laid off & who do they hire to fill in the spots & why home price in Bay Area has been kept high?

Many of these Bay Area Tech people buy homes in Orange County CA & fly to SF for work like twice or 3 times a week 🧐

With new inventory at 9 months, builder incentives will have to increase, so effective prices will likely keep dropping. Builders are leading the market down, as expected.

In addition, the new builders seem eager to create new style trends, which accelerates depreciation of existing homes. I can’t help but notice the new stuff is using a completely different color pallet, with a lot of grey/beige, blue earth tones including carpets, paint, and finishes. Metal is replacing wood in the stairways and other places. Tiles are larger in shape and a lot more modern looking. Exterior uses more sheets and larger formats. I’m not sure I like all this, but I do recognize the style is spreading fast.

Have seen mentioned how Trump may drop the capital gains tax on home sales (have no idea how this applies to CRE or other related perplexities). Yet wouldn’t that be something that a flood of homes for sale flooded the market, at reduced prices?

I know people who’d instantly put their home on the market if they don’t have to pay capital gains taxes on it. There is a lot of pent-up supply sitting around because of capital gains tax avoidance.

But it’s just another one of the thousands of daily Trump-saids.

While I also know some people who would sell today if they could take millions tax free, the oveall percentage of the population have homes that have appreciated more than $500K a married couple can already take tax free (every two years) is small. Of the people with homes that have gone up in value “more” that $500K I would bet that most are like me in their “forever home” who are not interested in selling even if the profit was tax free.

Get this, the govt devalues the currency, and ya’ll get to pay capital “gains” on that.

Home prices are actually bargain price right now.

not sure if this forum allows to post links, but search of long term trends real estate gold ratio. There’s a graph showing real estate was only ever lower briefly twice in the last 130 years: 1980 and 2012.

So I recently sold gold and bought a house.

If home prices “in real money” drop more, I will buy a couple more.

Oh look. Another fool that is comparing gold to home prices. Homes are not a bargain. They are vastly over priced and unaffordable. But go ahead and sell all your gold and buy homes. Enjoy those carrying costs as your real estate value declines

Don’t worry, pricing stuff in gold when gold is high is classic gold-bug stuff. After gold plunged by 50%, these comparisons stopped. So now they come again.

Gold can be a great long-term investment, but this gold-bug stuff is just funny.

Houses are a much bigger bargain when priced in stocks 🤣

Note I’m no longer a gold bug. The gold is gone. I’m a no-more-monthly-housing-payment bug.

Back in the 1960s you could buy houses in Hermosa Beach or Manhattan Beach, California for around $15,000 to $25,000 each and most of them were real dumps on tiny postage 30′ x 80′ beach pads. Now you can buy those very same dumps for around $3,000,000 each on the same tiny little lots with no landscaping or other amenities!

1960’s $25,000 / $35/oz = 714 oz gold

Today $3,000,000 / $3336/oz = 899 oz gold

So houses in that area appreciated a little. Considering 60 years passed, and if assume the person lived in it, not a rental and pretend there were no expenses the IRR on the purchase price is only 0.38%.

Once had a banker offer to buy back a farm my father had purchased from him for the purchased price. My thoughts at the time, did not voice these as I respected a family friend, was to ask if he was offering silver coin in 1975 value vs the fiat money currently in circulation?

Since then I have collected silver coin vs stock and wonder how you would consider this offer?

Mindless circus clown billionaire spits out stupid thought:

“If rates come down, we’ll have a huge boom in housing prices,” Greene told BI.

A reduction in rates would likely result in more houses on the market, as homeowners who took out long-term mortgages at low rates would then be willing to refinance and move home, (Jeff) Greene said.”

Item: “He is (was) currently constructing One West Palm, a twin-tower project in West Palm Beach, though its completion date is uncertain”

Item: “The housing inventory in West Palm Beach has surged to its highest level in over a decade. As of 2025, the number of active listings reached 14,738, surpassing even pre-pandemic levels seen in 2017–2019. This sharp rise in supply is one of the strongest signals yet that the local market is undergoing a correction”

* West Palm Beach: More than 1 in 5 listings have had a price cut in June

One can easily see why a real estate developer is hyping increased prices, as inventory expands — not to mention his 2nd grader theory, that lower mortgage rates will explode unaffordable real estate prices, into a super new hot, crypto-like bubble.

Nonetheless, in the background, is the bifurcated-resilience phenomena, that isn’t going away — there will be super wealthy investors churning and swimming like sharks, preying on weakness, and or, adding to portfolios that seemingly indestructible — while the vast super majority watch.

There’s absolutely no doubt, that wealthy people will gain more wealth – but the ludicrous notion that some total slime-ball snakes need lower mortgage rates is pathetic.

Way late here, but just read something from a fairly decent analyst on his blog — Peter Boockvar:

“We need BOTH lower mortgage rates and more home supply at the same time in order to unlock activity”

Great — yah, kinda, but —- the obvious elephant is home prices dropping — and I don’t see how that’ll happen.

What incentive will home builders have to build more homes as prices fall?

Adversely, if rates artificially fall because of a compromised Fed, won’t that stimulate demand, and push prices higher?

I don’t see how the trifecta of lower rates, more building and lower prices will ever converge.

The solution in this madness, is a serious housing recession, that crashes prices — which assumes a recession, with job losses. It’s a Schrödinger Cat thing, you can’t just jeep things in a state of suspended animation —- there has to be a reset that shocks the system — versus synthetically distorting a few variables.

“What incentive will home builders have to build more homes as prices fall?”

To keep their businesses alive maybe? The big homebuilders HAVE to build and sell homes, no matter what the market is, because that’s how they’re a company. Or else they’ll shut down and vanish. They cannot NOT do business.