Listings YoY: Orange County +66%, San Diego +55%, Fresno +48%, Sacramento +47%, Los Angeles +45%, Riverside-San Bernadino +43%, San Jose & Silicon Valley +39%; San Francisco metro +30%.

By Wolf Richter for WOLF STREET.

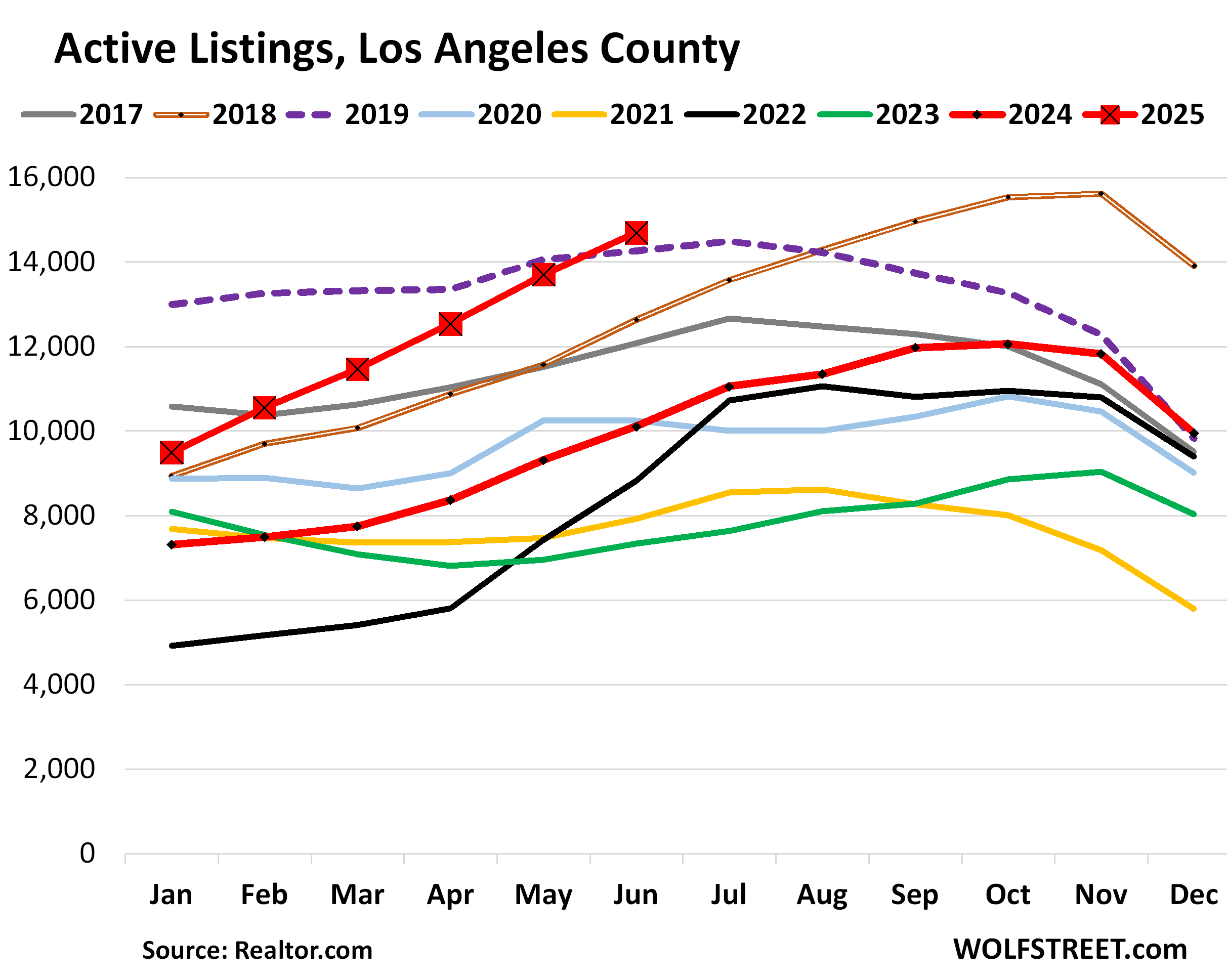

Los Angeles County: Active listings spiked by 45% year-over-year in June, to 14,692 homes for sale, the most for any June in the data from realtor.com going back to 2016, passing by even 2019 (dotted purple line).

In 2018 (brown double-line), the Fed was hiking rates, and the average 30-year fixed mortgage rate rose to 5% by November 2018. Home sales stalled and inventories piled up in the second half of 2018. And that inventory pileup continued into mid-2019 (dotted purple line). That’s the inventory level that 2025 just blew by. At the end of July 2019, with inflation substantially below target, the Fed cut its policy rates, and mortgage rates began to come down.

But that’s not what happened this time around. In the fall of 2024, the Fed cut its policy rates by 100 basis points despite re-accelerating well-above-target inflation. In response, the bond market, worried about inflation and a lackadaisical Fed to fight this inflation, threw a hissy-fit and longer-term Treasury yields and mortgage rates surged by 100 basis points. Active listings have been going straight up so far this year:

The median number of days that homes spent on the market in Los Angeles County before they were either pulled off the market (delisted) or sold rose to 47 days, matching June 2020, and both were the highest Junes in the data by realtor.com going back to 2016.

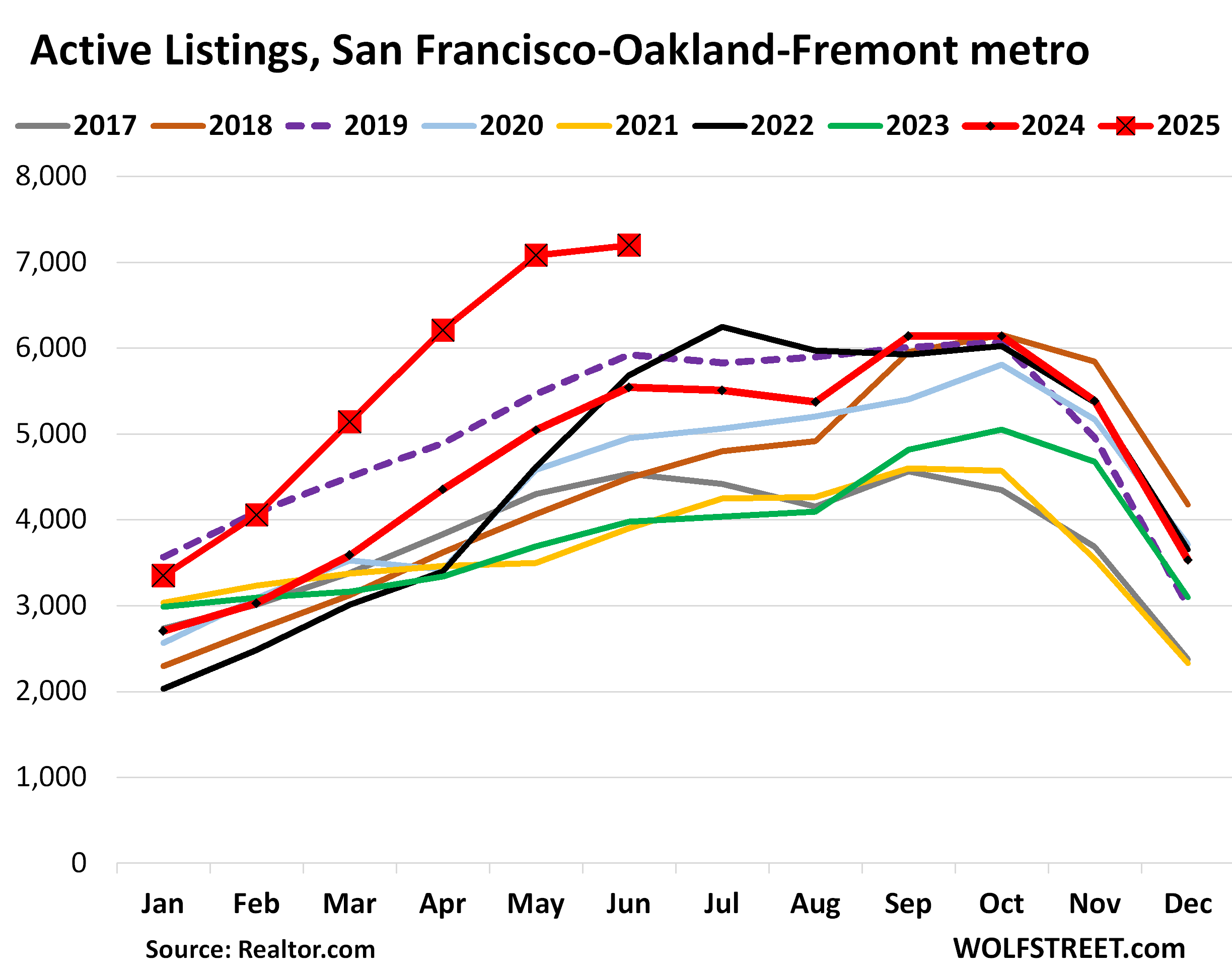

San Francisco-Oakland-Fremont metro: Active listings surged by 30% year-over-year in June, to 7,196 homes for sale, by far the most for any month in the data from realtor.com going back to 2016.

Compared to June 2019, the second highest June in the data (purple dotted line), active listings were up by 21%. Always astounding how a much-hyped “housing shortage” turns into an inventory pileup.

This metropolitan statistical area (MSA) includes the counties of San Francisco and San Mateo (northern portion of Silicon Valley), part of the East Bay, and part of the North Bay.

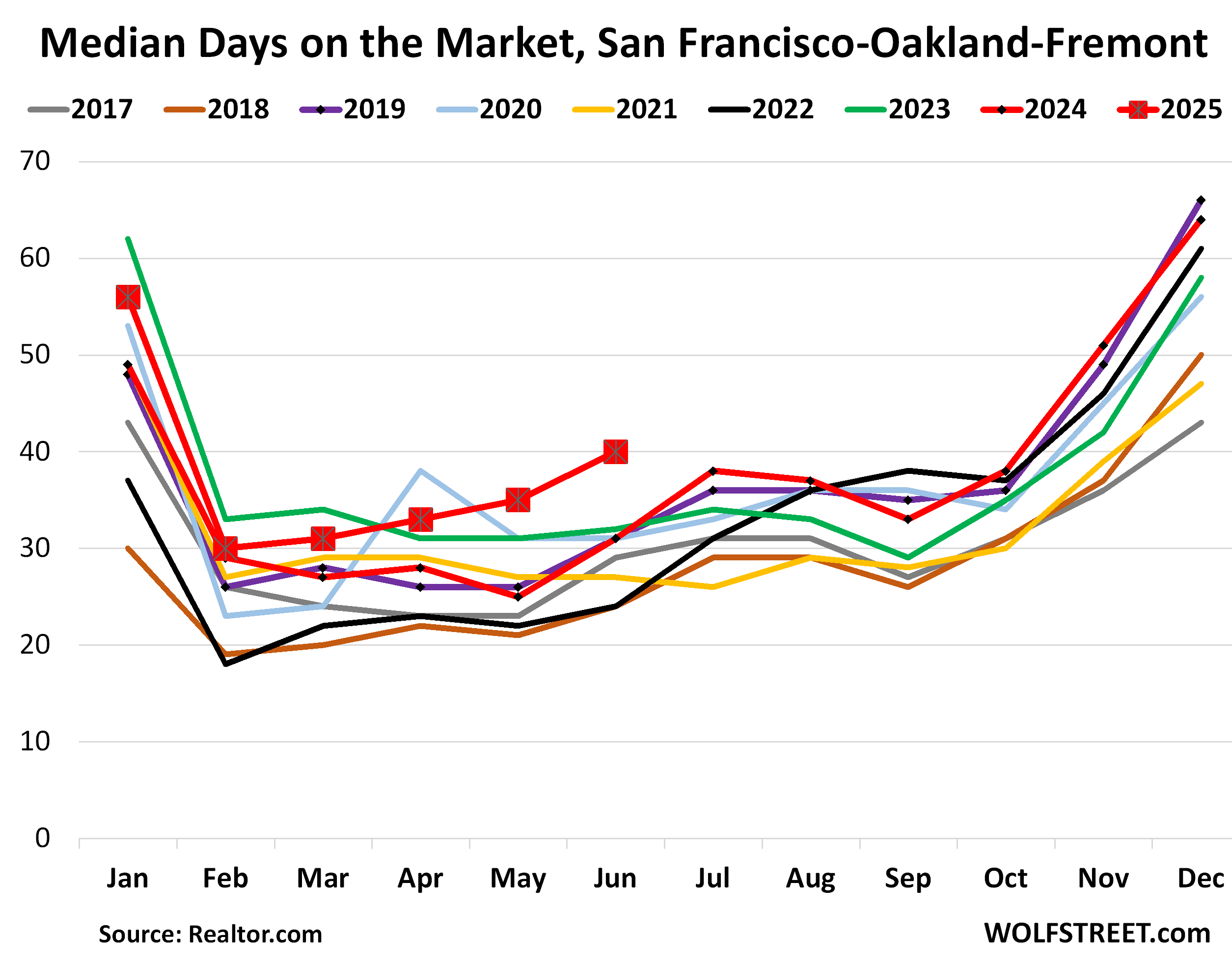

The median number of days that a home spent on the market in the San Francisco metro before it was either pulled off the market or sold jumped to 40 days, the highest by far for any June in the data from realtor.com going back to 2016, up from 31 days a year ago.

Sellers pull their homes off the market “in frustration.” This increase in median days on the market comes despite a surge of delistings across the US as frustrated sellers, seeing that demand has withered and that they can’t get the price they want, pulled their homes off the market and decided to wait for better days or whatever.

Delistings surged by 47% year-over-year across the US, as “sellers who can’t get their price quit the market in frustration,” realtor.com reported in a blogpost today.

“The trend is especially noticeable in the South and West, where inventory has surged back above pre-pandemic levels, and prices are flat or falling,” Realtor.com noted. So that includes California.

Prices in many of these markets have begun to drop – the “in frustration” part – and so sellers decided to wait until prices drop even further?

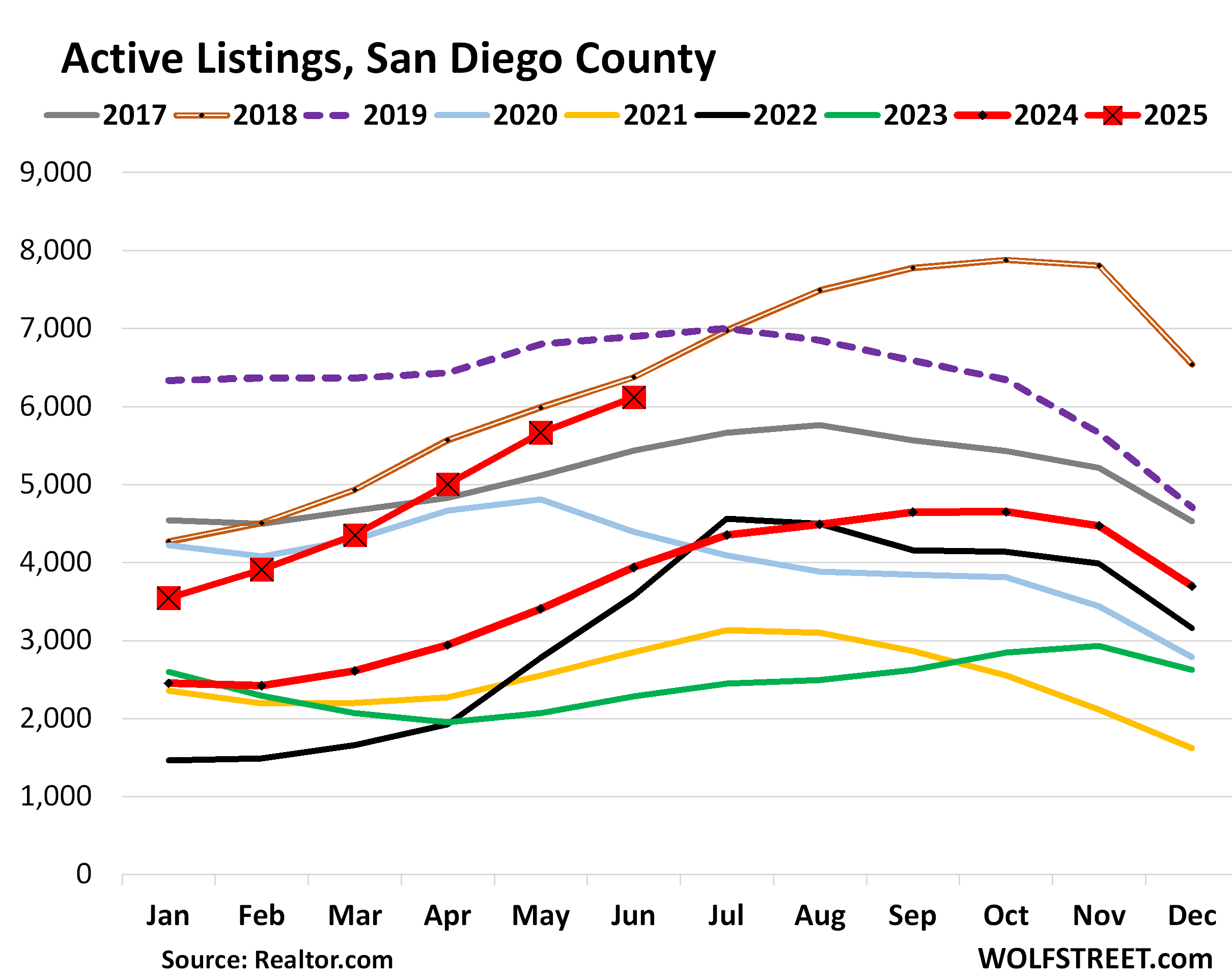

San Diego County: Active listings spiked by 55% year-over-year, to 6,116 homes for sale, the highest for any June 2018 (brown double line) and June 2019 (purple dotted line) in the data going back to 2016.

The median number of days that a home spent on the market in San Diego County before it was either pulled off the market or sold rose to 41 days, up from 33 days a year ago, and the second-highest June in the data from realtor.com going back to 2016, behind only June 2020.

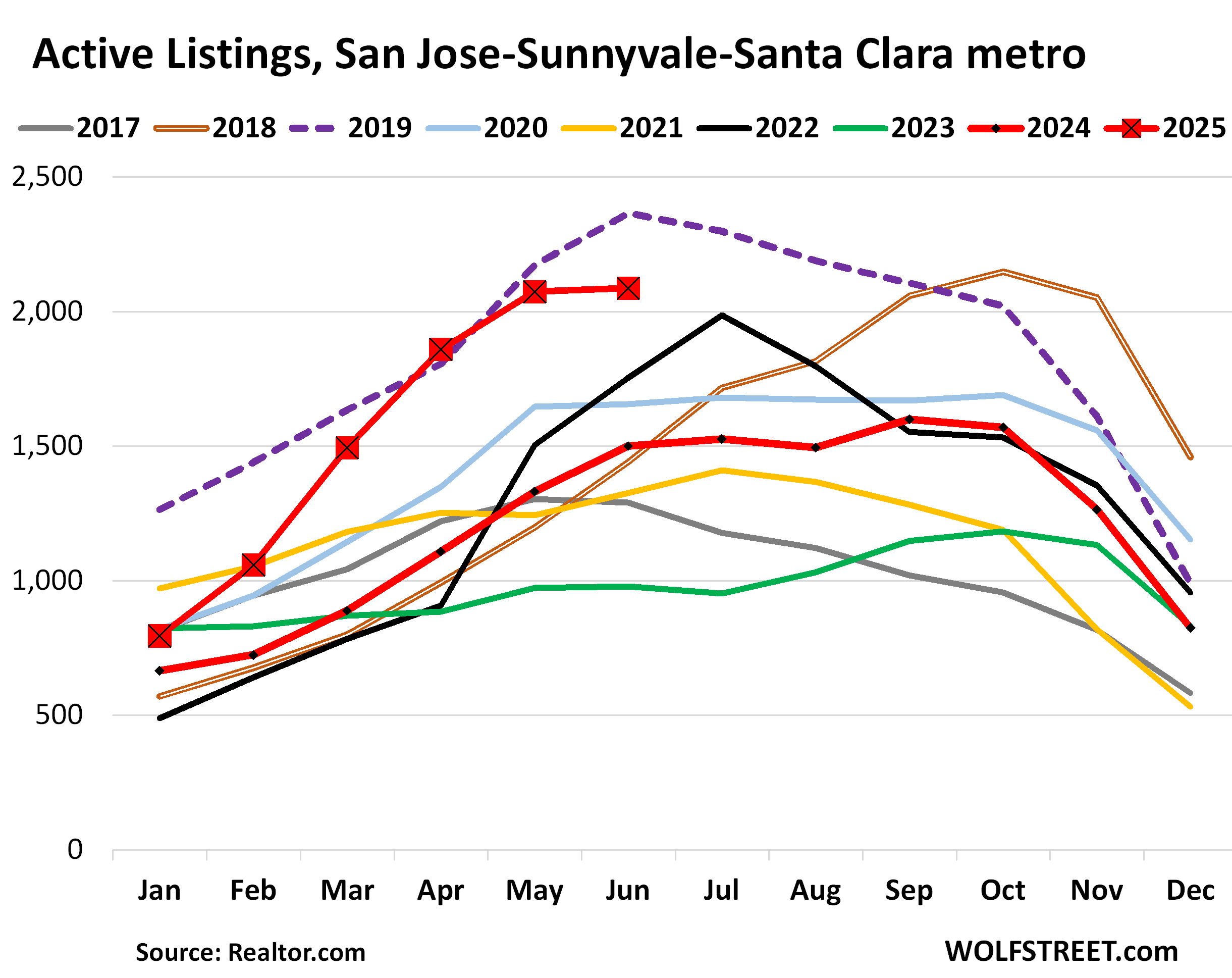

San Jose-Sunnyvale-Santa Clara metro: Active listings spiked by 39% year-over-year in June, to 2,087 homes for sale, the second-highest in the data going back to 2016, behind only June 2019.

The MSA includes Santa Clara County (San Jose and the southern part of Silicon Valley) and goes south into rural areas.

Median days on the market jumped to 34 days in June, the second-highest June in the data from realtor.com going back to 2016, behind only June 2020 (35 days), and up from 25 days a year ago.

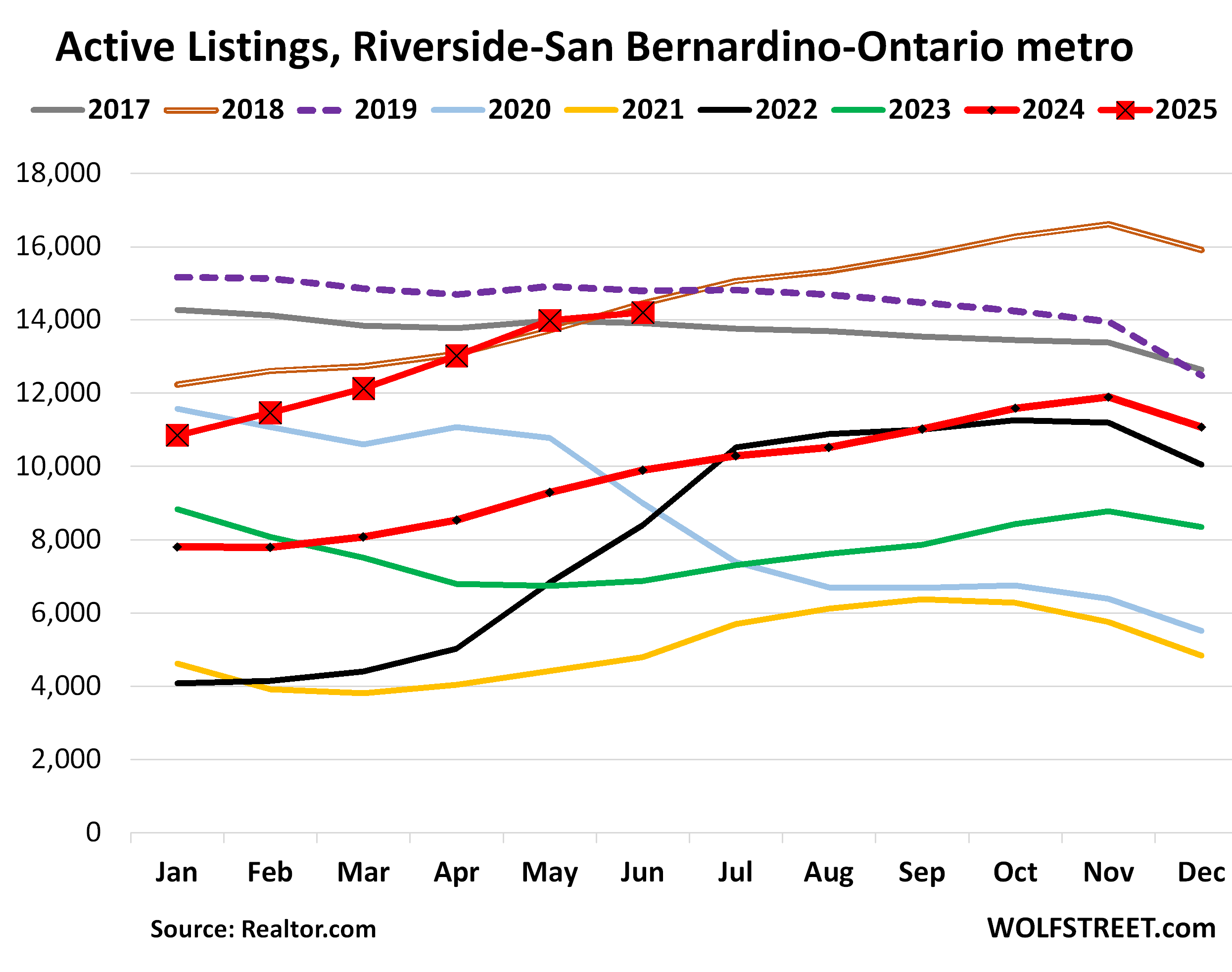

Riverside-San Bernardino-Ontario metro: Active listings spiked by 44% year-over-year, to 14,205 homes, just a hair below the Junes of 2018 and 2019, and all three were the highest in the data going back to 2016.

This metro is huge in terms of active listings and matches Los Angeles County: both had over 14,000 listings in June. The next largest market here is the San Francisco-Oakland-Fremont metro with 7,200 listings. San Diego County is next with 6,100, then the Sacramento-Roseville-Folsom metro with 5,400, Orange County with 4,700, Fresno with 2,100, and San Jose with 2,100 listings.

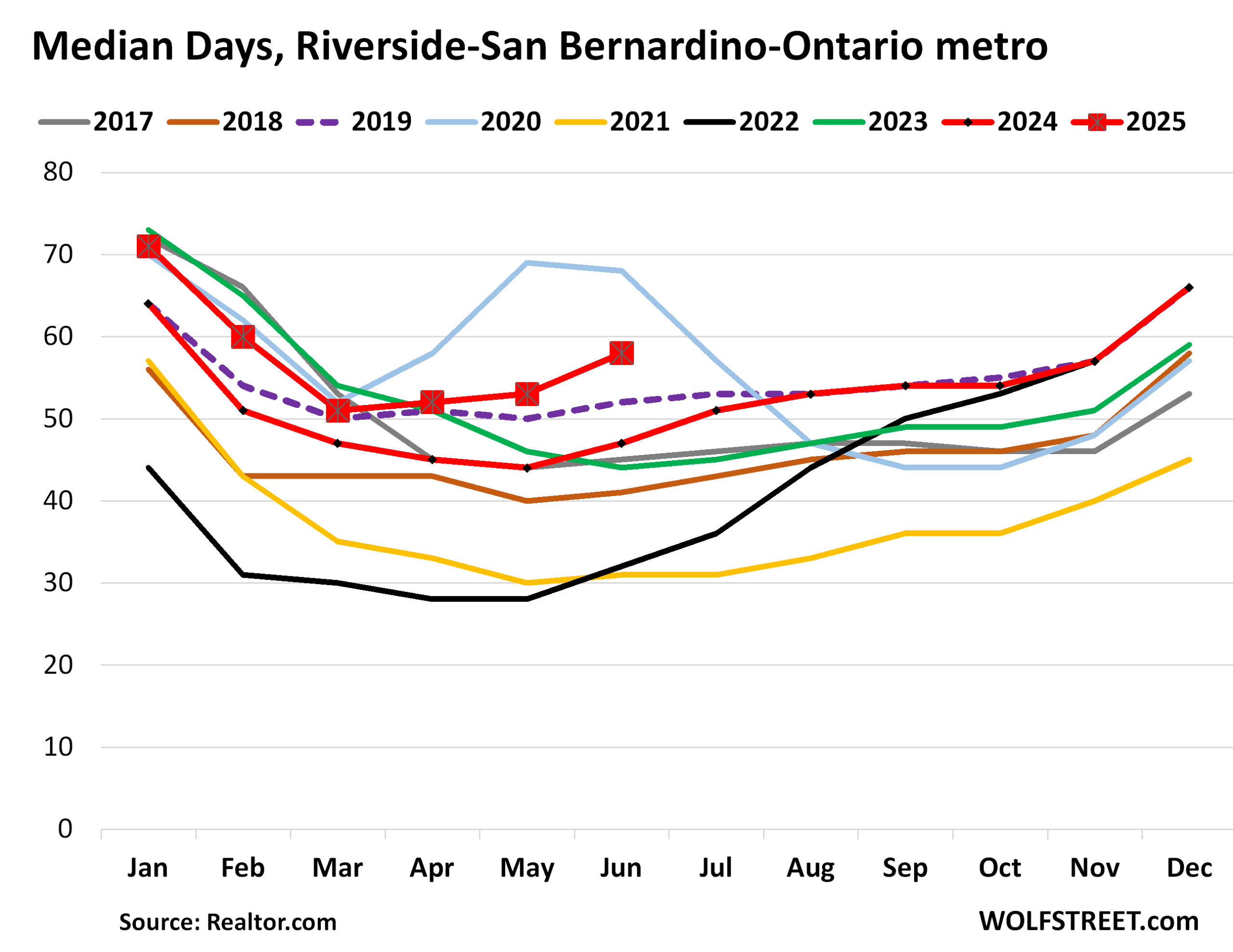

Median days on the market jumped to 58 days, the second-highest June in the data from realtor.com going back to 2016, behind only June 2020 (light blue), and up from 53 days in May.

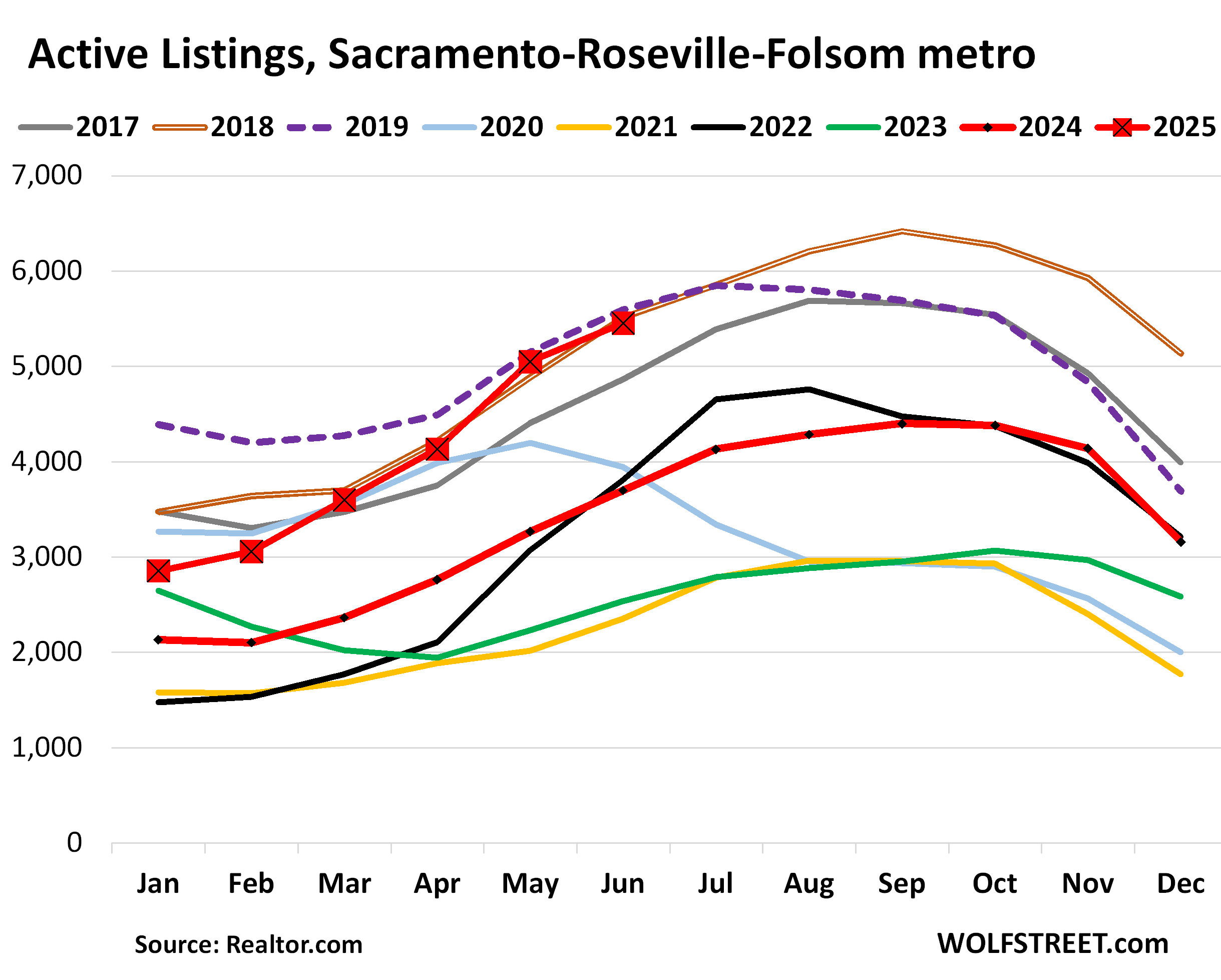

Sacramento-Roseville-Folsom metro: Active listings spiked by 47% year-over-year to 5,452 homes for sale, just a hair below 2018 and 2019.

Median days on the market jumped to 44 days in June, behind only June 2020, and up from 37 days a year ago.

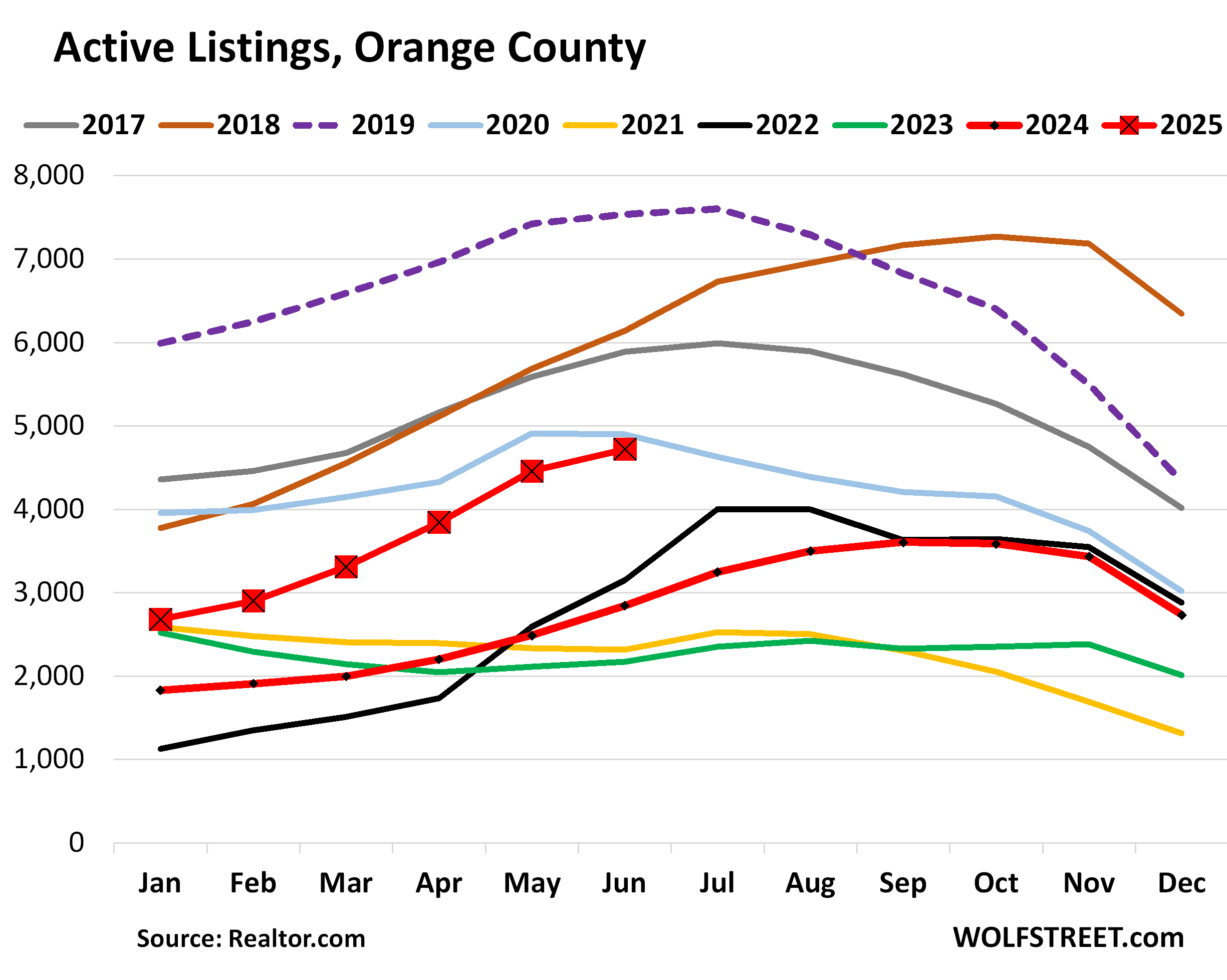

Orange County: Active listings spiked by 66% year-over-year in June, and by 118% from two years ago, to 4,719 homes.

Inventory has been low, as everywhere in 2021-2023, but got a late start taking off and was still low in 2024. But this year, the dynamics changed, and listings have more than doubled in two years.

Median days on the market have surged to 47 days, up from 37 days a year ago, and just a hair below 2019 and 2020, and all three are the highest in the data going back to 2016.

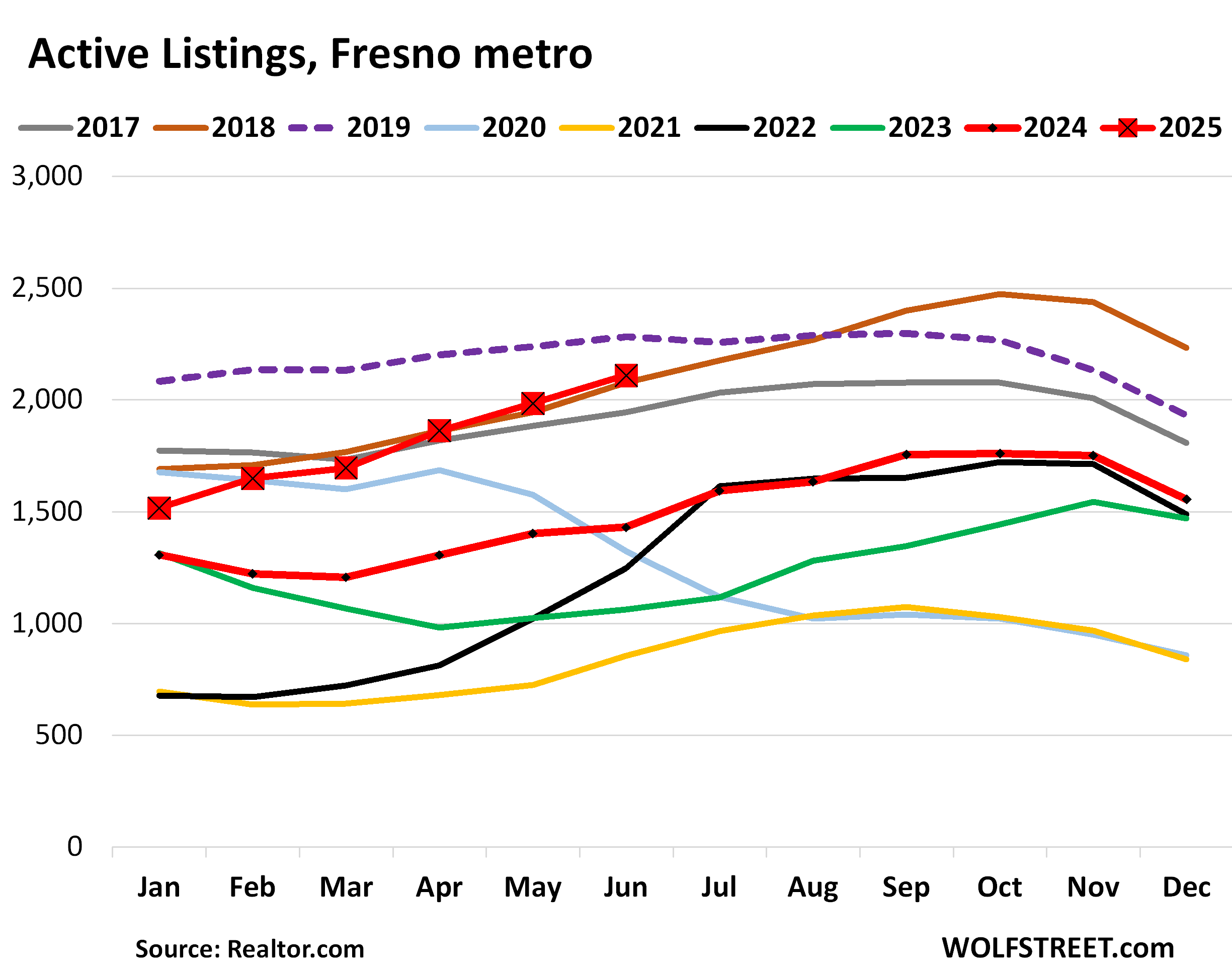

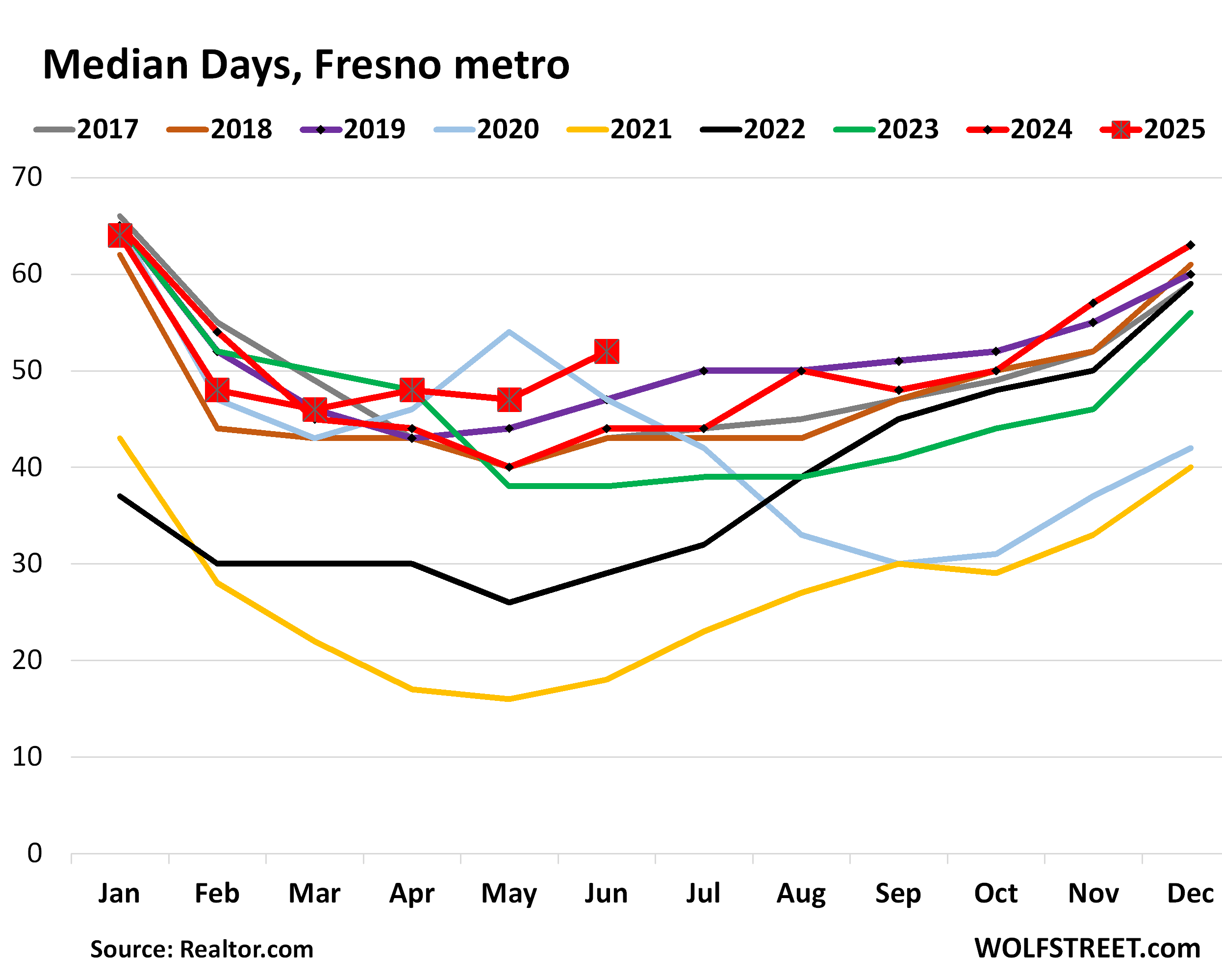

Fresno metro: Active listings spiked by 48% year-over-year to 2,110 homes for sale, the second-highest in the data going back to 2016, behind only June 2019. They doubled in two years.

Median days on the market before the home was pulled off the market or sold jumped to 52 days, the highest for any June in the data going back to 2016, and up from 44 days a year ago.

The problem is Demand.

It’s not that sellers are suddenly putting huge numbers of homes on the market; they’re not. But what is on the market doesn’t sell because prices, which exploded during the pandemic, are now too high, and demand at those too-high prices has withered. One of the most fundamental economic principles – demand destruction by too-high prices – has set in.

Active listings have surged because demand has withered, and despite the surging trend by sellers to pull their properties off the market, as realtor.com had put it, “in frustration” because they can’t get the prices they’d been dreaming about.

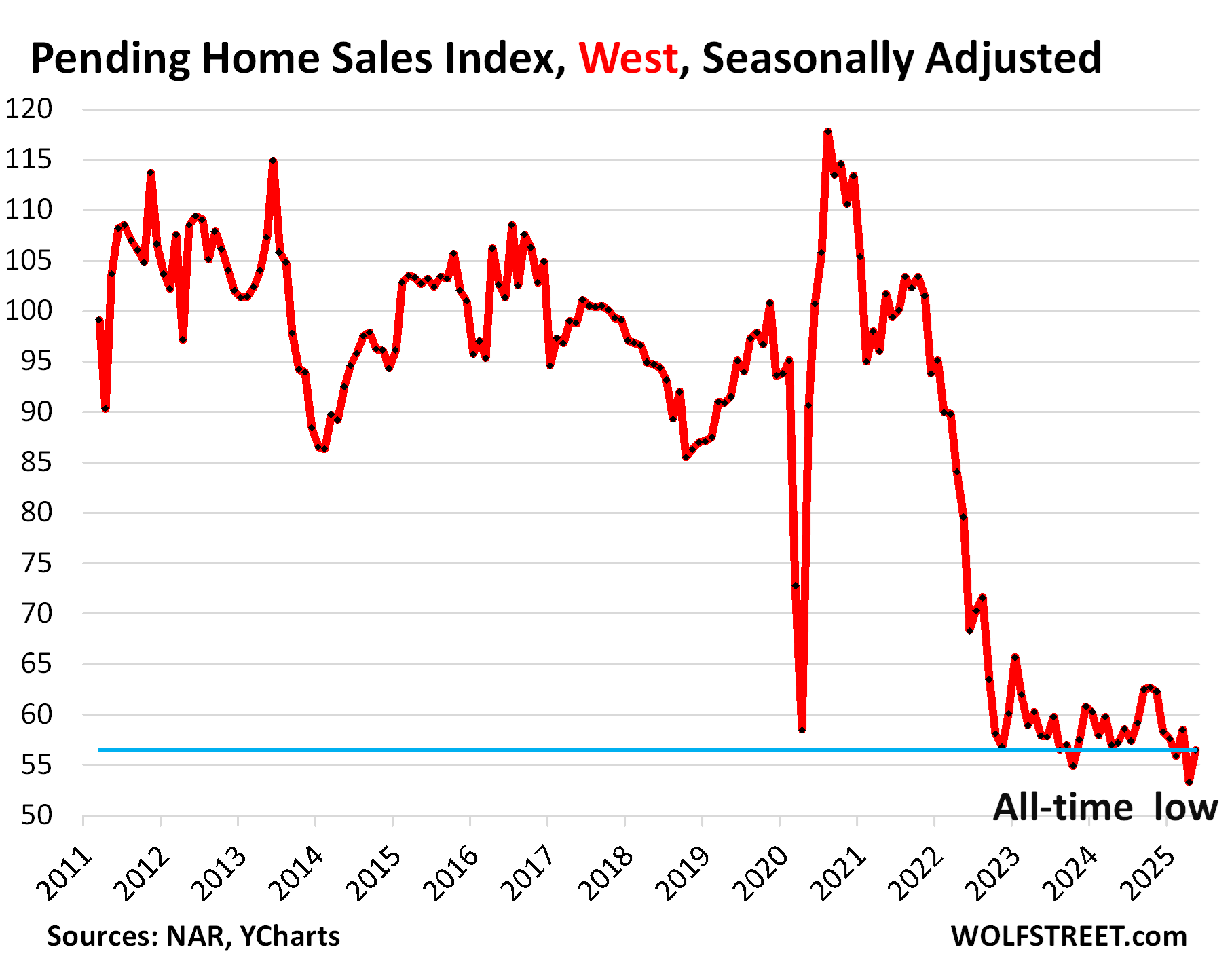

One of the measures for demand, pending sales of existing homes in the West plunged by 38% in May compared to May 2019, according to the latest data from the National Association of Realtors. April pending sales had been the lowest since at least 2011, the extent of the data.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The infalliable OC, SD and LA have surplus of inventory?…color me shocked ;p looks like sellers still holding the lines on prices though and they get their little dose of hopium when some buyers still bite on overpriced houses thinking they can still get in on the action. Btw, this came out of Realtor.com today, guess this is their playbook, maybe hoping for the rescue when they relist by next Spring…who knows, maybe this world might just be nutty enough that by next Spring, interest rates will be down to 3% and FOMO will be back to full force but if I were them, I wouldn’t bet the farm on it. The other side of that coin might just be staring into the abyss of chasing the market all the way down…enjoy..

“Delistings Surge Nearly 50% as Sellers Who Can’t Get Their Price Quit the Market in Frustration””

Even if interest rates drop, it doesn’t mean that yields will drop. With the debt getting higher and higher bond vigilantes might keep yields were they are, thus making mortgages stay were they are. Which is normal. I like it when wolf shows the historical mortgage rates graph because we can see that these ultra low mortgage rates that we had essentially since late 2000s are not the norm.

For 20 years the G used interest rate strangulation (FU savers) to create a fictional “reality” wholly divorced from true economic fundamentals in the US (collapse of international competitiveness).

But this denial of reality fixed *nothing* – it only de facto confiscated private savings (ZIRP) to feed lies (USD asset inflation even as USD reliability evaporated).

I just spoke with a Lennar sales agent here in Texas (north of Houston) this afternoon. Their new builds were reduced in price 12% to 17% based on the model yesterday. They are offering 4.25% FHA 30 year fixed financing with 5% down. An adder to the loan would be mortgage insurance.

Conventional rates are market (6.5%+?) but they have not had any applications for conventional loans in months.

There are a lot of new homes sitting here empty and the builders are scurrying to complete the neighborhoods before the end of the year. There will be a lot of rentals around here in the coming years.

New starter homes in this area are now selling for $150 per square foot.

“They are offering 4.25% FHA 30 year fixed financing with 5% down”

I wonder if those “30 year” mortgages at 3% under market actually reset to market in a few years.

4.25 rates in a 7.25 world for *30 years* is costly for Lennar (although who knows what obscene markup is actually placed on the ostensible product…the house…in the first place) so Lennar may have that rate subsidy go bye-bye after just a few years.

Once Lennar drags a buyer across the finish line (“sale”) they really don’t care too much about what happens to the mortgage loan (which Lennar almost immediately sells off).

That’s how you get 2008.

According to the rep, the 4.25 is the fixed rate with no reset. The only adder is PMI which would push the rate up to 5% or so. The houses are heavily discounted. This looks like a race to finish all the new builds in this area before years end.

I walked one 1,350 sq, ft. three bedroom (unsold @ $210 K) and it’s ultra cheap with no visible “upgrades” if you want to call them that. We are talking low ceilings, cheap cabinetry and counter tops, no Medicare cabinets in bathrooms, one sink in the master bath, etc, etc.

And a bit north of me, a builder’s sign along the road is advertising new homes starting in the $100,000’s.

I wonder what the percentage of empty overpriced houses is at this point.

10%? 12%? 15+%?

This housing “shortage” that keeps being talked about feels more like a glut of delusional property owners with green in their eyes.

@wolf I am curious to know how many of these sellers are selling & then moving to other states. Is there an easy way to find out ? I would not mind paying a small fee for any software which enables one to get that info.

I asked because I wondered if these sellers can sell at a big price cut & still be able to buy a high end house in another state (except NY). Maybe even have some cash left over after that.

This is why “California money” is so loved and loathed in other housing market. People who just sold their $1.5 million shack and see an overpriced $700,000 mansion in another market think they’re underpaying. They don’t even ask questions. And local Realtors know that. They love when they can hook a Californian that snowed into their town. Like manna from heaven.

All “gateway cities” are that way, from Miami to New York to Seattle.

Absolutely. My wife and I bought a beautiful home in Texas in 2017 for $248,000 moving from California. My mind was blow at the time that it was even possible. But everyone laughed saying we Californias overpaid. It was a brand new remodel 3 bed / 2 bath on a 1/3 acre lot, about 2000 SF in a good neighborhood. Prices in TX are coming down fast again and I am seeing 2017 prices again. I think another wave of Californians will do the exact same thing once they see TX prices come back down from pre-pandemic prices.

“All “gateway cities” are that way, from Miami to New York to Seattle.”

But the mystery has always been where *exactly* do all these *buyers* *into* California/other “gateways” come from.

By definition, the “home flip” engine doesn’t work in reverse – 90% of sellers in non-coastal locations can’t use home sale windfalls to “move up” to CA insanity prices – their Missouri gains are too small.

So who *pays* those soon-to-be-ex-Californians those huge prices for their houses?

If not other Americans…then it must be intl immigrants.

But that is *vastly* at odds with the human wave “economic refugee” stories we’ve been force fed for decades.

And, to be clear, observable daily reality.

In DC/Northern Virginia there is a huge (but hardly written about) contingent of expectedly economically stressed East African, 1st generation Americans.

How *exactly* does their *effective* demand (what they can afford) somehow magically power $750k median home prices?

See also, trafficked CA Mexican millions and the $1 million LA crap shack.

It isn’t that poor immigrants can’t create *demand* – but by definition the poor can’t provide *effective* demand for $1 million homes.

A lot of youngish people (from the US and foreign countries) come to gateway cities to make their fortune, and many do well, and along the way buy homes, and after a few decades, some (not all) depart with their cash. This is a flow that has been going on forever.

You’re just trying to make up BS conspiracy theories, as you always do about everything. There is no mystery in this. It’s well documented and understood.

There is a 2024 National Association of Realtors report on international buyers if you want to see some numbers. Like ignoring the bottom 50% in the larger economy, you can ignore the bottom X% of immigrants in the stratospheric CA real estate market.

What I can’t figure out is who is buying the California homes and keeping the gravy train rolling….

I have wondered the same thing. It is especially puzzling as California is not creating large numbers of new high income jobs….

Is there data on what % of delisted homes get rented after delisting?

I wonder how many listed homes are either owned outright or have a sub-3% mortgage, making it easier to hold on price levels rather than capitulate.

Would be interesting. Anecdotally, you can get a feel for some of the situations if you look on Zillow at the history of the home, when it was listed, delisted, put on the rental market, pulled off the rental market, listed again at a lower price, delisted, re-listed at a lower price, etc. until it finally sells, if it sells. But data would be nice on this.

In 2008 when low to no down payments were common, it was easier for underwater homeowners to accept the losses. Now we’re seeing that those who bought at the peak with 20% down facing significant losses especially in markets such as California and Seattle. These people have two choices realize the loss or sit out in hope that prices rebound. And as you’ve pointed out, life changing events such as divorce will force many to sell. Once these losses become more and more this will ripple through the economy.

I would not buy a home that has been rented, unless the price were recently dropped 15% or more. It’s a question I always ask. Renting is an indication there is no demand for the home.

The market has been so distorted the past few years I’m not sure that rule works anymore.

I wouldn’t buy a rental home because most landlords treat their tenants like a paycheck and defer maintenance to their house because it doesn’t affect them if it gets fixed on time.

I did it once and the house became a giant money pit because I had to fix 20 years of neglect. I did get a huge discount compared to what a well maintained house in the neighborhood would cost but I don’t think I’d do it again.

Paycheck or sucker, depends on the landlords. Some rare few do want tenants that will take care of their place and will charge a fair rate and not raise every year but those are rare find…most newer gen of landlords both old and young do see tenants as someone to either exploit or pass the bucks (mortgage+expense) to.

Personal example, dealt with a landlord last year, only after staying for one year proceed to ask me near the end of the lease term and asked if I intend to stay and asked how much I think I should pay in increase compare to last year? Guess the guy is so greedy he simply wanted to see how much additional rent he can extract from us, instead of doing homework to see what the surrounding Long Beach area are going for, his cap rate and how much increase he should be asking. When I did give him a number which accounted for inflation, he aruged it was too low and gave me examples of houses much nicer and why he should be charging the same. Long story short, told him to take a hike and think it eventually took him couple of months before finding another sucker.

This type of landlords are the kinds that I wouldn’t mind dishing out some schadenfreude on, if they end up losing their shirt if the market crash and they can’t sell or rent it out at a decent price.

Just about every 4th house in my neighborhood is rented. And there are entire single family house developments in which all the homes are rentals. This works well with low priced, cheap built homes, and we have tons of them here (in Texas).

Zillow shows which listing is from legit homeowners & which listing is from speculators. Wolf’s approach is 👍. If I remember this right – One home in Corona Del Mar (Newport Beach) sold in Dec 2022 for $2.2M. Rented out for $5.5k. Now listed for $9M. What a story! Too many homes sold in last 4 years show an interesting pattern. Unless something I miss, I see similarities between now & 2006. Only time can tell.

The most amazing part of that story is that a house that sold for $2.2 million was rented out at $5,500. Let’s say you paid 20% down. Even assuming you got the 2.8% rate, that is $7,600 a month, and we’re not even including taxes, insurance, maintenance or the opportunity cost lost on the $440,000 down payment.

I believe that rents and sale prices should be reasonably equivalent, over time. If they’re this out of whack, it means one of them is distorted.

Totall sound and one simple comparison calculator that you can find in New York Times (Rent vs Buy calculator) will give you that information..

But think the emotional part of the brain take over mathing for quite a number of buyers out there. When you only preceive a house as a one way lottery ticket and paying rent is like setting your money on fire…paying 30-50% more per month on owning becomes a no brainer when it reality the opposition is true.

I suspect that potential buyers, in addition to the high asking prices, are also hit with the revelation of the real estate tax bill. Which resets to the current tax rate upon sale. The existing owner, if they have owned for a while, is paying relative peanuts (why many CA owners don’t sell unless they have to). Really shafts the young (buyers) and benefits the old (sellers).

Good point.

In the aesthetics department: I recently spent several days in Monterey, CA. Had lived there during the 90s for a spell. The area looked run down to me – aging. 17 mile drive has its top tier wealth and looked maintained. But areas like Pacific Grove looked run down. Spoke with some “natives” who grew up there and they noted that part of the problem was a generational transfer of wealth to younger folks who simply were not up to the challenge of preserving their inherited gift. On the flip side, the area around Sea Side, which had been the dumps durning the 90s, looked more prosperous – probably in part to smart developers after the community cut a deal with Fort Ord after it was BRAC’ed in 1994.

pj – good observation on actual changes in the America family and it’s place ‘in the neighborhood’ today, vs. our relict-memory carried by many seniors. (Did my boot at Ft.Ord, Seaside/Marina were considered ‘the wrong side of town’ at the time…).

may we all find a better day.

Here in Northeast LA, it seems the market peaked in mid-June. From that sky-high altitude, a noticeable amount of helium has already escaped the balloon. Impossible to say what the future holds, but right now a situation in which “he who panics first panics best” seems just as likely as one in which we HODL our way back at new highs.

“he who panics first panics best”

You can be on the train.

Or under it.

@soybeanmagic I have never heard of USPS releasing change of address

or any good way to find out where the people selling our moving other than talking to a top 1% local agent who probably has a staff that tracks stuff like that. @Bobber renting “can” mean less buyer demand for a home or it can just mean that someone likes me wants to keep his last home as a rental.

Really good data, thanks for sharing

Spoke to a homeowner who just delisted his condo in the Atlanta area after two months. Dropped the price over 10 percent and received zero offers.

He had a contract on a house that was contingent on the current one selling. Cancelled it, too, after being under contract for two months.

He will re-asses in late winter.

I suspect this is a representative situation that is repeating in many places. Next spring might exert even greater pressure on the market if prices don’t break loose soon.

It’s an interesting pattern of behavior when they delist a shack because no one would pay the price of their inflated expectations, only to relist it later at a higher price.

It’s also incredible to me that any seller would accept an offer contingent on the buyer selling their other home. To me, that’s a worthless offer. Might as well make it contingent on getting the money from crypto.

I steer clear of places that’ve sat empty for years. They’re a headache waiting to happen: cracked plumbing seals, crusty wiring, funky HVAC mold, aged paint, stuck windows.etc.

Reminder to the housing hoarders: you’re sitting on a depreciating asset, especially modern builds, which go downhill rather quick.

I’m currently in escrow on a house in San Diego. Buying it from my friends parents. They’ve owned it for 20 years and own it free and clear. It’s been used as a rental for the past 10 years. They listed the home on the market, but the tenants were difficult to deal with so they couldn’t schedule any showings and had to turn people away. I offered a little more than what the fix-n-flip guys were offering and got it. It’s a 4/2 single family and under contract for $1.29MM while a couple 3/2 homes on the same street sold for $1.4MM over the past month.

From my anecdote above, the parents didn’t want to deal with tenants anymore since they’re getting older. They were about to delist the property before I showed up. They own 10 other rental properties in San Diego. They aren’t forced sellers. Another home I looked at was an Airbnb where the guy was just fishing for a high price and has owned the home for 15 years. Also was not a forced seller, and eventually just pulled it off the market. I saw the Airbnb listing and he’s getting ridiculous fees. A lot of these people have either no mortgage or locked-in costs that are so low vs. where rental rates are today that they couldn’t care less about selling unless they get a crazy good deal.

Regarding the Airbnb listing, you’re assuming he’s getting those fees, and that his place is occupied most of the time. Based on the whining I’ve seen on the AirBnb Host Reddit sub lately, I wouldn’t assume either of those.

Your comment shows how distorted the market is for younger people.

There is not a chance that any person under 30 could acquire 10 rental properties in SD at today’s prices.

My neighbor in SD is one of these people. They are retired boomers and own a huge home and a 3000 sqft rental property. They were both teachers. Now teachers are struggling to buy a condo.

California specifically and uniqely suffers from Prop. 13 where newbies have to pay 20x legacy owners in real estate taxes.

Anecdotally, I know first hand a good number of younger professionals who left California based on that injustice once they understood it.

Prop 13, while it sounds nice, tends to destroy public schools and government services. It also totally screws any new home buyers. California’s population is declining, accelerated by the out-migration of illegals (voluntary or not) and much greener grass in tax-free and low home value states like Florida, Texas, and Tennessee. All that will be left are geezers hanging on to their Prop 13 benefit, buyers who got the 3% gift (or shackles), those sucking off California’s generous welfare system, LGBTXYZ types, and socialists/communists.