Demand destruction on an epic scale, after the price explosion. And inventories are piling up.

By Wolf Richter for WOLF STREET.

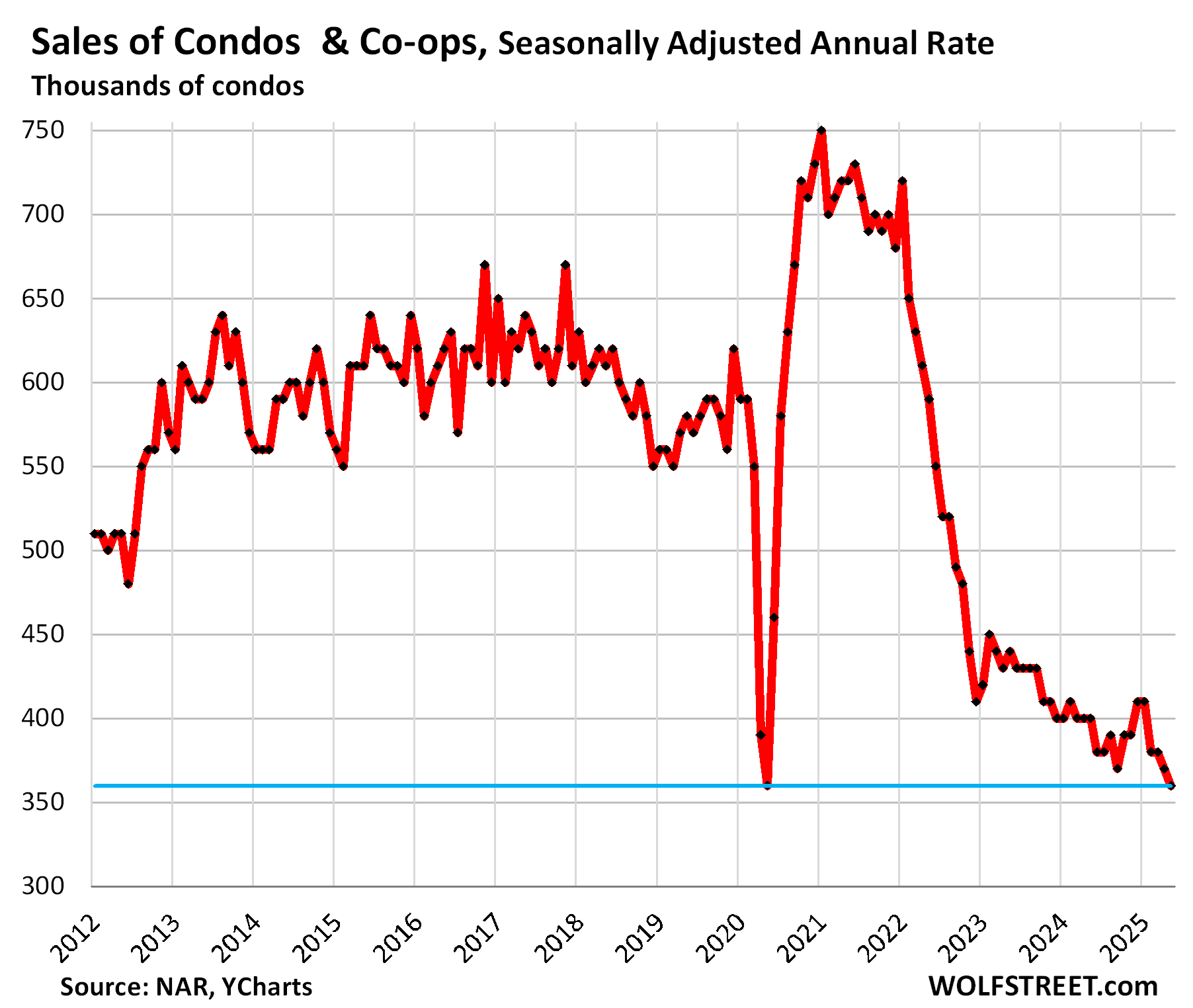

It boils down to this: In terms of condos, sales that closed in May fell further and hit the lowest point in the data, along with Lockdown May 2020, seasonally adjusted; supply spiked to the highest level since the Housing Bust.

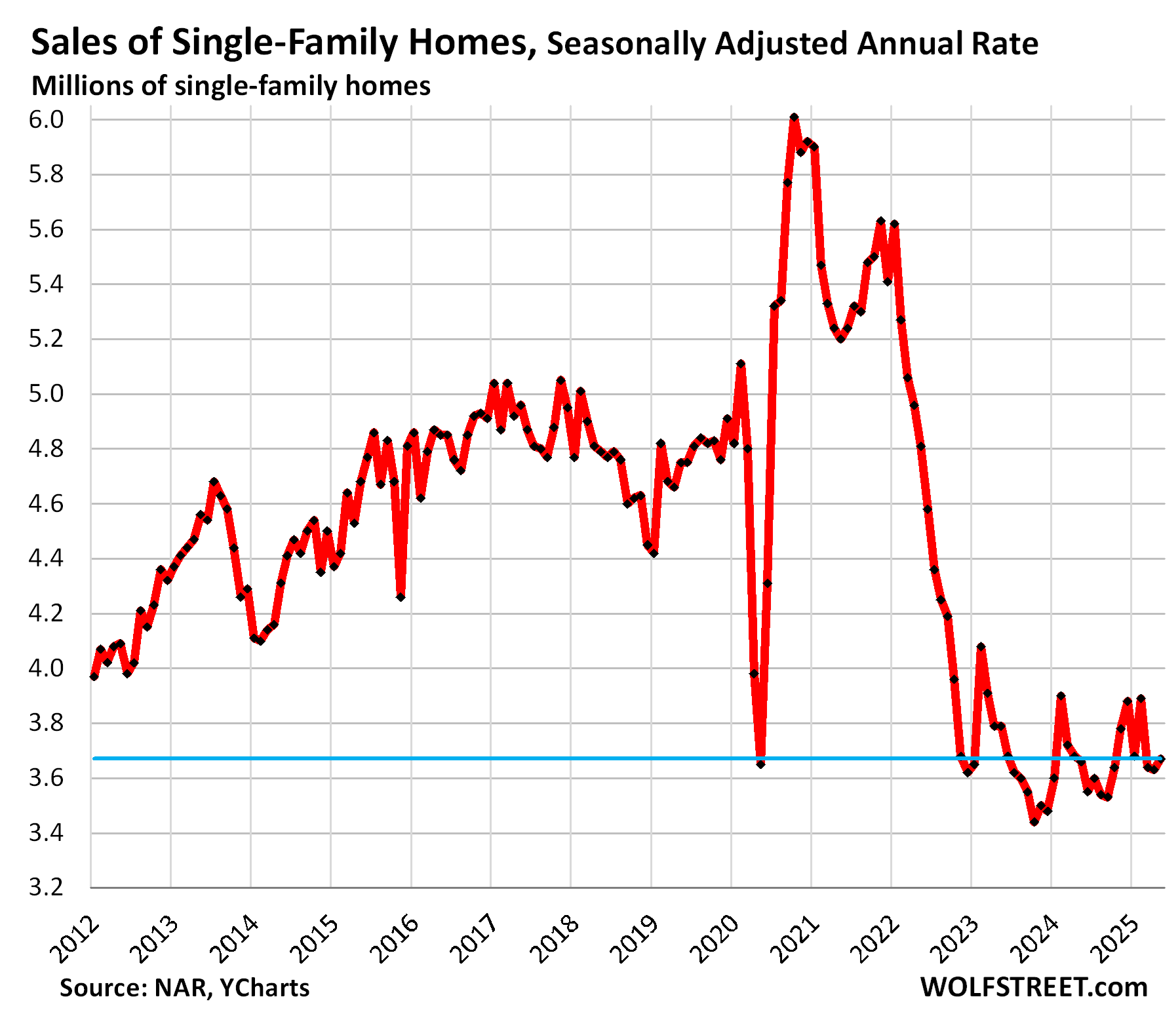

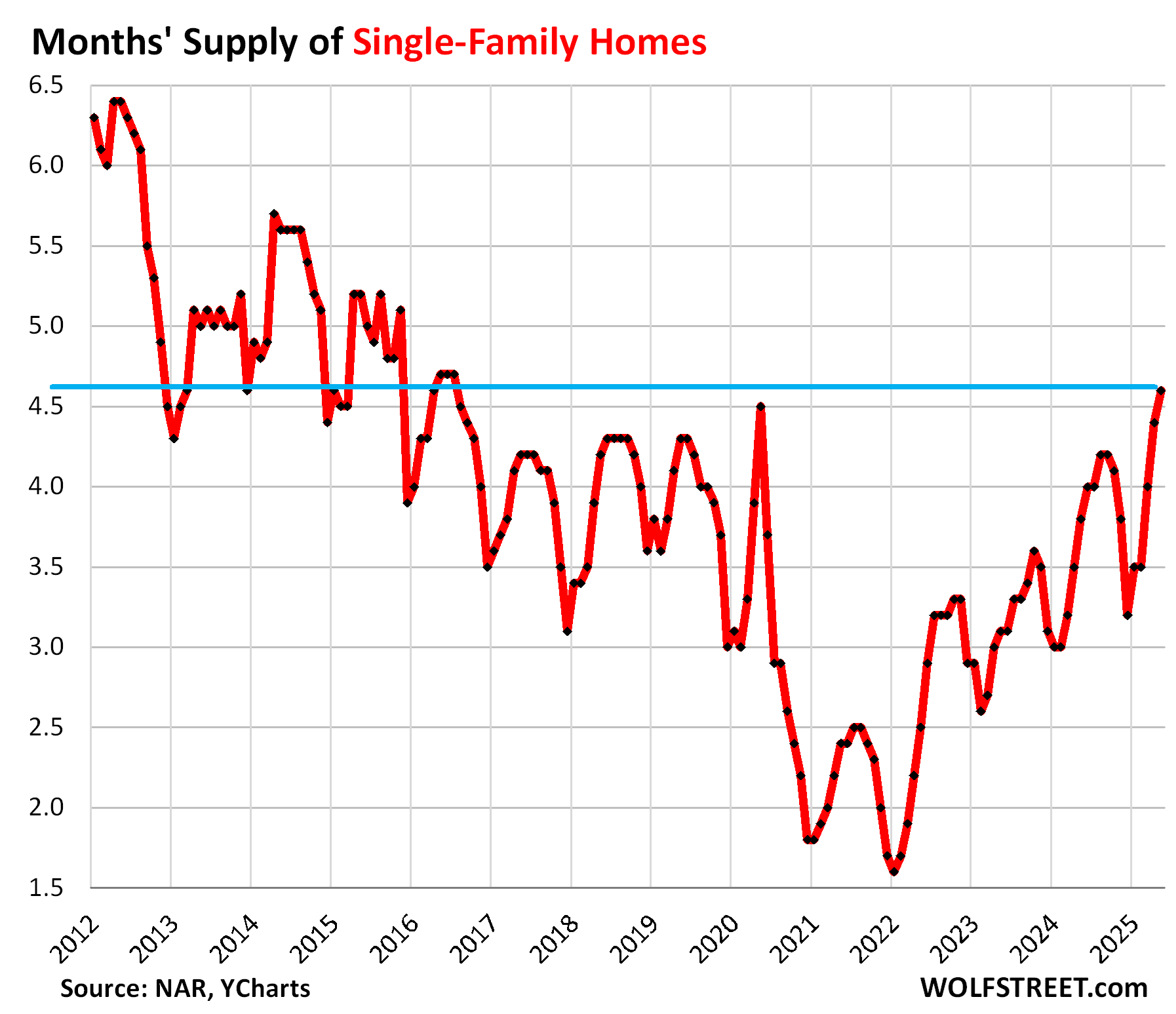

In terms of single-family homes, sales inched up, but barely, and remained at historic lows, and below May 1995, seasonally adjusted; supply spiked to the highest level since 2016, according to data from the National Association of Realtors today.

A Condo Bust is unfolding.

Condo sales, which have been careening lower all year, dropped further in May to a seasonally adjusted annual rate of 360,000 condos, the lowest in the data going back through 2012, along with Lockdown May 2020. Sales were down by 38% from May 2019 and by over 50% from May 2021. Demand destruction on an epic scale, a result of prices having exploded in recent years far beyond what the market can bear (historical data from YCharts):

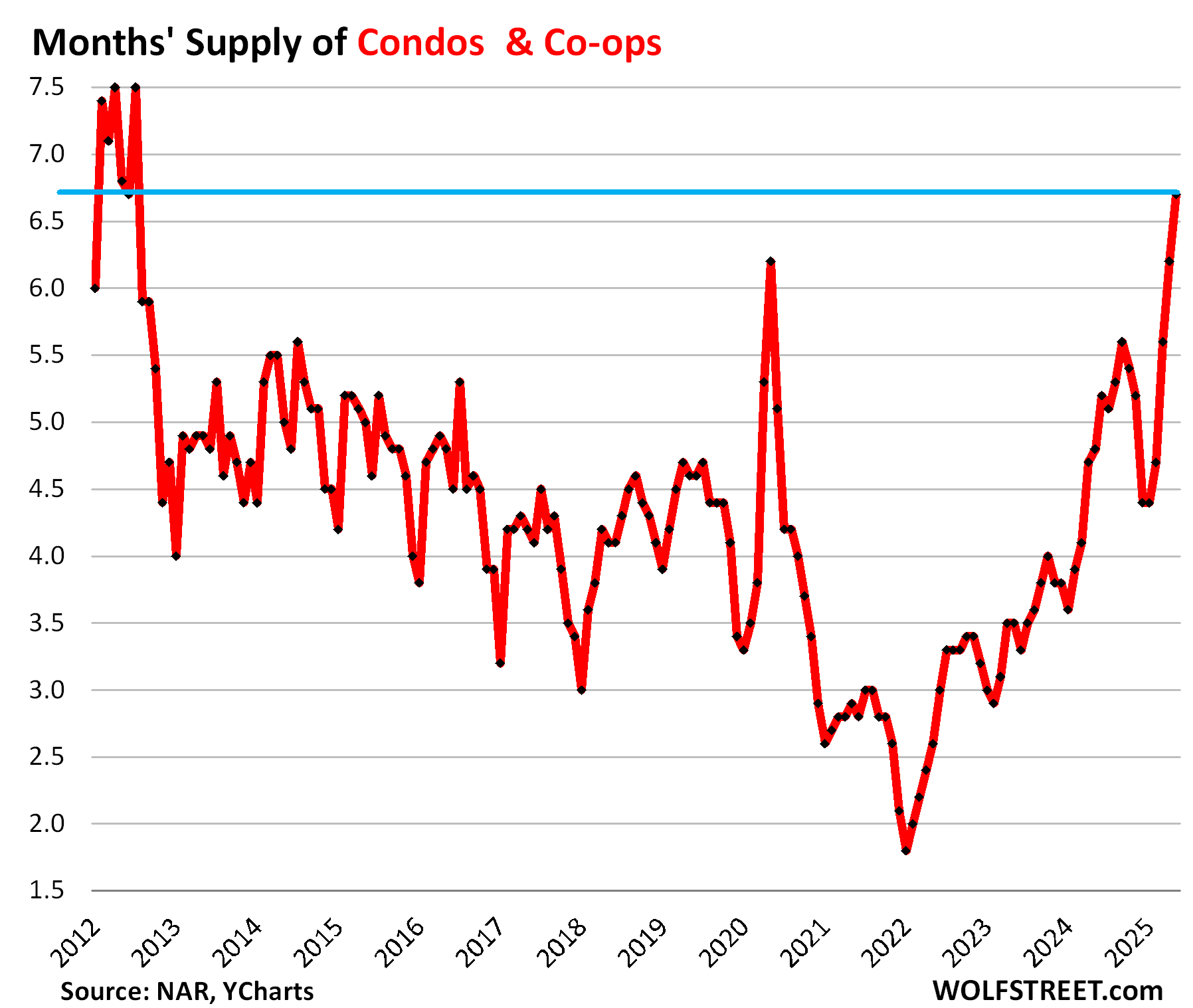

Supply of condos spiked to 6.7 months in May, the highest supply since the Housing Bust in July 2012 (historical data from YCharts):

Single-family home sales still below 1995, supply spikes.

Sales of single-family homes, which have been hobbling along the lowest levels since 1995, inched up a hair in May to a seasonally adjusted annual rate of 3.67 million homes, roughly flat with May 2024 – with 2024 having been the worst year since 1995. Sales were down by 23% from May 2019, down by 29% from May 2022, and down by 9% from May 1995 (historical data from YCharts):

Supply of single-family homes spiked to 4.6 months, the highest supply since July 2016:

When sales began plunging in 2022, the theory by the real estate promoters was that sales were plunging because there was a housing shortage and there was nothing to buy. But sales continued to plunge even as inventories rose, and now inventory is piling up and sales remain at collapsed levels, and the real reason is that prices have exploded beyond what the market can bear, and so demand has plunged because prices are way too high (historical data from YCharts).

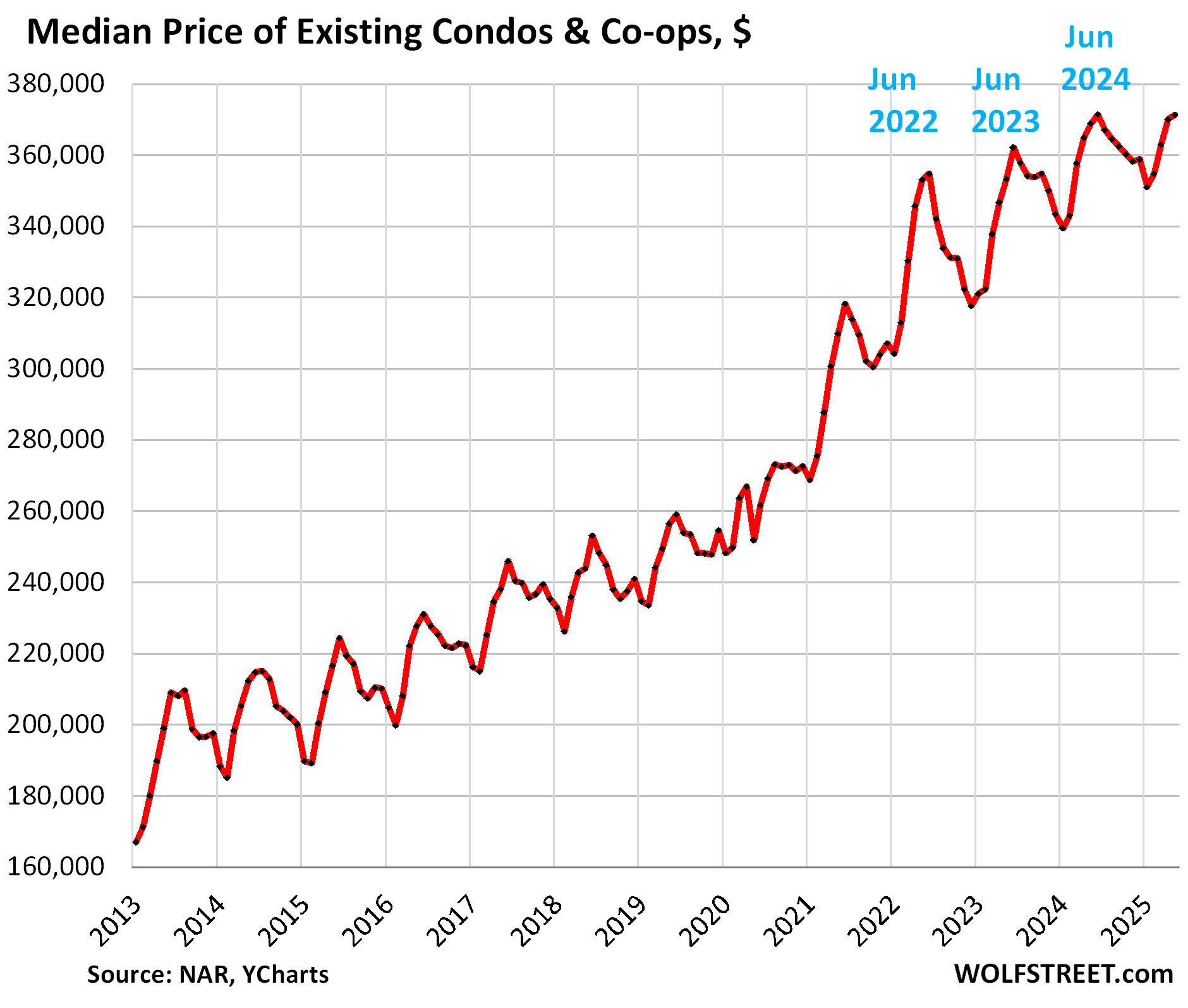

Median price for condos and single-family homes.

The median price can be heavily skewed by changes in the mix of homes that sold. In the spring, nationally, a larger number of higher-end homes come on the market and sell, which changes the mix of what sold and shifts the national median price higher. It does the reverse in the fall and winter. This contributes to the seasonal ups and downs of the national median price. Nearly every year, the national median price peaks in June and then declines through January or February (the exception was 2020).

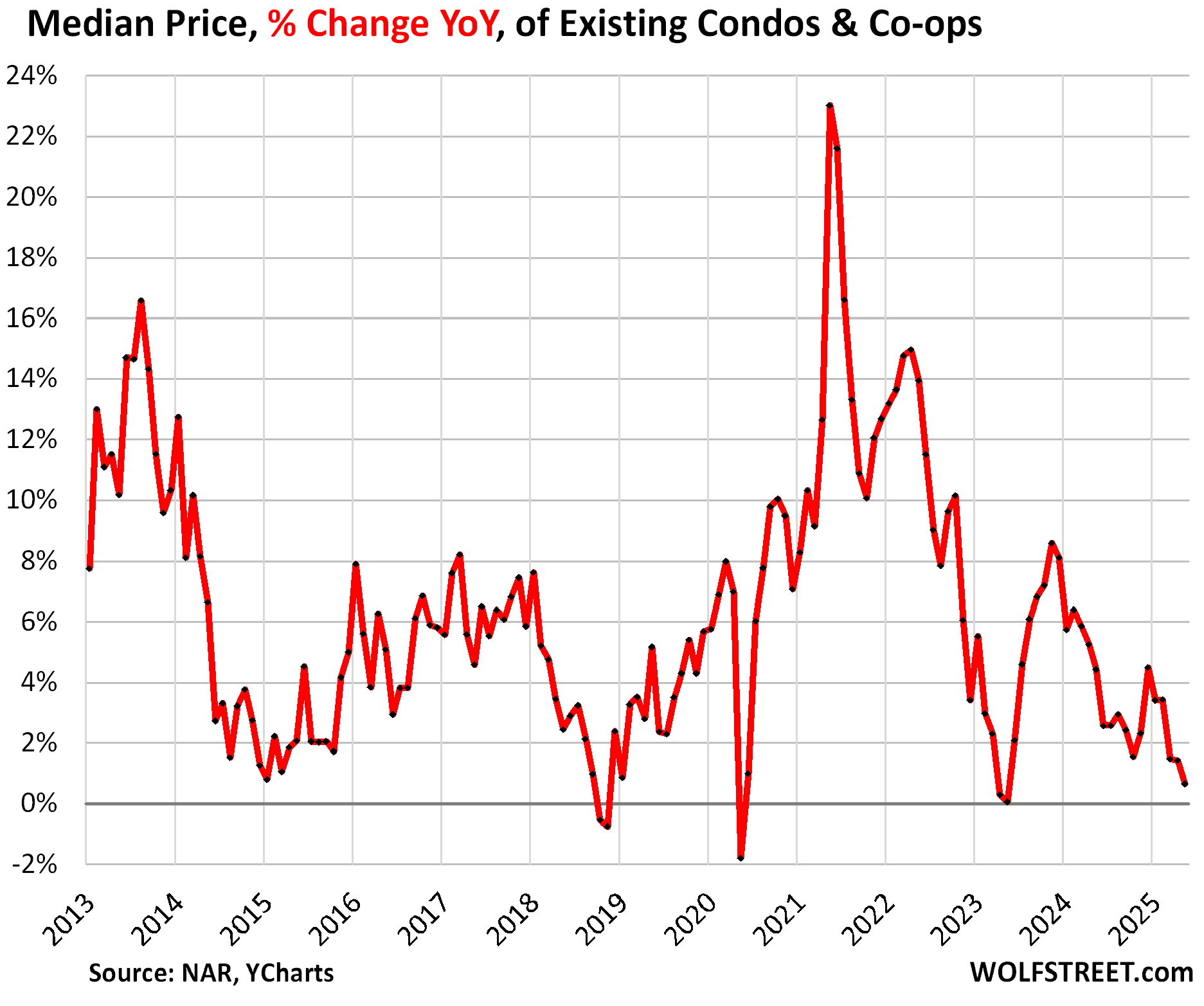

But the seasonal increases in May and in recent months have been weaker than in prior years, and the year-over-year gains have been melting away.

The median price of condos inched up just 0.3% to $371,300 in May from April, according to the National Association of Realtors today. That tiny uptick was far smaller than typical in May.

This measure of the national median price of condos has spiked by nearly 50% in five years, driven by the Fed’s interest-rate repression and FOMO.

In many cities, condo prices spiked by 60%, 70%, even 80% over those five years. Now prices are simply way too high and don’t make economic sense anymore.

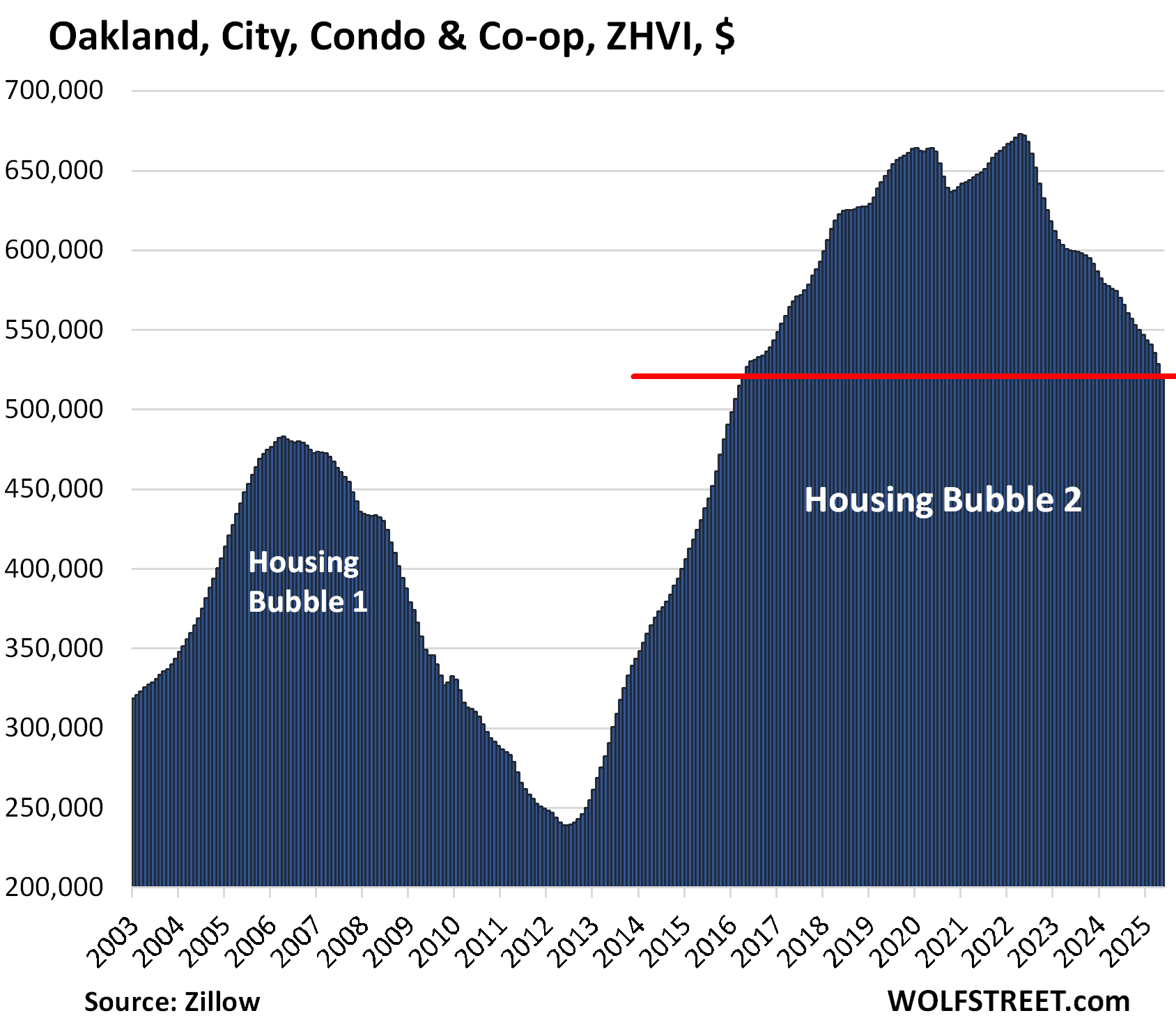

So in many cities, condo prices peaked in 2022 or 2023 and then started careening lower. Here are 20 bigger cities where condo prices have dropped by 10% to 23% from their peaks, unraveling the most epic condo bubble ever. Other cities are following with a lag. Some have just recently turned the corner.

For example, Oakland: Condo prices have returned to where they’d been in April 2016. That was 9 years ago. The pace of the price drops accelerated, with a month-to-month drop of 1.7% in May, seasonally adjusted, according to the Zillow Home Value Index.

The year-over-year percentage gain of the national median price of condos was whittled down to just 0.7% in May, from +1.4% in April, and from the range of +10% to +23% during the price explosion in 2021 and 2022.

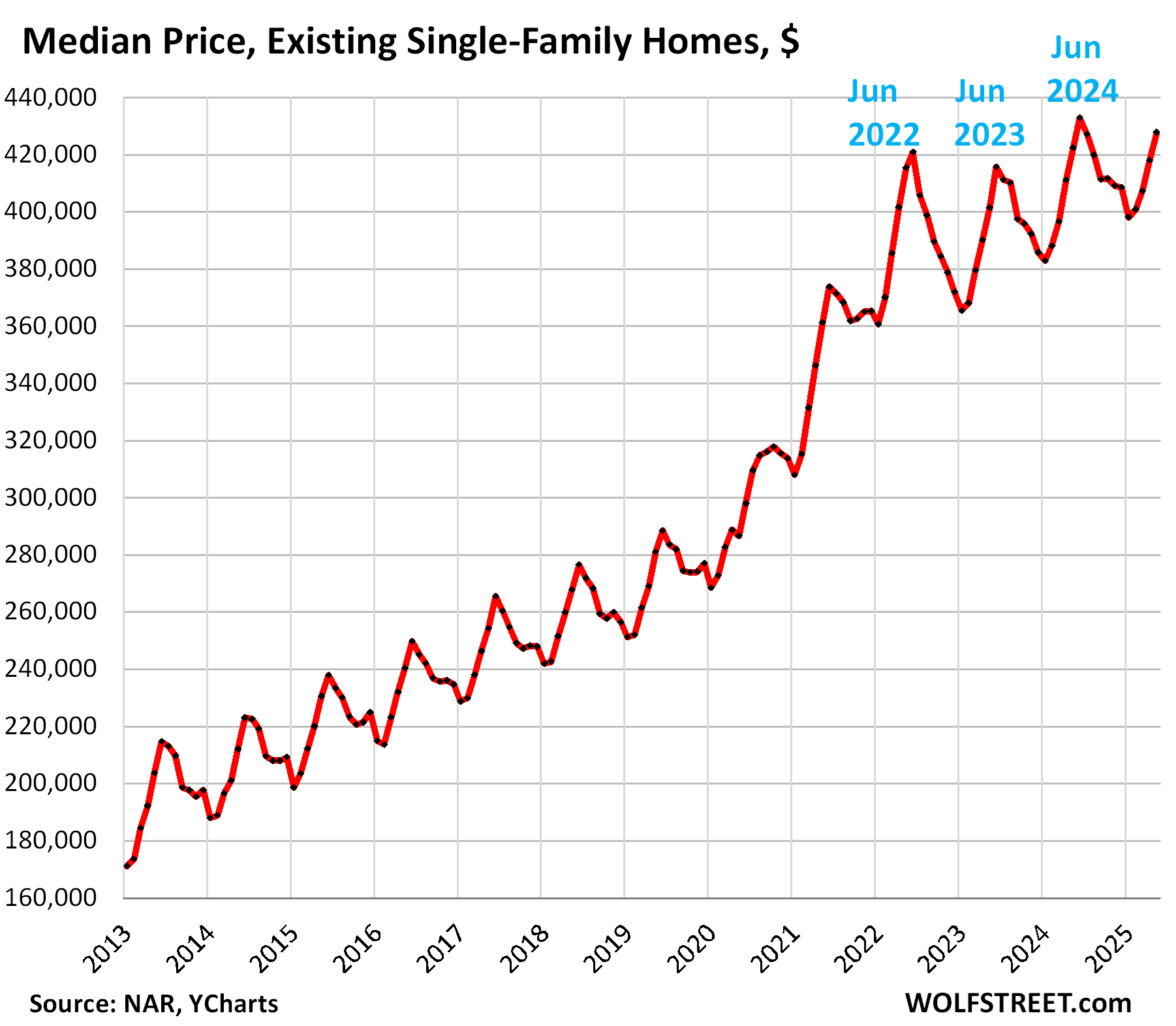

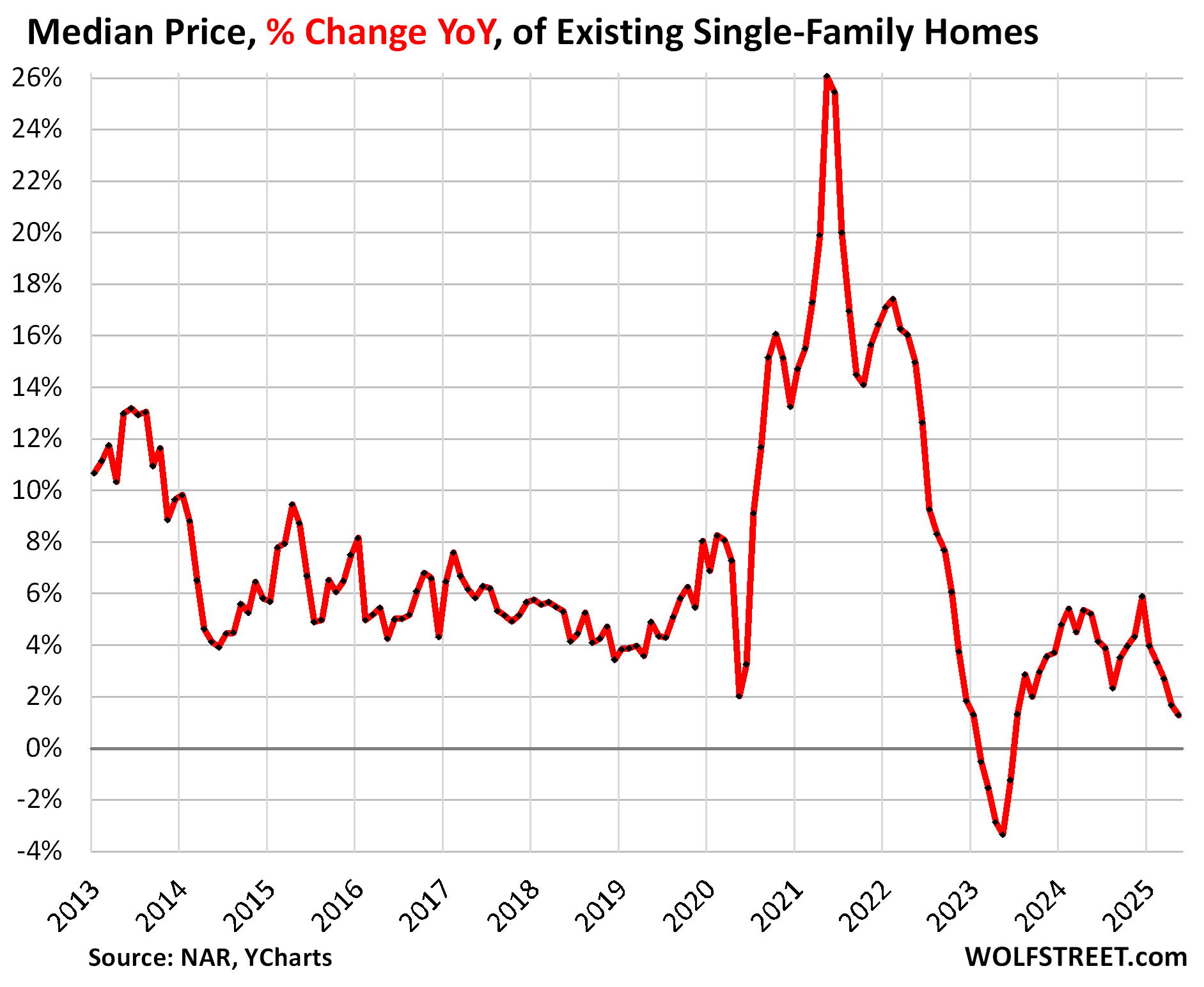

The median price of single-family homes rose to $427,800 in May, whittling the year-over-year gain down further to just 1.3%, the fifth month in a row of narrowing year-over-year gains (from +5.9% in December).

This measure of the national median price had exploded by 50% in the three years between June 2019 and June 2022, on top of the large price gains in the prior 10 years.

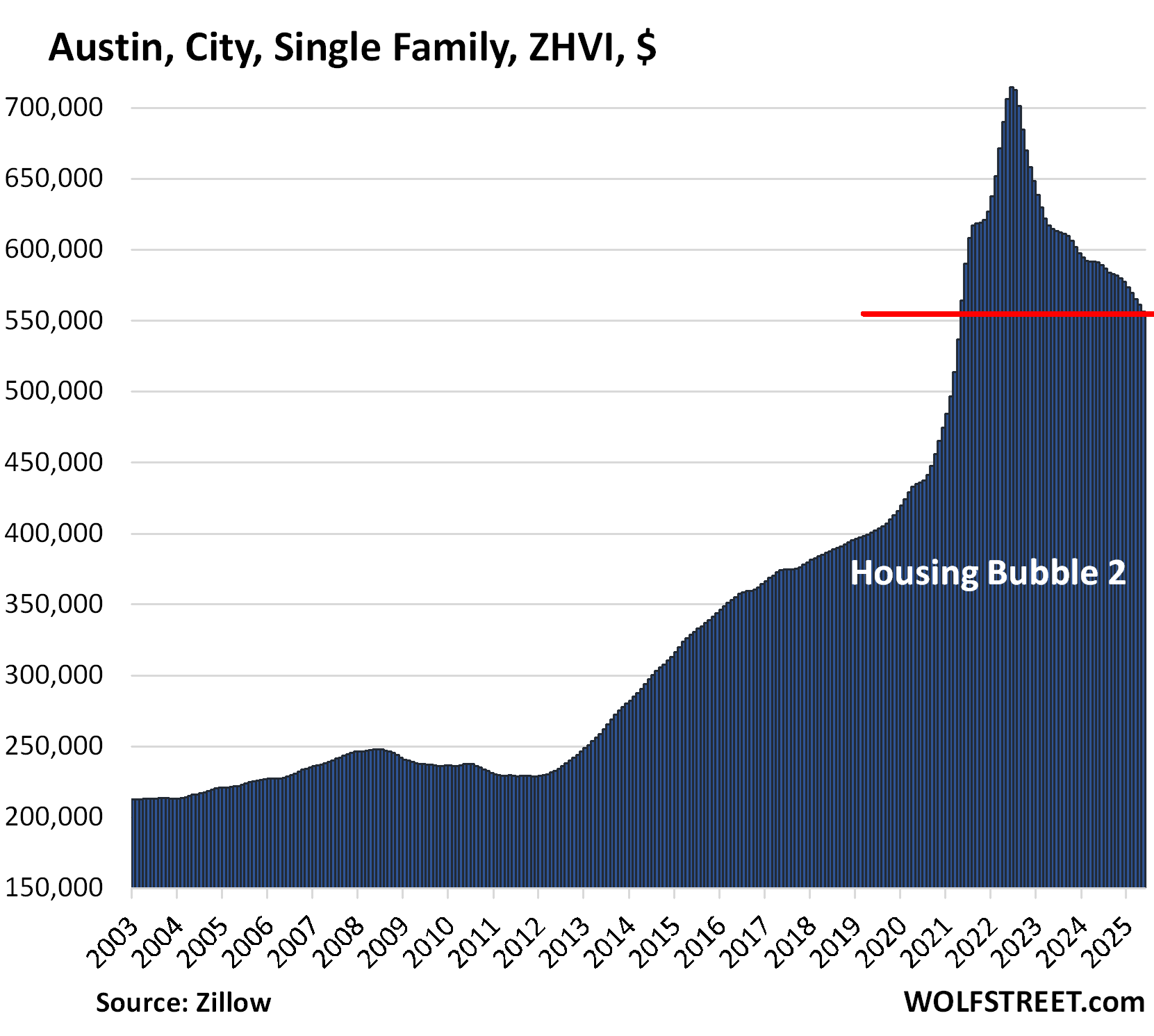

But lots of markets have turned. In 10 big cities, prices have declined by 8% to 22% from their peaks: Austin, Oakland, New Orleans, San Francisco, Washington D.C., Denver, Portland, Phoenix, Fort Worth, and San Antonio. Other big cities also experienced price declines but aren’t at 8% yet. Some smaller cities, such as Birmingham, have double digit price declines. So here are the 10 Big Cities with the Biggest Price Declines of Single-Family Homes. For example Austin:

Year-over-year, the national median price of single-family homes was up only 1.3% in May, the smallest gain since July 2023 when the national median price emerged from a period of year-over-year declines.

During the price explosion, the year-over-year increase peaked at 26% in mid-2021, which was completely nuts, and those too-high prices then triggered the epic demand destruction we’re now seeing. The market solution to this type of demand destruction is lower prices.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Where I live in an affluent area of Florida, homes are still selling and getting good prices; not as high as before, but still too high considering incomes. It is taking longer for the sale, but still selling at very high prices.

Condos, are not selling to well, though sellers are not lowering their prices much. So no liquidity for the seller, or no availability for the buyer…they must be too far apart. In previous situations like this, the sellers just waited it out for the market to return, i.e. a few years or a little longer.

No one said there were zero sales. Sure there are some sales, and obviously some homes are still selling, or else there would be no transaction prices. But sales are way down.

This “good price” you speak of is a lower price than a year ago and two years ago, but still too high for sales to return to normal.

Seems you’re in Naples (IP address), so you’re looking at this scenario:

Single-family: -6.7% YoY, -6.9% from peak in April 2024, -0.7% MoM, prices back to April 2022

Condo: -9.9% YoY, -12.0% from peak, -0.9% MoM, prices back to April 2022.

Look at that graph 400k to 700k in not even a couple of years absolutely insane. I hope the bust is equally violent.

“absolutely insane” is the correct technical lingo for this situation.

Funny how that works…majority, especially for the vested homeowners, this “absolutely insane” is all par for course, totally normal, nothing to see here, it is what it is…

But to imagine anything more than 10% down is absolutely not possible or the sky is falling because the housing will never be down narrative is such strong gospel, fascinating to see nonetheless

What’s insane is the payment of interest on interbank demand deposits. This resulted in Wolfs “interest rate suppression”. This propelled housing prices beyond any reasonable value.

The prescription for economic success is high real rates of interest where funds are expeditiously activated into real investment outlets.

As you wish, AGREE!!!!!!!

Keep dreaming

Hey Wolf, thanks for the update. Do you believe the administration might start making moves to support the slump in sales?

Recent look at Freddie Mac FMCC price up 587% from a year ago.

Maybe now that we have peace in the middle east something is in the works to pump economic support domestically?

The only thing FMCC’s price gains have anything to do with is whether or not Freddy Mac [FMCC] is going to get privatized, after having been put under government “conservatorship” during the Housing Bust. The administration has been talking about it, and I’ve published an analysis of the issues involved here:

https://wolfstreet.com/2025/04/01/not-another-free-lunch-dont-let-fannie-and-freddie-turn-back-into-gses/

Privatizing the GSEs might be a negative for the housing market as it might push up mortgage rates, depending on how they work out the government guarantee currently in place on mortgages that they securitize. It’s certainly not anything that would support the housing market.

Ackman wants to buy Freddie and Fannie (whoever named these must have been a Queen fan)

and he wants to raise mortgage rates a good bit higher.

So the future homebuyers will be making he and his ilk richer.

Nick, I almost laughed (no disrespect intended) at your question – “Do you believe the administration might start making moves to support the slump in sales?“

That’s NOT the Fed’s job. Not at all. That’s the job of the free market.

Prices are WAY TOO HIGH and they need to come down. When they do, sales will increase.

I read in Naples 70% of homes r empty. Most FL home owners r in denial. He sounds like one of them. There r real stats to contradict him

Where are you? I’m in Palm Beach County also in an affluent area, and from what I’m seeing, only “turnkey” homes are still selling at those good prices. Anything that needs work is sitting.

Anything that needs work can’t get insurance to satisfy the lender so it has to be an all cash purchase. It’s not even a matter of cost of insurance; they simply won’t.

That’s true too, but I wasn’t even referring to needing a new roof, but ones that are just not “new.”

The houses with the 15-20 year old or older kitchens and bathrooms are sitting. The only ones that are getting good prices have new roofs, new ACs, new kitchens, new bathrooms, impact glass and doors.

Thanks for the ground report Dan,

I am sure Florida home prices would fall hard. The signs are everywhere.

It’s a matter of time.

My mother has owned a condo for over a decade in North Naples and is considering selling. Comps in her building sold for $375k at the peak are now sitting at $325k and being delisted. Still double what she paid after GFC.

She rents it out part of the year. The problem is: i) increased common charges after surfside, ii) increased homeowner insurance after her first company dropped her, and iii) increased taxes based on recent property values. Now the rent matches the monthly expense at just over $3k – despite the mortgage only being 20% LTV and at COVID rates.

If this is a bad hurricane season,prices on the West coast of Fla will fall even further. Insurance rates up,HOa fees up.

Same

I guess it’s kind of like if someone takes a few grains of sand from a beach, it’s not very noticeable.

Then an article comes out, Sand is disappearing from the beach.

Never mind that it is a man made island and they have been dumping truck loads of sand on it for the past 15+ years.

None the less, I do appreciate the articles and comments section.

Just me, or does HB1/HB2 graphs seem to infer we are on the crest of disaster, if not a larger speculative bubble. We blame the GFC on widely reckless lending, no docs, ARM rates, and synthetic junk paper. But here we 20 years later with historically high home prices, and virtually none of the same lending practices. So if prices drop significantly its has nothing to do with lending or wall street and everything to do with human behavior.

Encouraging to see for sure, although wishing this is also spreading fast in SoCal as well but maybe in due time.

Wonder how this big adjustment down is having an affect on condos/houses removed from listing entirely. Saw a headline today stating houses for sale being removed from listing (withou being sold) is at the highest for a long time. Looks like there are still plenty of sellers thinking if they come back later they can get top dollar. This might also be true based on my very anecdote evidence, been getting way less of the Refin for sale emails like I experienced just a month or two ago, so either houses/condos are still selling or there are a lot of pulling off the market until better days..

Or how about this hopeful strategy? “Let’s just rent it out until the market improves.”

Of course, we at Wolf Street know that hope is not a strategy.

Condos will be rented out, rather than sold. They are smaller units and are located in prime working areas. Prices for these homes reflect single family homes, bizarre for something that used to be an entry for housing. If there are to be a correction in housing, it will be these. Less amenities and a smaller foot print. I see these go for a mortgage payment in my area for rent.

“Condos will be rented out, rather than sold.”

1. Look at the #2 chart. What does the huge spike in supply tell you, highest supply since 2012??? Those condos are coming on the market, that’s what it is telling you. Owners ARE trying to sell them.

2. If you purchased in recent years, your cash flow from rent, if you can even rent it, will be far lower than your cash expenses (mortgage payments, HOA, property taxes), not including special assessments. So every month, that condo is sucking cash out of your account and is losing value on top of it. It takes nerves of steel and a fat account full of disposable cash to sit this out.

Not in Canada. Massive oversupply. Big whammo coming.

The HOA fees, my god the HOA fees!!

Not unheard of to see monthly HOA fees greater than monthly *rents* were in living memory…(and by living memory I mean 2000…)

cas127

A lot of HOA fees are for paying the master insurance policy. They are sometimes like 60-70% of the budget. Lawn care is really expensive too.

But yeah mostly a PIA

FSBO property in my neighborhood wanted to make 50% by holding a place for two years. They even wrote some BS description about how they planned to live there forever or whatever, but had to move for work, and tried to imply that work had been done to the place. Just removed the listing with no sale. Guess they didn’t actually have to move after all?

Another place had trouble selling even in 2022, until it did for a discount. It’s horrible – I had to know for myself by going to an open house when the guy tried to resell it a year or two later at $200k profit. That one will sit forever. The guy moved across an alley to a new place, so I guess he doesn’t have to sell. Everyone (well, half of everyone) is still rich after all that QE.

We could see an uncle point and a big, sudden, collapse down.

Real estate crashes take several years to play out. Some markets will drop double digits YoY, but most markets will crash by 5% YoY declines for 5-6 consecutive years

“but most markets will crash by 5% YoY declines for 5-6 consecutive years”

Is that what happened in 2008?

ZIRP is a helluva drug and panic a helluva thing.

For me, the mystery is why the speculators weren’t on the first unZIRP train out of Dodge in 2022…

But in 2008 it was precipitated by mass defaults after huge numbers of mortgages had their rates adjust sharply upward, and a major bank invested in them failed (Lehman). So far there’s nothing like that on the horizon. Household debt is much less now, and foreclosures are nothing like that, so it may not materialize. But we know what to look out for as warning signs.

“ Is that what happened in 2008?”

Yes, crash went from 2007 – 2012. The national 27% decline didn’t happen all at once.

Dave,

The cliff diving of prices was concentrated in 2009-2010…the earlier and later periods of 2007-2012 had downward slopes that were much, much lower.

Basically, long, delusional periods of over-valuation prime the pump for cliff-diving price declines – as the mass of poorly informed speculators (who mostly look only at very recent trade prices) finally panic and dump once prices decline enough/long enough.

ZIRP from 2012 to 2022 created a *massive* amount of over-valuation. That which is affordable at 2% rates ceases to be at 8% rates – the discounted cash flows that pencil out at 2% become laughably impossible at 8%.

Nope. 2008-12 was a once in a lifetime opportunity.

There will be markets here and there that crash like that (Austin), but what is much much likelier to happen is nominal prices stay flattish, losing to inflation while incomes catch up to payments over the next 3-5 years.

Still holding onto that mythical idea that 3 years of minimal real wage growth will magically makes homes affordable again I see.

Sorry boomer. Your net worth is going to take a massive hit as home prices continue to slide.

Are you kidding?

The owners who wanted to sell didn’t start lowering their expectations and prices until 2012.

They were holding on to a hope they would get more later.

In 2008-9 no one even knew what hit them.

Monetary policy is tight. The FED should lower interest rates. But not even a 1/4 point drop will help housing.

Multifamily is a terrible way to live, if I get pinched, I’ll get a roommate in the spare bedroom and bath…Florida condos got some relief this year but if it’s 30 years old you got major reserve requirements forthcoming and their are 900,000 units 3 stories high or 30 plus years old…stay in your single family

Getting a roommate is the last thing I would hope to have happen. Never had a good one ! Goodness, maybe it’s me.

Ownership is expensive but so far, worth it. Just not at these prices.

Stop trying to be their friend and let them live their life.

They don’t want to share a nespresso with you!

lol I’m kidding around. Haha

“Multifamily is a terrible way to live, if I get pinched, I’ll get a roommate in the spare bedroom and bath”

So…you rather have someone *literally* in your space (shared kitchen at minimum, open bathrobe wandering at maximum – okay, maybe serial killer at maximum) rather than having your *own* completely unshared space in even a studio apt?

You are a rare bird.

Some high-end apartments rent for $30,000 a month. “Renters of choice” — that has been the target group of all new multifamily construction for two decades — routinely shell out $6,000 to $10,000 a month in rent because they like the relative luxury (including that the staff takes in your packages), and they don’t want to live in a house out in the boonies. Many of them prefer to rent because of the location, the views, the flexibility, the amenities of the building (staff, pool, weight room, etc.!), no maintenance and insurance issues, no property tax issues, etc. Gazillion excelled with his clueless comment.

Good luck explaining any logic of why someone wants to rent to boomer brains infected with house humping brainworm. You tell them you prefer to rent, they look at you like if you’re from the third world if they assume you can’t afford. If you can afford it but refuse to buy and sit on the sideline, they look at you with contempt like you just literally burn a pile of cash in front of them like Joker did in that scene in Batman…real time seeing their brain glitch out..

Had that happened to me couple of times, one from a friend that bought in San Diego during crazy bidding war period and he overbid to get his condo. Time will tell if that’s a wise investment but it’s quite amusing to see he simply cannot understand why I am doing my part participating in buyer strike

“House humpers”…nice phrase.

Basically, the 2002-2022 madness is a terrific example of half-understood economic advice that gets turned into near-religious dogma through secret personal uncertainty/fear.

The “house humpers” massively internalized the decent *historical* advice that buying sometimes/usually outperformed renting (if buyer had *actual need* for the significant incremental space…like 1-3 kids).

But no economic advice applies in *all* situations – once the ownership-to-rent price ratio passed a certain point (especially considering all the costs unique to owning) that historic dictum became inoperative – and, soon enough, madness.

But for the frightened speculative types, who fear they – in retrospect – maybe didn’t do enough due diligence, their fear transmutes into ever more strident public “certainty” – because the alternative is just too horrible to contemplate.

So, now, the sequel.

Always enjoy your analysis

Security Analysis by Wolf

Page 1 of 1:

Ahem,

RTFAGTFA

For sale on Amazon for $50

Signed copy $1,000

@Phoneix_Ikki wrote: “Saw a headline today stating houses for sale being removed from listing (without being sold) is at the highest for a long time.”

In 1995-98 and 2009-12 many homes and condos came on and off the market folloing this pattern.

1st time What they paid + Real estate commission + Profit

2nd time What they paid + Real estate comission

3rd time What they paid

4th time What they own the bank + Real estate comission

Most people that don’t have to buy are better off waiting (since most people that don’t “need” to sell are waiting) but for anyone making a move that wants to buy (or married to someone that wants to buy that they want to keep happy) should look for homes that an estate is selling. More often than not after the last parent dies the kids (usually in their 50’s and 60’s) just want to sell the house for cash (and you don’t have the drama that comes with trying to get a guy to sell for “less than he paid”)…

5th Time: What they think the bank bill accept as a short sale.

6th Time: No listing, just walk away and jingle-mail the keys to the bank.

Agree on tipping point where sellers get motivated and start to overwhelm the less-motivated buyers. Then prices drop more rapidly.

Oakland seems to be at that point.

Aaha…..the chase the market down syndrome that many have seen in San Diego last time around. Will it happen this time? Hopefully and let’s just say SoCal definitely need it badly to burst that seller hubris that have last for close to 5 years now, this picture is getting real old..

Oakland has to solve the crime problem or that drop will not correct.

For CA politicians, crime is not a “bug”, it’s a “feature”. They “could” fix it, just like they cleaned the streets and moved out the homeless for the visit of Xi, however there a lot of money to be grifted via all the social programs so the grifters endure the problems never get fixed.

The hill people will be fine. They can afford their $3m house with views and private school for the kid(s). The rest of the ‘Town, well, it’ll be the crime infested pit it’s been since my great grandmother warned my dad not to go below MacArthur (or Hollywood in those days)

“Oakland has to solve the crime problem”

Hell, it has only been 80 years…give them time…

Perhaps if there was a free market in housing without the domination of the interest rate curve by the Fed. I’m not suggesting that the synthetic economy is bad for me but rather bad for most people.

Let us not forget that the bubble in housing is an artifact of QE. zero interest rate policy.

Value has no anchor at ZIRP.

If there were a free market in housing you’d have to get rid of Fannie Mae, Ginnie Mae, the FHA, VA programs, and a host of other state and local housing incentives. Mortgages would be private with 10 years being the ceiling and private mortgages would would run at 10% interest rates. Prices would utterly collapse, taking out most of American’s perceived wealth. The government would be voted out and a new party elected that promised to bring back the old days of high housing prices when America was Great!

Kent, you hit the nail square on the head with that post!

HOA fee inflation likely has a lot to do with this trend. Labor, material, insurance, etc. inflation driving them up. But they are not affected by condo prices up/down. HOA fees trigger fear in buyers. They might double after buying the condo. Rarely if ever do they go down. Even as an owner, one has minimal to no control over HOA rates.

To wolfes point. The fed lowers interest rates and the 10 year goes up. With the easing of capital requirements on banks maybe we can rig these rates lower at the expense of a future crisis. Condos are in a real pickle. I have seen weston fl units sell 15% cheaper than 2 years ago in the same line and they are nicer than the comparable.

You bet! We sold my mother’s condo in 2011(I know, worst timing ever), but the massive HOA fees depressed the price even further. If half your monthly nut is HOA fees (which you have little control over), that leaves less for the mortgage = lower sale price! Ouch!

My parents bought a house in LA in 1960 for around $15k, and sold it 8 years later for a $400 profit.

That’s how real estate once went.

Indeed. House prices were $15,000 to $25,000 in Hermosa Beach and Manhattan Beach in the 1960s and what you got was a dumpy little old House. Now, you still get a dumpy little old house on a 30’x80′ lot but prices are well into the 7 figures and headed into the 8 figures.

It seems like housing inflation increased rapidly starting in the early 80’s. At least in CA. Partly due to high real inflation, partly due to Prop 13 rolling back and locking in property taxes, and partly due to slower building on the coast. Maybe also because of the California Dream at the time. The entire US thought that CA was Nirvana and the masses migrated there. Sort of like Austin, Boise, Phoenix, Denver…. during the last few years.

Everyone is looking for Nirvana which includes a high paying job. CA seemed to maintain the higher paying jobs with the better weather, but with the cost of higher expenses and many more people.

My parents moved to S CA in the early 70’s, before the gold rush, and sold their house in WI for the same price and size as the house they purchased in S. CA. The price difference changed rapidly starting in the 1980’s.

It is also true that Milwaukee was a booming industrial manufacturing city in the 60’s and 70’s with high wages while sleepy S CA was mostly lemon and orange orchards with some film jobs and the start of the aerospace industry.

That flipped in the 1980’s.

Not looking at Milwaukee or S CA, the population of LA County alone in 1960 (6,039,000) exceeds the population of Wisconsin in 2024 (5,961,000). The shift in to population to California generally, and Southern California specifically, happened long before though it continued through the 1980s (when LA County exceeded 8M). All those people were employed by more than lemon and orange orchards, some film jobs, and a nascent aerospace industry.

We’re one hurricane away from a housing market crash. All it will take is another doubling of insurance rates in Florida and the race for the exits will be deadening.

That was before America’s national strategy was to debase the currency as a strategy for building wealth.

With mortgage rates at 6.98%, home prices need to drop around 40% (from the peak) to have the same level of affordability as when mortgage rates were 3%. As most people borrow the money for a home purchase and affordability is calculated on monthly payments, not home price, this should give you some idea of what prices need to be to restart the housing market.

Some people with overpriced mortgages but access to capital can buy 30 year treasuries with half the cash of the purchase to cover the mortgage payment and rent it out until the sales value is sufficient.

I know, a small number of lucky people, convinced of their prowess.

I finally did that with my mortgage money, mostly just to keep it as a cheap loan if I ever need it in the future.

Well, I’m in bills at the moment. Not sure what it’ll take to get me in on a bond.

(1) Houses were already in bubble prices when rates were 3%. So drop >40% possible (watch Oakland).

(2) Offsetting that, the wage side of inflation has shifted typical incomes up about 20%. So monthly payment affordability could be restored with smaller price drops.

(3) I’m not confident mortgage interest rates will stay at 6%, we could see 10% if Congress continues to lose the support of the bond market. “Affordability” at 10% is a lot lower in price than 6%.

It would be interesting to see a chart showing median monthly mortgage payment as a percentage of median monthly income over the last 30 years.

There are home-ownership affordability trackers that are based on local home prices at the current mortgage rates (principal and interest payments), local wages, local property taxes, and local insurance costs. The Atlanta Fed has one that is interactive and you can choose your metro and see.

A post pandemic dynamic has been the unique effects of CRE demand collapsing, largely related to WFH — and the decrease in demand for office square feet.

The backdrop there, was too many underused and unwanted old buildings — and now, we see a glut of older condos experiencing similar fatigue.

I made that last part up, but assume there’s a tsunami of older condos that probably need bulldozing?

In that big picture, it’s interesting to see the bifurcation of old unwanted investments, versus the siren song of the AI age, and mindless new smart structures (whatever those are).

I don’t see that demographically driven narrative in mainstream stories — but, as these condo prices crash, who’s gonna walk into those cash pits and literally burn up future value?

This is kinda getting into complicated social order, in terms of how cities will function — as these older buildings and living spaces fall into disrepair.

Taken out several years, as AI efficiencies modify the labor force, what’s the interplay between a crumbling old world and new world no one can keep up with, or understand?

I don’t get the vibe that condo pricing is headed towards mean revision equilibrium — I think their headed towards the same exact fate as drive-in movie theaters.

There will always be people that want easy living with an ocean front view but can’t afford a 40 million + home. Condos fill this need. Condos have poor appreciation in general so when they accelerate in appreciation then you know a huge correction is coming.

Hell I’ll buy a ocean front condo here in FL for the right price as nice weekend getaway spot

Florida condos over 30 and higher than three stories are in for a tsunami. Waive reserves forever in a salt-filled environment, and with little ongoing maintenance, you face rebars rusting, spalling concrete, and stucco delaminating, and you FAFO. Add the utter failure of the legislature and governor to enact meaningful insurance reform (at least we’re safe from banned books), and voila. Many projects are worth the land on which they are built.

Not to worry the legislature is here to help. Desantis signed a bill that is reported to benefit Indian Creek Village, an exclusive island community where Ivanka Trump and Jared Kushner, along with other wealthy residents like Jeff Bezos and Tom Brady, reside.

What the bill does:

This bill helps Indian Creek Village potentially avoid paying a multi-million dollar fee to the neighboring town of Surfside for transporting their sewage under Surfside’s streets. The fee was reported to be around $10 million.

They are starting at the top- should start to trickle down soon.

Stainless steel re-bar may prove a timely investment!

This is not quite how it happened. More that Indian Creek Village needed to transport its sewage to a third town’s system (with permission), and Surfside’s leaders thought “Hey, these are rich people who have no options, let’s get greedy!” and came up with this extortionate $10 million fee. It didn’t cost them much if anything. Indian Creek was going to run the pipes underneath Surfside.

It reminds me of the old economics example of the land owner who closes off a river if you don’t pay a toll.

Big law firms still like to steal units from owners..M.E.E.B.. they are up north and in fla. Beware of them. They sued my 84 year old mother in superior court.case got dismissed but that aint stopping the bastards from trying to extort 20,000 from her..better being a renter than a condo owner..her place deffers maint..like roof for a decade then steal a few units from easy prey to get money. So pathetic..it is what it is.. never get a condo,stay away from all hoas.she lived and learned..there also is no legal help for unit owners..only the hoa.buyer beware.

I pray that this craziness finally ends. Been a long time coming.

I sort of see it as some sort of large financial batteries the government uses every now and then to store tons of value.

There are bubbles everywhere and new ones are forming.

And the problem is YOU! And your friends and family and all of us. Unrealistic expectations.

But also ask , how do I profit off of this? And avoid ruin.

I just bought a beautiful 2 bedroom condo in one of the nicest neighborhoods of Houston. Great school district. My condo has a fully renovated interior. The property did flood during Harvey, but only the parking lots, not the dwelling units. The people who live there simply put their cars uphill across the street when flood risk is high. The association is debt free. The property is well maintained. The HOA fees are low and include water and trash. It is a waterfront condo with water view. There is a beautiful swimming pool on the property. The property is quiet. Low crime zip code. I paid $155k for a place to live. This condo was originally listed over $200k but I got it for a lot less. Based on the docs I saw, I guess I got it for what the seller put into it cost + renovations.

I hear people complaining about condo fees- but single family homes are also expensive to operate. In Texas for a single family home, garbage and water is $120, yard care starts at $200/month. You have to water the foundation. Plus texas damages roofs (hurricane,hail) and foundations (bad slab foundations with plumbing in the slab). So your base price for SFH is $320/month plus you need reserves to handle $10-$30k roof replacement and $5-$20k foundation/plumbing. I’ve seen horrific SFH plumbing bills for $100k in Texas due to slab tunneling! Suddenly paying just $350 condo fee starts sounding very attractive!

Condos in this neighborhood are listed as low as $80k for a fixer, but those probably need $40k renovation so $120k is probably the current floor price for a livable condo in that area.

In other parts of Houston with high crime and bad schools, fixer condos are listed as low as $50k. Buyer beware but as soon as I get cash I’ll start bidding $10-$20k on some of those dirt cheap ghetto condos and try to become a slum lord.

I have no idea what home & condo prices will do in the future.

I agree! Condo HOA fees should be less than expenses for a single family home if both are well-built. It is an economy of scale.

Major expenses, such as a new roof should be much less per unit for the condo as opposed to replacing a roof on a house. Insurance costs per unit should also be cheaper than a house.

I think many people just look at the condo monthly fees which are used for future repairs. When you buy a house, you still have to save more per month to cover these repairs when needed. For a house, that is a hidden cost but it is a very real large expense when required.

I do agree that for a condo, you are paying for a gardener and have no choice to mow the lawn yourself. You might also be paying to maintain a pool, workout room, tennis court, etc that you may never use (but if your house has a pool, tennis court, etc, these are large hidden costs to maintain.)

Painting. Every decade at least for a SFR or even more frequently if you’re in a blasted climate. Right there are HOA dues.

Have you seen the price of paint lately??

@David People can choose to buy expensive paint if they want. When I used to have a single family home I always used recycled paint and received lots of comments on how my house looked and had no problem maintaining the exterior with that super affordable paint.

@BobE Thanks for post. Having shared-cost gardener is a wonderful thing.

Why is it no one seems to be able to mow their own yards? How freaking lazy are young people nowadays? It is, like, the easiest chore.

I want to agree that young people got screwed. But they also waste their money, so how bad can i feel for them?

@MussSyke

I like mowing my lawn, trimming the bushes, exterior painting, growing plants and stuff.

Unfortunately due to inflation, career losses, govt sponsored cartels ripping me off on healthcare, and starting a new career every minute I have to be working for profit. I’m working until midnight tonight. I have no free time for yard and house care. The fewer the sq ft and the less stuff in the house the better. Only a little free time every day for family and exercise. I haven’t even read or commented on Wolf Street for months until today! Good thing I lived below my means during the good years and saved up for this. At least I found finally found an affordable place to live.

Don’t tell her about the avocado toast!

Some people are old and arthritic

some people just want to make their Sims mow the yard. Lol

I own my condo outright. My annual costs including fees, insurance, taxes, and utilities is about $8k. I think it’s pretty cheap living and I don’t have any if the headaches of a SFH. It’s smaller and easy to keep clean. I love it, but I’m just a single guy.

I’m guessing there are places where the HOA fees *alone* are over $8k ($700 per month – I’ve seen near that in the poorer half of Vegas and I’m guessing the special assessments in FL push the fees way above that)

Me too. I have a 2 bedroom condo 900 square feet and it’s about 8K a year HOA, taxes, insurance, utilities. I have no complaints.

The Feds will lower interest rates aggressively just to appease the President. That should stimulate buying and maybe mute the housing crash. Of course, the purchasing power of the dollar will fall rapidly with premature interest rates falling, tariffs and an explosion in debt levels. Real estate will become expensive again relative to incomes.

“The Feds will lower interest rates aggressively just to appease the President. That should stimulate buying…”

LOL. the Fed already cut by 100 basis points, and mortgage rates spiked, and housing supply spiked, while sales remained at collapsed levels and deteriorated further, and prices are skedaddling downhill in many markets. I cannot wait for the next 100 basis points in cuts.

Wolf do you think QE or even just MBS QE is off the table permanently? Or maybe it depends who Trump puts in? I just have an extremely hard time envisioning the fed not jumping in if this starts to get ugly based on their previous actions.

In 2009, the Fed jumped in to save the US financial system (commercial banks, investment banks, etc.) that was beginning to topple under, among other factors, trillions of dollars of losses on mortgages. That is no longer the case. Now, YOU and I (aka “taxpayers”) are on the hook because the vast majority of mortgages are guaranteed by the US government, and most of the remainder are held by investors via private-label MBS. The banks are largely off the hook this time. So from that point of view, the Fed can let it rip.

See, in Canada, if a big wedge opened up between the central bank overnight rate and the fixed mortgage rate, everybody would take out variable (adjustable) rate mortgages. But that doesn’t seem to happen in the US for whatever reason. I wonder if that is just cultural or if there are regulatory barriers of some kind in the way as well

What Canadians don’t have is a government-subsidized 30-year fixed rate mortgage that is truly fixed for 30 years, but that can be paid off at any time without penalty. So if interest rates drop to 5% three years into a 7% 30-year fixed rate mortgage, the borrower may at their discretion refinance the mortgage at a lower rate for another 30 years or 20 years or whatever term they choose. But the lender cannot alter the terms of the mortgage on their own.

Our 30-year fixed rate mortgage is therefore very different from the Canadian “fixed-rate” mortgages that are “fixed” for only relatively short terms, such as 2 years or 5 years, and then they reset.

We also have 15-year fixed-rate mortgages and 20-year fixed-rate mortgages under similar terms.

There are adjustable-rate mortgages in the US that have fixed initial terms, such as two years or five years, and then they reset, and that would be close to the Canadian “fixed-rate” mortgages.

We also have truly variable rate mortgages just like Canadians have.

But variable rate mortgages and mortgages that reset after some years carry the extra risk of not knowing what the mortgage payment will be in 10 years and whether or not the borrower can afford to make the payments.

Canada has developed a system around it that increases the risk further, by banks allowing borrowers to keep making the same payment even when rates rise, which can lead to negative amortization of the mortgages, where the remaining mortgage balance actually gets larger with each monthly payment as the unpaid interest is added to the principal. Canadian banks are taking big risks there. But I guess (I don’t know) that these mortgages are also guaranteed by the Canada Mortgage and Housing Corporation (CMHC) which is a crown corporation, and the equivalent to our GSEs (Fanny Mae and Freddie Mac).

Thank you for responding to yet another factless post by a Trump hater.

Do you remember the end of 2019, Dude? Had he allowed QT to go forth, we probably wouldn’t be in this mess now.

Excellent analysis. Its incredible to me how so many intelligent people cannot grasp the concept of an interest rate curve where the x-axis represents the time on the terms of a given loan and y-axis represents a rate. short term rates can go up or down, not in tandem with long term rates.

I fear the same thing will happen here in Canada … similar situation but probably worse due to the slowly deteriorating economy.

This time they will change bank rules to buy more treasuries and yield curve control by QE like Japan. A step further to cuts. This is what my thinking is.

Also deficits are under control if tariffs stick, which i expect to. I even expect them to increase in July

Your “thinking” needs an enema.

Yield curve control in Japan was done by the Bank of Japan, where the BOJ printed yen and bought long-term JGBs with it, under its massive QE program.

Changing bank regulations to give commercial banks more regulatory flexibility how they deal with Treasuries and their capital ratios has ZERO to do with QE and yield curve control. Banks cannot do QE or yield curve control. Only the Fed can.

Where does this obliterating idiotic manipulative bullshit come from??? What moron out there is still spreading this BS??? Wherever you saw this, they’re lying to you, and you should never ever go back there.

I am curious how much further demand destruction will go once a downward trend returns to the stock market. I am hoping to see the trend your TGA account articles predict once the debt ceiling debacle ends, i.e., prices trend lower because of reduced liquidity.

I really don’t see the long end bond yield (10 yr and up) going down significantly enough to materially help housing with lower mortgage rates.

The reason for this outlook is the massive US debt overhang combined with a world that is increasingly skeptical of dollar hegemony. This second part, which is relatively new in the making, will all but prevent the Fed from trying to buy the long end to bring down interest rates there via QE. In fact, any responsible Fed would not entertain that “save”, if Congress had not gotten real about cutting deficits.

So, alot of homeowners will be stuck in place with their low interest mortgages and the remainder selling will, over time, accept lower sales prices.

It feels like this will be a more gradual process but with periodic ups and downs and local influences. Maybe akin to watching paint dry.

So for all intents and purposes, it is likely that the housing bubble has peaked.

Condos now have another much, much less expensive competitor, a tiny house. No HOA, low tax, low cost tiny home. It costs $10000 – 50000, plus land say, 20000 per acre. The range from 400 sq feet on up, like a condo.

This is the new home on the block, and it costs a great deal less than a condo or single family.

Mobile tiny homes count as RVs and are not generally legal outside mobile home parks, with a few rural and resort zoning exceptions, like the off-grid prepper destinations. Most places outlaw “park models” on residentially owned lots. Several years ago I built a house that was under 500 sqft, foundation and all in a dirt cheap rural area. It costs much more than what you say to build to code, even if you do everything yourself and use repurposed materials. If you want to flaunt the zoning, codes, and septic requirements, sure it’ll be cheaper.

Yes, you could still do it cheaper than a condo in some places, but there are no condos in armed prepper country.

Think again. There are lots of these going up. Try Boxable, Amazon, etc. Condos are just overly expensive for what you get, single family are good.

But these tiny-house developments are not near the center of a big city, where condo towers tend to be. This stuff is out in the boonies. So you have a tiny living space AND a long commute. I guess it suits some people, but it’s not a condo replacement near a city center.

“Try Boxable”

Complete scam. They have not delivered a single actual housing unit.

These “tiny” homes are for old, and almost broke, retirees. The next step down in size for them is a coffin!

Anthony,

“These “tiny” homes are for old…”

Yep, 30 year mortgage slavery with a casino-odds “payoff” at the end is much, much better.

The more abusive housing costs become, the more creative alternatives will be created (and sneered at). The only wonder is that more hasn’t been done, sooner.

Are these homes for Ants?! 🐜

Are 3000 SF McMansions for 2 people for giAnts?

Those tiny homes are depressing. I don’t see them catching on. Tiny homes may crash worse than condos.

FL (where is live) is following the 2007 playbook all over again:

People defaulting on car loans – ✅

Condo values crashing – ✅

SFH crashing – TBD

Thankfully the upcoming election of a full blown communist to NYC mayor will send another million New Yorkers to Florida to prop up demand.

All the New Yorkers that wanted out for political reasons have already bailed. Check out domestic migration to FL – it ain’t pretty.

Inventory will keep stacking and demand will stay low until home prices crash 20% +

But hey maybe real wages will grow 57% over the next three years (amount needed according to Atlanta Fed Home Affordability Monitor) and all will be well

Florida was still +64k last year and NY was -120k

Normal for FL is around +140k.

“Those tiny homes are depressing.”

Not as depressing as losing all your down payment/equity to a foreclosure.

Great idea. Where can I put a tiny house?

I like shipping container houses and would be happy to live in one, but while its easy to find a place to put one way out in a rural area, it’s hard to find pretty much unrestricted lots near jobs where there isn’t a minimum square footage limit that they fall below.

I think the big question re the RE correction, which may end up being the biggest since the Depression, can this much paper wealth, and the resulting ‘wealth effect’ evaporate without causing a recession.

If homes tank it’ll probably be because of a recession or simultaneously with one.

Lose job… Can’t afford mortgage/property expenses… Forced selling baby!

DM: Condo owners wake up to grim reality that their homes are worthless after law change

Florida’s condo market has become a nightmare for many residents trying to sell.

The Sunshine State’s retirees who flocked there for affordable condos now find themselves stuck with old properties worth virtually nothing that they are desperate to escape.

Pending mandatory repairs and rising HOA fees on aging towers have driven owners to list in a flooded market.

In Boynton Beach for example, a two-bedroom, two-bathroom condo at Hunters Run Country Club with access to a resort-style pool and high-end amenities is selling for just $10,000. The owner paid $60,000 for it in 2001. It’s now worth $3 per square-foot.

On Marco Island, a one-bedroom, two-bathroom condo complete with water access at Sunrise Bay Resort is listed for $9,000.

The hot state’s condo market has become a nightmare for many residents trying to sell.

This is from last year, but it ads perspective to my thesis that condos are equivalent to drive in theaters:

“ At the end of the second quarter, there were 17,776 available condos over 30 years old on the market in South Florida, up 12.7% increase from the previous quarter; that compares to 2,487 newer units, a 15% quarterly decline, according to a report from ISG World”

Baby Boom Castles are aging in place:

“The housing stock in the US is getting older, and the median age of a home is now 40 years, up from 31 years in 2005”

This looks like a slow motion silent train wreck — deferred maintenance and the increased cost of protecting value. I suspect insurance costs will rise,etc… this is a can of worms — think of all the unoccupied homes and condos sitting idle, not being maintained and homes people can’t upgrade, as costs increase beyond their means.

This kinda reminds me of Ai/ tech company valuations, versus dinosaur industries in decline. Investing in drive-in theaters seems a bit illogical.

There are developers that specialize in buying out owners in old condo buildings, and once they own all the condos, they tear down the building and put up something fancier and bigger. Generally, for owners in an old condo building facing big assessments and surging HOA fees, this is a good exit. But that process has gotten stalled recently for a variety of reasons.

Apparently a growing amount of condo inventory for developers to pick from.

I can see that a premium location might be a possibility to re-develop — but what a nightmare buying out a hodgepodge of owners — and making a new deal cost effective.

This is old by a few years, but gives a taste of this dynamic related to rentals and the fascinating relationships with supply and demand across the spectrum:

“As the current housing stock ages, maintenance and preservation are becoming increasingly important. JCHA reported the median age of rental housing increased from 34 years old to 44 from 2001 to 2021”.

I do not see any major price declines on condos in Los Angeles, although prices have been stagnant. Would love to see a crash but I don’t see it so far.

So very low sales actually happening and condo prices still go up?? Are we still in crazy land wolf>

Do please read the article before you comment, carefully all the way, looking at ALL the pictures and click on the link in this sentence just above the Oakland condo picture: “Here are 20 bigger cities where condo prices have dropped by 10% to 23% from their peaks, unraveling the most epic condo bubble ever.”

And here is the Oakland condo picture. The linked article has 20 cities in total with condo price declines of 10% to 23%:

Yes regionally some are down but the national number is up right?

The median price doesn’t tell you that. The month-to-month ups and downs are seasonal. They will peak in June and then decline through January — every year. That doesn’t say anything about actual prices. I explained in the article how seasonal shifts change the mix which skews the median price up and down every year the same way.

Here is more detail on the median price being skewed by changes in the mix of what sold. It has a fun chart in it too:

https://wolfstreet.com/how-median-home-prices-are-skewed-by-changes-in-the-mix/

1. You can compare the median prices only on a year-over-year basis, and so actual prices might be dropping for months, and the median prices will not tell you that. You have to wait until the YoY price changes turn negative… so from 12 months ago. And we’re almost there. See both yoy % change charts in the article. On a year-over-year basis, median prices have been losing ground for five months in a row. The YoY gain for condos was reduced to just 0.7%, and for single-family homes to just 1.3%. That reduction of the year-over-year gain from around 5% at the end of last year to near-nothing now tells you the direction of recent price movements.

2. There are SOME markets where prices are still rising, though fewer and fewer markets each month. And there are SOME markets where prices are falling, and that number has been growing every month. The national price reflects that – which is why the YOY gains in the national median price have been evaporating month after month.

3. You cannot buy, own, or sell the national median home at the national median price. You can only own, buy, and sell specific homes in specific markets. And those local prices are the ones you’re subject to.

Can you please comment on the bankruptcy trends, worthy a separate analysis. It seems there is an increase on an individual level by 9% yoy probably adding to the housing bubble.

I already commented on it many times: Nothingburger.

Corporate bankruptcies bottomed out during the free money era and are now coming up from that and in some months are higher than they were during the Good Times before the pandemic, and in other months they’re lower. They were MULTIPLES higher during the Great Recession, but the S&P data you’re probably referring to only goes back to 2010, mercifully, LOL, when bankruptcies had already come down from a three-year mega-mountain.

And here are consumer bankruptcies through Q1 2025 🤣

https://wolfstreet.com/2025/05/13/household-debts-debt-to-income-ratio-serious-delinquencies-collections-foreclosures-bankruptcies-our-drunken-sailors-debts-in-q1-2025/

Oh look, looks like the market and homebilder is starting to look and act desperate and Pow Pow is not making any friends..Search for this headline…Bill Pulte of Pulte home calling Pow Pow out? How rich, these people are worse than a hack, then again one can expect this when you appoint inmates to run the prison.

“FHFA’s Pulte Continues Attacks on Powell, Joined by Commerce Secretary Lutnick”

MW: Powell leaves door ajar to July rate cut, but an expected rise inflation is likely to keep the Fed sidelined

I disagree that this was the reason. Powell knows that inflation has nothing to do with tariffs. Inflation is still high because of his recklessness starting in 2019, and really, March and April of 2020. But he doesn’t want to take responsibility for it, so instead he says that tariff uncertainty is the reason for wait and see. It’s really because of his own actions.

I think Powell made a mistake when he cut rates by 100 bps last year before the election when there are no need to cut rates.

Republicans are politicizing this cut and putting pressure on Powell.

The problem is: Even after cutting rates by 100bps by Powell, mortgage rates went up by 100 bps.

Pulte has an excuse: his only loyalty is to Pulte Inc. He hasn’t sworn any oath to the independence of the Fed.

11:24 AM 6/24/2025

Dow 43,087.24 +505.46 1.19%

S&P 500 6,095.04 +69.87 1.16%

Nasdaq 19,929.10 +298.12 1.52%

VIX 17.64 -2.19 -11.04%

Gold 3,330.50 -64.50 -1.90%

Oil 64.45 -4.06 -5.93%

Yep. The animal spirits are back. The “buy the dip” so has been successful for the past 16 years it’s going to be very very hard to break that mentality.

No one cares about valuations any more because they don’t need to. I’m not sure at this point that we’ll ever have a normal valuation market absent major changes.,

What’s normal?

Not 30 price to earnings ratios, 200% market cap to gdp, nor 38% Schiller price to earnings ratios.

Bernanke: “Lower mortgage rates will make housing more affordable and allow more homeowners to refinance. Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending,”

Not so. Link: “Changes in Wealth and the Velocity of Money”

Obviously high prices and highish interest rates are the biggest cause, but how much are the increasing condo dues playing into this?

FYI —from May 29 Redfin:

The condo market heavily favors buyers; there are 83% more condo sellers than buyers. By comparison, there are 28% more sellers than buyers in the single-family-home market

Also see, drive-in theater business cycle:

“ The loss of the Highway 18 and Chilton Twilight leaves Wisconsin with eight drive-in movie theaters, and only one in southeast Wisconsin: the Milky Way Drive-In Theatre in Franklin, which opens for the season May 16.”

Reasonably priced homes are off the market in no time at all. But most sellers are extremely greedy and asking prices are outrageously high. They still get away with that in some market segments (good location, good school district, high income area), where people are able and desperate enough to stretch their budget to the limit.