Waiting for lower prices, higher incomes, and lower rates.

By Wolf Richter for WOLF STREET.

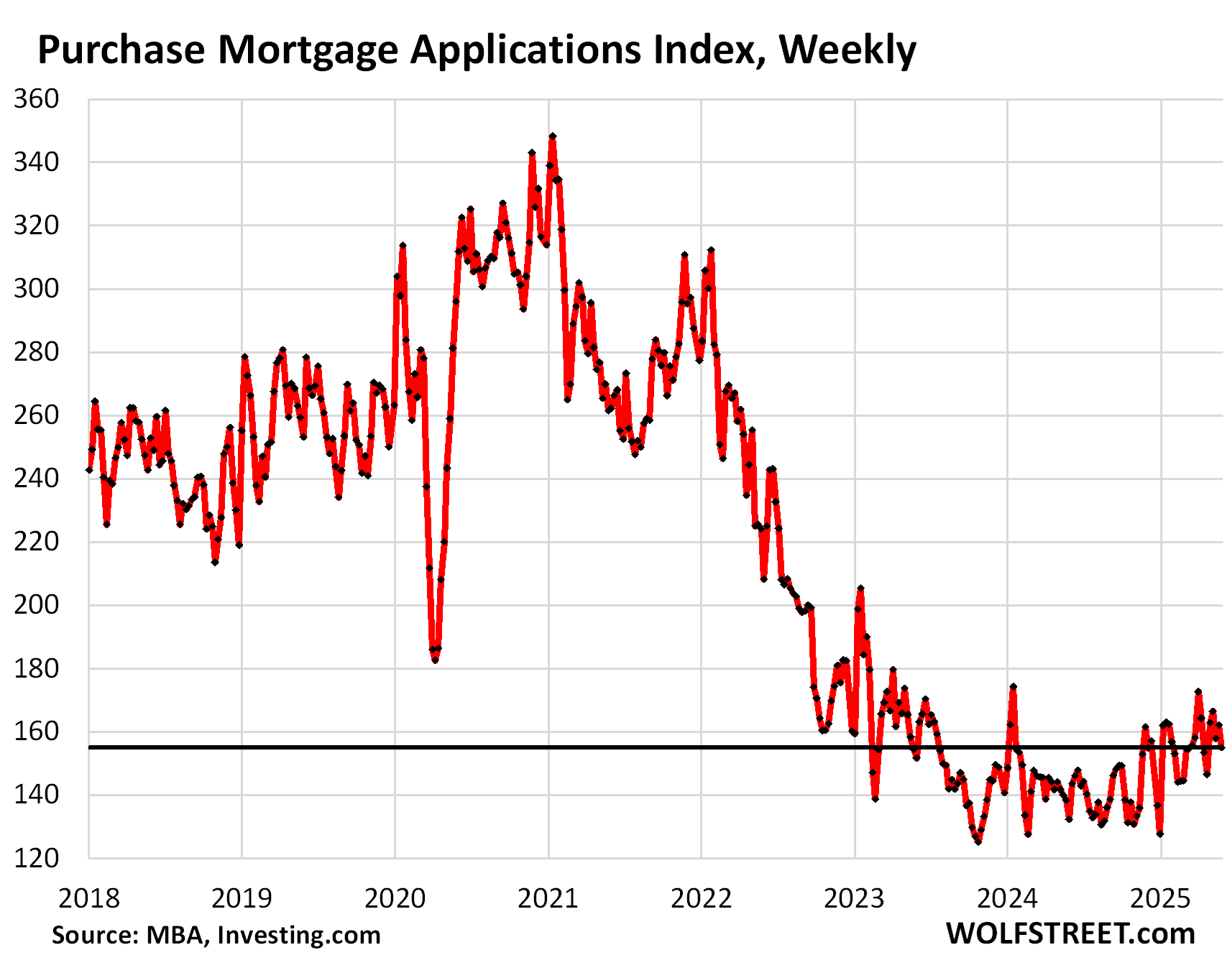

Applications for mortgages to purchase a home fell again in the latest reporting week, having collapsed by 39% from the same week in 2019, according to data by the Mortgage Bankers Association today. Mortgage applications are an early indicator of demand in the housing market, preceding “pending sales” and “closed sales” for this period.

This 39% plunge in purchase mortgage applications compared to 2019 documents the extent to which demand in the housing market has vanished, after prices spiked in just two years through mid-2022 by 50% and more – substantially more in many markets. Demand destruction sets in when prices are too high, a fundamental economic principle.

For two-and-a-half years, mortgage applications to purchase a home have been wobbling along above the record lows of November 2023 and February 2024 in the data going back to 1995.

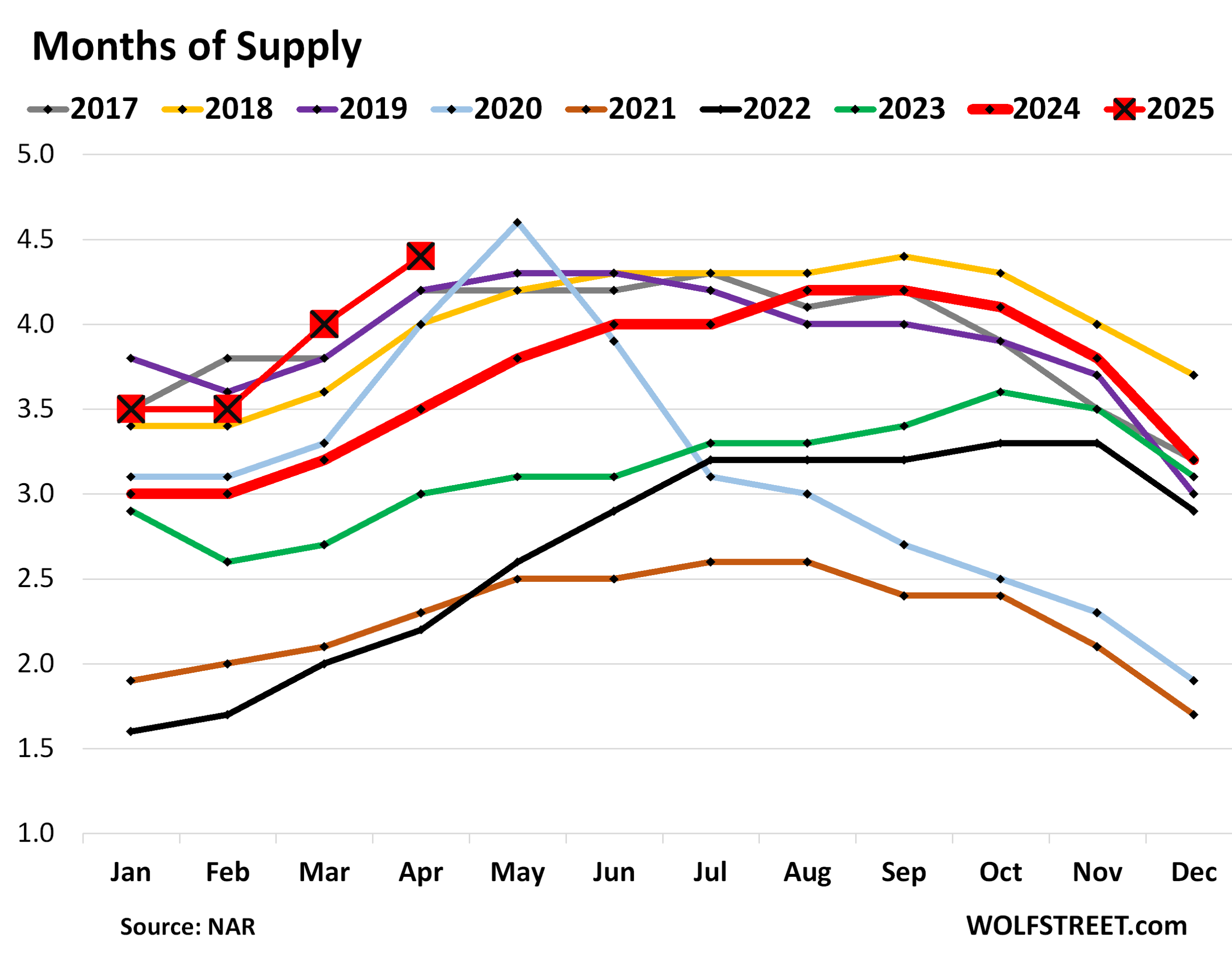

This lack of demand is now coinciding with, and is contributing to, the surge in supply, as listings sit longer and get stale. Supply of existing homes rose to 4.4 months in April, the highest for any April since 2016, according to data from the National Association of Realtors.

Back in 2022, they blamed the collapse in demand on the lack of inventory for sale. Inventory had dropped to very low levels as enough home buyers saw the historic price spike in progress and decided to ride it up all the way with their old home after they’d already moved into their new home, thereby taking one home off the market, and not putting their old home on the market. Now, those vacant homes are coming on the market, with impeccable timing after demand has vanished for price reasons:

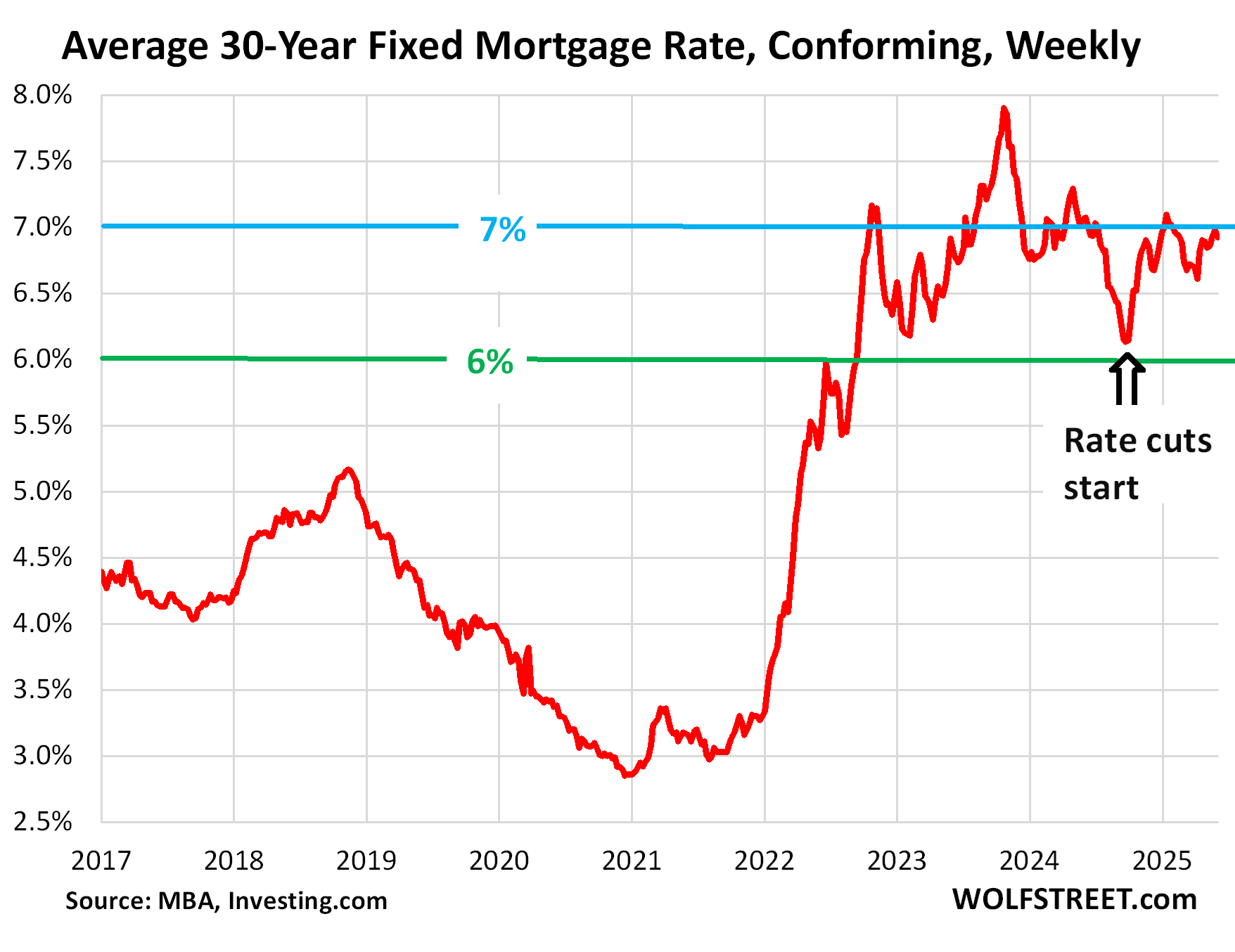

Mortgage rates have stabilized between 6.6% and 7.1% since October last year. In the latest week, the average conforming 30-year fixed mortgage rate ticked down to 6.92%, according to the MBA today, same as two weeks ago.

Mortgage rates in this range were normal to low in the pre-QE era before 2009. So that’s not the problem.

The problem is that home prices have exploded in a fantastical way during the Fed’s interest rate repression in 2020-2022 that generated the now infamous below-3% 30-year fixed-rate mortgages. That was a brief blip in history, but it did a lot of damage to the housing market by inflating home prices to absurd levels, the consequences of which are now here for all to see.

An event that taught the Fed a lesson was how mortgage rates re-spiked, along with long-term Treasury yields, from mid-September into January, as the Fed cut its short-term policy rates by 100 basis points, just as inflation had started to re-accelerate. This dovish move by the Fed, in face of rising inflation, spooked the long-term bond market. Inflation saps the purchasing power of long-term bonds, and investors want to be paid with higher yields for that expected loss in purchasing power, so long-term Treasury yields shot up, and mortgage rates along with them.

The MBA’s measure of the 30-year fixed mortgage rate surged by nearly 100 basis points, while the Fed cut 100 basis points.

It was a “Go ahead, make my day!” message from the bond market to the Fed that had been considering further rate cuts. And the Fed has since then put rate cuts on ice and started talking tough on inflation, which calmed down the bond market, and mortgage rates.

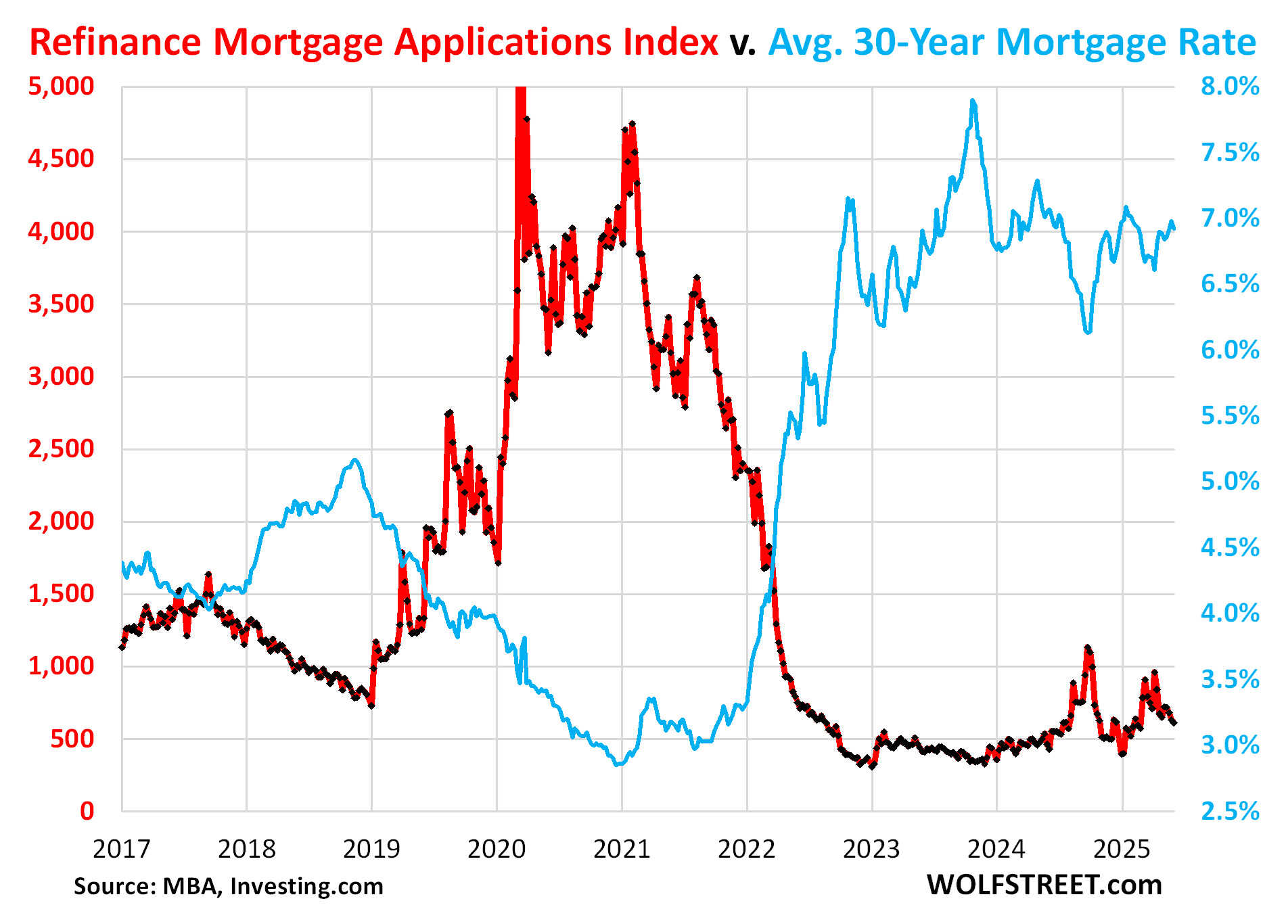

Mortgage applications to refinance a home fell further in the latest reporting week, and have been hobbling along collapsed levels compared to the 3%-mortgage era (-79% from 3 years ago).

But homeowners still want to refinance mortgages for various reasons, and they’re still happening despite the higher mortgage rates, but at a low volume. Mortgage refinance volume (red line) is inversely correlated to mortgage rates (blue).

The collapse in mortgage originations both to finance the purchase of a home and to refinance an existing mortgage has wreaked havoc in the mortgage lending industry, that responded quickly, starting in 2022, with mass-layoffs that have cut employment at nonbank real-estate lenders by 38%: Housing Bubble & Bust #1 and #2 as Seen through Employment at Mortgage Lenders: They Shed Jobs Again, 38% Gone

Many homebuyers remain on strike, now in its third year. They’re waiting for prices to come down, they’re waiting for their household incomes to rise, and they’re waiting for rates to come down. Household incomes have risen some, but not enough; and prices have come down only in some markets, but not enough (for example: The 10 Big Cities with the Biggest Price Declines of Single-Family Homes from their Peaks through April: -7% to -21%); and mortgage rates have stabilized in a range around 7%. And so the home resale market remains frozen.

With the extreme home-price distortions in many markets during the pandemic, it’s often a far better deal to rent an equivalent home, than to buy it, which gives lots of potential homebuyers some additional food for thought.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The cascade of price drops finally washed ashore on the Big Island. Of course, the insurance crisis has added fuel to the fire.

Best to just pay cash then “go naked” with no insurance.

That’s how I do it. Run around more naked than a toddler these days.

Jam out with your clam out

Really bad advice.

Actually yes. I agree. It’s probably better to risk it and put money on the side in case something happens than to pay a high premium. Even with insurance it’s probably better to pay out of pocket than to risk a premium increase if one files a claim.

If you’re the type who rolls up Benjamins to smoke in your cigars every day, sure. Otherwise that is the move of someone with a love for high-risk gambling.

I’m a smalltime landlord and I’ve had to deal with 3 fires over the years. I was underinsured and that was my mistake, but I can’t imagine if I had no insurance.

You can exclude certain risks. I know people here in Florida who have homeowner’s policies that cover everything except flooding and hurricane.

Until a tree falls on your house. Or maybe the city sewer line backs up and floods your home with icky water, or your newest light fixture catches fire and burns the whole place down.

My favorite was during a remodel. The contractor leaned the old windows against a tree for a day while he waited for a new dumpster to arrive. During the right time of day, one of the windows reflected the sun’s light at new vinyl siding, which caught fire and burned half the house down. Insurance approved it no questions asked. Adjuster said he’s seen it numerous times.

There are a lot of ways to save money, but going without homeowner’s insurance isn’t a good idea.

I live in Florida and own my house outright. I have a $25,000 hurricane deductible and a $15,000 everything else deductible. I can afford those in case of a catastrophe. But I still pay $1250/year for insurance. That’s the right balance for me.

Good to see that insurance companies are offering some high deductible options. For many it is all or nothing. Relatively low deductible options with huge premiums.

Yep. Out on Miami Beach I have a $50k hurricane deductible. Premium is higher at $7k but works for me. Better than paying California state income taxes

For the barrier island, that isn’t bad. I have a friend in Coral Gables paying $25k…

Great move! Self-insure except for catastrophe.

Shame on our overlords artificially pumping every asset class for their benefit and leaving a legacy of debt for future generations…DC about to get the memo from foreign creditors…we don’t want your weak currency nor your threats…probably just more manipulation and theater, I digress.

I disagree. Foreigners obviously want our “weak currency,” or they wouldn’t whine about the tariffs. If they keep selling to the US with huge trade surpluses, they will keep accumulating our weak currency and need to do something with it. Inevitably, a portion of those trade surpluses will find their way back into Treasuries.

Or gold.

I think they will buy property, gold or Bitcoin with it. Why take a guaranteed loss with us bonds? The to low interest is guaranteed until the US gets the debt and inflation under control.

Why would property be attractive in the face of taxes, insurance, maintenance, and possible forfeiture due to rapidly changing immigration policy? Seems like a liability now.

You need to think the process all the way through. If the foreign holder of dollars after running a trade surplus decides to buy property, gold, or Bitcoin, the person or entity they purchase it from will then have their dollars. The dollars don’t disappear, they move around from buyer to seller and are always held by someone. The cash also doesn’t bear any interest. Eventually some people will use some of the dollars to buy treasuries in order to earn interest on their non-interest bearing dollars.

You said: “Why take a guaranteed loss with us bonds?” The question doesn’t make sense because there isn’t a “guaranteed” loss. The sheer size and liquidity of the US Treasury market tells us that. If a loss was “guaranteed” no one would invest in the market. You may prefer other investments, but projecting that preference on other investors is often a mistake.

I prefer Grant’s term of “return free risk.” It’s not necessarily a loss, and it’s likely LESS of a loss than just inflated cash.

Gold (as compared to CPI) is looking expensive. While I still expect to see the price pull back, it could easily go pretty sideways for the foreseeable future, barring any catastrophic change (which could drive prices higher and substantially lower).

Similar things could be said for the BTC and even RE. The type and location of the property are all factors.

To Rojo’s point: asset holders and managers have to do something with their cash. The treasury is stable compared to other options.

“Inevitably, a portion of those trade surpluses will find their way back into Treasuries.”

So, basically, you are saying that the Chinese – who have spent 20 years screwing their consumers/US exporters by the forced conversion of Chinese export proceeds into CCP controlled Yuan – and the US government – who has spent the last 20 years screwing savers with ZIRP to shift control of the economy from the private actors to the G – have basically been in bed together?

1) China compels forced conversion of Chinese export proceeds into CCP controlled Yuan – completely short-circuiting the recycling of those proceeds into foreign exports *into* China – completely deranging the relative valuation of Yuan-USD, further distorting international trade.

2) China takes fraction of that “forced Yuan” and converts into USD with which to buy US Treasuries into order to suborn US Feds, who have spent decades crafting system of US perpetual national debt.

3) US Feds laughably ignore 20 years of clear Chinese currency manipulation (“forced Yuan”). Pure coincidence given massive buys of deeply-indebted US Treasuries by CCP.

4) ZIRP (created by #2 and outright money prints by Feds) expropriate trillions from US savers in order to minimize consequence of decades of Fed debt.

There’s a lot of political commentary in your comment I wasn’t addressing at all.

I was simply pointing out that many countries, through massive trade surpluses, appear eager to continue accumulating our “weak currency.” Since our “weak currency” needs to be invested in dollar denominated assets, some of it will eventually end up being invested in treasuries.

Everything else is your opinion.

The most interesting thing to me is how the 10Y treasury has diverged from the 30Y mortgage. Which it’s my understanding these generally followed each other. The 30Y mortgage rate is quite a bit higher. I think that suggests increased risk seen by mortgage lenders. I’d bet that risk is you can’t count on those homes gaining value anymore. You don’t mind lending for someone to buy a home if in the case you foreclose on them you make money on that sale(IE the home’s price rose). Not very risky to lend to buy something that you can sell for a profit.

Which I think creates a sort of anti-self fulfilling prophecy for the home sellers. Home sellers don’t want to drop their prices because they expect rates to fall and thus justify their price. But lenders can’t see more upside and so won’t lower rates because of the risk of lending for such an overpriced asset. One will have to budge and I doubt it’s the lenders.

The actual mortgage rate is lower than the advertised rate because homebuilders have been buying mortgages down to 5-6% for a few years now.

Existing home sales are harder because no one will buy down the rate to move the house.

This is another contributing factor to the increase in supply. Existing homes are harder to finance than new homes subsidized by builders.

“Existing home sales are harder because no one will buy down the rate to move the house.”

Not completely true, as some banks around here (Texas) are working with realtors and offering 2 year mortgage buydowns of 4.99% – 5.99% just to get the client’s loan.

Sure, but have builders always bought points so aggressively? They’re doing so to offset the high nominal rate. Whether through a lump sum via points or increased rates, the lenders seem to need to hedge some kind of risk here. Also I’m not sure I’d call it the ‘actual mortgage rate’ when only ~25% of sales are from builders.

Ultimately I’m sure the lenders would love to get some more business but perceive it as uneconomical to drive more business via lower rates. There was a time when lenders would do all kinds of crazy stuff to get you to get a mortgage but that was when home prices ‘could only go up’.

“The 30Y mortgage rate is quite a bit higher. I think that suggests increased risk seen by mortgage lenders.”

The lenders don’t hold MBS. The new mortgages are out the door from the mortgage brokers faster than[fill in the blank]. Bagholders hold MBS.

As for pricing, the typical mortgage is priced of the ten year, not the 30 year.

“The average length of U.S. home ownership in 2024 is 11.9 years.”

It was 6.5 years in 2006.

Should I spell out every little detail? Of course they don’t hold it. But they have to sell it. And the buyers of that aren’t buying at lower rates due to the risk. I’m sure there is some youtube tutorials that can help you with the details if you’re interested.

The vast majority of mortgages are securitized into MBS that are sold to investors.

Of those mortgages that are securitized, the vast majority is guaranteed by the government (Fannie, Freddie, VA, FHA, etc.), and investors buying the MBS do not carry any credit risk. You, me, Waiono, and other dutiful taxpayers are enthusiastically and usually unknowingly on the hook for these mortgages.

You said: “And the buyers of that aren’t buying at lower rates due to the risk.”

Well no, because the risk is with the taxpayers, and the buyers of the MBS assume no credit risk. They don’t care one iota about the housing market. All they care about is the path of long-term interest rates that make the market value of the MBS go up or down. And these long-term interest rates tend to fluctuate with expectations of future inflation. Higher inflation could cause long-term interest rates to rise, which would cause the market value of MBS (and all other bonds) to fall. So buying when yields are low is risky, because when yields then rise after you bought, the market value of your security goes down.

Mortgage interest rates are closely correlated with the 10-year (not the 30-year) US Treasuries and are headed much higher.

FNMA and FHLMC trade similarly to other agencies in the secondary market. Same yields on equivalent duration etc.

The treasury department just bought back some 10 UST. Their largest buyback ever. Sell notes to buyback the 10 y. The intent was Little temp relief in $TNX yield to try and get sp 500 to new highs, lower yield input to fuel the algorithm risk on. Treasury secretary is a smart fellow. We will see what happens, and the beat goes on and the beat goes on.

I should have kept reading before commenting. :) thanks for the post.

D Diamond

That $10 billion buyback was on Tuesday (“yesterday”). On Wednesday (“today”), they bought back $2 billion. But on Tuesday, day of the $10 billion buyback, yields rose; and Wednesday, day of the $2 billion buyback, yields fell. Obviously, the buybacks are not correlated to yield movements.

Do you honestly believe homes are overpriced when government debt is slated to reach 38 trillion by September,? Homes are simply one of the best places to store value in a hyper inflationary environment. High tariffs might solve the problem and contribute to debt reduction, but my experience with government is give them a dollar and they will take ten. A recession will not solve the problem either, the US government will simply try and spend it’s way out of it and create more inflation. Government live on inflation. In the end it eliminates their entire debt, paper money becomes worthless.

higher gov debt -> higher treasury rates -> higher mortgage rates -> lower home prices

Your ‘store of value’ is nothing more than a leveraged bet on getting much lower rates or much higher incomes in the future. Good luck with that

“Homes are simply one of the best places to store value in a hyper inflationary environment.”

That’s the conventional view – but it ignores the fact that homes are one of the least liquid assets out there – particularly in a crisis.

And an abusive government (which you describe well in terms of its predatory money printing) won’t shy away from ultimately using abusive property taxation as well – on very hard to liquidate/impossible to relocate real estate assets.

You may think the G will eat you last – but the less liquid/asset nimble you are, the easier prey you become.

Hard to leave a 2.25% 30 year mortgage for anything else.

Hard to leave a 2.15 mortgage. Probably never will.

Maybe after 30 years?

You certainly will when you eventually have to downsize to a casket.

Or an urn! Great point though.

We would leave ours, but not for a house that’s more expensive than the one we have now. We look at homes on Zillow where the seller is pretty much asking double what the house sold for in 2018-19. Eh, no.

We’re watching one that listed at 1.4 and now down to 1M after sitting for 5 months. Another one we were watching listed at 1.3 and sold a few weeks ago for 1M after sitting for 8 months. Based on new listings hitting the market, sellers are finally cluing in that they need to be more realistic with their pricing.

Even at $1M for both, depending on how nice the neighborhood is and how nice and big the actual house is, one can argue that even then it’s still way overpriced (if this is just your run of the mill 3 bedrooms or condo). For it to sit slightly longer but still able to sell goes to show there’s still plenty of willing bagholders out there, although definitely with less FOMO energy than before.

Sad to say we’re still not at a market where sellers are chasing the market all the way down yet…perhaps time hopefully will fix that

Some of the “2.25 percenters” are still moving, more than we would expect in our little neck of the woods but I guess when you gotta move you gotta move. And who knows, if they trade up for a less expensive market or just size down, things like homeowner’s insurance leave alone the property’s taxes might also be a better bargain, less pricey residential area also means insurers don’t have to charge so much to cover those homes so it can still make sense to move. Even been seeing more cases of people taking the plunge and moving to that dream retiree destination or job overseas. In those cases the change in interest rate or even having a gain at all at the sale may not be so important, they’re paying a lot less where they’re moving to so having liquidity from a sale even if at a loss is what matters, regardless of 2.25% rate or lower.

For some people, living their life around an interest rate makes life nice and simple. Maybe simple is all they can handle.

2% mortgages don’t matter as much on vacant homes. They’re sitting empty, costing money. Maintenance, property taxes, insurance. People are finding out being a landlord isn’t as easy as it sounds and some tenants are terrible. Lastly, not tax advice but from what I remember, to receive the capital gains tax exclusion you have to have lived in property 2 of the last 5 years. Lots of people need to get out soon or they’re going to pay 25% on their gains. Oh and if you’re one of the big cities that’s building lots, there’s so much new rental inventory good luck renting your place unless you update it and make it super nice or risk getting tenants with less than stellar employment records who can’t afford the nicer options.

The new inventory is mostly vacant properties – all other housing transactions are 1:1 – we wouldn’t have this kind of inventory spike without it

Howdy Prisoners. You are not alone. The Govern ment ZIRPed so many of you. Just don t move or pay cash for your next home and you will be fine.

U.S. economy stalled in May, Fed’s Beige Book survey finds

Even with treasury buybacks accelerating (today) — seems like mortgage rates will remain higher for longer — as housing inventory in at least 1/2 of America continues to rise.

Tax collection is how Uncle Sam pays interest on the debt, so seems like the higher deficit and debt burden will not fit well with less tax revenue ahead — and a tsunami of overpriced homes.

The ridiculous three year home buyers strike is about to be supercharged!

There was no “acceleration today” of buybacks. The Treasury bought back $2 billion, from one issue, a 20-year bond issued in Aug 2021, and it paid 65 cents on the dollar.

Buybacks have been in that range for months. In October, I discussed some buybacks, including on Oct 16, when $4 billion were bought back. And there have been bigger days in between.

https://wolfstreet.com/2024/10/25/treasury-buybacks-october-update-on-the-bond-market-bloodletting/

Note that the Treasury has to borrow more money (issue new Treasury securities) to get the cash to buy back these older “off the run” securities. Unlike the Fed, it cannot print money to buy back the bonds, it has to sell bonds to buy bonds — so this provides some liquidity for the off-the-run bonds as it replaces them with new on-the-run bonds. This is why the effect on long-term yields is negligible.

The Treasury could issue more T-bills and use the cash to buy back long-term notes and bonds. If it does enough of that, it might push down longer-term yields temporarily, but it would load up the market with T-bills even more than there already are ($6 trillion), leading to huge gigantic auctions throughout the week as T-bills constantly roll over, and there are problem with that.

I actually went and read that after posting my comment — that’s an excellent post, and it’s interesting that bessent is following the yellen playbook. I think that implies we’ll see a similar outcome, in terms of higher yields and larger deficit.

I think the slight difference now, is that as more issuance is needed going forward, there’s a change in narrative in terms of global support and demand for treasuries. Making our allies into enemies probably has a cost!

I realize there’s still substantial demand for treasuries, but the increased growth in debt seems to be outpacing overall enthusiasm — resulting in higher term premium (pushing rates higher).

I was very interested in your cost analysis of the complexity of the buybacks and the picture painted by the process — seems like it’s not necessarily a good trade off for treasury to lose taxpayer funds in order to cap rates — but as you imply, those dynamics are complicated and take time to understand.

Who is selling the bonds back to the govt for these losses? Is some of it the big bond funds like BND or TLT, and target date 401k funds, which would be locking in losses for their customers? I guess it might be a pretty small percentage of the bond funds holdings.

Anyone trying to sell a 20-year bond that they bought at auction in 2020 with a 1% or so coupon is going to take a huge loss. So the choice is:

1. get the bond off your books by selling it at a 35% loss and replace it with a new 20-year bond that earns about 5% (last 20-year auction) for the next 20 years.

2. Keep the bond till maturity, take no capital loss, but earn only 1% for another 16 year.

Insurers have been sellers of those bonds, bond funds might sell some, bank might sell those that they didn’t classify as “hold to maturity” bonds. Obviously, there are not a lot of sellers because these auction numbers are pretty small.

Calling a condo a home is a joke. I wonder what Wolf’s figures would look like if you took out all the condos from the above data. It would probably look even worse. Nearly all the work we’ve been getting over the past year has been condos. The second category is massively renovated investor homes that have been sitting for a long time. The last category, existing owner occupied homes are not selling and not even being put on the the market. Realtors who work on trying to get these listings might as well as hang it up and go look for a job pumping gas. New Jersey needs more of them.

Lots of people calling condos homes, a**hole.

I see Swamp’s point. No need to be obnoxious, Jake.

–Geezer

Aww, lighten up Geezer.

After all our Talker-In-Chief can call entire countries in Africa that, (as he leads us back to the comfortable Ozzie and Harriet days, where you will never be insulted by such trashy talk anymore.) Except in our overflowing prisons and “law enforcement” in selected “bad neighborhoods”…..which are becoming more and more of the content on our MSM.

(The good Dr Phil just built a whole network on it, FYI)

ATL Jake

A Condo we did several decades ago had a $1,000 maintenance fee, and a sign on the wall listing hundreds of “owners” who hadn’t paid their condo fee. These defaulted fees were passed on to the rest of the “owners” . Buyers of these “homes” were greeted in the lobby with this posting. Still think this is a “home” ? Just like a Norman Rockwell painting, right. This use of “home for condos is Inflation of the term “home”. Condos are a hybrid entity, somewhere between a “home” and an “apartment” . Direct your insults to someone else in the future.

“The second category is massively renovated investor homes that have been sitting ”

Honest questoin because I’m far away from this industry and don’t understand, but how do those real estate investors sitting for weeks (leave alone months) on a portfolio of so many unsold homes, not go completely belly up from doing this? Wouldn’t they get eaten alive by all the costs of the insurance, taxes, repairs and just plain maintenance and HOA or whatever other fees from just letting them sit there? I’m feeling like if you’re a flipper or home investor, whether big fish like Blackstone or some connection to an REIT or just a small-fry in a small-town, your whole business model would be centered around “sell, sell, sell as fast as possible, even if you take a big hit on the price and if it comes to it, sell a lot lower to cut your losses”.

Because seems like the very worst business mismanagement in the real estate flipping or in investment business, especially with a lot of homes is just letting them sit idle. Maybe some individual home seller households can get stuck for a few extra weeks in the collective delusion Wolf points out a lot, hesitant to drop prices even when it’s clear the buyers can’t stomach the high costs when they soar way past salaries and savings. But if you’re a real estate investor or flipper with a bunch of homes you’ve bought and want to sell, just letting those homes sit at unrealistically high prices is burning a big hole in your balance sheet and costing you everyday. Seems, like the flippers and investors would be the first to get real and put the big price cuts in.

In our market in west chicago burbs the homes that have been obviously flipped on the cheap and lack any character are experiencing price drops (10k here, 20k there). I think mostly that was due to coming in too high priced in the first place.

I see quite a few examples of this here in my market (Georgia) . Investor / flipper owned homes are on the market at prices lower than what they purchased for 6…8…12 months ago. And they pumped money into them for renovations, closing costs, commissions, etc. So yeah, some are severely belly up.

Ummm probably depends on your market. Lots of single family homes for sale where I live. Just a matter of if they cut price or pull it off the market and try again next year.

I’m a bit inclined to agree. The idea of condos is attractive. It’s the reality that is the problem. If a home is viewed as a store of value, then the idea is that there is less counter party risk. If I have no debt on the house then the only other claim on the property is the state through property taxes.

The main issue with condos seems to be that the HOA becomes another counter-party – another source of risk AND all the other owners become counter-parties as you depend on all of them paying their dues.

To many others agents in the mix over whom you have almost 0 control.

Waiting on 2019 prices to come back around – would be even happier if 2010 pricing hit. Hope the whole damn thing collapses. The affordable anything these days is killing everything I have worked for these past 30 years. Painful past five years of inflation every single year and getting worse. I have not seen anything go back to 2019 pricing that is necessary to live. The garbage like commercial electronics they give away.

I’m seeing lots of price cuts in San Diego. A few big ones ($100K) over the last week. Unheard of to cut $100K in summer selling season in the past.

Homes are just too expensive. People are trying to sell homes for $1.5M when they sold for $800K in 2019. At 7% interest that is nearly a $10K a month payment. The same house rents for $5K or less. And now people are realizing that homes don’t always go up since the last three years traded sideways.

Hopefully some prices start coming down substantially and everything returns to reality.

:Cluctching my pearls: SD? No freaking way….it just cannot be…ok maybe in SD but will it spread to South OC and further up north to theWestside like this? If it does, I am ripping off my pearls…

Let this be the appetizer to the main course especially for SoCal market…my worse fear is that some other event will cause this to reverse later this year or next spring season. I think it’s the right thing to do to not condition ourselves to think the ridiculous price we see now should be anywhere near the norm

I have a friend that bought rental houses in Austin, TX during high COVID. He’s ready to sell and I’m advising him to sell at a loss rather pour more money into them to cover substantial deferred maintenance. I truly don’t think he’ll cover the renovation costs and his initial purchase prices.

Austin was the country’s darling during COVID but without stimulus free money, its lustre has worn off.

Prices need to keep falling and I feel like there should be restraints to bar investment groups from buying single family homes. It’s destroying the fabric of communities.

I think Austin was not just free money, although that didn’t hurt, but also the temporary remote work and bigtech hiring booms. There’s a reason it has declined much faster than the other boom places, like Miami, where I am, and Nashville.

Just got back from a short trip to Austin, great town, one factor you didn’t mention is the huge number of condo towers popping up around downtown, the inventory increase at least in downtown is gigantic, I’m sure that’s also a factor in the price decline.

I used to live in a 38 unit condo building in downtown Austin that was bought out at a nice premium in 2021 and demolished in 2023 to make way for the tallest residential tower in town. That project was cancelled and there is now tall grass growing on the lot…

Agreed here and gave similar advice to an old friend in another market where home prices went totally crazy during pandemic, I forgot who it was said in an unwinding housing bubble or other bubble, he who panics first panics best, or something to that kind of effect. In my friend’s area the bubble was even more out of control than many others, median home price in a not at all luxurious area getting right close to half a million dollars with median total household income (for the whole household, not just one earner) way below $100K. No way to sustain those prices and even though he bought it early in Covid with one of those uber low interest rates, it’s not worth it to stay in delusion those prices would ever hold up. He was already decided based on recent events to move away at some point to be closer to his adult kids 2 states over and just question of when, so he smartly sold off at a minor loss just before prices plunged even more more just 3 months later, with other sellers really starting to panic.

This is why it’s bad idea for the Fed or legislature or any other policy-makers to inflate housing bubbles in the first place, eventually those home prices have to come down to more realistic levels that people can afford, and the longer they wait and the more they inflate, the more painful the inevitable correction is. That policy of ZIRP with crazy QE with MBS buying and basically money-printing in the pandemic is still one of the biggest monetary policy errors in American history and now we’re all about to pay the price in one way or another. Too, now all this unwinding is happening with the tariffs likely sparking then even more inflation and the bond-market laying down the law on careless policy. Bottom-line is homes are still too expensive for what buyers can afford realistically based on earnings and savings, and if sellers seeing a 10 or 15 percent drop in area prices delude themselves and fail to get the hint, there’s a good chance soon they’ll be staring at 20 percent and soon higher drops and bitterly regretting they didn’t cut their losses and sell earlier when they had the chance.

Buy, never sell… all of this short term panic is wasted energy. You own real estate for two reasons. One to avoid paying someone else’s mortgage (principal at least). And two as a safe inflation hedge. You signed a 30 year mortgage.

If it’s not an obvious good financial choice based on realistic financial calculus dont invest or sell.

The speculation I am reading in these comments is just that, admit you don’t know what will happen and plan for the long term. 10-20 years from now every comment here (possably including mine) will look silly.

“He who panics first, panics best.” -wolfstreet-10-8-24

“We wish Mr. Holmes the best of luck. But, he doesn’t need luck; he needs to cut the price boldly and pronto.”

I love how Miller decides it’s “Policy makers” that caused the housing bubble. No. Sorry. It’s not.

The true fault lies with the people who signed their name to the contracts and bought the properties they couldn’t afford who are at fault. Stop blaming anyone other than the knuckeheads that failed to apply financial discipline to their actions. Payment buyers always get hosed. They disconnect the purchase price from the transaction. Interest rates are irrelevant to the value of anything. The property is either worth “X” or it’s not. Just because the payment “pencils” doesn’t mean you made a solid financial decision.

in the car biz, they employ a tactic known as the “four square”. It confuses the rubes into buying more than they can afford.

The basic premise of committing no more than 1/3 your GROSS income applies to housing. That’s PITI. If you don’t fit that calculus, lower your expectations or rent. As someone else said, the HGTV crowd is going to get their lunch money stolen.

It’s not the “gubmints” fault that you, or anyone else, made a bad decision. Own it and move on. If enough “buyers” (and I use the word loosely) held to that conviction, you wouldn’t be here today.

Yes people should be careful and responsible but the qualities of good leadership are to look out for the people they are leading by making policy that is responsible. People will always have the opportunity to make bad decisions but bad policy makes it a lot worse. For example a lot of people wouldnt be able to mess up taking out a loan they cant afford if the gov’t hadnt artificially repressed rates.

Another reason people left Austin is that they could no longer deny that they lived in Texas.

Blackrock will be buying up all these defaulted homes and renting them out. You can kiss the community goodby.

Swamp Creature

That’s not what Blackrock does – or ever did. Blackrock is a fund manager… it manages stock and bond ETFs, mutual funds of all kinds, money market funds, etc.

You’re thinking of Blackstone, the PE firm. They did that at the end of the housing bust, after prices had collapsed by 50% or more on properties in foreclosure. But they packaged that outfit into a REIT, Invitation Homes, and sold it to the public via an IPO in 2014. A year ago, Invitation Homes started SELLING at peak prices those properties that it had bought on the cheap back at the time, and it has been building its own build-to-rent developments, with their own leasing and maintenance office, pool, and other common amenities. Build to rent is the hugest thing in the housing market right now. Invitation Homes has been bragging about all this in its earnings calls. But small investors are still buying houses, and they’re going to get run over, like they did last time.

Same sample of the market for sure but slower sales in used homes in Tyler Tx as well. Avg time on market is more than 4 months but maybe summer will allow some of these to move . The data wolf presented with mtg apps down suggests the opposite more pain for home sellers

I realize a goodly amount of the value of real estate is the land, but until recently with used cars, everything went down in value after you purchased it, sometimes demonstrably.

It blows me away that a 1965 3 bedroom house in LA is worth a million bucks, compare that with any common consumer item from 1965.

Say, how much would the mortgage be on said LA home if you bought it for a million?

Around $8-9k a month, maybe.

No wonder there’s a pile up next to the 405

Yeah it’s ridiculous in LA or anywhere near Westside and even the valleys too. The entitlement mentality of thinking the floor of asking price at $1m especially for some s***hole in questionable neighborhood is insulting at worst, comical to say the least. Majority are still hanging onto 2022 pricing and you can go further south and find houses for sale in Ladera Ranch asking $800k for some attached condo and price history just less than 2 yrs ago was 50% less. The whole thing feels a little like final rugpull moment when people are now coming out looking for the next bagholder.

I’m in the age group that had to sell our parents’ home in SoCal during the pandemic. The stories we have to tell about deferred maintenance! So lucky the trend was to defer inspections, but now that those are coming back it’s going to be interesting. Even more so since the cost of home repairs has skyrocketed and the wait lists to get things repaired or upgraded are formidable. It’s amazing what people were willing to put down when housing looked like a double-your-money sure-thing bet. Now, not so much.

Yup, sure do kind of remind me of a cult or diehard religion when it comes to narrative on housing for some people. Throw out any skepticisim or logic that what goes up can come down, don’t question or look at the fundamentals.

The whole buying without inspection thing is so bonker but so many have done it during that crazy time, another resembalance of a cult…Drink the Kool-Aid and dont’ question the leader what might be in it.

It cracks me up how personally you take this. Reminds me of….me, for decades.

Look, as long as ANY of those homes are selling at those prices (and some of them ARE selling…,the market is frosty, not frozen), then don’t blame the sellers, blame those who are still buying them.

:) Don’t worry I am equal opportunist, I have as much, if not more contempt towards the buyers. Just like there’s abuser, there’s also enablers and these buyers buying at sky high prices because of FOMO or whatever emotional reason they come up with are the enablers.

@ Xavier Caveat says:

> I realize a goodly amount of the value of real estate is the land,

Lots in decent parts of LA and the Bay Area sell for over $1mm, lots with crappy homes sell for a little more lots with nice homes sell for a LOT more.

> It blows me away that a 1965 3 bedroom house in LA is worth

> a million bucks, compare that with any common consumer

> item from 1965.

Nicer older homes in LA between Santa Monica and the 405 sold for ~$20K depending on size and condition and in 1965 and you could buy a new Shelby Mustang GT350 for ~$4K. Today the LA Home and Shelby Mustang are both worth about 100x more,

In 1965 you could get a nicer older home in Sacramento between the Capital and US 50 for ~$15K and buy a new Mustang GT K Block Mustang for ~$3K. Today the Sacramento Home and GT Mustang are both worth about 25x more

In Detroit MI you could get a home in 1965 for ~$15K and a new base model 6cyl Mustang for just over $2K and today many of the homes and 6cy Mustangs are worth about 5x more.

Someone near me on the SF just put the home they bought at the end of last year for $2.6mm after fixing it up for sale asking $4mm. I don’t think it is a “good deal” just like I don’t think that the early 70’s Mercedes 280SE Cabrio a friend just bought for $350K is a “good deal”. There are still some paying these crazy prices and until they stop won’t go down much.

The last sentence says it all. Sale volume has plummeted, but as long as a few idiots overpay, paying peak 2022 pricing as “that’s what the comps are, and I need a place to live”, it gives the remaining sellers hope that someone will come along and pay peak pricing for their overpriced house too.

Most don’t, of course, and if you have 20 overpriced houses in one community, and only 2-3 willing buyers at those prices, the odds are not good for any individual seller that their house will be the one picked, not unless they price significantly below the others, which many are not willing to do yet.

That said, where I am in Miami, I’m seeing a LOT of new inventory, and a lot of drops. even more importantly, I’m seeing a lot of houses go pending and sell for 15-20% below ask, which was unheard of a couple years ago. Sure, many are still overpriced, but it says something about how the dynamic has changed when a seller lists for $3.5 million, drops the price to $3.1 million, and ultimately sells for $2.6 million. It shows that he was in fear of farther drops, and wanted to get out at the $2.6 while he still could.

So many new rich people after the widening of the wealth gap from 15 years of reckless QE…my guess is that they’re the only ones that matter anymore – the only ones allowed or able to purchase goods and services beyond water and Government cheese. Or, at least that’s where this is headed.

The comparison is interesting but the 2025 Mustang is at least an order of magnitude better than the 1965, e.g you won’t get impaled by the steering column in a crash, you won’t need to do a valve job after 50k miles, you won’t fly off the road if you take a turn hard, the brakes actually work, etc.

New cars are amazing compared to the old iron. One of my daily drivers way back was a 70 RT/SE Challenger, but that thing was a death trap by modern standards, albeit a very stylish one.

And when you’re comparing relative prices, why is a 2025 Mazda 3 about the same price as a 2015 Mazda 3? (We bought one back then). Maybe it’s because Mazda has to accept lower margins on basic models, which to me means everyone whom assumes big margins are guaranteed are screwed when people start caring about prices.

I’m not sure land value is a coherent concept. Works for farms, but not sure works in heavily zoned residential cities like LA. I certainly don’t see it used consistently in SoCal prices.

Simple greed has been keeping those houses off the market, and now they’re paying the price for their avarice. When you reach too far for the prize, you get burned. It’s that simple.

In Chicago we still have very low inventory. Houses are selling like hot cakes.

Do a home search for zip code 60525.

I love it how some people say “in my area prices are crashing”. They won’t specify a zip code so people can independently verify it.

Geez, are you new here or haven’t pay any attention. There’s no one single national market as Wolf said many times, different regions and states are on different trajectory and timing. Do yourself a favor as there are many YT videos breaking out the markets differences. Even doomer like Nick on YT often show maps of tight inventory in certain Northern and Midwest markets.

Feels like you’re late to the party since your not in my area comments are often paraphrase by SoCal/NorCalers and look at how that dynamic has changed now…

Homes can’t be “selling like hot cakes” if there’s little inventory. Hot cakes are easy to make. Never a lack of inventory.

In the Chicago suburbs I watch (60067 & 60074) there was very little inventory until this week, when it about doubled.

Lack of inventory had kept prices stable, though not at absurd California levels. Around $500k for a decent 1970 era 3bdrm.

Some price drops.

Expect to see more.

Don’t worry. it’d come to this zipcode as well.

Free money was a nationwide phenomenon and it lifted price every where

Free money is gone, now at 7% mortgage rate, very expensive to own.

During last downturn, everywhere prices went down with a lag with each other.

Same this time unless this time is different

Interesting. But you got one thing wrong –

….taught the FED a lesson….

The FED does not & cannot learn any lessons. Their mandate is to make it easy for the well off to acquire more assets & never really have to pay their debt. Anything else is bullshit. I refuse to believe it.

6.89% mortgage rate is slightly below the historical average of 7.71% for a 30-year fixed mortgage. Mortgage payments have increased significantly over time though due to rising home prices. Additionally, homeowners insurance is rising due to climate change, property taxes are also rising and with rising materials cost and labor, it’s costing more to repair, replace worn out parts or renovate home features. an additional demographic thing that may be contributing is declining US mobility. Back in 50’s and 60’s relocation rate out-of-state was about twice as high as it is today. Right now, around 80% or so of people live within a hundred miles of where they grew up.US population is getting older and older people tend to move less. Though there was a boom in pandemic relocations, overall, the needle on rate of US relocations didn’t seem to move very much.

Buyers need to bite the bullet and dive into home ownership. Even at 7% they can always refinance if rates drop in the future. However, if rates go up then they will be kicking themselves for not having purchased at the 7% rate. Homes prices are not going to come down substantially. Inventory will increase a little as baby boomers like me put their largest nest egg on the market especially if it’s paid off. After 3 years, the signs indicate very little change in the marketplace and the Trump tariffs will not help. Cheers.

“Homes prices are not going to come down substantially.”

Your home is in a local market, and it’s not the national median home. Quite a few big local markets are already seeing “substantial” price declines. Here are some examples, and by the looks of it, it’s the beginning not the end:

https://wolfstreet.com/2025/05/26/the-10-big-cities-with-the-biggest-price-declines-of-single-family-homes-from-their-peaks-through-april-7-to-21/

Spoken like a true boomer with too much wealth vested in RE and counting on it to be the golden ticket to easy retirement. Nevermind the next couple of generation down that get saddle with unhealthy level of debt just to get that house.

But hey as long as I get mine, Fxxk the rest…

Of course he’s going to talk his book. He sounds like a RE agent.

It’s also a comfortable place to be, part of a generation of historical economic expansion, juiced by toxic policies and stolen futures (see: government debt, globalization, interest rate repression).

Good luck, good timing and a little bit of diligence, sure. However the economic landscape of the past 20-30 years is almost completely foreign to the 20-30 years prior (see: wage growth vs. inflation, pension vs 401k, wealth distribution and above toxic policies).

I remember 2005 in South Florida, when my coworkers were saying the same thing.

People are saying it again in South Florida, saying it’s “different this time” with “so many funds and banks moving to Brickell.”

It’s all BS. Most of these offices have 10-15 people.

I tend to agree with you vadertime, and I am not a real estate agent hahaha. Even looking at the weekly purchase mortgage application index chart, you can see it bottomed out in 2024 and is trending a bit higher since then, although its too early to call. Definitely not enough of an increase to compare to the inventory increase, but an increase nonetheless in a rising mortgage rate environment since the rate hit bottom a bit past mid 2024. Interesting times for sure but if you live in an area where the price has already decreased substantially it could be a good time to buy there.

Pull up a Zillow map of Naples, FL. Make sure you are wearing sunglasses because you are about to see a wave of red “for sale” listings. Never seen it like this.

“Waiting for lower prices, higher incomes, and lower rates”

Amen. Good luck!

Here’s my recent run in with inflation. 5 years ago I go a quote for a PlyGym picture window $126. Nowadays, the same building supply house, BFS (one of the largest in the nation), quoted me $620 for the exact same window or 500% higher.

This window is probably 50% higher today. Maybe. Building supply prices spiked during COVID, but most everything is way off their COVID highs. Sure a lot of stuff is 20-30% higher. But 500%? That’s beyond price gouging.

Again, this is what happens when you go 15+ years without a real recession.

Yes, I’ll only add that we haven’t allowed bad actors to suffer real consequences for their bad behavior (hello MBS), in fact, I’d argue that the financialization of everything, and monetization of debt has rewarded bad actors and bad behavior. Just look at CONgress.

Prices of most things (Food, Cars, Real Estate, Vinyl Windows) have been going up in price due to inflation for my entire life and I don’t see it stopping. P.S. To @GuessWhat get a quote on a Milgard window, they will cost a little more on average but are MUCH better than PlyGem/Cascade/Cornerstone vinyl windows (I’ve spent the last 20 years replacing aluminum single pane apartment windoes with vinyl double pane windows)

Thanks!

ApartmentInvestor: Two questions. What makes the Milgard better than a PlyGem, Alside, Pella 150 series, or any other vinyl window? And why bother replacing those metal single pane windows (which usually have 2 or 3 “storm sashes”) when you can service the glass, slides, and weatherstrips for another century?

@Mitry

1. I don’t know much about Alside or Pella, but Milgard windors have better quality vinyl, locks and glass (less UV coating failures) than PlyGem and Cascade (that are under the same corporate ownership).

2. Not many homes and apartments in CA have storm sashes and after 50 years most aluminum windows have bad rollers, locks and seals (and they look like crap).

Replacement windows are easy to pop in and make an apartment look newer and keep noise and drafts out of the apartments.

Got it. When I was younger I worked for a glass company that specialized in rehabbing those aluminum windows. We’d cut new glass on site, kept rolls of weatherstripping, and those rollers were just plastic bushings with no moving parts. Just a soft, sacrificial piece of plastic to keep the metal sash from sliding against the metal frame. About $15 worth of parts for essentially a new window. Same metal frames though, so you’re stuck with dark bronze in the end. I can see how new windows, especially in white, would improve the look of the room. I thought to myself back then, “If only I had an apartment building…”

I’m glad the windows are easy to replace. Here in MN they tend to have 2 nailing fins — one that goes parallel to the sheathing and another that goes perpendicular to that, into the framing of the building. They’re a lot of work to get out.

If you get a seal failure on your double pane glass (i.e. bloom from low E failure) the glass can usually be replaced from the interior. Pull off the glazing bead, cut the seal on the exterior, pull the glass out. Glad the Milgards are working out for you.

40+ years of financialization. This is what you get, lots of supply, lots of demand, but no one is buying because there is no true price discovery. Prices are still too damn high and the bankers and financiers will not allow any deflation.

Fine,

the financiers want to “let everyone eat cake”, fine, the outcome will be no different this time around.

FOMO being replaced by fear universal catching knife.

Your home price appreciating is not a profit, it is only enabling you to keep up with inflation, perhaps. Why sell it?

I had been saying for a long time that in my town outside of DC – but in the DC metro – houses in the good neighborhoods were still getting bid up, going over asking. And it seemed like we were beating the broader markets.

Suddenly, like in the last week or two, there’s houses – good houses – that aren’t selling. It’s amazing to me, but I guess even rich people are scared to death to make a wrong move right now.

I wasn’t planning on selling anyway, so I don’t care. I mean, I care that our country is going to shit and don’t want my town to follow suit, but I don’t particularly care about house prices (as long as no “rif-rafs” get in…I want to be the last of those…)

Globally, risk is being repriced. The upper middle class may be finally waking up to this. The Jamie Dimons of the world have known this for a while. More people should have cared about the country as we have been rewarding bad behavior for 40+ years. Moral hazard on an unprecedented scale, globally…

Just so a select few could maintain power and grow their wealth to unbelievable heights…

Humanity has been here before, hedge accordingly.

LoL, so we are going to do it again. The last housing crash was epic. So what happens when it gets going again? Those who remember just might panic and gtfo. Now, the next question is how much inflation would finally bail out the housing market? The median price should reflect the ability to buy at roughly median income plus 10. So, wages have to skyrocket, or prices have to come down. Or interest rates have to come down. I think they are going to go up. And up. Metals prices are starting to pop, and anything that can be exported will be, have to use those dollars before they burn.

The real question is if foreign holders of US assets begin to panic. Then what? The most evil statement in finance has to be “market discontinuity” and “fast markets”.

But hey, real estate only goes up? Really the question is now can the US solve the usual fiscal and financial crisis again like in the 1980s, or will we be paralyzed into a much larger crisis?

I vote for continual crisis.

Someday this war’s gonna end…

Great bubble and in this case epic bubble require great shock doctrine to keep it going. This has been true throughout modern history both in economics and our societal changes.

Shock doctrine is the playbook A great read if anyone interested in that book

I’ve read the Shock Doctrine but it’s less of a playbook more of an autopsy report at this point.

Winston Churchill once said that Americans can be counted on to do the right thing – after trying everything else first.

We’re still in the “trying everything else” phase.

@Citizen AllenM you are correct “last housing crash was epic” but we don’t have millions of “liar loans” and “neg am” loans today making an “epic” housing crash unlikely. We all know that most markets are flat are down (despite the fact someone just posted today that his zip code is up). Since I am in the rental business I can tall you that with rents going up with inflation combined with the low-interest rate loans that most homeowners have there are less people than ever that “need” to sell. Most older adult homeowners saw prices bounce back even higher after the last “epic housing crash”. I told my friend Tom to rent his family Tahoe cabin in 2011 after his Dad died but he panicked and sold for $900K. The guy that bought it rented it as an AirBnB until he sold for $1.8mm in 2016 and Zillow says it is worth $2.8mm today. Nobody wants to be like Tom (and all the other Toms that “sold at the bottom”) and all the guys with the 25% LTV 3% loans are in a MUCH better position to hang on (renting with a property manager if they do NEED to move) than the guys that saw their monthly payments double at the end of the teaser rate in 2009 and were forced to give the keys back to the lender.

Nope this time is going to be different, lol. We have instead a lot of recent buyers who are going underwater, and they will panic again. The other kicker is interest rates. Those cheap rates directly caused housing to soar (just like bonds), and now they will crash. Now, it may be profitable to rent and wait it out, which is what rich people do, but those who lose their income will, as usual, have to go. Demographic headwinds are also coming for us. Add in the high market costs, and the fact we will begin to suffer the effects of foreign investors pulling out their capital instead of putting it here. We are at the end of the center of the universe. But instead of worrying about minor financial moments, one should begin to worry about the end of growth in America, and what it really means for us to live within our means. The silly political posturing I see is even more ridiculous when we have to seriously raise taxes and that is going to cost us more than we believe possible at the moment.

Remember, it took a major herculean effort to affect the last bailout. Now, the capacity of markets to absorb massive amounts of UST debt is far less, and our international position is much worse.

Right now, the world still sees us as a destination, so cheap labor keeps appearing. But when you use total information to remove everybody who is not supposed to be here, well, a lot of rich people will have to pay a residence tax, or leave. And those pesky homeless just keep accumulating in our streets, putting a floor under used RV prices.

Our dollar, your problem was the old way, our dollar, our problems will be the new way.

Your name checks out nicely :-)

Depends on your market. Rents were down 5.8% yoy in Denver as of February or March and we’re still building!

Also with regards to “liar loans” again might depend on your market. I know multiple people who had to buy down their interest rate to get the acceptable debt to income limit to get approved for their loan. These buy downs were only 1 – 2 years though…. Also I’ve got pre-approved for some ridiculous amounts, yes I have an 800+ credit score, but still…

Also highly transient cities are more likely to experience issues. If you have a lot of people who bought in 2021 at the top with 3% down there could be an issue. Cities that don’t have a lot of turnover and homeownership is more long term, yeah they all refied the house they bought 10 years ago at 3% and they’re fine.

People are saying that since the M2 money supply and velocity are increasing that real estate won’t drop very much. Do you think this is true wolf?

M2 is an outdated garbage metric by the accounts it includes and excludes. Leaning on M2 to figure out anything is a fool’s errand. But the gold bugs and RE bugs seized on it.

Are these people Land Lord, Realtors or someone invested in real estate ?

Many hot markets have already seen price correction of more than 20%. The reason is same: Extreme un affordability.

4 states have now abolished RE Agents. They have been replaced by RE Brokers who have to take a difficult test to get their Broker’s license. These unemployed RE Agents are SOL (S$it out of luck) . The reason this was done was because the number of complaints against RE agents spiked to the point where it was causing serious problems in these state for the companies that employed them. I see the whole profession going under across the whole continental USA.

This was long overdue. In my own experience, every RE agent I have ever used in my lifetime has been completely incompetent. There are some good ones out there till, but they will get lumped in with all the incompetent ones, unfortunetly.

Amen to this, the last couple of RE agents that we had to deal with for rental properties we looked at was pretty worthless. The one we ended up dealing with was some old lady that should have retired long time ago. When we moved out and saw the rental listing relisted again her contribution was hammering a for rent sign at the front and added a plant inside for a nice than steller photo session. If they are all gone that honestly good fing riddance.

A year and a half ago I was with a friend of a friend who’s developed and sold a number of tech companies and now basically funds various startups (tech and non tech) – with a small group of partners. The current project he was excited about was software to replace real estate agents. That most contracts are pretty standard, with asking the right questions – paragraphs could be added or deleted etc. They’d charge 1% or half a % instead of the 2.5-3%. AI was newer then so they weren’t even including AI – but with AI I think the writing is on the wall. The software part is easy the politics may be challenging though.

The only reason they’re keeping their jobs is because now thanks to the new commission rules, I can’t see a house in Denver without a real estate agent. However, I have to sign a contract to work with them if I do want to see one. So basically they force one on you.

The tech solution will have some regulatory hurdles but is the future. My guess is phase 2 would be connecting that with the financing process. Again not hard, definitely could be automated. Remember when people used to do taxes on paper or pay a CPA? Now most people (unless they have a very complex situation) can just use TaxAct or HRBlock software which idiot proofs the system. Or remember when people used to meet with a banker in person to open a bank account? This will be the same thing.

While I don’t wish just losses on anyone, paying someone 3% which is upwards of $20k in a lot of markets is ridiculous. If the fees were lower it might make sense to keep them around – but the tech solution makes so much more sense at current prices.

My in-laws are elderly. They have a rental they decided to sell because they can no longer keep up with it. The suggestion was sell it “as is” now because you are opening up a can of worms as old wood frames in Florida always are.

No no no, we can make a bundle!

It’s now taken almost a year for them to finish putting all them worms back in the can.

My estimate, based on recent sales in that area of Tampa, they are going to net less finished than they would have as is, and the area is desirable and gentrifying close to downtown.

You can tell them, but you can’t tell them much….

Guess greed really don’t subside when you age….at some point maybe it’s wiser to realize you don’t live forever so netting 20% less might just be ok to still carry you through until 6 feet under ..

Or alternatively fly too close to the sun and get almost nothing, in that case probably have nothing to last until the finale .

Depends*…..good post…….think I’m good till exit (and can probably still leave 40 off grid acres to family…with a started 3 story five 20′ container home that has very stout back destroying foundation. Got it zoned for two homes anysize or FIVE if related…even loosely…plenty water….great piece of land……they will all probably just agree to sell it….somehow…….no cap gains, but there may be a few pioneer types left)…and always have option of early outs when things get worse. Meanwhile, have a Library and huge fast research staff all the robber barons would have envied…..dabble in social media although I generally have disliked it as much as reality shows and sitcoms…..I’m VERY curious, too.

* https://en.wikipedia.org/wiki/Idola_specus

No cap gains to PAY on maybe 150-250K at present.

@Phoenix_Ikki not to pick on you and I don’t know @LibDis’ parents but everyone that decides to invest some money and get a return is not “greedy”. Few people want to buy a fixer upper home, or car that does not start so if I make a home move in ready or a car drivable it it more about “wanting to sell it” than “greed” (like LibDis parents I have often spent more than I planned to make a home livable or a car drivable).

This make Ikki a troll? LOL, anyway.

Should have been under AI’s “in defense of greed” lecture.

Hint; Best to avoid word “greed” entirely and use in “job creator” or similar.

Plenty of examples around.

Phoenix_Ikki is the new Debt-Free-Bubba with already more than 10% of all comments.

Commenting rule 6 is really more of a guideline.

Please don’t make me count comments lol

Not enough worms left in the can 2 go fishing? I would think foreign investors would be buying up California real estate hand over fist? The word is out on Main Street, Sam’s club is fully stocked with my favorite tissue and paper towels. I don’t hear anyone complaining about there not being enough homes on the market or for rent. New car and truck purchases is where I will judge Americans economic collapse. Family vacations to Disney, visits to restaurants. There are lots of non profits initiatives not longer being funded by Trump’s administration, disposal income is not what it used to be. Cutting your throat to blow your nose is never a good idea, keeping up with the Joneses fantasy is now cancelled. Blood from a turnip with a 7% interest rates.

The thing about demand destruction is—it’s loud from above and silent from the street.

I’m standing on lawns in New Hampshire where houses never even hit the MLS because sellers still think they’re owed 2022 prices. What they’re really doing is hiding from the math. Meanwhile, the buyers are curled in the fetal position whispering “7.25%” to themselves.

We’re not just seeing cracks in the system—we’re watching a whole architecture of belief collapse in real time. Your breakdown gave language to what it’s felt like trying to work inside this hallucination.

(Also, I’ve got a haunted hot dog stand metaphor. But that’s for another day.)

Maybe it’s time to lower rates a bit. While tariffs may cause inflation in some sectors, people might just go without those items. Maybe they are secretly hungry for housing and lower mortgage rates too and will buy houses and refinance mortgages instead. But I’m just speculating.