Update on an ugly situation.

By Wolf Richter for WOLF STREET.

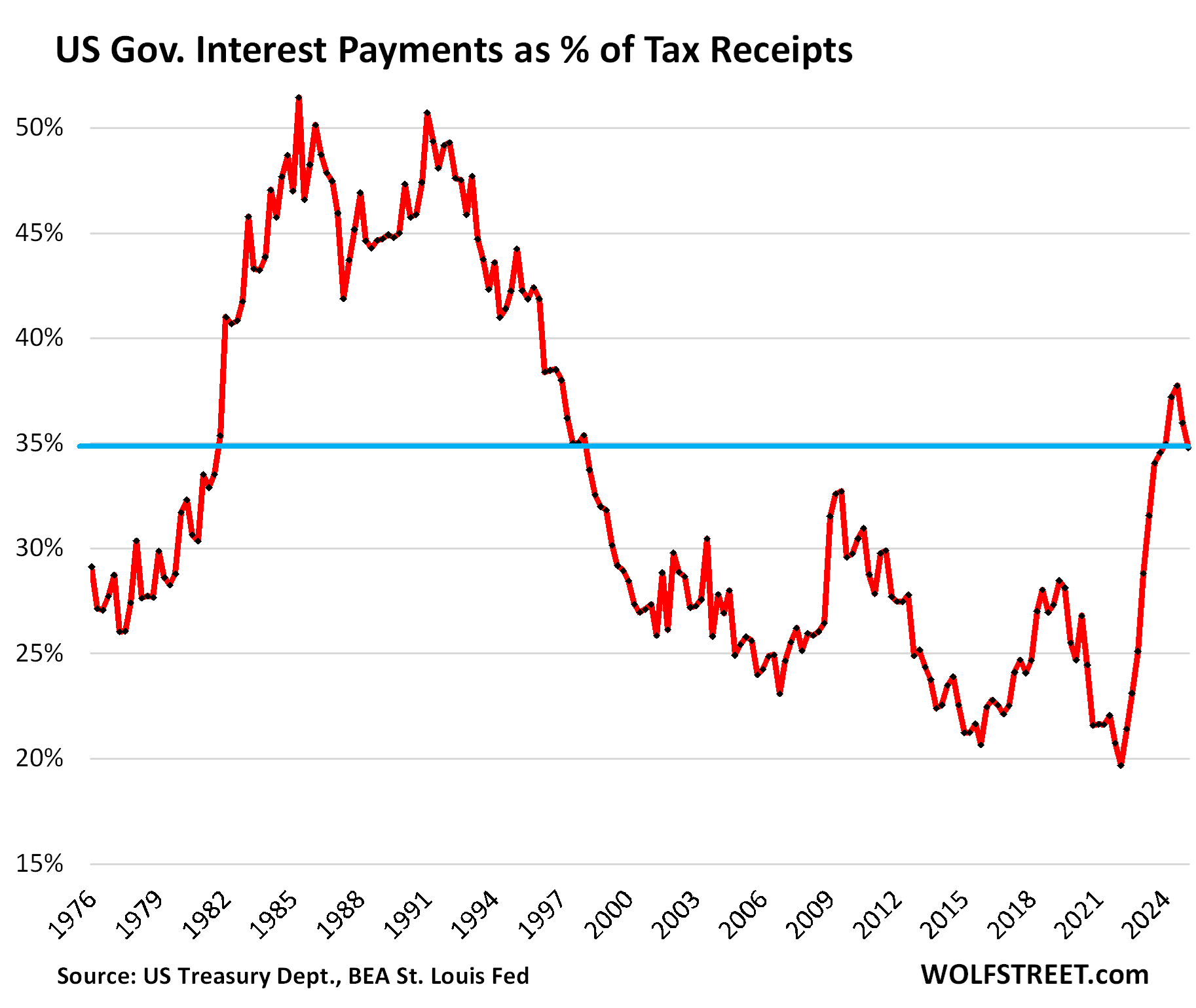

A key issue of the US government fiscal situation: What portion of the tax receipts are eaten up by interest payments on the monstrous and ballooning federal debt. At the peak of the last crisis in the early 1980s, that ratio had exceeded 50%. It was a crisis because the 10-year Treasury yield was over 10% for six years in a row and mortgage rates were over 10% for 12 years in a row, an unimaginable number today but bitter reality back then.

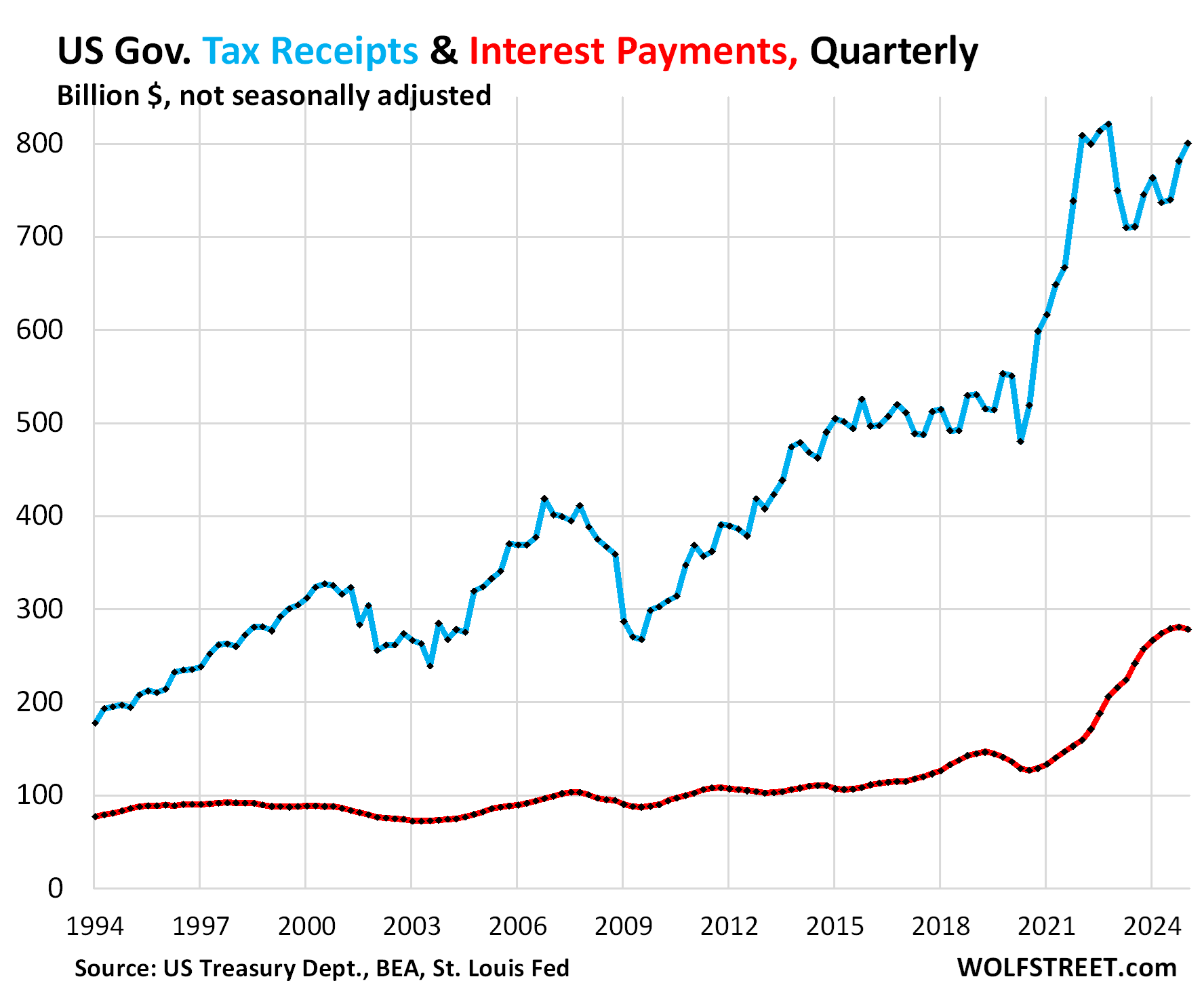

Interest payments by the federal government on its monstrous $36.2 trillion in Treasury debt dipped by 0.9% in Q1 from Q4, to $279 billion (red in the chart below), helped by the lower interest rates on the $6 trillion in Treasury bills, whose yields track the Fed’s short-term rates that got cut by 100 basis points last year; and by the debt ceiling that temporarily prevented the debt from surging further though it will make up for it when the debt ceiling is lifted or suspended.

Tax receipts by the federal government rose by $19 billion (+2.4%) in Q1 from Q4 and by $37 billion (+4.9%) year-over-year, to $801 billion (blue in the chart below). Tax receipts jump and drop with capital-gains taxes, while employment taxes and income taxes rise fairly slowly and steadily unless there’s a recession. Q1 tax receipts benefited from last year having been good for stocks and other assets, with capital gains taxes due by April 15. Q2 will also benefit from those capital gains taxes. By contrast, 2022 was a bad year for stocks, and tax receipts in Q1 and Q2 2023 came in much lower, after the spike during the free-money-from-heaven pandemic.

This measure of tax receipts was released today by the Bureau of Economic Analysis as part of its second revision of Q1 GDP. It tracks the tax receipts that are available to pay for general budget expenditures, such as defense spending, interest payments, etc. Excluded are receipts that are not available to pay for general budget expenditures, primarily Social Security and disability contributions that go into Trust Funds, out of which the benefits are then paid directly to the beneficiaries of the systems.

Interest expense as a percent of tax receipts: Interest payments in Q1 ate up 34.8% of the tax receipts that were available to pay for them. The ratio declined for the second consecutive quarter, driven by higher tax receipts and the dip in interest payments.

The recent high occurred in Q3 2024, at 37.7%, the worst ratio since 1996, when it was on the downtrend from the scary times in the 1980s. The magnitude and speed of this spike over the prior two years was unprecedented in modern US history:

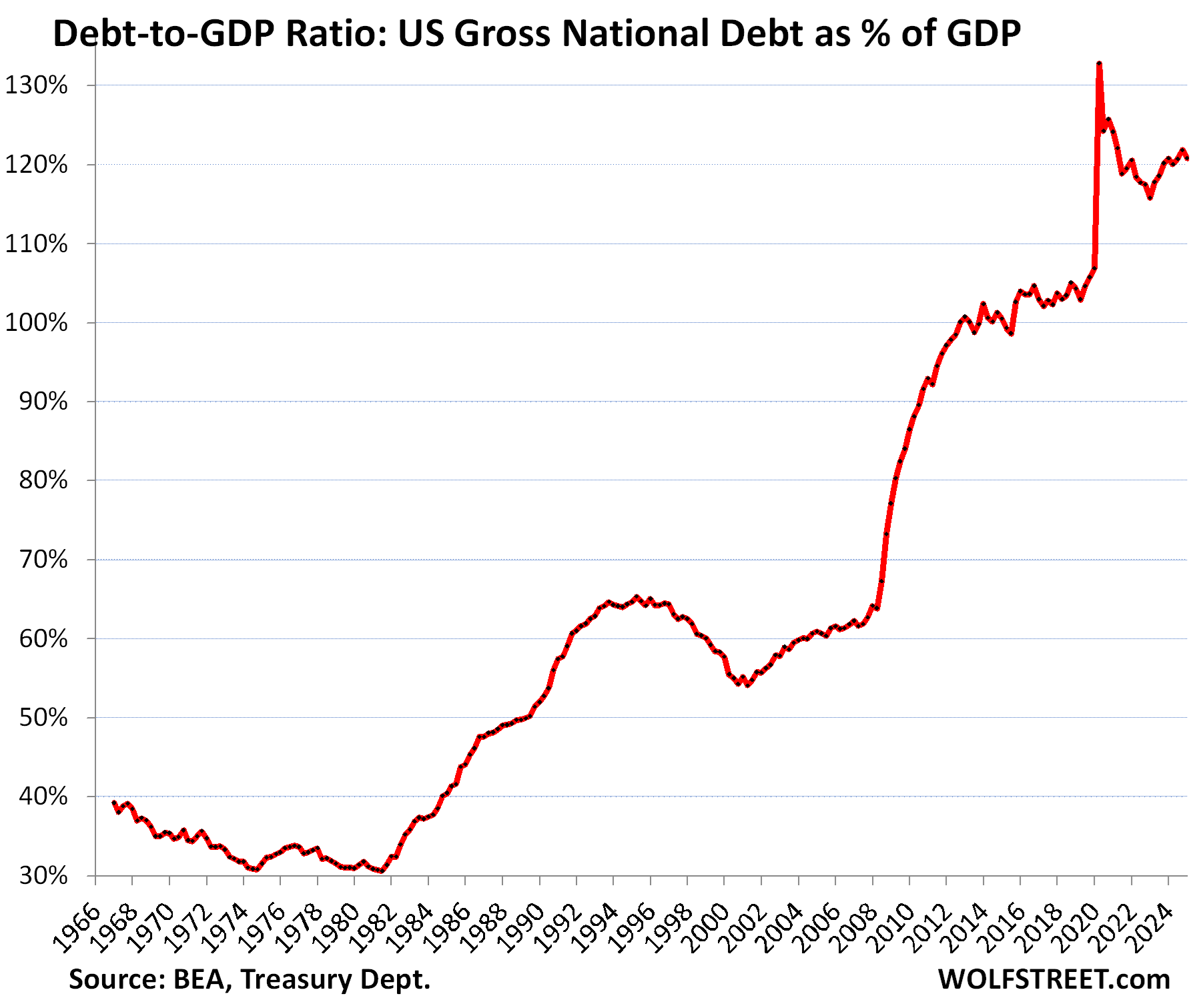

The debt has ballooned by $13 trillion (by 56%) in just five years, from $23.2 trillion in Q1 2020 to $36.2 trillion in Q1 2025, including by $2.2 trillion in 2024 despite above-average real GDP growth.

The ballooning of the debt is temporarily on hold due to the debt ceiling, but to make up for it, because there are no free lunches, it will spike by $1 trillion within months of the debt ceiling getting lifted, and will continue to balloon with renewed vigor afterwards.

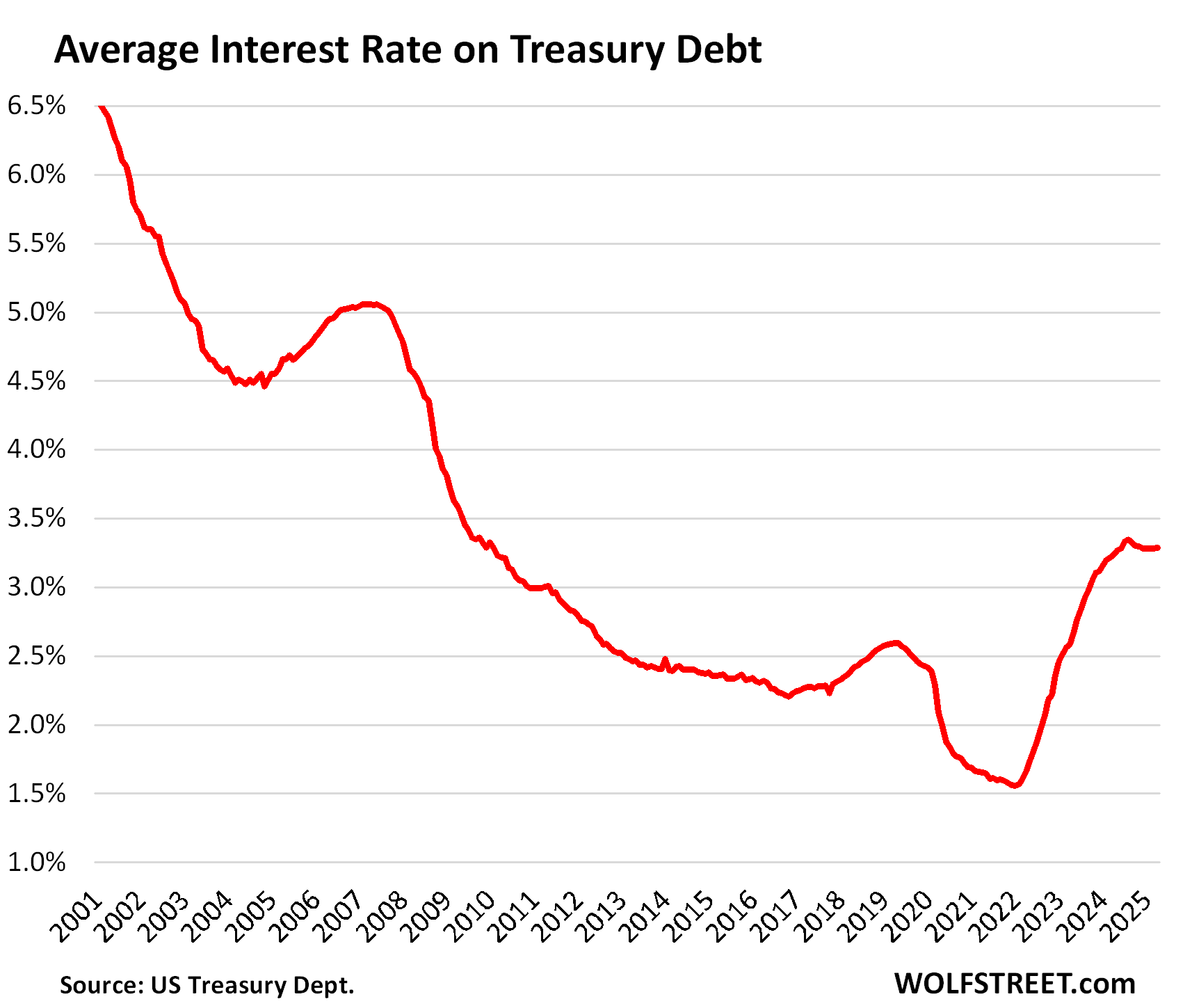

Interest rates are much higher than the historic lows five years ago.

Short-term interest rates had been at near-0% in 2020 and 2021, but started rising in 2022 and reached about 5.4% in mid-2023 and then stayed there for a year. Last fall, the Fed cut its policy rates by 100 basis points, which has pushed down the interest rate at which the government can sell T-bills to about 4.3%. The $6 trillion in T-bills are constantly getting rolled over as they mature, and new T-bills are sold at lower interest costs for the government, which contributed to the dip in interest expenses.

However, the interest rates at which the government can sell long-term Treasury securities have not changed much over the past two years. For example, the 10-year yield lurched up and down over those two years, sometimes violently, but has mostly remained in a range between 3.7% and 4.7%, and is now about where it was a year ago (4.4%). And those rates are far higher than where they’d been.

For instance, the 10-year Treasury issue that matured this month was sold in May 2015 at a yield of 2.24%. The government replaced it this month with new 10-year notes that it sold with a yield of 4.34%, nearly double the interest cost for the government.

In addition, the size of the issue has doubled, from $24 billion in 2015 to $42 billion in this Month.

But the process is slow. Long-term securities by definition are slow to cycle out of the debt, so changes in long-term interest rates filter only slowly into the debt as old maturing debt is replaced with new debt that comes with the new interest rates.

These dynamics form the average interest rate that the government pays on its total outstanding debt. That average interest more than doubled from 1.55% in 2022 to 3.35% August 2024. Since then, it has eased a hair. In April, it inched up to 3.29%, according to data from the Treasury Department:

The ugly Debt-to-GDP ratio: Total debt as percent of GDP eased in Q1 to 120.8%, based on the second estimate of Q1 “current dollar” GDP released by the BEA today. It dipped because the debt ceiling temporarily blocked the debt from growing.

The Debt-to-GDP ratio = total debt (not adjusted for inflation) divided by “current dollar” GDP (not adjusted for inflation). Inflation cancels out because the inflation factor affects both the numerator and the denominator equally.

Obviously, the US, by controlling its own currency, cannot default on its debt because it can always “print” itself out of trouble (Fed buys some of the debt). But printing money to service an out-of-control debt and deficit in an inflationary environment could cause inflation to spiral out of control, which would wreak havoc on the economy, lead to years of economic pain, wealth destruction, and lower standards of living. So this is nothing to be trifled with. The far better solution is to trim the annual deficit down to where economic growth and modest inflation outrun it, which would over time alleviate the problem.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Obviously, tax cuts at this time are irresponsible.

If GDP growth averages 3% and inflation averages 2% then what level of deficit can be outrun by those levels? I’m not sure I understand that part.

Just some basic thoughts.

1. Deficit and debt are not adjusted for inflation, so you must relate them to GDP not adjusted to inflation (= “current dollar” GDP = nominal GDP). Current-dollar GDP growth in 2024 was 5.2%.

2. Over time (if there are no changes in the tax law), tax receipts grow at about the same rate as current dollar GDP.

3. If “current dollar” GDP grows by 5.2% in one year, and the debt grows by 3%, year-over-year, then over time, without tax law changes, the burden should diminish.

4. But last year, the debt grew by 6.5% from $34.0 trillion to $36.2 trillion, and the economy grew by 5.2%. So that’s a no-go. And it has been that way for years.

5. In addition, there are constantly tax law changes that worsen the relationship between tax receipts and current-dollar GDP, where it takes more current-dollar GDP to generate the same tax receipts. The current tax bill also seems to do that. So it’s not a straight line.

6. The debt grew by 6.5% in 2024 because the debt issued to fund the 2024 deficit added $2.2 trillion to the debt. But to get the deficit down to where it only increases the debt by 3%, you’d have to cut the deficit by over half (to $1.0 trillion).

7. Higher inflation causes current-dollar GDP growth to run at a higher rate so that helps. The old debt is fixed (except inflation-protected bonds), and a higher current-dollar GDP due to inflation allows the government to pay borrowers with dollars that lost their purchasing power. This is why the bond market HATES inflation – because bondholders get screwed. But the government loves inflation because it devalues the debt.

So all roads lead to “financial repression”? At least for the last 2 years they haven’t been too successful on that front. I guess TIPS would be a decent defense?

Re 2. Could this become not true as household wages diminish relative to GDP per capita?

I know GDP is convenient to measure “the economy” but could there be a better measure of “total of things the government typically taxes to get revenue?”

And maybe that’s too tricky given point 5. But given the outsized role of income taxes, is income alone enough to compare against?

Dave

The BEA, which puts together GDP, also puts together a sister measure, Gross National Income (GNI), which tracks the economy at the income level. Over the long term, they run about the same growth rates.

In terms of your point: “Re 2. Could this become not true as household wages diminish relative to GDP per capita?”

About two-thirds of GDP comes from consumer spending. Consumers spend most of their income and save the rest. So if consumer income declines, their spending will decline, and GDP will decline.

In terms of the “per capita,” what moves that needle is the number of “capita.” So if the population surges through an explosion of immigration, such as in 2021-2024, there are more “capita” to divide GDP by, and per-capita GDP rose less than overall GDP. In Canada, where this took place on a relatively much larger scale in 2021-2024 than in the US, per capita GDP growth went negative for a few quarters due to the explosion of their population, while overall GDP growth was positive.

Finally, Mr. Wolf. Now start to talk about a VAT tax, and a solution to the present debt problem.

Andrew pepper

When I was an expat in Europe, I lived with a ca. 20% VAT. Not a fan.

I’m a big fan of a transaction tax, a minuscule one, such as 0.1% but on ALL transactions, seller pays, from stock trades to selling homes, to selling food. That $5 loaf of bread would increase by half a cent, but when Apply buys a company for $20 billion, the sellers would pay $20 million in transaction taxes. If you sell a $500,000 home, you’d pay $500. You would barely notice it among all the other fees you’re paying. High-speed trading firms in the financial markets would pay a lot since they run such huge volume, and it might put a damper on that section of Wall Street, and that would be a good thing. The $5 trillion a day repo market would pay a lot, and it would slow that form of lending down, and that would be a good thing (the repo market blew out in 2019 and required Fed money-printing to deal with it). A 0.1% transaction tax on ALL transactions, no exceptions, including anything crossing the border, would slow a lot of the excesses in this system.

Is there any reason that the US could not impose a 25% AMT on incomes over $1M and 10% AMT on corporations with over $1B in revenue. A Chat GPT check states that in theory that would reduce the deficit by $1.2T annually.

@PeterG – TIPS yields are historically high now, but …

Taxes eat away at those returns.

So unless you’re in a very low Federal Tax bracket in a low-income-tax state, it’s very hard for TIPS to outrun inflation after paying taxes.

I-Bonds are a similar option and come with an education tax break provided income is low enough to qualify.

One of the differences between TIPS and ibonds is that the inflation protection added to the principal of the TIPS is taxable income in the year it is added to the principal. So every year you get a 1099 for the income that was added to the principal, and you pay taxes on non-cash income since you never got paid that interest. You will get the inflation protection all at once when the TIPS matures, but you already paid your taxes on the inflation protection and are good to go. So it’s best to have the TIPS in a tax-deferred account, such as an IRA or SEP IRA.

It’s variable, depending on economic growth and inflation as you say, but historically the debt to GDP ratio starts to decline when the deficit falls under 3% or so.

India equity/futures/option “volume” wise (not $ wise)among the 1st/2nd in the world. Securities Transaction Tax is levied in India on all stock,index futures and options. Next to excise duty and customs duty , STT tax isa big tax revenue for central govt . (GST aka vat /sales tax 5/12/18/28 % is only for business that is passed on to the end consumer ) Retail MRP is inclusive of all taxes) STT rate on stocks is 0.025% on all sell transacions. Equal value is levied on option premiums sold. no estate tax, no gift tax. but short term capital gains tax on all rea estate /equity/bond is 15% (less than 1 year ) long term capital gains tax 10% (above 1 year ). Service tax gst @18% is levied on most of the services.

Well done, so about 3.3 average interest rate, why am I always seeing that number and using lurched is classic…you can see from 2010 to 2025 the same chart on stocks, just overlapping them…

I agree that further additional tax cuts would be irresponsible.

But only in the upside down world of DC is continuing current tax rates “cutting taxes”.

So yes, some tax increases are probably necessary.

But what is even more essential is real cuts to entitlement and defense spending and a complete gutting of the IRA. If we raise taxes but don’t cut spending, we’ll be in this same place again within 5 years, because entitlements are out of control.

To follow up with a few detailed examples from recent history.

When the ACA was enacted in 2008, the cost was low-balled by the CBO because the tax provisions applied for 5 years but the start of the program was delayed for 3 years.

So basically you had 5 years of revenue for 3 years of benefits. So the CBO estimate underestimated the long term costs by 40%.

And it ended up being less expensive only because SCOTUS allowed states to opt out of the Medicaid expansion, and 20 states did. Most of them have since opted in because it’s almost free money to the states. This is a fiscal disaster that was totally underestimated by the CBO increasing massively in cost about 8% year over year.

The other example is the IRA. Projected by CBO to cost 370 billion over 10 years.

But the open ended nature of some of the credits means the true costs are closer to a Trillion per several analyses. For what? For things that won’t move the global temperature even 0.1 degree C.

Defense spending is also far above sustainable. Why are American troops stationed in Korea and Europe 80 years after wars there? Let’s let those countries defend themselves. Are we going to be there 300 years?

In other words, this can’t be solved just by taxes. We MUST slow down the spending.

Happy1,

“In other words, this can’t be solved just by taxes. We MUST slow down the spending”

In general I agree – but American “leadership” (government, corporate, institutional) has caused things to be so horrifically out of control – *for decades* – there is simply no other way to remotely address the accumulated cancers.

There is going to have to be *some* additional level of taxation *in addition to* serious spending cuts.

The heroin illusions of money printing are more and more playing out their string – terminally toxic inflation will result from leaning on that tool much more.

Willingness to even accept wealth taxes is (very slowly) beginning to grow – at least against the deserving disfavored (college endowments – absurdly untaxed for decades and decades and decades).

When things really begin to be hopelessly awful, I don’t think the resistance to (very heavy) taxation of multi-million dollar inheritances (paper circumventions like manipulative trusts only endure as long as public tolerance does) is going to last very long.

Some innocent wealthy are going to be unfairly screwed, but, as a *class* the wealthy have grotesquely mismanaged the nation into the ground (1946 – unquestioned premier World Power – 1966 to 2026 – increasingly financially crippled wreck).

When things get bad enough, nowhere near enough people are really going to rally to the defenses of people like Musk (who, for his real world accomplishments, has also shown himself to be an unstable blow-hard – equally capable of idiotic failure as well as challenging success).

Pushed against a fiscal wall, almost no one will ultimately die on the hill of ensuring that Musk’s 4 dozen love children inherit tens of millions.

The tide of necessary taxation will sweep far wider than that – but those starting points are essentially inevitable.

Only near-intentional Democrat political incompetence has kept that wave from starting already.

As the article notes, about a third of your tax dollars are going to pay the interest on the national debt. The national debt was accrued starting in the 1980s with various tax cut bills that have continued to this day, 45 years later.

Had these tax cuts not occurred, perhaps the national debt would be trivial and we’d not be spending over $1T per year on interest. Talk about wasteful spending… all we receive from this extortion is the opportunity to live another day without the currency collapsing.

So now we’re talking about cutting Medicaid, Medicare, and Social Security – programs that worked fine since the 1940s and 1960s – because the tax cuts of the past 45 years have run up such an expensive interest bill on the federal side. We will have elderly, poor, and disabled people dying and starving in the streets like some third-world country because of those decades of tax cuts that were supposed to make us prosperous, not a debt shell.

When one finds oneself in a hole, the first thing to do is stop digging. Yet, what are we doing? Falling for the free money gimmick one more time.

Chris,

I am not sure where you ever got the idea that Social Security, Medicare, and Medicaid have “worked fine since the 1940s and 1960s” but nothing could be further from the truth.

Congress tinkered around with the Social Security payout formula so much in the 1950s, 60s, and 70s that the whole program teetered on insolvency by 1983. A blue-ribbon committee headed by Alan Greenspan proposed a series of reforms that extended the life of Social Security by 50-plus years but even now we are approaching the end of that time horizon.

Medicare has even worse funding problems and has done so right from when it was first enacted in 1965. Payroll taxes covered about 73% of Medicare expenses in 1970 but now contribute only 36% of the program’s cost. General Fund contributions now make up 43% of the cost of the program and Medicare is now 14% of the federal government’s total spending (NET the collected Payroll taxes and Premiums).

Fortunately Congress learned its lesson in 1983 and has largely left Social Security alone… which is why it can be tweaked and extended pretty easily. But Medicare’s uncontrolled growth is threatening to take down the entire budget and there are no easy solutions to fix it. BOTH “trust funds” are expected to become insolvent in the mid-2030s so if you have any solutions then NOW is the time to propose them.

The BBB keeps current tax rates constant, otherwise the rates will return to the previous levels and cause a $4 trillion tax increase.

To me it’s not clear that tax cuts are irresponsible. It’s like a marriage where 1 party pays and the other party spends. The spending party tells the paying party, “you are irresponsible because you propose reducing the amount you are willing to pay while I am determined to spend more and more regardless”.

It might be irresponsible if the spender and the payer were one in the same person. We are told that is the case because: “democracy” and we are all represented and all in this together. That is at best a misunderstanding and at worst a lie.

The continuance of your argument would be that the payers – the 50% of tax payers who pay 97% of the bill should be “responsible” and agree to pay more. However, all of the evidence is that the spenders will take all the extra the payers pay and spend that and more and use the reality of having a bit more income to justify spending that and even more for “democracy”, “compassion”, “the children” and the mean men “Putin” and “Xi”

I would argue that tax cuts are actually the path of virtue. Give people more of their own money so they have a better chance of preparing for the reckoning that will come some day. And at the same time, hastening the day of that reckoning while we still retain some strength to meet it and recover.

Preach it brother! If they come up with new taxes they’ll come up with more ways to spend it. Congress has lost its mind

Nonsense. A huge tax hike on the poor and middle class will cripple the economy, devastating revenue. Spending will INCREASE, exacerbating the problem and bringing us to the warning issued in the article’s last paragraph.

We have a spending problem. Congress MUST codify DOGE cuts and find more areas to cut themselves, period.

Printing money to service an out-of-control debt and deficit is the definition of inflation.

It is called “monetization of debt”. And, when it happens, history guides us.

It will finally come to an end point. When and how it plays out are Xs In the monetary outcome.

My guess is more and more inflation leading to a serious crisis.

Cheers,

B

Brewski – In history’s examples of nations monetary outcome were those nations the worlds default currency, largest economies and largest military along with technologically more advanced than any other nation?

History rimes it does not always repeat. No?

Britain in the Victorain era (late 1800s early 1900s) met all the criteria and only had a very narrow escape from its debt trap. Thanks in part to the United States.

For the U.S. today, few reasonable options remain available. It’s not worth risking calamity over debt, but here we are.

My best guess on the endgame here is an interplay between a debt crisis in the bond market driving up interest and mortgage rates, the climate crisis affecting the insurance industry, feedbacks between those two problems and then both of them blowing up the housing market and the rest of the economy with it.

Those are both already pretty mainstream theories anyway. The budget committee from the last senate published a lot on the latter problem, and everyone from Wolf to Paul Krugman to Jamie Dimon have been talking about the former.

@micheal I think the factors you’re listing there are really only useful for buying us time.

Oh please, there is no climate crisis. Too many people are building and living in high risk areas.

The ‘green house effect’ meaning increased retention of the sun’s infra- red radiation is scientific fact. I looked up how it is demonstrated and was surprised to find its a 1-2 hundred dollar ‘table top’ deal often done in colleges, even juniors.

Required: two transparent containers, separated by a thin layer insulation. A basic air temp thermometer in each one. A 100 watt halogen bulb, and a source of C0 2. This has actually been done using a carbonated beverage as source, or a school boy’s fave,

baking soda plus vinegar.

One container has ordinary atmospheric air, the other lots of CO 2. It heats up faster.

Is adding lots of CO2, unfair, because it’s way more than normal air? The point of the demo is to quickly show that CO 2 traps more infra- red. The actual rise in atmospheric CO 2 is very slow by human standards, which relates everything to how long we live. By the standards of the Earth sciences, the rise is very rapid. They only started drilling ice cores to test air bubbles less than a hundred years ago, which is yesterday. The mass burning of fossil fuels started the day before yesterday.

Venus is the extreme example: Although further from the Sun than Mercury, it is hotter, about 800 degrees on the surface,

Its atmosphere is over 90 % CO 2, All infra- red is retained.

Why this demo is not a common public sight is odd.

Galileo was already sure that heavier cannon balls wouldn’t fall faster. If you put them both in a box, does the lighter one slow down the heavy one, or does the whole box now fall faster, because it’s heavier? He was demonstrating it.

Thanks Nick. I wrote a detailed reply earlier and didn’t post it because I’m always dealing with the climate deniers on here and any kind of detailed explanation of the situation we’re in gets pretty depressing. I’d love to hear a single one of these guys explain to me what precisely is wrong with the greenhouse model as well as with the multiple independent lines of evidence supporting anthropogenic climate change. That would probably be outside the scope of this blog though.

I agree it is odd that none of this is really taught in school, and with everyone who I’ve had ask me about it, I’ve had to start by explaining really basic elements like wavelengths. I’m not even a professional here.

For anyone who wants the details as told by a bunch of actual actuaries in this field, see the recent IFoA “Planetary Solvency” report. There’s also some economic modelling that’s been done on this; the most relevant one I’ve seen so far is the MEDEAS framework from 2020. The TLDR is basically that we need to get our s**t together like right now.

No, it’s not. Inflation can happen without out-of-control debt.

But it can cause inflation to spiral out of control which is bad for more the the 50 states. Much of the US influence in the world is economic; damage to the currency in that way risks (accelerates?) its decline as the world power.

Yes, central bank balance sheet expansion= inflation. These over lords are quite a cult.

Gazillion:

I am confused. The Feds balance sheet expanded rapidly from 2009 to 2020 while price inflation was extremely low. Asset inflation and Fed Balance sheet growth correlate but not price inflation. Right?

Michael,

It is a fair question to ask about correlation/timing between the various modes of Fed money printing and the various modes of inflation (asset vs real good).

There definitely did appear to be a multi-year lags between Fed interventions (manipulations of interest rates) and real good inflation (asset inflation seemed to happen pretty damn quick).

But money printing/interest rate manipulation is almost by definition playing-with-fire, since fundamentally altering the ratio between societal money supply and societal real asset supply is about as fundamental a manipulation of the macro-economy as is possible.

Credit expansion can show up as either asset-price inflation or consumer price inflation, depending on who is receiving the “fresh” money.

When the fresh money is going to the working class, with a high propensity to spend every penny they earn, that fuels consumer price inflation. See 2020-2022.

“The Feds balance sheet expanded rapidly from 2009 to 2020 while price inflation was extremely low.”

I’m guessing you weren’t watching real estate prices.

Home prices are not part of consumer price inflation. Consumer price inflation tracks consumables. Real estate is an asset, not a consumable, and is tracked by various asset-price inflation measures. There is also producer price inflation (PPI), wage inflation, grade inflation…

Tariffs will have impact. Trump will slowly work tariffs up to 20-22 pc level from current 17 pc level (and less than 2.5 before he took office). I see millionaires tax in senate bill plus some doge cuts, and may be intelligent use of sec 899 to target foreign ownership firms, combined with some ira to roth flat tax tricks.

Tariffs will net 2tn to 2.5tn over 10 yrs =200bn annual. They will add more tax ginmicks for 0.5-0.8tn 10 year (discussed above)

They will thus reduce 300bn annual deficit.

Some forced fed cuts plus shorterm borrowing for govt will save interest by yield curve control

Trump’s plan is a good one, if judges let him do it. The VAT tax is an alternative.

“fed cuts”? have you not read what’s actually in that “big beautiful bill”? He is increasing spending, not cutting. CONgress is fully owned, and not be the taxpayer.

Democrats; “you got us, we printed trillions”

Republicans; “hold our beers…”

Seems people do get the government they deserve after all. LMFAO!

And there won’t be any increase in domestic prices because the exporters will eat the tariffs.

Not all, but part of it. Another big part of the tariffs will be eaten by the importers. Walmart, Costco, Macy’s all the big ones said that they’re working with their overseas suppliers to eat some of those tariffs, and they’re shuffling supply chains around to more US production, and they themselves will eat some of the tariffs (lower profit margins, or they stopped giving guidance), that’s what they all said, and some said that price increases to consumers will be the “last option” (Target and others), that they will try to “avoid” price increases (Macy’s) because they’re already facing sales declines, and that they may “surgically” raise some prices but “cut prices where we can” (Costco). You just have to listen to them carefully — instead of just reading stupid-ass headlines. None of them can just pass price increases to consumers because their sales would collapse, DUH.

Regarding the debt and fiscal responsibility; “meet the new boss, same as the old boss”.

My wife an I got married in 1981. We were both 26. In 1983 my wife and I I bought a small sailboat. At the time we were living rent free in her parents home as they sailed their boat around the world. Interest rate on the loan was 17%. In 1984 they returned from their journey and we needed to move. So we bought a small house in an acre with a pond. 76k, 10% down, interest rate was 16%+ .5PMI. I was a lawyer, my wife was a teacher. I think our combined income was about 40k. As interest rates came down I think we refinanced that house 3-4 times and refinanced the boat once. In 1989 we sold the boat for the same amount we paid for it and bought a bigger boat. Or combined income in 1989 was 70k. We lived in our house for 25 years until we sold it in 2009. By the time we sold it the ‘value’ which peaked in mid 2006,’ had fallen by 40%. We bought a bigger boat and in 2011 atvtgecagevof 56 set out on our own adventure to sail around the world. We never did make it all the way around, as my wife developed Parkinson’s. But we are still living on the boat, just not crossing oceans anymore.

As I watch my millenial children come to the realization that the same opportunities that I had have been stolen from them by the FED, an out of control govt, and a cabal of elites who would happily kill their own mother to make a buck, I feel bad for all the young people today who face an uncertain and likely bleak future.

My advice (I’m 70 now so I guess I feel I’m old enough to say what I want) is this: “If you’re not a contrarian, you’re bound to be a victim”.

Could not agree with you more sir. I will turn 70 on my next birthday, so you and I are close in age. Have a similar life story….and were it not for the fact that my son will inherit our paid-off home…..not sure how he would come up with the 20% down on a average home now going for half a million. The Fed taking interest rates down to nearly zero percent…..and causing home values to sky-rocket…..will plague our country for years to come. Likewise, our government borrowing like there is no tomorrow…will haunt America in horrid ways that we can only begin to speculate on. Pushing tax cuts for the wealthy is truly irresponsible….but, the overall attitude of everyone deserves a free lunch will someday be replaced by how could we have been so stupid.

“I feel bad for all the young people today who face an uncertain and likely bleak future.”

Almost certainly true.

But, the thing is, plenty of conservatives were screaming about this dystopian future as early as the 1970’s/early 80’s.

But unless Americans are being consumed by fire at *that very instant* they are easily lied to that fire can’t exist.

The multi-decade news media oligopoly (1945-1995) made lying to the people easier for the “elites” – had the internet arrived even 10 years earlier, the country might have been saved (since transparent lies would have been punctured by disparate view points).

Eric:

I second your “contrarian ” advice, but investing in the USA is one’s best option if you have enough income and savings to truly be an “investor.” I am fearful when the market is giddy and greedy when the markets are in shambles – but you need enough wealth to be able to “stay the course.” Most people do not have enough money to stay invested long-term and many chase idiotic investment choices pushed by brokers and financial consultants.

You have plenty of assets to help your children now. Too many people wait to die before they use their money

Thank you for the clear explanation, Wolf. So for retirees who rely on SS and treasury ladders, what do you all think about TIPS as reliable protection against possible oncoming inflation if the govt doesn’t trim the annual national deficit? Or is now the time to lock in these 4+% longer-term treasuries (5-10 yr)?

Ladder your bond purchases on the short end. Interest paid on TIPS have consistently been well below real inflation rates and in many cases even nominal inflation. It’s a bit of work on your part, but heck, for a while there T-bills 4-8 week were over 5%. TIPS are a joke IMO.

What is real and nominal inflation? Real and nominal GDP growth or income growth, for example, are measured in reference to inflation. What is inflation measured against to have real and nominal components?

Well inflation could spike

I doubt Powell could fix it this time without being Volckeresque

and he will be attacked constantly in the press, until his replacement comes, who prob will be less qualified.

Scary times

Howdy Reader Learn about the old time squirrels. CASH as KING and retirees don t care what inflation or Govern ment is doing to the peasants…..

It is interesting, but there is a faction of (albeit) conservative investors who seem to really obsess about squeezing the last possible marginal basis point out of their investments – yet who at least seem to spend nowhere near as much time thinking about techniques that trim expenses (which tend to be *much* more within the discretionary, safe control of savers).

I’m not saying this is you, ReaderinCA, but I do wonder if you have thought as much about the inescapable costs of the CA lifestyle, as you have about the incremental basis point earnings of various Treasuries’ techniques.

I truly do applaud the safety first/Treasury mindset – but its advantages can be monumentally undermined by the very fact of living in certain places.

Perhaps CA = Central Alabama. Bless your heart.

Wolf, this isn’t directly on topic, but a question I’ve wanted to ask for a while:

You’ve written a lot about how tariffs are part of a reversal of the decades-long trend of increased globalization and trade flows. But one other trend that has happened simultaneously over the last few decades has been reduced barriers to capital flows, at least in the US and Europe (China is not included).

I remember when I was starting my career, you could buy JGB futures or German Bund futures, or maybe CME currency futures, but for a retail investor, the transaction costs were prohibitively high. Now, anyone with a retail account can trade anything they want (bonds, equities, funds) in USD, GBP, EUR, JPY with minimal costs. The first reversal of this trend that I’ve seen might be contained in the proposed tax on foreign holders of US securities, but I’m having trouble wrapping my head around the implications. Do you see a possibility of the trend of free capital flow breaking down along with globalized trade? And, if so, what would be the consequences? Lower US asset prices in general? Increased cost of US govt debt funding? Something else entirely?

As things likely get worse, capital flow restrictions will very likely follow trade restrictions – regardless of what the now-discredited Church of the WTO thinks.

(Observation – Britain – ultimate free trade champion from 1850 to say, 1925, really didn’t blink – *couldn’t* blink – at imposing devaluation/capital controls by 1950. Their economic position had degraded that far, that fast. See America – Today).

It is hard to see what all the blow-back will be and when it will occur.

But the fundamental fact is *this* –

Within about 30 years, the Chinese have created an industrial, real-asset based economy that is more and more putting the US (and everybody else) to complete shame.

*That* is the base reality to which the “financial economy” is just an overlay, one that must ultimately adhere to the real/base reality.

All the financial manipulations/distortions in the world will not alter the relative productive capacities of various nations at this late date – perhaps in 2005 or 2010 – but things are now much further gone).

That said, the declining nations’ “leadership” will try all sorts of desperate financial impostures to obscure the fundamental, painful necessity of real asset economy reform.

After all – that is *exactly* what they have been doing for the last 30 years.

Glad to see the tax receipts are going up, because risk is being repriced across the board and interest rates are going up.

Aren’t tariffs a tax on American businesses? As such, won’t they increase the Cost of Goods sold and therefore decrease profits? Lower profits will result in lower income taxes, so while tariffs increase government revenue, lower profits will decrease income tax and lower government revenue.

No, because many of these companies already pay few or no income taxes in the US, such as big pharma, Apple, etc. So tariffs may be the ONLY taxes on income that they pay in the US. You should have listened to Trump explain this. He singled out Apple and big pharma with their tax entities in Ireland.

“So tariffs may be the ONLY taxes on income that they pay in the US.”

Actually, this is an excellent point.

(Of course, alternatively, Trump could also just exterminate the off-shore tax dodge in the first place…)

But the very fact that almost everybody missed it really highlights (again) the counter-productiveness of Trump’s fire-hose approach to…everything.

I read where Bessent is expected to continue Yellen’s focus on short-term Treasury issuance. And with the coming change to the Supplementary Leverage Ratio, one really has to wonder how much or if the long end of the yield curve is going to drop as much as the Fed expects.

It all seems like a big shell game, moving borrowing around to try to stave off the looming growth in yields. This is going to be a very interesting final Trump term. Lots of things pushing & pulling around what the Fed can do to minimize inflation & interest expense.

“It All Seems Like a Big Shell Game – History of US Economy from 1965 to Imminent Death”

‘Debt and deficits don’t matter…until they do.’ — Richard Cheney

The Dick’s of the world always make the obvious statements that can never be empirically tested.

There are not enough “rich people” to get the taxes you need. If it were possible, it would have been done here already. It has been tried many times before in other countries and does nos work out well.

I can do many things to prevent you from taking it from me. That is the problem. Then you may see less tax revenue than you saw before you began your lame-brained scheme.

tax the rich. tax their wealth/assets. problem solved

LOL! The problem seems to be with the definition of “rich”. More generally, in order to pay anything, the company/person must be liquid or solvent (i.e. has cash or assets that can easily be sold). If you give a tax bill to a person/company that is more than their cash reserves, they will fire sale assets. Precisely why I am contemplating selling some older, paid-off rental properties. Property valuations at 20x the average income is pure greed on behalf of the county. F-em.

That’s what the original income tax was proposed to be in 1913 or whatever. Look how that turned out.

The problem is that “the rich” don’t have the money to pay for the ever increasing social spending and IRA climate boondoggle spending. Either you have broad based middle income income or VAT taxes, or you cut entitlement spending drastically. I know which I prefer.

Happy1,

Choosing not to believe in climate change doesn’t make it not exist. The evidence is clear that humans are causing the problem.

We will ultimately pay for it one way or another, whether through devastating droughts, severe storms, spiking insurance prices in hurricane and fire prone areas or through paying to mitigate some of its harms.

https://ourworldindata.org/cheap-renewables-growth

This article explains why the IRA was a good investment. Solar photovoltaic and onshore wind are the cheapest sources of electricity as measured by levelized cost of electricity for new builds. The costs associated with building new wind and solar power plants has fallen exponentially over the past decades at a rate that corresponds to the total amount of solar PV and wind power installed as the industries become more efficient due to learning curves.

There is a lower bound to fossil fueled power beyond which producers will not expand production because it’s not profitable. This puts a floor under the levelized cost of electricity of fossil fueled power.

Renewables do not have this problem because the fuel cost is free, their costs are determined by the cost of the technology and installation costs. As more renewable power is installed, the technology becomes more efficient and the industries themselves become more efficient due to learning curves. This is why spending money to expand renewable energy was a good investment.

This is also why both Texas and California are all in on wind and solar, despite vastly different politics.

It’s foolish to not develop our renewable resources and the associated manufacturing supply chains here in the US due to a political preference to assist the fossil fuel industries.

Ultimately, consumers will pay more over time as we depend more on fossil fuels for energy generation while simultaneously expanding our energy use to bring new industries home, for AI, crypto, etc. All of this is happening along with exporting massive volumes of oil products and natural gas while the Trump administration simultaneously cuts efficiency standards that help keep costs down and allow more efficient use of our resources.

It was a far better use of a few hundred billion dollars to assist renewable industries than squandering it on tax cuts that largely benefit wealthy individuals. The IRA was a good policy beyond its climate and environmental benefits and the majority of the jobs in manufacturing and installation largely benefitted red states. Republicans in House largely shot their constituents in the foot with that one.

I would love for Wolf to do an article on levelized cost of electricity or energy by source. I think it’s a fascinating topic and he does a good job of presenting data in a way that is easy to understand.

I didn’t say I don’t believe in climate change. Don’t put false words in my mouth.

I did say that the IRA doesn’t move the needle even 0.1 degree C on climate change. This is the estimate provided by multiple objective outside observers and is pretty much indisputable.

So you are arguing that spending a Trillion dollars we don’t have and borrowing from our grandchildren to pay for it, to make no difference in the climate makes sense somehow. That isn’t science, it’s pseudo religion. I respectfully disagree.

The IRA is virtue signaling and pork for favored businesses and it should be completely repealed.

And if solar and wind and other renewables are the cheapest energy, then they will take over based on cost alone, because that’s how markets work.

So why do we borrow a Trillion from our grandchildren to help something that according to you, doesn’t need our help because it is already less expensive? Either it is more expensive and needs subsidy to compete, or it is cheaper and needs no subsidy. It can’t be both.

Happy1,

I’m replying here because it won’t let me reply directly to your comment for some reason.

Since the price of power from renewables drops exponentially as more are installed, spending money to accelerate this process and help develop these industries ultimately leads to cheaper electric power in addition to supporting American manufacturing. It’s an investment with an obvious return that benefits not just the renewable power industries but also the electric power sector and consumers.

The free market does not price in the costs of pollution and climate change into the cost of generating power. Any attempts to account for this by taxing carbon emissions or other types of pollution is essentially a no-go as long as Republicans have control of Congress, so subsidizing renewable power is the only solution that had any chance to make a difference.

I would far prefer a tax on carbon emissions as well as air and water pollution be applied in general to the energy sector so that the costs of remediation are not forced onto states or private property owners.

Additionally, Trump is opposed to allowing the free market to favor renewables. This is why he cancelled offshore wind leases even for projects already in progress, while enacting policies that favor fossil fuels like declaring his phony “energy emergency” to help fossil fuel producers get around environmental regulations on federal lands.

The big beautiful bill also calls for lower lease rates for oil and gas drilling on public lands, which is a subsidy to the fossil fuel industries that is also paid for by money borrowed from the deficit.

https://www.eia.gov/todayinenergy/detail.php?id=65064

Ultimately, we all will pay for climate change one way or another. China installed 277GW of solar power last year, the US had 121 GW of solar power installed in total. If they can do it there is no reason we can’t do it except for political choices that favor the fossil fuel industries while spreading denial about the true costs and dangers of not addressing climate change and pollution.

The IRA was imperfect, but it was the best that could be done in the current political climate.

Happy1. We don’t need to tax the 1% at 90% rates, just go back to how they were taxed in the 1950’s. The USA did pretty well with taxing them at the Eisenhower(R) rates.

Bagdad Barbie (Karoline Leavitt) says Trump’s Big Beautiful Bill will not add to the deficit. But Politifact and the CBO disagree:

” using preliminary information from the Congressional Budget Office and Joint Committee on Taxation, multiple outside groups’ analyses project that the bill would INCREASE deficits by $3 trillion to $4 trillion over the next decade.”

When they say “increase deficits”, I believe they mean add to the existing Federal deficits plus another $3 to $4 Trillion over 10 years. And the bill includes cuts to SNAP, Medicade, Housing subsidies, Earned Income Tax Credit (EITC) and the Child Tax Credit (CTC).

For sure the house bill will increase deficits, I don’t support it.

I would support some small increases in taxes in exchange for dramatic, fundamental changes and cuts in entitlement and defense spending. Which neither party will do. But at least one party isn’t suggesting massive entitlement expansion and student loan forgiveness, which would make the problem exponentially worse.

And regarding Eisenhower era tax rates, the top rates were near 90% in that era, but at the time, all of Europe and Asia were smoking ruins, and the rest of the world was living in the stone age, so we had no economic competition. If we taxed at similar rates now, business would leave for other locations.

In the 50s, we had social security, but no Medicaid or Medicare, no SNAP, no welfare, no IRA, this is more than half our current budget. So if we are returning to Eisenhower tax rates, I would take that bargain if we can also return to Eisenhower era Federal spending.

Happy1. If you don’t like the Republican tax rates (Eisenhower). Why not go back to the Democratic (Bill Clinton) rates ?

FYI. The Federal government got into “Welfare” in a big way back in 1935. To great Republican fanfare, Bill Clinton ended the tradition “Welfare Program” here in the USA back in 1996.

The dreaded AI search (which has gotten me into trouble with Wolfe before) says: “Under the Clinton administration, the maximum individual income tax rate was 39.6%, while the top corporate tax rate was 35%.”

Clinton (D) was able to balance the budget for the first time since 1969. Wikipedia : ” Besides the record-high surpluses and the record-low poverty rates, the economy could boast the longest economic expansion in history; the lowest unemployment since the early 1970’s…”

On the downside, there were few Billionaires, and no one was building $500 million yachts. But I can live with that.

I hate to break it to you but the top tax rate in the Eisenhower (R) years WAS 90 percent!!! It didn’t drop to 70% until JFK’s tax cuts of 1962… which (as the Laffer Curve predicts) produced LARGER tax receipts. In fact federal tax receipts went up by 5% a year for the first three years following JFK’s tax rate cuts.

All of which might have been an acceptable approach to funding the government except that Medicare came into being in the mid-60s and it has been GROSSLY underfunded by the withholding taxes right from the jump. Couple that with the wasted billions spent fighting the Vietnam War and we ended up with the situation in the late 70s and early 80s that Wolf described above… “10-year Treasury yield was over 10% for six years in a row and mortgage rates were over 10% for 12 years in a row”.

In short, 80% of the problem is on the spending side of the federal budget…and 20% on the taxation side. And it has been this way ever since the end of the Cold War. As you yourself point out, income tax rates have been remarkably steady since 1990 (35 to 39.4%)… but (as Wolf’s second chart shows) the debt funding issues since 1990 have only been a problem following some type of spending blowout (Iraq War, Housing Financial Crisis, COVID, Inflation Reduction Act).

In short, Congress can tinker around with the tax code a bit but the real solution to the Federal Deficit is to be found on the spending side of the equation.

Pretty sure if we repealed every tax law enacted in the past 50 years, after the recession we’d be back to having balanced budgets. It’s a choice we make to pay this much in interest.

PI (Personal Income) came in at .8% and the the expected number was .3%. Take a look at the FRED graph on PI. $20 trillion in 2020. $24 trillion now. 20% growth in 5 years. No wonder the drunken sailors are spending. Their personal income is going up. The chart looks exponential. LOL

In 2010 it was 12 trillion.

Personal income is the income that persons receive in return for their provision of labor, land, and capital used in current production and the net current transfer payments that they receive from business and from government.

Your dream of a new tax regime reminds me of young Mr. Tobin’s design of financial taxes. Unfortunately, Mr. Tobin was quickly reassigned to a backwater southeast Asian brokerage, never to be heard from again!

Are you talking about James and the Tobin tax, which was an idea to reduce foreign currency speciulation? His tax never caught on but he worked at Yale for almost his whole career and earned several awards.

In macroeconomics there is no such thing as ‘taxing the rich’. That expression is simply a marketing tool used to justify transfers of capital wealth from the private to the public sector.

Better just to have more nationally owned interests, such as places like Finland. We privatize the wealth of the country to put the benefits in the hands of the few, and of course no consideration of those who rightfully own those resources to start with.

Better? Or worse? To have more nationally owned interests such as places like Russia, China or India?

Has the privatization of wealth in this nation by companies like XOM benefited fewer people than the nationalized equivalents such as Pemex or PDVSA?

Broadly speaking aren’t there are two kinds of people in this country; those who give more to the public sector than they take, and those who take more from the private sector than they contribute?

Best wishes to all, OBC

So I put Finland to avoid the reactionary judgments of the countries you decided to substitute. Oh well.

Two types? Why must we always be binary? C’mon, it’s a spectrum

On paper the situation looks very sustainable. It could have been argued the USA was going to go bust in the 90’s with interest payments approaching 50% of the budget (the yearly budget was only about $1TT)

4% interest is very reasonable, but if we get a repeat of the 1970’s with 15% rates that would put a fork in the whole thing.

Yea same – looks sustainable. Date I’d say 3.5% rate looks normal. Too low and you’re artificially stimulating the economy – that pendulum swings back. Too high is obvious nobody wants.

The receipts verses interest expense seems to suggest we’re collecting more net-after-receipts tax as expected of debt-stimulated growth.

Debt to GPD looks bad, sure – downright 40’s and we all remember how terrible the late 50’s and 60’s were economically, so cite those consequences if you’re looking to understand what cyclically takes places when debt pushes up GDP (side note, note when the debt to GDP chart cuts off, now go look at debt to GDP since the Great Depression).

Lastly, we all get so frightened about the debt expense, but rarely do we ever talk about the interest income receipts of US persons. I’m still not convinced all this debt isn’t bovine.

From 1970-1980 the deficit increased from 381 Billion to 909 Billion.

From 1980-1990 the deficit increased from 909 Billion to 3,206 Trillion.

Everyone needs to stop and take a deep breath because it’s been worse and it can be a lot worse!

Would it be possible for a transaction tax accross the board to solely fund the government? I can’t find any proposals for this on Google so there must be downsides and or I am not using relevant search terms.

Wolf mentioned that in one of his posts (as an alternative to a VAT tax) but I had never heard of it either. So I would be interested in finding out more as well.

I will say that I kind of grinned when I read his post because it sounded suspiciously like the Stamp Act that King George III tried to impose on America about 250 years ago!!!

I am not an expert in Irish corporate taxes or Pillar 2, but my understanding is that the scam that allowed “non resident” Irish companies to have “no where income” (IP income) and thus no corporate taxes has ended. Recently, the Irish corporate tax rules under Pillar 2 will likely require companies like Apple to pay 12.5 to 15% (subject to R&D special credits or deductions) corporate tax rates. So Ireland remains a tax haven to a lesser degree now than earlier years when many large US companies paid no corporate income taxes on IP income by their offshore Irish subsidiaries. It was a standard gimmick that the Big Four accounting firms sold with juicy accounting fees. jmo