As homebuilders got aggressive with mortgage-rate buydowns, incentives, and lower prices, sales held up, unlike sales of existing homes, which collapsed.

By Wolf Richter for WOLF STREET.

With inventories of new single-family homes for sale very high – more on those in a moment – the big homebuilders have been aggressive in their efforts to sell the homes they’ve completed, and those they’re building and planning to build, because they’re in the business of building houses, and they have to try to keep their stocks from collapsing, and they cannot just stop building just because inventories are high or because the housing market is tough.

So they’re lowering prices, they’re building at lower price points, they’re throwing lots of incentives at potential customers, and most importantly, they’re buying down mortgage rates, which is costly for builders but less costly than just cutting the contract price far enough to get the payment down to the same level.

Lennar, for example, disclosed in its 10-Q filing that the total cost of incentives, including mortgage rate buydowns, rose to $60,000 per house sold on average in Q1, up from $50,600 a year ago, to 12.9% of its average sales price. And those incentives are in addition to any actual price cuts.

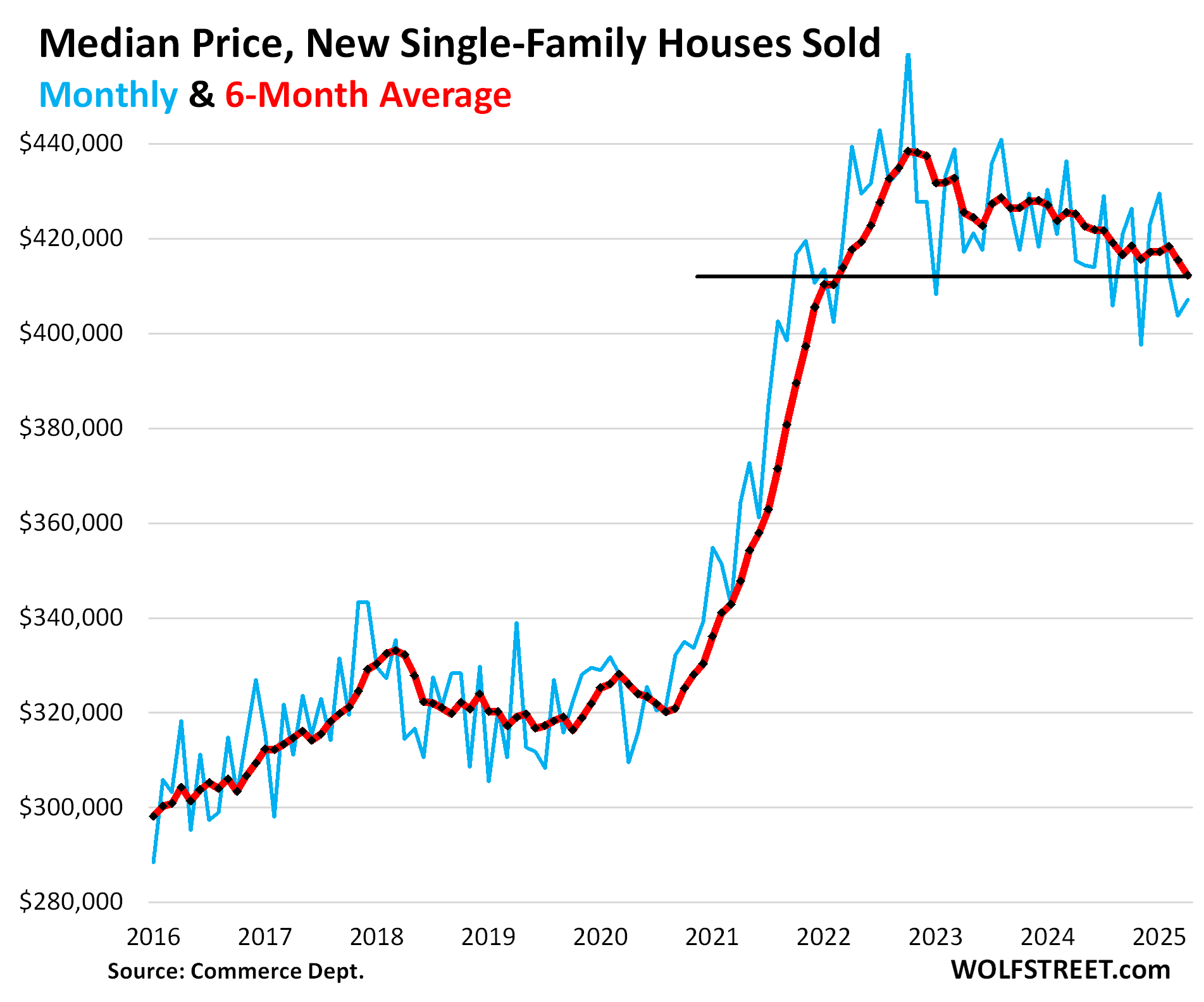

The sales prices in the contracts between the homebuilder and homebuyer do not include the costs of the mortgage rate buy-down and some other incentives, such as free upgrades. It is these contract prices that are tracked by the Census Bureau, and even though they don’t include the costs of mortgage-rate buydowns and some other incentives, they have been zig-zagging lower since late 2022.

In April, the median contract price, at $407,200, was down by 2.0% year-over-year and by 11.5% from the October 2022 peak, according to the Census Bureau today.

The six-month average, which irons out the month-to-month squiggles, declined to $412,300, the lowest since February 2022:

Inventories for sale are sky-high, especially in the South and West.

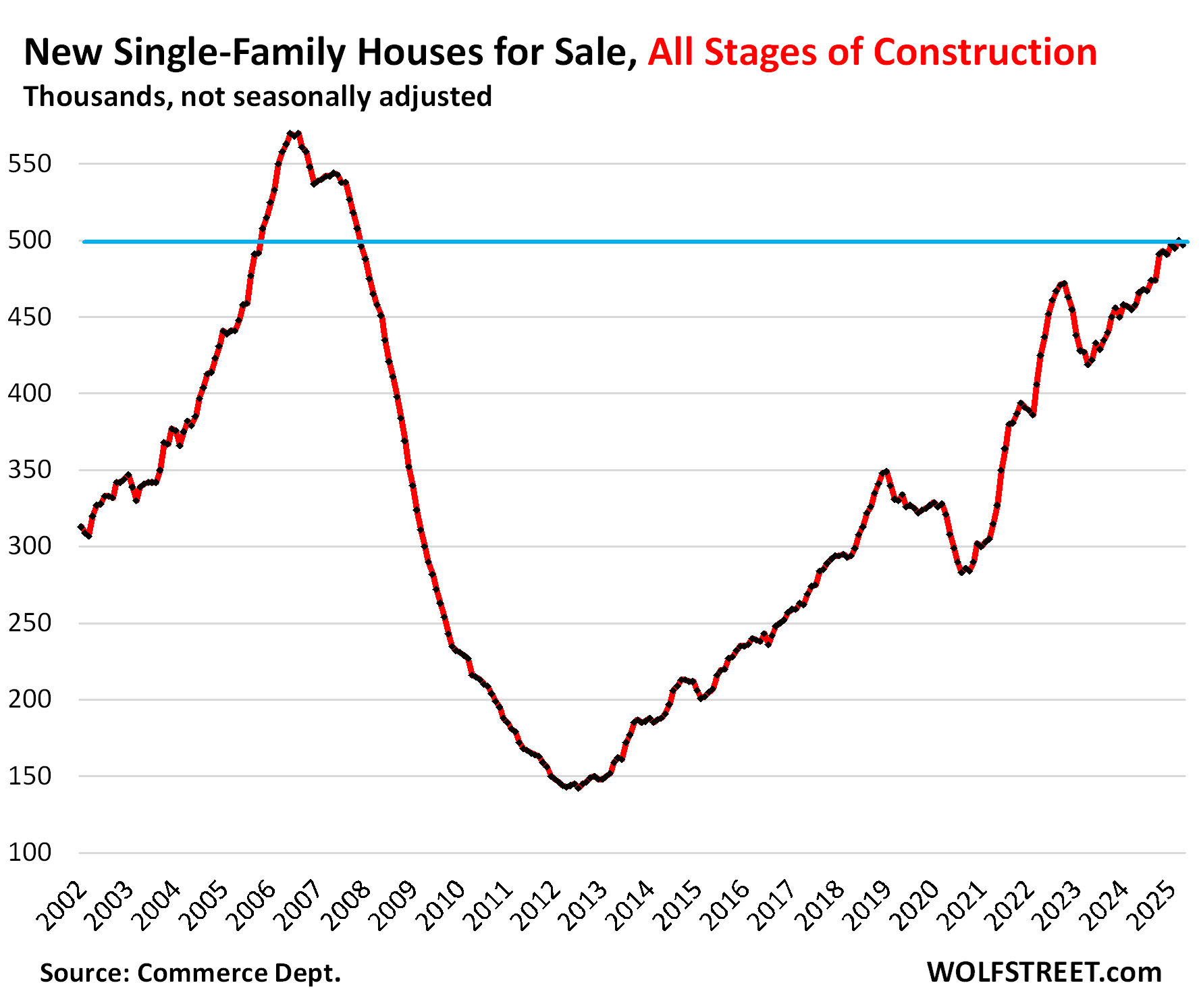

Single-family houses for sale at all stages of construction was revised up for March to 500,000 today, from the originally reported 493,000. In April, inventory was 497,000 houses, according to the Census Bureau today.

Inventories over the past four months, after revisions, have been right at 500,000, the highest since November 2007, when they were on the way down as the industry was near collapse during the Housing Bust, and up by 51% from March and April 2019.

Thanks to fairly brisk sales that homebuilders obtain with lower prices, mortgage-rate buydowns, and incentives, this inventory has translated into 8-9 months’ supply over the past six months – rather than double-digit supply.

A glut of new houses for sale is exactly what this overpriced housing market needs the most. And lower prices bring out more buyers. And we’re seeing that.

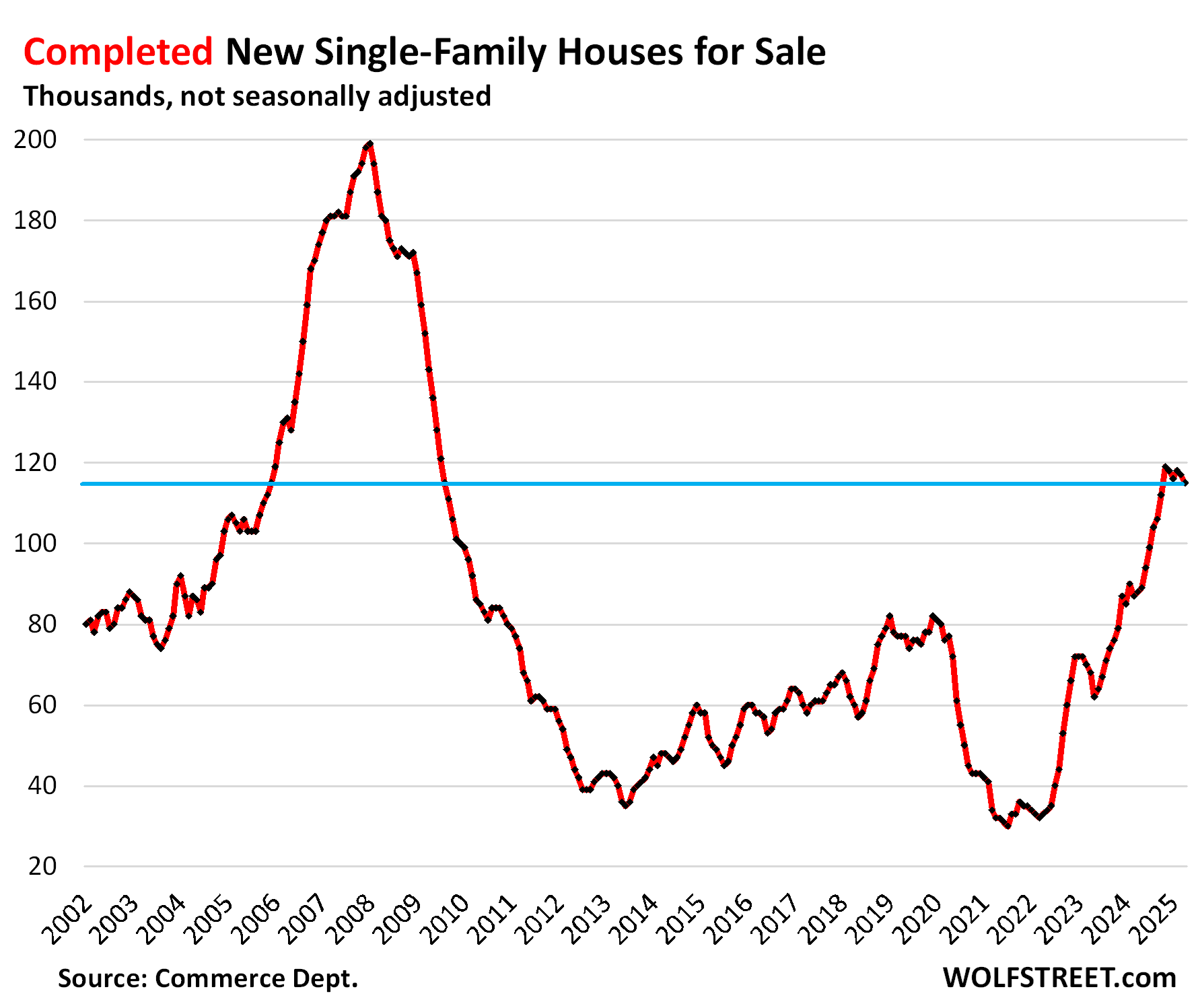

Inventories of completed single-family houses for sale in April, at 115,000, were up by 31% year-over-year, by 49% from April 2019, and about where they’d been on the eve of the Housing Bust in January 2006.

Homebuilders are very motivated to sell these spec houses quickly because they tie up a lot of capital.

Inventory for sale by region.

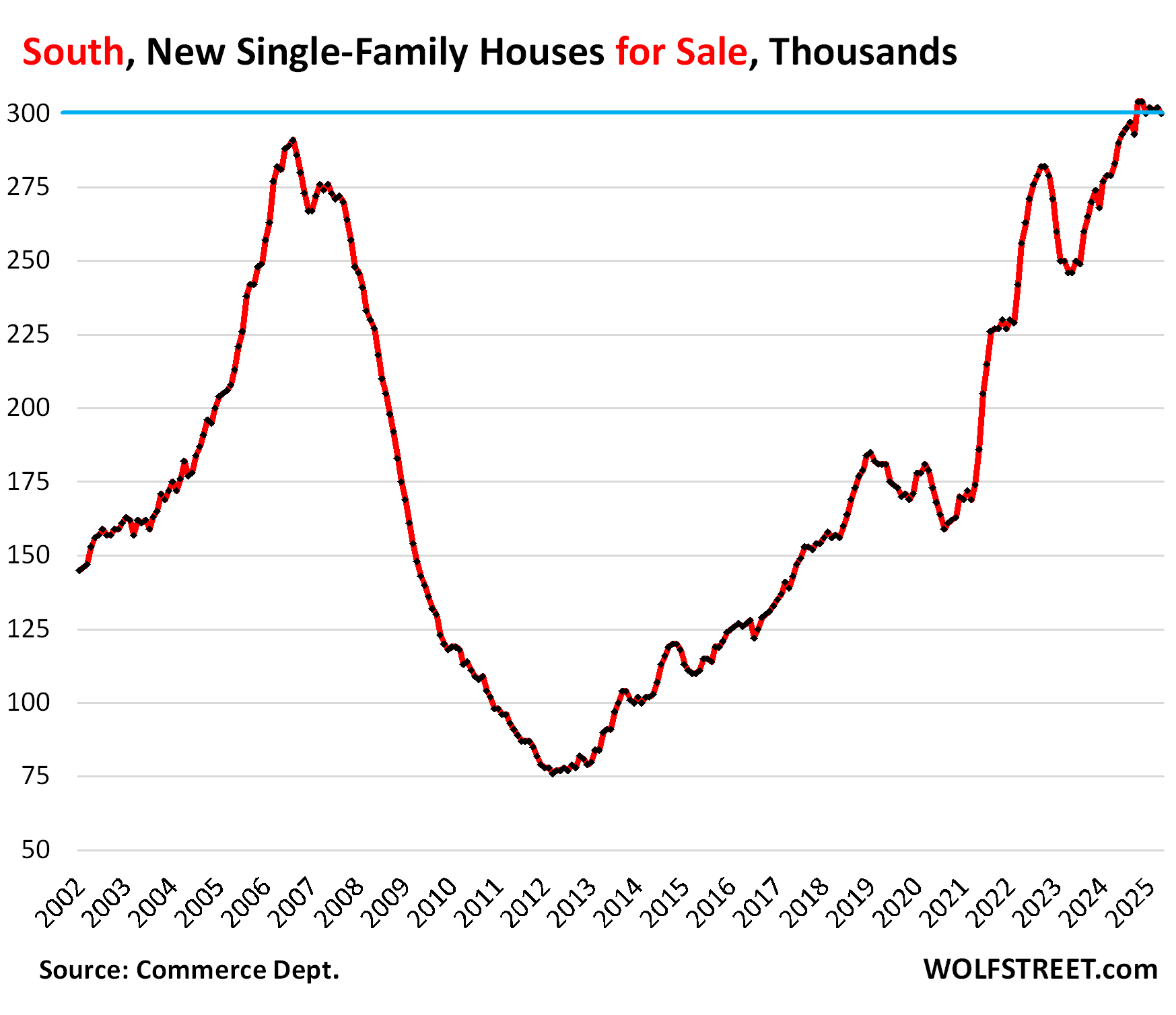

In the South, inventories of new houses for sale at all stages of construction in March was revised up to 302,000 (from the originally reported 295,000). And in April, reported today, there were 300,000 new single-family homes for sale, up by 6% from a year ago, and up by 66% from April 2019!

Inventory for sale has been above the Housing Bust peak since May 2024.

The South, dominated by Texas and Florida, is by far the largest market for new houses in the US, accounting for 60% of US inventory, and for 63% of US sales (a map of the four Census regions is in the comments below the article).

Sales rose by 5% year-over-year and by 5% from April 2019, pushed forward by mortgage-rate buydowns and incentives. At least, they didn’t plunge by 25%, as sales of existing homes have done in the US. This translates into 7 months’ supply.

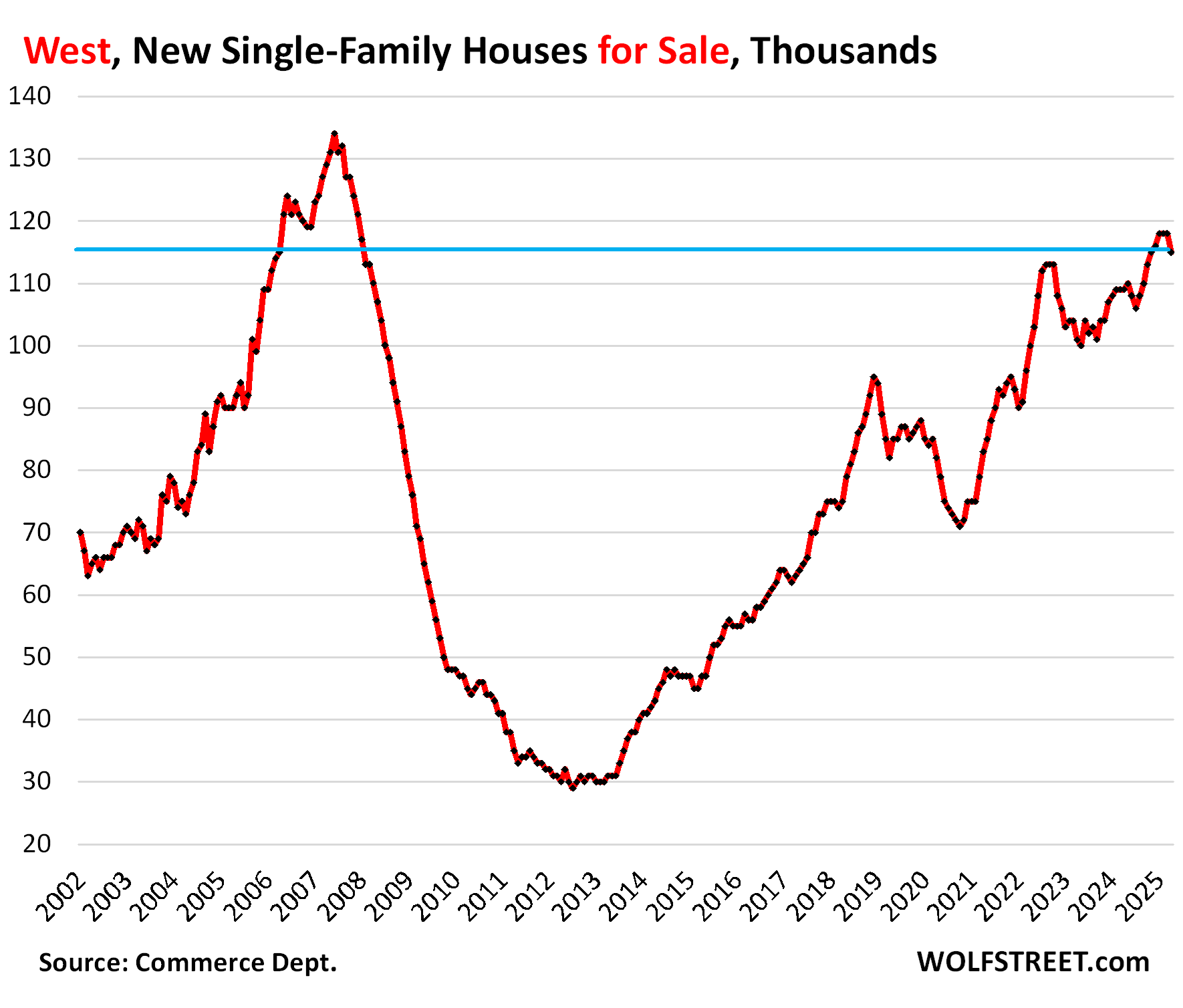

In the West, inventories of new houses, at 115,000, were up by 6% year-over-year, by 40% from April 2019, and where they’d been in March 2006. This represented about 8.2 months’ supply.

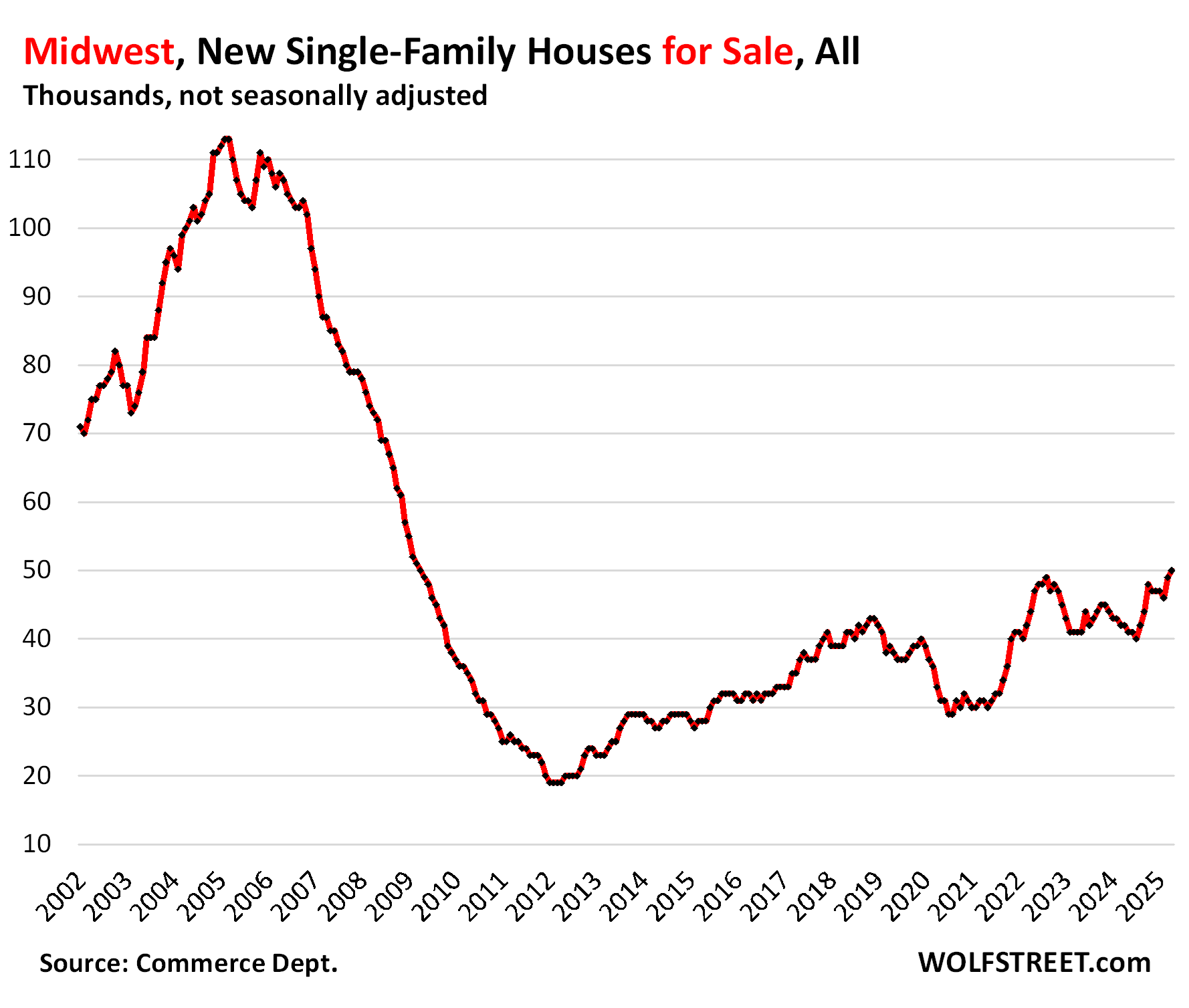

In the Midwest, inventory at 50,000 new houses for sale, was the highest since April 2009, up by 19% year-over-year and up by 28% from April 2019.

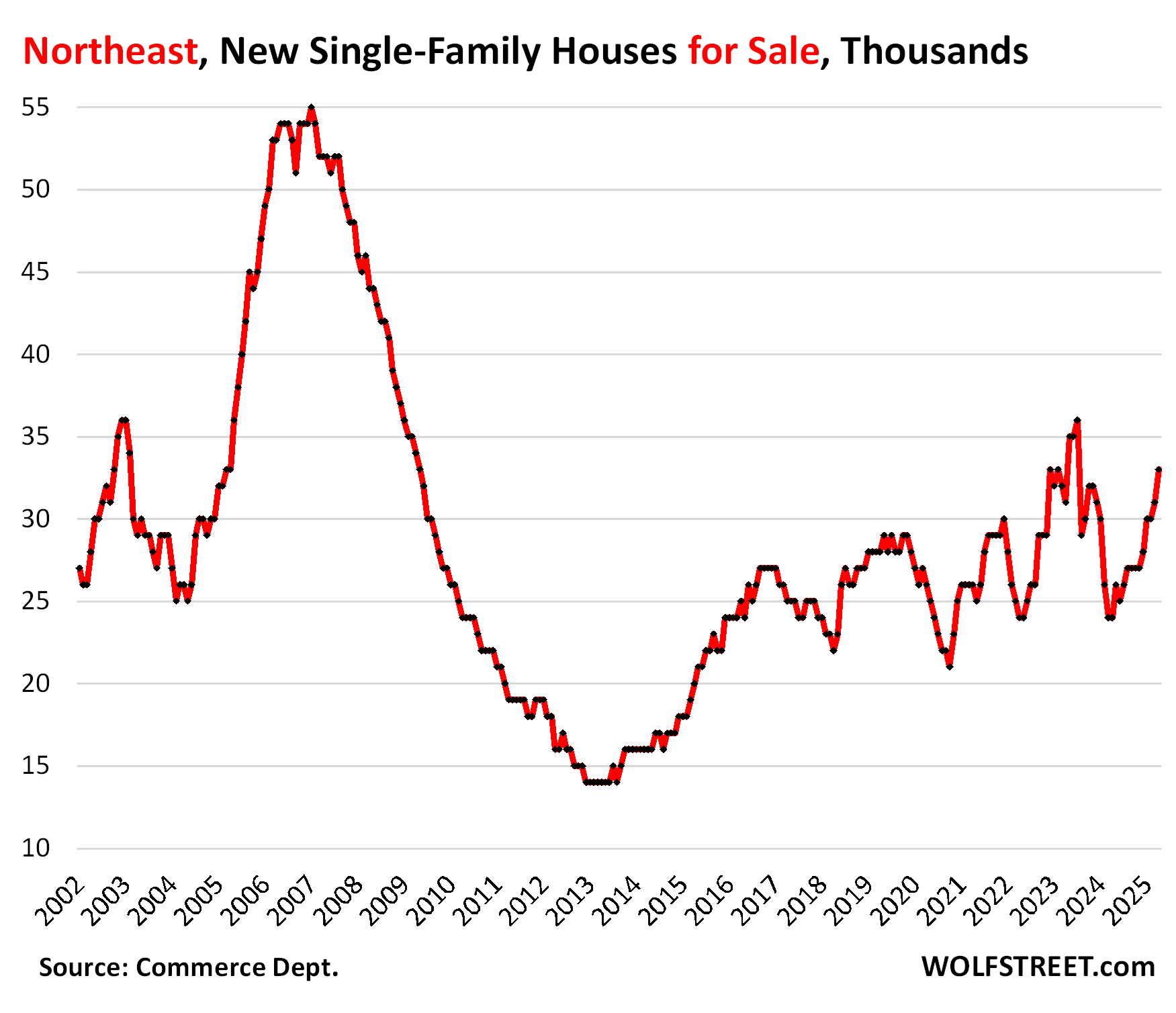

In the Northeast, inventory for sale, at 33,000 homes, was up by 37% year-over-year and by 18% from April 2019.

Sales in the US overall are decent.

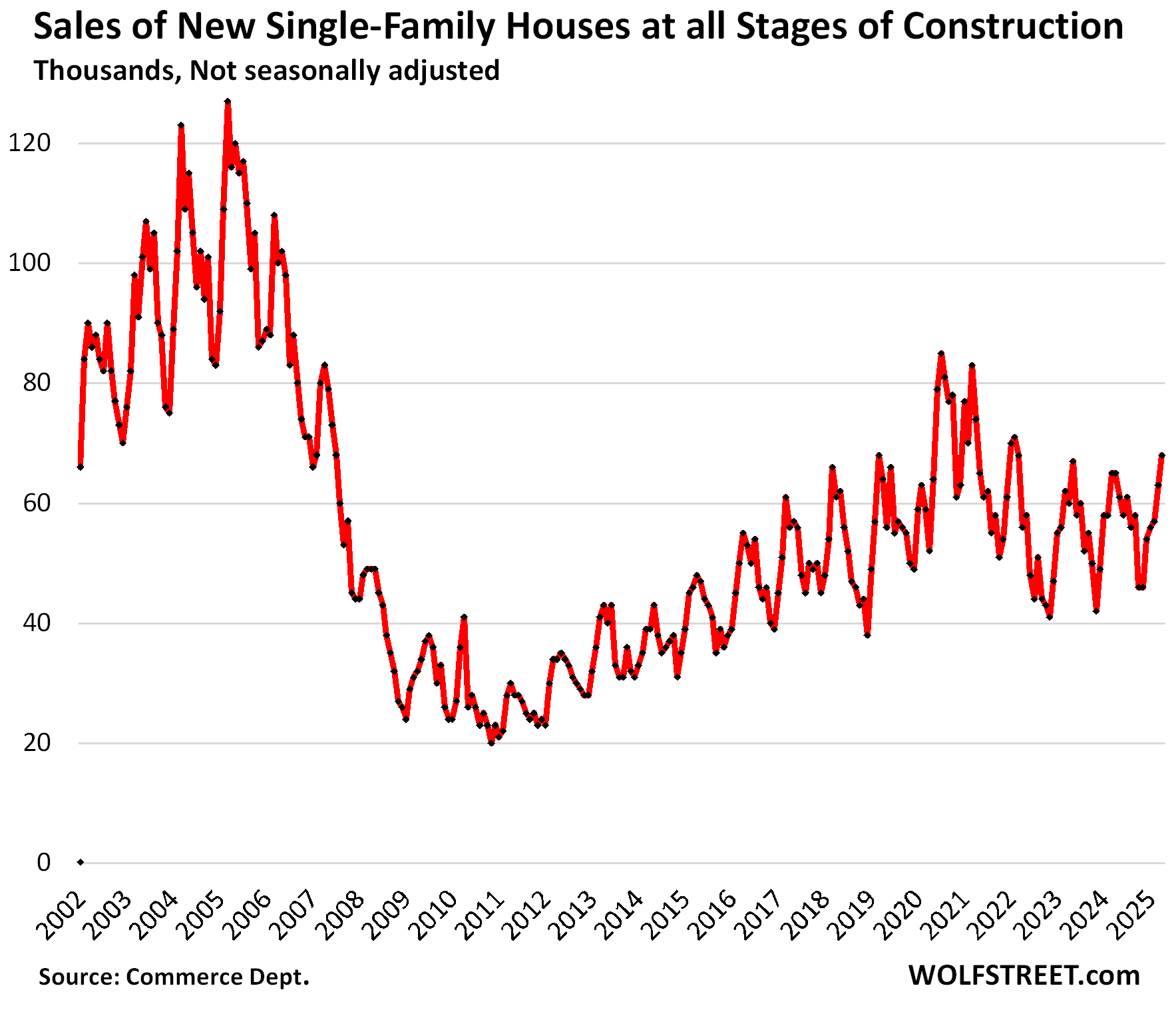

Sales of new houses at all stages of construction for March was revised down to 63,000 signed contracts today, from the originally reported 69,000. In April, as reported today, 68,000 new houses were sold. Despite the down-revision for March, these are decent levels of sales.

April was up by 4.6% from a year ago and by 31% from April 2019. But we don’t get too excited about a strong figure in a first estimate as there is a good chance that it will be revised back into line, as March was.

At these sales, supply rose to 7.3 months in April, from 7.0 months in April 2024, and from 5.2 months in April 2019.

The homebuilders…

Homebuilders have grappled with this market by deploying a mix of lower prices, incentives, and mortgage-rate buydowns, and sales have held up, compared to sales of existing homes that have been at collapsed levels for over two years and just booked the worst April since 2009.

In this environment, stocks of the publicly traded homebuilders have zigzagged down from their highs in September, for example: DR Horton [DHI] -40%, Lennar [LEN] -44%, KB Home [KBH] -41%, and PulteGroup [PHM] -34%.

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

The promised map of the four Census regions of the US:

Live in Town of Paradise Valley, AZ in Maricopa County which is one of the fastest growing counties in the country. Maricopa County added 57,000 new residents in 2024 and 38,310 new housing units. That seems like a lot of housing coming online even with the growth overall. City of Phoenix added 16,933 of the new housing units with population of 1.67MM. Prices of houses in close in desirable neighborhoods are still too high. Cromfort Report for May reports active listings for the metro are up 53% y/y but pending and under contract are down about 3% y/y.

How do they provide water for all of these new homes???

From the Salt River, the Colorado River, maybe some aquifers, etc. Although groundwater is no longer allowed to be considered in the 100-year water plan for new construction, which was a very responsible move on the governor’s part.

I personally will not purchase a home produced from 2020 to current time, Absolute thrown together junk, I dont care what kind of con job “incentives” they threw at Me..

I would prefer existing homes especially from the 40s and 50s built with pride and quality materials.

Have a fantastic Memorial Day Weekend.

I haven’t looked at any of the new builds in detail but my one observation is simply the move to smaller and smaller lot sizes. Convenient for high fiving your neighbor or them passing TP is your run out. Probably can share wifi too so all kinds of advantages. On the positive almost all of them have nice parks close by.

The whole conversation on housing is about how unaffordable and too expensive housing has become, and all you do is bitch about homes that are built to address this issue, that are built on smaller lots and with modern lower-cost construction materials and methods, and you bitch about these houses that are built to address this affordability issue. And those houses are selling because there is demand for them. I just don’t get why you’re denigrating this market and the people that buy those houses.

Honestly wasnt “bitching” just making the point about lot sizes. Where the housing market right now is irrelevant to me as my house is paid for, have no plans to move for several years so I just see it for what it is. I get the market is going to do what the market is going to do and since I can’t influence it I just accept it for what it is. Plus the design of these houses often includes neighborhoodsparks which was something unusual whore I grew up.

I live in a development built in 2012. The ground has yellow and blue clay down to around 50 feet below. The houses have structural problems like foundation issues, cracked walls, cracked concrete, etc. A couple of years ago, a developer built lots right next to my house, sold the lots, and builders built houses according to “market prices” or “affordable” as you say. A year later, they all have problems with broken windows, cracked sheetrock, foundation issues, etc. Lawsuits all over the place and no one is held accountable. Do the owners not have a right to “bitch” about being screwed over for buying what they thought they could afford according to the “market”?

Nottasheep

The construction issue you cite has zero to do with the issue I addressed. Your issue is the same kind of issue that the ultra-luxury Millennium Tower (high-end condos) in San Francisco faces. It’s leaning, stuff is cracking and leaking, elevators failed because of the angle of the building, lawsuits all over the place, very expensive efforts to try to mitigate the issue, etc. etc.. these are issues that are unrelated to what I said and what I replied to. You just changed the topic.

People will see 1 TikTok of shoddy workmanship in some house somewhere and decide all new homes are “junk”. Social media and internet comments sections just deep fry people’s brains.

It’s a blessing that builders are increasing active inventory and, effectively, capping price increases. The civil courts are there to sort out the rest.

Wolf,

It is like anything else, it is a matter of degree.

A builder can,

1) Build a more affordable house by,

a) selecting less expensive lots

b) reducing square footage

c) simplifying rooflines

d) using more basic finishes

e) not expecting/demanding ZIRP Zuper Margins

But all those fixes can be taken to an absurd level of parody (really in the name of preserving the Super Margins).

As early as 2005, LV was building literal crap-shacks (a one car garage on first floor, with equal width (although front-back overhangs) living space on second floor. That was it – looked like *zero* homes from *ever* – at best maybe like a severed, standalone townhome (no wider than 1 car garage) with a sloping brow.

They were of course cheaper to build (tiny, tiny frontage) but they sold for “only” 2x 2002 prices instead of the median 3x in 2005.

Even the “fixes” in an insane era, take on the quality of insanity.

Other than ZIRP, absolutely nothing justified doubling/trebling home prices in Housing Insanity 1.0 – but lopping the arms off a monster still leaves a monster.

What’s your problem??? If these houses are so bad, no one buys them, and then their price collapses and they’re really cheap. But if people keep buying them, then their prices are high. Basic economics. Quit buying houses, and prices will come down. That’s how that works.

Houses from the 40’s and 50’s had no insulation, oil or coal fired furnaces, plaster walls, unsafe wiring, no circuit breakers (fuses), and terrible windows. I rented one when I was in college in the late 1960’s and heated my soup cans on steam radiators. No one in their right mind would want one of these unless you tore it down and built over again.

With respect to new, inexpensive builds, what would you build for the common man and his family these days…..$750,000 custom homes? These smaller, tact homes are suited for young family’s getting started, seniors retiring and anyone else priced out of the “better” home market.

The best houses are from the 1890’s. The house I lived in during college had (I kid you not) asbestos siding. It was great when the neighbor’s (barely 3 feet away speaking of lot sizes in the good old days) caught on fire. Absolutely no damage to my place.

Pros and cons to everything. The older houses might have as asbestos, electrical wiring that needs updating, be really energy inefficient and result in higher energy bills, lead pipes, older roofs and furnaces if they haven’t been replaced in recent years by previous owners. One probably isn’t better than the other – they’re just different.

Don’t know where you’re located, but I can testify that in FL and CA you really DON’T want to buy anything built before the more modern codes were initiated.

Hurricane Andrew in 1992 opened a LOT of eyes, and the insurance industry audited every municipality and county building department in FL, and then paid the politicians in Tally to upgrade ALL the codes including the codes/laws regarding building departments and individuals within them.

Similar in CA after the San Fernando and Loma Prieta EQs.

I helped, pro bono, many homeowners get their houses back onto their foundations after the LP one, and it was a huge mess…

Similarly knowing friends who did the same after Andrew when I was involved in the industry in FL.

The Sun Belt homes are the drivers of the U.S. construction economy. As Wolf points out, Florida and Texas are the gigantic engines of the national economy. The balmy weather of those two states, and the strong business climate, are drawing in thousands of new residents at a time when the Northeast is struggling to hold onto its population…

Florida is not balmy but it is way too hot, all the time. All people do there is stay inside unless they live on the coast where it’s windy and cooler. But, few can afford that more expensive spot. That’s what my Uncle Ralph told me after he lived his dream by moving to Florida. Fun to visit and be warm for a week but not every day and night, he said.

Took me a 1 year lease to figure out that I’d never want to live there long term. It’s nice 4 months out of the year and you pay for it by opening your door to a furnace the other 8.

Anecdotal far shore: Two new houses right behind us, (NOT in flood zone!) both about 3K SF, one ”under contract” before construction begins at $1.3MM, the other unsold at $1.6MM to be completed in August.

Right Price = sold, eh

Delusional sellers (existing) vs Pragmatic sellers (homebuilders), battle of the century. Have my popcorn ready and looking forward to existing sellers getting some much needed does of reality smack into them….maybe some of them have forgotten what chasing the markets down looks like and don’t think it will ever happen again..

For markets with way more limited new builds, consider yourself lucky for now and maybe your stubborness will ride out the price correction…time will tell

I hope you got the extra large popcorn bucket with free refills. Gonna be a long movie…

Non stop building in Northern California, both in the downtown with taking down failed retail that are torn down to major new areas that will have thousands of units of various types, new schools and more(Innovation Park, former stadium area for Sacramento Kings). Can’t drive up highway 80 anymore without seeing new developments as far as the eye can see. This project obviously has had years of planning but clearly they expect to unload them all 10% will be affordable housing along with combo of residential houses, apartments and condos. I haven’t heard of a lot more jobs coming to the area but a huge part of this area is government.

“I personally will not purchase a home produced from 2020 to current time, Absolute thrown together junk, I dont care what kind of con job “incentives” they threw at Me..”

These monster homes in my area are mostly thrown together junk. After they are built you see repair trucks lined up in front of the homes for 6 months or more fixing all the defects. The windows alone cost $20K right out of the gate to replace as they are not energy efficient.

Funny homes built in the 20s to today all can have cheaper windows cheaper everything as Wolf says read the article where the subject is not quality but quantity and margin . Homebuilders have to build homes people want and they are building them and selling them with lower margins and higher costs. More inventory is driving prices higher and the incentives builders offering helps the buyers. I can think of lots of reasons to buy these more inexpensive homes myself.

1. Less expensive

2. New neighborhoods new neighbors maybe friends for kids and newer schools

3. Usually nicer age demographics where neighbors are similar age and income with similarities

4. Lower costs no expenses for a decade or more

5. Smaller or no yard lower cost of ownership

6. New styles and amenities

7. At least that’s what I thought of

8. Great job by the home builders building things people want and helping keep economy pumping

9. Hope the trend continues with sales and supply similar

10. Custom homes are very expensive very nice generally but expensive

Looks like supply is slowly increasing but maybe the supply is even cheaper homes with minimal energy requirements . Maybe the latest federal administration relaxed the requirements and regulations for home builders that can install lower cost items in a home if that is what a customer wants ! I do think the regulation for NG stoves and hot water heaters was removed by Fed Government but that was not set to kick in for a few years anyway

So new homes make up a larger portion of sales than they have been historically and are being booked at fake prices ~12% above the actual realized price after incentives (and the discount required to sell is increasing). The question is, when will enough “used” home sellers be forced to sell at a lower price point that everyday people realize prices are falling and sales activity dries up even further

A tale of two markets.

For homebuilders who have to sell or they might go under, or at least slow down production, they’re making the math work for the market.

For owners on the resale market, they’re “holdin’ and hopin'” that Daddy Powell will fix their affordability issues and ROI dreams.

But time has value as well. Having to sit on property creates costs. Having to sit on financed property costs more, as do lost opportunity costs or eating commutes. Pick your poison.

Don’t hold your breath! Many people with more than one home have little need or interest in selling. Nor do they sit there and glot over their homes value.

Not a week goes by that someone does not offer to buy land next to my home. If I needed the money I would sell, but I like the natural woods and wildlife.

If you are waiting for prices to fall, you may be in for a long wait if you factor inflation.

At least half the homes on this lake are vacant or just for weekends. Few sellers and lots and lots of lookers.

If you believed most of these posts, you would think everyone is worried about every dime and it just ain’t so.

Agree.

Also, many long time homeowners, myself included, welcome a decrease in assessed home value because it lowers our property taxes and puts home prices in a range for our children to buy. My home in Denver has tripled in value and all that does for me is increase taxes and homeowners insurance. I would welcome a 50% decline in assessed value, as I am not planning on moving to another part of the country.

Only 2 prices matter, what you buy at and what you sell at. In between, it’s just taxes and insurance.

Builders really screwed up here. Too many homes were built in pandemic locations since people thought work from home is permanent. Too few homes were built around large metro areas were the jobs are. This will be interesting … perhaps a housing crash in pandemic locations is in the cards while large metro areas hold up.

Home inventory in Chicago, IL is still extremely low.