Who’s on the hook this time? Mostly not the banks, but taxpayers, except for HELOCs.

By Wolf Richter for WOLF STREET.

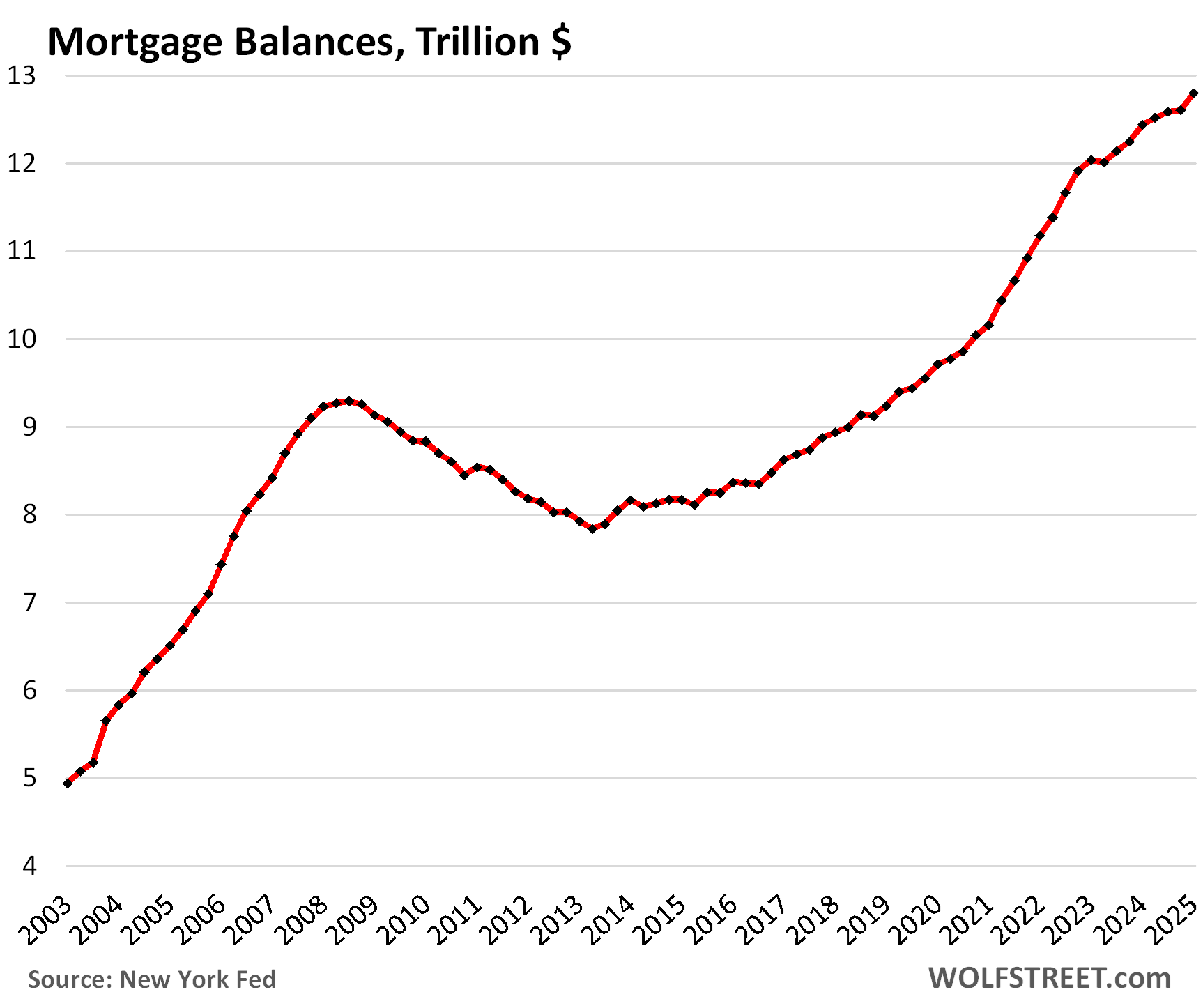

Mortgage balances rose by $195 billion (+1.5%) in Q1 from Q4, and by $358 billion (+2.9%) year-over-year, to $12.8 trillion, according to the Household Debt and Credit Report from the New York Fed, based on Equifax credit report data.

The year-over-year increases in Q1 and Q4, both at 2.9%, were small compared to year-over-year increases in the 8-10% range in 2021 and 2022. Since then demand for existing homes has plunged, while demand for new houses has been decent, and mortgages got a little bigger with home prices.

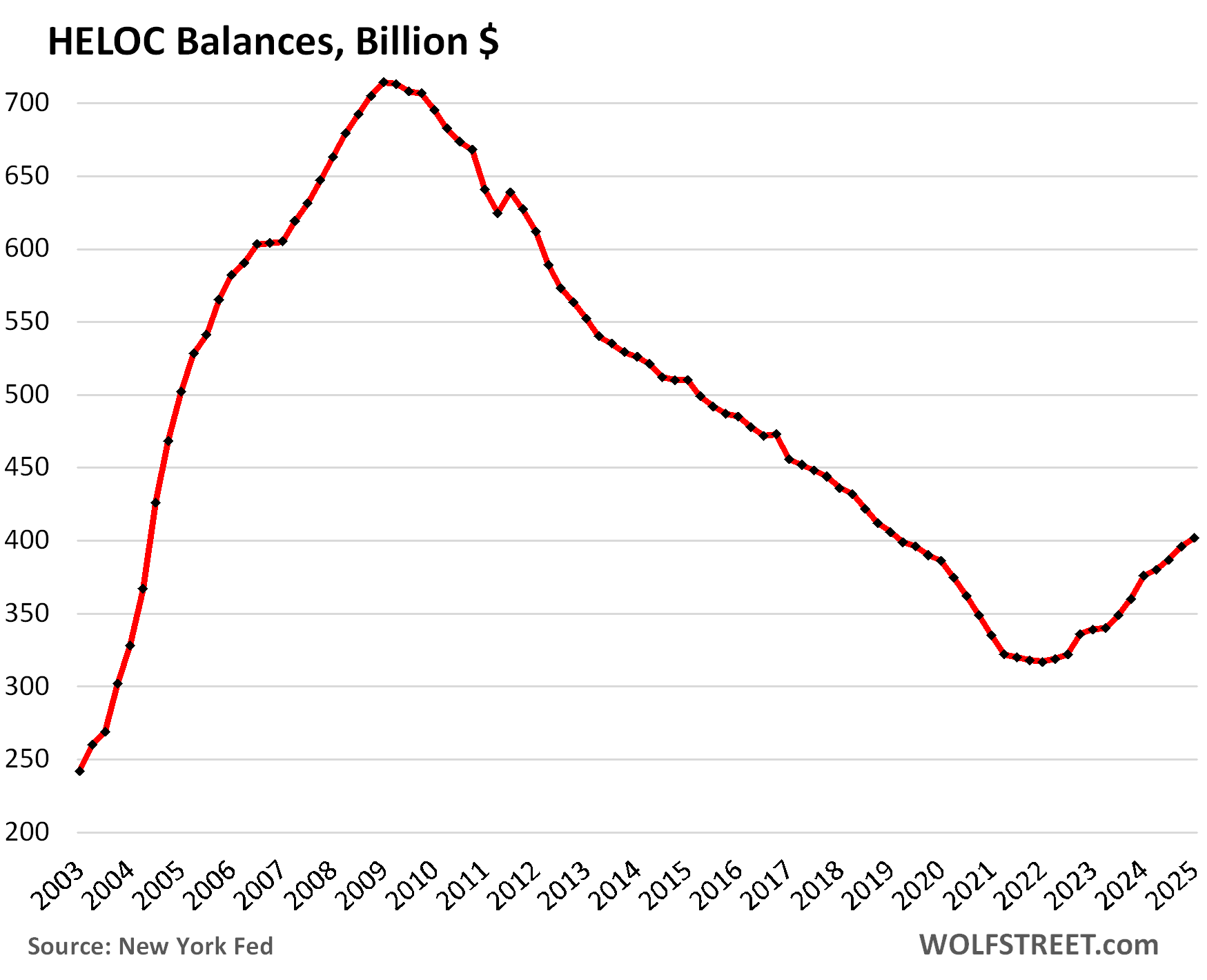

Here come the HELOCs: +27% in three years.

Balances of Home Equity Lines of Credit rose by 1.6% quarter-to-quarter in Q1, and by 6.9% year-over-year, to $402 billion. Over the past three years, HELOC balances have shot up by 27%.

Even after the 27% surge, HELOC balances remain relatively low after 13 years of lessons-learned declines coming out of the Housing Bust during which HELOCs did a lot of additional damage. These are the actual balances drawn on HELOCs:

People who want some cash for home improvement projects or other purposes, or at least have the ability to draw on this cash when needed, are doing the math: It can be less costly for homeowners with a 3% mortgage to take out a HELOC at the higher rates that HELOCs come with, and not cash-out-refinance the entire existing 3% mortgage at 7%. In addition, HELOCs are lines of credit that can be kept on standby, for just in case, with no interest being due until actually drawn on.

About three-quarters of recently originated HELOCs had credit limits below $150,000, according to an earlier report from the New York Fed. At the top end, about a quarter had credit limits of $150,000 to $650,000, and only 1% had credit limits of over $650,000.

HELOCs come with a second lien on the home, and if homeowners default on the HELOC while keeping the first-lien mortgage current, they can still end up in foreclosure. In addition, after a foreclosure, when the first-lien lender takes the home, lenders of the HELOC can haunt homeowners with deficiency judgements for the unpaid HELOC balances even in the 12 “nonrecourse” states, including California, that don’t allow deficiency judgements on first-lien mortgages.

So HELOCs come with some extra risks for borrowers and lenders – which is also why lenders charge a higher rate for HELOCs than for first-lien mortgages.

The burden of housing debt: Housing-debt-to-Income Ratio.

A common way of looking at borrowers’ ability to manage the burden of debt is the debt-to-income ratio, or a debt-to-cash-flow ratio. With households, “disposable income” roughly represents cash flow after payroll taxes that is available to spend on housing, debt payments, food, fuel, and other expenses. The portion of disposable income that households don’t spend represents savings.

Disposable income is household income from all sources except capital gains, minus payroll taxes: So income from after-tax wages, plus income from interest, dividends, rentals, farm income, small business income, transfer payments from the government, etc.

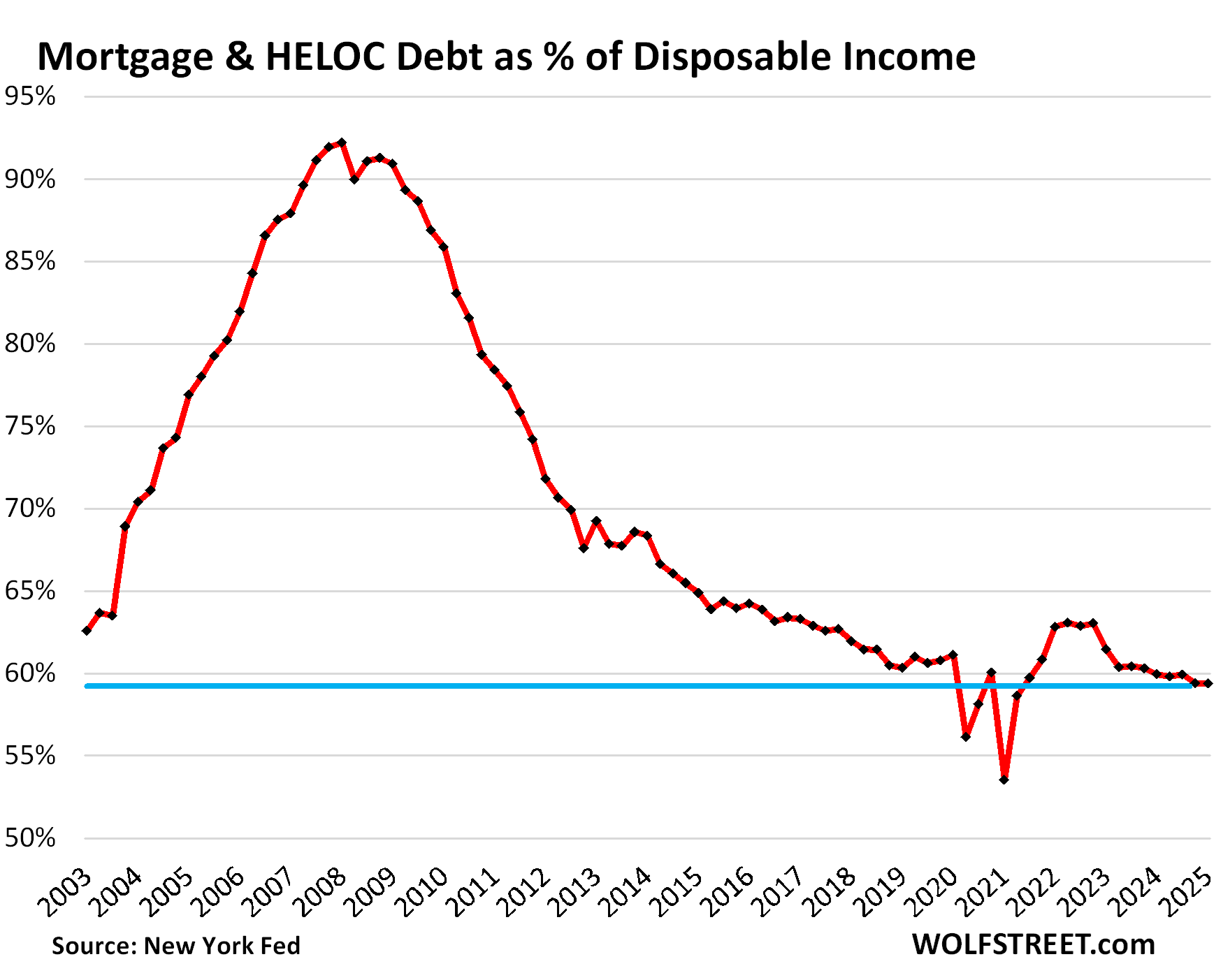

To view the burden of total housing debt on households, while accounting for more homes and higher incomes, we use the housing-debt-to-disposable-income ratio.

Disposable income rose faster year-over-year than total housing debt – mortgage debt plus HELOC debt – and kept up with housing debt growth quarter to quarter:

- QoQ: disposable income +1.6%, housing debts +1.5%.

- YoY: disposable income +4.0%, housing debts +3.0%.

With disposable income keeping up with the growth of housing debt on a quarter-to-quarter basis, the housing-debt-to-income ratio remained at 59.4% in Q1, same as in Q4, and both were the lowest in the data, except for the brief period when free-money from the government wildly distorted disposable income.

It’s obvious where the problem was in the run-up to the mortgage crisis that nearly blew up the financial system in 2008.

Housing debt is bigger now than it was in 2008 (+33%), but there are a lot more households, and they earn a lot more money, which translates into far higher disposable income (+107%), which is why the burden has plunged, even as the absolute debt has risen:

Who is on the hook this time?

Banks are mostly off the hook, except for HELOCs. Of the $12.8 trillion in mortgages outstanding (first chart above), commercial banks only held $2.37 trillion, or 18.6%, according to Federal Reserve bank balance sheet data.

Banks are more exposed to HELOCs, but the numbers are smaller. Of the $402 billion in HELOC balances outstanding, commercial banks have $267 billion, or 66.4%, on their books. But $267 billion amounts to only 1% of the $24 trillion in total assets in the vast US banking system.

Mostly the taxpayer. The government through a slew of entities – Fannie Mae, Freddie Mac, Ginnie Mae, VA, FHA, USDA, etc. – guarantees the majority of residential mortgages. Those mortgages were packaged into MBS and sold to investors. If borrowers default, the taxpayer has to eat the loss.

And some institutional investors. Mortgages that banks didn’t keep on their books and that the government didn’t guarantee, such as jumbo mortgages, have been packaged into “private label” MBS and sold to institutional investors around the globe, such as pension funds and bond funds, and it’s these investors that carry the credit risk for those mortgages.

That shift from banks to the government is one of the huge changes coming out of the Financial Crisis: It’s no longer the banks and investors that are primarily at risk from bad mortgages, but US taxpayers.

So far, so good.

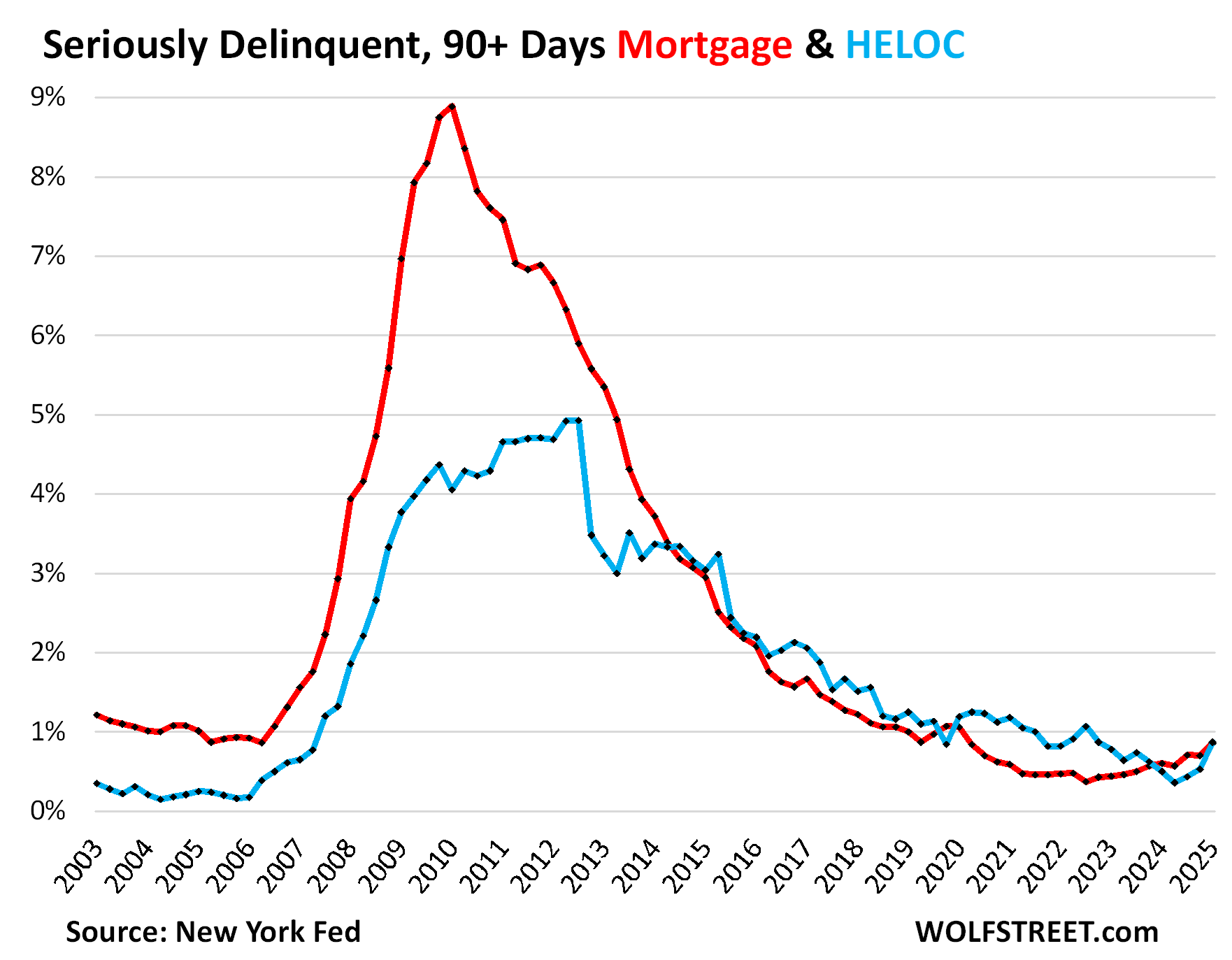

Serious delinquencies have come up, but remain low. Mortgage balances that were 90 days or more delinquent have risen from the free-money lows during the pandemic to 0.86% in Q1, which is still below the prepandemic low in Q2 2019 and substantially below the range of 1.0% and 1.7% of the rest of the quarters in 2017-2019 (red in the chart).

HELOC balances that were 90 days or more delinquent jumped to 0.87% in Q1, from 0.53% in Q4, still below the prepandemic range, but that was quite a jump, albeit from very low levels (blue).

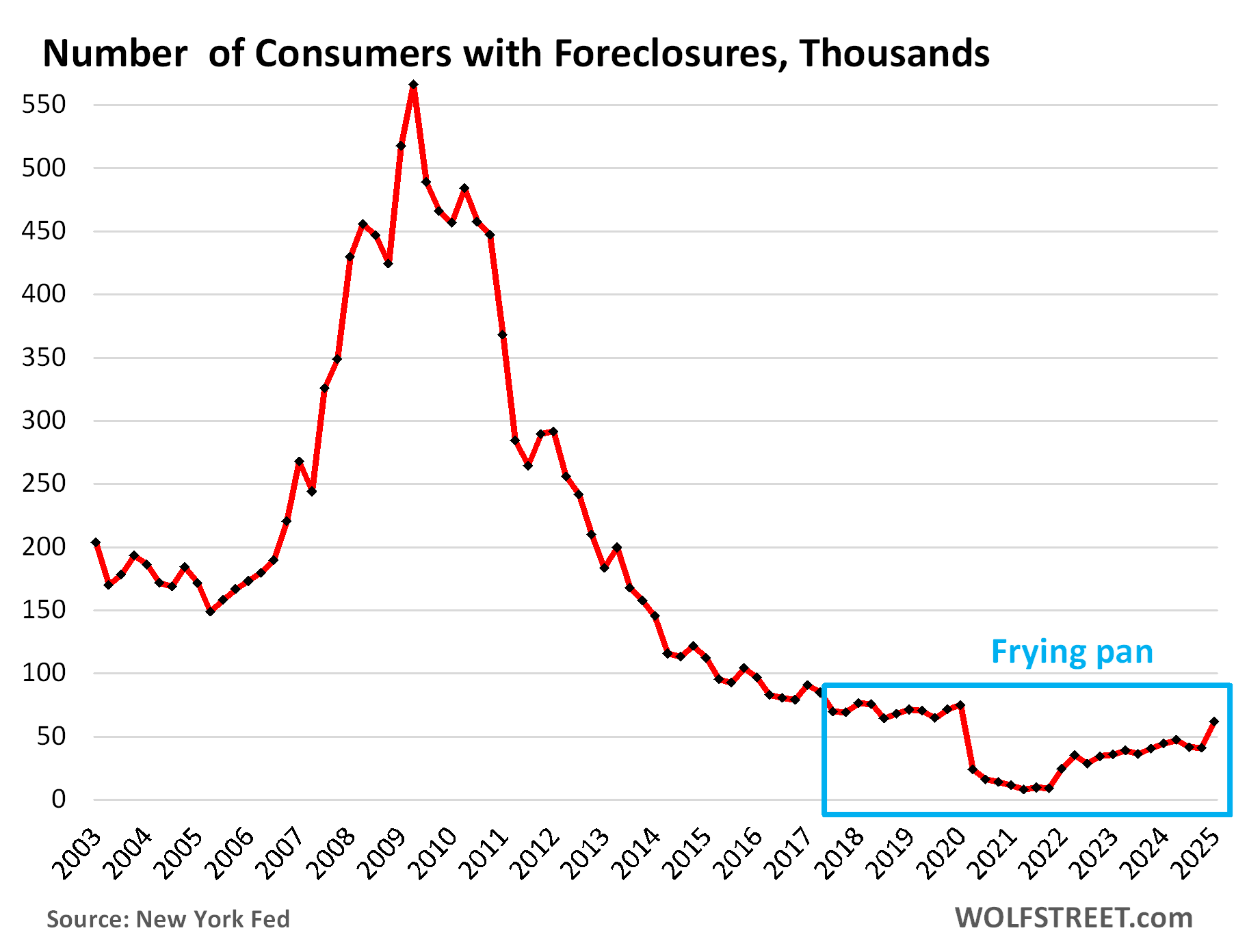

Foreclosures are low: the “frying-pan pattern.” The number of consumers with foreclosures in Q1 rose to 61,660. Though that was quite an increase, the number is still below the range of the Good Times in 2018-2019 between 65,000 and 90,000.

The mortgage forbearance programs and foreclosure bans during the pandemic, and other government programs for government mortgages, essentially made foreclosures impossible, and the number of foreclosures fell to near zero.

Most of these programs have ended, and some are now being ended, and foreclosures have risen from the free-money lows and are on their way to normal-ish levels, forming a “frying pan pattern” that has been cropping up in other credit metrics of the pandemic and its aftermath.

What is keeping foreclosures still low currently is that home prices exploded during the free-money era – see our Most Splendid Housing Bubbles in America – so most homeowners that cannot make the payments can sell their home for more than they owe on it, pay off the mortgage, and walk away with some cash. At this point, only a relatively small number of defaulting homeowners are enough underwater to not be able to pay off the mortgage with the proceeds from a sale. And those are primary candidates for foreclosure.

And in case you missed it on Wednesday: Household Debts, Debt-to-Income Ratio, Serious Delinquencies, Collections, Foreclosures, Bankruptcies: Our Drunken Sailors’ Debts in Q1 2025

Enjoy reading WOLF STREET and want to support it? You can donate. I appreciate it immensely. Click on the mug to find out how:

![]()

Great article. I just don’t see much basis for the doom and gloom except for going through a terrible inflationary period and people still reacting to that.

Thanks wolf

I’m interested to see how much impact student loan repayment has on this one.

Anyone foolish to take a Heloc out will feel it whether they keep their house or not.

Plenty of Doom of Gloom in PE backed businesses, debt covenants blown, plenty of business can’t pay Mezzanine debt, banks are refusing to call in the loans. Private credit originators are freaking out too, Credit bubbles don’t deflate without pain they usually pop. Symptoms of mis allocation of capital are everywhere today. Japan refused to write off bad debt after their credit bubble popped in 90, zombie companies lasted for decades. China is dealing with the same thing now. What’s coming up next, D-risking D~leveraging D~faults and D~listings. It’s just matter of time. All I see is the biggest credit bubble of all time, if you do the crime you have to do the time eventually. We have 27 trillion dollars of foreign capital invested here, it’s free to leave! Our Trade deficit made us the world piggy bank that reinvestment of capital is going away. Risk on trade running out of steam. Stocks rallied 10 trillion in 5 weeks, 15 trillion down on deck. Batter up!

China was dealing with this for more than 20 years now. What has happened in the last 2 years is a cascade effect of bad policy time and time again. Who buys a house in America, pays mortgage for 2 years, and does not live in their home? Says no American.

Banks don’t call loans when their cash on hand is 4% and the FED is in bed with them. The discount window shows no sign of that whatsoever.

Credit is endless and it will bite the consumer in the rear soon. Buy now pay later for groceries should not be a thing.

Finally, if the treasury secretary didn’t attempt to bash the 10 year down, then this economy would be far worse off. Only reason why countries like Japan have not resorted to treasury sell offs of which they were getting really squeamish a couple months back.

The trade deficit also is the creation of over consumption and dollar globalism. When those tariffs fail the next step is Nationalization and getting rid of useless corps like Whirlpool. Substandard product, dirty factory. It wouldn’t take much to improve it. China is already slowly moving away from American multinational companies. My guess by 2050, it will be 100% pan China, sending manufacturing products to the world. While the fatties in the US wait for that next consumption fix…….which by then will be fleeting.

re: “… useless corps like Whirlpool. Substandard product, dirty factory”

Source? When we did a remodel of our house both our (trusted) contractor and the kitchen designer at Lowes said they saw the least issues with their appliances (even considering the fancy German brand). We’re going on 5 years now with no problems (though their timing beepers are wimpy).

CalBob-…one should always factor in a firm’s constant and continuing dedication to the quality of its products versus the willingness/QA awareness of its strategic/financial management and shareholders to cut beans from same (…apocryphally, what happened to Nissan some years ago when management determined their product was *built TOO well* compared to the competition, implying longer repeat customer turnover time was the reason market share wasn’t increasing. Answer: essentially a return to planned obsolescence to fix the issue. Further deponent sayeth not…). A lot can change overnight, let alone in five years-yet we still seem to long for stability, be it in prices or society…

may we all find a better day.

Wolf,

I agree – strong/useful/clear article.

“Of the $12.8 trillion in mortgages outstanding (first chart above), commercial banks only held $2.37 trillion, or 18.6%, according to Federal Reserve bank balance sheet data.”

Wolf,

So Who owns the other 80%+?

And are they shielded by government guarantees (putting US citizens at risk again and again).

So, is the other 80%+ of mortgage debt mostly in mortgage-backed-securities (with G guarantees)?

Are there specific numbers for that?

Other than the bank retained 19% of mortgages (presumably the best loans get retained and the sh*t sold off into public markets), do *any* private sector investors buy US mortgage debt *without* 100% US Gvt backing?

If not, that tells you what those investors really think of US mortgage debt…

It is like the whole US housing/mortgage finance market has rapidly evolved (essentially post 1990) into a system where periodic collapse is built into the system – stupid overvaluation booms inevitably followed by wholly predictable catastrophic collapses, all empowered by an already debt-crippled DC government.

“So Who owns the other 80%+?”

LOL, read the next four paragraphs.

Wolf,

If these entities are holding the rest (majority) of the debt, so if case of the bust, what will happen? is government intervention largely possible with printing money and paying off the mortgage, at least partially?

See ‘Walmart Earnings Call’…

We’re cooked.

Who dis? New Tax who?

More clickbait BS and manipulative propaganda.

The Truth hurts, I know.

We all have to pay more to make CEOs happy.

😃

A nugget

from article:

““If Walmart’s coming out — with its scale and its buying power and its focus — and saying prices are going to rise, everyone else is going to have to follow suit,” Neil Saunders, managing director at retail consultancy GlobalData, shared with NBC. “Walmart is firing the starting gun on a period of price increases.”

sufferinsucatash

You don’t understand what YOU are doing: YOU are spreading Walmart’s propaganda that tries to manipulate people into paying higher prices rather than walking away when they see the higher prices, which is what people are doing right now, they’re not buying products with price increases, which is why goods inflation has turned negative (deflation) since 2023. But YOU are helping Walmart in trying to get people back to paying whatever.

The only thing that keeps inflation at bay is people refusing to pay whatever. People paid whatever in 2021 and 2022 because they didn’t care, and because companies (incl Walmart) took advantage of the pay-whatever syndrome at the time, and they fattened up their profit margins that way.

A lot of this done publicly in 2021 and 2022, exactly like Walmart now, with manipulative statements that became clickbait in the media, about price hikes that encourage other companies to also hike prices (collusion!) and made people feel like they didn’t have a choice.

Then in 2023, people came to their senses and stopped paying whatever, and when a company hiked prices, sales of those items collapsed because people refused to buy it, and that ended the price hikes on many goods, and prices of many goods have dropped since then because companies didn’t want to see their sales collapse. Walmart was one of the companies that cut prices on thousands of items (“price roll-backs” it called them when it talked to investors about it) because it saw that sales dropped on items where it had hiked prices.

What YOU are doing is helping Walmart manipulate people into paying whatever again, like they did in 2021 and 2022. You’re abusing my site to spread this stupid corporate manipulative clickbait here.

my father is a farmer. he usually get 2/3 of the final product price in the supermarket.

now he gets roughly 1/2. he gets less. more due to inflation but less in the end of year.

Consumers are the only ones with power enough to make a change and they will do if they take a look. just a look.

Competence is the best thing for both consumers and producers.

we still have some of that and we should always take a look and speak the truth.

it is like the child who never start a fight but always kick the bullied in the ground. they did not start inflation but they get a very big piece of the cake.

Eliminate the Biden mortgage relief program ASAP.

One of my employees just did a home refinance today on a home he bought a few years ago so he can dump his 7-year old dying p.o.s. Kia and get something that runs. Feel bad for him that he had to do it. Not sure if that speaks more to the car or what our state agency pays but regardless, not everyone doing it does it for the kitchen remodel or student loans. But I get your point.

That was a cash-out refi; that wasn’t even a HELOC. And sure, people do refis for all kinds of reasons, same as HELOCs, and it doesn’t matter why they’re doing them, but that they’re doing them. But a HELOC is different from a cash-out refi — credit line, and 2nd lien.

Howdy Lone Wolf. I said it before and will say it again. Prisoners, you can free yourself with a HELOC and build wealth. Just need to know how to add and subtract and balance budgets. Make a widget that people want and prosper.

wait, so he refinanced from a 3% mortgage to a 7% mortgage to get money for a car? am i understanding that right?

yeah, this would be an insane thing to do.

My sister has a Kia. The engine seized at 125,000 miles. Known problem and Kia replaced the engine for free, with a used one. The new engine has about 30,000 miles on it and is making the same noises the first one did before it seized. The Kia dealer told her no more fixes and they won’t take it on a trade in. She’s a paycheck to paycheck gal, and coming up with $20k for a new used car isn’t in the cards. But its Florida. You have to have a car, so you do what you have to do.

Toyota. buy once, cry once

Gotta say, getting to 155k miles on a Kia without having to pay for a major repair isn’t bad at all.

That is like 12 years (!) of typical annual mileage – plenty of time to have saved *some* money for a replacement.

And there *are* used cars going for significantly less than $20k.

Kia, a military term for “killed in action”. Seems to be an appropriate name for that car company.

Don’t buy crappy Korean stuff.

Why people buy Hyundais and Kias is beyond me.

People are cheap.

Just kit 200k on my 01 5 series. BMW inline 6’s are some of the best engines ever made! Cheap to maintain if you know what you are doing.

It does seem scary/weird to refi your house to buy a car.

I just checked and the average used car loan rate is 11.5% and a new car loan is at 7.2%. Maybe the house refi at 7% for 30 years is more affordable? The payments are certainly lower but I wouldn’t want to be still paying for a car that has been dead for 20 years. Maybe if I was 85 when I took out a 30 year refi. I may be dead before the car.

I seriously wonder what people are doing with the cash they receive for cash-out refis or HELOCs? Enhancing their house? Paying off 30% credit cards? Living the Dream?

My dream would be to live in a house in coastal CA that I purchased 40 years ago for 200K and is now worth 3M at the peak of this bubble. I’d take a 30 year refi for 2.4M and live the dream. Darn, I have heirs that might be upset with that.

If he bought the home 3 years ago, he had a 6% mortgage.

Geez, why not just do a car loan thru a credit union?

Then their house is not at risk. Only the car and their credit.

These online credit products are out of control, Rocket Refi or whatever.

Debt financing is almost always a mistake, unless you’re a large corporation that can reasonably expect to earn back its investment in the marketplace. The people who turn to loans to buy something need to have a little “heart-to-heart” with themselves as to whether it’s really necessary.

Isn’t that the entire private equity model?

Few weeks ago guy I know asks if I know about reverse mortgages. I

I say I know what they are but not the details, not enough to offer advice.

Turns out he and wife want to buy new car for 63 K and are looking at using hse loan to finance same.

Since this leaves me aghast, they may be talking to wrong guy..but I suggest seeing what same model just off 3 yr lease costs.

This seems kinda familiar. Get a bunch of debt living a lifestyle you can’t afford or sap the equity from your home to buy nonsense you don’t need. Soon enough, you’re up a creek and there goes your paddle. Sounds pretty 2008 to me, maybe not the exact same adjustable loan issues (although some are out there), people just can’t help but to pretend to be more than they are.

Good comment

Its not 2008 in terms of big banks. This is more widespread and much more in flyover country.

I’m planning to apply for a HELOC SO I CAN PAY OFF MY MORTGAGE FASTER. PLEASE KINDLY ADVISE ME ?

Sounds like someone is doing some good ole American recession planning!

A dear friend took out a reverse mortgage and went on the most baffling spending spree I’ve ever seen. She was clearly not of sound mind, but the bank didn’t care. They did the deal anyway.

She wound up losing the house.

Great article Wolf and maybe ties into the theme of the Drunken Sailor article that shows spending continues. Employment strong discretionary wages growth exceeds debt obligations . Vehicles vacations food consumption services spending all happening.

I need a new roof current 20 year shingles don’t have any life left . Maybe HELOC is an option . I am retired and roof quotes are about 40k . This expense is much like a vehicle expense. I should have had a roof replacement fund . I had a car replacement fund . Suggestions are welcomed ! Just an FYI apples to apples comparison for roof replacement have ranged from 35k-48k I was surprised at the range. East Texas pricing .

The big roof replacement shock is coming due. Don’t now about your roof, but zillions of McMansions have the most difficult (and expensive) roofs to cover. Steep pitches, lots of valleys, dormers, hips, etc. Most never thought about what it would involve to reshingle. Then of course our recent inflationary impulse has added another 20-30%. I had our 2000 sq ft roof replaced in 2018 for $12K and with architectural shingls and full ice and water underneath. Simple hip roof. Sorry for your plight.

Calculate the square footage of shingles you’ll need. You can hire a company called HOVR to do it for you with a drone. Now go to a lumber yard that sells shingles. Cheapest one around here is Beacon Building Products. Ask your salesperson what materials you’ll need to do your roof. Show them the HOVR report. Then ask your salesperson if they could get you in touch with a subcontractor. Call a few subs and ask for quotes. The subs do all the work anyway. GCs just mark it up and get paid to push paper. You could probably save 50% compared to the retail price. Maybe more if you’re patient.

Good Advice. Same approach can be applied to lots of other needed goods and services. Do the ground work, go direct and eliminate the distributor and middlemen. 👍💰👍💰

WOLF

Other than being a line of credit vs a lump sum, what is the differences if any between a HELOC and a second trust?

Howdy Swamp. I am not the Lone Wolf, and HELOCs in the olden days, would lend over the appraised value of the home. 20 % over the appraised value was common for me.

You mean a “second-lien” mortgage? You got it.

Second mortgages can be fixed rate loans as well as adjustable. Aren’t HELOCs generally only adjustable rate? Like, Prime rate or LIBOR or whatever, plus a spread?

Howdy Folks. “Who’s on the hook this time? Mostly not the banks, but taxpayers, except for HELOCs. ”

Taxpayers are on the hook always. Almost 37 Trillion we don t have too.

I can’t speak for all banks in all 50 states but most HELOCs I am aware of from Banks and Credit Unions in CA over the years were very conservative (like $100K on a $1.5mm home with a ~$700K 1st TD balance). It was the 2nd TD people, especially the “hard money” aka “loan to own” guys that got real aggressive loaning money to people who would have a hard time paying (so they could foreclose and get the property). I had a $500K HELOC from Wells Fargo on my home (that I own free and clear) for years that I used a couple times in the past decade when I needed a couple hundred grand fast (it was set up so I could instantly put the money into one of my checking accounts using the Wells Fargo app on my phone) but it is gone now since Wells Fargo stopped doing ALL new HELOCs or extending old ones this year.

Howdy Apartment I. Morgan Stanley Dean Witter , years ago, offered a 125% equity HELOC, no closing costs, with a 10000 immediately draw. Receive a 200 bonus check. Pay the months interest on the 10000 grand and still make money just to open a HELOC.

Then the psychopaths decided to do the same thing with buying a house. Pay you for just signing your name…..

Is there any plan to get the taxpayer off the hook for mortgage debt?

Maybe not put it back on the banks, but surely it can be pushed into the “private label” MBS again? Could the end of conservatorship for Freddie and Fanny do that?

I’d guess mortgage interest rates would have to go higher to generate the yields to offset the expected defaults, but I don’t really see that as a problem. The higher the mortgage rates go, the lower the prices have to go to get a sale to transact; that’s pretty simple math.

They’re discussing making universities pay for student loan defaults.

Do the same for the lenders that originated mortgages.

And credit card companies that gave people cards they don’t pay off.

And let’s get rid of LLCs so their owners have to use their personal assets to pay off their business debts. That would stop people from making stupid decisions with other people’s money.

How can we blame this on tariffs?

Where there’s a will, there’s a way?

Nice read. I think that we are likely to see an early 00’s spike in HELOCs over the next five years. Many Millenials made the mistake that Boomers and X made in the late 90’s and ran up staggering levels of consumer credit debt between 19′ and 23′. In this environment of more historically normal rates, a HELOC is one of the best tools to slash the servicing cost losses keeping people in long-term debt on consumer credit.

As Millennial all me and my wife did was to stay out of this car shortage mania, and pay off our first ever brand new Japanese and Korean econobox leased 2 cars with all cash to stay out of debt.

As Wolf may know, most of dealers are not there to sell you new/used cars, they are there to trick you to get as much unnecessary options on your new car and shove the payment into your loans. Lol, like a big mark-ups for a new design corolla!, OMG!

Now the house inventories are started to get bigger because the demand is not there, no one can stand the monthly payment, due to high price and secondly the mortgage rate. This is slow moving heavy train, but I just want to know how government want to intervene if this train is going to hit a big thing!

Wash, rinse, repeat. Or maybe, “the more things change the more things stay the same”. Same old story with the average American consumer. No financial discipline, knowledge, or even basic understanding of economic or financial concepts. Just keep spending with money made out of air (i.e., excessive value of homes inflated by the Fed) and don’t worry about tomorrow.

BTW, if WR’s prediction/position about residential home prices and how they most fall in order to re-balance supply and demand in the residential home market comes through, the entire structure and market of HELOCs, loan to value ratios, available home equity, etc. will eventually get reset. And so once again, the drunken consumer will end up enduring a painful hangover. Can anyone say “margin call”.

That was a pretty good movie…”Margin call”

Gotta go bury my dog.

That looks pretty good. People seem to generally be getting in a better position with respect to debt-to-income.

Dear Wolf, being a chart junkie, I couldn’t help but notice the slight valley created between 2003 and 2007 that was below 1% just like now-in the “seriously delinquent 90+day mortgage &HELOC chart. I may be of a simple mind, but we either need greater incomes to afford homes for the generation that are starting new families, or a price drop in a significant way (depending on what “significant” 20-25% or more???). Perhaps deflation? I really don’t see this happening, but I have been surprised many times before.

What would the landscape look like, if we had these rates go up to a range of 2 to 4% on that same chart?